A leading biotech investor

BB Biotech is the oldest-established, the largest and, over the longer term, one of the best-performing of the small group of closed-end funds that specialise in the biotech sector. It offers investors a vehicle to gain exposure to a focused portfolio of predominantly-US small-to-mid-cap biotech companies developing therapeutic products, with a strong bias towards cell, gene and particularly RNA-based technologies.

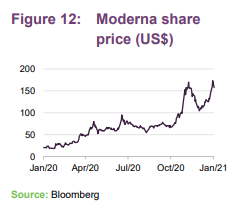

The company has a consistent 27-year record of outperformance against the broad US biotech indices and aims to deliver its shareholders at least a 15%/year growth in capital, including a 5% dividend per year. It has met this target comfortably over the past 10 years with a 17%/year compound return in share price (excluding dividends), which equates to 26% on a total return basis. Performance in 2020 was driven, in part, by an investment in Moderna, whose stock price rose more than five-fold last year on the back of the rapid and successful development of its COVID-19 vaccine (mRNA-1273).

High conviction, fundamental and long term

BB Biotech is a high-conviction, fundamental and long-term investor that offers investors direct access to a select portfolio of promising, fast-growing and profitable biotech companies listed on stock markets around the world, but with a strong bias to the US. BB Biotech aims to deliver a compound total return of at least 15% per year with an annual dividend equivalent to 5% of NAV.

| wdt_ID | Year ended | Share price TR (%) | NAV TR (%) | Nasdaq Biotech Index (NBI) TR (%) | MSCI World Healthcare TR (%) | MSCI World TR (%) |

|---|---|---|---|---|---|---|

| 1 | 31 Jan 2017 | 20.60 | 14.90 | 1.30 | 0.70 | 14.20 |

| 2 | 31 Jan 2018 | 38.40 | 22.20 | 16.70 | 17.20 | 19.20 |

| 3 | 31 Jan 2019 | 0.30 | -4.40 | 2.90 | 9.30 | 0.20 |

| 4 | 31 Jan 2020 | -0.90 | -3.70 | 1.00 | 12.70 | 14.90 |

| 5 | 31 Jan 2021 | 34.00 | 43.60 | 31.50 | 8.10 | 7.20 |

Fund profile

BB Biotech is a large ($5.7bn market cap) Swiss-domiciled investment company with a concentrated portfolio of shareholdings in predominantly US-based and/or Nasdaq-listed biotech companies. It was launched in 1993 and is both the largest and longest-established of the dozen or so closed-end funds that specialise in the biotech/pharma sector that are listed on European and US stock exchanges.

In terms of style, BB Biotech is a high-conviction, fundamental and long-term investor. It is also a long-only investor; i.e. it is not a hedge fund and does not use financial instruments to reduce individual stock or market risk (in contrast to one of the other biotech specialists within its peer group).

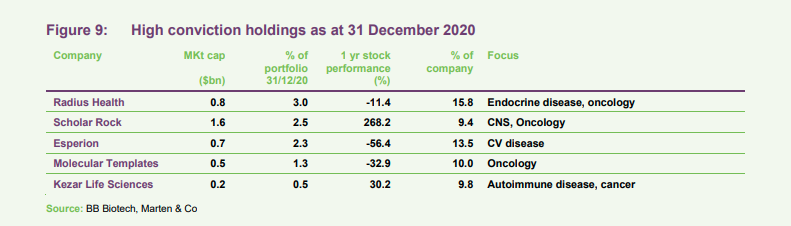

BB Biotech invests across the small-to-mid-cap spectrum of the US biotech sector and does so exclusively in human therapeutic companies (thereby excluding med-tech, diagnostics and other activities that may be included in a broader definition). This means it has an investment universe of around 300 companies.

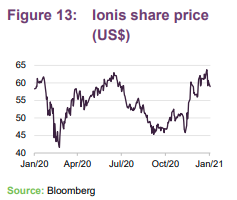

Its portfolio holdings are often individually large and there is a strong bias towards companies with cell, gene and particularly RNA-based technologies. Notably, some of its largest investments are in companies exploiting different RNA-based technologies – Moderna and Ionis Pharmaceuticals– and these together make up more than 17% of its portfolio value.

The portfolio is highly concentrated with just 35 holdings, many of which have been held for a number of years. BB Biotech makes a relatively small number of new investments each year, usually around six, and does so only after an extensive due diligence process (detailed further down). Individual holdings in the portfolio can be material both in terms of the portfolio value (up to 10% of NAV currently, although even higher figures have occurred at times) and the investee company (up to 15% of equity).

The manager believes that the portfolio concentration, investment strategy and practice of maintaining holdings over extended periods offers the opportunity to achieve differentiated returns if investee companies’ development activities are successful. Often an exit can come about through the investee company being acquired.

Financially, BB Biotech aims to deliver at least a 15%/year total return – a target it has met over the past 10 years, with 17% compound (CAGR) growth in its share price – in addition to an annual dividend equivalent to 5% of NAV.

BB Biotech has its primary listing on the Swiss Stock Exchange (SIX: BION), with secondary listings on Borse Frankfurt (BBZA GY) and Borsa Italia (BB IM), the latter two being denominated in Euros.

It has been run since its inception by Bellevue Asset Management, a boutique biotech investment manager with a team of experienced analysts and portfolio managers based in Zurich and New York. The lead manager, Dr Daniel Koller, has been in place since 2010 and heads a team of seven specialist investment analysts.

Investment strategy

BB Biotech’s investment strategy is to acquire positions in what it believes are promising companies at the early clinical stage (often in the $1–5bn market cap range) and hold these over an extended period (five to six years on average), adding or reducing in response to developments, but ultimately with the aim of capturing the value created as investees develop products successfully and evolve into commercial entities. Such investments are made usually initially made in the secondary market (possibly in a secondary offering), although BB Biotech has at times invested in IPOs.

If the investee company’s development activities are successful, smaller holdings will grow into larger ones and over time may eventually become core holdings (companies that typically have reached market capitalisations of $10–20bn or more). Given their substantial portfolio weightings, the usually five to eight core positions are expected to be mature companies, generating both revenue and income.

BB Biotech expects to make modest reductions in its core holdings over time as the opportunity arises to provide capital to make new investments. Currently, BB Biotech considers six of its investments to be core holdings, which account for 40% of the portfolio value.

The portfolio can have between 20 and 35 holdings and in recent years has been towards the upper end of this range. Large core positions will be taken in five to eight companies, the top holdings, which must account for no more than two-thirds of the portfolio and no single position should have a weighting greater than 25%. Currently the largest two each represent around 10% of the portfolio value.

Binary events

As a long-term investor with large individual equity stakes, BB Biotech is inevitably exposed to the binary events – typically the outcome of late-stage clinical trials or interactions with regulatory agencies – that occur in its larger holdings. These are a normal phenomenon in biotech and can cause large share price changes for the companies involved – often 50% or more if positive, or falls of as much as 70% if negative – although the relative magnitude would tend to be smaller for larger, more diversified companies.

In contrast to some peer group funds, BB Biotech does not pursue a risk mitigation strategy designed to avoid holding companies through their binary events. On the contrary, it sees these as part of its investment process. Moreover, it has achieved a good record with such events in recent years.

Last year, for example, there were 11 potential US regulatory approvals within the portfolio, 10 of which occurred as planned (the only negative one being the FDA’s rejection of Intercept Pharmaceuticals’ application in non-alcoholic steatohepatitis). This ratio has been consistent over at least the last three years, with 10 of 11 possible approvals obtained in 2019, and 10 of 12 in 2018.

Investment restrictions

BB Biotech’s structure requires it to have at least 90% of its shareholdings in listed companies (thus 10% may be in private companies, although currently there are none in the portfolio). It is also required to have more than 50% of its assets in equity investments, although in practice this is usually close to or at 100%. BB Biotech can invest in other types of security, such as corporate bonds or traded options, but in practice it sees common equity as being preferable for liquidity and risk/return reasons.

BB Biotech does have two minor holdings in the form of Contingent Value Rights (securities that make a fixed payment if certain future milestones are met). These were issued in connection with acquisitions and both were indeed obtained in this way (rather than being acquired in the market). One has technically expired, having failed to meet a regulatory deadline in 2020 (albeit mainly as a result of the pandemic); this may, however, have some residual value as the outcome is widely expected to be litigated.

Foreign exchange exposure

As a Swiss legal entity, BB Biotech’s reporting currency is the Swiss franc. As it invests exclusively in US dollar-denominated securities and, as a policy, does not make use of financial instruments to hedge currency, BB Biotech’s investors should be aware that currency movements (particularly USD-CHF) will have an impact on its NAV (and hence, indirectly, on the share price).

The Swiss franc strengthened against the dollar in the last quarter of 2020, having been relatively stable (between CHF0.9-1.0) over most of the 2010–2020 period, (the Swiss franc also strengthened appreciably in the first decade of the 2000s). A rise in the Swiss Franc relative to the dollar reduces the translated value of US dollar assets, and so tends to depress NAV. However, US healthcare/biotech stock prices also tend to benefit from a weaker dollar (because of translation of ex-US earnings), so there is some natural offset to this impact.

Currency movements can also affect the value in local currency of BB Biotech shares held by non-Swiss investors. Over the long term, the Swiss currency has appreciated against both sterling and the Euro (the latter having declined from broadly CHF1.5–1.6 between 2000 and 2010 to CHF1.1–1.2 between 2010 and 2020). This means that the share price return in domestic currency for UK and Eurozone investors over these longer periods will have been higher than for that of investors based in Switzerland.

Note: For simplicity, Marten & Co will use CHF in this report, as BB Biotech’s reporting currency and that of its primary listing.

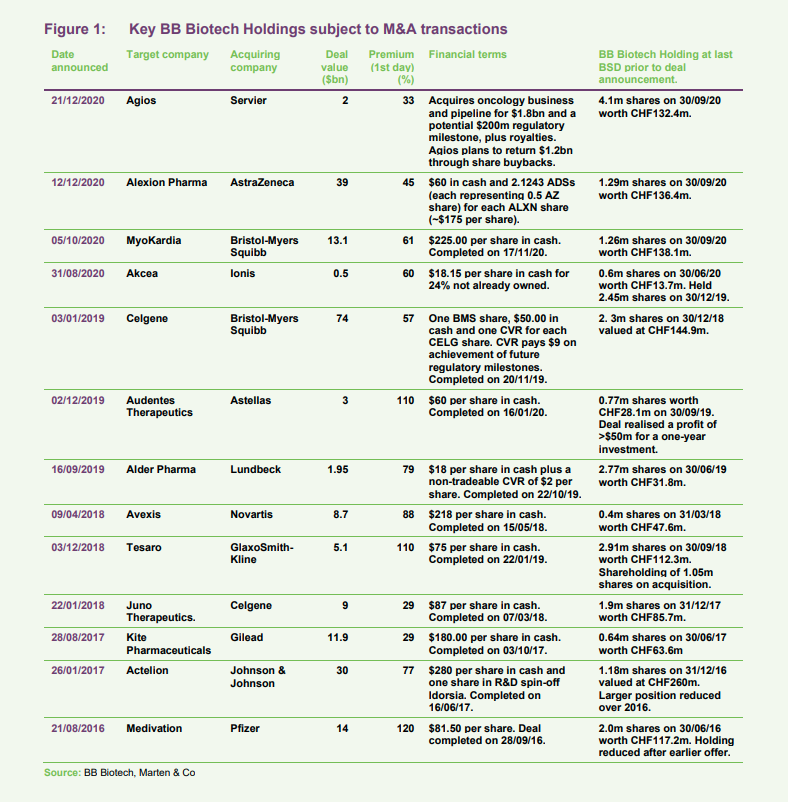

M&A as liquidity events

BB Biotech’s long-term horizon means that liquidity events in its portfolio can often come about through industry M&A. One such example that occurred last year was MyoKardia, in which BB Biotech first invested in 2018. This company was acquired by Bristol-Myers Squibb last year at a valuation which represented a more than three-fold increase over two years.

Marten & Co has identified 13 M&A transactions involving BB Biotech holdings that have occurred or announced over the past five years, which is a relatively high proportion given the size of its portfolio. This is perhaps a reflection of the fact that BB Biotech’s investment approach would tend to select companies that, if their therapeutic development activities are successful, are likely to become M&A targets for large-cap pharma or biotech companies.

The premiums paid in such transactions tend to vary between 30–100% on the day of the announcement, and in all cases the investments have delivered significant positive returns for BB Biotech. Marten & Co estimates the deals involving MyoKardia and Audentes, for example, (two of the more recent transactions) to have achieved cash returns for BB Biotech in excess of 245% and 181% respectively, based on the share price at the quarter-end when the investment was first made.

Furthermore, at least four of BB Biotech’s current holdings have been tipped by sell-side analysts as being possible M&A targets in 2021 (Radius Health, Sage, Scholar Rock and Intercept).

Liquidity

BB Biotech’s shares are liquid and also appear to be less volatile on a daily basis than its NAV.

Transparency/IR

BB Biotech is transparent about its investments and aims to be professional and investor-friendly in terms of its IR activities. For example, it publishes its entire portfolio with a commentary quarterly as well as its NAV in CHF and Euro daily. The trust’s website and investor materials (which include news updates and investor presentations) are made available in English, German and Italian, with three IR professionals each dedicated to one of these language-based regions. One of the IR professionals is based in London and is having an ongoing and close dialogue with the company´s growing UK investor base.

Unusually for an investment company, it also offers a mobile app that can be used to access daily share price, trading information and other investor updates.

Investment process

BB Biotech identifies and selects potential investments via a thorough, multi-level due diligence process. This places a particular focus on the analysis of financial parameters, the competitive environment, the development pipeline, IP and the perception/perspectives of end-users (prescribing doctors and patients).

Like other biotech specialist investors, Bellevue’s analysts gain insights from attending (albeit virtually at the moment) the important industry meetings (particularly investment banking and key medical conferences) and holding virtual meetings with current and potential investee company managements. Bellevue has access to sources of primary market research, sell-side research and data aggregators (Bloomberg etc), and can obtain input from key opinion leaders (doctors considered to have in-depth experience in specific fields) in the course of making investment decisions. It can, of course, also draw upon in-house expertise with the team in various disciplines.

These interactions allow the team to identify companies and profile them in relation to their competitors. The firm actively monitors news from portfolio companies and their competitors, as well as general industry developments. The investment process includes qualitative judgements, based on the expertise of the team, of the quality of management and views of the sell-side/buy-side (i.e. analysts and other investors).

New investments are likely initially to have a weighting of between 0.5% and 4% of portfolio value, which is designed to balance upside potential with R&D risk. Often BB Biotech will increase the initial holding over time, as the investee companies’ products advance through clinical development and can increase portfolio weightings as a position increases in value. Thus, smaller positions can become a core holding if the business develops and milestones are achieved as expected. All positions and valuations are continuously monitored, taking into account their growth potential and other aspects, and will be reduced if and when it is deemed necessary to do so.

New investments

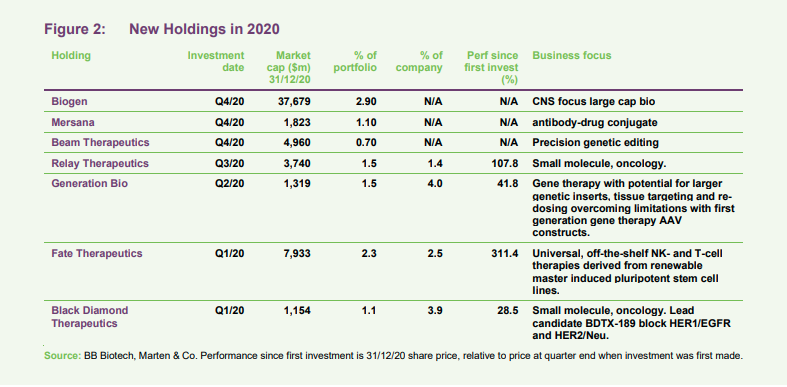

BB Biotech makes a small number of new investments each year. Over the past three years, it has made a total of 19 new investments: seven in 2020, five in 2019 and seven in 2018.

The new holdings added to the portfolio last year were in Relay Therapeutics, Generation Bio, Fate Therapeutics, Black Diamond Therapeutics, Mersana, Beam Therapeutics and Biogen. All but one (Mersana), have shown a positive share price return to date, with Fate Therapeutics being a particular standout with a more than three-fold rise.

The investment in Biogen is described as a tactical one, effectively BB Biotech’s managers believe there is a better chance of approval of the company’s Alzheimer’s treatment aducanumab that is reflected in the current share price. Furthermore, as a large cap bio, Biogen would normally fall outside the company’s investment universe, but it sees this as a special situation. The market has been very sceptical of aducanumab’s chances of gaining approval, but the manager thinks that this may be changing after the FDA recently requested addition time to complete its review. A decision must now be rendered by the agency by 7 June 2021.

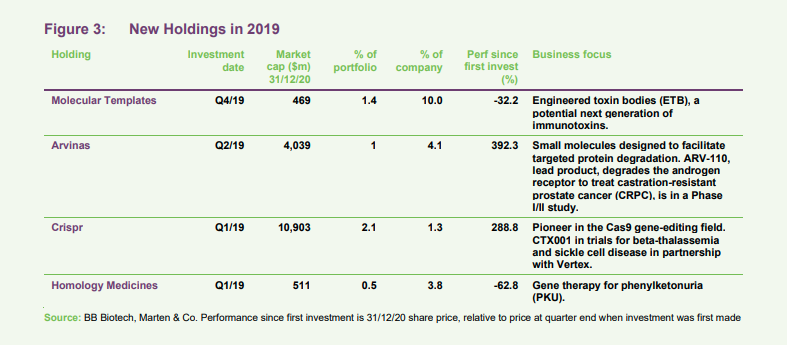

Five investments were made in 2019: Molecular Templates, Arvinas, Crispr, Homology Medicines and Argenx, the latter which has more than doubled in size over two years and already become a core holding. However, for this cohort, the performance data are more mixed, but perhaps also more representative of the risk/reward inherent of investing in early-stage biotech: three are positive, two strongly so, but two are negative, having encountered difficulties or seeing a competitive position erode.

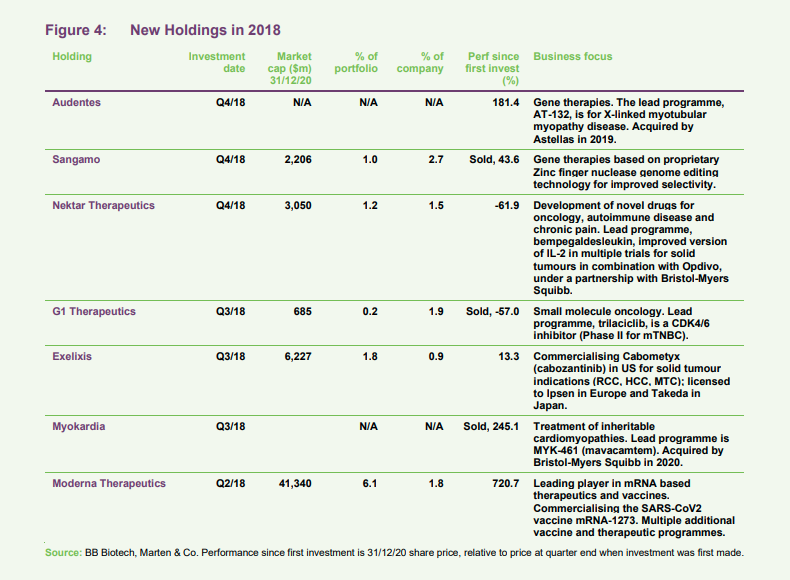

In the fourth quarter of 2020, BB Biotech exited from two companies that had been new investments in 2018, Sangamo and G1 Therapeutics, citing changes to the investment case. The Sangamo position was closed with a 43% return, while the G1 returned -57%.

Manager’s comments/macro view

Bellevue’s Dr Daniel Koller notes the rally in biotech in late 2020, and attributes this to the sector having acquitted itself well in the COVID-19 pandemic, with the successful development of a number of therapeutics and in particular the vaccines.

BB Biotech believes that 2020 saw strong operational progress in many of the portfolio holdings, and a pick-up in M&A activity with AstraZeneca´s takeover of Alexion, and Servier acquiring the oncology franchise of Agios – both BB Biotech holdings – being announced in December.

The manager thinks that markets expect the incoming Biden administration to pursue a centrist approach, which may limit the ambitions of any reform of the US healthcare system. Even though Democrats will effectively control the Senate as well as the House of Representatives, and have the power to choose which health care proposals reach a vote in Congress, the 50-50 split in the Senate (with Vice President Kamala Harris potentially exercising a tiebreaker vote) means that it requires bipartisan support to pass plans and prevent filibustering. This is thought likely to make it difficult to undertake some of the more ambitious health care proposals, such as offering Americans a government-sponsored public insurance option.

Market background on biotech

Biotech stocks enjoyed a remarkable boom in 2020, and a number of closely-watched indicators broke new records.

The two main biotech stock indices (NBI and XBI) are trading close to record levels, despite both – alongside stock markets generally – having seen a c.30% fall between 21 February and 17 April last year, as the world entered the first lock-down.

2020 saw a record number of biotech IPOs – between 70 and 84, depending on definition – but either way, more than twice that of 2019 or 2018, the latter having the highest number (35) of any of the past 10 years. There was also a record performance in terms of first-day closing price rise for IPOs (+45% on average).

2020 also saw 53 drug approvals in the US, which is the second highest number of any calendar year in the past decade (2018 had 58). The impact of the pandemic on the FDA’s working practices meant that a number of approval decisions were deferred into 2021 for pandemic-related reasons (lockdowns, inability to inspect manufacturing facilities etc).

Asset allocation

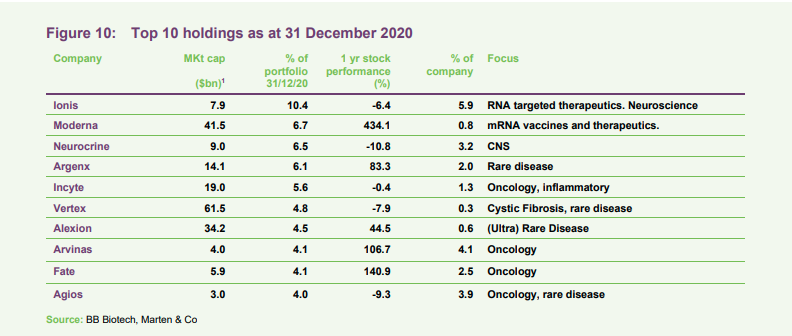

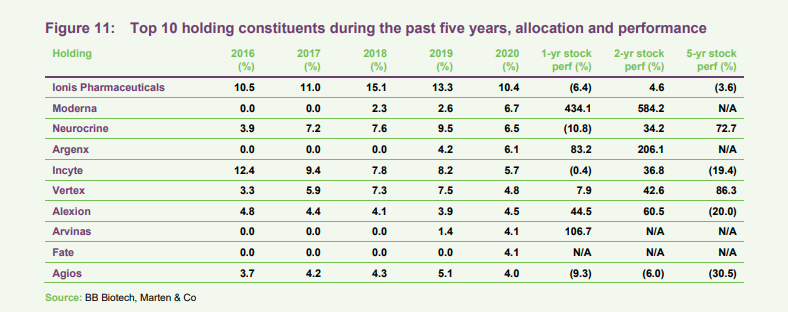

As at the end of December 2020, BB Biotech had 35 holdings, with the top 10 holdings represented 56.9% of portfolio value and the top 20, some 85.4%.

The six “core” holdings of Moderna, Ionis, Neurocrine, Incyte, Vertex and Argenx represented 40% of the portfolio value.

With the exceptions of Moderna and Argenx, whose stock rose by 87% in 2020, the other core holdings saw relatively flat performance last year. BB Biotech reduced its holdings in five of its six core holdings in 2020, with that of Ionis Pharma alone increasing through the share exchange buy-out of minority investors of its formerly part-owned subsidiary Akcea (which was also a holding).

Top 10 holdings

Marten & Co has identified five high-conviction holdings within the portfolio, where the shareholding represents a large (>9%) stake in the company’s equity. Performance of these was varied in 2020. Esperion, which has previously been a top 10 holding, for example, has seen its share price come under pressure as it struggled to market its cardiovascular product in the pandemic. By contrast, Scholar Rock has seen a three-fold rise.

Top 10 holdings over the past five years, with share price performance, are shown in the table below.

Figure 11 shows how the weightings in the 10-largest holdings as at the end of 2020 have evolved over the past five years.

Core holdings

The six core holdings are profiled in more detail below.

Moderna

Moderna (moderna.com) is the industry leader with the broadest development pipeline in the field of mRNA therapeutics, with a pipeline of therapeutics in oncology and vaccines for cancer and viral diseases. It has become famous for its development of mRNA-1273, one of three COVID vaccines that have received emergency use authorisation in Western markets. The company’s stock rose five-fold in 2020 and peaked at $170/share on 8 December. However, it has been volatile since, and has come off as some investors have taken profits. The company expects to deliver 600m doses of its COVID-19 vaccine and has signed $11.7bn worth of advanced purchase agreements with governments around the world to supply the vaccine this year.

Ionis Pharmaceuticals

Ionis Pharmaceuticals (ionispharma.com) is the leader in anti-sense mRNA drugs. It has three approved products: Spinraza (nusinersen, sold by Biogen), for spinal muscular atrophy; Tegsedi (inotersen), which it markets itself, for hereditary transthyretin amyloidosis; and Waylivra, approved in Europe for familial chylomicronaemia syndrome (FCS) and sold in collaboration with Swedish Orpham Biovitrum.

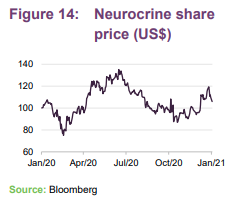

Neurocrine

Neurocrine (neurocrine.com) is a commercial-stage neuroscience-focused company with two marketed products – Ingrezza (valbenazine), for tardive dyskinesia, and Ongentys (opicapone) for Parkinson’s disease. 2020 revenues of Ingrezza are c.$993m, with key data from a Phase III trial in chorea in Huntington’s disease due in Q4 this year. The shares underperformed in the second half of 2020, as a result of difficulties commercialising products during the pandemic.

Incyte

Incyte (incyte.com) is a small molecule development/marketing company with interests in oncology and inflammatory disease. It generates $2bn/year in revenues, largely (~85%) from Jakafi for myelofibrosis, and has just raised its long–term sales guidance to $3bn (from $2.5bn) to reflect new indications and competitive changes. The stock underperformed last year as investors appeared to become increasingly concerned by the over-reliance on Jakafi and the company’s mixed success in with other compounds in late-stage R&D. The company has recently signed a collaboration agreement with Morphosys for tafasitamab, which is under regulatory review for diffuse large B-cell lymphoma.

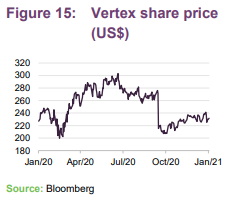

Vertex

Vertex (ptcbio.com) is focused on developing therapies for rare diseases. The company has become the industry leader in products for cystic fibrosis and has a growing portfolio in other rare diseases, including Alpha-1 antitrypsin deficiency, sickle cell disease and beta-thalassaemia. The stock price has soared apparently on strong sales of its Trikafta combination therapy for cystic fibrosis Its stock rose by 8% in 2020.

Argenx

Argenx (ir.exelixis.com) is the only non-US based company (it is based in Belgium), although listed on Nasdaq. It has been one of the best investments for BB Biotech, after Moderna, on the back of an 83% stock price rise in 2020. The company’s core product, efgartigimod, is an unusual “pipeline-in-a-drug” opportunity in autoimmune/neurology, with potential in generalised myasthaenia gravis (filed), followed by immune thrombocytopaenia and pemphigus vulgaris in Phase III, chronic inflammatory demyelinating polyneuropathy (Phase II) and a fifth indication expected to be disclosed soon. Argenx has just announced a successful interim review of its study in chronic inflammatory demyelinating polyneuropathy and proposed a $750m stock offering.

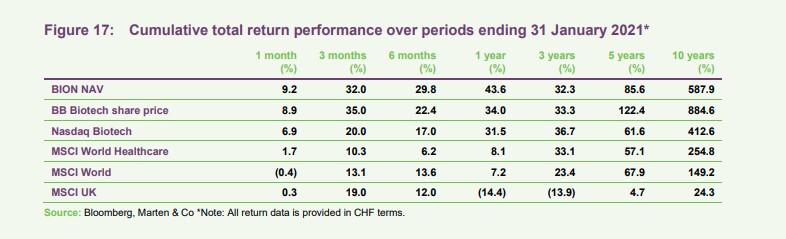

Performance

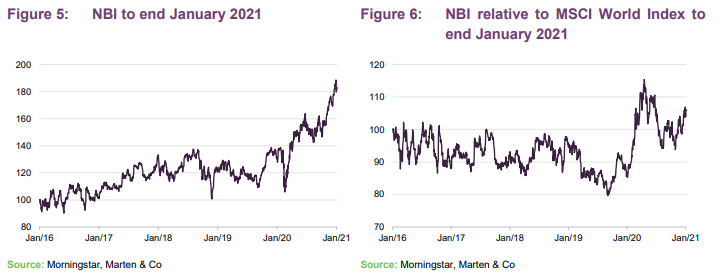

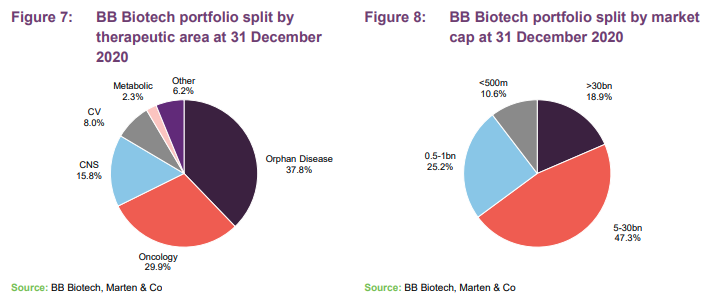

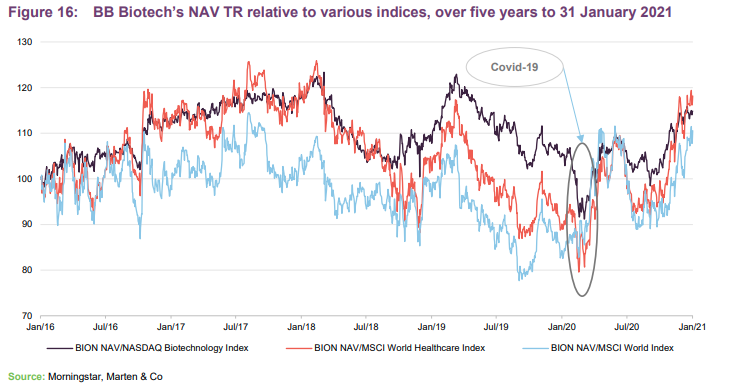

BB Biotech has a long record of out-performance against biotech market indices, such as the Nasdaq biotechnology index (NBI), although its investment performance is not formally benchmarked against this. The NBI is a broad, non-capitalisation weighted index of c290 biotech stocks (recently increased from 200) and is one of several commonly used proxies for biotech market as a whole. Furthermore, the biotech sector has itself outperformed almost all other stock market segments (except technology) over the period of the fund’s existence.

From inception to the end of 2020, BB Biotech returned 2,849% in terms of share price, equivalent to 13.3% compounded (2,585% and 12.9% in terms of NAV).

Performance in 2020

In 2020, the trust achieved a 24.3% total return in NAV in total return terms and a 19.3% total return in share price terms. This was marginally less than the Nasdaq Biotechnology Index, which rose by 25.6% last year, reflecting something of a boom that occurred after the initial phase of the pandemic in biotech generally and in particular of certain sub-segments (COVID-related stocks and gene editing/therapy companies being among the most notable).

Although BB Biotech has a number of holdings in the top-performing areas, it trailed the NBI in 2020, although the overall effect was also a result of the currency impact of the late-year strengthening of the Swiss franc versus the US dollar. However, because of the long-term investment horizon and the volatility of the sector, it may be worth looking at periods longer than one year. Over 10 years, BB Biotech achieved an average 27% annual return (including dividends).

The trust’s best-performing investment in 2020 was Moderna, whose stock price rose roughly five-fold on the back of the rapid and successful development of its COVID-19 vaccine (mRNA-1273). Moderna was in fact also the best-performing biotech stock – and the fourth-best-performing stock of any sector – that were included in the Russell 1000 index in 2020.

Unusually, BB Biotech had taken equity in Moderna as a private company, prior to its initial public offering in December of 2018, which raised more than USD 600 million and was the biggest IPO in the history of the biotech sector. Although Moderna could be said to be a textbook example of BB Biotech’s investment approach, the 430% one-year return and 530% over two years is something of an outlier that perhaps largely reflects the unique circumstances of the SARS-CoV-2 pandemic in 2020.

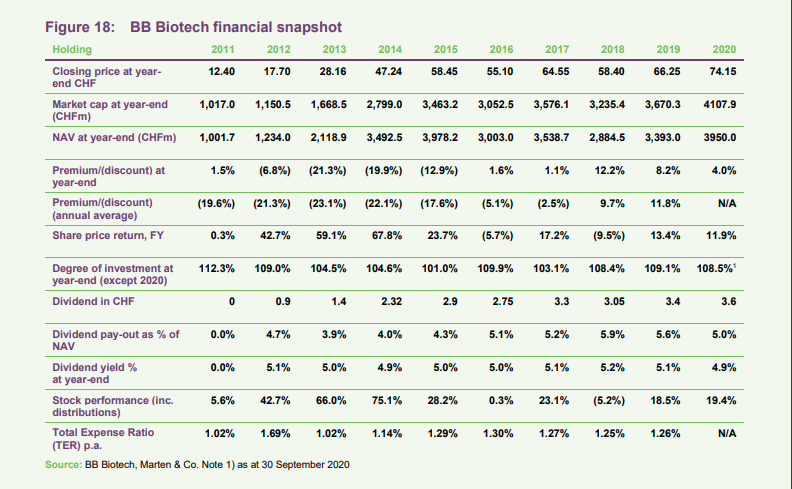

10-year financial snapshot

A 10-year financial snapshot is shown in the table below.

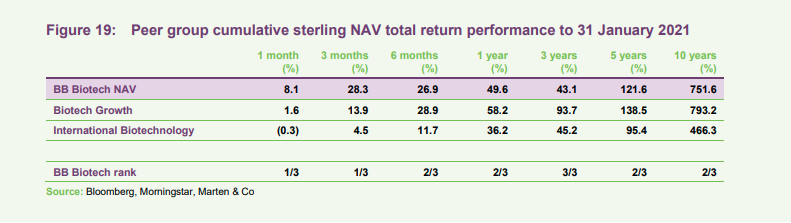

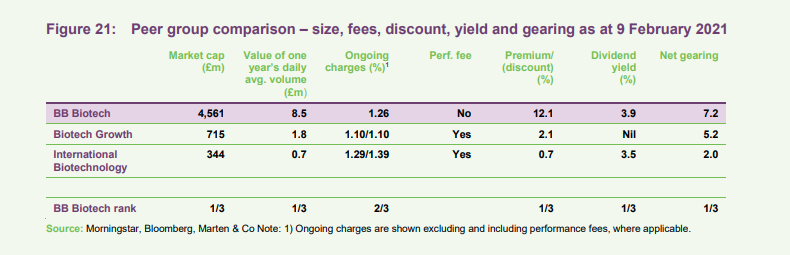

Peer group

In Figures 19, 20 and 21 below, we compare BB Biotech to two peer group investment companies; namely Biotech Growth Trust (LSE:BIOG), and International Biotechnology Trust (LSE:IBT). It should be noted that BIOG and IBT are both London-listed, whereas BB Biotech’s primary listing is in Switzerland. We have excluded from comparison certain investment trusts that are largely or primarily focused on private/unquoted equities in biotech (Arix and Syncona), as well as the other London-listed trusts that are focused primarily on healthcare.

In this part of the note, we have used values in sterling.

Biotech Growth and IBT portfolios are managed with the aim of outperforming the Nasdaq Biotechnology Index in relative terms, rather than on an absolute basis, and. the latter also actively manages its portfolio to avoid binary events. All of the funds have a similar focus on the US.

BB Biotech and Biotech Growth vie for best performing fund over most time periods.

BB Biotech is considerably larger than either of its biotech-focused peers; its market cap is 5x greater than the next-largest, BIOG. It is also the most liquid; at current prices, the value of the equivalent of its one-year average daily volume is about £8.5m worth of shares, which is about 4.7x that of the next most liquid, BIOG.

BB Biotech has the largest premium to NAV and offers the highest dividend yield. BB Biotech is the only fund in this group that does not pay a performance fee and its ongoing charges ratio is middle of the pack.

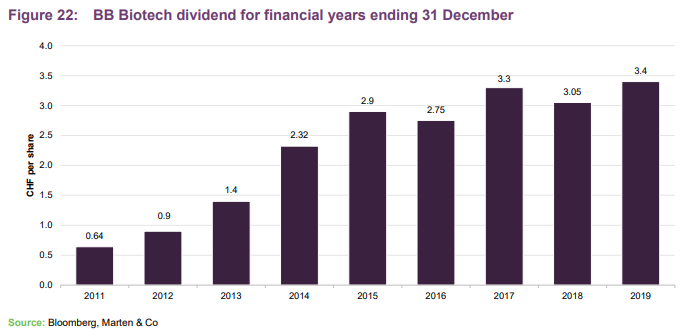

Dividend

BB Biotech intends to propose a dividend of CHF3.6/share in respect of 2020 to its AGM, which if confirmed, will be payable in March 2021. BB Biotech has paid a single annual dividend since 2012 and aims to offer investors a yield broadly equivalent to 5% of previous year-end NAV (so probably CHF3.8/share for FY2020, payable in March 2021). It is notable that BB Biotech pays the dividend from capital, as none of its holdings pay an income. Non-Swiss investors should note that Switzerland levies a 35% withholding tax on dividends, although can be reclaimed.

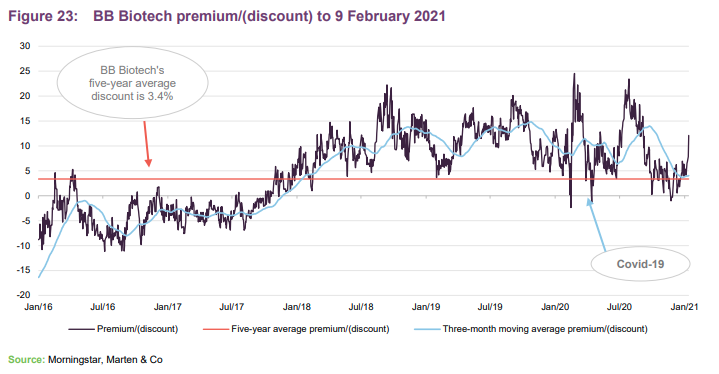

Premium/discount to NAV

BB Biotech currently trades at a 12.1% premium to NAV. It has traded at a premium for most of the past three years, typically in the high single-to-low double-digit percentage range. In contrast to the common practice of UK investment trusts, BB Biotech does not issue equity when its shares stand at a premium, which means that this situation tends to persist.

BB Biotech does, however, buy back shares when these fall below a certain discount to NAV, as was the case in 2010-2016. This is achieved through an automatic facility, but this has not been exercised in any of the past four years.

Fees and costs

Bellevue Asset Management, as manager, is entitled to a management fee at the rate of 1.1% per annum of NAV, with no performance fee. The total expense ratio for the year ended 31 December 2019 was 1.25% (2018: 1.26%).

Capital structure

BB Biotech has 55.4m ordinary shares outstanding. There are no other classes of share capital. BB Biotech’s financial year-end is 31 December and its AGMs are usually held in March. Annual and quarterly results and portfolios are updated in February, April, July and October.

Gearing

BB Biotech is allowed to borrow up to 15% of NAV to enhance returns, but normally its gearing is around the 10% level. At the end of September 2020, BB Biotech’s net gearing was 7.2%. This took the form of a CHF245m short-term loan with interest payable at 0.40% per annum.

In 2021, BB Biotech expects to receive cash in part-payment from the proposed sale of Alexion to AstraZeneca as well as a potential distribution from a transaction involving Agios.

Financial calendar

BB Biotech’s financial year-end is 31 December. It usually published its annual results in February (with quarterly interim results announced in April, July and October) and holds its AGMs in March. Where applicable, it pays its annual dividend shortly after its AGM.

The management team

BB Biotech is managed by Bellevue Asset Management, which is a division of Bellevue Group, an independent Swiss financial boutique specialising in asset management. Established in 1993 and listed on the SIX Swiss Exchange (SIX:BBN. market cap CHF429m), Bellevue Group is a standalone asset manager with about 100 employees.

BB Biotech is the firm’s largest single fund and accounts for about 40% of its AUM. Bellevue’s team also manages the smaller (and London-listed) investment trust BB Healthcare (LSE: BBH). This trust has a similar investment style to BB Biotech, but is focused mainly on large caps, although the two Bellevue-managed vehicles both have Vertex Pharmaceuticals (market cap $61bn) as a top 10 holding.

BB Biotech’s lead manager, Dr Daniel Koller, who has been in place since 2010, heads a team of seven specialist investment analysts, which has been very stable over time.

Dr Daniel Koller

Dr Koller joined Bellevue Asset Management in 2004, and has been head of the Investment Management Team of BB Biotech AG since 2010. From 2001–2004, he was an investment manager at equity4life Asset Management AG and from 2000–2001 an equity analyst at UBS Warburg. He studied biochemistry at the Swiss Federal Institute of Technology in Zurich (ETH) and earned his doctorate in biotechnology at the ETH and Cytos Biotechnology AG.

Felicia Flannagan

Ms Flannagan has been senior portfolio manager since 2004. Previously a biotech equity analyst at Adams, Harkness & Hill (now Canaccord Genuity) (1999–2004) and at SG Cowen (1991–1999), she holds an MBA from Suffolk University, Boston, and a BA in Communications from Boston College.

Dallas Webb

Mr Webb has been portfolio manager since 2006. Formerly, a SVP and equity analyst at Stanford Group (2004–2006) and Sterling Financial (2003–2004) and prior to that, an equity analyst at Adams, Harkness & Hill (now Canaccord Genuity), he holds an MBA from Texas Christian University and a BSc in microbiology/zoology from Louisiana State University.

Dr Stephen Taubenfeld

Dr Taubenfield has been a portfolio manager since 2013. Formerly senior analyst and founding partner at Iguana Healthcare Partners (2009-2013), consultant with Merlin BioMed Group (2008–2009) and MD/PhD Fellow in Neuroscience at Mount Sinai Hospital, New York (2004–2008). He holds an MD and PhD in Neuroscience from Brown University School of Medicine.

Dr Christian Koch

Dr Koch has been an equity analyst and portfolio manager since 2014. From 2013–2014 he was a sell-side pharma & biotech equity analyst at Bank am Bellevue and from 2010–2013 a research associate at the Institute of Pharmaceutical Sciences, ETH Zurich. He holds a PhD in Chemoinformatics & Computational Drug Design from ETH Zurich and an MS in Bioinformatics from Goethe University.

Dr Maurizio Bernasconi

Dr Bernasconi has been a portfolio manager since 2017. Previously, he was a pharma/biotech analyst at Bank am Bellevue (2014–1017) and chemist at SIGA Manufacturing. He holds a PhD in organic chemistry from University of Basel and an MS in Chemistry from ETH Zurich.

Dr Samuel Croset

Dr Croset is a relatively new appointment as analyst and portfolio manager and digital transformation lead (since Oct 2020). He was previously at Roivant Sciences (2018–2020) and Roche (2014–2018) and holds a Ph.D. in Bioinformatics from the University of Cambridge, an MS in Bioinformatics and an MS in Biochemistry from the University of Geneva.

The board

BB Biotech has four directors, two of whom have been associated with the company for many years and two who joined in 2020, replacing directors who stepped down on the grounds of age. Details are shown in the table below. Note: both BB Biotech’s chairman and vice-chairman are executive roles and are therefore different in responsibility to those typical of UK investment trusts.

Dr Erich Hunziker (chairman)

Dr Hunziker has been a director of BB Biotech AG since 2011 and president since 2013. Previously CFO of Roche Group (2001–2010), prior to that he held various executive positions at Corange (1983–2001), the holding company for Boehringer Mannheim (which was acquired by Roche in 1997) and before that at Diethelm-Keller-Gruppe, where he ultimately served as CEO. He holds a PhD in Industrial Engineering from the Swiss Federal Institute of Technology. He is chairman of Light Chain Biosciences AG, NovImmune SA, Entsia International AG and discoveric ag, and a director of LamKap Bio alpha AG, LamKap Bio beta AG and LamKap Bio gamma AG.

Dr Clive Meanwell (vice-chairman)

Dr Meanwell has been vice-chairman of BB Biotech AG since 2003. He co-founded The Medicines Company in 1996 and has been at various times chairman, executive chairman, CEO and CIO, as well as a director until January 2020 (when it was acquired by Novartis). He was a founding partner and managing director of MPM Capital (1995–1996), and had previously held various positions at Roche. He holds an MD and PhD from the University of Birmingham (UK), and trained in medical oncology.

Dr Thomas von Planta

Dr von Planta has been a director of BB Biotech since 2019. Since 2006, he is owner/director of CorFinAd AG. Previously he worked for Vontobel Group from 2002–2006 as head of corporate finance and member of the extended executive board. Prior to that he was with Goldman Sachs from 1992–2002. He holds a degree in law from the University of Basel and University of Geneva. He is a member of the board of directors of Bâloise Holding AG and a member of the advisory board of Harald Quandt Industriebeteiligungen GmbH (a family office investor active in the German-speaking region).

Dr Susan Galbraith

Dr Galbraith has been a director of BB Biotech AG since March 2020. She serves as head of oncology research & early development at AstraZeneca, and co-head of the Cambridge Cancer Centre Onco-Innovation Group. Dr Galbraith joined AstraZeneca in 2010 from Bristol-Myers Squibb, where she headed clinical discovery oncology & immunology and clinical biomarkers. Dr Galbraith is also a director of Horizon Discovery.

Prof. Dr Mads Krogsgaard

Prof Dr Thomsen has been a director of BB Biotech since March 2020. He is executive vice president, head of R&D and chief scientific officer at Novo Nordisk and president of the committee of the University of Copenhagen. He joined Novo Nordisk in 1991 and has held various positions, including head of Growth Hormone Research, SVP of Diabetes R&D. He holds a DVM from the Royal Veterinary and Agricultural University at the Faculty of Health and Medical Sciences of the University of Copenhagen.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on BB Biotech AG.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.