Time to shine

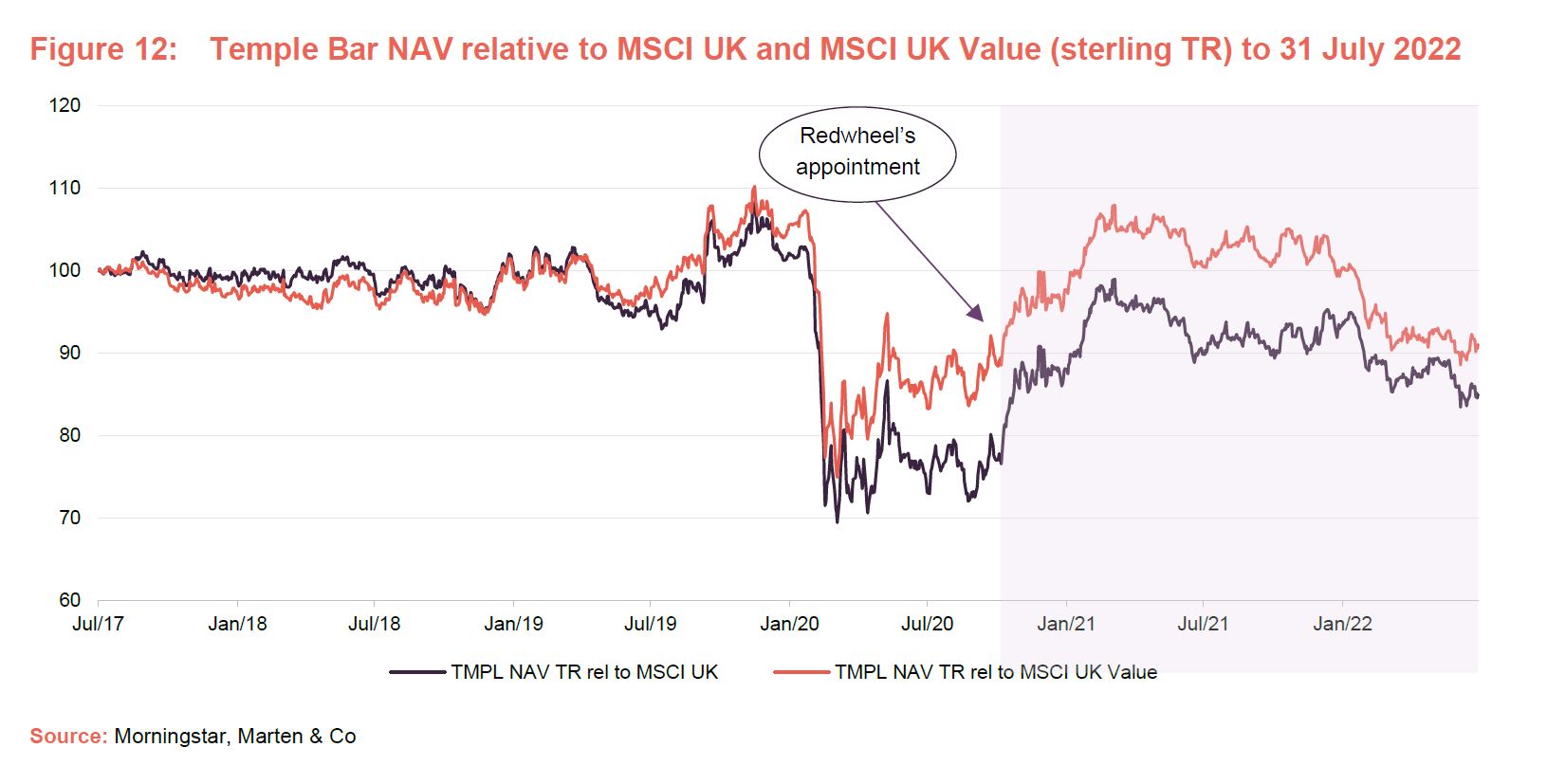

It is coming up to two years since Redwheel (formerly RWC Partners) took over management responsibility for Temple Bar (TMPL), and performance figures show that the change has proven to be a good decision for the trust. Of course, the change in investor appetite from growth to value-style investing has helped it along its way, but the willingness of the managers – Ian Lance and Nick Purves – to go against the trend (by buying cyclical businesses at the lows, for example) shows the importance of stock-picking too. The managers say that valuations are a measure of appetite for risk, and that on that score we are back down to the lowest levels we have seen for about the past 25 years. In times like this (as seen during the global financial crisis, for example), they say, it pays to take on more risk.

UK equity income and capital growth

TMPL aims to provide growth in income and capital to achieve a long-term total return greater than its benchmark (the FTSE All-Share Index), through investment primarily in UK securities. The company’s policy is to invest in a broad spread of securities, with the majority of the portfolio typically selected from the constituents of the FTSE 350 Index.

At a glance

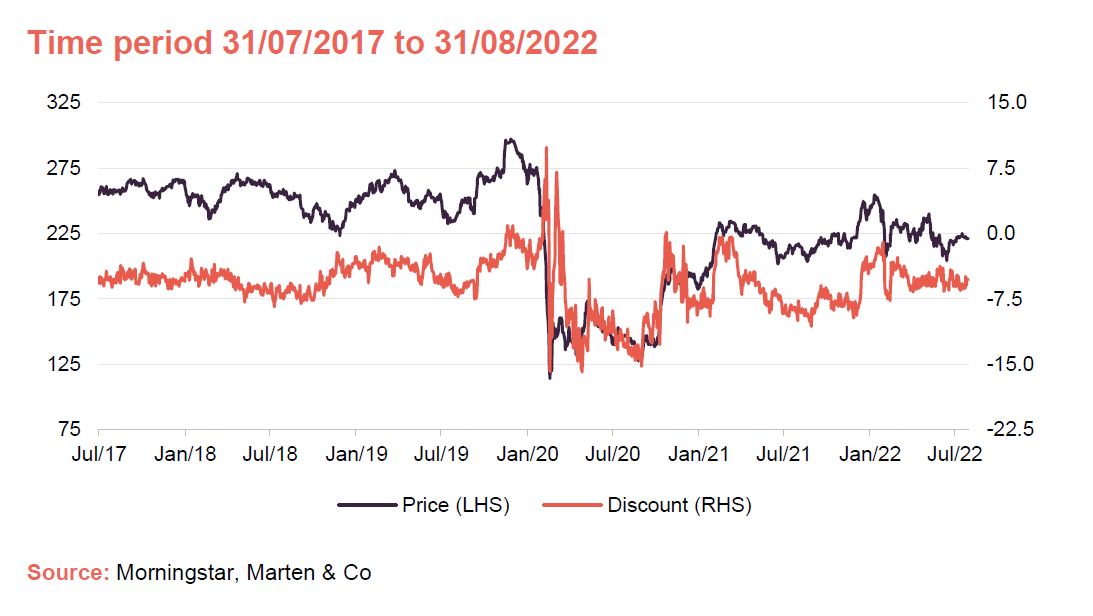

Share price and discount

TMPL’s discount was extremely volatile over the period of turmoil in markets triggered by the pandemic. The discount narrowed during November 2021’s vaccine rally and even briefly traded at a premium. During the first half of 2022, the discount narrowed from 7.8% to 3.8% as the board continued efforts to generate more buying interest in the company, and has been active in pursuing its buy back policy (purchasing nearly 2 million shares).

Performance over five years

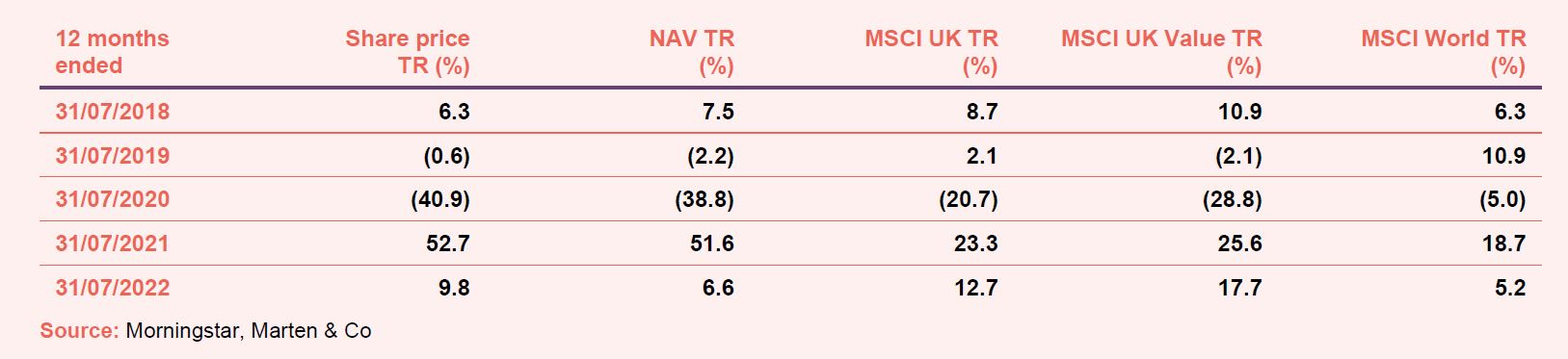

TMPL’s performance turned around significantly following Redwheel’s appointment as manager in 2020, though its relative performance got a significant boost shortly after as global market sentiment improved in response to positive COVID-19 vaccine news. This drove a sharp and significant rotation from growth sectors to value sectors, with mining, energy and banks doing particularly well.

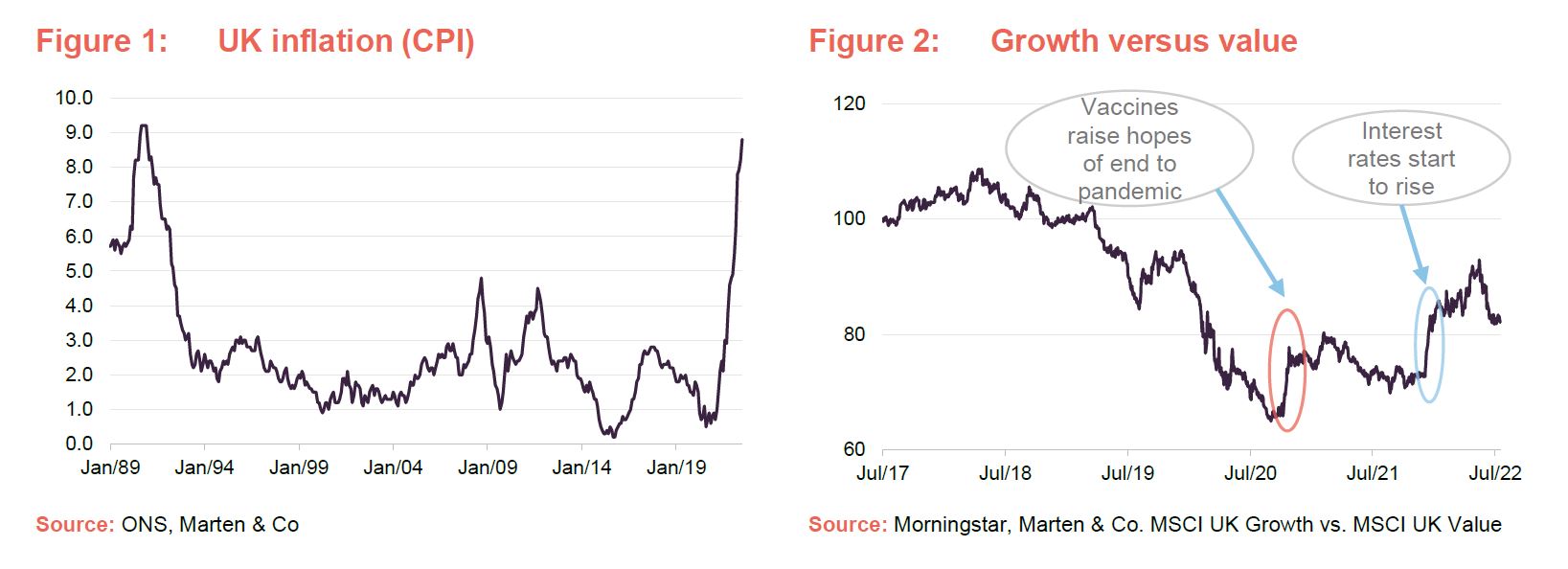

Rising rates and inflation

As we approached the end of 2021, investors grew increasingly concerned about inflation and began to anticipate interest rate rises. Following a significant increase in energy costs and household expenses more generally, the Bank of England’s Monetary Policy Committee (MPC) has now raised its key rate to 1.75% with 0.25% jumps in February, March, May and a 0.5% increase in early August; more is expected. This has triggered a sharp rotation from growth-style investing – the second-biggest – into value globally in 50 years – while pressures have increased on food, commodity and energy prices, with consumers facing the prospect of a significant increase in the cost of living.

Meanwhile, the Russian invasion of Ukraine, which started at the end of February this year, has made investors more risk-averse and exacerbated the inflation problem. While both countries’ economies are small in terms of their contribution to global gross domestic product (GDP), the ramifications of Russia’s shocking actions and the sanctions applied have already been felt in commodity markets and are weakening the outlook for the global economy and sentiment more generally. Energy prices, which were already high, have increased further, driven by rising natural gas prices. The Bank of England is now forecasting recession in the UK over the next five quarters.

Worst period for markets in over 50 years – but for the UK

Most global indices suffered over the first half of 2022, with the S&P 500 falling just over 20% – its worst half-year performance since 1970. The Dow Jones was down 15%, while the technology-heavy NASDAQ lost just over 30%, its biggest half-year loss ever. At the same time, yields on 10-year US Treasury bonds spiked, but for now at least appear to have peaked in mid-June, suggesting that investors believe that the aggressive rate hikes in the US are doing enough to bring inflation there back under control.

The UK equity market, however, has fared much better than most of its peers. From 1 January 2022 to 31 July 2022, the MSCI UK is up 1%, compared to negative returns from the MSCI USA (-4.2%), MSCI Europe ex UK (-11%), MSCI China

(-11%) and MSCI Emerging Markets (-9%).

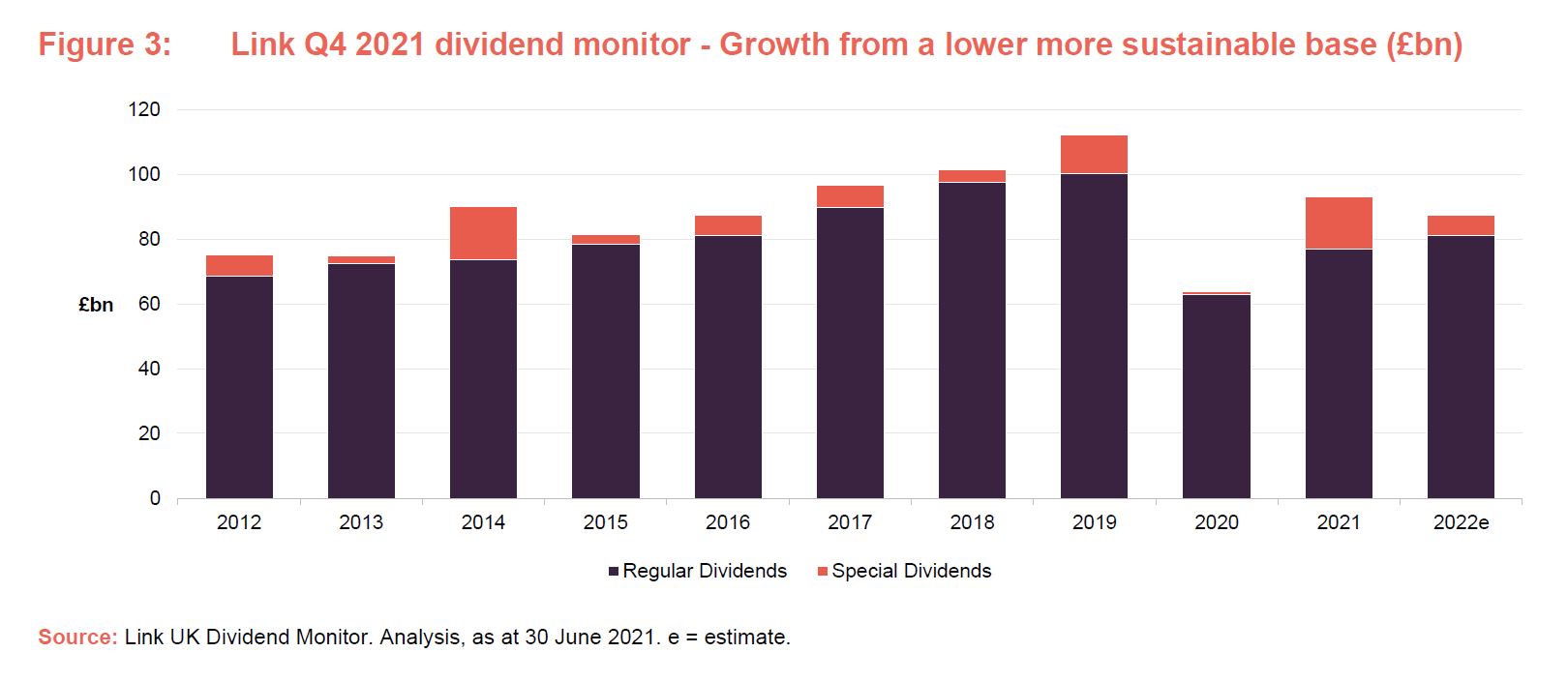

Furthermore, after the significant fall in UK company dividends in 2020 due to the pandemic, there has been a strong recovery in market income with previously suspended dividends in the banking sector returning and strong growth in dividends from the mining sector. According to the Link UK Dividend Monitor (see Figure 3), market dividends in aggregate in the UK rose by 21.9% last year on an underlying basis (excluding special dividends), recovering to 2015 levels. They remained, however, 23% below the levels of 2019, before the pandemic struck.

Manager’s view

The value-investing philosophy that underpins TMPL managers Ian Lance’s and Nick Purves’s approach to running the portfolio was set out in our December 2021 note. They reiterate that studies suggest that backing value, momentum and size (favouring small cap) all work over the long term, while growth and quality do not.

The managers attribute the growth- and quality-focused environment that we have experienced in recent years to ‘peculiar monetary conditions’, and a mindset amongst investors that it is rational to pay a premium for owning an above-average quality or growth stock.

The ongoing low-growth/low-interest rate environment saw valuations of growth stocks become very expensive. However, even ahead of this year’s market falls, the managers believe that the tide was already turning; smaller stocks in the NASDAQ were falling at the tail end of 2021.

The managers say that it is both common for investors to drive share prices of favoured stocks way above their intrinsic value and overreact to perceived bad news on the downside, commenting that, for example, cyclical businesses are often priced as if they will never recover. These can be fertile hunting grounds for value investors. Ian and Nick are willing to go against the trend and buy cyclical businesses at the lows.

Economic uncertainty has increased markedly, the war in Ukraine has compounded inflationary pressures, and the consensus is that we are going into a recession, not just in the UK but probably also in the US and large parts of Europe.

The managers say profit forecasts are not meaningfully different from where they were at the start of 2022 and so earnings forecasts have not yet reflected the new reality. In some of the more cyclical names, companies that have fared the worst during the last six months are those thought to be most vulnerable to a more difficult economic environment where demand is likely to be lower and costs are likely to increase. Reflecting a rapidly rising cost of living, consumer cyclicals have suffered, as have cyclical companies with relatively low margins.

Cracks under the surface

The managers say the past decade – and the last two years in particular – have been an “epic” bubble in growth stocks, particularly technology. In 2021, US equity funds overall saw the same volume of inflows as the previous 19 years combined. Unsurprisingly, it has been technology stocks that have attracted the strongest level of inflows. The managers refer to the dot-com bubble, when software stocks traded at over 10x sales and then saw a loss of more than 80% in just over a year and they believe that there are some similarities today, with the same sector peaking at 18x sales in 2021. They say that only small cracks are showing at this point, with 40% of the smaller end of the NASDAQ falling by half of their 12-month highs, but they highlight that in 2022 we have already seen big quality growth companies and world leaders such as Facebook and Netflix fall by as much as 75%.

Ian and Nick also compare this period to the 1970s. They say that, outside the ‘nifty fifty’ – the informal name given to a group of US growth stocks had performed strongly in the late 1960s and early 1970s – valuations were relatively low. As inflation – triggered by an energy price shock – soared and remained high for the remainder of the decade, the nifty fifty stocks fell far more than the wider market and then, when things turned, recovered less than the market. The managers point out that there wasn’t anything operationally wrong with these companies, but they were insanely overvalued at the start of the decade and the market came to take a more realistic view of them.

The attraction of the UK

Ian and Nick highlight several reasons to invest in UK companies: they are cheap, offer some of the highest dividend yields, have a large weighting to sectors which do well in inflationary environments and low valuations. They add another reason to buy UK value in particular – because it did well, at least in nominal terms when we had sustained inflation in the 1970s.

It is cheap: whilst equities look expensive in most parts of the world, Ian and Nick point out that one exception is the UK. 50-year averages show that the UK has traded on a 17% discount to the MSCI World, widening to 45% during the middle of last year. Outperformance so far this year has brought this back down to around 38% but by historical standards, the UK is incredibly cheap compared to other markets.

A high dividend yield: Investors have grown used to seeing healthy capital gains from their equity portfolios which have reduced the need to produce an income as investors could sell part of their capital to generate income. However, the changing environment means investors can no longer rely on predictable capital gains and so dividend income may once again become important. The managers note that the UK offers a clear advantage here, as it currently has the highest dividend yield of any developed market of around 4% (ex commodities), compared to 2% from the US.

It is defensive: During the bull market in growth stocks, many investors overlooked the UK as it had limited exposure to the technology, particularly the bigger names. However, Ian and Nick say that the change in monetary backdrop has created a regime change in which the best-performing sectors have been energy and mining, which do well in an inflationary environment, and to which the UK has high exposure.

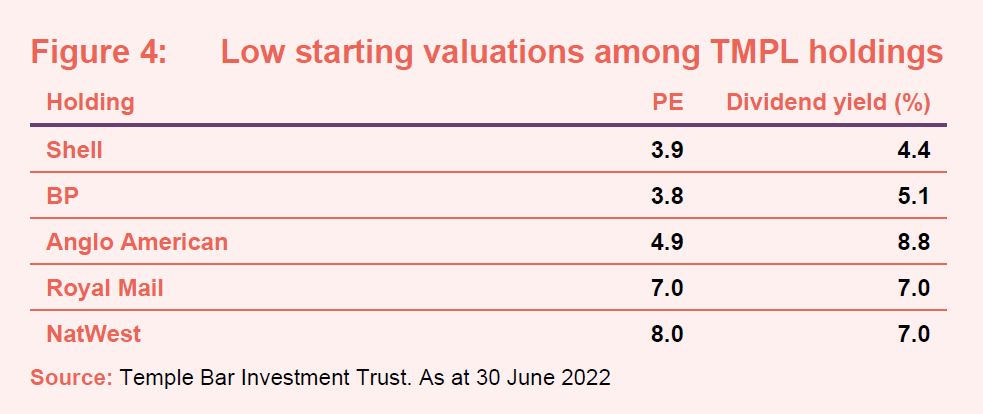

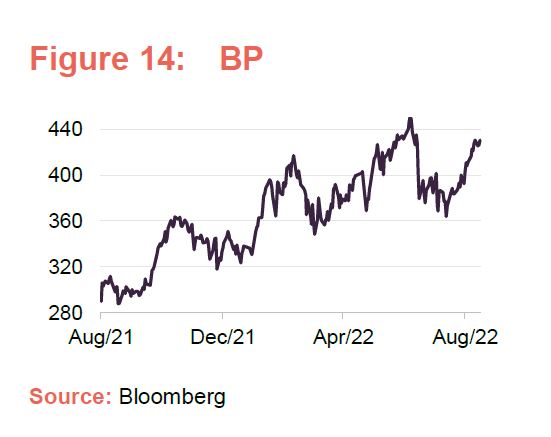

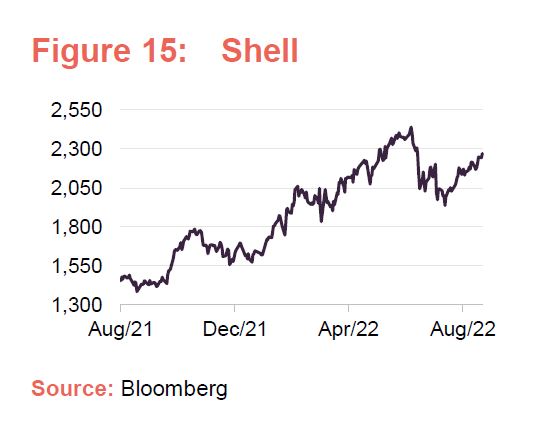

Low valuations: Finally, the valuations of many of the trust’s largest holdings are amongst the lowest that the managers have witnessed over their investing careers (such as Shell, BP and Anglo American – see Figure 4). Although this is no guarantee of success, historically, low starting valuations have been highly correlated with strong subsequent returns.

The managers also note that, while profits downgrades are accelerating – particularly for growth companies – for many of their companies, not much has changed. Generally, they suspect that earnings forecasts are not reflecting the new reality.

Asset allocation

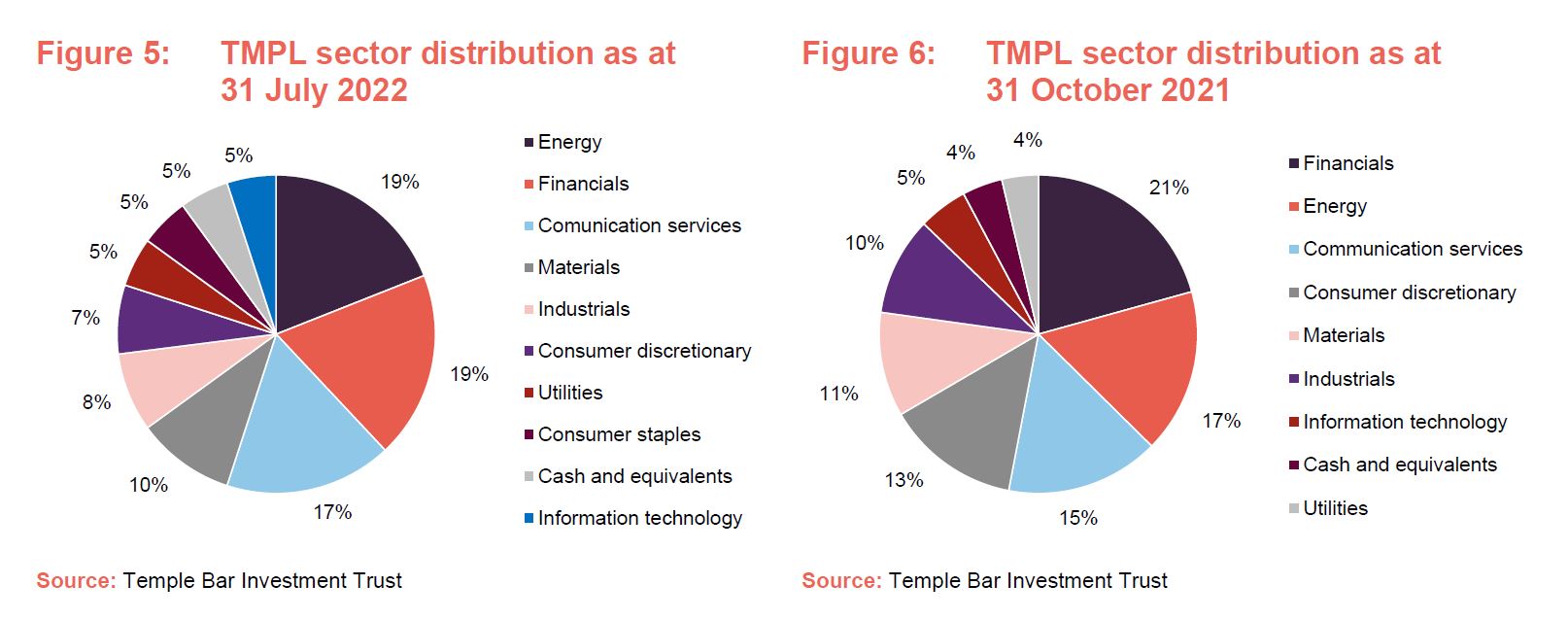

Since our last note, (using data as at end October 2021) TMPL’s sector allocation has seen some small changes. The energy allocation has increased from 17% to 19%, now making it the joint-largest sector weighting alongside the trust’s financials allocation. TMPL’s consumer discretionary weighting has almost halved from 14% to 7%, while exposure towards communication services has increased, albeit marginally. There is now a significant weight of 5% of the portfolio towards consumer staples, which was not present in October 2021.

The managers cut gearing in February, ahead of the outbreak of war in Ukraine, on concerns about the inflationary pressures building in the economy. The managers have started to slowly reintroduce it to take advantage of more-attractive valuations.

Top 10 holdings

Since we last published, Aviva and WPP have dropped out of TMPL’s list of 10-largest holdings to be replaced by Centrica and Pearson. Whilst the ranking of stocks may have changed and some positions may have been added to on weakness or trimmed on profit-taking, Redwheel’s UK’s equity income portfolios tend to be fairly stable.

The managers say they have not completely sold out of any portfolio holdings, nor have they bought anything new since our last note. The only changes they have made have been topping up or trimming existing investments.

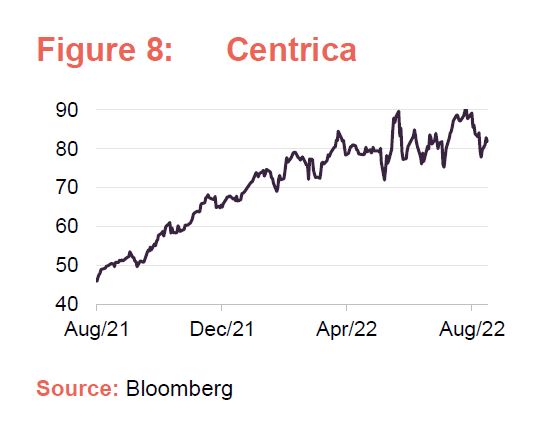

Centrica

Centrica (www.centrica.com) is an energy and services company headquartered in Windsor. Ian and Nick say it was once their problem child and the worst performing stock in the portfolio but over the last couple of years things have been going right. Last year saw lots of competitors in the energy supply market go bust, mainly as a result of pricing too aggressively and not hedging energy supply. This gave Centrica an increase in customer numbers, while the improved regulatory environment has also helped. The value of some of Centrica’s assets has gone up (it has a stake in nuclear producer British Energy) while a change in management saw the sale of its North American assets and a refocus on UK energy supply.

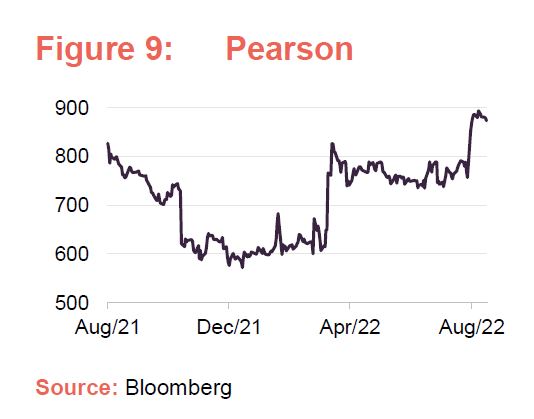

Pearson

Pearson (www.pearson.com) is an education publishing and assessment service for schools and corporations. The company has struggled in recent years, particularly in response to the transition from physical textbooks to digital learning. However, the managers highlight that Pearson has worked hard to boost its online presence and subscription service. Its share price jumped in March on the back of two separate bid approaches from private equity firm, Apollo, and although both bids were rejected – which Ian and Nick praise – the approach serves to highlight the undervaluation in the company’s shares. The managers say that it did not seem right to sell, as Pearson’s performance was finally turning around, and that the board made the correct decision.

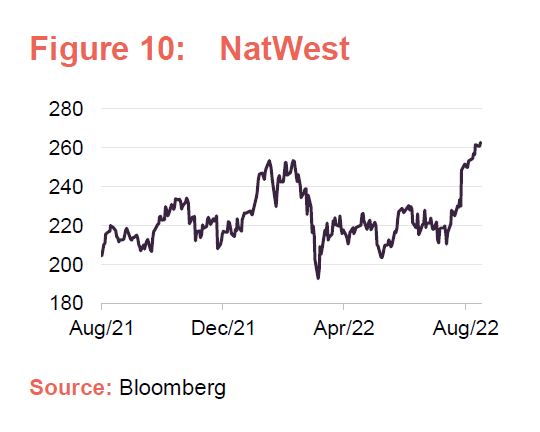

NatWest

NatWest (www.natwest.com) is a major retail and commercial bank in the UK and, along with the financials sector, has performed well in light of the changing economic environment. Many banks have been getting upgrades as higher interest rates usually means higher margins and growing revenues. In its 2022 Q2 results, NatWest’s CEO said the group has a well-diversified loan book and it has not yet seen any significant signs of stress. TMPL’s managers say that they like the bank because it is a simple business with a much more prudently-run balance sheet than many of its peers. They add the management team are really doing a good job in difficult circumstances.

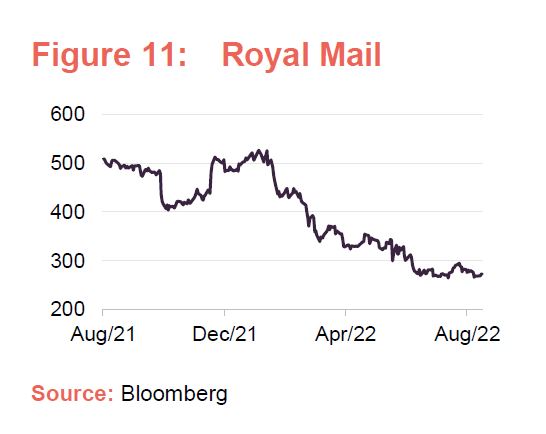

Royal Mail

British postal service Royal Mail Group (www.royalmail.com) has been a long-term favourite of TMPL’s managers and boasts a historical yield of more than 20%. It had a good 2021 and was able to return earnings in the form of dividends, special dividends and share buybacks. For the year ended 31 March 2022, Royal Mail generated £353m of in-year trading cash flow. This was down from the £614m for the prior year, but included an increase in capex of £257m, mainly due to investment in vehicles, hubs and automation in Royal Mail.

The managers note that this year will be more difficult especially with reported strike actions and what with it being a low-profit-margin business. The company has pricing power, but Ian and Nick say that the nature of inflation is that you cannot move fast enough. The most important metric in a logistics company like Royal Mail is the extent to which it is automated. The company is around 50% automated and plans to increase that to 90% over the next two years. This gives it significant scope to drive down costs, which should be helpful against a backdrop of rising inflation.

For the managers, a large part of the attraction of the company is its European parcel business GLS. This fast-growing business is already more profitable than Royal Mail’s traditional business. The company has reiterated its forecast of revenue growth year on year of a high single digit percentage in Euros and operating profit in the range of €370 to €410m for the 2023 financial year.

Performance

TMPL’s performance turned around significantly following Redwheel’s appointment as manager, though as discussed in previous notes, its relative performance got a significant boost as global market sentiment improved in response to positive news on vaccine development in November 2020. This drove a sharp and significant rotation from growth sectors to value sectors, with mining, energy and banks doing particularly well.

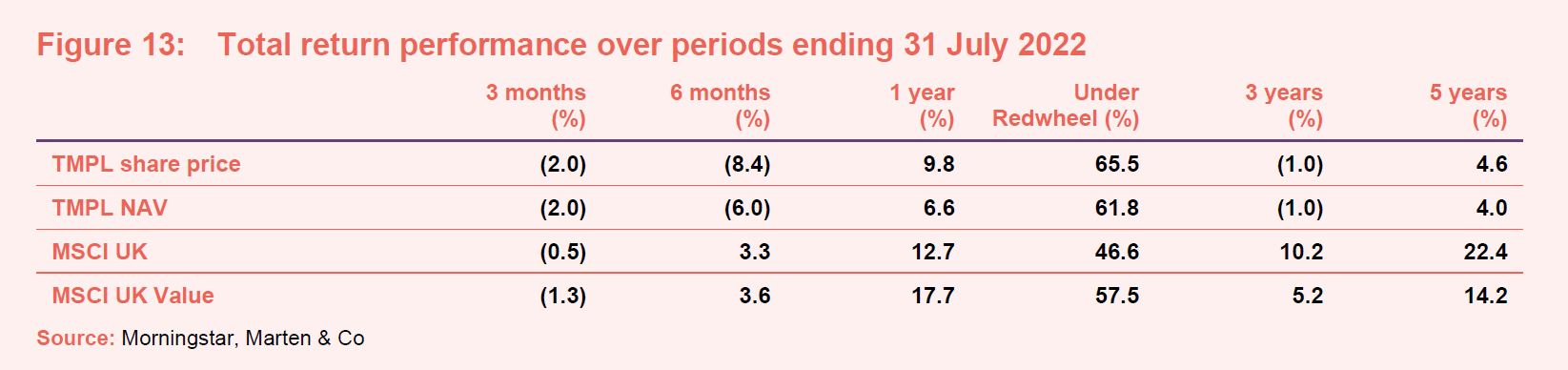

When measured against the MSCI UK and MSCI UK Value, TMPL’s performance has fallen behind over the past three and six months (see Figures 12 and 13). This may prove to be temporary, and we think that long-term strategies such as TMPL’s are better assessed over longer time horizons.

Attribution

Energy companies

TMPL’s three energy companies Shell, BP and Total Energies, were the top-performing contributors to return during the first six months of 2022. They soared on the back of rising oil and gas prices caused by the war in Ukraine, coupled with a muted supply response caused by several years of under-investment in bringing new resources to the market. Ian and Nick add that the companies’ balance sheets are in “good nick” and that they don’t need the oil price to be at the current high levels for very long, as they have generated good cash flow. They say they cannot predict where oil and gas prices might end up in the next few months, but point out that the share prices of all three companies already discount commodity prices that are much below where we are today.

By way of illustration, according to their own sensitivity analysis, BP, Shell and Total Energies are valued on price to earnings ratios of 8x to 9x assuming $60 brent oil (according to Bloomberg data). In late July, oil prices were around $100 brent per barrel, and the managers therefore believe that there is a considerable margin of safety built into the share prices of all three companies.

Standard Chartered

Another strong contributor for H1 2022 was Standard Chartered. This has been a beneficiary of rising dollar interest rates, which in turn should lead to higher income growth and help the bank achieve its 2024 10% return on tangible equity target. The managers say that, although a large increase in interest rates could lead to credit stresses and increased loan loss provisions, the bank has been significantly de-risked over the last few years and lending standards have improved. Therefore, credit provisions may not need to be increased from current levels. The managers say that the company is priced at less than eight times this year’s expected earnings.

Vodafone

https://quoteddata.com/wp-content/uploads/2022/08/220831-TMPL-QD-Fig-18.jpg

Vodafone’s shares have struggled for some time as the company has experienced ongoing price deflation in its main European markets and there is pressure on management to demonstrate the value that exists within the business. In the last few months, both Etisalat and activist investor, Cevian have taken stakes in the company with plans to accelerate the pace of change.

Vodafone has a €12bn holding in separately quoted Vantage Towers (owner of mobile infrastructure), which does not contribute much in the way of cash flow to the group. Ian and Nick believe that if Vodafone were to monetise this asset and return at least a portion of the proceeds to shareholders, the remaining business would be valued on a price earnings ratio of around 8x. The company also has the potential to improve its below-industry-average margins through market consolidation, particularly in the UK and Spain.

Meanwhile, four domestically focused names, Royal Mail, Marks & Spencer, ITV and Currys were detractors from performance during the first six months of 2022.

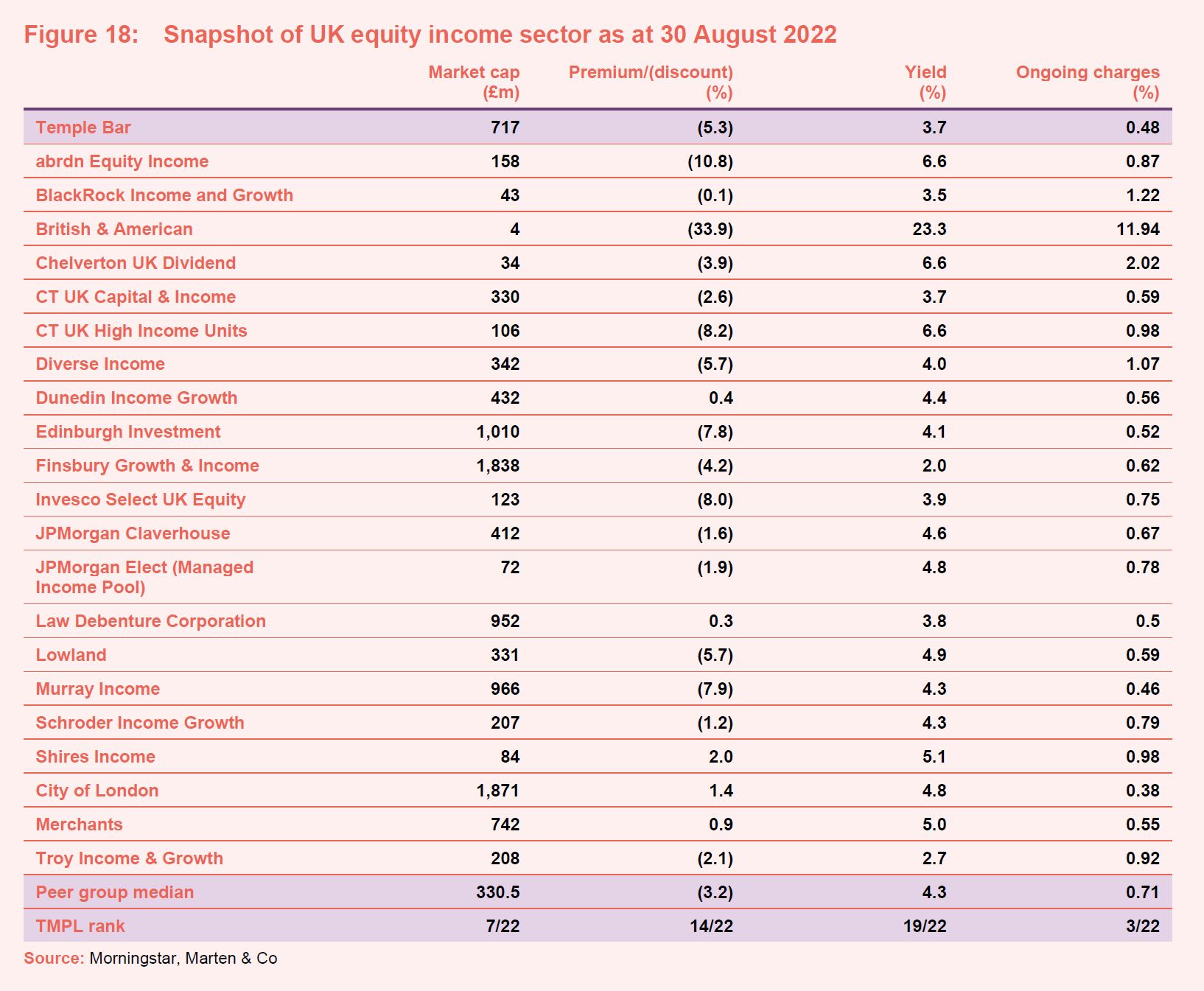

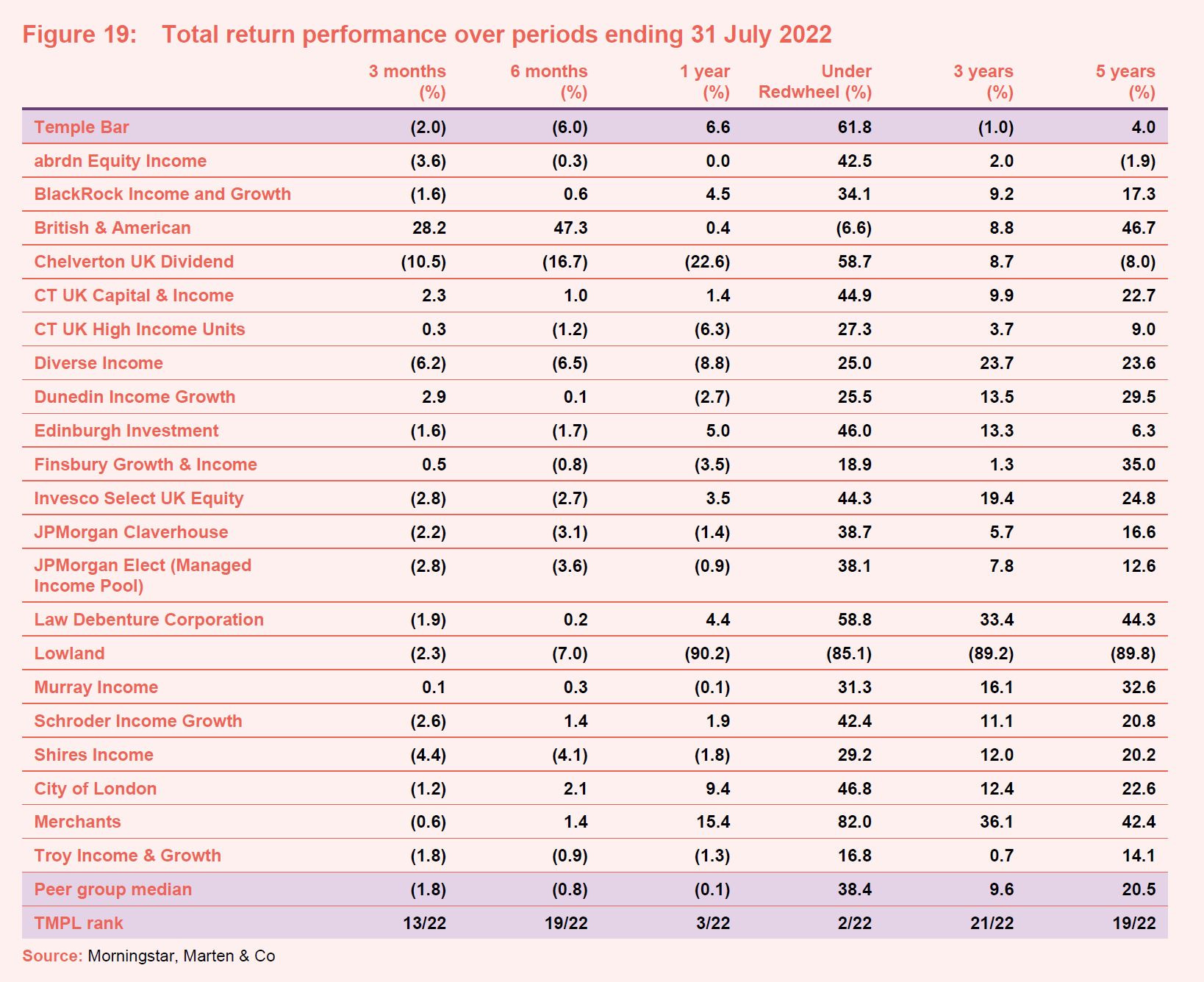

Peer group

TMPL is one of 22 funds in the AIC’s UK equity income sector. It is one of the larger funds in its peer group and this is a factor in its extremely competitive ongoing charges ratio, which is one of the lowest in the sector. Discounts have continued to widen out across the sector since we last wrote, and TMPL sits around mid-table here. The trust’s yield is towards the lower end of the peer group ranking with a figure of 3.7%.

TMPL’s long-term performance numbers are poor compared to its peers. However, the figures improved dramatically following Redwheel’s appointment and, while the six-month numbers reflect the downturn felt across all markets since the start of the year, the three-month figures are more encouraging.

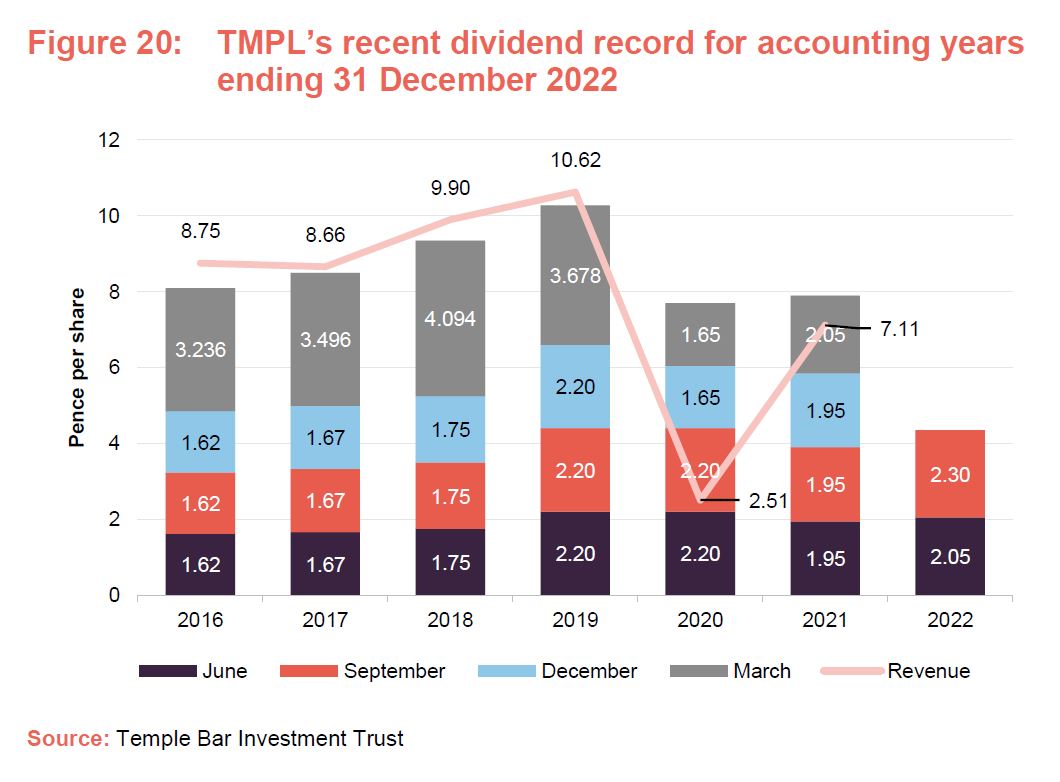

Dividend

TMPL saw a significant increase in income in for the year to 31 July 2021 compared to the previous year, receiving over £30.7m, as its portfolio holdings resumed paying dividends following temporary reductions and suspensions.

Looking at the current financial year, the board of directors declared its first interim dividend of 10.25p per share shortly after its AGM in May 2022. This was based on the number of shares in issue prior to the share split explained here. Taking into consideration the five-for-one share split, the first interim dividend was 2.05p per share, which was paid on 30 June 2022 to shareholders registered at the close of business on 10 June 2022.

TMPL announced its second interim dividend for the year on 16 August 2022 of 2.3p per share, to be paid on 30 September 2022 to shareholders registered at the close of business on 9 September 2022.

TMPL intends to pay four interim dividends totalling at least 8.2p per ordinary share (post-share split) for the year ending 31 December 2022. This will represent growth of at least 3.8% on the equivalent dividends paid for the year ended 31 December 2021.

It is anticipated that this level of dividend will be fully covered by earnings. Going forward, revenue projections imply that in the coming years, further rises in the dividend will be warranted by the portfolio generating more dividend growth.

As is shown in Figure 20, the revenue per share for the 2020 accounting year fell well short of the dividend paid, and the balance was met from revenue reserves. At 31 December 2021, the trust’s revenue reserve stood at £11,708,000 and by 30 June 2022, this had fallen to £11,442,000.

As at 30 June 2022, the company had capital reserves of £611,085,000.

Premium/(discount)

As we discussed in our last note, TMPL’s discount was extremely volatile over the period of turmoil in markets triggered by the pandemic. The discount narrowed in the wake of November 2021’s vaccine announcements and even briefly traded at a premium.

During the first six months of 2022, the discount narrowed from 7.8% to 3.8% as the board continued efforts to generate more buying interest in the company, and has been active in pursuing its buy back policy. During the period, nearly 2 million shares were bought back.

Over the 12 months ended 31 July 2022, TMPL’s shares have traded between a 10.7% and a 1% discount. The average discount over that period was 6.3%. Since the start of 2022, TMPL has largely traded on a single digit discount, and as at

30 August 2022, this stands at 5.3%.

At each AGM, the board asks shareholders for permission to buy back and issue shares within the usual parameters. Repurchased shares are held in treasury.

Five-for-one share split

Following shareholder approval at the trust’s AGM on 10 May 2022, TMPL undertook a five-for-one share split on 13 May 2022. The board proposed the split as they hope it will improve the liquidity and marketability of the trust’s shares. They believe that it will be particularly beneficial to shareholders who invest a regular amount or reinvest their dividends. We agree with the board and welcome the split.

Fund profile

TMPL aims to provide growth in income and capital to achieve a long-term total return greater than its benchmark (the FTSE All-Share Index), through investment primarily in UK securities. The company’s policy is to invest in a broad spread of securities with typically the majority of the portfolio selected from the constituents of the FTSE 350 Index.

Co-managers Nick Purves and Ian Lance aim to rotate the portfolio into those companies which they believe are available at a significant discount to intrinsic value. This involves buying the shares of attractively valued, out-of-favour companies and holding them for the long term until their share prices more appropriately reflect their true value, or until even more attractive ideas present themselves.

For 18 years, TMPL was managed by Alastair Mundy, who was head of the Value Team at Ninety One UK. He stepped down as manager in April 2020, and on

23 September 2020 the board announced that it had selected RWC Asset Management (which rebranded as Redwheel earlier this year) as TMPL’s new investment manager. Redwheel took on responsibility for the portfolio with effect from 1 November 2020 with Nick and Ian named as co-managers. They have over 50 years’ experience between them and have worked together for more than 13 years. The two co-manage over £3bn of assets across a number of income funds. TMPL’s alternative investment fund manager (AIFM) is Link Fund Solutions.

Previous publications

QuotedData has published three notes on TMPL. You can read these by clicking the links in the table below or by visiting our website.

| Title | Note type | Date |

| Keeping faith | Initiation | 23 September 2020 |

| Just getting started | Update | 23 April 2021 |

| No compromise | Annual overview | 8 December 2021 |

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Temple Bar Investment Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication.

Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.