Public matters

On 24 June Caledonia Investments (CLDN) hosted a public companies spotlight event, where the managers presented in detail on the company’s global portfolio of publicly listed investments. This element of the portfolio has a strategic allocation of between 30% and 40% of NAV, currently making up 33%. Around 30 companies are held across two portfolios, with a capital portfolio accounting for 72% of the total and income 28%. The target return is 10% per annum for the capital portfolio and 7% for income.

This note focuses specifically on the public companies strategy, and accompanies our note from April which looked at CLDN’s private capital strategy, following a similar spotlight event. The most recent event could assure one about the high quality of the companies held and the established investment process that determines their selection.

Inflation-beating returns

CLDN’s aim is to generate long-term compounding real returns that outperform inflation by 3%-6% over the medium-to-long term, and the FTSE All-Share index over 10 years.

| 12 months ended | Share price total return (%) | NAV total return (%) | Inflation – CPIH (%) |

|---|---|---|---|

| 31/08/2021 | 34.7 | 29.9 | 2.7 |

| 31/08/2022 | 12.3 | 22.0 | 8.7 |

| 31/08/2023 | (5.0) | 3.1 | 6.2 |

| 30/08/2024 | 9.9 | 7.9 | 3.1 |

| 29/08/2025 | 4.3 | 4.0 | 3.8 |

Company background

Investors may wish to consult the trust’s website at www.caledonia.com

As we covered in detail in our initiation note, which you can read here, CLDN’s investments are spread across three major strategies: private capital, funds, and the focus of this note; public companies. Broadly speaking, the trust applies the same strategic approach to each of these segments: identifying and backing what its managers believe are high-quality and growing companies. They say that one element that is crucial to CLDN’s success is their ability to invest time in understanding these companies and their return drivers. CLDN buys to hold, has a long-term time horizon, and undertakes extensive due diligence on its investments.

The company has a strategic objective to grow the real value of its net assets and dividends, while managing investment risk for long-term wealth creation. CLDN has set itself the target of generating long-term compounding real returns that outperform inflation by 3%-6% over the medium-to-long term, and the FTSE All-Share index over 10 years.

Over the past decade, the company has beaten these targets, generating an annualised NAV total return of 9.5%. A limited number of listed investment companies have an explicit objective of growing shareholders’ capital and income in real terms, and less have been able to deliver such returns on a consistent basis. CLDN’s managers say that the trust’s performance has been built on their ability to focus on a long-term investment horizon and invest only when it believes it has the best opportunities, underpinned by the permanent nature of its balance sheet. As a self-managed trust, CLDN is not constrained by a need to meet short-term performance objectives or comply with fixed-life fund cycles. Without external pressure, the managers are able to ignore fluctuations in markets and can focus on exploiting secular growth rather than short-term cyclical opportunities.

Public companies strategy

The public companies segment of CLDN is split between capital and income portfolios.

CLDN aims to hold between 15 and 20 companies in each of the capital and income portfolios. As at 31 March 2025 there were 18 companies in the former and 17 in the latter. Five companies were held in both portfolios. The capital portfolio is significantly larger, at £698m versus £267m for the income portfolio; together they represent just under £1bn of CLDN’s assets.

The stated aim for the capital portfolio is “investing in companies that will continue to provide compounding returns to shareholders”. This leads to an unconstrained mandate, in that there is no income requirement and as an “all cap” portfolio there is no constraint on the size of the companies held. The target return is 10% per annum.

For the income portfolio, the aim is “investing in resilient businesses with the capacity to pay sustainable dividends”. The target return is lower at 7% per annum, with a target initial yield on cost of 3.5%.

Both portfolios are constructed using the same research methodology. The focus is on holding the highest quality companies, with pricing power and capital allocation particularly important. The managers say that there is no desire or need to invest in super high-growth or super high-income stocks, but instead always this focus on quality.

CLDN is typically a long-term owner through the cycle – the average holding period across the portfolios is 7.4 years. CLDN’s managers seek to build a deep understanding of its investments, and has direct access to senior company management, allowing it to engage in a substantive way.

Each portfolio has a global mandate. Most companies are headquartered in the US, UK or Europe, reflecting what CLDN identifies as the places with the best opportunities. However, the companies are generally global in nature, with geographically diversified revenues.

CLDN’s managers comment that a consistent focus on the investment process, backed up by the permanent balance sheet and depth of knowledge, allows them to take advantage of specific opportunities during periods of market dislocation, when other investors may be constrained. There are therefore times when gaining exposure to quality companies at a cheap price is possible in their view.

Public companies team

Both portfolios are managed by the same team, which comprises six professional managers. Between them, the team has more than 100 years of experience, around half of which is at CLDN.

The team is led by two co-heads, Alan Murran and Ben Archer. Alan is the lead manager on the capital portfolio, a position he has held for six years, having worked at CLDN since 2016. Ben is the lead on the income portfolio. He joined CLDN in 2013 and was appointed to his co-head role in 2022.

The team is completed by Henry Morris (director), Lucy Adams (investment director), Ollie Botes (investment director) and Lukas Brueckner (investment manager).

Together the team brings a high level of expertise to the investment process, backed up by a cohesive culture. The structure of the company allows a dedicated emphasis on investing, which is often not the case at other equity funds. The team feels that a lack of a benchmark ensures that it only acts when the fundamentals are right, while the long-term approach means that short-term market noise can be disregarded.

The team is also fully aligned with shareholders, with members incentivised with an LTIP linked to CLDN’s NAV. There are no carried interest arrangements.

Investment process

CLDN has a robust investment process, centred on its “Quality Matrix”.

The investment process has a focus on bottom-up stock selection, rather than being driven by the macro environment, and is anchored by CLDN’s “Public Companies Quality Matrix”, which helps its managers analyse and benchmark prospective investments. This is shown in Figure 1, with examples of a holding that rates highly in relation to each particular aspect shown around the outside.

Figure 1: CLDN’s “Quality Matrix”

Source: Caledonia Investments

Every company that the managers consider is scored on each metric within the Quality Matrix, which acts as a benchmarking tool for the portfolio and for the internal “work in progress” list of potential investments. The matrix specifically promotes debate within the team.

All the companies held across the two portfolios will score well on most of the metrics within the Quality Matrix, but some are relatively stronger in certain areas. Particular examples of this are shown in the stock-specific case studies that follow.

The managers do not need to consider index weightings, which leads to a wide opportunity set. Fundamental analysis is undertaken, with in-depth research on the specific company and its industry. CLDN’s financial review has been built in-house and is therefore proprietary and not reliant on third parties. Data have been built up over many years, allowing the managers to get a granular picture of how a company has performed over the long-term and through business and market cycles.

The financial review is underpinned by an “owners’ earnings analysis”, that is free cashflow after maintenance capex but before growth capex. The calculation takes net income, adds back non-cash charges such as depreciation and subtracts necessary capital expenditures and working-capital changes. Unlike reported net profit, owners’ earnings focus on the actual free cash available to shareholders, rather than accounting figures influenced by non-cash or timing adjustments. As such, capital deployment can focus on companies that consistently produce surplus cash, aligning with CLDN’s long-term approach.

This analysis is fundamental to decisions on portfolio construction and ongoing monitoring. Specifically, for each company there is a long-term owners’ earnings range which, together with forecasts, helps guide the team as to when its shares are look attractively valued. The managers comment that this allows them to move quickly to take advantage of particular moments of opportunity, such as the immediate aftermath of President Trump’s “Liberation Day” announcements in April.

If the entire public companies team agrees with the investment case for a stock, it progresses to CLDN’s central investment committee, which is chaired by the CEO and comprises the executive directors and heads of the pools of capital. After approval, the team’s valuation discipline means that the managers will wait and look for a favourable entry point before initiating a position.

After purchase, the team will seek to capitalise on market movements to either add to or top slice the holding. This is aided by the nature of the portfolios, which are characterised by high conviction and concentration, with the aim that the team can maintain a deep understanding of the companies held.

The team believes that having a long-term investment horizon means that it can gain have superior investor access, allowing for closer monitoring of portfolio positions. The team prefers to meet companies, be that board members or regional management teams, outside of the reporting cycle, when the individuals in question are not so focused on quarterly or half-year results. Instead, conversations can focus on the long-term opportunity and investment case.

The portfolios have long holding periods.

Both portfolios exhibit long holding periods, at an average (calculated on an AUM basis) of 8.4 years for the capital portfolio and 4.7 years for the income portfolio (equating to an overall average of 7.4 years). Despite being investments in listed companies, these are longer periods than is the case for many private equity investors. In the case of the income portfolio, the managers expect the holding period will increase further, as the current figure has been depressed by a strategy reset five years ago.

Case studies

Fastenal

Source: Bloomberg

Fastenal is one of North America’s largest distributors of industrial and construction supplies, founded and headquartered in Winoma, Minnesota. The company is known for its extensive branch network of 3,600 sites and automated point-of-use distribution model – through vending machines, bin-stocking programmes and more than 2,000 on-site locations – which provides fasteners, safety products, tools, and other consumables to a broad industrial customer base. CLDN’s managers say that Fastenal’s strategy of embedding directly within customer operations fosters long-term relationships, recurring revenues, and strong cash generation. Revenues have grown to more than $7.5bn per annum.

Fastenal was first on the team’s watch list in 2017, with detailed analysis completed in 2019 and early 2020. Under CLDN’s Quality Matrix, Fastenal has consistently ranked as a high-quality compounder. CLDN’s managers note that Fastenal’s business moat and resilience are underpinned by its unrivalled proximity to customers and an owned distribution fleet that ensures a critical service advantage and high switching costs.

Digital capability is another important feature in the managers’ view, with automated vending and Fastenal-managed inventory now accounting for more than 40 per cent of sales, reflecting a growing use of technology to deepen customer integration and reduce working-capital needs. It adds that Fastenal demonstrates a “owner mentality”, with a decentralised model, long-serving employees and a management team that prioritises prudent reinvestment and capital discipline.

The managers comment that these business attributes translate into favourable financial characteristics. For example, Fastenal has no debt and does not pursue acquisition-driven expansion, yet consistently delivers high-single-digit organic revenue growth, operating margins of around 20 per cent and a return on capital employed close to 30 per cent. They add that such capital discipline and predictable cash generation fit squarely with CLDN’s emphasis on companies capable of long-term compounding without dependence on leverage.

Covid provided CLDN with an opportunity to invest at what its managers believe was a favourable average multiple, and in the subsequent five years compounding has delivered strong results they note, with 21% annualised total return since purchase. A recent top slice locked in a proportion of the profit on the holding. Net dividend yield at purchase was 2.7%, and dividends have since grown at a CAGR of 12%.

Representatives from the CLDN team met with Fastenal management in 2022, 2024 and 2025 and have regular calls with the CFO. The company has described it as “a pleasure working with investors of their calibre”.

Pool Corp

Figure 3: Pool Corp (USD)

Source: Bloomberg

Pool Corp (poolcorp.com) is the world’s largest wholesale distributor of swimming pool supplies, equipment and related leisure products. Headquartered in Louisiana and operating under various brand names, it serves more than 120,000 customers through a network of around 450 sales centres across North America, Europe and Australia. Its product range spans chemicals, construction materials, replacement parts, outdoor furniture and irrigation products, positioning it as a one-stop supplier to pool builders, retailers and service professionals.

CLDN’s managers citePool Corp as an example of a business with a decentralised structure that adds value to the business, with the local sales centres empowered to make decisions that suit their local market. This shows up in the owner mentality aspect of CLDN’s Quality Matrix and its managers say that it is particularly beneficial in the fragmented pool and outdoor living industry. They comment that, by giving each sales centre autonomy over purchasing decisions, product mix and customer relationships, the business can remain closely attuned to regional market conditions and consumer preferences. This flexibility allows Pool Corp to adapt quickly to seasonal demand patterns, climate differences and regulatory requirements, in their view.

An factor aspect that is visible in the Quality Matrix is Pool Corp’s pricing power, stemming from what CLDN’s managers describe as its dominant market position and broad product range: they believe that customers value reliability of supply and service more than marginal price differences. They add that Pool Corp’s management has demonstrated that it is able to make good capital allocation decisions, for example, consistently reinvesting in the branch network, making selective bolt-on acquisitions and providing disciplined shareholder returns. In April 2025, the company expanded its share repurchase programme by $309m, bringing total authorisation to $600m. At the same time, it declared a quarterly dividend of $1.25 per share, a 4% increase and the twentieth consecutive quarterly rise since 2004.

In terms of digital capability, another pillar of the matrix, Pool Corp has invested heavily in e-commerce platforms, inventory-management systems and data analytics that allow customers to place orders seamlessly and track delivery in real time, while providing Pool Corp with valuable insights into demand patterns.

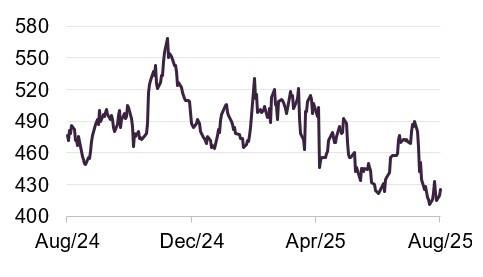

Watsco

Figure 4: Watsco (USD)

Source: Bloomberg

Watsco (watsco.com) is held in both the capital and income portfolios. It is the largest distributor of air conditioning, heating and refrigeration equipment and related parts and supplies in the Americas, serving a network of contractors across residential and commercial markets. Headquartered in Miami, the company operates more than 600 locations throughout the United States, Latin America and the Caribbean, providing products from leading manufacturers alongside its own private-label brands.

CLDN’s managers say that Watsco has invested heavily in digital tools and e-commerce platforms to support its contractor customers – tying in with the Digital element of the Quality Matrix. This initially had a negative impact on profits but created an entry point for CLDN and, in the managers’ view, enabled the company to be future-fit, it also enhanced the owner mentality of employees – another aspect that features in the matrix. The managers add that the corporate culture at Watsco is to empower associates and promote entrepreneurialism, and over time this reinforces the company’s competitive position and ensures a long-term focus that is aligned with shareholders.

Recently, Watsco has expanded its footprint through strategic acquisitions, bringing Southern Ice Equipment Distributors, Lashley & Associates in Houston and Hawkins HVAC Distributors in the Carolinas into its portfolio. These deals added over 10 new locations and around $47m in annual sales. In addition, July’s announcement of a $3 quarterly dividend marked its two-hundredth consecutive quarter of payouts.

Oracle

Figure 5: Oracle (USD)

Source: Bloomberg

Oracle (oracle.com) is a global provider of enterprise software, cloud services and database technology, perhaps best known for its flagship Oracle Database and broad suite of applications spanning enterprise resource planning, customer relationships and supply chain management. The company has evolved from a database-focused business into a diversified technology giant, with a strong emphasis on cloud infrastructure and software-as-a-service offerings.

CLDN’s managers say that Oracle’s competitive edge lies in integrating advanced technologies such as artificial intelligence, analytics and cybersecurity across its platforms, enabling organisations to modernise operations and improve efficiency. They add that a particularly attractive feature is the stickiness of its customer base, reflecting the extent to which Oracle’s software becomes integral to its clients operations. As well as boosting pricing power – one of the aspects of the Quality Matrix – CLDN’s managers say that leads to a high level of customer retention and resilience through business cycles.

They add that the company’s buyback discipline and sustained dividend growth highlight its strength in making capital allocation decisions, per the matrix, while ongoing investment in AI-driven cloud infrastructure strengthens its digital credentials and competitive positioning.

Recent newsflow for the company is covered on page 15.

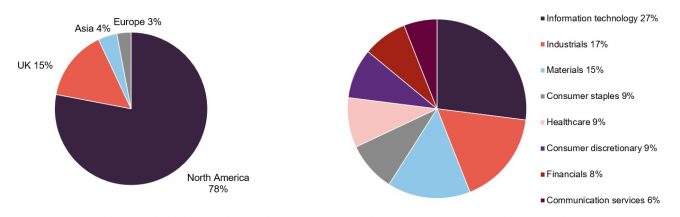

Capital portfolio

CLDN’s public companies strategy is dominated by the £698m (as at 31 March 2025) capital portfolio.

Asset allocation

Figure 6: Split of capital portfolio by geography as at 31 March 2025

Figure 7: Split of capital portfolio by sector as at 31 March 2025

Source: Caledonia Investments

Source: Caledonia Investments

As shown in Figure 6, North American-headquartered companies dominate the capital portfolio, with a moderate exposure to the UK and negligible holdings elsewhere. The largest sector exposure, per Figure 7, is to technology, the majority of which is accounted for by Microsoft and Oracle, the two largest holdings (which have both increased in value since the end of March, as covered on page 15).

Top 10 holdings – capital portfolio

Figure 8: 10 largest holdings in capital portfolio as at 31 March 2025

| Holding | Business | First invested | Value (£m) |

|---|---|---|---|

| Microsoft | Software | 2014 | 73.6 |

| Oracle | Software | 2014 | 72.3 |

| Philip Morris1 | Tobacco and smoke-free products | 2016 | 64.8 |

| Watsco1 | Ventilation products | 2017 | 58.4 |

| Texas Instruments1 | Semiconductors | 2018 | 46.5 |

| Charter Communications | Telecommunications | 2017 | 40.4 |

| Thermo Fisher | Life sciences | 2015 | 38.7 |

| Moody’s Corporation | Financial services & analytics | 2022 | 38.3 |

| Hill & Smith | Infrastructure products | 2011 | 35.6 |

| Pool Corp | Pool distribution | 2024 | 31.9 |

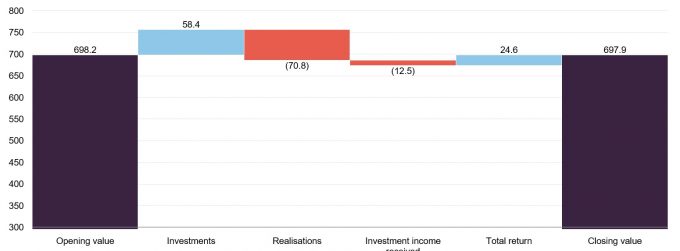

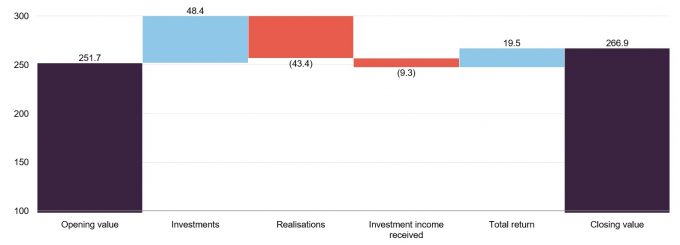

Portfolio movements

Figure 9: Capital portfolio movements (£m) over one year to 31 March 2025

Source: Caledonia Investments, Marten & Co

During the year there was one new purchase, namely Pool Corp, which is explored in more detail above. British American Tobacco was the one complete sale.

There were partial sales during the year of Fastenal, Oracle and Watsco, in all cases realising gains following sustained share price increases. All three stocks are covered later in the report.

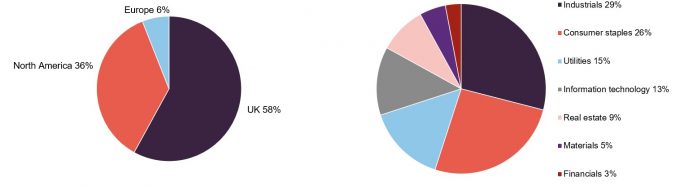

Income portfolio

The income portfolio is a much smaller part of the public companies strategy, with a value of £267m (as at 31 March 2025).

Asset allocation

Figure 10: Split of income portfolio by geography as at 31 March 2025

Figure 11: Split of income portfolio by sector as at 31 March 2025

Source: Caledonia Investments

Source: Caledonia Investments

As illustrated in Figure 10, the UK is the largest geography in the income portfolio, which is a market dominated by companies in sectors that tend to pay higher yields. North America makes up just over a third and Europe the remainder. The sector exposure, per Figure 11, is relatively diversified, with only a modest technology weighting. Holdings are also spread across areas that tend to be noted for paying consistent income streams to investors, such as utilities and consumer staples.

Top 10 holdings – income portfolio

Figure 12: 10 largest holdings in income portfolio as at 31 March 2025

| Holding | Business | First invested | Value (£m) | Yield (%) |

|---|---|---|---|---|

| Philip Morris1 | Tobacco & smoke-free products | 2021 | 25.3 | 5.7 |

| National Grid | Utilities | 2015 | 20.9 | 5.6 |

| Unilever | Consumer goods | 2019 | 18.9 | 3.5 |

| Fortis | Utilities | 2020 | 18.5 | 3.8 |

| Watsco1 | Ventilation products | 2020 | 18.2 | 6.1 |

| Relx | Information &analytics | 2023 | 18.2 | 2.4 |

| Texas Instruments1 | Semiconductors | 2020 | 17.7 | 3.9 |

| SGS | Testing | 2020 | 16.8 | 2.4 |

| Sage Group | Software | 2024 | 16.6 | 1.6 |

| Fastenal1 | Industrial distribution | 2020 | 15.4 | 4.3 |

Portfolio movements

Figure 13: Income portfolio movements (£m) over one year to 31 March 2025

Source: Caledonia Investments, Marten & Co

There were three new positions initiated in the income portfolio over the year: Sage, Howdens and Croda.

Sage – an accounting, HR, and payroll software provider to small and medium-sized enterprises. CLDN’s managers comment that Sage has a record of consistent operational delivery, with stable recurring revenues, adding that its AI-powered offerings are seeing strong demand, with Sage Copilot – launched in 2024 – already serving 40,000 UK customers. Similarly, Sage Business Cloud is achieving double-digit revenue growth. Following a £400 million share buyback in late 2024, Sage extended the programme by an additional £200 million in mid‑2025, while raising its interim dividend by 7%.

Howdens – the UK’s largest trade kitchen supplier. The managers note that Howdens has a track record of generating consistent cash returns, defending margins and expanding market share even in a subdued UK kitchen and joinery market. With gross margins above 60% and a nationwide depot expansion strategy, Howdens offers a combination of operational resilience, disciplined capital allocation and growth potential in the managers’ view. The company recently committed to a £100m share buy-back programme, and the share price has risen by around 30% since April.

Croda – the speciality chemicals company, which is also held in the capital portfolio. The managers comment that Croda’s shares have been under pressure due to operational deleveraging amid demand headwinds in its end markets, and this weakness presented them with a favourable entry point. Croda is a long-term buy in their view, given its record of disciplined cost cutting and growth in its higher‑margin divisions, as well as consistent dividend increases. Its ongoing transformation plan includes a target of £100m annualised cost‑saving by 2027 and an asset optimisation programme that is already yielding benefits. The managers add that demand in the Consumer Care division, together with stable Life Sciences performance, underpins confidence in Croda’s ability to return to growth.

Three holdings were exited over the year: DS Smith – following the announcement of the agreed offer from International Paper – Pennon Group, and Reckitt Benckiser.

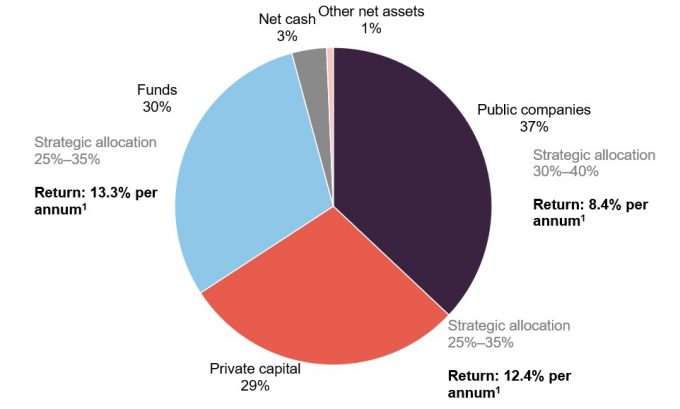

Asset allocation – whole portfolio

Figure 14: Split of portfolio by type as at 31 August 2025

Source: Caledonia Investments. Note 1) average over 10-year p

There is minimal change to CLDN’s overall allocation from the time of our last note in April. Private capital and net cash allocations have reduced slightly, with public companies increasing from 33% to 37%.

Sale of Stonehage Fleming

CLDN announced on 2 September, as this note was being written, that it had agreed terms for the sale of its largest overall holding, Stonehage Fleming, to Miami-based Corient Private Wealth. CLDN had a large minority stake of 36.7% in the multi-family office, held within the private capital pool, and will receive £251m when the deal closes in the first half of 2026. A further £37m will be paid in two tranches six months and a year after completion. Another £9m may be received if Stonehage hits three-year revenue targets under its new owner.

Including dividends received, CLDN says it will make a 3.2x return on its initial £90m investment in 2019, including a £67m or 30% uplift from its £221m value at 31 March. The proceeds will be held on deposit for future reinvestment.

CLDN’s managers see this as a positive outcome, adding that this is another example of its investment process securing favourable outcomes for shareholders over the medium and long-term.

The following sections all use data from 31 August, before the Stonehage sale was announced.

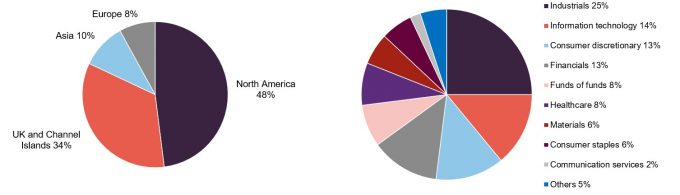

Figure 15: Split of CLDN portfolio by geography as at 31 August 2025

Figure 16: Split of CLDN portfolio by sector as at 31 August 2025

Source: Caledonia Investments

Source: Caledonia Investments

Top 10 holdings – whole portfolio

Figure 17: CLDN 10 largest holdings as at 31 August 2025

| Business | Value (£m) |

% of NAV 31/08/25 | % of NAV 31/03/25 | Change (%) |

|

|---|---|---|---|---|---|

| Stonehage Fleming | Family office services | 222.4 | 7.6 | 7.6 | n/a |

| Cobepa | Investment company | 196.4 | 6.7 | 6.6 | 0.1 |

| AIR-serv Europe | Forecourt vending | 173.2 | 5.9 | 6.8 | (0.9) |

| Butcombe Group | Pubs, bars and inns | 137.5 | 4.7 | 4.7 | n/a |

| Oracle | Software | 101.9 | 3.5 | 2.4 | 1.1 |

| Microsoft | Software | 95.0 | 3.2 | 2.5 | 0.7 |

| Phillip Morris | Tobacco & smoke-free products | 90.6 | 3.1 | 3.1 | n/a |

| HighVista Strategies | Funds of funds | 86.7 | 3.0 | 3.4 | (0.4) |

| Texas Instruments | Semiconductors | 77.6 | 2.7 | 2.2 | 0.5 |

| Axiom Asia funds | Fund of funds | 65.8 | 2.2 | 2.5 | (0.3) |

| Total | 1,247.1 | 42.6 | 51.1 |

As would be expected for a fund with a long-term approach to investments, there have been limited changes to the makeup of the top 10 holdings since our note published earlier in the year (which used data as at 31 March). Texas Instruments is the one new entry, and is explored in more detail below. It has replaced Watsco.

Oracle has risen from tenth- to fifth-largest holding due to a sharp increase in the shares over recent months. CLDN’s managers comment that this was driven by quarterly earnings that were well ahead of analyst expectations, and standout future guidance. They add that this was largely due to Oracle’s Cloud Infrastructure (OCI) and AI offerings; the former is growing by more than 50% year-on-year. The company has signed a $30bn cloud services agreement as part of its Stargate venture with OpenAI and SoftBank, as well as a strategic partnership agreement with Google Cloud, enabling Oracle to offer Google’s Gemini AI models through its OCI platform. Oracle is covered in more detail on page 8.

Although Oracle’s returns are particularly strong, the wider US technology sector has risen strongly in recent months, which enabled Microsoft to climb from eighth to sixth position in CLDN’s top ten.

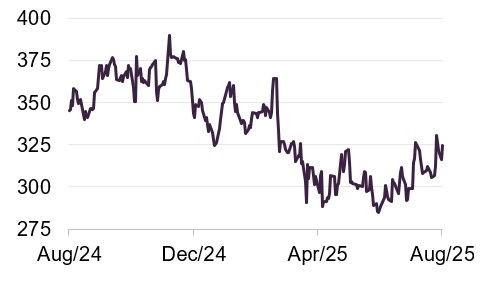

Texas Instruments

Figure 18: Texas Instruments (USD)

Source: Bloomberg

Texas Instruments (TI, ti.com) is a large US-based semiconductor designer and manufacturer, specialising in analog chips and embedded processors. Headquartered in Dallas, TI’s technology has a long history of technological development, from pioneering the integrated circuit and handheld calculator to powering industrial, automotive and consumer electronics with reliability and scale.

TI has moved into CLDN’s overall top 10 holdings due to a recent share price increase, which has seen the share price rise by a third from its April low. The company broke a nine-quarter streak of declining sales and earnings when it reported results that month, while also presenting what CLDN’s managers describe as optimistic future revenue and earnings guidance. In addition, as a domestic manufacturer, TI secured exemptions from President Trump’s potential 100% semiconductor tariffs, and is reportedly set to increase prices across 10,000-20,000 products by between 20%-50%, providing a significant boost to margins.

Longer-term, TI has strategically increased its US manufacturing footprint, with the first fab at its Sherman mega site (SM1) due to begin production later this year. This is one of three major manufacturing sites that TI is building in the US as part of its $60bn investment in domestic semiconductor capacity. The company’s ongoing shift to more cost‑efficient 300mm fabrication is expected to significantly boost free cash flow by 2026. The company also has an unbroken record of 50 years of dividend payouts.

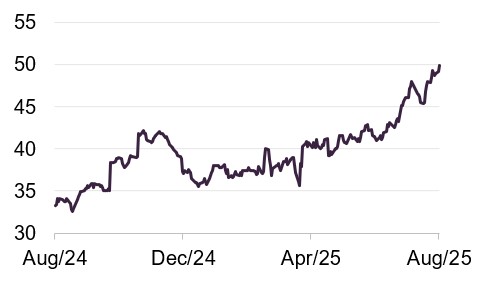

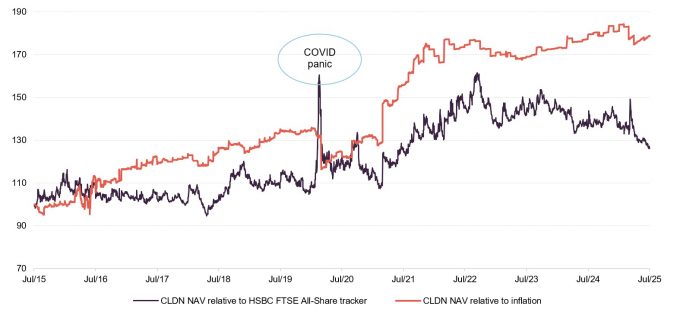

Performance

CLDN has beaten both the FTSE All-Share Index and inflation over 10 years.

The performance of CLDN is not benchmarked against an index or peer group. Nonetheless, the fund has set itself a target of generating long-term compounding real returns that outperform inflation by 3%-6% over the medium-to-long term, and the FTSE All-Share Index over 10 years.

Figures 19 and 20 show that CLDN has surpassed both these objectives, with 10-year returns notably above both UK equities and inflation. Some investors may consider that, for a fund with such a clear long-term focus, this sustained long-term performance is an important consideration. For the purposes of this report, we have used the HSBC FTSE All-Share Index Fund Class C accumulation units, which seek to track the returns of the FTSE All-Share Index. As a measure of inflation, we have used UK CPIH, which is the consumer prices index including owner-occupiers’ housing costs.

Over 10 years to 31 March 2025, the public companies pool specifically delivered an 8.4% annualised return, split 10.2% for the capital portfolio and 4.6% for the income portfolio.

As explained in more detail on page 17, whilst NAV returns have been robust, those to shareholders have been held back by the fund’s discount.

Figure 19: CLDN NAV total return performance relative to HSBC All-Share tracker and UK inflation (CPIH) over 10 years ended 31 July 2025

Source: Bloomberg, Marten & Co

Figure 20: CLDN total returns for periods ending 31 July 2025

| 3 months (%) | 6 months (%) | 1 year (%) | 3 years (%) | 5 years (%) | 10 years (%) | |

|---|---|---|---|---|---|---|

| Share price | (0.9) | (2.3) | 0.2 | 1.0 | 59.0 | 101.5 |

| NAV | 2.9 | (0.4) | 3.8 | 17.1 | 85.5 | 147.6 |

| Inflation (UK CPIH) | 0.6 | 2.5 | 4.2 | 14.3 | 26.8 | 38.5 |

| HSBC FTSE All-Share tracker | 9.5 | 8.8 | 12.2 | 34.9 | 78.0 | 96.2 |

| MSCI ACWI | 13.0 | 1.3 | 12.5 | 40.8 | 81.0 | 207.2 |

| Inflation plus 3% per annum1 | 1.3 | 4.0 | 7.2 | 24.4 | 46.0 | 84.4 |

| Inflation plus 6% per annum1 | 2.0 | 5.4 | 10.2 | 35.1 | 67.5 | 143.6 |

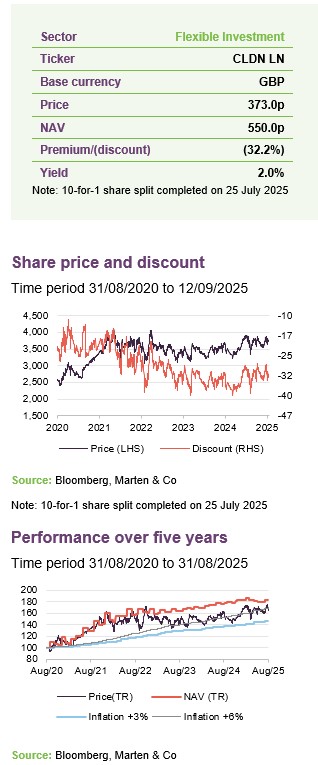

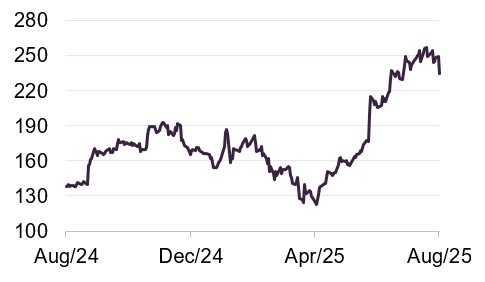

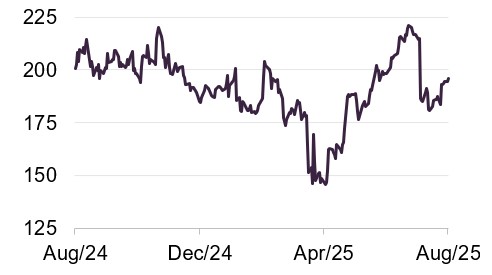

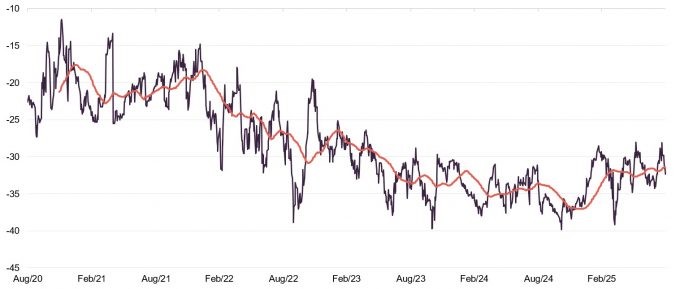

Discount

We have written about the persistent CLDN discount in all of our previous notes, and the position remains broadly unchanged. Over the 12 months ended 31 August 2025, the range was 28.1% to 39.9%, with an average of 33.6%. The current discount is 32.2%, versus 35.5% at the time of our previous note in April and so there has been a modest narrowing. Nonetheless, the board and managers have stated that they anticipate some narrowing over the long term.

Figure 21: CLDN discount over five years ended 31 August 2025

Source: Bloomberg, Marten & Co

The board actively seeks to address the continued discount. As we have covered in previous notes, shareholders approved a “Rule 9 waiver” under the Takeover Code, allowing the Cayzer family’s share of the trust to increase above 50% without the family being obliged to make a takeover bid. At the shareholder meeting in December, it was approved that the company can repurchase up to 5% of its shares in issue.

In addition, the board proposed a 10-for-1 share split, that was implemented in July 2025. That rationale behind the split was that, by reducing the nominal price of each share, the trust should become more accessible, hopefully improving liquidity and potentially reducing bid-ask spreads. It should also make smaller shareholdings more feasible, potentially attracting a broader set of investors.

The board also changed the balance between the interim and final dividends. By increasing the interim dividend to be closer to 50% of the total, income is more evenly spread during the year, which again is intended to increase the attraction of CLDN’s shares.

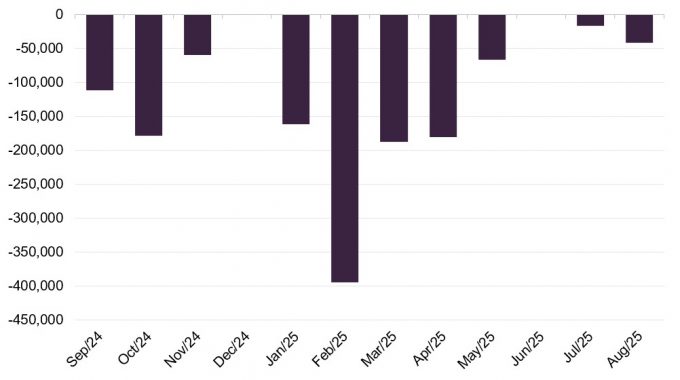

Figure 22: CLDN share buybacks by month

Source: Caledonia Investments. Note: repurchases after the 10-for-1 share split on 25 July have been adjusted to ensure comparability.

As shown in Figure 22, the board has actively used this approval to buy back shares. Over the past year, 1,398,885 shares have been repurchased (note that, due to the 10-for-1 share split in July, figures since then have been adjusted to ensure comparability), which enhances NAV for shareholders and provides liquidity to those wanting to sell. It seems reasonable that CLDN could continue to repurchase shares, albeit the rate has slowed somewhat in recent months.

Previous publications

Readers interested in further information about CLDN may wish to read our previous notes listed below. You can read them by clicking on the links in Figure 23 or by visiting our website.

Figure 23: QuotedData’s previously published notes on CLDN

| Title | Note type | Date |

|---|---|---|

| Time, well invested | Initiation | 15 July 2024 |

| Addressing the discount | Update | 9 December 2024 |

| Playing the long game | Update | 14 April 2025 |

IMPORTANT INFORMATION

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Caledonia Investments Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it. Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.