Focused on the future

In our last note in January, we set out the reasons why we felt that Saba Capital’s proposals were not in Herald Investment Trust (HRI) shareholders’ interest and why shareholders should vote against them to protect their investment in the trust. Thankfully, the vast majority of HRI’s investors agreed, handing Saba a resounding defeat.

Whilst the continued presence of Saba on the shareholder register creates some uncertainty, HRI has continued to show the benefits of its closed-ended structure, taking a long-term view by investing in pioneering technology companies at an early stage. The portfolio has been profiting from its exposure to Artificial Intelligence (AI), but the managers believe this has a long way to run as the theme broadens and the tailwinds extend to innovative smaller businesses too.

HRI continues to increase its international exposure over the UK, with North America now being the largest geographical weighting. This reflects a more difficult home market, and a plethora of opportunities internationally.

Small-cap technology, telecommunications and multi-media

HRI’s objective is to achieve capital appreciation through investments in smaller quoted companies in the areas of telecommunications, multimedia and technology. Investments may be made across the world, although the portfolio has traditionally had a strong position in UK stocks.

| 12 months ended | Share price total return (%) | NAV total return (%) | Deutsche Numis ex IC plus AIM (%) | B’berg US 2000 Tech TR (%) |

|---|---|---|---|---|

| 31/10/21 | 36.0 | 39.0 | 43.5 | 50.0 |

| 31/10/22 | (26.6) | (24.3) | (24.9) | (19.5) |

| 31/10/23 | (6.4) | (6.8) | (5.9) | (9.0) |

| 31/10/24 | 28.9 | 21.7 | 20.0 | 23.1 |

| 31/10/25 | 20.4 | 21.0 | 11.0 | 19.5 |

Saba threat defeated; HRI looking to the future

In our last note, published in January, we detailed how Saba Capital, a US-based hedge fund, had built up a substantial stake in HRI, and requisitioned its board with proposals to remove all members of the board and dismiss the current investment manager, replacing them with Saba appointees in each case. We set out the reasons why we felt that Saba’s proposals were not in shareholders’ best interests and why we believed that shareholders should vote against the resolutions to protect their investment in the trust.

Saba’s proposals were resoundingly defeated by HRI’s shareholders

It was therefore very heartening to witness the resounding Saba defeat at the requisitioned general meeting held on 22 January 2025. HRI’s shareholders voted against the proposals by 65.1% to 34.9% on a turnout of 80.6%. Stripping out the Saba votes, just 0.15% of non-Saba shareholders voted in favour of its proposals. This victory was then followed up at the AGM in March, where 99.9% of non-Saba votes cast were in favour the continuation of the trust. Elsewhere in the investment trust sector, the shareholders of the six other trusts targeted in the same way also resoundingly rejected Saba’s resolutions.

Whilst the initial threat from Saba has passed, the hedge fund retains a large position. As at 3 November, it held 25.1% of the share capital and a further 5.6% of voting rights through other financial instruments. Although its overall voting rights are therefore over 30%, it is not obliged to make an offer for the company, as such a large holder would be ordinarily, as it breached the threshold passively, through HRI buying back its own shares.

Until recently, Saba has not given any indication of its future plans for its stake, and is not in active communication with HRI’s board or manager. However, it has recently been reported that Saba plans to launch an exchange-traded fund (ETF) that will target investment companies and trusts on wide share price discounts. It is possible that Saba’s HRI stake could be transferred to this new vehicle at some point, and we will continue to monitor the situation closely.

In the meantime, Katie Potts and the rest of the management team have continued to focus on managing HRI’s portfolio, which remains genuinely unique within the UK investment universe.

Market update

Trump’s Liberation Day tariff announcements led to market upheaval

Our last note was published five days before the inauguration of Donald Trump for his second term as US president. The months since have been dominated by his actions. Most significant was the fall-out from his “Liberation Day” tariff announcements in April, when Trump announced a baseline 10% tariff for all countries, and additional reciprocal levies, the levels of which were calculated based on bilateral deficits with the US.

Developments since April have been fractured and chaotic. A week after the initial announcement, dramatic fluctuations in equity, currency and bond markets prompted a 90-day pause from the White House on the additional tariffs above the base line 10% level.

Since then, the administration has focused on securing bilateral trade agreements. In May, the UK reached a deal with a baseline 10% rate, while the EU reached a framework deal in July with most EU goods facing 15% tariffs. In August, Trump announced a further 90-day pause on sweeping tariffs on China until 10 November as talks continue.

What happens from this point is unclear to everyone – probably including the US president himself. Nonetheless, markets have returned to a sanguine mood. The S&P 500 has more than erased its losses since April, trading at an all-time high. Similarly, the FTSE 100 is strongly up year-to-date and again at or near its record high.

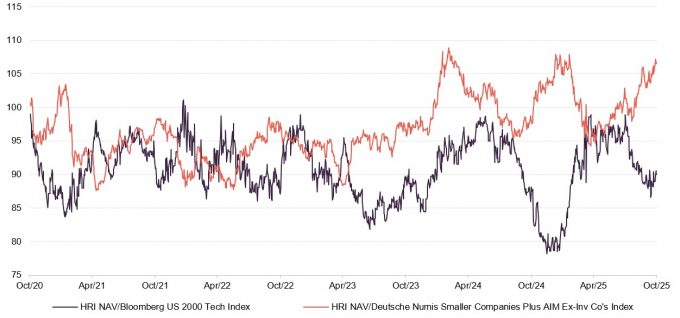

More relevant to HRI is the performance of smaller company indices. Figure 1 shows two of these: Bloomberg US 2000 Technology (small- and mid-cap US technology) and Deutsche Numis Smaller Companies Plus AIM Ex Inv Cos (bottom 10% of the UK market).

Figure 1: Markets year-to-date to 3 November 2025, indices rebased to 100

Source: Bloomberg, Marten & Co

Both indices have followed a similar course this year, that is itself not dissimilar to the large-cap indices. They fell in the early part of the year, particularly in the wake of “Liberation Day”, and have steadily recovered since. The fall in technology stocks was especially pronounced given the sector’s vulnerability to supply chain disruption, and sensitivity to souring market sentiment, particularly when focused on more “growth”-focused stocks. As this has improved since April, the recovery in the Bloomberg US 2000 Technology index has been particularly pronounced.

A mixed inflation and interest rate picture

Away from tariffs, investors have continued to focus on the future direction of inflation and interest rates.

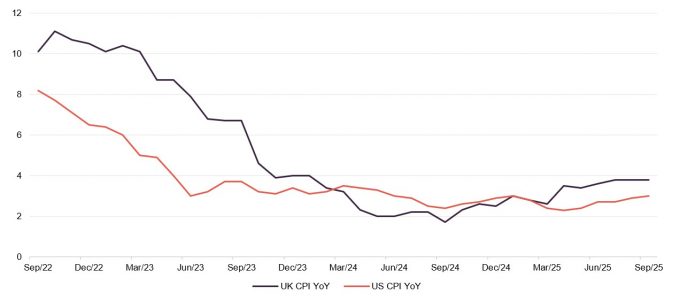

Figure 2: Inflation over three years to 30 September 2025

Source: Bloomberg, Marten & Co

As shown in Figure 2, inflation has clearly fallen significantly in both the US and UK in recent years, as it has across the developed world, and this has allowed central banks to cut interest rates. However, price rises have remained stubbornly higher than in the pre-2022 period, and are above the 2% target in both the US and UK.

In the UK in particular, CPI has risen uncomfortably in recent months, to near 4%. The Bank of England is therefore having to tread cautiously on further rate cuts, despite weak growth, keeping its base rate at 4% at its November meeting. The Federal Reserve cut its main rate by 0.25% at its most recent meeting. This was only the second cut of 2025, and the recent pace of cuts has disappointed investors – and President Trump.

Sticky inflation therefore remains a risk to elevated stock markets. This is particularly relevant for smaller companies and the technology sector, both of which impact HRI. In each case, shares are valued largely on future earnings and growth expectations, which are discounted by the current interest rate. Therefore, elevated rates could act as a break on further gains, particularly if future cuts take longer to materialise than investors hope, or if higher rates are instead needed to subdue a sustained inflationary spike.

Technology sector – large cap stocks driven by momentum, and AI

For now, investors remain firmly positive on the technology sector, in large part because of the ongoing artificial intelligence (AI) megatrend. AI is fuelling momentum, which was only briefly interrupted by the uncertainty caused by “Liberation Day” tariffs, although this has clearly been focused on the larger end of the market. We are seeing resilient demand for cloud, semiconductor and software solutions in particular, and a substantial increase in the number of sectors and services being dramatically impacted.

HRI – capitalising on themes within technology

HRI has proven itself adept over many years at capitalising on specific themes within the technology sector; in the past this has included the likes of “software as a service” (SaaS). The current portfolio, and recent trading activity, exhibit exposure to a number of themes that are relevant in the market now.

AI – not just a mega-cap story

The AI theme is benefitting smaller companies, which are often on lower valuations

Across the whole technology sector, the most important theme at present is AI. While the majority of capital continues to flow into the largest American businesses – most obviously the “Magnificent Seven” of Alphabet, Meta, Microsoft, Tesla, NVIDIA, Apple, and Amazon – there is a clear spill over into smaller companies. In some cases, this reflects investor sentiment, but in others it is due to a company’s specific role in the AI revolution. At the same time, while in many cases large-cap valuations remain stretched, there are in many cases more attractive opportunities at the smaller end of the market.

Within HRI, AI has been a major factor behind a significant concentration of returns in recent years. Over the period from 1 January 2020 to 30 June 2025, HRI made total gains of £497m, but 45% of this came from just four stocks (particularly striking in a portfolio of over 300 companies): Super Micro Computer, BE Semiconductor Industries, Fabrinet and Celestica. All four are enablers of AI infrastructure.

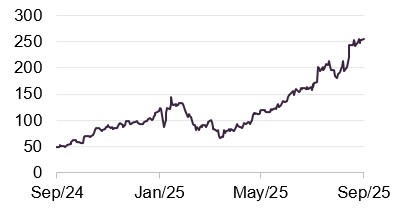

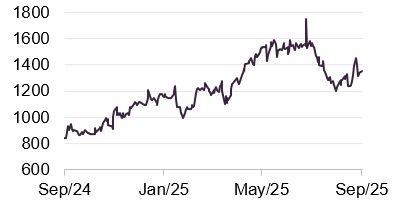

This concentration of returns has been particularly exemplified by the extraordinary performance of Celestica, HRI’s largest holding.

Celestica Inc

Figure 3: Celestica Inc (USD)

Source: Bloomberg

Celestica (www.celestica.com) is a Canadian-American technology manufacturer specialising in hardware platforms and supply-chain services. We looked at the company in some detail in our last note, but it is worth covering again here, given the extent of its share price rally over the past year, as shown in Figure 3.

Celestica has been a big beneficiary of AI infrastructure tailwinds, and in the eyes of investors it has morphed from a modest electronics and machinery company into a gateway to the AI and hyperscaler supply chain.

As such, a key driver of the rally is Celestica’s deepening involvement in AI networking and cloud infrastructure through its Connectivity & Cloud Solutions (CCS) business, as well as computer hardware. Its particular strengths are partnerships with hyperscalers and its design-manufacturing capabilities for server infrastructure. In its recent quarterly update, the company reported 21% year-on-year revenue growth and also raised guidance, with much of the upside attributed to strong demand within its CCS business.

Investing across the phases of AI adoption

Since the emergence of AI as an investable theme, most of the focus has been on infrastructure and the supply chain, in particular large language models (LLMs), graphics processing units (GPUs), accelerators and networking. HRI’s portfolio has exposure to this theme through holdings such as Celestica, Fabrinet and Super Micro Computer.

However, HRI’s managers believe that the AI theme is moving beyond this infrastructure layer to a data and application layer, and the beneficiaries and adaptors are starting to broaden out. Specifically, we are in the midst of a new wave of customer-facing, revenue-generating products emerging. Implementation costs are falling, and most value is accruing to those companies that hold data. There are a number of companies in HRI’s portfolio involved in this next iteration of AI, including Five9 and Sidetrade.

Five9

Figure 4: Five9 (USD)

Source: Bloomberg

Five9 (www.five9.com) is a leading US provider of cloud-based “contact-centre-as-a-service” software. Its platform allows companies to manage customer interactions across voice, chat, email, SMS, and social channels, while embedding analytics and AI to improve efficiency and service quality. Five9 benefits from the ongoing shift away from legacy on-site systems towards AI-powered systems in the cloud.

Five9’s shares have fallen steeply in recent years. However, at the end of 2024 they benefitted from a rapid re-rating, which was driven by excitement around its platform, strong double-digit revenue growth and activist pressure for margin expansion and strategic action. However, this was followed by an equally sharp correction beginning in February. As well as sentiment towards the wider sector deteriorating, there were specific concerns about profitability and free-cash-flow sustainability after Five9 repaid large convertible notes, reducing its cash buffer. A second-quarter 2025 earnings miss, management changes and ongoing activist scrutiny added to the uncertainty.

Nonetheless, for the last full year, the company delivered record revenue of just over $1bn, up around 14% from the prior year, and management has guided to further growth in 2025, helped by further strong uptake of AI-driven features. For HRI, Five9 offers exposure to a global leader in cloud communications and next-generation customer-experience technology with a recurring-revenue model.

Sidetrade

Figure 5: Sidetrade (EUR)

Source: Bloomberg

Sidetrade (www.sidetrade.com) is a French software company specialising in AI-powered “order-to-cash” solutions that help its customers optimise their cash collection and working capital. Its cloud platform uses predictive analytics and machine learning to forecast customer payment behaviour, automate processes and improve cash-flow visibility.

The company serves a broad client base spanning manufacturing, technology, media, and professional services, benefiting from the long-term trend for digital transformation of cash management.

Sidetrade has consistently delivered double-digit revenue growth, driven by expanding subscription income and international sales, particularly in North America and the UK, which generate the majority of new business. The company’s margins and recurring revenues would appear to support a robust balance sheet and cash generation. Sidetrade therefore offers exposure to a niche global leader in AI-driven financial software with high customer retention and a subscription-based business model.

Exposure to companies benefiting from increased defence spending

Despite the intense investor focus on AI, it is important to remember that there are still a number of non-AI growth drivers available within the technology sector. For HRI, these include robotics and machine vision through the likes of Ouster and Advantech, and space technology through Spire Global, Filtronic, and Lumibird.

Of particular significance, given widespread geopolitical instability – with a mercurial president in the White House, European rearmament and ongoing wars in the Middle East, eastern Europe and elsewhere – is defence. The war in Ukraine has shown the importance of drones and autonomous systems in war and, together with laser technology, these offer distinct opportunities for small, nimble defence suppliers. Two companies that exemplify this, and have performed very strongly over the past year, are Cohort in the UK and Leonardo DRS in the US.

Cohort

Figure 6: Cohort (GBP)

Source: Bloomberg

Cohort (www.cohortplc.com) is a UK-based defence technology group that provides specialist products and services across electronic warfare, surveillance, communications, and training systems. Operating through six subsidiaries, the group supplies advanced solutions to the UK Ministry of Defence and a range of international customers. Its expertise spans areas such as counter-drone technology, autonomous maritime systems, and secure communications. It is therefore benefitting from rising demand for sophisticated defence capabilities and networked warfare.

The company has delivered robust growth in recent years, supported by a healthy order book and increased overseas revenues. Contract wins in naval electronic warfare and surveillance, together with long-term service agreements, underpin strong revenue visibility. In addition, Cohort’s diversified portfolio and focus on high-value, niche segments of the defence market allow it to compete effectively against larger companies while maintaining attractive margins.

HRI’s managers believe Cohort should be well positioned to benefit as UK and allied governments reprioritise defence modernisation and resilience. This trend clearly has a long way to go, with NATO countries recently committing to eventually spend 3.5% of their GDP on defence, well in excess of the current level in most cases.

Leonardo DRS

Figure 7: Leonardo DRS (USD)

Source: Bloomberg

Leonardo DRS (www.leonardodrs.com) is a US defence technology company specialising in advanced sensors, network computing, force-protection systems and integrated mission solutions for the US military and allied forces. This puts it in a strong position within high-growth sectors like autonomous operations and next-generation communications.

The company operates as a majority-owned subsidiary of Leonardo S.p.A., the Italian aerospace and defence group. Leonardo S.p.A. retains around 73% of the US business and provides strategic oversight and technological collaboration, while DRS remains listed independently on NASDAQ. This structure allows Leonardo DRS to access US defence contracts and maintain security clearances as an American entity, yet also draw on its parent’s global R&D capabilities and international customer base.

Leonardo DRS has recently reported steady growth, supported by a robust order backlog and exposure to key US defence priorities such as electronic warfare and power systems for naval platforms. Recent awards for next-generation sensor and computing programmes show its competitive edge in supplying mission-critical technologies.

Asset allocation

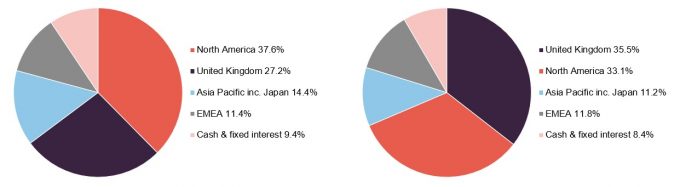

HRI’s portfolio now has a higher allocation to the US than the UK, a big change from previous years

In our recent notes, we have regularly discussed the decline in HRI’s allocation to the UK, and the parallel increase in the North American allocation. As shown in Figures 8 and 9, this trend has continued over the past six months, and indeed North American exposure is now higher than the UK. This is significant, considering that less than four years ago HRI had double the allocation to the UK compared to North America (47.7% and 22.3%, respectively, in December 2021).

This trend continues to reflect both the relative performance of the regions, with US technology companies outperforming their international rivals, and the number of respective opportunities available. The broader UK market appears to be in long-term decline, with an inexorable shift of investor assets overseas, and companies seeing less attraction in being listed in London. This has become a self-perpetuating problem.

Specifically, within the technology sector the US has benefitted from being at the vanguard of the AI megatrend. Although this has predominantly benefitted the largest companies so far, most notably the “Magnificent Seven”, it has also filtered through to the smaller end of the market. As covered elsewhere in this note, many of the best-performing holdings within HRI have been significantly boosted by AI.

Katie says she has currently got slightly more exposure to the US than she would like. However, the managers of HRI also make the point that their North American exposure covers more than just the US, with a number of important Canadian holdings – not least Celestica, the largest holding in the fund (listed in New York but headquartered in Toronto). The allocation also covers Israeli companies that are listed in the US, for example Freightos and JFrog.

Only around half of the reduced allocation to the UK since November has gone into North America, with the remainder reinvested into Asia Pacific. The EMEA (Europe, the Middle East, and Africa) allocation remains largely unchanged from our last note.

Around 30% of HRI’s European portfolio by value has left the portfolio in the past year due to private equity takeovers, which has been a headwind to increasing exposure. Although these were generally at premiums of 30-50%, this is no more than the team considered fair, given these companies’ prospects. Comfortably the biggest of the takeovers was of Esker, which was sold for €1.62bn to Bridgepoint (HRI received cash proceeds of £22m) in partnership with General Atlantic and Esker’s management. Much of the proceeds of these recent sales has been used to fund repurchases of HRI’s own shares (see page 15). The managers would ideally like to have a higher allocation to both Europe and Asia.

Despite the understandable focus on geographical allocation, Katie and the team are keen to emphasise that for the majority of their holdings, revenues are global, rather than being focused on the country in which they are listed. The managers generally prefer global companies because by their very nature they tend to be more competitive.

Despite maintaining a broadly flat overall cash allocation, the HRI team has continued to be proactive in managing liquidity.

Figure 8: Geographic allocation as at 30 September 2025*

Figure 9: Geographic allocation as at 30 November 2024*

Source: Herald Investment Management *Note: as a proportion of gross assets

Source: Herald Investment Management *Note: as a proportion of gross assets

Top 10 holdings

Figure 10 shows HRI’s top 10 holdings as at 30 September 2025 and how these have changed since our last note (which used data as at 30 November 2024).

Celestica remains the largest holding, and the top six holdings are broadly unchanged. The exception is Trustpilot, which has fallen to position eight following a torrid period for its shares. Further down the list, there are three different names in the top 10: Silicon Motion Technology, Nordic Semiconductor, and Volex. Silicon Motion Technology was looked at in some detail in our note in June 2024 (see here), and we cover Nordic Semiconductor and Volex below. We note that none of these companies are new holdings for HRI, as the team typically initiates with smaller position sizes, with these building over time as the thesis plays out.

Figure 10: Top 10 holdings as at 30 September 2025

| Holding | Sector | Country | Allocation 30/09/25 (%) | Allocation 30/11/24 (%) | Percentage point change |

|---|---|---|---|---|---|

| Celestica Inc | Tech hardware and semiconductors | US | 4.2 | 2.3 | 1.9 |

| Fabrinet | Tech hardware and semiconductors | US | 2.7 | 2.3 | 0.4 |

| BE Semiconductor Ind. | Tech hardware and semiconductors | Netherlands | 2.0 | 1.9 | 0.1 |

| Pegasystems Inc | Software & computer services | US | 1.9 | 1.7 | 0.6 |

| Silicon Motion Technology | Tech hardware and semiconductors | US | 1.9 | 1.2 | 0.7 |

| Diploma | Support services | UK | 1.8 | 2.0 | (0.2) |

| Super Micro Computer | Tech hardware & equipment | US | 1.8 | 1.6 | 0.2 |

| Trustpilot | Software & computer services | UK | 1.4 | 2.2 | (0.8) |

| Nordic Semiconductor | Tech hardware and semiconductors | Norway | 1.4 | 0.8 | 0.6 |

| Volex | Tech hardware & equipment | UK | 1.3 | 1.3 | – |

| Total of top 10 | 20.4 | 18.5 | 1.9 |

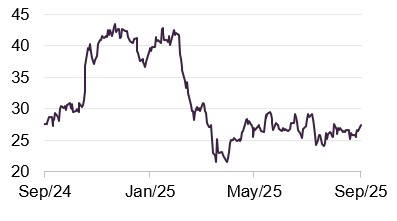

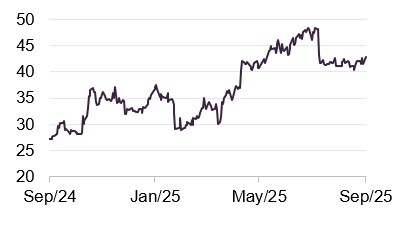

Nordic Semiconductor

Figure 11: Nordic Semiconductor (NOK)

Source: Bloomberg

Nordic Semiconductor (www.nordicsemi.com) is a Norwegian fabless semiconductor company headquartered in Trondheim. It specialises in ultra-low power wireless communication technologies, particularly for the Internet of Things (IoT) market. Its product range includes system-on-chips (SoCs), system-in-packages (SiPs) and connectivity solutions.

A key competitive strength for Nordic Semiconductor lies in its lead in short-range wireless technologies. Its Bluetooth LE solutions, in particular, have become widely adopted in consumer electronics, healthcare devices and smart home systems. Historically, the company’s nRF51 and nRF52 product series enabled it to capture large footprints in low-power wireless markets. More recent generations show Nordic’s strategy of broadening beyond short-range protocols into longer-range, more connected applications. The company recently acquired Memfault, a cloud service provider and former partner, to bolster its offerings in cloud-based device management.

Recent share price growth has been driven by strong financial results. In Q2 2025, the company reported revenue of $164m, up around 28% year-on-year, and core EBITDA of around $21m, beating analyst forecasts. There has been renewed demand in Nordic Semiconductor’s core markets, and product innovation and strategic moves such as expanding into new radio-standards and longer-range connectivity.

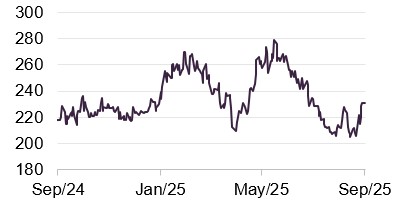

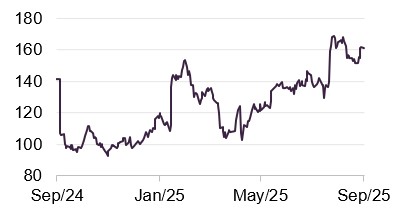

Volex

Figure 12: Volex (GBP)

Source: Bloomberg

Volex (www.volex.com) is a UK-headquartered integrated manufacturer specialising in power and data connectivity solutions for critical applications. It is structured around five main business divisions, and its operations include manufacturing ruggedised wiring harnesses, printed circuit board assemblies and other integrated systems for equipment and contract manufacturers.

As is illustrated in Figure 12, during the last year Volex has seen its share price drift down and then experience a sharp drop, followed by a strong recovery. The moves came in the midst of President Trump’s “Liberation Day” tariff announcements, which subsequently softened, and this wider context was clearly at least partly responsible for the share price moves.

However, there were also stock-specific reasons, as investors reacted to concerns and reassurances from Volex’s financial results and strategy. Initially, sentiment turned negative after its half-year results in November. Although these showed revenue up about 30% year-on-year, earnings per share rose only 2%, and net debt increased to $205m. Unsolicited takeover bids for TT Electronics, a designer and manufacturer of advanced electronic components, also sparked concerns about overpaying and further leveraging Volex’s balance sheet. These bids were ultimately unsuccessful.

In contrast, full-year results delivered in June reassured investors. Volex exceeded $1bn in revenue and achieved its first underlying operating profit above $100m, with operating margins of around 10%. This cemented a recovery in the share price.

Performance

As shown in Figures 13 and 14, HRI has outperformed the Deutsche Numis Smaller Companies plus AIM ex-Investment Companies Index (which captures the performance of the wider UK small-cap market) in NAV terms over five years. After struggling somewhat over much of 2023 and 2024, HRI posted very positive absolute numbers in 2024, and so far for 2025, and this has improved the longer-term relative NAV performance versus UK small caps. However, HRI’s particularly strong relative performance at the start of the COVID pandemic has now fallen out of the five-year numbers, depressing the picture somewhat compared to when we last reported.

HRI’s NAV performance as measured against the Bloomberg US 2000 Technology Index has been somewhat more challenged, although was in-line on a relative basis until a divergence over the past few weeks. Nonetheless, there have been periods of both marked outperformance and underperformance over the past five years. Overall underperformance relative to US small-cap technology stocks can in large part be attributed to the relative dominance of US tech companies over their international peers, both in terms of scale and performance. As detailed on pages 9-10, HRI continues to maintain a strong allocation to the UK market, but the fund’s US allocation has steadily increased.

Figure 13: HRI’s NAV total return relative to relevant indices, over five years to 31 October 2025

Source: Bloomberg, Marten & Co

Figure 14: Cumulative total return performance over periods ending 31 October 2025

| 1 month (%) | 3 months(%) | 6 months (%) | 1 year (%) | 3 years(%) | 5 years(%) | |

|---|---|---|---|---|---|---|

| HRI NAV | 4.2 | 7.7 | 28.2 | 21.0 | 37.3 | 44.4 |

| HRI share price | 1.6 | 1.8 | 25.2 | 20.4 | 45.3 | 45.0 |

| Deutsche Numis Smaller Cos plus AIM ex IC | 0.4 | 2.5 | 14.4 | 11.0 | 25.4 | 35.1 |

| Bloomberg US 2000 Technology | 5.0 | 17.9 | 39.2 | 19.5 | 33.8 | 61.5 |

Dividend

HRI is focused primarily on generating capital growth, and dividend income makes up only a small part of returns. The consequence of this is that HRI only declares a dividend where this is necessary to retain investment trust status, and in practice, no dividend has been declared since 2012.

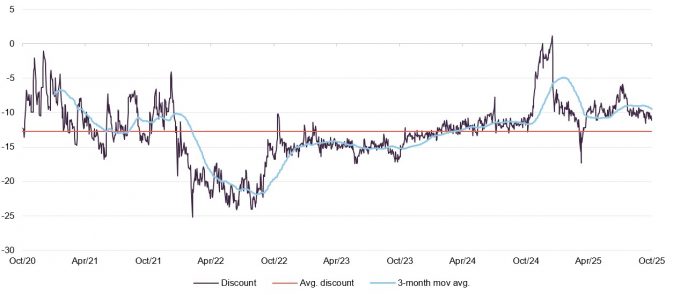

Premium/(discount)

HRI’s discount narrowed during the Saba episode. It has since settled at a lower level than its average.

Over the five years ended 31 December 2024, HRI traded on an average discount of 12.9%. However, over the last 12 months the trust has traded at a narrower average discount of 8.7%. The range was between a discount of 17.3% and a premium of 1.1%.

As shown in Figure 15, there was a significant narrowing of the discount towards the end of 2024, and the shares even briefly traded at a premium right at the end of the year and again at the beginning of 2025. A major contributing factor was the large-scale buying by Saba detailed earlier in the report, and the shares moved back to trading at a discount following Saba’s defeat. It is encouraging that the discount has settled at a somewhat lower level than its average, although we are cognisant of the risk posed by the continued holding of 30% of the share capital by Saba – specifically, the downward pressure that could be put on the share price and discount if Saba were to look to exit its position quickly.

As of 13 November 2025, HRI trades on a discount of 12.1%. The discount widened at the time of President Trump’s “Liberation Day”, but quickly narrowed once more. The slight widening in recent weeks is likely due to wider investor concerns about the UK market in advance of the Budget on November 26, where tax rises and other growth-stifling measures are widely expected.

Figure 15: HRI premium/(discount) over five years to 31 October 2025

Source: Bloomberg, Marten & Co

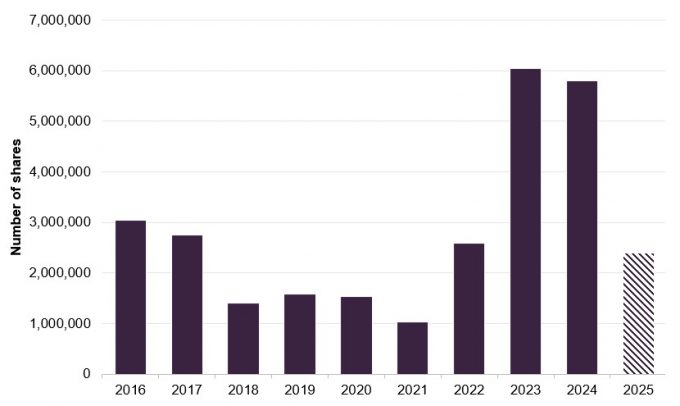

Whilst the board’s general policy is to not attempt to control the discount, given the limited liquidity available within the underlying portfolio companies, the trust will repurchase shares opportunistically.

As shown in Figure 16, 2023 and 2024 saw particularly high levels of repurchases. So far this year, buybacks have returned to a more normal level, at just under 2m shares repurchased year-to-date.

Figure 16: HRI share repurchases over the past 10 calendar years

Source: Herald Investment Trust

Fees and costs

Tiered management fee structure with no performance fee element

1% annual management fee up to assets of £1.25bn and 0.8% thereafter; no performance fee

HIML is entitled to an annual management fee of 1% of HRI’s net assets up to £1.25bn and 0.8% of HRI’s net assets above this level.

The NAV is calculated monthly using mid-market prices, which is somewhat unusual, as most NAVs are calculated at bid prices. However, given that many of HRI’s underlying holdings trade on wide spreads, the mid-market valuation gives a better indication of the true value of the portfolio. There is no performance fee. The management fee also covers the cost of company secretarial services. Since 1 October 2024, these have been provided by NSM Funds (UK) Limited, who took over from Law Debenture Corporate Services.

In the year to the end of December 2024, HRI’s ongoing charges ratio was 1.08%, very slightly higher than the 1.07% of the year before. The asset management contract is subject to 12 months’ notice.

Capital structure and life

Simple capital structure

HRI has one class of ordinary share in issue. It can gear up to 50% of net assets

HRI has a simple capital structure with one class of ordinary shares in issue. Its ordinary shares have a premium main market listing on the London Stock Exchange and, as at 13 November 2025, there were 47,858,467 in issue with no shares held in treasury.

The trust is permitted to borrow up to 50% of net assets; however, it currently has no form of credit. It previously had a £25m multi-currency revolving loan facility with RBS that matured on 31 December 2019 and was not replaced. As at 30 September 2025, HRI had net liquid assets of 9.4% of its total net assets, held in a combination of cash and government bonds.

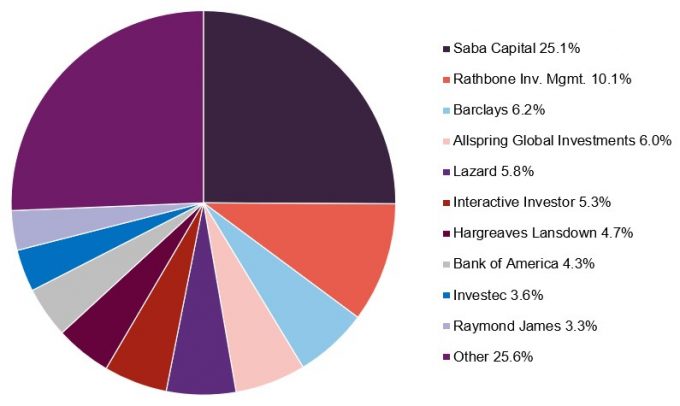

Major shareholders

Figure 17: Major shareholders as at 3 November 2025

Source: Bloomberg

Saba Capital remains comfortably the largest shareholder in HRI. In addition to its direct shareholding, it has further voting rights through other financial instruments. When last reported to the market on 8 July, these amounted to a further 5.6% of the total.

Barclays and Bank of America have both substantially increased their holdings in HRI in recent months, which may be related to Saba’s holdings through financial instruments.

Unlimited life with three-yearly continuation votes

HRI does not have a fixed life, but shareholders are offered a continuation vote every three years. The next continuation vote is scheduled for the trust’s AGM in March 2028.

Board

HRI’s board has five non-executive directors

HRI’s board is composed of five directors, all of whom are non-executive and considered to be independent of the investment manager. The current chairman, Andrew Joy, was appointed to the role in April 2023. He replaced Tom Black, who had indicated his intention to retire from HRI’s board at its AGM in April 2023.

James Will served as a non-executive director until he stepped down at the AGM in March 2025; his senior independent director responsibilities passed to existing director Henrietta Marsh.

Figure 18 shows the current composition of the board and provides some information on members’ length of service and shareholdings in the company. It is board policy that all serving directors retire and offer themselves for re-election annually.

Recent share purchase and disposal activity by directors

Christopher Metcalfe has added to his personal holding of HRI shares

As is illustrated in Figure 18, with the exception of Priya Guha, all directors have personal investments in the trust, which we consider to be favourable as it helps align directors’ interests with those of shareholders. No directors have purchased HRI shares during the last 12 months. The most recent purchase was by Christopher Metcalfe, who added to his inaugural purchase of 3,000 shares by buying a further 2,200 shares on 1 August 2024. None of the directors has disposed of any shares during the last year.

Figure 18: Board members – length of service and shareholdings

| Director | Position | Date of appointment | Length of service (years) | Annual fee (GBP) 1 | Shareholding 2 | Years of fee invested3 |

|---|---|---|---|---|---|---|

| Andrew Joy | Chairman | 1 October 2022 | 3.0 | 43,950 | 6,000 | 3.4 |

| Stephanie Eastment | Chair of the audit committee | 1 December 2018 | 6.8 | 35,575 | 3,200 | 2.2 |

| Henrietta Marsh | Senior independent director | 1 September 2019 | 6.1 | 29,950 | 1,000 | 0.8 |

| Priya Guha | Director | 13 December 2023 | 1.8 | 29,950 | – | – |

| Christopher Metcalfe | Director | 24 April 2024 | 1.4 | 20,714 | 5,200 | 6.2 |

| Average (service length, annual fee, shareholding, years of fee invested) | 3.8 | 32,028 | 3,080 | 2.5 | ||

Board diversity

Two out of the three most-senior board positions is held by a woman

A majority of the board – three out of five members – is female. Two of the three most senior positions (chair of the audit committee and senior independent director) are held by women, and one (chairman) is held by a man.

At present, the board is composed of four individuals who are classified as White British or other White (including minority-White groups) and one that is minority ethnic. Appointments to the board are made on merit. However, the board will ensure that a diverse group of candidates is considered, and these will be evaluated against objective criteria having regards to the benefits of diversity – including gender, social and ethnic background and personal strengths, experience, and knowledge.

Andrew Joy (chairman)

Andrew is highly regarded for his extensive knowledge of the financial sector and of the high-growth part of the smaller company sector. He was one of the founding partners of Cinven, a leading private equity firm investing in Europe and US, and has been chairman or director of numerous growth companies over the past 30 years. He is also a senior advisor of Stonehage Fleming, chairman of the investment committee of FPE Capital, and a trustee of several charities. He was previously chairman of The Biotech Growth Trust Plc.

Stephanie Eastment (chair of the audit committee)

Stephanie is a chartered accountant and company secretary with over 30 years’ experience in the financial services industry. She has considerable experience in the investment trust sector and is a member of the AIC’s Technical Committee. Stephanie qualified with KPMG and held various accounting and compliance roles at Wardley and UBS before joining Invesco Asset Management in 1996 as Manager, Investment Trust Accounts. When she left Invesco in July 2018, she was Head of Specialist Funds Company Secretariat and Accounts. Stephanie is the non-executive senior independent director of Murray Income Trust Plc, a non-executive director and audit chairman of Impax Environmental Markets plc and Alternative Income REIT plc, and a non-executive director of RBS Collective Investment Funds Limited.

Henrietta Marsh (senior independent director)

Henrietta has a background in fund management, having worked in UK small-cap and private equity investment over several decades. From 2005 until 2011, she was AIM fund manager at Living Bridge Equity Partners and, prior to that, she spent 14 years at 3i in several roles, including as fund manager of 3i Smaller Quoted Companies Trust Plc (1997–2002). Henrietta spent her early career with Morgan Stanley and Shell. More recently she has pursued a non-executive career, having served on the boards of discoverIE plc, Alternative Networks plc, Electric Word plc and Gamma Communications plc (AIM-listed) where she was the senior independent director.

Priya Guha MBE (director)

Priya has significant knowledge of the global technology sector and experience in both public and private sectors. She currently has a portfolio of roles across the global and UK technology and innovation landscape, including as a non-executive director at UK Research & Innovation and Digital Catapult, a member of the Investment Governance Board at Future Planet Capital, a UK VC Fund and an advisor to various start-up companies including Gallos Technologies. She is also a non-executive director at Reach PLC and chairs its sustainability committee

Christopher Metcalfe (director)

Christopher has considerable investment management experience, having worked previously at Newton Investment Management (2006–2017), Schroder Investment Management (1995–2006) and Henderson Administration Group plc (1985–1994). He is currently chairman of the Martin Currie Global Portfolio Trust, senior independent non-executive director at JP Morgan US Smaller Companies Investment Trust Plc, and a non-executive director of Columbia Threadneedle UK Capital and Income Investment Trust Plc. He was previously a non-executive director of abrdn Smaller Companies Income Trust Plc until its merger with Shires Income in December 2023.

Management team

Katie Potts

Katie is the managing director and also the lead fund manager for HIML. She established HIML in December 1993 to manage HRI, which was launched in February 1994. Katie read Engineering Science on a GKN Group scholarship at Lady Margaret Hall, University of Oxford. She worked for five years in investment management at Baring Investment Management Limited before joining S.G. Warburg Securities’s UK electronics research team in 1988. The team was consistently voted top team in the Extel survey of analysts in the sector, and she was voted top analyst by finance directors of electronics companies canvassed by The Treasurer magazine. In addition, Katie had responsibility within S.G. Warburg’s UK research department for commenting on accounting issues.

Katie is supported in managing the funds by a team of nine other investment professionals in the UK, and one at HRI’s US affiliate.

Fraser Elms

Fraser Elms joined HIML in May 2000. He is the deputy manager of HRI and has lead responsibility for managing HIML’s Asian portfolios. Prior to joining HIML, Fraser was a technology analyst with Dresdner Kleinwort Benson, where he covered the European technology sector. Before this he worked at Prudential for three years as member of a team of three UK unit trust fund managers that managed £5bn in equities, with Fraser having lead responsibility for three funds collectively worth £400m. He graduated from Lancaster University with a degree in Economics and initially joined Prudential as a product manager for their unit trusts, before completing an MSc in Investment Analysis at the University of Stirling and re-joining Prudential in an investment role. Fraser covers the semiconductor sector.

Taymour Ezzat

Taymour joined HIML in November 2004. He has responsibility for the European portfolio and analytical responsibility for the media sector. Previously he spent a year appraising several venture capital opportunities for E.D. Capital Partners. Prior to that, Taymour had spent six years at Northcliffe Newspapers, the regional newspapers division of Daily Mail & General Trust (DMGT), latterly as Finance Director of its electronics publishing arm, after working for Reuters in London and Eastern Europe for four years. He qualified as an accountant with Price Waterhouse and studied Economic History at the London School of Economics and Political Science. He was also a portfolio manager on the venture funds (which were wound up in H1 2023) sitting on the venture committee and taking lead responsibility for a number of the investments in the venture portfolios.

Hao Luo

Hao joined HIML in 2004 and works with Fraser Elms on managing the Far East portfolios. He also has analytical responsibility for the manufacturing sector globally. Hao obtained a BA in Economics from Hunan University in China and a Masters degree in Finance from Manchester University, and worked for J&A Securities in Shanghai from 2000-2002. He is a CFA charterholder.

Peter Jenkin

Peter joined HIML as an analyst in 2015. He covers the software sector and contributes to the overall investment selection. Previously, Peter worked jointly on the European portfolio, but now has responsibility for HRI’s North American portfolio. Before joining HIML, he studied Construction Engineering Management at Loughborough University.

Danny Malach

Danny joined HIML in 2016. He was the lead dealer for the fund and in 2022 began working as an analyst on the UK team. He has analytical responsibility for computer gaming and IT services companies globally. Danny has a CFA qualification.

Fati Naraghi

Fati joined HIML towards the end of 2019 to focus on the Herald Worldwide Technology Fund and to cover some of the larger technology companies. Prior to joining HIML, she spent 20 years at Newton Investment Management, where she was responsible for the global tech sector. Fati has a PhD in Communications Systems and is qualified as an AWS Cloud Practitioner.

Matthew Lloyd

Matthew joined HIML in 2019 as a portfolio assistant and analyst. He has analytical responsibility for Alternative Energy and began working with the Asia team in 2020. Matthew has a MEng in Mechanical Engineering.

James de Jonge

James joined HIML in 2022 as an analyst on the UK portfolio, and was subsequently given analytical responsibility for the defence and medical technology sectors worldwide. Before joining the team at Herald, he managed the audits of FTSE-listed commodities trading and renewables infrastructure clients at Deloitte. James is a qualified accountant and a CFA Level 3 candidate.

Bob Johnston

Bob was recruited in 2016 to establish a US office for HIML. He has more than 20 years’ experience in the technology sector on the sell-side, and has worked with the HIML team for roughly 15 years. Most recently, Bob was with technology specialist Pacific Crest. He previously also worked for Hambrecht & Quist and SoundView Technology Group. Bob has taken on responsibility for telecommunications, networking and security analysis. US companies do not come to the UK as they used to, and Herald feels it necessary to have a US presence to enable maintenance of frequent contact with companies.

Fund profile

More information can be found at the trust’s website: www.heralduk.com.

Established in 1994, HRI invests globally in small technology, communications, and multimedia companies with the aim of achieving capital growth. It is the only listed fund of its type. The trust invests globally, and continues to have a strong bias towards the UK, although this has been reduced in recent years. However, HRI’s strong allocation to the UK further distinguishes it from other global technology funds, which tend to be heavily biased towards the US.

New investments in the fund will typically have a market capitalisation of $5bn or less but are generally much smaller when the first investment is made. If successful, these can grow to be a multiple of their original valuation. This type of investing is longer-term in nature and so the trust’s portfolio tends to have low turnover. Reflecting the risks inherent in this type of investing, and the liquidity constraints of having a small-cap investment remit, the trust maintains a highly diverse portfolio of investments (typically in excess of 250) to help mitigate this risk.

Experience is important in markets such as these

HRI’s lead fund manager, Katie Potts, has managed HRI since its launch. Her track record shows how important experience is in markets such as these.

Aside from the numerous advantages of HRI we outline in this note, one notable benefit has been the considerable experience provided by Katie and her team. Katie was a highly-regarded technology analyst at SG Warburg (later UBS) prior to launching the fund. Katie is supported by nine dedicated professionals, and has built a team of considerable skill around her that now manages a large proportion of HRI’s portfolio.

Noteworthy members of the Herald team include Fraser Elms – HRI’s deputy manager – who joined Herald Investment Management in 2000 and covers Herald’s Asian portfolios and the semiconductor sector; Taymour Ezzat, who joined in 2004 and covers Herald’s European investments and media; Hao Luo, who also joined in 2004 and helps cover Asia and manufacturing sectors; and Peter Jenkin, who joined Herald in 2015, and also covers Herald’s North American and software investments.

Katie owns a substantial stake in the company and a significant minority stake in the management company, and therefore is clearly motivated to ensure the success of the fund.

HRI’s closed-ended structure can be advantageous during market selloffs

The HRI team has navigated several downturns and has benefitted from its ability to select companies capable of weathering difficult conditions. HRI’s closed-ended structure has also been used to great effect. Whilst open-ended funds are often forced sellers, HRI can capitalise on its ability to gear and to pick up lines of stocks at attractive prices, though it has been keeping a net cash allocation more recently.

HRI’s size and focus on smaller companies, and the depth of expertise within the management team all mean that it plays an important role as a provider of much-needed capital to listed technology companies looking for expansion capital. This is particularly valuable in a downturn and has offered HRI further opportunities to generate alpha when others may not have been able to.

HRI offers a liquid subcontract for any investor looking to gain access to this part of the market, and we believe that an investment in HRI complements an investment in one of the large-cap technology funds.

SWOT analysis

Figure 19: SWOT analysis for HRI

| HRI is a genuinely unique proposition, giving investors access to smaller technology companies in the UK and overseas in a liquid vehicle, which it would be hard to invest in otherwise. |

| A very long-term track record of strong performance and expertise. Katie Potts and her team are world leaders in investing in this specialist space. |

| This can be a very volatile sector, with big swings in the underlying company share prices. However, with more than 300 holdings, the portfolio is very well diversified. |

| No dividend is paid, making this an unsuitable trust for income-seeking investors. |

| We are likely to still be in the early stages of the AI megatrend, and there are signs that, as it broadens beyond the picks and shovels players, it could increasingly benefit smaller companies. |

| There are a number of themes aside from AI that are driving growth in the technology sector. Among these is the opportunity from increased defence spending across the Western world. |

| Saba Capital continues to own a significant stake in HRI, and its intentions at this stage are unclear. |

| Technology and smaller companies investing can be particularly vulnerable to increases in inflation and interest rate expectations, irrespective of the strength of underlying companies. |

Bull vs bear case

Figure 20: Bull vs bear case for HRI

| Performance | HRI has a very long-term track record, and this compares well to the most relevant indices. Katie Potts and her team have a well-earnt reputation of delivering for shareholders. | It is reasonable to compare HRI to the US technology market, particularly the MSCI ACWI Information Technology Index. Performance can look underwhelming given the dominance of US tech and HRI’s more global allocation. |

| Dividends | HRI focuses on capital growth rather than income, and will only declare a dividend where necessary to retain investment trust status. | HRI’s lack of dividend makes it unsuitable for income-seeking investors. |

| Outlook | There are signs that the opportunities in AI are broadening out to a new data and application layer. This should benefit many of the smaller companies in HRI’s universe. | If inflation returns, as there are signs of in the UK in particular, the higher interest rates that could result would act as a brake on the technology sector. |

| Discount | After the defeat of Saba, HRI again trades at a discount, which could narrow or even move to a premium if the market environment is positive and HRI’s numerous themes play out as the managers hope. | The most recent narrowing of the discount, and move to a slight premium, was largely due to the activist moves made by Saba, rather than anything more fundamental. Saba still has a substantial stake that, presumably, it will want to exit at some point. Such selling could weigh on HRI’s discount if it is not managed properly, although this would not be in Saba’s best interests either. |

We are likely to still be in the early stages of the AI megatrend, and there are signs that, as it broadens beyond the picks and shovels players, it could increasingly benefit smaller companies.

There are a number of themes aside from AI that are driving growth in the technology sector. Among these is the opportunity from increased defence spending across the Western world.

Previous publications

Readers interested in further information about HRI may wish to read our previous notes. You can read the notes by clicking on them in Figure 21 or by visiting our website.

Figure 21: QuotedData’s previously published notes on HRI

| Title | Note type | Date published |

|---|---|---|

| Invest in the future | Initiation | 16 August 2016 |

| Tech bids demonstrate value | Update | 20 December 2016 |

| Backing growing businesses | Update | 11 July 2017 |

| Who wants to be a billionaire? | Annual overview | 7 December 2017 |

| From small acorns…. | Update | 12 June 2018 |

| Shifting sentiment | Annual overview | 12 February 2019 |

| “Profits are only profits when they are realised” | Update | 8 October 2019 |

| Change is a coming | Annual overview | 4 April 2020 |

| Hot chips | Update | 5 November 2020 |

| The future is bright | Annual overview | 2 February 2022 |

| Efficiency Savings | Annual overview | 11 January 2023 |

| Patience and power | Update | 13 November 2023 |

| Heralding in the age of AI | Annual overview | 25 June 2024 |

| Vote against Saba to protect your investment | Update | 15 January 2025 |

IMPORTANT INFORMATION

This marketing communication has been prepared for Herald Investment Trust Plc by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and, if you are not a professional investor, or in any other way are prohibited or restricted from receiving this information, you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it, but in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.