Table of contents

Table of contents

- Tyking over…nicely

- Data summary

- Investment summary

- Company profile: Virtual development

- TYK2 – autoimmune disease

- SRA737 development affected by Sierra’s strategic change

- Investment thesis – valuation

- Previous publications

- The legal bit

Tyking over… nicely

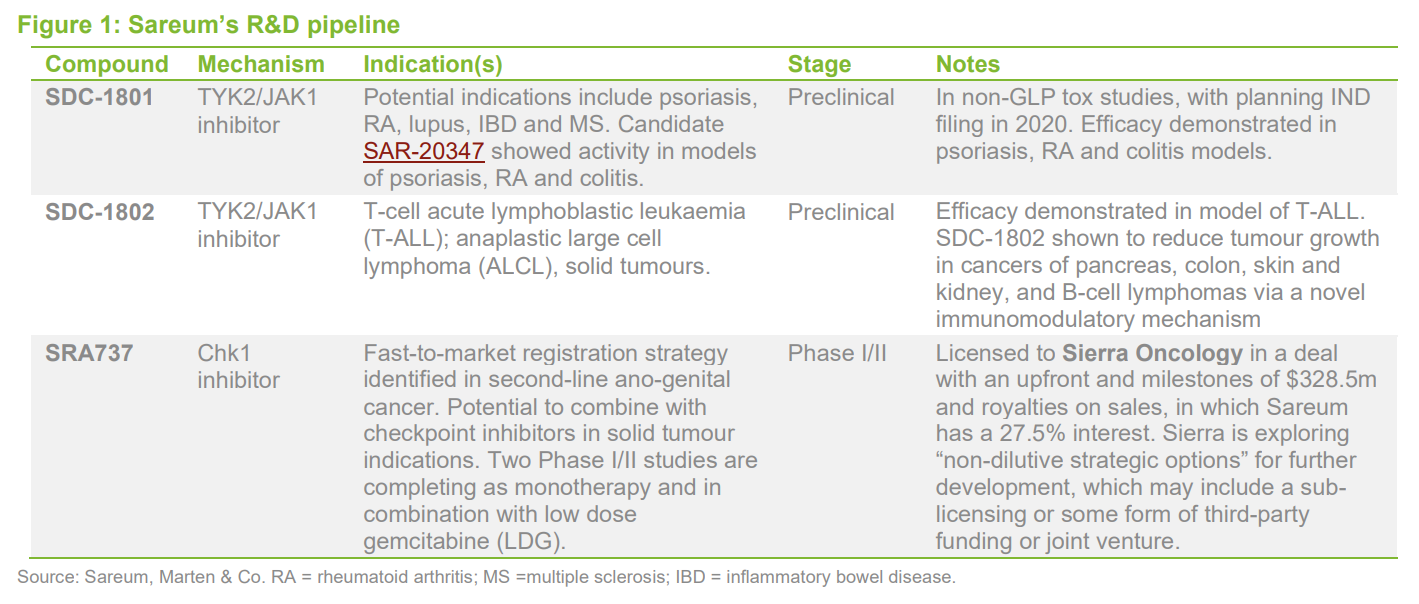

Sareum’s investment case centres on the development and potential out-licensing of its two internal, preclinical-stage TYK2/JAK1 inhibitors, which are proceeding towards IND (investigational new drug) filings in 2020. Development of Sareum’s Chk1 inhibitor, SRA737, is ongoing for now, but is likely to see a pause, while Sareum’s partner, Sierra Oncology, attempts to secure a sub-licensing deal following a change in its own strategic priorities. The uncertainty created by this decision has weighed on Sareum’s share price, despite trials of SRA737 yielding some promising early data and highlighting a fast-to-market development plan.

However, increased visibility of Sareum’s cancer-focused TYK2 programme SDC-1802 and progress with the previously higher profile autoimmune candidate SDC-1801 has led to an increase in the notional value of the two combined TYK2i assets to c.£20-25m in QuotedData’s model. However, uncertainty over SRA737’s future has led to a hopefully reduction in the value of this asset, previously estimated at £20m in QuotedData’s model.

Within QuotedData’s model, these two countervailing effects suggest that a current value for Sareum now lies in the £20-25m range (0.65-0.81p/share), versus the previously published £25-35m (after normal assumptions for research and development, corporate overheads and tax). Despite the overall fall, the new valuation still offers up to 92% upside against the current share price. There is also the potential for further gains if a satisfactory resolution to the uncertainty over SRA737’s future can be found (see page 8).

| wdt_ID | Year ended | Rev (£m) | PBT (£m) | EPS (p) | DPS (p) |

|---|---|---|---|---|---|

| 1 | 30 Jun 2017 | 0 | 0.40 | 0.02 | 0 |

| 2 | 30 Jun 2018 | 0 | -1.70 | -0.05 | 0 |

| 3 | 30 Jun 2019 | 0 | -1.70 | -0.05 | 0 |

| 4 | 30 Jun 2020 | 0 | -1.70 | -0.05 | 0 |

Data summary

Investment summary

- Sareum’s investment case centres on successful development and potential future out-licensing of two TYK2/JAK1 inhibitors, which are proceeding through towards planned IND (investigational new drug) filings in 2020.

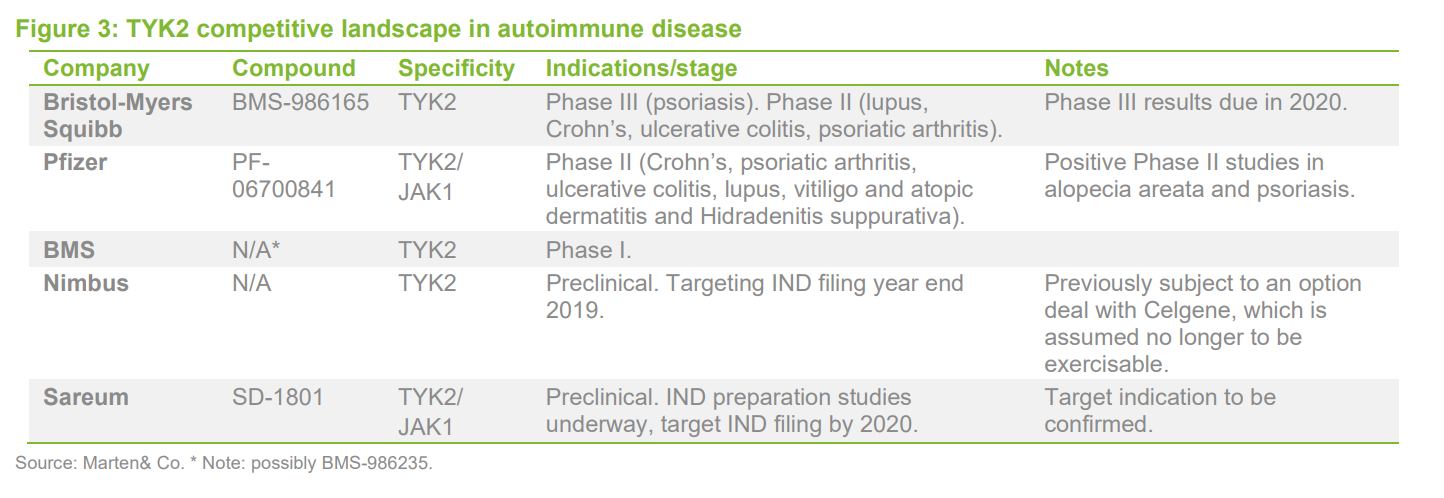

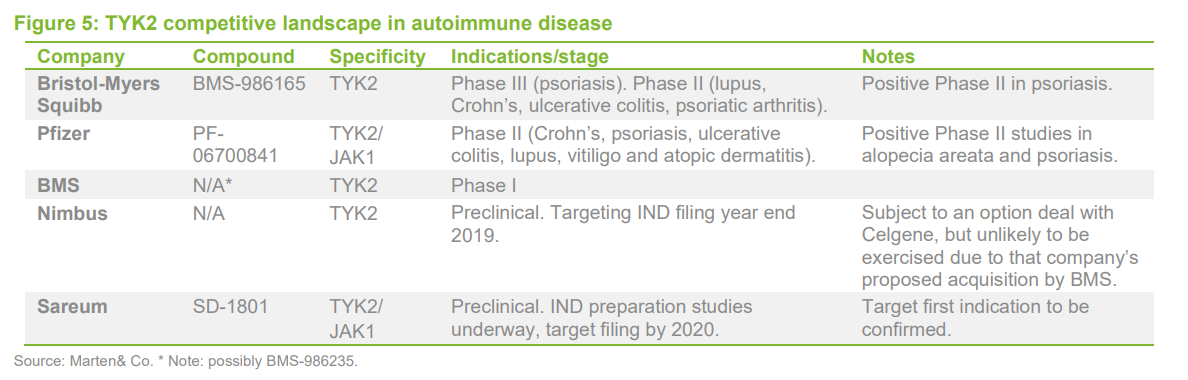

- Sareum is one of only a handful of companies with a TYK2 (or dual TYK2/JAK1) inhibitor in development (see Figure 3). Although Sareum’s candidate is behind the two class leaders, its autoimmune disease-targeted SDC-1801 has the potential to be highly attractive as a licensing opportunity, as the therapeutic areas that it addresses are large and have historically supported multiple agents with similar mechanisms.

- The most advanced compound in the TYK2 class is Bristol-Myers Squibb’s BMS-986165, which is in Phase III trials for psoriasis and in Phase II for several other autoimmune indications. Pfizer also has an TYK2/JAK1 inhibitor in mid-stage clinical development. Both compounds have shown highly promising efficacy in a range of autoimmune indications.

- Greater visibility of Sareum’s cancer-focused TYK2i SDC-1802 through conference presentations/publications and solid progress with the higher profile autoimmune candidate SDC-1801 has led to an increase the notional value of its combined TYK2 assets in QuotedData’s model to around £25m.

- Development of the Sareum’s Chk1 inhibitor SRA737 continues, but it appears that this is likely to pause while partner Sierra Oncology explores “non-dilutive strategic options” for further development. This follows a change in Sierra’s strategic priorities. Sierra is effectively looking to divest SRA737 (together with another asset) through a sub-licensing deal or spin-out. Early trials have yielded some promising data and highlighted a fast-to-market development strategy in ano-genital cancer. SRA737 is one of only two molecules with this mechanism in development, the other, by Esperas Pharma (a venture capital backed vehicle), is in Phase I/II studies.

- It should be noted that there is no guarantee that Sierra will be successful in securing a licensing deal or other arrangement to allow development of SRA737 to continue. However, if there is an extended delay in finding a partner and no active development underway, CRT Pioneer Fund (the counterparty in the current licensing deal) may seek to recover rights under the diligence clauses. This would, however, be unlikely to be possible before 2021 (development continues for now and there needs to be a period in which there is no development for the clauses to kick in) and the fund would then have attempt to re-license it.

- Sareum has a 27.5% economic interest in a licensing deal covering SRA737, which we assume would be maintained in the event of any transaction over the asset by Sierra. Marten & Co valued this interest in SRA737 at £20.3m last year, but the uncertainty over timelines and the indications that may be pursued means that this should be considered impaired, pending resolution of the situation.

- Sareum otherwise remains exposed to risks normally associated with drug development, including the uncertain outcome of clinical trials, its reliance on partners, and the success or failure of competing molecules.

With reasonable assumptions for research and development spending, overheads and tax, QuotedData’s model suggests a current value of Sareum to lie in the £20–25m (0.65–0.81p/share) range, versus the previously published £25–35m. As noted on the front page of this note, this valuation still offers up to 92% upside at the current share price, with potential for further gains from a satisfactory resolution of the current uncertainty over SRA737.

Company profile: Virtual development

Sareum is a UK-based biotech company that operates on a virtual basis (in that most of its activities are outsourced to third parties) and specialises in the early-stage development of compounds that inhibit a class of cell signalling molecules known as kinases. These function as “on/off” switches for many cellular functions. One sub-type of these, tyrosine kinases, is the target for a large and well-established drug class, tyrosine kinase inhibitors (TKIs). More than 50 TKIs have been approved, mostly for cancer, and many more are in development. Kinases are also used to treat autoimmune/inflammatory conditions, albeit with only a small number of approved products to date.

Sareum was originally formed in 2003 as a management buy-out from Millennium Pharmaceuticals, a large US biotech company (now a subsidiary of Takeda). The company originally operated a hybrid business model, in contract research and development, based on its expertise in solving the 3D structure-activity relationships of “challenging” drug targets. This provides a basis for the optimisation of molecules that could selectively block those targets selectively without affecting other mechanisms.

Sareum’s structure-based approach particularly lends itself to kinases as the large number of these targets, and their closely-related nature, means that prior knowledge of 3D structure is often required to achieve adequate levels of selectivity. Sareum is one of only a handful of companies that have identified a selective TYK2 inhibitor, especially one that avoids JAK2/3, and it is effectively one of only two that are unpartnered. There is therefore reason to believe it could find a partner on economically attractive terms. Historically, autoimmune-condition market opportunities have tended to support at least four compounds in the same class, as is the case with JAK1 inhibitors for rheumatoid arthritis (RA).

Sareum listed on the AIM market of the London Stock Exchange in 2004 and has funded its activities through periodic share issues, which have totalled approximately £14m to date. The company took a strategic decision to sell its contract research activities in 2008, evolving into a pure drug-development business. Since then, it has focused purely on advancing its portfolio with the aim of reaching recognised value inflection points, such as demonstrating desirable pharmacological properties and activity in animal models.

The company expects to license out compounds after reaching important value inflection points – typically to larger biotech or pharmaceutical companies – for further development and commercialisation. This is a well-established business model for biotech companies and, indeed, pharmaceutical companies typically source as much as half of their research and development pipeline in this way. Returns from licensing deals typically come in the form of an upfront payment, followed by milestone payments (payments made on successful completion of key development stages; regulatory filings or approvals; or achievement of sales thresholds) and then royalties (a percentage of sales) payable on a territory-by-territory basis until the expiry of the licensed intellectual property.

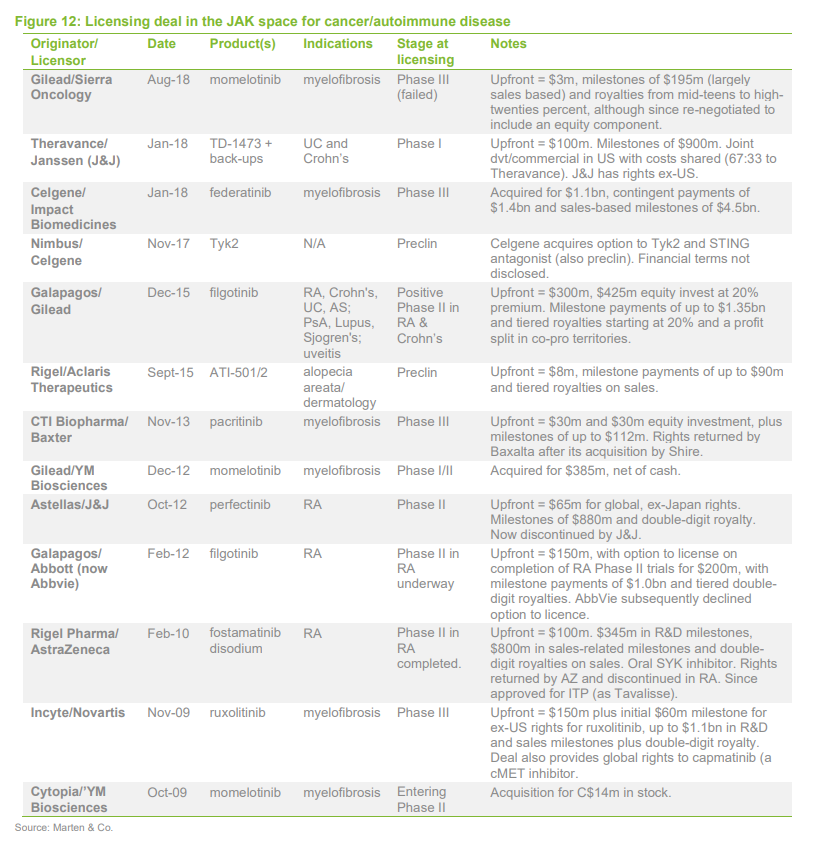

It is, however, difficult to predict the level of interest on the part of potential licensees as well as the timing and outcome of licensing negotiations (disclosed terms of licensing deals in the TYK2/JAK space are summarised in the Appendix later). Nevertheless, assets that are likely to be most attractive to potential partners would be expected to be those with the strongest competitive position among those with the same or a similar mechanism. This competitive position in the wider landscape, therefore, should be an important consideration for investors.

TYK2 – autoimmune disease

Sareum is one of five companies developing TYK2 (Tyrosine kinase 2) inhibitors in autoimmune disease and the only one known to be currently targeting a specific cancer indication. TYK2 is a member of the Janus Kinase family (which also includes JAK1, 2 & 3) of non-receptor tyrosine kinases. TYK2 has been shown to play an important role in the signalling of type I interferons (a large subgroup of interferon proteins that help regulate the activity of the immune system), as well as IL-12 and IL-23, via phosphorylation of downstream STATs (signal transducer and activator of transcription proteins), and hence inhibition of its activity can switch off production of pro-inflammatory cytokines.

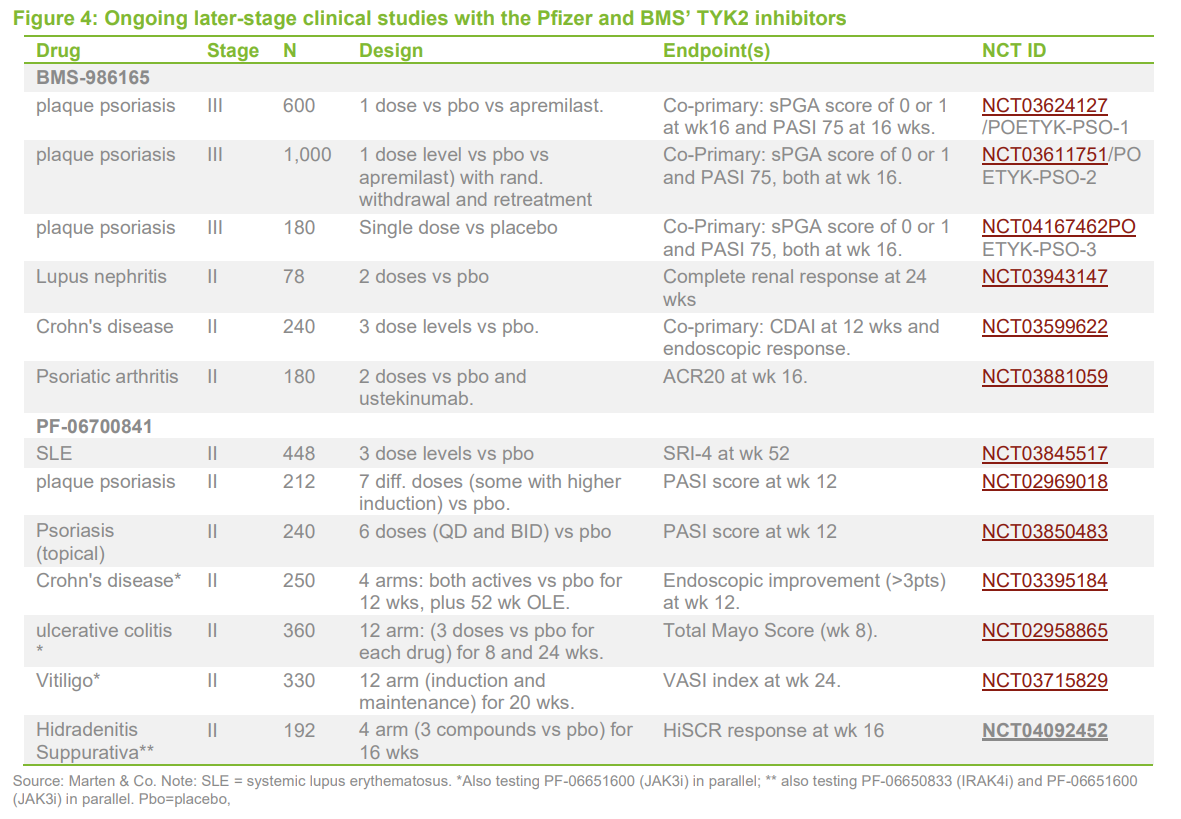

Two products in this TYK2i (Tyrosine kinase 2 inhibitor) class are in mid/late clinical stage trials – Bristol-Myers Squibb (BMS-986165) and Pfizer (PF-06700841). BMS has two registration trials underway in psoriasis and both companies have multiple mid-stage studies underway in other indications including systemic lupus erythematosus (SLE), Crohn’s and ulcerative colitis (UC), psoriasis/psoriatic arthritis and vitiligo. Pfizer also has a topical version (one that is applied to a particular place on or in the body) of its molecule in mid-stage studies for psoriasis.

It is notable that in connection with its recently completed merger with Celgene, Bristol-Myers Squibb (BMS) elected to retain BMS986165 and divest Otezla – an approved oral treatment for psoriasis with blockbuster sales – in order to meet US anti-trust requirements, suggesting the high perceived value of its compound.

Phase II data from several completed studies with the Pfizer and BMS compounds have been published in psoriasis and alopecia areata. These data were extremely strong and have validated the TYK2 mechanism in these two indications. A potentially important difference between the molecules is that BMS’s is a pure TYK2 inhibitor while that of Pfizer is a dual TYK2/JAK1 inhibitor. The publication of the psoriasis data has meant it is now possible to compare efficacy of the two compounds in the same indication. At first glance, there appears to be an advantage to the dual TYK2/JAK1 approach at the highest doses tested, which would be consistent with the fact JAK1 is also a validated target. This may translate into an advantage for dual mechanism molecules, such as Sareum’s, in autoimmune disease.

Interestingly, Pfizer’s Phase II study in alopecia areata also examined a JAK3 inhibitor in parallel and, in this case, the efficacy of the TYK2/JAK1 inhibitor was appeared to be better. However, Pfizer decided to advance its JAK3 inhibitor into Phase III trials in this indication, possibly for commercial reasons.

JAK1 inhibition is also a validated target in autoimmune disease. There are three products with this mechanism that are now approved for rheumatoid arthritis (Pfizer’s Xeljanz, Lilly’s Olumiant and AbbVie’s Rinvoq) as well as positive studies in other indications (psoriasis, atopic dermatitis, Crohn’s and UC). Xeljanz, a JAK1/3 inhibitor, gained approval in 2012 for rheumatoid arthritis and subsequently for psoriatic arthritis and ulcerative colitis. It recorded sales of $1.8bn in 2018 despite carrying a “black box” warning.

Lilly’s Olumiant, the second JAK inhibitor to be approved has a peak sales forecast of c.$2bn/year. It also carries a black-box warning for serious infections, lymphoma and thrombosis. Olumiant is in late-stage development for other indications including atopic dermatitis, in which it has reportedly positive Phase III studies, and lupus. Abbvie’s Rinvoq, which was recently approved for rheumatoid arthritis, has peak sales estimated at $3–5bn/year. This and a fourth product, Gilead’s filgotinib (currently being filed), are considered second-generation agents with greater JAK1 specificity.

There are few other products in the same space. Pfizer has a JAK1 inhibitor, abrocitinib (PF-04965842), which has successfully completed Phase III trials for atopic dermatitis. Galapagos is also known to be interested in the TYK2 space. It advanced a compound into Phase I trials this year, but dropped the drug as a result of poor pharmacokinetics (pharmacokinetics assesses how a drug affects an organism. Specifically, what happens to the chemical from the moment it is administered to the point at which it has been completely eliminated from the body).

Sareum is considering a strategy that may see lupus or lupus nephritis (the kidney damage associated with later stages of the disease) become the lead indication(s) with SD-1801, in order to avoid the more competitive areas such as psoriasis. Lupus is being studied by BMS in a large Phase II study, which if successful, could see SDC0-1801 becoming a “fast follower” with a potentially better dual targeting mechanism.

Lupus has been historically extremely challenging indication for pharmaceutical development but, in recent months, the field has seen some unexpected positive results from AstraZeneca, Roche, Biogen and latterly Aurinia Pharmaceuticals. This may in turn prompt heightened interest from potential licensing partners.

Sareum’s other TYK2i compound, SDC-1802, has shown activity in cellular and disease models of T-cell acute lymphoblastic leukaemia (T-ALL) and B-cell lymphoma. T-cell ALL is a rare sub-type of ALL. It accounts for around 10-15% of cases. Sareum estimates there may be 2,000 cases per year in Europe and the US. The condition is currently treated with chemotherapy and stem-cell transplant, but no targeted therapies have been developed. TYK2 inhibition may represent be an approach to treating T-ALL, as the TYK2/STAT1/BCL-2 pathway is implicated in the survival of leukemic cells.

Inhibiting TYK2 may be an approach in solid tumours. Sareum has generated evidence of activity in disease models of kidney, colon, skin and pancreatic cancer, and further work may elucidate a strategy in solid-tumour indications, possibly with immune checkpoint inhibitors. These data were recently presented at the AACR-NCI-EORTC meeting (see link).

SRA737 development affected by Sierra’s strategic change

Sierra Oncology is currently conducting studies of SRA737, but, as noted earlier, it is now seeking a partnership for further development, following a change in strategy. This change came about as a result of the subsequent acquisition of a Phase III stage drug, momelotinib, and furthermore, the decision to divest the rights to SRA737 seems to have come about as a condition of a major refinancing. It is not necessarily a reflection of the prospects for SRA737 per se.

Sareum holds a 27.5% interest in the licensing deal that covers the compound, which arose as a result of an earlier partnership it had with the Institute of Cancer Research, with early funding provided by Cancer Research UK. The licensing deal, which was executed by CRT Pioneer Fund (CPF), the investment arm of CR UK, has a headline value of $328.5m plus royalties.

SRA737 is a highly selective inhibitor of Checkpoint kinase 1 (Chk1). This is a key regulator of cell-cycle progression and DNA damage repair/replication stress response. The strategy is based on the fact that cancer cells are normally in a state of intrinsic replication stress caused by oncogenes, mutations in DNA repair machinery, a dysregulated cell cycle or other genomic alterations. This replication stress leads to a dependency on Chk1 for survival. Thus, targeted inhibition of Chk1 should cause the selective death of cancer cells in replication stress, a process known as “synthetic lethality”.

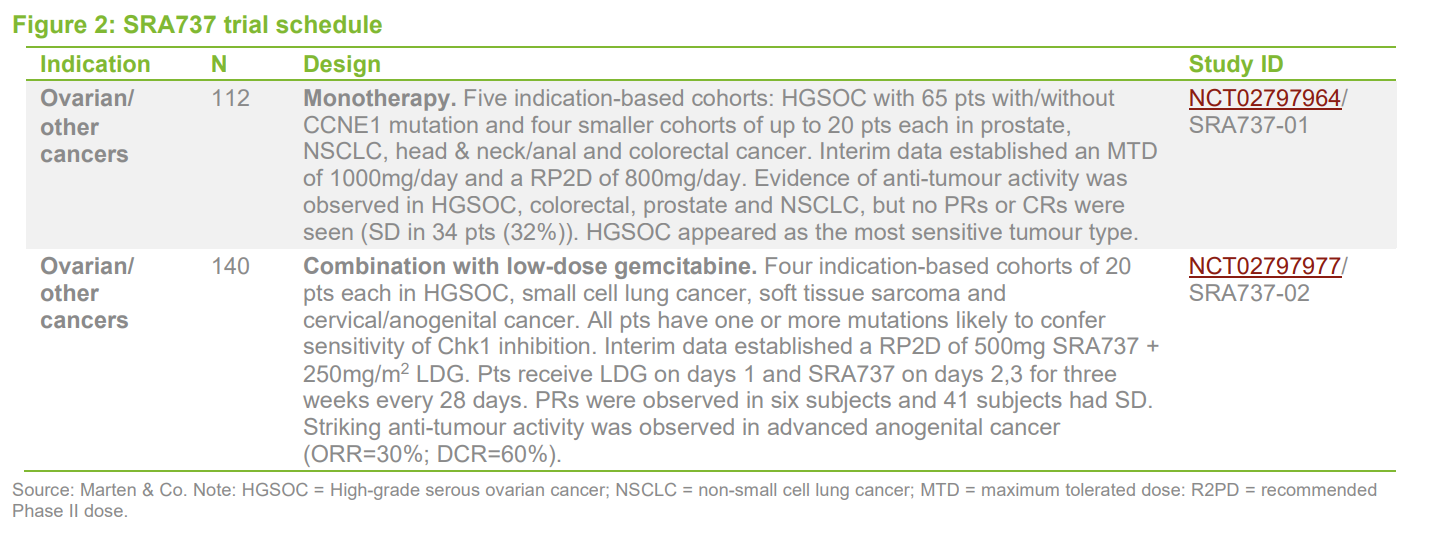

SRA737 is being evaluated in two separate Phase I/II trials, one as a monotherapy and the other in combination with low-dose gemcitabine (LDG). Both studies remain underway and should complete in Q2 next year, although it has to be presumed that planning for future studies is on hold and therefore the programme may enter a period of abeyance until after a new licensing partner is found.

Both studies reported initial findings earlier this year showing anti-tumour activity, although arguably these may not be sufficient for further development as a monotherapy. However, there was a very solid signal from the combination study that would support a fast-to-market development plan in ano-genital cancer.

The combination study also attempts to look at patients with specific mutations (such as CCNE1) that may lead to increased replication stress, in order to see if this would make them particularly susceptible to the combination strategy. As yet, no strong signal on this has been seen, although there were probably too few patients to be definitive. Nevertheless, this probably weakened the case for a tumour-agnostic development strategy, which had been the planning scenario in QuotedData’s earlier model.

By contrast, separately published preclinical data of SRA737, in combination with low-dose gemcitabine and a checkpoint inhibitor, showed profound synergy and highlighted a very promising approach that is likely to be taken in development.

Although both trials are continuing, development of SRA737 will have to be transferred to a third party at some point and this will inevitably lead to a delay in previously expected timelines. Furthermore, there is no guarantee that Sierra will be successful in securing a licensing deal or other arrangement to allow development of SRA737 to continue. If there is a substantial delay in finding a partner, CRT Pioneer Fund, could seek to recover rights under the diligence clauses of the contract.

Investment thesis – valuation

QuotedData’s model assumes that Sareum’s TYK2/JAK1 compounds to form the core of the investment case and, given the current circumstances, its interest in the SRA737 licensing deal likely to provide upside, pending clarification of future funding arrangements.

Unfortunately, it is highly problematic to try to calculate a value (based on an NPV, for example) for preclinical-stage assets, as these are highly sensitive to a number of unknowns (such as targeted indications, timelines, probabilities of success etc) and if conservative assumptions are made, they would in any case tend to provide a negative value at this point. Such compounds, however, are typically thought to have a value in the industry of ~$20-30m, based on the upfront values in M&A transactions (such as Amgen’s purchase of Nuevolution, earlier this year).

Nevertheless, QuotedData’s model considers increasing visibility of Sareum’s cancer-focused TYK2 programme SDC-1802 – based on the recent data presentation – and similarly good progress with the higher profile autoimmune candidate SDC-1801 to have boosted the notional value of the two combined TYK2i assets to around £20-25m. This indicative value is based on a review of values of upfronts obtained in licensing agreements for preclinical-stage autoimmune assets, again heavily discounted, and based on the experience of the analyst. It is also worth stressing that economics obtained in licensing deals can – and usually would be – much larger than these sums, sometimes by several orders of magnitude.

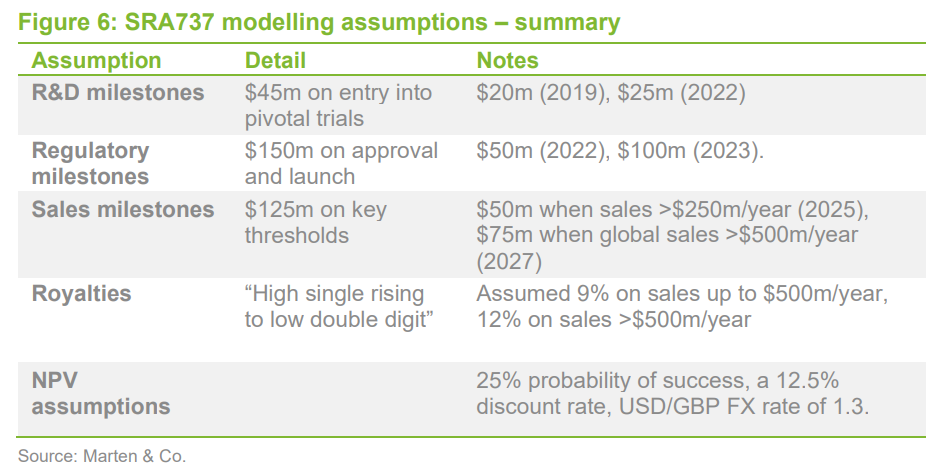

As noted earlier, QuotedData’s model suggests that the value of SRA737 has been reduced for now, pending resolution of the current uncertainty by Sierra, and have ascribed a figure in the order of £5m. QuotedData’s model previously had an estimated value in the region of £20m, based on a strategy of tumour agnostic development.

Given the uncertainty over SRA737’s development and the presumed reduction in its value, there is little point in updating QuotedData’s valuation from last year. As a reminder, QuotedData’s model suggested a value for Sareum’s interest in SRA737, by making assumptions about the size and timing of future milestones (which, as is usual, have mostly not been disclosed) in the licensing deal. These would in theory remain in any sub-licensing arrangement, but the timing of their trigger points will likely be delayed by one year or more, even if a deal is concluded soon.

For completeness, the milestone and royalty income assumptions have been summarised in Figure 6, although any future development will probably focus on ano-genital cancer and possibly in combination with a checkpoint inhibitor in as-yet undefined indications.

With normal assumptions for research and development spending, overheads and tax, Marten & Co believes a fair valuation for Sareum now lies in the £20–25m range (0.65-0.81p/share), versus our previously published £25–35m. Nonetheless, this new valuation still offers up to 92% upside against the current share price, with potential for further gains from a satisfactory resolution of the uncertainty over SRA737.

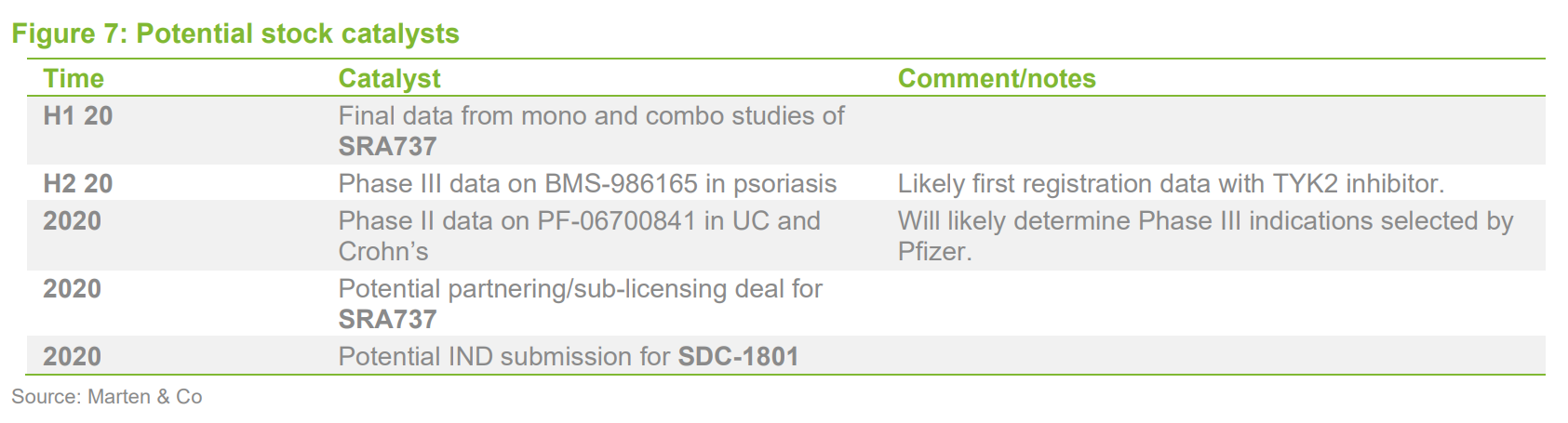

Stock catalysts

Investment sensitivities

Sareum is exposed to the risks typical of biotech company drug development, including the uncertain outcome of clinical trials and reliance on third parties (notably, Sierra achieving a successful sub-licensing of SRA737) to advance the development of licensed assets and its own internal TYK2 assets.

We note that for commercial reasons a potential partner(s) for the TYK2 compounds may insist on rights to both autoimmune and cancer indications and thus it may not be possible to license the two compounds separately. The value of the TYK2 assets may be affected by the success or failure of competitors, both within the TYK2/JAK class and, to a lesser extent, for other oral molecules addressing autoimmune/inflammatory indications. In order to be commercially successful, new oral agents will likely have to show levels of efficacy that approach or match those of biological agents while offering side-effect advantages, such a lower tendency for immunosuppression.

Management & shareholders

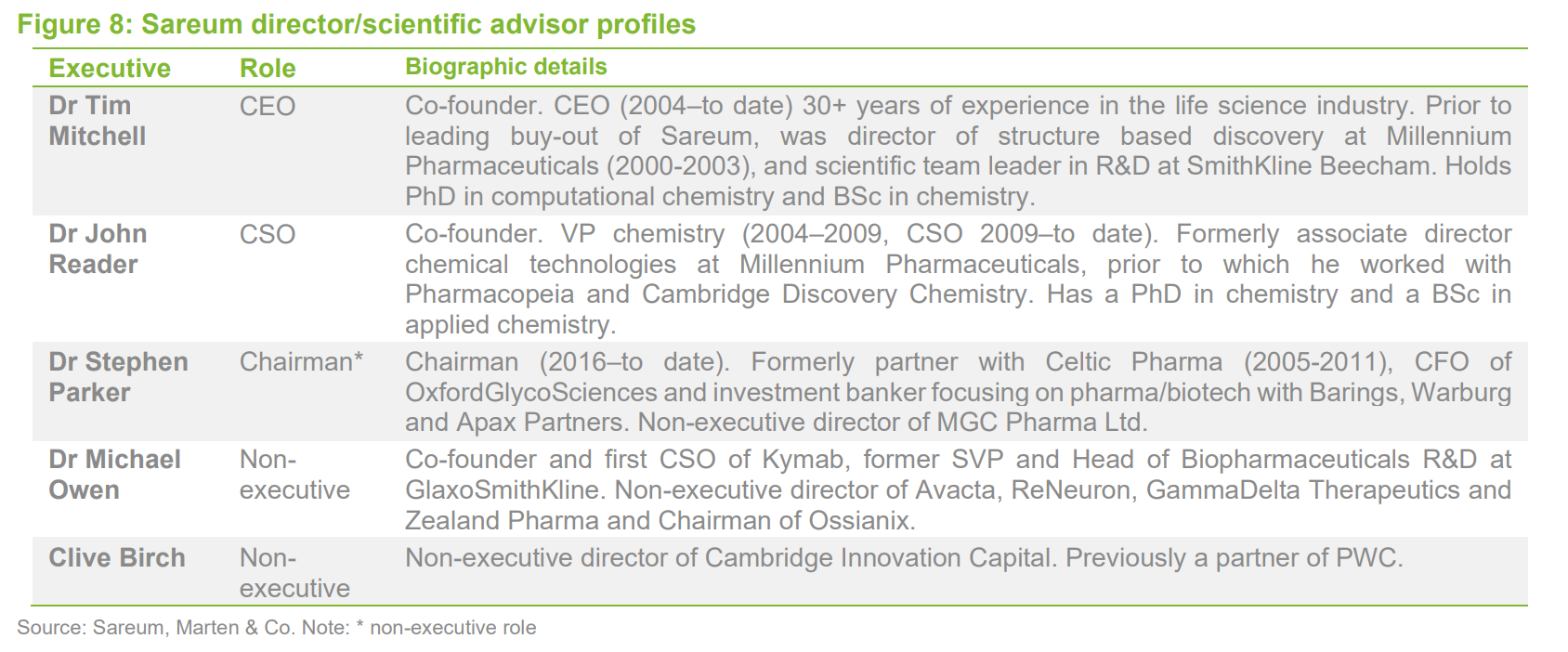

Sareum has 3.07bn shares in issue and there are no other substantial or disclosable (>3%) shareholdings. Sareum has enlarged its board in the past year with the appointment of Dr Michael Owen and Clive Birch as non-executive directors. Further information on the company’s board/management is provided in the Figure 8 below.

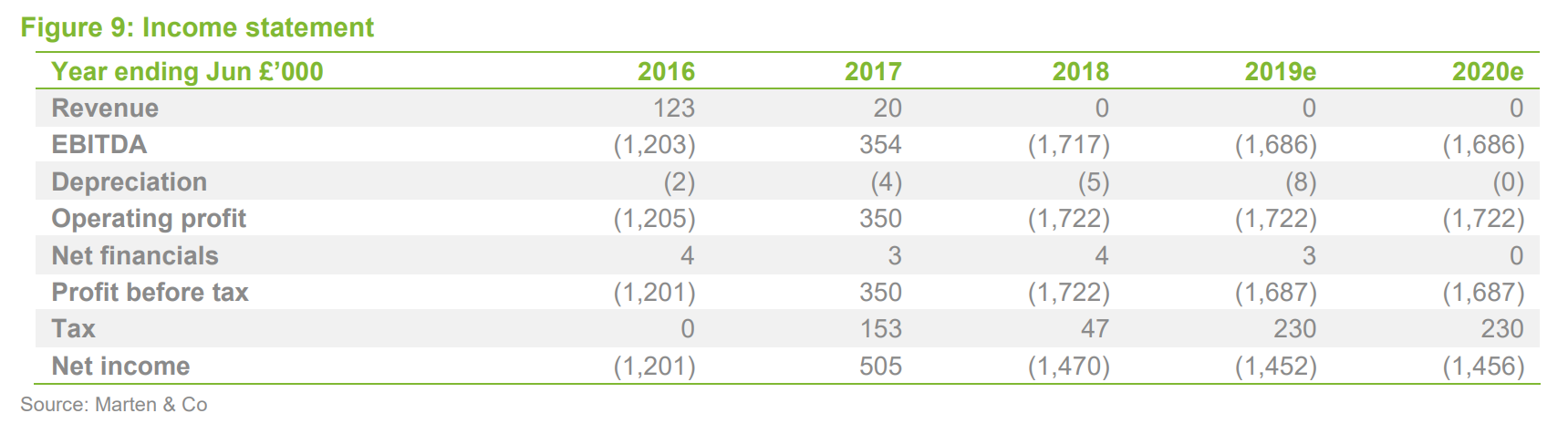

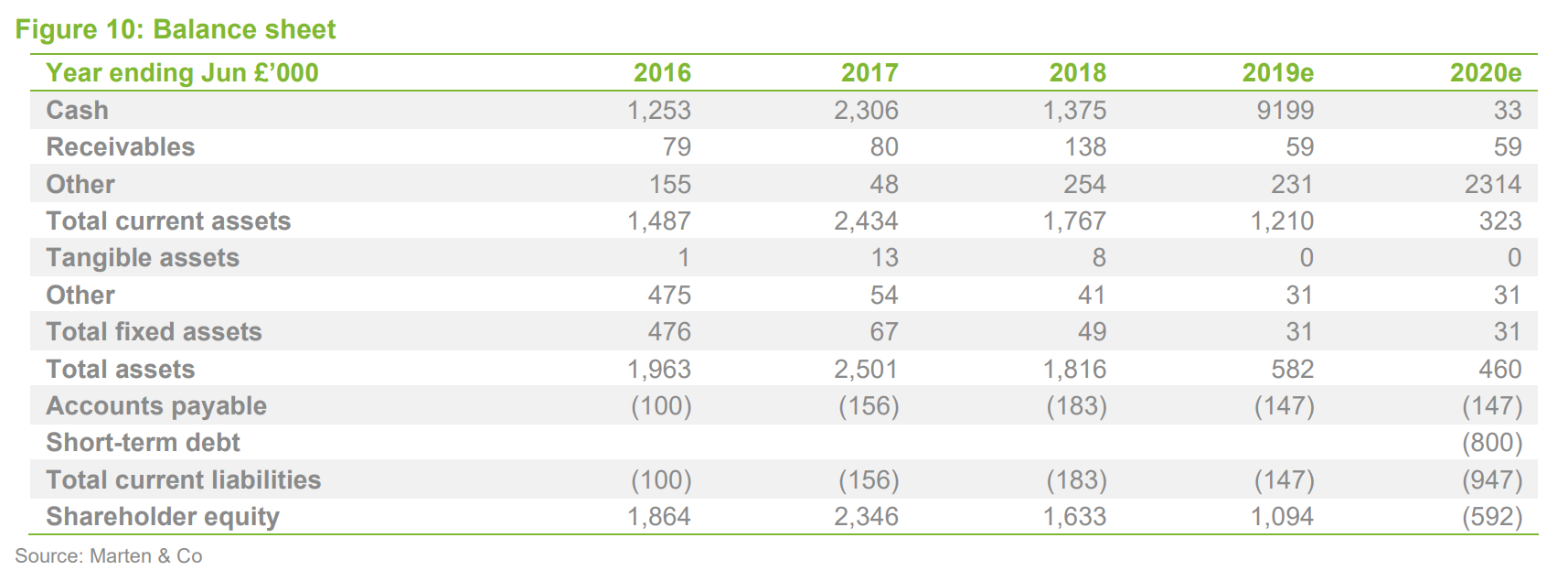

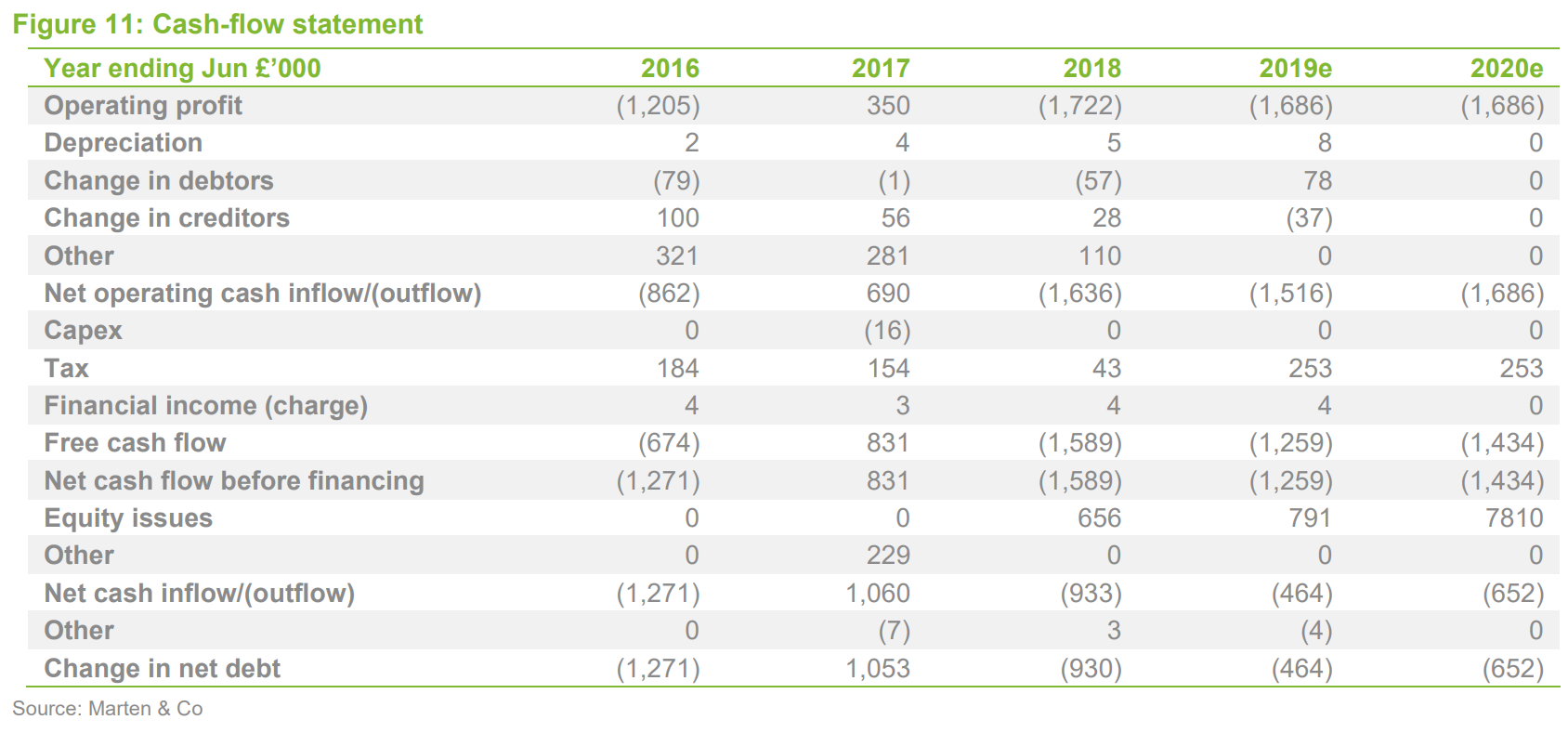

Financials

Sareum reported pro forma cash of £1.7m at year end (30 June, adjusted for a subsequent share issue), which – if current spending levels are maintained – should provide a runway into FY2021. The financial model has not materially changed, except for adjustments to reflect share issues, and we do not consider it to be a major factor in the investment thesis, except in relation to Sareum’s ability to fund its planned future development activities.

Appendix – JAK licensing deals

Previous publications

Readers interested in further information about Sareum may wish to read QuotedData’s initiation note, Tyking the boxes, which was published on 7 November 2018 and our update note, Key ‘737 data coming up, published on 7 March 2019..

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Sareum Holdings Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.