Our review of last month’s big risers and fallers shows how concerns about President Trump’s threat to the independence of the Federal Reserve exacerbated concerns over US inflationary pressures. This made August a good month for investment companies exposed to gold and Asia, but less kind for listed renewables and some growth funds as forecasts for long-term interest rates rose.

Trusts that shone

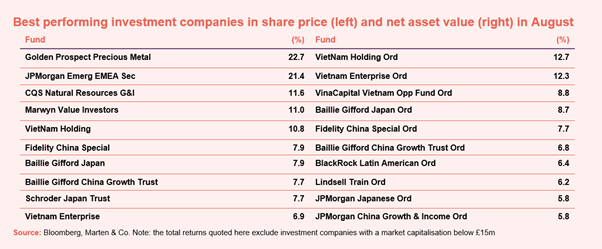

Gold, which has rallied around 35% this year as investors look for a safe haven against a dollar deliberately weakened by Trump’s policies, underpinned two of the 10 biggest risers in August.

Golden Prospect Precious Metals (GPM), a £71m portfolio of gold and silver miners run by Keith Watson and Robert Crayfourd at Manulife, led the way with an impressive 22.7% share price leap.

With gold hitting a fresh record high of over $3,500 an ounce this week as the Trump administration pressed on with its dismissal of Fed governor Lisa Cook, shares in the investment company have continued to advance. Up 98%, they have nearly doubled this year, with the gap, or discount, to net asset value (NAV) narrowing to 13% compared to a one-year average of 19.5%.

Stablemate CQS Natural Resources (CYN), which Watson and Crayfourd run with lead manager Ian Francis, also did well, rising 11.6%. Further gains in September have pushed the shares up nearly 41% this year with the discount on the £162m closed-end fund shrinking to just 1.7% in response to investor demand and a tender offer.

Emerging markets funds have come in from the cold as the weak dollar encourages investors to look further afield in pursuit of diversifcation from a richly valued US stock market.

In second place in our table of risers, JPMorgan Emerging EMEA Securities (JEMA) jumped 21.4% after the Russian court suspended the $81m claim by VTB Bank against eight JP Morgan entities including JEMA. This is while the English court considers VTB’s appeal against a decision to grant the JP Morgan grouping an anti-suite injunction. Shares in the £100m trust have shed much of these gains in the past two weeks but still stand on an extraordinary 320% premium over asset value which reflects some investors’ faith that money will be extracted from its written down Russian holdings one day.

Vietnam, China and also Japan funds rallied with share price gains of 7%-11% in August underpinned by uplifts to the underlying asset values as shown in the right hand column of our table. Vietnam Holding (VNH) did best with its shares up 10.8% on the back of a 12.7% estimated increase in net asset value (NAV) and an annual redemption.

Fidelity China Special Situations (FCSS), the largest of the three London-listed China trusts, rose 7.9% to take its year-to-date advance to 39%, though the shares still trade around 9% below NAV.

Not everything China related did well. As already highlighted in our monthly REIT review, shares in Macau Property Opportunities (MPO) tumbled 23% to top our second table of fallers. This was a response to an end-of-month update of a 23.5% plunge in net asset value caused by the company having to slash prices of properties it is trying to sell in its long-running wind-down amid economic uncertainty afflicting the special administrative region on the superpower’s south coast.

Bond falls weigh on renewables

Government bonds have been under pressure from inflation. Concerns over the UK’s fiscal position ahead of the November Budget have seen rises in long-term UK gilts yields that point to higher costs of borrowing which have sapped a mixture of growth and renewables funds.

Having rallied strongly in the stock market’s recovery from US tariff fears in April, Seraphim Space (SSIT) retreated in August, with a 16.7% decline in its shares. The £164m investor in space commercialisation companies remains 27% up this year, however.

It was also a difficult month for fellow growth capital fund Literacy Capital (BOOK). Shares in the UK private equity fund that supports reading charities fell 10.6% in August, despite revealing a 5.4% first half rise in assets and committing to a return of capital later this year to compensate investors for the wide 27% discount on their shares.

Renewable energy funds were also weak with most reporting declines in net asset value due to rises in discount valuation rates and falls in power price forecasts.

Recharging battery fund Gresham House Energy Storage (GRID) fell 12.7% on the month despite unveiling a long-awaited £220m refinancing that will enable it to complete a three-year recovery plan and resume dividend payments cut in last year’s downturn. The shares have still made a decent 50% rebound this year though.

Also weak were rival Gore Street Energy Storage (GSF), winding-up Aquila European Renewables (AERS) and NextEnergy Solar (NESF), whose 3.6% NAV decline left it close to its 50% debt ceiling.