A taste of more to come

The UK market has been making somewhat of a comeback since the start of 2021, after years of uncertainty, volatility and being outright unloved. Henderson High Income (HHI) has been a beneficiary of the recovery in the UK’s fortunes, outperforming its benchmark and putting its NAV ahead of comparable indices over all time periods. Manager David Smith is positive about UK equity markets going forward and believes there is plenty more upside to come in the form of economic recovery following the pandemic, M&A activity and improving dividends. The trust currently yields an attractive 5.60%.

High income from a diverse UK equity income portfolio

HHI invests in a prudently diversified selection of both well-known and smaller companies to provide investors with a high income stream while also maintaining the prospect of capital growth. Gearing is used to enhance income returns, and also to achieve capital growth over time. A portion of gearing is usually invested in fixed interest securities, which helps dampen the overall volatility of the trust.

Market outlook

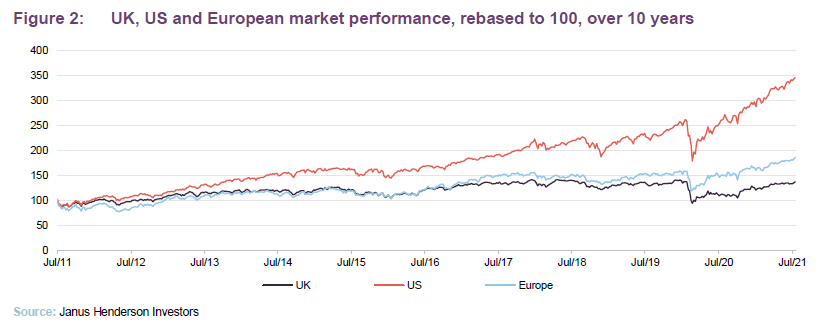

In recent years the UK has had one of the worst-performing equity markets across the globe, submerged in volatility caused by Brexit (among other political factors), falling foreign direct investment and, of course, the more recent coronavirus pandemic. Over the past five years, the MSCI UK Index is up by 31%, though this figure is well behind the US (+112%), Europe (+52%) and even China (+47%). The MSCI World ex UK is up 91%.

However, the story finally appears to be changing as Brexit uncertainty is subsiding, FDI projects are on the increase and the UK’s vaccination programme has been one of the most successful among its peers, with more than 75% of adults now fully vaccinated. In performance terms, the UK is up 14% year-to-date, in line with Europe and only slightly behind the US, which is up 19%. The MSCI ex UK is up 16%.

Meanwhile on the bond front, 2021 did not start well for investors, as inflation fears drove yields higher. However, since the middle of May yields have been falling once again, and in July were at their lowest levels since February. Regardless, bonds have remained popular among UK investors, with figures from the Investment Association showing fixed income funds took in nearly £7bn on a net basis in the first five months of the year.

Strong start for UK M&A

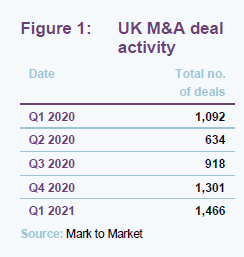

Deal activity has rebounded strongly since the market collapse caused by the pandemic, with Q1 2021 figures higher than deal volume pre-lockdown.

Inbound M&A investment from overseas has increased significantly despite ongoing lockdown measures and travel restrictions. According to M&A data and analytics platform Mark to Market, inbound M&A in the first quarter of 2021 was worth £58.7bn, more than three times the £18.6bn figure seen in Q1 2020. With 196 inbound deals, Q1 2021 also represented the largest quarterly inbound deal count since Q3 2017, while the largest portion came from US investors. This highlights the UK’s continued position as an attractive market for international investment and cross-border transactions.

The largest EMEA transaction of the year so far is National Grid’s £14.2bn acquisition of Western Power Distribution. A further 27 deals in the energy, mining, and utilities sector makes it the most active area for M&A by value with £20.7bn. This reflects a trend of more deals being driven by the energy transition as the UK works towards achieving net zero carbon emissions by 2050.

Meanwhile, the technology sector saw £20.4bn of transactions in Q1 2021, making up just over one quarter of UK deal-making. Other major M&A deals of the year so far include the acquisitions of UK sports nutrition bar brand Grenade by multinational confectionery firm Mondelez and ASOS’s acquisition of Arcadia Group brands such as Topshop, Topman, and Miss Selfridge. In terms of UK listed companies, there were 24 bids announced during H1 2021, double the number announced in the first six months of 2020.

Manager’s view

David Smith, manager of HHI’s portfolio of typically 80% UK equities and 20% UK fixed income, remains positive on the UK, despite some investors fearing that economic momentum has peaked. He says the market is currently in a consolidation phase, given the strong performance from its pandemic lows, but that valuations are still attractive. Above trend economic growth, as economies recover from the pandemic, should ultimately be supportive of equity markets. Meanwhile, he believes that the UK is still home to one of the cheapest equity markets of the developed world, which, combined with low bond yields, makes it an attractive environment for M&A – which, as discussed earlier, is already coming through.

A lost decade

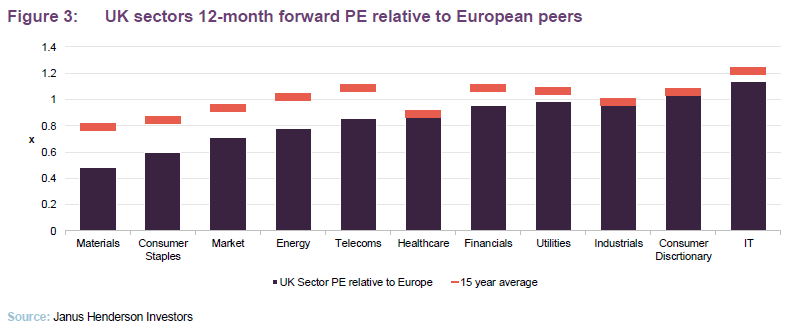

As shown in Figure 2, UK equity market returns have been lacklustre, underperforming other regional equity markets, but especially those in Europe and the US. Many believe this is because the UK index has large sector weights in banks and energy, but David highlights that the UK is cheap across all sectors (evident in Figure 3). He says this has been a full market issue, and not just one involving banks and energy. This, however, means that value opportunities are appearing across all sectors and is why M&A is so prevalent.

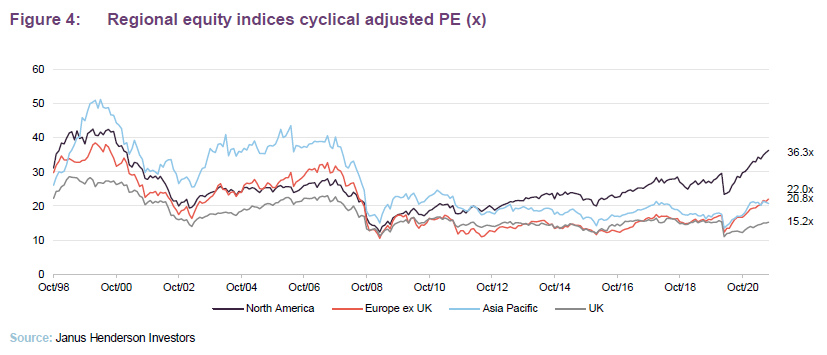

Given the recent trough and rebound in earnings, David says historic price-to-earnings ratios are not a true reflection of UK market valuations. The best numbers to look at are therefore on a 10-year rolling period, as shown in Figure 4. This shows the UK market is cheap, not only to its own relative history but also to overseas indices.

Improving outlook for income

Another reason for David’s optimism is the improving outlook for income over the past six months. He attributes this to three main drivers:

1. Strengthening mining sector – companies such as Rio Tinto and Anglo American are seeing strong free cash flow coming through from the commodity price environment which has led to strong dividend growth ahead of investor expectations and has been supplemented by special dividends.

2. Banks back on track – the Bank of England has now lifted dividend restrictions on banks and so interim dividends were paid, which David believes can grow back towards pre-pandemic levels. However, he cautions against investors expecting significant returns of excess capital via dividends, as some banks will choose to do share buybacks instead.

3. Earlier recovery – companies have restarted paying dividends sooner than expected and also, in some cases, stronger. Burberry, for example, has started paying pre-pandemic dividend figures.

Asset allocation

David says that since the start of 2021, he has been reducing HHI’s bond exposure and upping equities as well as increasing the trust’s gearing.

He has reduced exposure or completely sold out of a number of overseas defensive names such as RWE. Around three percentage points in the bond portfolio has been sold over the past six months. With yields at all-time lows, the manager said it made sense to make this change. As a result, HHI now has the lowest bond exposure it has had in its history, and David says he is happy to keep it this way for the time being.

It is these sales that have provided funding towards new cyclical names including Paragon, a specialist buy-to-let lender, and Volvo, a Swedish truck manufacturer. He has also been topping up what he considers to be more ‘stable’ holdings such as AstraZeneca and RELX, both of which have underperformed since the UK’s vaccine programme was first announced.

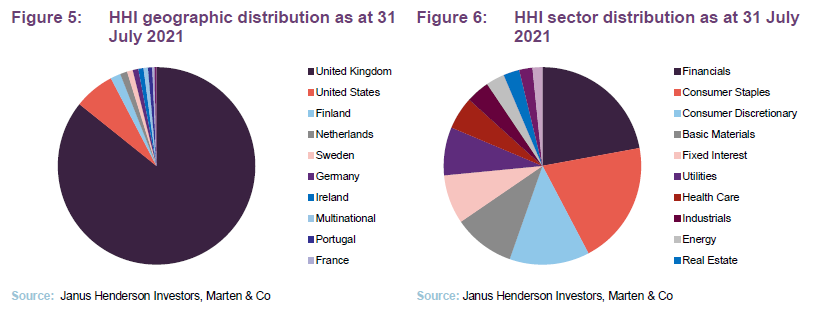

Financials remains the biggest sector allocation in the trust compared to December 2020, followed by consumer names. Fixed interest was the third-biggest allocation at the end of 2020 but, as mentioned, this has been significantly reduced relative to the trust’s history.

Top 10 holdings

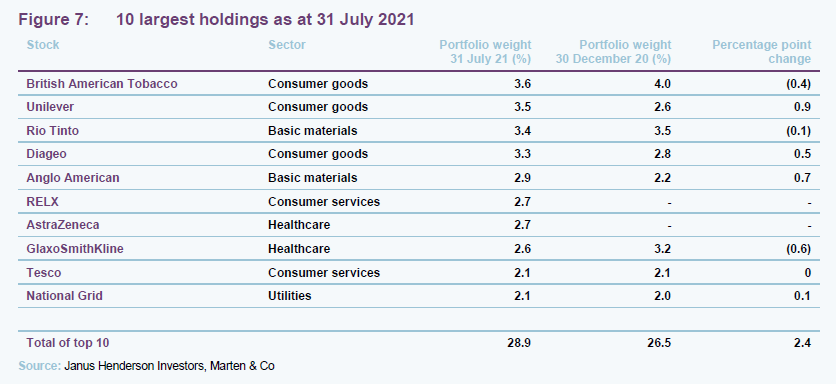

HHI’s top 10 holdings have changed little since the start of the year. There are two new entries, RELX and AstraZeneca, while 3i and Royal Dutch Shell have been removed. British American Tobacco remains the trust’s biggest holding, despite decreasing by 0.4 percentage points. As at 31 July 2021, HHI’s top 10 represent 28.9% of the portfolio, an increase of 2.4% since 31 December 2020.

British American Tobacco

British American Tobacco (www.bat.com) has been in HHI’s portfolio since before David’s appointment and is currently its largest holding. David says BAT is a great example of a company that has undeniably strong pricing power, which has been pivotal for the company to still grow profits, cash flow and dividends despite the decline of traditional cigarette smokers over the past 40 years. Meanwhile, BAT’s next-generation products such as its vaping range and ‘heat-not-burn’ business are also performing well. The latter still involves a cigarette stick hence the company’s high barriers to entry are still relevant going forward. David believes the strong cash flow comfortably covers the attractive dividend with any excess likely to be used for share buybacks in the next 12 months which could see the shares re-rate.

Tesco

Tesco (www.tesco.com) is another one of HHI’s longest-standing holdings, an investment since 2017. The household name has undergone a significant transformation over past five years, but its share price has remained relatively flat, despite improving its food quality and prices and growing its online presence. David says he expects its cash flow growth to come through in the next couple of years but that the market doesn’t believe this, which is where the opportunity lies. The company will not have to face the sharp increase in costs caused by the pandemic and it – hopefully – will hold onto the new customers it gained during the past 18 months. A higher focus on its own branded products will be better for cashflow, and its healthy dividend is likely to be supplemented with buybacks. David says Tesco could turn into a compounding cash flow story going forward.

New names

Paragon

Paragon (www.paragonbank.co.uk) is a UK-based bank that specialises in buy-to-let mortgages and commercial lending, with a focus on strong credit quality. David says it is a way to get banking exposure without buying a big player and that loan pricing in these areas is attractive, given the lack of competition from the main high-street banks. Paragon is writing new loans on higher yields than its back book, which underpins up-side to its net interest margin. Last year the company managed to generate a 10% return on equity, which should improve to 15% as the UK economy recovers. This isn’t reflected in the current valuation of 1.1x book. The company has a strong capital position and an attractive 4.5% dividend yield.

Volvo

Volvo (www.volvogroup.com) manufactures trucks and construction equipment. After a number of years in decline, with an acceleration in 2020 due to the pandemic, the truck cycle has turned and is now recovering. David says demand for trucks should be robust as economies emerge from the pandemic further supported by governments’ infrastructure spending. In recent years, management has increased the variability of the cost base, which should lead to higher through-the-cycle margins. Volvo has also launched a range of commercial long-haul electric trucks, which is a global first. The company has net cash on the balance sheet and an attractive dividend which was enhanced by the announcement of its intention to pay a special dividend (7% all in yield) which it could repeat going forward.

Other exciting plays

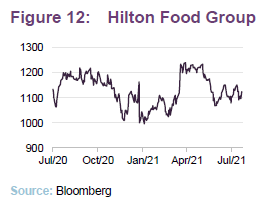

Hilton Food Group

Hilton Food Group (www.hiltonfoodgroupplc.com) processes, packs and distributes protein products to international food retailers. While this may not sound like the most exciting business, David says its straightforward and attractive business model has enabled it to deliver superior returns and excellent growth. Since its establishment in 1994 as a provider of red meat packaging to Tesco, the company has evolved and grown. It now occupies 18 sites in 16 different countries, partnering with large scale retailers to provide food services across an expanding product range including meat, fish, plant-based proteins and pre-prepared meals.

The company has built up a strong reputation of food safety, quality and best-in-class service levels, attributes which were further enhanced through the pandemic, and which have enabled them to successfully deliver on significantly increased volume demand. David explains that the company’s high cash generation and robust balance sheet means the business can afford investment to maintain its competitive advantage, pursue new growth opportunities and pay an attractive dividend, which has grown at an average annual rate of 11% since its IPO in 2007.

“Zero-yielders”

HHI also has exposure to a small number of zero-yielders, as David likes to play recovery positions too. Hospitality brand Whitbread (www.whitbread.co.uk), which owns Premier Inn, and coach operator National Express (www.nationalexpress.com) are just two examples of companies that have further recovery potential as the pandemic subsides. David says that recent worries about the Delta variant of the coronavirus caused the shares to underperform recently but with clear evidence that vaccinations are working and breaking the link between case numbers and severe illnesses, he says they can return to full profitability as life returns to normal, which isn’t discounted in the current valuations. The economy is still moving, and we are learning to live with the virus better than we did this time last year, he says, and so when it returns to ‘normal’, there could be material upside.

Performance

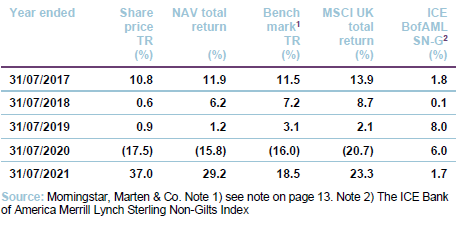

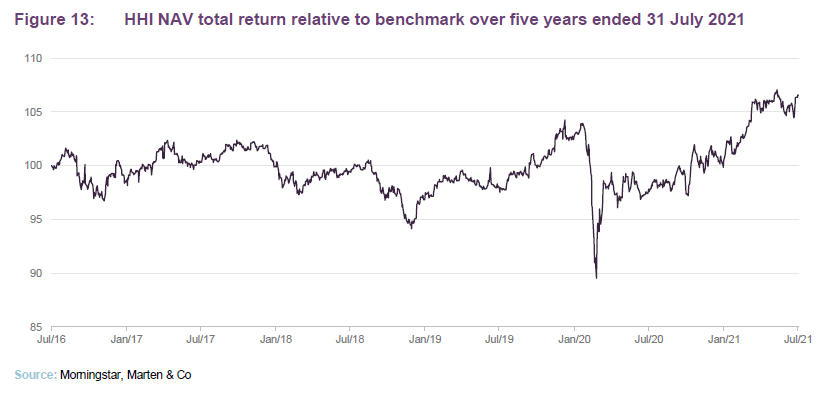

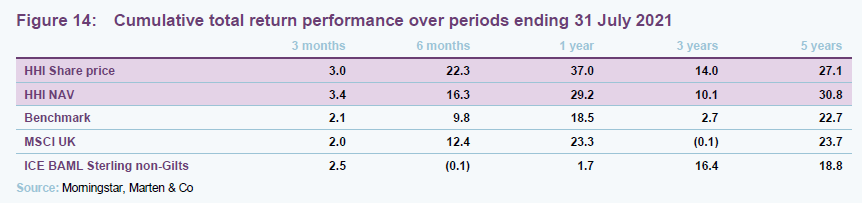

HHI has performed well so far this year, with a share price total return of 21.5% and an NAV return of 14.9%, well ahead of its benchmark. The trust is also ahead of its benchmark over one, three, five and ten years.

He adds that the narrowing of HHI’s discount of 6.5% in January 2021 to a 1% premium by the end of June 2021 has been a driving factor behind the trust’s share price return.

Attribution

David says the biggest drivers of performance during 2021 so far have been the following companies:

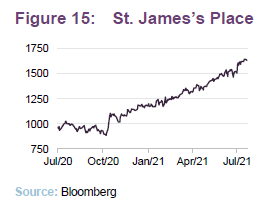

St. James’s Place

St. James’s Place (www.sjp.co.uk) is a wealth management company and constituent of the FTSE 100 index. The management produced updated long-term guidance this year, which included an increased focus on controlling cost growth that should lead to positive operational gearing. This was received well by the market, as the significant increase in costs and expenses over the last few years had been a particular criticism of the company. SJP has also delivered strong inflows so far this year.

Big Yellow Group

Big Yellow Group (www.bigyellow.co.uk) is a self-storage company headquartered in Bagshot, with 100 sites across the UK (as at December 2020). The company posted good results this year and David says it has achieved strong occupancy driven by an accelerated awareness of self-storage in the UK due to the pandemic (for example, those doing housing renovations, creating space for working from home and business customers using self-storage for last-mile delivery).

Other

David adds that Anglo American has also helped boost performance year-to-date, supported by strong commodity prices and with results that have beaten expectations with higher-than-expected dividends. Meanwhile, Intermediate Group Capital also posted good results this year, with continued momentum in fundraising in its asset management business.

Revenue reserves and dividend

As discussed in our annual overview from December 2020, HHI’s board announced early last year that it would have to dip into its revenue reserves to maintain its dividend. HHI declared two quarterly dividends of 2.475p, utilising a small transfer from reserves.

David says the trust is still facing a revenue deficit and that it is likely the board will have to once again use its revenue reserves to pay shareholders a healthy dividend. However, given the recovery in market dividends, he says, the revenue deficit this year is likely to be less than last year.

Revenue reserves are currently around the £9m mark, which covers approximately 70% of a full year dividend, which David says is more than enough to see the trust through until it gets back to its pre-pandemic income generation levels. He says there is no reason to suggest HHI would not be able to at least maintain its dividend this year.

At the end of December 2020, HHI had revenue reserves of £8.9m, equivalent to about 7p per share.

Peer group

HHI sits within the AIC’s UK equity & bond income sector. There is just one other constituent, Acorn Income, and that is a split capital trust with a small-cap focus. Acorn’s capital structure amplifies NAV moves, both positive and negative. In this section, we have also compared HHI to the UK equity income sector, which has 22 constituents.

Within that group are a few investment companies with unusual structures or asset exposures, including British & American (highly-geared and significant biotech exposure), Chelverton UK Dividend (another split capital structure) and Law Debenture (this has a subsidiary engaged in commercial activity that distorts its figures). The closest comparator to HHI is probably Shires Income, which is a smaller trust and whose fixed interest investments are largely represented by preference shares.

HHI’s ongoing charges ratio is competitive for its size and would likely be lower if the trust was as large as the median fund in the UK equity income sector. As at 24 August, HHI’s ongoing charge is 0.93%.

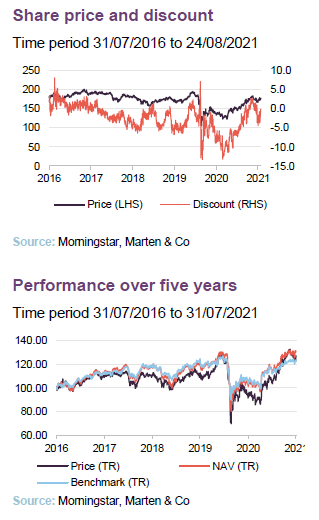

Premium/(discount)

Over the past 12 months, HHI has traded between a discount of 13.2% and a premium of 2.8%. The median discount for the period is 5.3% while the average is 4.6%. As at 24 August, HHI was trading on a premium of 0.12%. As mentioned earlier, the narrowing of the 6.5% discount in January this year to a 1% premium by the end of June helped boost HHI’s share price total return.

Looking over the past five years however, as is shown in Figure 19, the range has been much wider, and HHI has previously traded at a premium as high as 8.1%. The average discount over the past five years is 2.4%.

The board considers the issuance and buy-back of the company’s shares where prudent, subject always to the overall impact on the portfolio, the pricing of other comparable investment companies and overall market conditions. The board believes that flexibility is important in this regard and that it is not in shareholders’ interests to set specific levels of premium and discount for its issuance and buy-back policies.

Fund profile

Henderson High Income Trust (HHI) invests in a prudently diversified selection of both well-known and smaller companies, to provide investors with a high-income stream, while also maintaining the prospect of capital growth.

The majority of HHI’s assets are invested in the ordinary shares of listed companies with the balance in listed fixed interest stocks (no unquoted investments). Investee companies should have strong balance sheets that are capable of paying dividends. There is a focus on well-managed companies whose qualities may have been temporarily overlooked by investors and which offer the potential for capital appreciation over the medium term. A maximum of 20% of gross assets may be invested outside of the UK.

Gearing is used to enhance income returns, and to help achieve capital growth over time. A portion of gearing is usually invested in fixed interest securities.

Henderson Investment Funds Limited is the company’s AIFM and it delegates investment management services to Henderson Global Investors (both are subsidiaries of Janus Henderson Group Plc). The lead fund manager assigned to the trust is David Smith. He was made co-manager of the trust in 2014 and has been sole manager since 2015.

Blended benchmark

HHI benchmarks itself, for performance measurement purposes, against a blend of 80% of the FTSE All-Share Index return and 20% of the ICE Bank of America Merrill Lynch Sterling Non-Gilts Index. For the purposes of this note, we have replaced the All-Share with the MSCI UK Index.

Focus on sustainability

HHI’s business model includes environmental, social and governance (ESG) considerations which are integrated into the investment process. This includes the following four steps:

• Identifying risks – such as carbon risk exposure;

• Analysing the controls and actions – such as improving the management of the release of emissions or investing in green energy projects;

• Assessing sustainability targets – for example, targets linked to executives’ pay or aiming for a 2% to 3% reduction of net carbon emissions over the next three years; and Diversification, high income

• Engaging with management – having regular meetings with senior management on topics such as renewable investments, energy transition, human capital and renumeration.

David explains that HHI does not have negative screening; that is, it does not exclude any particular companies or industries but rather, is mindful of environmental, social and governance risks over both the long and short term.

He says when a company does not have appropriate policies and processes in place or aren’t making sufficient investments to evolve the business model to remain sustainable in the long term, this would prompt him to divest a company or not make an initial investment.

Previous publications

Readers interested in further information about HHI, such as investment process, fees, capital structure, life and the board, may wish to read our annual overview note “Robust high yield”, published on 4 December 2020, as well as our previous update note and our initiation note (details are provided in Figure 20 below). You can read the notes by visiting our website.

The legal bit

This marketing communication has been prepared for Henderson High IncomeTrust Plc by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and, if you are not a professional investor, or in any other way are prohibited or restricted from

receiving this information, you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the

period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.