Lar España Real Estate

Real estate | Initiation | 14 March 2023

Dominant assets make a resilient business

Lar España Real Estate has passed probably the most severe stress test in recent history in the form of the pandemic. 2022 results show that the value of its Spanish shopping centre and retail park portfolio has rebounded (seemingly undeterred by rising interest rates in the second half of the year). Sales at its assets broke through the €1bn mark for the first time and are well ahead of pre-pandemic levels.

The good operational performance can be put down to the quality of the portfolio and dominant nature of the assets in their region, the manager says. Online retailing is having less of an impact in Spain, but nevertheless the company’s portfolio is geared up for an omnichannel retail future, the manager adds, with several initiatives to optimise footfall and sales.

The group’s debt is at a fixed rate of 1.8%, having been refinanced in 2021, with a maturity of almost five years. Its share price is trading on a discount around 50% and the yield is over 11%.

Exposure to Spanish retail

Lar España Real Estate aims to grow its EPRA net tangible assets (NTA) through active asset management of Spanish commercial real estate, and deliver high returns primarily through the payment of considerable annual dividends.

Fund profile

The company’s website is larespana.com.

Lar España Real Estate is a SOCIMI (the Spanish equivalent of a listed Real Estate Investment Trust (REIT)) that has been listed on the Madrid Stock Exchange since 5 March 2014.

Lar España was the very first Spanish SOCIMI to be floated. It was also the first listing on the Madrid Stock Exchange for three years, and the first listing of a real estate company in seven years. It was founded at the bottom of the Spanish property cycle when real estate prices were at record lows and the real estate market was entering a new cycle.

The company is focused on investment in real estate assets throughout Spain, in the retail sector. It aims to deliver high returns for its shareholders through the payment of considerable annual dividends and create value by increasing the company’s EPRA net tangible asset (NTA) through active asset management. The group’s portfolio comprises nine shopping centres and five retail parks and was valued at just over €1.473bn on 31 December 2022.

The manager – Grupo Lar

Grupo Lar has €3.5bn AUM in six countries.

Lar España is exclusively managed by Grupo Lar, a private Spanish real estate company that has more than 53 years’ experience in the sector. It has expertise in development, investment and asset management and boasts a large team of professionals that actively manage its portfolio to maximise operational efficiency.

Grupo Lar is 100% owned by the Pereda family and has 248 employees in six countries. It has €3.5bn of assets under management spread across six countries in Europe and the Americas, diversified across the residential, retail, offices and industrial sub-sectors. It has established joint venture partnerships with several prominent international investors including Green Oak, Grosvenor, Goldman Sachs, Henderson Global Investors and Ivanhoe Cambridge.

Strong results reflecting quality of portfolio

Proposed dividend increase of 66.7% off back of operational performance in 2022.

In February, Lar España reported annual results for 2022, in which EPRA NTA increased 5.0%. This was despite significant interest rate rises last year and their impact on valuations in the real estate sector. The company’s EPRA NTA was €10.93 per share at the end of 2022, versus €10.41 a year prior. The EPRA NTA on a pro-forma basis (following a €110m bond buy back in January 2023 – more details on page 16) was €11.16 per share.

The value of the group’s portfolio rose by 3.5% over the year to €1.473bn (up 3.2% in the first half of the year and 0.2% in the second half), with gross rental income up 6.9%.

Off the back of the performance, the company has proposed a dividend for the year of €0.60 per share – a 66.7% increase on the level paid in 2021 (see the dividend section on page 13 for more detail). This would offer a dividend yield of 11.7% on the current share price. EPRA earnings per share was €0.48 per share – up 71.4% year-on-year.

Operationally, the company carried out 176 lease agreements during the year (20 new lettings, 50 re-lettings and 106 renewals), which was almost double the number conducted in 2021. This achieved a rental uplift of 1.3% (excluding an inflation-linked uplift) and saw occupancy across the portfolio increase to 96.6% (from 96.1%).

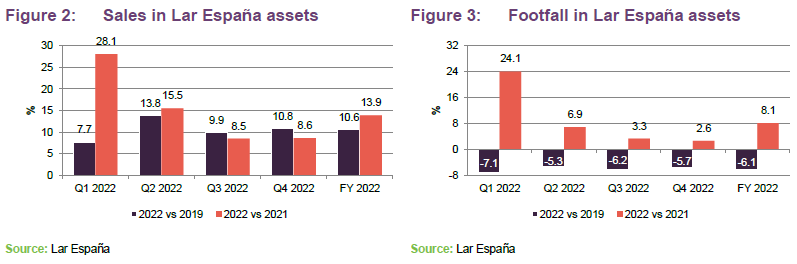

Sales reported by its tenants reaching €1.051bn in 2022 – the highest in the company’s nine-year life, and the first time that sales have exceeded one billion euros. This equated to an annual growth of 13.9% and is 10.6% up on the pre-pandemic level in 2019. Last year also saw 80.5 million visits to its assets, which is up 8.1% on the previous year but down 6.1% on 2019.

Outlook for retail in Spain

GDP growth of 5.5% in 2022, but economy still 1.1% below pre-pandemic level.

Spain’s economy grew faster than analysts had expected in 2022, with gross domestic product (GDP) expanding 5.5%. It grew 0.2% in the final quarter of the year despite fears of a global slowdown – a seventh consecutive quarter of growth.

Public spending drove the economy in the final quarter, compensating for a contraction in private consumption. Spain’s central bank expects GDP growth will slow to 2.1% in 2023, although economists – including the OECD – expect a sharper slowdown, projecting activity to grow by 1.3% in 2023 and 1.7% in 2024.

Despite the bounce back in 2022, Spain’s economy remains 1.1% below its pre-pandemic level – a laggard in Europe. In the third quarter, eurozone GDP was already 2.3% above pre-pandemic levels.

OECD expects that high inflation will curb household purchasing power, but that savings accumulated during the pandemic will support consumption. With deteriorating demand prospects and rising financing costs, private investment is expected to remain subdued, it added. It forecasts that inflation will decline to 4.8% in 2023 and 2024.

Meanwhile, consumer confidence fell to very low levels – close to those reached in the beginning of the pandemic – and the unemployment rate rose to 12.7% in the third quarter (from 12.5% in the second quarter).

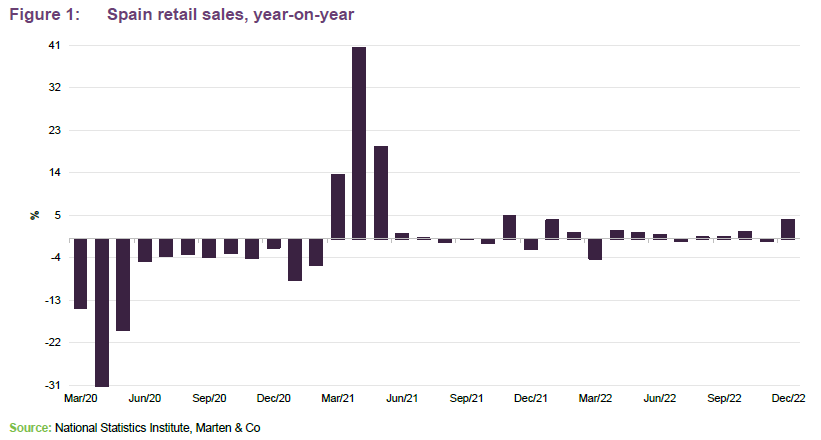

Retail sales grew 4.0% in Spain in December 2022.

Retail sales grew 4.0% in December 2022 compared to December 2021, rebounding significantly from a 0.5% fall in the prior month. It was the strongest growth in retail sales since January 2021, and was driven by sales of non-food products (up 9.5%). On a monthly basis, retail sales decreased by 1.7% in December, after four consecutive months of increases. Retail sales for the whole of 2022 were up by 0.8% over 2021.

The sales figures among Lar España’s assets beat the national average in 2022, as mentioned earlier, with sales in its shopping centres and retail parks up 13.9% over the year and 10.6% up on 2019, as shown in Figure 2. Figure 3 shows that footfall is yet to recover to pre-pandemic levels, but has been steadily increasing.

The strong performance data reflects the quality of Lar España’s portfolio of properties, the manager states, which are mostly categorised as ‘dominant’ – large centres, in large catchment areas with little competition. The effort rate – a key retail performance metric that measures the ratio between the total cost to the retailer (including rent and charges) and the turnover generated at the property (also known as the occupancy cost ratio) – was 9.2%. This increases the appeal of the assets to retailers, the manager says.

To highlight this point, the manager says that the company saw just one Inditex store close throughout its portfolio, out of 55 stores, as part of the fashion retail giant’s store closure programme – which it announced in June 2020 would see between 1,000 and 1,200 stores close across Europe to focus on larger concept stores. As part of the programme, Inditex expanded or updated many of the stores in Lar España’s portfolio – increasing its floorspace in the portfolio by 2,500 sqm.

The manager says that the quality of the assets puts the company in a strong position and gives it confidence in weathering the storm should the Spanish economy go into a recession.

Investment and leasing market

Spanish retail property investment levels remain subdued. Leasing market showing positive signs of recovery.

The Spanish retail investment market has seen suppressed levels of activity over the past three years, with several major global events stifling investor sentiment. The outbreak of the pandemic meant the main transactions to conclude in 2020 and 2021 were distressed sales. There was an initial uptick in transaction levels in 2022, but firstly the Russian invasion of Ukraine and then higher interest rates (and the subsequent re-rating of real estate assets) in the second half of the year quelled investment activity. It appears unlikely that investment levels will return in any meaningful manner until there is greater economic stability.

The leasing market, on the other hand, has shown signs of rebounding both nationally and within Lar España’s portfolio. As mentioned earlier, the company carried out 176 lease agreements during 2022, almost double the number conducted in 2021. These were at a 1.3% uplift to previous rents (excluding the CPI inflation-linked uplift).

All of the leases signed with Lar España are subject to annual rental uplifts in line with CPI. The company says that it plans to pass the full amount on to tenants this year, as was the case in 2022, which contributed to a 6.1% increase in gross rental income.

Retail in Spain – differentiated offering

Online retail penetration rates in Spain expected to reach 8% in 2024, far below other European countries.

The Spanish retail sector is unlike that of the UK and US and has, therefore, been less impacted by structural events that have plagued the retail sectors in these countries, the manager says. The boom in online retailing that has been prevalent in the US and UK over the past decade (which was accelerated during the pandemic) has yet to be seen in Spain. The manager believes that for many reasons online retailing as a percentage of total retail sales will not hit the levels of 20% to 30% seen in the UK and US.

Online retail sales are expected to rise to 8% of total sales in 2024 (from 5% in 2019). Outside of the big two Spanish cities of Madrid and Barcelona, online retailing penetration rates will remain at very low rates, the manager believes, due to a number of factors including poor infrastructure and the geographical landscape obstructing the effective operation of online retail. The manager adds that many challenges to online retailing have yet to be considered or worked out, including how to deal with returns in a cost-effective manner, and sustainability issues.

The Spanish culture also has a role to play, the manager notes. The combination of hot weather and the social nature of Spanish people means that they spend less time in their homes and more time socialising than their Western counterparts, according to the manager. This means that retail destinations are for more than just shopping, but a social occasion, it adds.

What has been borne out in both the UK and US retail markets is an apparent oversupply of space, which has had the effect of pushing vacancy rates up and rents down. There are no such oversupply issues in Spain. The country’s density of shopping centre space per inhabitant is 0.34 sqm, according to the Caixabank 2021 Retail sector report, which is well below the figure in the US of 2.35 sqm per inhabitant. The total floorspace classified as shopping centre in Spain amounts to 11.5m sqm across 410 assets (centres over 5,000 sqm), according to Cushman & Wakefield. In comparison, there is around 17.5m sqm in the UK across 726 shopping centres. This led to a vacancy rate of 18.2% across shopping centres in the UK at the end of 2022 (according to the British Retail Consortium). In Spain, the shopping centre vacancy rate is lower and just 3.9% at Lar España’s shopping centres.

Spanish malls have less exposure to department stores, which have fallen out of favour with consumers elsewhere. A lot of the vacancy in the UK and US has come from the failure and downsizing of department stores, with shopping centres in both countries having significant exposure to department stores. For instance, 46% of US mall space was let to department stores or hypermarkets, according to the Caixabank 2021 Retail sector report, compared to 24% in Spain.

Omnichannel the future

Despite the relatively low online retail penetration rates in Spain, the manager has taken various steps to respond to technological and digital advances and their impact on the way we shop. It describes Lar España as “an omnichannel business”, meaning the assets in its portfolio serve both traditional retail and online retailing.

The company has developed various asset management and interaction tools that it says will help create value and optimise processes. These projects include:

- The implementation of ‘smart’ technology such as parking apps, wayfinding apps, security and waste management technology. The smart technology can also produce consumer analytics based on customer’s journey and spending.

- A CRM customer loyalty programme. The scheme has 150,000 members and allows the company to collect customer data, classify and bundle the data and sell it to its retailers. It aims to grow its membership to 400,000 by June 2023 (which would be 10% of its unique customers). Data collected includes personal data as well as total consumption recorded in the centre; consumer categories and brands; consumption days; coupons usage; and visit rate.

- Click & Shop – a website where retailers in the shopping centre can promote their products and discounts, enabling customers to buy products online and collect in store. This service was launched at the beginning of 2022 and has been rolled out across all its shopping centres. The aim is to attract more customers into the stores, while offering a digital service to drive sales.

- Lar Conecta – an initiative that gives stores access to each shopping centre’s digital communication channels and their online traffic (Lar España’s shopping centre website has 1,750,000 visits and more than 500,000 social media following), helping them to promote their brands and increase sales. The service has been available since January 2023.

- WhatsApp Shopping – this gives customers the chance to access personal shopping and style advice through WhatsApp, giving retailers the opportunity to use their expertise to offer customers personal shopping advice, and providing shoppers with real-time information on product specifications and availability, as well as offering them the option to collect purchases in-store or have them delivered to their homes. WhatsApp Shopping is operational in over 50% of the portfolio.

The manager says that it intends to continue to develop and implement initiatives at all of its properties, to drive business development and gain a deeper understanding of user behaviour and profiles.

Investment process

Lar España’s investment strategy focuses entirely on retail properties in Spain. It identifies assets that it deems to be “poorly-managed” and that have strong upside potential, especially malls where there is an opportunity to reposition them.

The company’s investment policy is mainly focused on:

- Strategic assets in the shopping centre and retail parks sub-sectors, with strong growth potential;

- ‘Dominant’ retail assets in their catchment area that offer significant upside via asset management, avoiding locations where there is greater competition; and

- Risk diversification through a portfolio of asset located across Spain.

Focus on ‘dominant’ centres in large catchment areas.

Lar España favours what it calls ‘dominant’ retail assets. In the shopping centre sub-sector, that means the malls having a catchment area of around 350,000 to 400,000 people and no significant competing retail schemes. To be considered as dominant, the assets also must have a gross leasable area above 40,000 sqm, at least 4m visitors per year (footfall), above 90% occupancy levels, and have at least five critical retail operators. Seven of the nine shopping centres in Lar España’s portfolio are classified as dominant.

In the retail park sub-sector, ‘dominant’ is defined as at least 20,000 sqm in gross leasable area, 3m visitors per year, and above 90% occupancy levels. All of Lar España’s retail parks are also classified as dominant. More information on Lar España’s portfolio is on page 9.

Repositioning assets

After identifying and acquiring assets with strong upside potential, Lar España aims to add significant value through investment in major refurbishments. Works carried out will depend on each individual asset, but will generally include the reconfiguration of space to maximise natural light, and the incorporation of new food courts, expanded leisure offering, improved outdoor/public realm, and an enhanced fashion/shopping quarter. The company may also opt to redevelop an asset, as was the case with its Lagoh shopping centre in Seville (more details on page 11), which delivered an 8% yield on cost.

The majority of its portfolio (93.3%) has been refurbished or developed in the last five years. Lar España’s portfolio has increased in value by 54.0% (as at 31 December 2022) versus the acquisition price.

ESG

Portfolio obtained a score of 85/100 for ESG credentials, 8% ahead of peer group.

ESG is a cornerstone of Lar España’s investment policy, the manager states. Refurbishments and developments are all completed to high sustainability credentials. The company has obtained a rating in the Global Real Estate Sustainability Benchmark (GRESB) assessment of 85 out of 100, which is a 55% increase on its 2019 score. GRESB is the global ESG benchmark and reporting framework for the property sector, both listed and non-listed, and is one of the world’s leading sustainability indices. The company’s score is 8% higher than the average score among its peer group. 100% of the portfolio is BREEAM-certified, with an ‘excellent’ or ‘very good’ rating.

Lar España reduced energy consumption and carbon emissions from its portfolio over 2022, employing many initiatives. These included conducting waste management and energy efficiency plans, implementing a data automation programme across its portfolio that records energy consumption and emissions data, and improving environmental requirements in refurbishment projects. ‘Green leases’, whereby the tenant is incentivised to meet sustainability and energy usage targets, are applied on more than 10% of the portfolio.

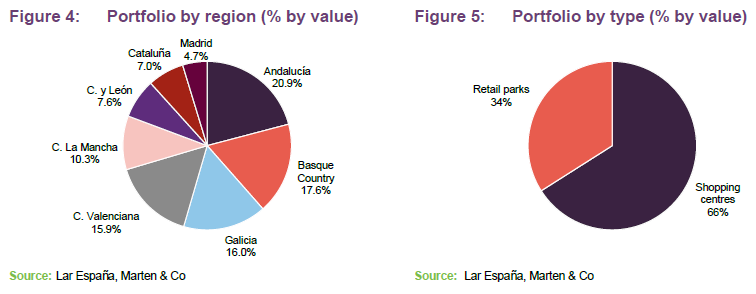

Asset allocation

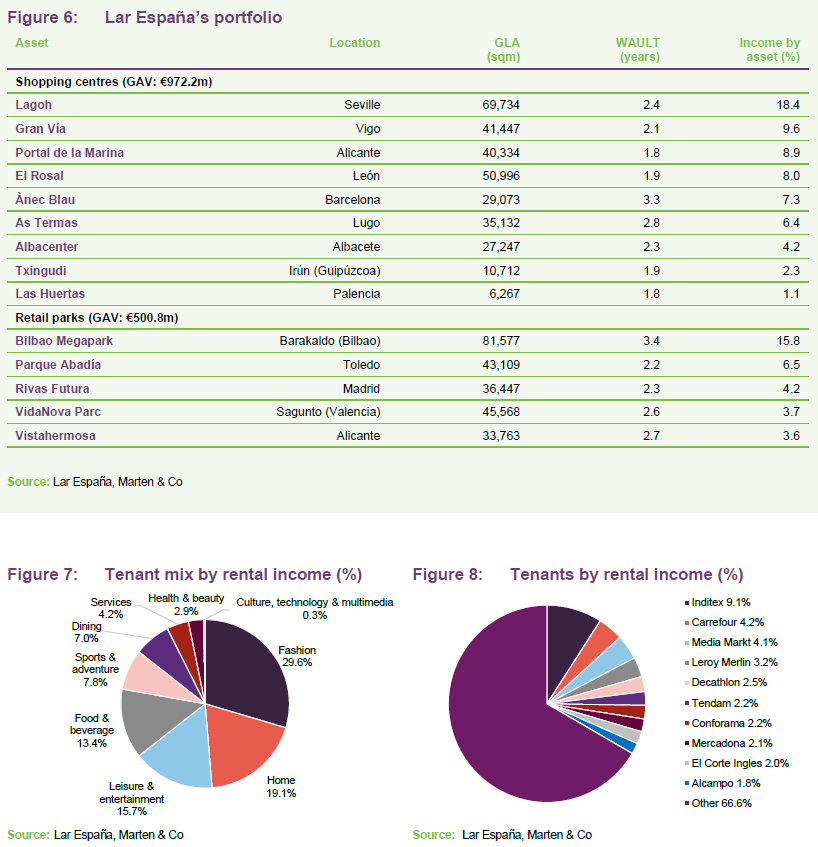

Lar España’s portfolio was valued at €1.473bn on 31 December 2022. It comprises nine shopping centres and five retail parks. It has a diverse range of tenants, as shown in Figures 7 and 8, with more than 1,000 leases and an occupancy rate of 96.6%. Its top 10 tenants account for 33.4% of the company’s rental income, while 65% of leases have expiries beyond 2025. The portfolio has a WAULT of 2.5 years.

6/

6/

Lagoh shopping centre

The largest asset in Lar España’s portfolio, the company bought the site of the Lagoh shopping centre in March 2016 for €38.5m and completed the development of the 69,734 sqm mall in 2019. It opened its doors in September 2019 and is home to a range of retailer and leisure brands. The centre comprises 148 stores.

It is located in the centre of Seville, the fourth-largest city in Spain, which has a population of 676,000 and 1.5m in the Greater Seville metropolitan area. Despite the demographics, the Lagoh shopping centre is the first dominant shopping centre in the Greater Seville area. In December 2022, the centre recorded one million visits – the highest monthly footfall figure since it opened.

The brand-new shopping centre was designed with technology and sustainability at its core. Technology initiatives at the mall include a sensor system that monitors visitors’ flow around the centre and use of space, which can inform prime footfall areas and marketing decisions. Sustainability features include solar panels providing low-carbon electricity and geothermal technology. Energy provided to the whole complex is 100% renewable and the scheme has been awarded the BREEAM Sustainability Building Certification. The scheme was awarded the Best Shopping Centre in Spain award by the Spanish Association of Shopping Centres.

Bilbao Megapark retail park

Megapark is the largest retail complex in the Basque Country and the fourth largest in Spain, covering a total area of 128,000 sqm, of which Lar España owns 81,577 sqm. It is the only retail park within a radius of 400 kilometres and is the leading scheme in the Bilbao area, with a catchment area of more than 2.2m people.

Developed in 2007, Lar España bought its holdings in two separate deals in 2015 and 2017 for a combined €178.7m.

Comprised of 81 retail units and 8,200 car parking spaces, Megapark is home to leading international retailers, such as Ikea, Mediamarkt and Leroy Merlin, and hosts the cinema with the highest box-office turnover in the Basque Country.

Gran Via shopping centre

Located in the largest city in the Pontevedra province, Vigo, the Gran Vía shopping centre has 41,453 sqm of lettable space and is the main shopping centre serving 482,100 people in the catchment area. The mall opened in 2006 and was acquired by Lar España in September 2016 for €141m.

It comprises 121 retail units that are let to a mix of international brands and Spanish companies, including Zara, H&M, Massimo Dutti and Carrefour.

Asset recycling programme on the cards

Last year the company set out an asset recycling plan that would see it sell some of its more established assets, where asset management initiatives and/or refurbishments have taken place and value-add opportunities have been exhausted, by 2025.

With the proceeds and cash reserves (it has €115m in the bank), it would look to acquire new assets that fit its investment criteria (large, dominant centres in their catchment area that have significant capital and rental growth potential through intensive asset management opportunities such as refurbishments, extensions or redevelopment). The company says that this is where higher returns can be achieved, but given the current economic environment, transaction activity is unlikely for the foreseeable future.

Performance

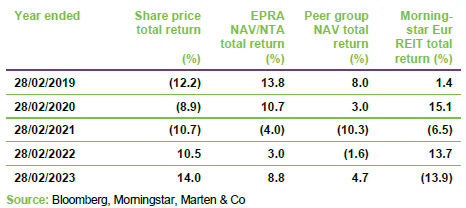

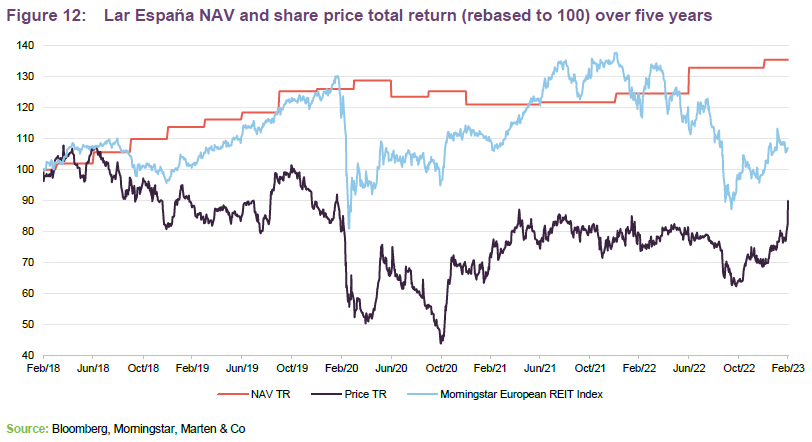

Lar España has posted a NAV total return of 35.5% over a five-year period.

Lar España’s EPRA NAV/NTA total return grew strongly since its launch due to acquisitions and value accretive asset management initiatives, such as refurbishments and redevelopments, as well as a strong dividend policy. The value of its portfolio fell during the pandemic, but held up relatively well, perhaps due to the dominant nature of the assets and consistently high occupancy rates. The EPRA NTA has recovered strongly in the last year and over five years it has returned 35.5%.

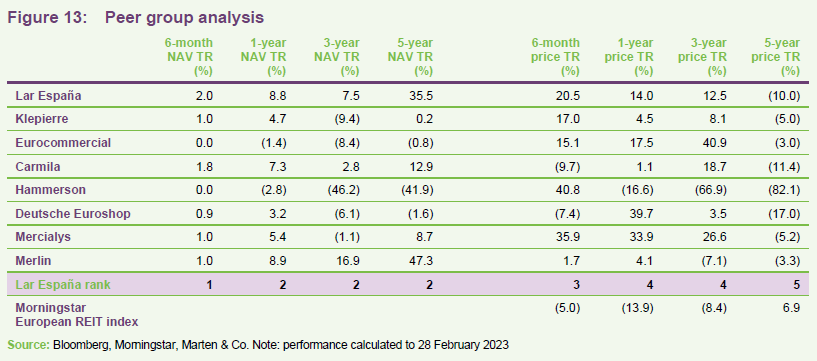

Peer group analysis

We have put together a comparison of Lar España’s listed peers in Europe, including pan-European and country-specific retail landlords and a Spanish peer. The peer group we have assembled consists of: Klepierre, Eurocommercial and Carmila (which are pan-European); Hammerson (UK), Deutsche Euroshop (Germany) and Mercialys (France), which are country-specific; and Merlin (which owns Spanish real estate predominantly in the office sector). We have also used the Morningstar European REIT Index as a comparator on share price returns.

Figure 13 shows Lar España’s short- and long-term performance versus its peers. It ranks highly among its peers over every time period in NAV terms, while its share price has started to recover over the short term.

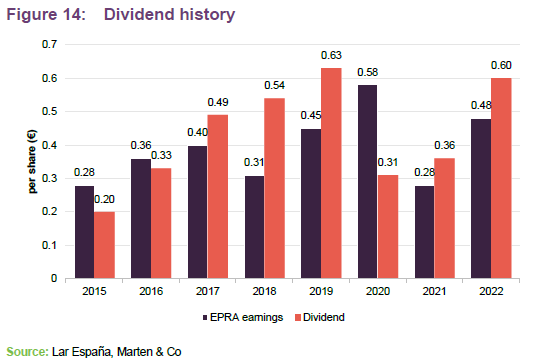

Dividend

Lar España pays a dividend once a year, in accordance with the SOCIMI rules. It has consistently distributed a high level of dividend to shareholders since its launch and has proposed a dividend of €0.60 per share for 2022 (to be paid in May 2023, subject to shareholder approval), equating to a dividend yield of 14.2% based on the share price at 31 December 2022. This is a 66.7% increase on the level paid last year and back to pre-pandemic levels. Lar España’s EPRA earnings per share increased 71.4% in 2022 to €0.48 per share, again almost back to pre-pandemic levels.

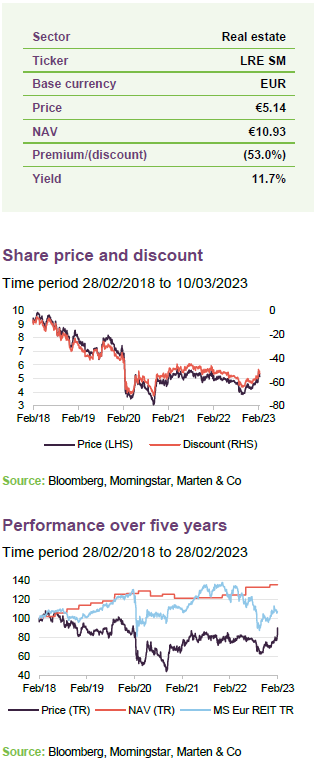

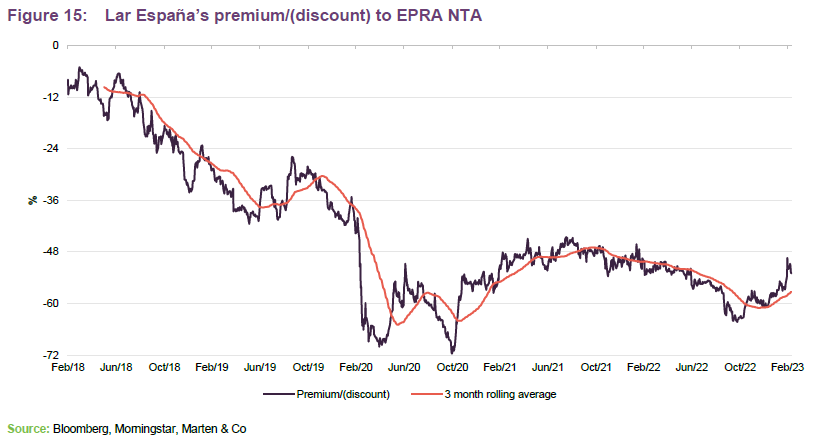

Premium/(discount)

Lar España’s shares have been trading at a discount to EPRA NAV/NTA for the past five years. Its share price started to fall in 2018 and 2019 when investor sentiment towards the retail sector appeared to be waning. It plunged further at the onset of the COVID-19 pandemic in early 2020 and despite a small recovery, its share price still lingers at an extremely wide discount of 53.0% at 10 March 2023.

Lar España is authorised to repurchase shares. Over the last four years the company has repurchased 17.1m shares, equivalent to 13.4% of its share capital, in three share buyback programmes. The most recent was in October 2021, where it acquired just over 3.9m shares for a total of €20.8m and an average price of €5.27 per share. This was a 48.2% discount to its NAV at 30 June 2021. The manager says a fourth share buyback plan may be initiated in due course.

Fees and costs

Grupo Lar’s current investment manager agreement (IMA) ends on 31 December 2026, having been renegotiated in 2021. Grupo Lar is entitled to a fixed annual base fee set at 0.62% of Lar España’s EPRA NTA. Previously, the base fee was the higher of €2m or 1% of EPRA NTA up to €1bn and 0.75% over €1bn.

A performance fee is paid annually to the manager based on Lar España’s EPRA NTA and share price performance over the year, subject to maximum amount of 1.5 times the annual base fee, with a hurdle of 8.5%. This is calculated as 8% of the growth in EPRA NTA beyond the 8.5% annual increase and 2% of the amount beyond the 8.5% annual increase in the market capitalisation. 80% of the performance fee will be calculated based on growth in NAV per share and the remaining 20% will be calculated based on the company’s share price. The performance fee will be payable, at the discretion of the company, in cash or treasury shares valued at their closing price at an agreed date. Grupo Lar was paid a total of €5.471m in 2022 (a base fee of €5.391m and a performance fee of €0.08m). This was substantially less than under the old IMA, which in 2021 saw Grupo Lar paid €8.743m (base fee of €8.609m and a performance fee of €0.134m).

Under the IMA, an additional performance fee is paid to Grupo Lar when the company undertakes new asset development or extension work on its current assets, calculated as a percentage of the total capex of the project (excluding land costs). The rate is 4% of total costs up to €40m and 3% of total costs above €40m. Refurbishments are not included. In 2022 no additional performance fee was paid.

Capital structure and life

As at 10 March 2023, Lar España had 83,692,969 ordinary shares in issue and no shares held in treasury. The company’s financial year end is 31 December and AGMs are usually held in April, with the next scheduled for 31 March 2023.

Debt facilities

Two green bond issues refinanced debt, markedly reduced cost and extended maturity.

The majority of Lar España’s debt is made up of two bonds. It raised €700m through the issuance of two unsecured senior green bonds in 2021 (€400m in July and €300m in October). The €400m bond, which was more than four times oversubscribed, matures in 2026 and has a fixed annual coupon of 1.75%. It was used to refinance €267m of debt that had been due to expire in 2022 and 2023 and to buy back secured senior simple bonds, issued in February 2015 for a total of €140m, which matured in 2022.

The €300m bond, which was five times oversubscribed, has a fixed annual coupon of 1.84% and matures in 2028. It was used to refinance €246m of mortgage debt. The refinancing of the debt with the bonds resulted in a reduction in its financial costs in 2022 of 43.5% (from €27.1m in 2021 to €15.3m in 2022).

Following both bond issues, Lar España’s debt is 100% unsecured at a fully-fixed rate, with the average maturity of its debt now 4.8 years (up from 2.6 years) and the average cost of debt 1.8% (reduced from 2.2%). The rating agency Fitch assigned an investment grade or BBB (stable) rating to both Lar España and the green bond issues. The company also has a €70m corporate loan, which matures in 2027.

In January 2023, Lar España bought back €110m of bonds, at a discount of 18% for a consideration of €90.5m, using cash reserves. A total of €98m was amortised from the €400m bond issue, while €12m was redeemed from the €300m issue. This leaves the total value of bonds in circulation of €590m.

The group’s debt now stands at €660m, with €115m in cash reserves. This equates to a loan to value (LTV) ratio of 37.1%.

Major shareholders

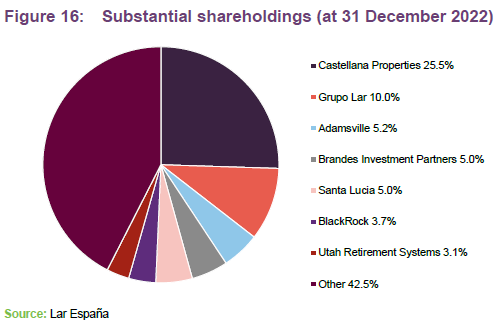

South African fund Vukile Property, through its Spanish subsidiary Castellana Properties (a REIT that also specialises in shopping centres), acquired a 21.7% stake in the company in January 2022 and topped up its shareholding in September.

Management team

Lar España is exclusively managed by Grupo Lar, as mentioned earlier. A management team of four people runs Lar España under a collective agreement.

Jon Armentia

Jon is the corporate director and chief financial officer of Lar España. He joined in 2014, having been chief financial officer of Grupo Lar since 2006, covering the retail sector. Previously he worked at Deloitte (formerly Arthur Andersen) for four years. Jon has a Bachelor’s Degree in Business Management and Administration from Universidad de Navarra and a General Management Program (PDG) from IESE and has over 20 years of experience in audit, finance and real estate, having participated in several committees and boards of directors.

Susana Guerrero

Susana is the legal manager and vice-secretary of the board of directors of the company. She joined Lar España in November 2014 and previously worked as a corporate and M&A lawyer at Uría Menéndez for 10 years. She has extensive experience in corporate governance, serving as secretary of the board of directors at companies across a range of different sectors. Susana is currently deputy director of the ESADE Center for Corporate Governance and head of its opinion and public debate area. She studied law at the Complutense University in Madrid and has an LLM in Business Law from Instituto de Empresa.

Harnán San Pedro

Hernán is the head of investor relations (IR) at the company, having joined in January 2016. Previously he worked at Grupo Sacyr Vallehermoso as head of IR, Skandia-Old Mutual Group and Banco Santander. Hernán studied law at Universidad San Pablo CEU (Madrid), holds an MTA from Escuela Europea de Negocios and has over 30 years of experience in different positions in the financial, insurance, construction and real estate sectors.

Jose Ignacio Dominguez

Jose Ignacio is the internal audit director of Lar España and joined the company in September 2021. He has extensive experience in several fields of private listed multinational companies, related to finance, internal audit, risk management and compliance and corporate governance. Previously, Jose Ignacio has worked for PriceWaterhouseCoopers, Fomento de Construcciones y Contratas, and more recently Grupo Ezentis. He graduated in Economics and Business Administration from the Complutense University of Madrid and the San Pablo CEU University College. He has a Postgraduate Master’s degree from the IESE Business School and is a member of the Official Register of Accounts Auditors of Spain, (ROAC) and certified by the Global Institute of Internal Auditors (IIA).

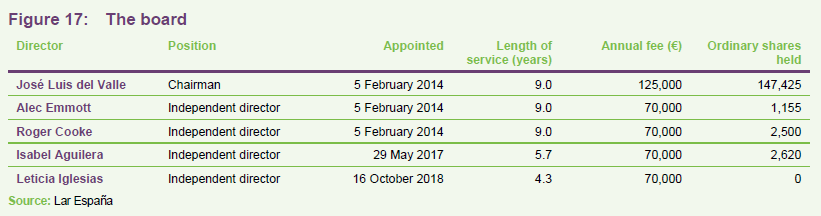

Board

The board comprises five non-executive, independent directors, three of whom were appointed on the company’s incorporation in 2014.

José Luis del Valle

José has extensive experience in the banking and energy sectors. From 1988 to 2002 he held various positions with Banco Santander, and in 1999 was appointed senior executive vice president and chief financial officer of the bank. Subsequently he was appointed chief strategy and development officer of Iberdrola, one of the main Spanish energy companies. José was also chief executive of Scottish Power between 2007 and 2008. He was until February 2023 chairman of WiZink Bank. He is currently a director at insurance group Ocaso, and the Instituto de Consejeros-Administradores. José has a Mining Engineering degree from Universidad Politécnica (Madrid, Spain), a Master of Science and Nuclear Engineering from the Massachusetts Institute of Technology (Boston, USA), and holds an MBA with High Distinction from Harvard Business School (Boston, USA).

Alec Emmott

Alec has a long career in the listed and unlisted real estate sector in Europe. He served as chief executive of Société Foncière Lyonnaise from 1997 to 2007 and subsequently as senior advisor until 2012. He is currently the principal of Europroperty Consulting, and since 2011, a director of CeGeREAL S.A. (representing Europroperty Consulting). He is also a member of the advisory committee of Weinberg Real Estate Partners. Alec has been a member of the Royal Institution of Chartered Surveyors (MRICS) since 1971 and holds an MA from Trinity College (Cambridge, UK).

Roger Cooke

Roger has more than 40 years of experience in the real estate sector, having started his career at Cushman & Wakefield in 1980. From 1995 until 2013, he served as chief executive of Cushman & Wakefield Spain, leading the company to attain a leading position in the sector. In 2017, Roger was awarded an MBE for his services to British businesses in Spain and to Anglo-Spanish trade and investment. He was previously the president of the British Chamber of Commerce in Spain and is currently chairman of the RICS in Spain and member of its European advisory board. He is also a member of the executive committee of the British Hispanic Foundation and editorial advisor to the property journal Observatorio Inmobiliario. Roger holds an Urban Estate Surveying degree from Trent Polytechnic University (Nottingham, UK) and is currently a Fellow of the Royal Institution of Chartered Surveyors (FRICS).

Isabel Aguilea

Isabel’s career has spanned various companies and sectors. She has served as president for Spain and Portugal at General Electric, general manager for Spain and Portugal at Google, chief operating officer at NH Hoteles Group, and chief executive for Spain, Italy and Portugal at Dell Computer Corporation. She is currently a director at Cemex Group, Oryzon Genomics and Clínica Baviera. Previous directorships include at Indra Sistemas, Banco Mare Nostrum, Aegon Spain, Laureate Inc., Egasa Group, HPS (Hightech Payment Systems) and Banca Farmafactoring. Isabel has a degree in Architecture and Urbanism from the Escuela Técnica Superior de Arquitectura of Seville, and a master’s degree in Commercial and Marketing Management from IE. She has completed the General Management Programme at IESE and the Executive Management of Leading Companies and Institutions Programme at San Telmo Institute. Isabel is currently an associate professor and consultant at ESADE and is also a director of the non-listed company Canal de Isabel II as well as Making Science (listed in the alternative market BME Growth).

Leticia Iglesias

Leticia has vast experience in both the regulation and supervision of securities markets and in financial services. She started her professional career in 1987, in the audit division of Arthur Andersen, and further developed her career in the Securities Exchange Commission of Spain. From 2007 to 2013 she was chief executive of the Spanish Institute of Chartered Accountants (ICJCE). From 2013 to 2017 she was a director at BMN, taking on roles in the executive committee as chair of the global risk committee and member of the audit committee. Leticia is currently a director at Abanca Bank, AENA SME, S.A., ACERINOX S.A, and at non-listed company Imantia Capital. She has a degree in Economics and Business Studies from Universidad Pontificia Comillas (ICADE) and is a member of the Official Registry of Auditors of Spain (ROAC). She is a patron of the PRODIS Foundation Special Employment Center and a board member of ICADE Business Club. She is also a member of the International Advisory Board of the Faculty of Business and Economics at ICADE.

Previous publications

QuotedData has previously published two short version notes on Lar España: in December 2020, Built to last, and in November 2021, Ducks in a row. You can read them by clicking the links.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Lar España Real Estate.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it, but in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.