CLSC Initial Public Offering

Investment companies | IPO note | 22 November 2022

Conviction Life Sciences Company (CLSC) has a target issuance of up to 100m ordinary shares at 100p per share as part of the company’s initial issue, equal to an initial market cap of up to £100m.

CLSC is being launched to capitalise on two avenues of return presented by the global life sciences and medical technology markets, the first being the inherent structural growth opportunities which are presented by the sector, and the second being what the directors believe is a materially undervalued sector, particularly outside of the United States. CLSC’s addressable markets will include, for example, novel therapeutics (both large- and small-molecule), medical technology (including devices and diagnostics), pharmaceutical services, and digital health.

Life sciences and medical technology

CLSC will seek to deliver capital appreciation to shareholders by investing in a high conviction portfolio of both publicly traded and private life sciences and medical technology businesses, based primarily in the UK, Europe and Australasia. CLSC will target an annualised NAV total return of 20% over the long term.

The details of the share issue, including the risk factors that investors should take into consideration, are more fully described in the prospectus published by Conviction Life Sciences Company on 16 November 2022 and we urge readers to read this before making any investment decision. The approval of the prospectus by the Financial Conduct Authority should not be understood as an endorsement by the Financial Conduct Authority of the securities offered. If you have any doubts about the suitability of an investment you should seek professional advice.

IMPORTANT INFORMATION

NB: Marten & Co has been paid to prepare this note on behalf of Conviction Life Sciences Company. This is a marketing communication and not a prospectus.

The note is based upon publicly available information and information provided to us by Conviction Life Sciences Company and should be read in conjunction with the Conviction Life Sciences Company Prospectus published on 16 November 2022 and which can be found at clsc.uk

Readers should not place any reliance on the information contained within this note.

The note does not form part of any offer and is not intended to encourage the reader to subscribe for ordinary shares in Conviction Life Sciences Company or deal in any other security or securities mentioned within the note.

Marten & Co does not seek to and is not permitted to provide investment advice to individual investors.

The note is not intended to be read and should not be redistributed in whole or in part in the United States of America, its territories and possessions; Canada; Australia; the Republic of South Africa; or Japan.

Click for links to trading platforms

Click for a link to an interview with the manager

Click here for link to the share trading platforms

Investment proposition

CLSC is aiming to raise up to £100m through its initial issuance of shares, with an initial issue target of up to 100m ordinary shares at 100p per share. The initial issuance is open from 16 November 2022 until 3:00pm on 13 December 2022 for application from the intermediaries offer, 11:00 am on 13 December 2022 for online applications or application forms in respect of the offer for subscription, and 5:00pm on 13 December 2022 for commitments under the initial placing. The announcement of the results of the initial issue will be made on 14 December 2022, with dealings in the ordinary shares commencing at 8:00 am on 16 December 2022.

CLSC may subsequently issue further shares under the share issuance programme until 15 November 2023.

Application will be made for the shares to trade on the premium segment of the main market of the London Stock Exchange.

Investment objective and policy

Aims to generate at target annualised NAV total return of 20% over the long term

CLSC aims to deliver capital appreciation to shareholders over the long-term by investing in a high-conviction portfolio of both publicly traded and private life sciences and medical technology businesses, based primarily in the UK, Europe and Australasia. CLSC has been designed to capitalise on the structural growth opportunities presented by the global life sciences and medical technology markets. Examples of companies that CLSC will target include novel therapeutics, medical technology, pharmaceutical services, and digital health. CLSC will invest in a concentrated portfolio of 20-40 businesses to capitalise on the perceived structural undervaluation and the attractive asymmetric return profile which may result if it unwinds. CLSC will invest in both public and private companies, though with a targeted allocation of 70% and 20% respectively, public equities will make up the bulk of CLSC’s portfolio.

CLSC has a target annualised Net Asset Value (NAV) total return of 20% over the long term. However, this is intended to be a target only and reflects the board’s and the investment manager’s expectations of the potential returns that can be generated by CLSC.

Why life sciences?

CLSC is being launched in part to capitalise on the inherent structural growth opportunities which are presented by the sector

CLSC is being launched to capitalise on two avenues of return presented by the global life sciences and medical technology markets, the first being the inherent structural growth opportunities which are presented by the sector, which reflect the world’s ever-increasing demand for both greater quantity and complexity of medical treatments. Be they the inherent technological progress occurring within the industry, the health issues arising from aging global demographics, or simply a changing regulatory environment which is conducive of higher investment spending into medical sciences, these structural opportunities go hand-in-hand with what the directors believe is a materially undervalued sector, particularly outside of the United States. CLSC’s addressable markets will include, for example, novel therapeutics (both large- and small-molecule), medical technology (including devices and diagnostics), pharmaceutical services, and digital health.

The manager

CLSC is an internally managed Alternative Investment Fund and has appointed Plain English Finance to provide certain services in relation to CLSC and its portfolio, including portfolio management, and due diligence in relation to proposed investments. Three members of Plain English Finance have been identified as the core management team: Andrew Craig, Dr Luke Zhou, and Roderick Collins.

CLSC and the investment manager have formed an investment committee, which will report to the board of CLSC. The investment committee will be chaired by Geoff Miller (see page 15) and will consist of the core management team, and Dr Victoria Gordon and Geoff Miller on behalf of the board.

Andrew Craig and Dr Luke Zhou will present all potential portfolio businesses to the investment committee, which will determine which investments to approve. Only such approved investments may be purchased.

Andrew Craig (Founder of Plain English Finance)

Andrew is a finance author and former partner at a specialist life sciences boutique investment bank, WG Partners LLP. He acted for more than 60 life sciences companies in his time at WG Partners LLP. Andrew began his finance career at SBC Warburg in the late nineties. His first book, “How to Own the World“, has been No.1 rated on Amazon in categories such as Pensions, Investments and Personal Finance for much of the last few years. Andrew’s next book “Our Future is Biotech” is slated for publication in the first half of 2023.

Dr Luke Zhou

Luke is an experienced cancer-research scientist and sector investor with expertise in cell-biology and gene-therapy. His work has been published in leading journals and has been recognised by Cancer Research UK and Children’s Tumour Foundation (US). Luke is also an experienced entrepreneur and angel investor in the sector and has co-founded several companies in the UK and China.

Roderick Collins

Roderick has had a long and distinguished career in financial services and wealth management. He held senior management positions with NM Rothschild and James Capel and was the chief executive of the private banking activities of Matheson & Co from 1985 to 2000. Roderick has particular expertise in closed-end fund management.

An investment opportunity supported by sectoral tailwinds

The creation of CLSC reflects an intention by the directors to capitalise on what they believe are clear structural opportunities across both the wider world as well as specific to the medical sciences industry. They believe that these opportunities will be able to offer CLSC’s shareholders the potential for an attractive level of capital growth.

The directors also believe that superior valuation opportunities will be found outside of the United States, and CLSC will thus focus on companies in non-US regions. We note that this regional focus will set CLSC apart from the typical exposure of major global biotechnology and life sciences indices, which often have the majority of their exposure to the US market.

Scientific and technological progress

Of all the various tailwinds, the directors believe that the dominant force is the increasing possibilities presented by global scientific and technological progress

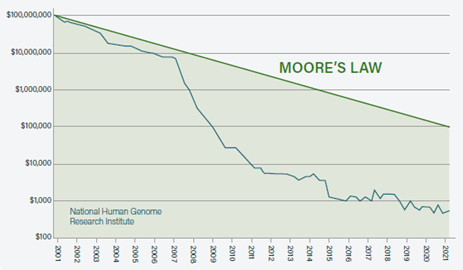

Of all the various tailwinds driving the growth in the life sciences and medical technology sector, the directors believe that the dominant force is the increasing possibilities presented by global scientific and technological progress, where the increased capabilities of medical research can create significant economic value. For example, publications have shown that since the 1990s, the cost and time required to sequence a human genome have fallen by magnitudes, from approximately US$3bn and about thirteen years, to US$200 and a few hours.

Figure 1: Cost per Human Genome

Source: National Human Genome Research Institute

Whilst the medical applications of biotechnology are apparent, what readers may not be aware of are its multiple non-medical applications, with the technology having been responsible for very significant value creation in the last few decades. This is a trend that the directors believe will continue for decades given that the most intractable remaining challenges for humans concern biological systems. They give examples of biotechnology having a key role to play in clean power generation, improving agricultural productivity and environmental stewardship, and even in the development of processing power. In practical terms, global consultancy firm McKinsey, has estimated that up to 60% of the world’s physical inputs could, in principle, be made using biological means, while up to 45% of the world’s disease burden could be addressed using science that is conceivable today, leading to US$2-4trn of global annual direct economic potential using biological applications by 2030-40.

Supportive demographics

An ageing world will lead to increasing more, and more complex, medical issues which will need to be remedied

The world is ageing at an increasing rate, with the UN predicting the median age of the global population to rise by approximately 20% between 2020 and 2050. Age may bring not only wisdom but also, unfortunately, more complex medical problems, increasing the rates of many diseases, particularly cancer, and thus the demand for healthcare overall, as outlined by the American cancer society. The advent of new illnesses is not simply a reflection of age, but also of a more modern, industrialised society, one which has led to a raft of new diseases which need to be addressed, with the likes of eczema, asthma, autism, diabetes, epilepsy now requiring greater volumes of treatments. These “diseases of modernity” are in addition to increased autoimmune diseases as well as rising mental illness and lifestyle issues also needing attention, which present unfortunate (but necessary) opportunities for businesses to develop new treatments.

However, this ageing is also expected to be accompanied by greater wealth, especially amongst the emerging market regions, with regions that previously had no access to modern medicine now having functional healthcare services and drugs available to them. In 2021, India announced plans to double healthcare spending as a percentage of GDP, for example. The Chinese healthcare market is already the second-biggest in the world, having grown rapidly for many years.

Increased support from the public sector

There is an increasing political will to increase the funding for regulators

Given the issues we have outlined above, it should come as no surprise that there is an increasing political will to increase the funding for regulators, with COVID-19 arguably being a wake-up call for many governments, as Linklaters reported that post COVID-19 governments are looking at ways to increase the speed at which important products are able to gain market access by removing or easing some of the regulatory burdens. There is also an economic advantage for governments to invest in healthcare research as well, the pharmaceutical consultancy Astrix has found that the sector creates significant economic value and average wages are materially higher than in many industries. We give several concrete examples of how governments have increased funding and support for their medical industries below.

US

- President Biden’s budget for the 2023 financial year included a sum of US$62.5bn to be allocated to the National Institutes for Health, the primary federal agency in the US responsible for conducting and supporting medical research

- There are numerous federal, state and city programmes, that support the sector over and above high-profile private sector organisations such as the Bill & Melinda Gates Foundation, the Chan-Zuckerberg Initiative, and the Salk Institute.

Europe

- The European Investment Bank has provided a total financing of close to €35bn for healthcare-related projects worldwide and has noted that European healthcare expenditure was more than 8% of its GDP in 2019 and by 2020.

UK

- In December 2017 the UK government committed £500m for the sector in its “Life Sciences Sector Deal”. In July 2021, it published the “UK Life Sciences Vision” strategy and announced the launch of a “Life Sciences Investment Programme”, increasing the funding available to £1bn.

India

- India has the largest public health insurance scheme in the world, providing 500m people with free healthcare. In its 2021 budget, the Indian government increased spending on healthcare and well-being by 137% from the previous year’s allocation, which, according to Deloitte, represents 1.8% of its GDP.

China

- China’s government health expenditure has more than tripled since health reforms began in 2009, increasing from CNY482bn in 2009 to CNY1,640bn in 2018.

- In October 2016, President Xi Jinping announced the Healthy China blueprint, a declaration that made public health a precondition for all future economic and social development. It aims to expand the size of the health service industry to CNY16tn by 2030.

Australia

- In 2015, the Australian government set up its Medical Research Future Fund (MRFF). In 2019, it published its first 10-year investment plan which committed to spending AUD5.1bn on 20 initiatives between 2019 and 2029. By July 2020, the MRFF had grown to approximately AUD20bn.

The points that have been outlined above might suggest that that even if CLSC avoids investing in the US on valuation concerns, there are still plenty of remaining opportunities on which CLSC could capitalise, as multiple billions of dollars are being readied by other governments for investments into new medical technologies over the coming years.

Market dynamics

There is a myriad of stock-level opportunities within the sector, which reflect the idiosyncrasies of life science companies

The opportunity set presented to CLSC is not simply the result of broader macro-level trends within the global economy. There is also a myriad of stock-level opportunities within the sector, which reflect the idiosyncrasies of life science companies, be it the varying growth rates of subsectors, how certain services mesh with ESG considerations, or their overall balance sheet strength.

Whilst the aggregate pharmaceutical industry was valued at US$5.5tn at the end of 2021, with their revenues expected to achieve compounding annual growth rate (CAGR) of 12.7% over the next five years, the investment managers believe that even greater growth opportunities are available within the specific sub-sectors on which they intend to focus CLSC’s portfolio, with key high technology sub-sectors such as cell and gene therapy and gene editing, and robust growth in a broad range of disease treatments including, but not limited to, cancer, diabetes and many autoimmune diseases and mental health conditions.

The investment managers believe that key areas of scientific innovation and value-creation include gene and cell therapy and immunotherapy, gene editing/CRISPR, tissue engineering and 3D printing; precision and personalised medicine; synthetic biology; liquid biopsy; surgical robotics; artificial intelligence as applied to drug design; microbiome therapeutics; and novel anti-infectives. There is also significant structural growth in a number of pharmaceutical services businesses, driven by an increasing trend for large pharmaceutical and biotechnology companies to outsource non-core activities, including to contract research organisations (CROs) and contract development manufacturing organisations (CDMOs). It has been estimated that the global CRO services market will grow from approximately US$73bn in 2022 to approximately US$163bn by 2029, a CAGR of 12.1% Similarly, it has been estimated by the consultancy firm Fortune Business Insights that the global CDMO market will grow to nearly US$280bn by 2026, a 10% CAGR annually.

Fundamental strength

The directors believe the long-run double-digit growth rates the biotechnology sector has already demonstrated can continue.

While much of this discussion has been around the sector-specific issues of medical and life sciences investing, CLSC’s target companies will also need to face the same scrutiny as any other listed company, regardless of their sector or region. The investment management team feels that it is able to point out a number of positive attributes in that regard.

The team believes that the wider healthcare sector can demonstrate extremely strong balance sheets. For example, Ernst & Young says that the combined global biopharmaceutical and medical technology “firepower” (being the ability of companies to implement merger and acquisition transactions based on the strength of their balance sheets) was US$1.466trn.

The directors comment that in general, biotechnology companies which deliver commercially typically enjoy strong cash generation, high margins, high barriers to entry and long product cycles as a result of their long-duration intellectual property (usually by way of patent protection); all of which are characteristics of a ‘high-quality’ company, irrespective of the industry.

Whilst CLSC’s target annualised return of 20% per annum is not guaranteed, the directors believe the long-run double-digit growth rates the biotechnology sector already demonstrated can continue in the future given the structural drivers already mentioned.

ESG

The life sciences and medical technology sector may be well placed to benefit from this increased allocation to ESG compliant investing.

By investing exclusively into the life sciences and medical technology, there is potential for CLSC to capitalise on the wider momentum behind environmental, social, and governance (ESG) investing (a style which is very much in vogue). In the last three years, ESG funds worldwide attracted US$285bn, US$542bn and US$649bn of investment capital, respectively, as reported by Reuters, which represents nearly half of all new investment flows for the last two years in Europe. Even in 2022’s difficult markets, ESG funds attracted net inflows of US$120bn in the first half of the year, according to Morningstar.

The life sciences and medical technology sector may be well-placed to benefit from this increased allocation, as according to reputation data and insights firm RepTrack the life sciences and medical technology sector is also often ranked as the top-rated sector for ESG investing. The recent trend in ESG investing is arguably becoming a long-term sectoral growth driver, as younger investors seem more likely to prioritise ESG investing. According to the charitable donation manager Fidelity Charitable 77% of wealthy millennials have made an “impact” (ESG) investment in 2019.

Valuation opportunities

The investment management team believe that there are numerous life sciences and medical technology businesses which are undervalued.

The sectoral growth opportunities presented earlier in the note are not the only way in which CLSC can generate value for shareholders. The investment management team believe that there are numerous life sciences and medical technology businesses which are undervalued, particularly in the United Kingdom, Europe and Australia, which explains CLSC’s low allocation to the United States. It is through the narrowing of this valuation gap that CLSC can add additional value to shareholders beyond that presented by the natural growth in the life sciences sector.

One reason why life sciences companies can be undervalued is due to their maturity and complexity, whereby earlier-stage, innovative life sciences companies are usually smaller companies. These are factors that lead them to be viewed as too ‘specialist’ for many investors, given the complexity of their products as well as the inherently-riskier nature of younger, smaller companies. These risks are also compounded by their lack of profitability, which adds further complexity as it can make it difficult to value such companies using conventional cash-flow-based valuation techniques. This complexity and risk means that investors will simply avoid certain types of life sciences companies in their entirety, which can lead them to trading at a lower valuation compared to other sectors.

The investment manager believes that non-US small cap companies often fly under the radar of the typical investor, leading to them trading at discounted valuations.

Some two-thirds of CLSC’s portfolio is expected to be invested in companies with a market cap under US$500m. The relative illiquidity of such smaller companies may preclude them from being deemed as suitable investments for larger investors. In the investment manager’s experience, institutional investors looking to invest in specialist sectors like life sciences are typically required to deploy large amounts of capital, making it difficult to give serious consideration to smaller companies. This issue is compounded by most specialist investors being based in the US and prioritising domestic life sciences companies over foreign ones. Evaluating foreign companies may require additional analyst resources that simply are not available to them. The investment manager believes that non-US small cap companies often fly under the radar of the typical investor, leading to them trading at discounted valuations.

In the investment manager’s opinion, however, those companies which can navigate the aforementioned structural challenges, survive and fund themselves long enough to demonstrate they have valuable intellectual property, can be some of the best-performing companies in their respective stock markets in the fullness of time. Crucially, the investment manager believes that there are considerably more companies close to this inflection point than was the case in the past.

Such a trajectory can be the result of an announcement of material positive news, such as a successful clinical trial, an approval for a medical device or a licensing or other commercial deal, all of which would serve to increase a company’s profile amongst new investors. This increased attention can have a snowball effect, one example being how an upward trajectory can be compounded further by indexation, should a UK company enter the FTSE250 or an Australian company the ASX300, for instance, as index-tracking investors can be forced to purchase said stock. The investment managers have also observed that this behaviour results in large specialist investors investing in companies only once they have reached critical mass rather than any earlier and, ultimately, paying a materially higher price for reasons which have little to do with the underlying commercial trajectory of a given business.

Narrowing the valuation gap

The investment managers foresee a number of clear factors which can directly lead to an unwinding of an undervaluation.

Identifying undervalued companies is a largely futile prospect if there are no factors which can lead to an unwinding of the valuation gap. Thankfully, the investment managers foresee a number of clear factors which can directly lead to an unwinding of said undervaluation, potentially creating significant value for CLSC’s shareholders. In additional to the natural tailwinds which come from the structural growth trends outlined earlier in this note (which can lead to inherently stronger demand for life sciences companies), the investment managers believe that the greatest will be: one, a tangible commercial delivery from the companies themselves; and two, increasing interest in the sector as an understanding of the pace of scientific progress becomes more widespread. The investment manager believes that many smaller life sciences companies are on the cusp of delivering key clinical inflection points but that this potential is not yet reflected in valuations.

The investment managers also believe that there is an inherent momentum behind the unwinding of the sector’s wider undervaluation. Once companies do achieve success, such as announcing a successful clinical trial, then it will attract additional press interest around life sciences. This attention will naturally increase awareness of the potential benefits of investing in the sector as well as increasing awareness of other companies yet to achieve such successes, raising their profile over time and thus starting to remove many of the causes (outlined above) of the existing structural undervaluation in the sector. In the manager’s view, such awareness also increases the likelihood of the company becoming the target of an acquisition by the larger pharmaceutical companies looking to bolster their therapeutic programmes or medical technology divisions, paying a premium for these companies and thus unwinding any remaining undervaluation. The investment managers do note that, like the typical specialist investor, these large firms will often overlook successful life science companies when they are at their smaller, more undervalued stage.

Stock selection

Buy rationale

CLSC will look for the following characteristics when selecting a potential investment:

- Addressing a very sizeable market.

- Scope to be first in class, best in class or garner significant market share as a result of another structural reason (lower cost of goods, excellent sales and marketing partner).

- Evidence that the current valuation does not reflect this potential.

- Validation, which may include some or all of:

- an existing on-market product which can fund earlier stage pipeline;

- strong data and intellectual property;

- a high-quality scientific advisory board and/or the involvement of key opinion leaders.

- partnerships with large and well-established pharmaceutical companies; or

- pre-existing investment from leading specialist healthcare investors.

- Sufficient financial resources (or access thereto) to achieve clinical and/or commercial inflection points.

- Strong and demonstrably ethical management, board and other stakeholders, ideally with equity ownership and a track record of creating value.

- Credible commercial plan and route to market.

- ESG: focus on patient outcomes and stripping cost out of healthcare systems.

The investment manager will seek to construct a portfolio of investments such that there will be a number of clinical and commercial inflection points within the portfolio as a whole throughout each quarter.

Particular focus will be given to the balance sheet strength of portfolio businesses.

CLSC does not expect to have a controlling or majority position in any holding but given the sector knowledge and advisory experience of the board and the investment manager, CLSC expects to have value-adding engagement with a number of its portfolio holdings on a case-by-case basis.

Portfolio businesses may be private or already publicly traded, primarily on AIM, the London Stock Exchange and the ASX, with 20% of the portfolio expected to be invested in private companies. Given the nature of the holdings, the company will adopt a long-term, buy and hold approach with limited portfolio turnover. The directors expect value to be created via positive clinical trial results, regulatory approval, commercial deals, initial public offering, or trade sale.

Sell discipline

The aim of CLSC is to realise long-term value though exiting its investments over time. Accordingly, minimal portfolio turnover is expected but a partial or full exit will be considered in each of the following scenarios:

- The portfolio business has achieved its key clinical or commercial goal or failed at a key inflection point.

- The portfolio business has transitioned from primarily a research and development-driven business to a cash-generative business.

- An initial public offering of the portfolio business has been achieved (for private holdings).

- The portfolio business has relisted on another exchange: e.g., on NASDAQ, the Hong Kong Stock Exchange or the Singapore Exchange.

- A value objective of the portfolio business has been achieved.

Example portfolio

At an underlying investment level, CLSC will be largely diversified across various different characteristics.

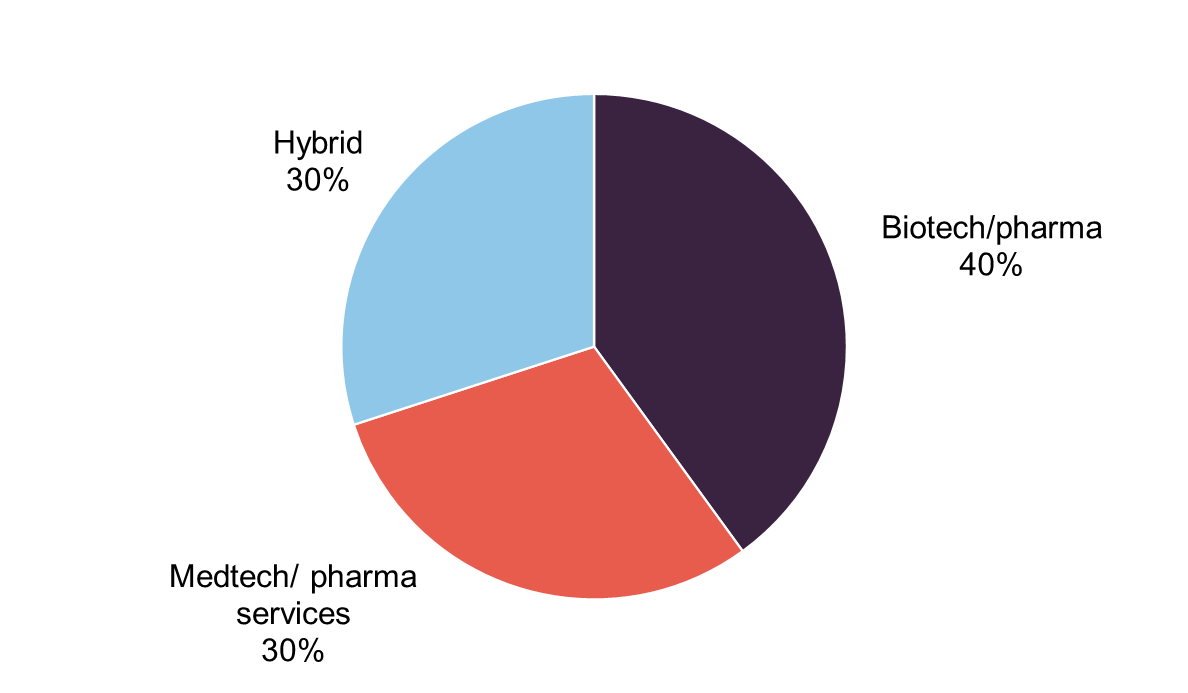

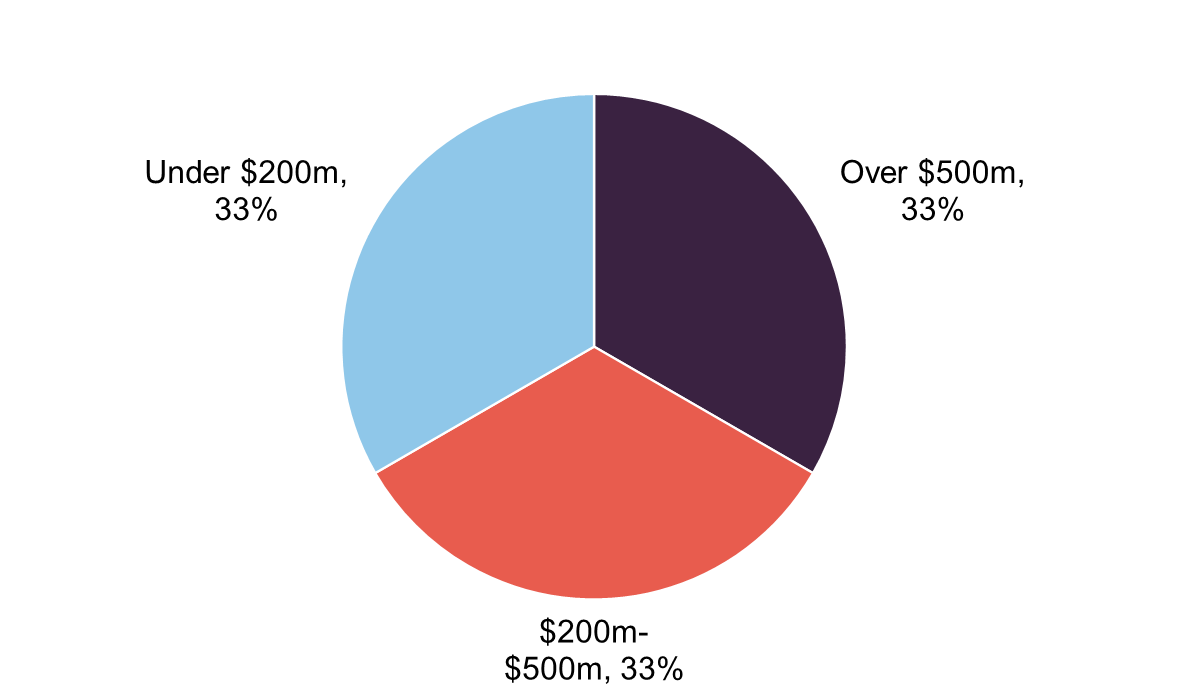

The investment management team have provided an example of what a portfolio could look like for CLSC. It is their intention to allocate CLSC’s portfolio across 30-40 companies, with the majority of the portfolio allocated to the top 10 positions. At an underlying investment level, CLSC will be largely diversified across various different characteristics, as can be seen by the charts below, albeit with a substantial 65% allocation to companies based in the UK or Europe, 25% in Australia, and the remaining 10% being held in cash. Whilst CLSC is diversified across the types of company it holds, its overall portfolio may be considered to be biased to small and medium-sized companies, when compared to the median market cap of broader global equities. The investment management team believe that such a portfolio implies a highly asymmetric risk/reward profile, skewed in favour of CLSC. Of the 90% invested in companies in Figure 2, the investment managers expect 70% to be held in quoted equities and 20% to be held in private companies.

Figure 2: Type of company

Source: Plain English Finance. Split of invested NAV

Figure 3: Target market capitalisation

Source: Plain English Finance. Split of invested NAV

Premium/discount control

Following initial admission, the company has shareholder authority to issue up to 250m ordinary shares less the number of ordinary shares to be issued under the initial issue, on a non-pre-emptive basis.

No ordinary shares will be issued at a price less than the last published NAV unless they are first offered pro rata to existing shareholders.

CLSC will start life with authorisation to repurchase up to 14.99% of the aggregate number of issued ordinary shares immediately following initial admission. The board will seek shareholder approval to renew its authority to make market purchases of CLSC’s ordinary shares at each annual general meeting.

The board will aim, through effecting buybacks of ordinary shares if necessary, to ensure that the ordinary shares do not trade, over the longer term, at a significant discount to NAV, in normal market conditions.

Dividend

Given the capital return nature of the CLSC’s investment objective, it does not have a dividend target and the board does not anticipate providing shareholders with a particular level of distribution.

Fees and expenses

The fees charged by CLSC will include both a management fee (outlined below) as well as all other expenses, such as custodian costs, director fees, and administration fees.

Management fee

Under the investment management agreement, the investment manager is entitled to a management fee of 1% of NAV per annum, payable monthly in arrears.

The investment manager is also entitled to a performance fee equal to 10% of the amount by which the adjusted NAV per share exceeds the performance hurdle (being the higher of the gross proceeds of the initial issue; and the adjusted NAV per share on the last business day in the previous performance period in respect of which a performance fee has been paid, in each case compounded by 10% per annum) and provided that the high watermark (being the higher of the gross proceeds of the initial issue; and the adjusted NAV per ordinary share at the end of the last performance period in relation to which a performance fee was earned) has been exceeded.

Private investments

CLSC is expected to invest approximately 70% of its capital in publicly traded companies and 20% in private businesses.

CLSC is expected to invest approximately 70% of its capital in publicly traded companies and 20% in private businesses, retaining approximately 10% of its capital as cash for follow-on investments. There will be no additional investments made in private companies if the total exposure of CLSC exceeds 40% of gross assets, measured at time of investment.

Private investments will be valued using recognised valuation methodologies in accordance with the International Private Equity and Venture Capital Association valuation guidelines (IPEVCA Guidelines) or any other guidelines the investment manager and the board consider appropriate. These methods will include primary valuation techniques, such as revenue or earnings multiples, discounted cash flow analysis or recent comparable transactions, in accordance with the IPEVCA Guidelines.

Hedging

CLSC is expected to hold companies across multiple different currency regions, not only sterling. The board does not intend normally to employ currency hedging in relation to either the company’s portfolio or cash flows. The company may, however, use hedging for specific short-term risk management purposes if and when the board deems this appropriate. Derivatives, such as swaps, may be used for currency hedging in such circumstances.

Capital structure

On admission, CLSC will have ordinary shares in issue and no other classes of share capital.

Continuation resolution

CLSC has an unlimited life. However, at the annual general meeting in 2028, the directors shall propose an ordinary resolution that the company continues its business. Assuming that is passed, the directors shall propose an ordinary resolution that the company continues its business as then constituted at each fifth annual general meeting of the Company thereafter.

If any continuation vote is not passed, the directors shall put forward proposals for the voluntary liquidation, unitisation, reorganisation or reconstruction of the company to members for their approval at a general meeting of the company to be convened by the directors for a date not more than six months after the date on which the continuation vote was not passed.

Gearing

CLSC does not intend to use structural gearing to enhance returns on investment.

CLSC does not intend to use structural gearing to enhance returns on investment. It may, from time to time, use short-term borrowings to manage its working capital requirements, for efficient portfolio management purposes and for follow-on investments in portfolio businesses where CLSC does not have ready cash available to fund such follow-on investments in the short term. In any event, borrowings will not exceed 10% of the NAV, calculated at the time of drawdown.

Board

The directors are responsible for the determination of the company’s investment policy and have overall responsibility for the company’s activities, including the review of investment activity and performance and the control and supervision of the company’s service providers. All of the directors are non-executive and are independent of the investment manager. The directors will meet at least six times per annum.

Geoff Miller, non-executive chair

Geoff has over 20 years’ experience of working in financial services, both as an equity analyst covering investment banks, asset managers and investment companies and as a senior fund manager. He was formerly the non-executive chairman of Globalworth Group, a quoted international property business with a market capitalisation of approximately €1bn. Geoff is currently chairman of AIM-listed MJ Hudson, a director of several private companies, and a principal in a venture capital business based in Guernsey, focused on financial and technology sectors.

Grant Cameron, non-executive director

Grant has been a director of Ninety One Asset Management Guernsey Limited (Ninety One), previously Investec Asset Management, since 1997. Prior to joining Investec in South Africa, he trained as an accountant at KPMG. Grant is a director of a number of investment funds and was previously chairman of the Guernsey Investment Funds Association. During his tenure, Ninety One grew roughly 50-fold in assets under management, including the successful merger with Guinness Flight Asset Management in Guernsey.

Dr. Victoria Gordon, non-executive director

Victoria is managing director and chief executive officer of QBiotics Group. Her additional board experience includes serving as a non-executive director of Biopharmaceuticals Australia, and a non-executive director and non-executive chairman of the Australian Rainforest Foundation. She has served two consecutive terms on the Queensland Government Biotechnology Advisory Council, Federal Government Expert Forum on Biomedicine, Federal Government Expert Forum on Environmental Biotechnology, and the Queensland Government Science Education Taskforce. Victoria holds a PhD in Microbiology, Bachelor of Applied Science in Chemistry and Biology (Honours), and Diplomas in Human and Animal Health.

John Whittle, non-executive director

John is a Fellow of the Institute of Chartered Accountants and holds the Institute of Directors’ Diploma in Company Direction. He was formerly chief financial officer of Vodafone Retail and has been an independent non-executive director since 2009. He is currently a non-executive director of £3bn market cap FTSE 250 constituent The Renewables Infrastructure Group Plc, non-executive chairman of Starwood European Real Estate Finance Ltd, non-executive director of Sancus Lending Group Ltd and audit committee chair of Chenavari Toro Income Fund Limited. Prior to these roles, John was senior independent director and audit committee chair at FTSE 250 company International Public Partnerships Ltd and audit committee chair of Globalworth Real Estate Investments Limited.

Important Information

NB: Marten & Co has been paid to prepare this note on behalf of Conviction Life Sciences Company. This is a marketing communication and not a prospectus.

The note is based upon publicly available information and information provided to us by Conviction Life Sciences Company and should be read in conjunction with the Conviction Life Sciences Company Prospectus published on 16 November 2022 and which can be found at clsc.uk.

Readers should not place any reliance on the information contained within this note.

The note does not form part of any offer and is not intended to encourage the reader to subscribe for ordinary shares in Conviction Life Sciences Company or deal in any other security or securities mentioned within the note.

Marten & Co does not seek to and is not permitted to provide investment advice to individual investors.

The note is not intended to be read and should not be redistributed in whole or in part in the United States of America, its territories and possessions; Canada; Australia; the Republic of South Africa; or Japan.

Legal

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Conviction Life Sciences Company Limited.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it and readers should place no reliance on the information contained therein.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

This note has been compiled from publicly available information and should be read in conjunction with the Conviction Life Sciences Company Limited prospectus published on 16 November 2022.

This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

This is an advertisement and not a prospectus for the purposes of Regulation (EU) No. 2017/1129. Potential investors should not apply for or buy any shares in Conviction Life Sciences Company (the Company) except on the basis of information contained in the prospectus published by the Company in connection with the offer of shares in the Company.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.