Decision time

Shareholders in Polar Capital Global Healthcare (PCGH) are being asked to approve a package of measures that repositions the trust for what is hopefully a profitable future. The package – which we describe in detail in this note – includes lower fees, improvements to the trust’s structure, and regular, five-yearly, 100% exit opportunities.

There is also an exit available now. Investors in PCGH need to decide whether they want to continue their investment in the trust. However, hopefully much of the drama of that has been removed by the trust trading close to asset value; sellers have had an opportunity to exit through the market. Regardless, we feel that now is not the time to be exiting a healthcare sector which is both unloved and cheap, yet still showing much promise. If anything, we would be considering adding to positions.

Long-term capital growth from healthcare stocks

PCGH aims to deliver long-term capital growth to its shareholders by investing in a diversified global portfolio of healthcare stocks.

| 12 months ended | Share price total return (%) | NAV total return (%) | MSCI ACWI Healthcare TR (%) | MSCI ACWI total return (%) |

|---|---|---|---|---|

| 31/10/2021 | 31.8 | 24.4 | 21.7 | 30.5 |

| 31/10/2022 | 9.0 | 7.9 | 10.2 | (4.1) |

| 31/10/2023 | (5.6) | (4.4) | (7.3) | 4.8 |

| 31/10/2024 | 24.5 | 21.7 | 13.0 | 26.0 |

| 31/10/2025 | 5.3 | 0.2 | (2.0) | 20.6 |

Fund profile

PCGH aims to generate capital growth through investments in a global portfolio of healthcare stocks which is diversified by geography, industry subsector and investment size.

More information is available on the trust’s website polarcapitalglobalhealthcaretrust.co.uk

PCGH started life in 2010 as Polar Capital Global Healthcare Growth and Income Trust with an issue of ordinary shares and subscription shares. The subscription shares were exercised in full in July 2014 and this distorts the trust’s NAV returns for that early period. In June 2017, the trust was reconstructed and adopted its current name. About 26.3m shares were bought back and 27.8m shares issued around that time.

The team has considerable real-world experience of the pharma and biotech industry

PCGH’s investment manager and AIFM is Polar Capital LLP. The lead managers on the trust are James Douglas and Gareth Powell (more information on the managers is available on page 15). The management team has considerable real-world experience of the pharma and biotech industry, which should help inform their investment decisions.

PCGH’s performance is benchmarked against the total return of the MSCI ACWI Healthcare Index (in sterling).

Liquidity event

An end to PCGH’s fixed life structure

100% tender offer now at NAV less costs

Currently PCGH has a fixed life structure, which – if shareholders do not back these proposals – would mean that the company holds a liquidation vote at its 2026 AGM. The board is hoping to pre-empt that by providing a liquidity event now in conjunction with a number of measures designed to optimise PCGH’s structure. Such measures will require a change to the company’s Articles of Association.

If shareholders approve it, PCGH will hold a 100% tender offer now that will allow shareholders to sell some or all of their shares for cash at a price equivalent to the NAV at the close of business on 27 November 2025 less the costs of providing the tender (including the stamp duty that has to be paid on buying the shares). Those costs will be capped at 1% of that NAV.

Tendered shares can be resold

100% exit opportunities every five years from 2031

Again, providing that shareholders give permission, shares bought back at the tender offer could then be resold at a price below NAV but in any case, above the tender price.

Further 100% tender offers will be provided at five-yearly intervals, with the first of these scheduled to be held on or before 31 March 2031.

PCGH is convening a meeting of its shareholders on 27 November 2025. If you are a shareholder, it is important that you vote your shares. Remember that your investment platform may require you to get your votes in well ahead of the deadline on 25 November.

Resetting the structure

In addition to giving the trust an indefinite life, shareholders are being asked to approve some other changes to the Articles of Association.

- As per the current practice, they formalise that all of the directors will have to submit themselves for re-election at every AGM.

- There are changes to the rules around how general meetings are conducted, permitting, where deemed appropriate, online attendance or even entirely virtual meetings, for example (which would have been useful during the pandemic).

- The rules around how to treat untraceable shareholders and permissions for scrip dividends.

- There are new rules around how US investors may be identified and treated – to avoid falling foul of US securities regulations.

New lower fee arrangement and no performance fee

The manager has agreed to scrap the performance fee and to replace it with a new base management fee structure that introduces a tiered arrangement. The fee would be reduced from a flat 0.75% fee to 0.70% on the first £500m and 0.65% on any balance. The basis for the calculation remains on the lower of PCGH’s market cap and NAV. This is a structure that we favour as it better aligns the manager with shareholders.

Based on the NAV at the end of September 2025 and assuming a 5% discount, PCGH estimates that the new fee structure would have saved shareholders over £212k per annum.

Buybacks to control discount volatility

The regular exit opportunities should be helpful when it comes to PCGH keeping its discount under control. However, the board will also use share buybacks with the aim of managing PCGH’s discount volatility and, to the extent that it can, keeping it at an appropriately narrow level (not defined).

When it comes to managing the portfolio, the investment objective will remain unchanged. One tweak to the investment approach is that the majority of assets will remain invested in large capitalisation companies, with up to 30% of the portfolio invested in small/mid capitalisation companies – those with a market capitalisation below $10bn at the time of investment. This replaces the idea of the trust having distinct growth and innovation pools of investments, where “growth” and “innovation” were defined in part by the size of the company.

The trust will hold up to 65 companies, as before, maintaining its high conviction approach.

Roughly 10% gearing in normal market conditions

The trust will use gearing. This will remain capped at 15% of NAV at the time that it is taken out, but investors should expect gearing to be around 10% in normal market conditions.

Minimum size

Minimum £270m of NAV immediately after tender

At the time of publication, PCGH’s NAV was £494m. The board believes that to be viable the company should have a minimum NAV of £270m following the initial tender. If the tender looks set to shrink the company below this minimum level, the board may decide to withdraw the tender offer and put forward a proposal to liquidate the company instead.

At QuotedData, we think the trust could easily be viable below £270m of assets, but this is the board’s decision, having engaged with shareholders.

PCGH ought to grow rather than shrink

As we set out in the next section, we also think there is a strong case for shareholders hanging onto their existing positions and even considering adding to them.

Market background – sector looks oversold

Figure 1: MSCI ACWI Healthcare index over five years in sterling

Figure 2: Healthcare relative to world index

Source: Bloomberg

Source: Bloomberg, Marten & Co. MSCI ACWI Healthcare Index relative to MSCI ACWI

The sector has trailed a rising market by some distance, fortunately PCGH has outperformed

As Figure 1 shows, the healthcare sector has made only modest progress over the past five years. However, fortunately, as we discuss later in this note, PCGH’s shares have provided about double the return of this index over this period.

The most important story, though, is provided by Figure 2, which shows how the healthcare sector has performed relative to the wider market.

We think that now is not the right time to be thinking about exiting the sector

On all sorts of measures, the sector appears out of favour with investors, and the managers observe that funds flow data backs this up. This is the chief reason why we think that now is not the right time to be thinking about exiting the sector, but – if anything – considering adding to your investment.

The healthcare sector’s problems began when biotech stocks sold off in the wake of rising interest rates. This was coupled with an unwinding of some irrational exuberance that accompanied the success of the COVID vaccines.

More recently, President Trump’s victory in last year’s US elections, his views on drug pricing, the appointment of Robert F Kennedy Junior as Secretary of Health and Human Services, and a slew of Executive Orders that were perceived as negative for the sector have weighed on sentiment. In addition, AI-related plays have sucked money out of the rest of the market.

Biotech valuations – recovery may have begun thanks to a pick-up in M&A

However, in recent weeks, biotech stocks have started to recover, helped by a surge in M&A activity. PCGH has been a beneficiary of this, with bids for Merus and Avidity Biosciences, for example, both of which came at more than 40% premiums to prevailing share prices.

The managers believe that this has a way to run yet. They observe that the industry is highly fragmented. The pharmaceutical sector is facing a sizeable patent cliff as high-selling drugs are approaching the end of their patent lives, at which time they can be displaced by much cheaper generic drugs, or in the case of biological treatments, biosimilars. The pharmaceutical companies are cash-rich but need to find new products to bolster their revenues. They can fill sales pipelines by acquiring promising products developed by cash-strapped biotech companies.

Innovation continues apace and new therapies are being approved

The managers also point out that the pace of innovation is accelerating in both the area of therapeutics and also medical devices. They cite examples such as the success of GLP-1 agonists in obesity, new devices to manage atrial fibrillation, the first approvals of drugs to slow the progression of Alzheimer’s, and new respiratory therapies including for chronic obstructive pulmonary disease (COPD) – more commonly known as smokers’ cough.

What is more, despite fears to the contrary, the FDA is still approving new drugs at about the same rate as it did last year. DOGE cut the FDA’s workforce, but about a quarter of those laid off have since been rehired. The agency is also making use of AI to speed up the approval process.

The political clouds are clearing and/or priced in

The political clouds overshadowing the sector do appear to be clearing, although RFK Junior’s well-known vaccine scepticism continues to be an issue for companies with that focus. The One Big Beautiful Bill cut access to Medicaid and that will have a knock-on effect on demand for healthcare, but that is now factored into valuations.

In May, Trump signed an Executive Order that called for Americans to have access to the most-favoured-nation (MFN) price for drugs. In other words, US citizens would not pay more for their drugs than patients in the G7 countries, Netherlands, and Switzerland. The Order also called for the establishment of a mechanism by which drugs could be sold at those prices direct to consumers.

It is true that US drug prices are often much higher than those in other countries, and this was taken as a major negative for the sector. In September, this was compounded by an announcement that imported brand names and patented pharmaceuticals would face 100% tariffs unless the manufacturer agreed to build a plant to produce these in the US.

However, drug companies have started to reach compromises with the US government on these topics and news of this has contributed to the sector’s recent rally.

Companies are tackling the disparity between US drug prices and those in other countries

Pfizer was the first company to strike a deal with the government. It said that it would implement measures designed to ensure Americans receive comparable drug prices to those available in other developed countries and pricing newly launched medicines at parity with other key developed markets. Revenue earned by selling drugs at higher prices to G7 countries, Netherlands, and Switzerland would be repatriated to the US to help lower drug prices there. Pfizer will also participate in a new direct-to-consumer platform, since christened TrumpRx.gov, that will allow American patients to purchase medicines from Pfizer at a significant discount. Pfizer also secured a three-year grace period during which time it will not face tariffs while it invests in manufacturing in the United States.

AstraZeneca has since made a similar announcement, saying that it will offer MFN prices to Medicaid patients, and will also sell drugs and devices such as asthma inhalers on TrumpRx.

PCGH’s managers say that most large pharmaceutical companies have announced significant investments in US capacity, which should mean that they are excluded from the 100% tariff policy. They think that whilst there may be short-term downward pressure on earnings as a result of the MFN and tariff policies, greater visibility should, in time, lead to improved sentiment and higher multiples in the sector.

Long-term drivers remain intact

Part of the managers’ thesis for their upbeat assessment of the sector’s prospects is a long-term trend of increased utilisation of healthcare services and products. There are a number of underlying drivers that support this, including demographics, emerging market growth, and – shorter term – the ongoing need to clear waiting lists that built up during the pandemic (NHS England says 7.4m patients were waiting to start treatment at the end of August 2025. Pre-pandemic that number was closer to 4m, and in 2009 it was closer to 2m).

Demographics

The world’s population is ageing and, unfortunately, that brings with it increased demand for healthcare. As illustrated in Figure 3, we show that the UN projects that the number of over 75s in North America and Europe is growing: from 31m to 51m in North America and 71m to over 100m in Europe between 2025 and 2040.

That matters because unfortunately this cohort of the population needs far more healthcare than younger generations.

Figure 3: UN population projection data by age and by region 2025–2040

Source: UN Department of Economic and Social Affairs – World Population Prospects 2024

A study published by the UK Health Security Agency in 2019, which drew on data produced by the Office for Budget Responsibility (OBR) highlighted that not only were people living longer, but they were also doing so in increasingly poor health. This puts upward pressure on healthcare costs as Figure 4 shows.

Figure 4: Healthcare spending over an individual’s lifetime

Source: OBR

Economics – the potential within emerging markets

As countries become richer, the proportion of income spent on healthcare tends to grow, although the quantum may be heavily influenced by the choice of healthcare model.

Crucially, a shift in demographics in parts of Asia – notably China – means that the growing population of over 75s is far more pronounced there. Based on the same data that we used to construct Figure 3, the number of over 75s in Asia is projected to grow from 179m to 341m between 2025 and 2040.

Figure 5 breaks down the proportion of GDP spent on healthcare for some of the world’s largest countries by population. While there is the odd exception, there is a clear divide between the developed and emerging world.

Figure 5: OECD data on healthcare spending as a percentage of GDP for selected countries

Source: OECD, data is last available for that country – ranging between 2022 and 2024

Asset allocation

PCGH’s managers have sought to express a number of themes within the portfolio that reflect their outlook for the sector. In addition to innovation, M&A and increased utilisation, which were discussed above, these include:

Access & affordability and the outlook for the market for generics and biosimilars. An annual report produced by the Association for Accessible Medicines in conjunction with the IQVIA Institute suggests that the use of generics and biosimilars has saved the US healthcare system $3.4trn over the past 10 years. These medicines account for 90% of all prescriptions but just 12% of total expenditure on drugs.

Emerging markets where, as discussed above, rising disposable incomes and a growing middle class will translate into higher expenditure on healthcare. The managers cite data from a range of sources that suggests China’s healthcare spending per capita will grow at an annualised rate of 7.7% between 2014 and 2040 and at a rate of 5.5% in India.

Machine learning and artificial intelligence where productivity gains are already being achieved in areas such as diagnostics, radiology, the coordination of care, and robotic surgery. There is more to come as the technology continues to advance. The impact on screening for health conditions and drug discovery could eventually be significant.

Figure 6: Portfolio by sector as at 30 September 2025

Figure 7: Portfolio sector weights relative to benchmark as at 30 September 2025

Source: Polar Capital

Source: Polar Capital

Figure 8: Portfolio by country as at 30 September 2025

Figure 9: Portfolio country weights relative to benchmark as at 30 September 2025

Source: Polar Capital

Source: Polar Capital

At the end of September 2025, there were 34 positions in PCGH’s portfolio, and it had an active share of 75.4% relative to its benchmark. On a market cap basis, 26% of the portfolio was in mega-caps ($100bn+), 49% exposure in large-cap ($10bn–$100bn), 18% in mid-cap ($5bn–$10bn), and 5% in small-cap (under $5bn). About 2% of the portfolio was in cash.

The portfolio has a longstanding underweight exposure to pharmaceuticals (reflecting the potential negative impact of patent expiries) and notable overweight exposures to healthcare equipment and biotech.

Top 10 holdings

Since we last published, using data as at the end of July 2025, Genmab, Teva Pharmaceuticals, Exact Sciences, and Sandoz have moved up into PCGH’s top 10 holdings to replace Argenx, Intuitive Surgical, United Health Group, and Ascendis Pharma.

Figure 10: PCGH 10-largest holdings as at 30 September 2025

| Stock | Sector | Country | % at 30/09/25 | % at 31/03/25 | % change |

|---|---|---|---|---|---|

| Eli Lilly | Pharmaceuticals | United States | 7.1 | 8.8 | (1.7) |

| AstraZeneca | Pharmaceuticals | United Kingdom | 6.1 | 4.6 | 1.5 |

| Abbott Laboratories | Healthcare equipment | United States | 5.0 | 4.0 | 1.0 |

| UCB | Pharmaceuticals | Belgium | 3.8 | 3.7 | 0.1 |

| Genmab | Biotechnology | Denmark | 3.6 | – | 3.6 |

| Thermo Fisher Scientific | Life sciences tools and services | United States | 3.4 | – | 3.4 |

| Teva Pharmaceuticals | Pharmaceuticals | Israel | 3.3 | – | 3.3 |

| Sandoz | Pharmaceuticals | Switzerland | 3.3 | 2.2 | 1.1 |

| Exact Sciences | Biotechnology | United States | 3.2 | 1.6 | 1.6 |

| Edwards Lifesciences | Healthcare equipment | United States | 3.1 | – | 3.1 |

| Total | 41.8 |

Genmab (genmab.com) is a biotechnology company with a focus on antibodies and their use to tackle areas of disease (primarily in oncology). It has two approved products – one focused on metastatic cervical cancer and the other on lymphoma – seven in Phase 3, five in Phase 2, seven in Phase 1, and a number of pre-clinical programmes.

Teva Pharmaceuticals (tevapharm.com) has a strong presence in generics and biosimilars, and is redeploying cash flow into developing its own new therapeutics. Newer products – including a therapy for tardive dyskinesia and chorea associated with Huntingdon’s disease, one targeted at preventing migraines, and another for schizophrenia – are helping to drive revenue growth.

Exact Sciences (exactsciences.com) is developing tests to improve cancer diagnosis, including tests for colorectal and breast cancer.

Sandoz (sandoz.com) is a leading player in generics and biosimilars. Third quarter figures released at the end of October showed mid-single-digit revenue growth (a trend that it expects to persist for the full year), helped by growing sales of biosimilars, which account for 30% of its sales. Full year margins are expected to be 21%–22%.

Relative positioning

In addition, PCGH’s managers have supplied us with data on the 10-largest under- and overweight exposures in the portfolio relative to the benchmark. The list of underweights reflects PCGH’s bias away from large cap US pharmaceuticals, many of which are the companies plagued by the patent cliffs that we discussed earlier, and some of which are exposed to the pressure on drug pricing related to the US government’s MFN pricing policy.

Figure 11: Top 10 overweights

| Stock | % at 30/09/25 |

|---|---|

| UCB | 3.35 |

| Genmab | 3.35 |

| Exact Sciences | 3.16 |

| AstraZeneca | 3.02 |

| Teva Pharmaceutical | 3.00 |

| Sandoz | 2.97 |

| Penumbra | 2.87 |

| Centene | 2.85 |

| Ascendis Pharma | 2.85 |

| H Lundbeck | 2.80 |

| Total | 30.23 |

Figure 12: Top 10 underweights

| Stock | % at 30/09/25 |

|---|---|

| Johnson & Johnson | (5.81) |

| AbbVie | (5.33) |

| UnitedHealth | (4.08) |

| Roche | (3.13) |

| Novartis | (3.12) |

| Merck & Co | (2.75) |

| Amgen | (1.98) |

| Pfizer | (1.89) |

| Boston Scientific | (1.88) |

| Gilead Sciences | (1.80) |

| Total | (31.76) |

Most of these stocks have been discussed in this or prior notes (see page 17 for a list of these). Two we would highlight this time as they are relatively new entrants to these lists are Penumbra and Centene.

Penumbra

Figure 13: Penumbra (USD)

Source: Bloomberg

Penumbra (penumbrainc.com) is a medical device company that is focused primarily on cardiovascular and neurovascular conditions. Its products are used for procedures such as the removal of clots (thrombectomy) and stopping bleeding. It is bringing a number of new products to market

Third quarter results show year-on-year revenue growth of 21%. Gross margins of 67.8% for the quarter are targeted to exceed 70% next year. The company guided towards full year sales just shy of $1.4bn (up about 15% on the prior year). In PCGH’s interim results, the managers said that the mechanical thrombectomy market is one of the fastest growing areas of the healthcare equipment market, with Penumbra being one of the leading players in this field.

Centene

Figure 14: Centene (USD)

Source: Bloomberg

Centene (centene.com) is a US managed healthcare company, providing access to services for Medicare and Medicaid patients as well as privately insured patients. Services include care provision for people with age-related and chronic conditions, and those with disabilities. Centene also operates speciality pharmacy services, dental care plans, opticians, and clinical support services.

The PCGH managers feel that, after a period of margin and earnings pressure, a possible rerating could be driven by a faster-than-expected operational recovery for Centene.

Performance

Figure 15: PCGH NAV total return performance relative to benchmark over five years

Source: Bloomberg, Marten & Co

In our view, PCGH’s managers have done a great job of navigating a difficult environment for the sector and Figure 15 illustrates that.

Figure 16: Total return performance for periods ending 31 October 2025

| 3 months (%) | 6 months (%) | 1 year (%) | 3 years (%) | 5 years (%) | Since 31 July 2019 (%) | |

|---|---|---|---|---|---|---|

| PCGH price | 16.9 | 18.0 | 5.3 | 23.7 | 77.7 | 77.2 |

| PCGH NAV | 14.7 | 13.1 | 0.2 | 16.5 | 56.4 | 66.5 |

| Benchmark | 9.7 | 5.8 | (2.0) | 2.7 | 37.7 | 50.3 |

| MSCI ACWI | 9.4 | 23.8 | 20.6 | 59.3 | 99.4 | 103.4 |

| NASDAQ Biotech | 21.3 | 28.5 | 13.9 | 17.0 | 34.2 | 57.4 |

In recent months, PCGH has benefited from some of the M&A that has been going on in the biotech sector and the start of improving sentiment towards the sector. The managers are optimistic about the future.

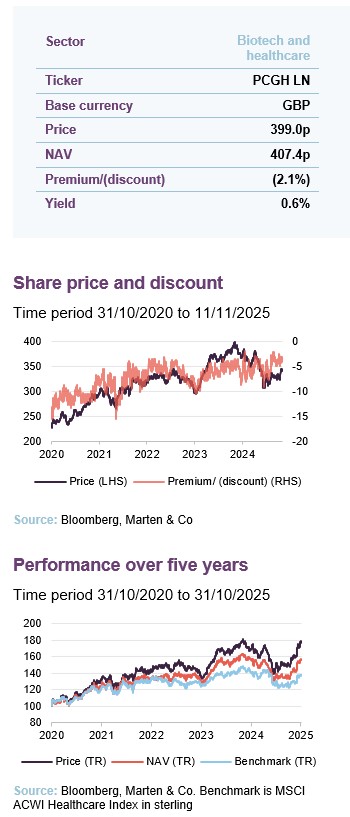

Premium/(discount)

Over the 12 months ended 31 October 2025, PCGH’s discount moved within a range of 9.1% to 1.0% and averaged 4.6%. At 11 November 2025, PCGH was trading on a discount of 2.1%.

Figure 17: PCGH premium/(discount) over five years

Source: Bloomberg, Marten & Co

PCGH’s sector-leading long-term returns (it has the highest 10-year returns of any trust in the AIC’s biotechnology and healthcare sector over the past 10 years) ought to be enough to merit a high rating. The current exit opportunity and those planned for the future are a help too.

PCGH’s plan to use share buybacks to modify discount volatility should also help keep the discount within a relatively narrow range going forward.

At each AGM, PCGH shareholders are asked to approve the issuance of up to 10% of its share capital and the repurchase of up to 14.99%.

Managers

PCGH’s co-managers are James Douglas and Gareth Powell. They form part of an eight-strong team.

Gareth Powell

Gareth joined Polar Capital in 2007 to set up the Healthcare team. Prior to Polar Capital, he worked at Framlington, where he began his career in investment management in 1999. Soon afterwards, he joined the Healthcare Team and helped launch the Framlington Biotech Fund, which he managed from 2004 until his departure.

Gareth took a Masters in Biochemistry at Oxford, during which time he worked at Yamanouchi, a leading Japanese pharmaceutical company (later to become Astellas). As well as this, he worked for the Oxford Business School and various academic laboratories including the Sir William Dunn School of Pathology and the Wolfson Institute for Biomedical Research.

Gareth is a CFA Charterholder.

James Douglas

James joined Polar Capital in September 2015 and was appointed co-manager for PCGH in August 2019.

James has 24 years’ experience having worked in equity sales specialising in global healthcare at Morgan Stanley, RBS and HSBC, prior to joining Polar Capital. He also has equity research experience garnered from his time at UBS, where he worked as an analyst in the European pharmaceutical and biotechnology team. Before moving across to the financial sector, James worked as a consultant for EvaluatePharma.

James has a PhD and BSc (1st Class Hons) in Medicinal Chemistry from Newcastle University. He also holds the ACCA diploma in financial management (DipFM).

Deane Donnigan

Deane joined Polar Capital in June 2013 and is the lead manager of the Polar Capital Healthcare Discovery Fund.

Prior to joining Polar Capital, she began her career at the Medical College of Georgia, before becoming a clinical specialist in Drug Information and Adult Internal Medicine with Emory University Hospital in Atlanta, Georgia. After several years, she moved to the UK to join Framlington (now AXA Framlington) as an analyst for the healthcare unit trust, led by Anthony Milford. She went on to become lead portfolio manager of the Framlington Healthcare and Framlington Biotechnology funds. Deane is both a US and UK citizen.

Deane is a Doctor of Pharmacy (PharmD), Clinical Pharmacy, University of Georgia in conjunction with the Medical College of Georgia. She is also a board-certified and licensed pharmacist, ACCP board certified pharmacotherapy specialist, and is IMRO qualified.

David Pinniger

David joined Polar Capital in August 2013 as a portfolio manager within the Healthcare team, to launch the Polar Capital Biotechnology Fund. Prior to joining Polar Capital, David was portfolio manager of the International Biotechnology Trust at SV Life Sciences.

Previously, David spent three years working at venture capital firm Abingworth as an analyst managing biotechnology investments held across the firm’s venture and specialist funds, and four years at Morgan Stanley as an analyst covering the European pharmaceuticals and biotechnology sector.

David has a BA (1st Class Hons) in Human Sciences from the University of Oxford and is a CFA Charterholder.

Brett Pollard

Brett joined the Polar Capital Healthcare team in September 2021 and has 24 years of healthcare industry experience, 15 of which have been in healthcare investing.

After completing a PhD in Molecular Virology at the University of St. Andrews, he worked as a healthcare research analyst, covering stocks in pharmaceutical, biotechnology, medical device, and healthcare service subsectors. In 2008, he co-founded an in vitro diagnostics business where he initially led corporate and business development before taking on the role of chief operating officer.

After time spent in strategic advisory services, Brett moved back into corporate development and investor relations’ roles before joining the Polar Capital Healthcare team. His extensive industry and investment experience has allowed him to rapidly build up detailed coverage of the healthcare sector in emerging markets.

Brett studied cell and molecular biology at the University of St. Andrews, and has a PhD in molecular virology.

Tara Raveendran

Tara joined Polar Capital in September 2021 as a consultant focused on independent research for the team. Prior to joining Polar Capital, she was the head of Healthcare & Life Sciences Research at Shore Capital.

Previously Tara spent over 15 years working in equity research, specialising in European pharmaceuticals, biotechnology and medtech at Lehman Brothers and Jefferies. She has also worked with a number of healthcare-focused start-ups through her life sciences consultancy, SSquared Consulting, most recently working with the UK government’s Vaccine Taskforce.

Tara has a BSc in Biochemistry and a PhD in Structural Biology from Imperial College, London.

Leanne Smith

Leanne joined the Polar Capital Healthcare Team as an investment analyst in October 2024. She started at the company in 2021 in the Client Services team as part of the Investment 20/20 scheme. Leanne has a BA in Cells and Systems Biology from the University of Oxford and has passed Level 1 of the CFA.

Damiano Soardo

Damiano joined the Polar Capital Healthcare team as an investment analyst in October 2020. He started at the company in 2016 as part of the operations team before moving to the risk team in 2019. Prior to joining Polar Capital, he worked as a technical consultant at a fintech company. Damiano has an MSc in Mathematics and Foundations of Computer Science from the University of Oxford and is a CFA Charterholder.

Previous publications

Readers interested in further information about PCGH may wish to read our earlier notes. You can read the notes by clicking on them in Figure 18 or by visiting our website.

Figure 18: QuotedData’s previously published notes on PCGH

| Title | Note type | Publication date |

|---|---|---|

| Healthy returns and a rosy outlook | Initiation | 5 March 2024 |

| Vital signs are good | Update | 14 November 2024 |

| Recovery Play | Update | 20 August 2025 |

IMPORTANT INFORMATION

This marketing communication has been prepared for Polar Capital Global Healthcare Trust Plc by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and, if you are not a professional investor, or in any other way are prohibited or restricted from receiving this information, you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it, but in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.