Second quarter of 2024

Investment Companies | Quarterly roundup | July 2024

Election season!

After a fast start to the year, markets have experienced a more subdued second quarter, although returns have remained positive, driven mostly by the outperformance of US mega caps. AI giant Nvidia has continued to lead the way, delivering enormous gains, especially when measured in terms of market cap. The company is now up 166% so far this year, briefly overtaking Microsoft as the world’s largest company in the process. This was despite a three-session, 13% decline in June which wiped over $400bn off the company’s value (almost double the dollar value of the entire investment trust sector). Highlighting the dominance, Nvidia contributed more than one quarter of the entire MSCI ACWI’s share price growth so far this year.

Outside of the AI euphoria, markets continue to reflect anticipation of falling interest rates, with at least one cut priced in for the US, UK, and Eurozone this year.

The median NAV return for the investment trust sector was 1.4%, with several rate sensitive sectors performing strongly.

While having a less tangible, or at least immediately measurable, impact on markets, politics have also been front and centre with several of the world’s largest economies going to the polls over the last few months, including India, Mexico, France, and the UK. However, attention now turns to the US election in November.

New research

So far in Q2, we have published notes on: Polar Capital Technology, Herald Investment Trust, CQS New City High Yield Fund, RIT Capital Partners, Montanaro UK Smaller Companies, Polar Capital Global Financials Trust, Ecofin Global Utilities and Infrastructure Trust, Vietnam Holding Limited, BlackRock Throgmorton Trust, AVI Global Trust, Impax Environmental Markets, Downing Renewables and Infrastructure Trust, Lar España Real Estate, Grit Real Estate Income Group, CQS Natural Resources Growth and Income, Bluefield Solar Income Fund, HydrogenOne Capital Growth, abrdn Private Equity Opportunities and Oakley Capital Investments

At a glance

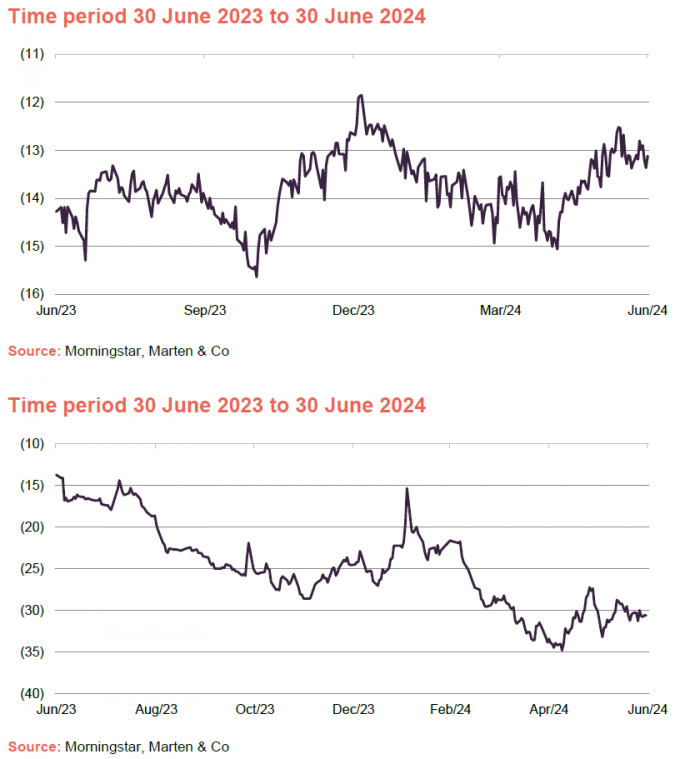

All investment companies median discount

As the chart highlights, discounts have been trending in the right direction over the last few months, helped by the expected path of interest rates, although this momentum has stalled somewhat in recent weeks. The median discount narrowed marginally, from 13.6% at the end of Q1 to 13.1% as of 30 June.

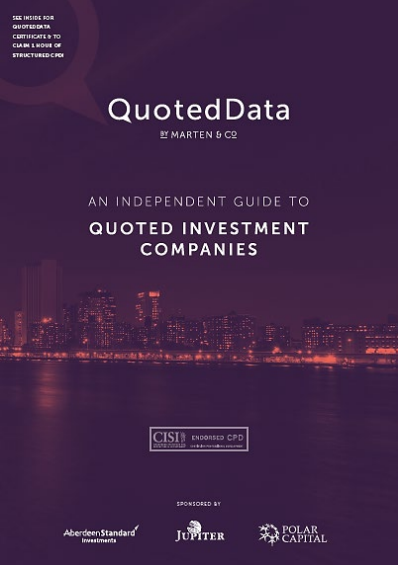

Renewable energy infrastructure median discount

It has very much been one way traffic for renewable energy infrastructure companies so far this year. Discounts have been amplified by relatively resilient NAV performance across the sector. In Q2, we have seen discounts narrow for some of the better performing trusts, although as a group the sector remains deeply depressed.

| 30/06/2024 | Change on quarter (%) | |

| Pound to US dollar | 1.2645 | 0.2 |

| Pound to Euro | 1.1801 | 0.9 |

| Oil (Brent, in dollars) | 86.41 | (1.2) |

| Gold (in dollars) | 2326.75 | 3.3 |

| US Treasuries (10-year yield) | 4.40 | 4.7 |

| UK Gilts (10-year yield) | 4.17 | 6.1 |

| German government bonds (bunds, 10-year yield) | 2.50 | 8.7 |

Source: Bloomberg

Winners and losers

As noted, several rate sensitive sectors have performed well in anticipation of interest rate cuts, although in most cases discounts remain stretched. The median NAV return for the investment trust sector was 1.4%, while discounts narrowed slightly from 13.6% at the end of the first quarter of 2024 to 13.1% at the end of the Q2.

Best performing sectors over Q2 2024 by total price return

| Median share price total return (%) |

Median NAV total return

(%) |

Median discount 30/06/24

(%) |

Median sector market cap 30/06/24 (£m) |

Number of companies in the sector | |

| Infrastructure securities | 13.1 | 7.1 | (16.9) | 107 | 2 |

| India/Indian subcontinent | 12.9 | 12.0 | (14.7) | 434 | 4 |

| Technology & technology innovation | 12.1 | 10.8 | (10.1) | 2,738 | 2 |

| UK smaller companies | 11.2 | 6.7 | (13.8) | 136 | 25 |

| Financials & financial innovation | 10.2 | 0.2 | (24.2) | 356 | 2 |

Source: Morningstar, Marten & Co. Note: inclusive of sectors with at least two companies. Note: many alternative asset sector funds release NAV performance on a quarterly basis

Infrastructure securities was the best performing sector in the second quarter, led by Premier Miton Global Renewables which was up 18%. Ecofin Global Utilities and Infrastructure was also up strongly, returning 8%. Both companies are heavily exposed to renewable energy infrastructure, which has suffered from deeply negative sentiment over the past 18 months. It appears we have reached an inflection point now however as inflation begins to fall and electricity prices across the UK and Europe continue to recover. Demand for power is rising, in part thanks to power-hungry AI data centres. We have also seen an uptick in private market activity reflecting the perception that the market has become oversold.

India has been one of the best performing markets globally, tapping into a strong domestic economy which grew at 8.2% over the last fiscal year. Its benchmark Nifty 50 index is up 25% over the past 12 months despite a period of increased volatility following the election which saw the market-friendly Bharatiya Janata Party, led by Narendra Modi, lose its long-held majority.

The Technology & technology innovation sector is heavily exposed to Nvidia and the wider AI trade, which has maintained its momentum throughout the year.

The UK smaller companies sector is another which has benefited from falling inflation and interest rate expectations. Takeovers, as overseas investors and private equity have taken advantage of cheap valuations have been a factor too.

The performance of the Financials & financial innovation sector was driven by Augmentum Fintech which was up 19% in the second quarter, and solid numbers from Polar Capital Global Financials Trust. Augmentum has benefited from solid portfolio execution over the past 12 months. Despite this, it continues to trade on a steep discount of 28%, reflecting the still marginal sentiment towards more growth orientated sectors of the market.

Worst performing sectors over Q2 2024 by total price return

| Median share price total return (%) |

Median NAV total return

(%) |

Median discount 30/06/24

(%) |

Median sector market cap 30/06/24 (£m) |

Number of companies in the sector | |

| Japanese smaller companies | (3.6) | (0.8) | (8.8) | 255 | 4 |

| North American smaller companies | (3.6) | (4.5) | (11.9) | 197 | 2 |

| Property – UK residential | (3.4) | 0.8 | (55.6) | 157 | 7 |

| Japan | (2.9) | (2.8) | (9.2) | 307 | 5 |

| Biotechnology & healthcare | (1.4) | (0.9) | (10.1) | 530 | 6 |

Source: Morningstar, Marten & Co. Note: inclusive of sectors with at least two companies. *many alternative asset sector funds release NAV performance on a quarterly basis

Japan’s benchmark Tokyo Stock Price Index is up almost 25% over the past year thanks to accelerating corporate governance reforms and steady economic growth. However, one of Japan’s major issues is its deteriorating currency which has now reached a 34-year low against the US dollar. The weak currency has driven up the cost of food and energy, contributing to a steep drop off in consumer spending (which makes up more than half of Japan’s GDP). This has had an outsized effect on smaller companies which are traditionally more domestically focused and tend to have less exposure to export revenues which benefit from a weak currency.

While markets are pricing almost 50pbs of interest rate cuts in the US by the end of 2024, yields across the curve are still close to cycle highs as inflation expectations remain elevated (made worse as the odds of a Trump election victory have increased). In combination with mixed economic data, this has left the backdrop for highly rate sensitive small caps uncertain, leading the sector to stay range bound so far this year.

In the UK, the prospect of a Labour government may have spooked shareholders in residential property companies, with rent controls and a revamp of the social housing sector some of the more radical theoretical policies of a left-wing government, but in reality, both are highly unlikely.

It was a highly bifurcated month for the biotechnology & healthcare sector with a 28% spread between the best and worst performers. Syncona saw the steepest fall, down 12%, as it continued to suffer from negative sentiment towards growth equity, with its shares down almost 30% over the past year.

Top 10 performers by fund

Best performing funds in total NAV (LHS) and price (RHS) terms over Q2 2024

| Fund | Sector | (%) | Fund | Sector | (%) |

| abrdn New India Investment Trust | India/Indian subcontinent | 19.8 | Gresham House Energy Storage | Renewable energy infrastructure | 68.2 |

| Rockwood Strategic | UK smaller companies | 19.6 | Hipgnosis Songs | Royalties | 48.4 |

| Golden Prospect Precious Metals | Commodities & natural resources | 16.0 | Foresight Sustainable Forestry | Farmland & forestry | 43.2 |

| Manchester & London | Global | 14.6 | Harmony Energy Income Trust | Renewable energy infrastructure | 36.2 |

| Chelverton UK Dividend Trust | UK equity income | 14.3 | Rockwood Strategic | UK smaller companies | 26.7 |

| Strategic Equity Capital | UK smaller companies | 13.0 | abrdn New India Investment Trust | India/Indian subcontinent | 26.4 |

| India Capital Growth | India/Indian subcontinent | 12.8 | Cordiant Digital Infrastructure | Infrastructure | 22.2 |

| River UK Micro Cap | UK smaller companies | 11.8 | Chelverton UK Dividend Trust | UK equity income | 21.1 |

| Allianz Technology Trust | Technology & technology innovation | 11.7 | Schiehallion Fund | Growth capital | 20.9 |

| Ashoka India Equity Investment | India/Indian subcontinent | 11.2 | EPE Special Opportunities | Private equity | 20.3 |

Source: Morningstar, Marten & Co.

As noted, Indian markets have continued to perform strongly so far in 2024, and following the election it is hoped that a more balanced coalition will bode well for both markets and the wider economic landscape. The sector is well represented with three companies in the top 10 best performing funds. abrdn New India Investment Trust led the way and continues to comfortably outstrip the benchmark NIFTY 50 index, up 45% over the past year. This momentum has continued through Q2 thanks to strong earnings performance across a number of its portfolio companies.

Rockwood Strategic was the best performing UK small cap, while Strategic Equity Capital and River UK Micro cap were also up strongly, with the whole sector benefiting from the expectation of easier monetary policy and an improving outlook for M&A. Rockwood Strategic in particular has continued to execute well over the past year despite broader economic challenges with several of its largest holdings generating strong returns. For example, education service provider RM, which accounts for almost 10% of the fund, announced plans to quintuple its 2023 pre-tax profits.

Golden Prospect Precious Metals represents a leveraged play on the price of gold, which is up strongly over 2024 despite real rates rising steadily. Fears around the Federal Reserve’s control of inflation seem to be the most likely explanation for the rally.

Manchester & London represents the most concentrated play on the AI trade in the entire investment trust sector. Nivida and Microsoft, which are up 166% and 26% respectively so far this year, make up more than 50% of the trust. Allianz Technology Trust has benefited from similar tailwinds.

Chelverton UK Dividend Trust’s returns are amplified by the gearing provided by its zero dividend preference shares. It has benefitted from the tailwinds behind the rest of the UK smaller companies sector. Its performance has been boosted by an increasingly active M&A environment, as private markets have begun to recognise the attractive valuations on offer. In Q2, the company noted two key contributions to its performance were the takeover bids of portfolio companies Tyman, and TClarke for respective premiums of around 35% and 28%.

In terms of share price movements, we have seen a number of significant increases. The largest of these was Gresham House Energy Storage which along with Harmony Energy Income Trust has lost almost half its market value over the last year. The root of the problem has been falling and less volatile power prices, and issues with the UK’s national gird balancing mechanism. Promisingly, over last few months the situation has improved. The Gresham House trust also surprised the market by announcing a deal with Octopus Energy that should help underpin its revenues for a while.

Both Hipgnosis Songs and Foresight Sustainable Forestry received buyout offers well above their prevailing NAVs.

Early in May AVI Global trust, which is known to take large positions in companies trading at attractive discounts (it contributed to and then benefitted from the Hipgnosis Songs takeover), purchased a significant stake in Cordiant Digital Infrastructure from Sarasin & Partners. The sale appears to have removed an overhang from the shares, which are up 18% since the announcement.

There does not seem to be one specific factor driving the shares of Schiehallion Fund higher. The rally coincided with the release of its annual report while also lining up with the discount falling over 50% which resulted in a significant increase in trading volume. We have also seen several positive updates regarding SpaceX which is the company’s largest holding.

The move in EPE Special Opportunities is more a function of timing, with the trust trading on thin volume and a persistent discount of around 50%.

Bottom 10 performers by fund

Most of the damage in the biotechnology & healthcare sector occurred in April, following the Federal Reserve meeting which suggested that estimates for both the frequency and magnitude of US interest rate cuts over the course of 2024 would need further moderation. Bellevue Healthcare in particular noted that this had an acute effect on its portfolio of small and mid-cap stocks. This sentiment is also likely the man driver of the fall in Brown Advisory US Smaller Companies fund.

Gulf Investment Fund suffered from escalating political tensions in the Middle East. Impax Environmental Markets fell steeply in April, coinciding with the release of its annual report, but again likely driven by interest rate uncertainty. Several of its portfolio companies also provided relatively weak forward guidance, while there are concerns relating to the announcement of tariffs on $18bn of imports from China specifically targeting low-carbon technologies.

Worst performing funds in total NAV (LHS) and price (RHS) terms over Q2 2024

| Fund | Sector | (%) | Fund | Sector | (%) |

| Baillie Gifford Shin Nippon | Japanese smaller companies | (10.4) | Regional REIT | Property – UK commercial | (21.7) |

| RTW Biotech Opportunities | Biotechnology & healthcare | (7.2) | VPC Specialty Lending Investments | Debt – direct lending | (16.4) |

| Bellevue Healthcare | Biotechnology & healthcare | (7.1) | Riverstone Energy | Commodities & natural resources | (12.6) |

| Gulf Investment Fund | Global emerging markets | (5.6) | BlackRock Latin American | Latin America | (12.4) |

| Impax Environmental Markets | Environmental | (5.2) | Life Science REIT | Property – UK commercial | (12.2) |

| Castelnau Group | Flexible investment | (5.1) | Syncona | Biotechnology & healthcare | (11.5) |

| VPC Specialty Lending Investments | Debt – direct lending | (5.1) | Aquila European Renewables | Renewable energy infrastructure | (11.3) |

| Geiger Counter | Commodities & natural resources | (5.0) | Gulf Investment Fund | Global emerging markets | (10.9) |

| Brown Advisory US Smaller Companies | North American smaller companies | (4.9) | Chrysalis Investments | Growth capital | (8.3) |

| Martin Currie Global Portfolio | Global | (4.9) | Bellevue Healthcare | Biotechnology & healthcare | (8.0) |

Source: Morningstar, Marten & Co. Note: excludes trusts with market caps below £15m at 30/09/23

The fall in Castelnau Group was due to some stock specific factors including a 19% drop in portfolio company, Hornby, in May. VPC Specialty Lending Investments continued its steep sell off this year, with shares now down 40% in the last 12 months. After an impressive rally through 2023, Geiger Counter shares have fallen steadily as the spot price of uranium has dropped well off its highs.

Despite significant exposure to Nvidia and the AI trade, the Martin Currie Global Portfolio has suffered from weakness across several of its large positions including Sartorius Stedim, Estee Lauder, and Illumina.

Of those companies not already discussed, the worst performing company in terms of share price return was Riverstone Energy which has suffered from the decline in global commodity markets. Falling commodities and weakness across Latin American currencies have also contributed to the negative performance of BlackRock Latin American.

Aquila European Renewables is down 20% so far this year with falling power prices in Spain and lower irradiation levels contributing to the weakness over the second quarter. Chrysalis Investments continues to struggle with negative sentiment towards growth stocks. The company has also suffered from several stock specific issues, most notably stories about solvency concerns relating to its second largest holding, Wefox, which did make up around 14% of the fund.

More expensive/cheaper

More expensive (LHS) and cheaper (RHS) relative to NAV

| Fund | Sector | 31 Mar disc (%) |

30 Jun disc (%) |

Fund | Sector | 31 Mar disc (%) |

30 Jun disc (%) |

| Hipgnosis Songs | Royalties | (26.6) | 7.0 | Castelnau Group | Flexible Investment | (2.6) | (22.2) |

| Foresight Sustainable Forestry | Farmland & forestry | (34.8) | (6.7) | Aquila European Renewables | Renewable energy infrastructure | (20.9) | (30.6) |

| Gresham House Energy Storage | Renewable energy infrastructure | (68.0) | (46.7) | VPC Specialty Lending Investments | Debt – direct lending | (32.6) | (41.7) |

| Harmony Energy Income Trust | Renewable energy infrastructure | (61.9) | (43.9) | Regional REIT | Property – UK commercial | (65.7) | (74.4) |

| RTW Biotech Opportunities | Biotechnology & Healthcare | (32.3) | (14.6) | Riverstone Energy | Commodities & natural resources | (36.4) | (44.4) |

| Schiehallion Fund | Growth capital | (32.8) | (15.4) | Golden Prospect Precious Metal | Commodities & natural resources | (14.1) | (22.1) |

| JPMorgan Global Core Real Assets | Flexible investment | (31.1) | (17.2) | Syncona | Biotechnology & healthcare | (34.8) | (42.4) |

| Augmentum Fintech | Financials & financial innovation | (40.0) | (28.9) | Atrato Onsite Energy | Renewable energy infrastructure | (17.1) | (24.4) |

| Cordiant Digital Infrastructure | Infrastructure | (47.7) | (37.2) | Life Science REIT | Property – UK commercial | (51.8) | (58.6) |

| NextEnergy Solar | Renewable energy infrastructure | (31.7) | (22.3) | Gulf Investment Fund | Global emerging markets | (0.8) | (7.4) |

Source: Morningstar, Marten & Co. Note: excludes trusts with market caps below £25m at 30/06/24

Getting more expensive

Of the funds not referenced above, JPMorgan Global Core Real Assets has managed to drive down its discount through share buybacks. The board has also suggested a change to the fund’s investment policy, aimed at giving the manager greater flexibility.

NextEnergy Solar was up strongly following the release of its annual report which accompanied news of progress within its capital recycling programme. The announcement built on some positive momentum generated in recent months and there is hope of more good news to follow on this front.

Getting cheaper

In terms of the trusts getting cheaper, VPC Specialty Lending Investments has fallen steeply since it announced it would be proposing a managed wind down at the end of 2022. Shares have lost almost half their value since the announcement, with the illiquid nature of its investments increasing the challenges of returning capital to investors. Regional REIT announced a deeply discounted rights issue.

Money raised and returned

Money raised (LHS) and returned (RHS) in £m over Q2 2024

| Fund | Sector | £m raised | Fund | Sector | £m returned |

| JPMorgan Global Growth & Income | Global equity income | 91.9 | Scottish Mortgage | Global | (543.5) |

| Ashoka India Equity Investment | India/Indian subcontinent | 48.4 | Smithson Investment Trust | Global smaller companies | (137.8) |

| Globalworth Real Estate Investments | Property – Europe | 28.9 | Finsbury Growth & Income | UK equity income | (80.4) |

| Invesco Bond Income Plus | Debt – loans & bonds | 7.7 | Monks | Global | (73.8) |

| CQS New City High Yield | Debt – loans & bonds | 7.6 | F&C Investment Trust | Global | (61.8) |

Source: Morningstar, Marten & Co. Note 1) value of shares issued/repurchased as at 30 June 2024

Money coming in

The fundraising environment remains difficult. An attempt to launch a new trust to take advantage of falling property values and possible distressed sellers in the space failed to meet its minimum target and was withdrawn. Aberforth managed to rollover its split capital trust into a new vehicle, but this did not attract much new money.

JPMorgan Global Growth and Income has continued to successfully raise capital along with usual suspects, Invesco Bond Income and CQS New City High Yield. Ashoka India Equity Investment has benefited from the stability provided by markets in India and has been able to sustain a stable premium over the past six months. The Globalworth Real Estate trust has also continued to issue shares to satisfy its stock-based compensation plan despite trading at a significant discount.

Money going out

In terms of money going out Scottish Mortgage continues to deliver on its £1bn share buyback scheme, which was announced in the face of stake building by activist investor Elliott Associates. Smithson Investment Trust, Finsbury Growth & Income and Monks regularly feature on this list.

Major news stories over Q2 2024

Visit www.quoteddata.com or more on these and other stories plus in-depth analysis on some funds, the tools to compare similar funds and basic information, key documents and regulatory news announcements on every investment company quoted in London

Upcoming events

Here is a selection of what is coming up. Please refer to the Events section of our website for updates between now and when they are scheduled.

Interviews

Every Friday at 11 am, we run through the more interesting bits of the week’s news, and we usually have a special guest discussing a particular investment company.

Research notes published over Q2 2024

Polar Capital Technology’s (PCT’s) manager remains all in on the artificial intelligence (AI) investment theme, having fine-tuned the portfolio towards the ‘AI enablers’ and ‘AI beneficiaries’ that it considers will outperform the wider sector over the long-term.

In a world where the share prices of AI-related companies have determined the fortunes of global equity markets, Herald Investment Trust (HRI) offers a way to capitalise on these potent tailwinds while still offering an arguably seldom-found discount opportunity within a universe known for its high valuations, coupled with the trust’s shares currently trading on an attractive 11.5% discount to net asset value (NAV).

CQS New City High Yield Fund (NCYF) is consistently one of the highest-dividend-yielding funds in its debt – loans and bonds peer group and, over the longer term, is also one of its best-performing (see page 17). NCYF has benefitted from an uplift in capital values as the headwind of higher interest rates that weighed on bond valuations in 2022 and 2023 has turned tailwind – a trend which its manager, Ian “Franco” Francis, thinks has further to go.

RIT Capital Partners’ (RIT’s) private (unquoted) investments portfolio, which for the past two years has dragged on the trust’s net asset value (NAV) returns, could be the spark for a change in its fortunes over the next 12 months. Several holdings are considering initial public offerings (IPOs) that could present healthy premiums to the typically conservative values that they are held at on RIT’s books and will allow the manager to reallocate capital to areas of the equity and credit markets that it has identified as undervalued.

Charles Montanaro, the manager of Montanaro UK Smaller Companies Investment Trust (MTU), has remained stalwart in the face of investor aversion to the UK equity market. His bullishness is based on the increasingly attractive valuations being assigned to UK equities, as many of MTU’s holdings continue to generate decent earnings based on their historic performance, with several reporting their highest ever annual revenues

Polar Capital Global Financials Trust (PCFT) has had a good six months both in net asset value (NAV) terms, where returns have been ahead of both its MSCI All-Countries World Financials Index performance benchmark and the global MSCI All Countries World Index, and in share price terms, as the share price discount to NAV has narrowed. Next year’s liquidity opportunity (see page 12) ought to help the discount narrow further

After a challenging 18-month period, things are beginning to look a lot brighter for the Ecofin Global Utilities and Infrastructure Trust (EGL). Since the middle of February, strong earnings, artificial intelligence (AI) related momentum behind growing electricity demand, and a shifting macroeconomic outlook have contributed to a 23% bounce in the company’s shares.

Vietnam Holding (VNH) has provided strong absolute and relative returns during the last 12 months, expanding its record of outperformance of both peers and relevant benchmarks. The introduction of a share redemption opportunity at net asset value (NAV) less associated costs (the first of which is on 30 September this year – see page 21) has significantly narrowed VNH’s share price discount to NAV so that a 25.7% NAV return translated into a 48.2% share price return over the 12 month period ended 31 May 2024.

Dan Whitestone, BlackRock Throgmorton’s (THRG’s) manager, believes that the historic selloff of UK equities, with investors taking their money out of UK equities in record numbers, is a behaviour that represents both a disconnect to the strong earnings reported by UK companies, and an attractive valuation opportunity based on the current price of UK equities relative to said earnings.

The AVI Global Trust (AGT) has gone from strength to strength as its managers identify a wealth of opportunities. A share price total return of over 30% in the past year highlights the value of the company’s strategy of targeting high-quality companies whose shares are trading at a discount to their intrinsic value.

Impax Environmental Markets (IEM) invests in good-quality, fast-growing companies that are providing innovative solutions to environmental challenges or improving resource efficiency. The pace of change may be slower in some countries than others and, overall, slower than many of us would like, but it is inexorable, which underpins an attractive long-term outlook for the trust. The advent of higher interest rates in 2022 triggered a widespread sell off of growth stocks and IEM was caught up in this.

By almost every measure, Downing Renewables and Infrastructure Trust (DORE) has delivered above expectations since its IPO in December 2020. A net asset value (NAV) total return of 33% over this period highlights the already strong performance of the trust and there remains significant scope for the asset value to compound further as the portfolio develops.

Lar España Real Estate celebrated its 10-year anniversary last month, and despite facing some potentially crippling challenges to its Spanish retail portfolio in that time – including the COVID-19 pandemic and now a higher interest rate environment – it has consistently posted strong shareholder returns. Its 10-year net asset value (NAV) total return is 57.2%, putting it among the upper echelons of the European retail players.

Having successfully undertaken its latest act of corporate engineering, Grit Real Estate Income Group (Grit) is in a good place to realise substantial capital value and income growth over the medium term. The sale of two assets to meet a capital call by its majority-owned development partner (Gateway Real Estate Africa – GREA) means GREA is well capitalised to deliver a near-term pipeline of developments, including a diplomatic housing scheme pre-let to the US government.

Following a very strong period of outperformance for the commodities and natural resources sector, the last 18 months have been more challenging. However, barring the odd wobble, inflation and interest rates look to be past their peaks. This puts the sector in a strong position to outperform once again, particularly once the attractive valuations on offer are factored in (metals and mining are trading at a 25% discount to broader global equities, while energy is on a 41% discount – see pages 4 and 5).

In common with the other funds in the renewable energy sector, the last six months have continued what has been a challenging period for the Bluefield Solar Income Fund (BSIF), with its ongoing fundamental performance (including strong revenue and earnings growth) failing to reverse a steady slide in its shares which began back in May 2023.

While shares of HydrogenOne Capital Growth (HGEN) have continued to fall, investors should be buoyed by the ongoing growth of the portfolio and the accelerating development of the green hydrogen sector. Despite challenging macro-economic conditions (including stubborn inflation and still elevated interest rates), HGEN’s net asset value (NAV) grew 5.8% over 2023, while the portfolio generated aggregate revenue growth of 125%.

Despite navigating through challenging conditions in 2023, abrdn Private Equity Opportunities (APEO) achieved remarkable success with recently published annual results reporting both positive net asset value (NAV) growth and double-digit share price returns. APEO’s discount to NAV has narrowed by more than 10 percentage points in recent months, so that it is shares are trading on a 28.9% discount currently, narrowing from about 45% last October.

In spite of an uncertain macroeconomic environment, Oakley Capital Investments’ (OCI) underlying portfolio continued to generate robust earnings growth in 2023 (average 14% EBITDA growth), which in turn drove 4% net asset value (NAV) growth. More importantly, OCI achieved an 18% total shareholder return during the period, extending the long run of strong share price performance delivered by the company (an average compound annual growth rate of 24% per year).

Guide

Our independent guide to quoted investment companies is an invaluable tool for anyone who wants to brush up on their knowledge of the investment companies’ sector. Please register on www.quoteddata.com if you would like it emailed to you directly.

Appendix 1 – median performance by share price return over Q2 2024

| Share price Q2 24 TR (%) |

NAV Q2 24 TR (%) |

Discount 30/06/24 (%) |

Median market cap 30/06/24 (£m) |

Number of companies in the sector | |

| Royalties | 48.4 | 0.0 | 7.4 | 1238.2 | 1 |

| Farmland & Forestry | 43.2 | 0.0 | (6.7) | 164.1 | 1 |

| Infrastructure Securities | 13.1 | 7.1 | (12.8) | 107.2 | 2 |

| India/Indian Subcontinent | 12.9 | 12.0 | (12.8) | 433.5 | 4 |

| Technology & Technology Innovation | 12.1 | 10.8 | (8.9) | 2738.5 | 2 |

| UK Smaller Companies | 11.2 | 6.7 | (12.5) | 136.3 | 24 |

| Financials & Financial Innovation | 10.2 | 0.2 | (18.6) | 355.7 | 2 |

| Asia Pacific | 9.1 | 6.3 | (11.7) | 571.1 | 6 |

| Asia Pacific Equity Income | 8.5 | 5.6 | (9.3) | 342.4 | 5 |

| Asia Pacific Smaller Companies | 7.2 | 6.5 | (14.1) | 360.3 | 3 |

| UK Equity Income | 6.2 | 3.6 | (8.8) | 401.9 | 24 |

| UK All Companies | 5.8 | 2.6 | (10.9) | 212.0 | 9 |

| Insurance & Reinsurance Strategies | 5.0 | (0.4) | (8.4) | 35.2 | 2 |

| Flexible Investment | 4.7 | 0.7 | (17.2) | 93.4 | 20 |

| China / Greater China | 4.6 | 4.5 | (10.2) | 181.8 | 4 |

| Share price Q2 24 TR (%) |

NAV Q2 24 TR (%) |

Discount 30/06/23 (%) |

Median market cap 30/06/24 (£m) |

Number of companies in the sector | |

| Property – Europe | 4.3 | 0.0 | (40.3) | 247.3 | 5 |

| Commodities & Natural Resources | 4.1 | 2.0 | (20.9) | 69.9 | 9 |

| Leasing | 4.0 | 1.6 | (33.1) | 133.4 | 7 |

| Renewable Energy Infrastructure | 3.8 | 1.5 | (30.6) | 323.3 | 22 |

| Debt – Structured Finance | 3.5 | 2.8 | (14.3) | 155.0 | 6 |

| Global Equity Income | 3.4 | 0.7 | (10.0) | 324.3 | 7 |

| Private Equity | 3.3 | 0.0 | (36.7) | 493.9 | 19 |

| UK Equity & Bond Income | 3.0 | 4.4 | (10.7) | 269.4 | 1 |

| Global Emerging Markets | 3.0 | 2.3 | (11.9) | 272.2 | 11 |

| Debt – Loans & Bonds | 3.0 | 3.0 | (2.5) | 109.0 | 15 |

| Debt – Direct Lending | 2.8 | 1.7 | (16.5) | 118.3 | 8 |

| Global Smaller Companies | 2.7 | (1.3) | (11.4) | 784.1 | 5 |

| Global | 2.4 | 1.5 | (8.6) | 1058.2 | 16 |

| Country Specialist | 2.4 | 0.9 | (12.6) | 434.1 | 5 |

| North America | 2.1 | (0.4) | (11.0) | 497.6 | 6 |

| Infrastructure | 1.5 | 1.5 | (23.4) | 822.6 | 10 |

| European Smaller Companies | 0.2 | (0.8) | (11.3) | 477.7 | 4 |

| Europe | 0.2 | (0.1) | (9.8) | 444.0 | 7 |

| Hedge Funds | 0.0 | 0.5 | (9.1) | 85.9 | 8 |

| Growth Capital | 0.0 | 0.0 | (42.7) | 129.5 | 7 |

| Property – UK Logistics | (0.2) | 0.0 | (25.7) | 555.0 | 3 |

| Property – Debt | (0.2) | 0.2 | (20.0) | 48.1 | 4 |

| Property – UK Healthcare | (0.4) | 1.4 | (28.4) | 421.8 | 2 |

| Environmental | (0.6) | (3.7) | (25.4) | 81.0 | 3 |

| Property – UK Commercial | (1.1) | 1.7 | (26.2) | 135.1 | 14 |

| Biotechnology & Healthcare | (1.4) | (0.9) | (10.1) | 529.8 | 6 |

| Japan | (2.9) | (2.8) | (9.2) | 307.3 | 6 |

| Property – UK Residential | (3.4) | 0.8 | (55.6) | 156.9 | 7 |

| Property – Rest of World | (3.4) | 0.0 | (69.6) | 22.0 | 4 |

| North American Smaller Companies | (3.6) | (4.5) | (11.9) | 196.6 | 2 |

| Japanese Smaller Companies | (3.6) | (0.8) | (8.8) | 255.4 | 5 |

| (12.4) | (17.5) | (10.5) | 101.9 | 2 | |

| Median | 3.0 | 0.8 | (11.9) | 269.4 | 6 |

Source: Morningstar, Marten & Co. Note: all figures represent median values of the constituent funds from each sector. To 30/06/24

IMPORTANT INFORMATION

This note was prepared by Marten & Co (which is authorised and regulated by the Financial Conduct Authority).

This note is for information purposes only and is not intended to encourage the reader to deal in any of the securities mentioned within it. Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

Marten & Co may have or may be seeking a contractual relationship with any of the securities mentioned within the note for activities including the provision of sponsored research, investor access or fundraising services.

The analysts who prepared this note may have an interest in any of the securities mentioned within it.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.