Urban Logistics REIT (SHED) this week has announced another potential equity raise, having already invested all the proceeds of its £136m placing from March 2020.

The news underlines the polarisation we are seeing in the property market, with other sectors such as retail and offices struggling in the face of uncertain futures.

As many of you know, the logistics market has continued in growth mode – the global Covid-19 pandemic accelerating online consumption trends that had been playing out for the best part of a decade.

The fundamentals supporting the ‘urban logistics’ sub-sector is compelling.

These properties are smaller in size than the huge distribution warehouses you see on the side of motorways and are located in and around cities and towns.

They are in huge demand, especially by retailers and parcel delivery companies, exacerbated by the huge spike in online orders from an increasingly tech-savvy population.

The properties, usually sized between 20,000 and 80,000 sq ft, play a pivotal role in the transport of goods to homes across the country, acting as the final touching point before delivery.

Being located as close to densely populated, large urban areas has never been as important to ecommerce players, as online orders soar.

As demand has increased, supply of these properties has not kept up and in many areas, including London, has shrunk, with existing estates turned into homes.

Where supply and demand imbalance exist, pressure on rents will follow. Few, if any, property sub-sectors can match the supply-demand characteristics shown in urban logistics.

As the name suggests, Urban Logistics REIT (SHED – the colloquial term used in the property industry to described the industrial and logistics sector) is the only listed property company solely focused on the urban logistics sub-sector.

LondonMetric Property (LMP) has changed course to focus on growing its exposure to this sub-sector, with 35% invested in urban logistics. While Warehouse REIT (WHR), which is often compared to SHED, has a very different portfolio composition – this week buying two larger distribution warehouses.

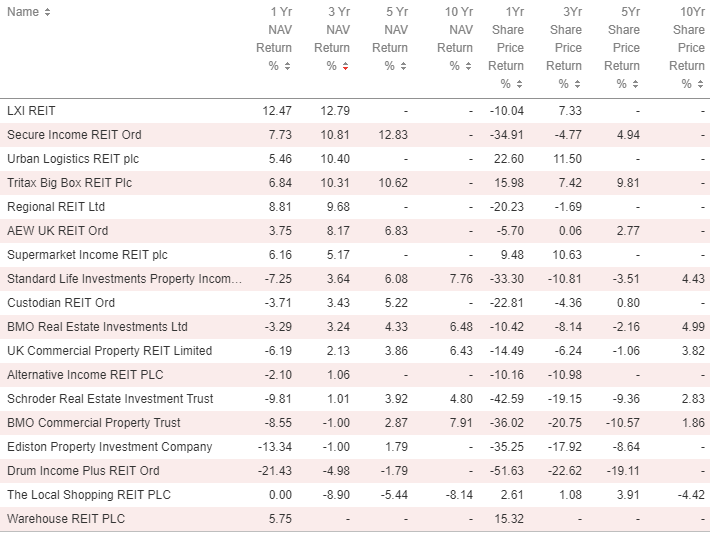

A look at SHED’s performance numbers since it launched in 2016 make for interesting reading. Over three years it has a NAV total return of 10.4% – putting it third among commercial property REITs behind the two long income funds LXI REIT and Secure Income REIT. In share price returns, it is top of the peer group with a 11.5% return over three years.

In announcing the potential equity raise, SHED said it has identified a pipeline of potential acquisitions worth £389m across 33 assets with a current rent roll of around £26.7m a year and with a weighted average net initial yield of 6.43%.

It is currently on an 5.1% premium to its last reported NAV. A low average passing rent on its current portfolio of under £5/sq ft and the rental growth prospects of the sector points to potentially significant value uplift.