Economic and Political Monthly Roundup

Kindly sponsored by Allianz

A collation of recent insights on markets and economies taken from the comments made by chairs and investment managers of investment companies – have a read and make your own minds up. Please remember that nothing in this note is designed to encourage you to buy or sell any of the companies mentioned.

Roundup

The arrival of Omicron – the latest COVID-19 variant – to wrap up what was already a tough year for many, saw further restrictions and lockdowns enforced in December across the world. While this had a knock-on effect on some markets, this was much smaller than previously seen in the face of new variants – perhaps because the shock factor is no longer applicable two years on since the virus was first discovered, or maybe because consumer spending has been high in the run-up to the holiday period and New Year celebrations. The good news is that this variant appears to bemilder than its predecessors and with more than 60% of the world having received at least one dose of vaccine (according to Our World In Data), perhaps the end is in sight. This may provide a brief respite in market volatility but concerns over supply chains, inflation and rising interest rates promise 2022 certainly won’t be dull.

December’s Highlights

Global

Alasdair McKinnon, manager of Scottish Investment Trust, notes that investors have become concerned that economic stimulus could be scaled back due to increasing inflation.

The chair of Majedie also believes inflation is the biggest question on investors’ minds at the moment.

Manager of BMO Global Smaller Companies, Peter Ewins, highlights ongoing supply chain challenges as a result of the surge in demand.

Signs suggest markets are becoming fundamentals-led

Securities Trust of Scotland manager, James Harries, believes interest rates cannot rise too much as there is simply too much debt.

Henry Strutt, chair of Edinburgh Worldwide, says there are now signs that markets are becoming more fundamentals-led rather than momentum driven.

The team at Monks says the pandemic has triggered an avalanche of change and that there will be structural consequences not yet fully understood or appreciated.

UK

The managers of Artemis Alpha highlight the themes which have influenced the macroeconomic environment over some of 2021.

Miton UK Microcap’s managers mull the lack of institutional interest in microcap stocks.

Mark White, chair of Aberdeen Standard Equity Income says a number of uncertainties remain on the horizon, from new COVID-19 variants to energy shortages.

Ultra-low interest rates may turn around as inflationary pressures build

The managers of Lowland think the era of ultra-low interest rates might be ending as inflationary pressures build.

Gresham House Strategic (now Rockwood Realisation) manager, Laurence Hulse, says monetary policy failure remains a key market risk and which could mean increased volatility over the next year.

BMO UK High Income chair, John Evans, highlights the uncertain macro background created by central banks scaling back support.

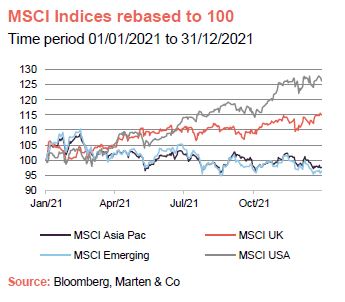

Asia Pacific

The chair of Aberdeen New Dawn remains positive on the long-term prospects for Asia, and says the region is now home to innovative businesses at the forefront of emergent trends.

The managers of Schroder AsiaPacific note lack of supply combined with rising costs in some parts of Asia, therefore increasing cost pressures for certain companies.

Cost pressures are causing a concern in some parts of Asia

The JPMorgan Asia Growth & Income team say the biggest opportunities – as well as the biggest risks – over the next 12 months lie in China.

Renewable Energy Infrastructure

SDCL Energy Efficiency Income chair, Tony Roper, explains why the US is one of the largest and most dynamic markets for investment in clean energy and energy efficiency.

Jonathan Parr of Triple Point Energy Efficiency Infrastructure says it is a good time to be investing in energy efficiency projects with increasing government support and the drive towards net-zero.

Other

We have also included comments on Europe from JPMorgan European Discovery and Henderson European Focus; Japan from JPMorgan Japan Small Cap Growth & Income and JPMorgan Japanese; China from JPMorgan China Growth and Income; India from JPMorgan Indian; flexible investment from MIGO Global Opportunities, Aberdeen Diversified Income and Growth and Momentum Multi-Asset Value biotechnology & healthcare from Polar Capital Global Healthcare; environmental from Jupiter Green; technology & media from Polar Capital Technology; private equity from Seed Innovations; debt from Henderson Diversified Income; leasing from Amedeo Air Four Plus and Doric Nimrod Air Two; Infrastructure from GCP Infrastructure; and property from Ediston Property Investment Company, Civitas Social Housing, Residential Secure Income, Tritax EuroBox, Schroder European REIT and Industrials REIT.

Full version

Click on the link at the bottom of the page to access the full report.

Kindly sponsored by Allianz

The legal bit

This note was prepared by Marten & Co (which is authorised and regulated by the Financial Conduct Authority).

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

Marten & Co may have or may be seeking a contractual relationship with any of the securities mentioned within the note for activities including the provision of sponsored research, investor access or fundraising services.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.