October 2024

Monthly | Investment companies

Kindly sponsored by abrdn

Winners and losers in October 2024

North American stocks ended October with gains after employment reports failed to hit estimates, recording the lowest increase in jobs since the end of 2020, thereby improving hopes of interest rate cuts. Nevertheless, the dollar strengthened against the pound, and this accounted for the bulk of the NAV appreciation in US dollar-exposed investments over the month (including investment companies in the hedge fund and debt sectors). More growth-focused trusts such as Baillie Gifford US Growth led the pack. As sterling NAVs rose, discounts on US trusts narrowed, boosting share price returns.

Best performing sectors in October 2024 by total price return

| Median share price total return (%) |

Median NAV total return (%) |

Median discount 31/10/24 (%) |

Median sector market cap 31/10/24 (£m) | Number of companies in the sector | |

|---|---|---|---|---|---|

| North America | 5.5 | 3.4 | (11.2) | 518.1 | 6 |

| Hedge funds | 4.3 | 4.1 | (9.1) | 88.0 | 7 |

| Technology & technology innovation | 3.5 | 4.1 | (12.0) | 2,538 | 2 |

| Debt – loans and bonds | 3.5 | 2.3 | 0.4 | 137.7 | 9 |

| Debt – structured finance | 3.4 | 2.1 | (21.0) | 167.2 | 5 |

On the downside, in the wake of the budget, select Property – UK logistics funds suffered share price falls, led by Tritax Big Box REIT, whilst the Property – rest of World sector returns were impacted by discount widening. This included Ceiba Investments, which continues to be hit by macro factors surrounding Cuba’s economic difficulties and worsening relations with the US, and Macau Property Opportunities. Across the globe, Indian equities were affected by a somewhat unexpected large bout of profit taking by foreign investors, with the Nifty 50 index, the country’s top benchmark, falling by over 6%, marking the worst monthly fall since March 2020. It may be that investors had concerns over the weaker than expected Q2 earnings results.

Worst performing sectors in October 2024 by total price return

| Median share price total return (%) |

Median NAV total return (%) |

Median discount 31/10/24 (%) |

Median sector market cap 31/10/24 (£m) | Number of companies in the sector | |

|---|---|---|---|---|---|

| Property – UK logistics | (6.7) | 0.0 | (26.8) | 555.9 | 3 |

| Property – rest of World | (5.8) | 0.0 | (68.1) | 19.1 | 3 |

| India/Indian Subcontinent | (5.0) | (1.4) | (16.4) | 408.0 | 4 |

| Europe | (4.1) | (3.2) | (11.2) | 532.5 | 6 |

| Japan | (4.0) | (1.1) | (15.3) | 284.8 | 5 |

In early October, European stocks had a downturn fuelled by disappointing results from large companies such as the fashion giant LVMH, a core holding for some European focused funds, and higher than expected inflation which has likely scuppered the chances of a 0.5% interest rate cut in December. The benchmark European index Stoxx 600 closed the month with a monthly decline of 3.4%, the worst in a year.

In Japan, uncertainty over the Bank of Japan’s upcoming decisions, and a setback for Prime Minister Shigeru Ishiba as voters in his snap general election deserted the LDP, may have unnerved investors.

Best performing

As above, US dollar strength had a big influence on the table. An all-time high price of gold in October saw both Golden Prospect Precious Metals’ NAV and share price rise by double figures. This has seemingly been driven by increasing concerns surrounding geopolitical risks, alongside the uncertainty of the direction of inflation brought on by potential outcomes of the US election, resulting in investors looking to protect their investments. Elsewhere in the commodities world, Geiger Counter’s NAV was driven by renewed optimism in nuclear energy, in addition to rising prices amidst limited supply due to a Western ban on Russian uranium as the war in Ukraine continues.

Manchester & London’s NAV continues to climb, driven by share price appreciation of its largest holding, Nvidia, with the Bank of America among others, raising its rating for the stock.

PRS REIT enjoyed a 11% growth in NAV from increasing rental income on its private rented housing portfolio which grew by 12% on a like for like basis. Later in the month, the trust announced that it was undertaking a strategic review to consider the future of the company following shareholder pressure. PRS REIT enjoyed a 11% growth in NAV from increasing rental income on its private rented housing portfolio which grew by 12% on a like for like basis. Later in the month, the trust announced that it was undertaking a strategic review to consider the future of the company following shareholder pressure.

Best performing funds in total NAV (LHS) and share price (RHS) terms over October 2024

| Fund | Sector | (%) | Fund | Sector | (%) |

|---|---|---|---|---|---|

| Golden Prospect Precious Metal | Commodities and natural resources | 13.5 | Ecofin US Renewables Infrastructure | Renewable energy infrastructure | 20.1 |

| Manchester & London | Global | 10.3 | Atrato Onsite Energy | Renewable energy infrastructure | 18.6 |

| Geiger Counter | Commodities and natural resources | 9.2 | Livermore Investments | Flexible investment | 16.1 |

| PRS REIT | Property – UK residential | 7.8 | NB Distressed Debt Inv Extended Life | Debt – loans and bonds | 14.0 |

| NB Distressed Debt Inv Extended Life | Debt – loans and bonds | 7.6 | JPMorgan Emerg Europe, ME & Africa | Global emerging markets | 13.7 |

| Third Point Investors USD | Hedge funds | 7.1 | JPEL Private equity | Private equity | 12.1 |

| CQS Natural Resources G&I | Commodities and natural resources | 6.8 | UIL | Flexible investment | 10.9 |

| NB Distressed Debt | Debt – loans and bonds | 6.5 | Golden Prospect Precious Metal | Commodities and natural resources | 10.7 |

| US Solar Fund | Renewable energy infrastructure | 5.1 | US Solar Fund | Renewable energy infrastructure | 10.3 |

| Baillie Gifford US Growth | North America | 5.1 | Life Science REIT | Property – UK commercial | 9.9 |

NB Distressed Debt’s NAV and share price came from the release of $10.7m via cash distributions from an oil & gas asset, that raised the prospect of cash distributions to shareholders. Livermore’s discount narrowed, but it is not clear why, perhaps a delayed reaction to the results it announced at the end of September. In contrast to the share price move, the news on JPMorgan Emerging Europe, Middle East and Africa’s Russian assets was negative – during the month, the company said: “we believe our ability to recover or realise the value of assets has now become even more uncertain”. That makes the share price move all the more puzzling, but since the end of the month, Trump’s win may have improved the odds a little, and perhaps the share price move was in anticipation of this.

It seems that Ecofin US Renewables Infrastructure’s surge in share price is a delayed reaction to the announcement of its windup in September. There has been a fair bit of turnover in the stock which may have cleared out a seller. Also in the Renewable energy infrastructure sector, Atrato Onsite Energy’s share price shot up after news of the sale of all of its solar assets to a joint venture vehicle owned by Brookfield and RAIM Apollo at a headline price of £218.7m.

JPEL Private equity, which is in winddown mode, has entered into a put option arrangement in respect of its largest holding, which could accelerate its chances of turning it into cash. UIL announced plans to go private and began a restructuring of its portfolio.

Worst performing

Home REIT’s place in the table reflects the long-awaited publication of its 2022 annual results. This confirmed a large decrease in NAV, and this was followed by shareholders approving a managed winddown of the portfolio. Two other funds in this table have also since thrown in the towel – Weiss Korea Opportunity Fund, where its board launched a strategic review of the back of weak performance, and JPMorgan Global Core Real Assets (see below).

In the UK, one big factor was the impact of the UK budget, as investors took profits ahead of an expected CGT hike and changes to inheritance tax. AIM shares were particularly affected, disproportionately hitting UK smaller companies trusts.

Rising government bond yields knocked interest rate sensitive sectors such as utilities, infrastructure, renewable energy generation, real estate, and growth capital – hitting funds as diverse as Premier Miton Global Renewables, Seraphim Space, JPMorgan Global Core Real Assets, and Tritax EuroBox.

Literacy Capital had a bad month as news of its first quarterly NAV decline since 2020 was accompanied by a decision to raise management fees and cut its donations to charity.

Worst performing funds in total NAV (LHS) and share price (RHS) terms over October 2024

| Fund | Sector | (%) | Fund | Sector | (%) |

|---|---|---|---|---|---|

| Home REIT | Property – UK residential | (62.7) | JPMorgan Global Core Real Assets | Flexible investment | (14.6) |

| Premier Miton Glb Renewables | Infrastructure securities | (7.7) | Seraphim Space Investment Trust | Growth capital | (13.4) |

| Weiss Korea Opportunity | Country specialist | (7.0) | Oryx International Growth | UK smaller companies | (12.8) |

| Odyssean Investment Trust | UK smaller companies | (6.7) | Literacy Capital PLC | Private equity | (10.2) |

| BlackRock Greater Europe | Europe | (5.2) | Tritax Big Box | Property – UK logistics | (10.2) |

| Henderson Smaller Companies | UK smaller companies | (5.1) | Gresham House Energy Storage | Renewable energy infrastructure | (9.6) |

| Aberforth Geared Value & Income | UK smaller companies | (5.0) | Foresight Solar | Renewable energy infrastructure | (9.4) |

| Fidelity European Trust | Europe | (5.0) | SDCL Energy Efficiency Income | Renewable energy infrastructure | (8.9) |

| Aberforth Smaller Companies | UK smaller companies | (4.8) | Chrysalis Investments Limited | Growth capital | (8.6) |

| Schroder UK Mid Cap | UK all companies | (4.6) | Miton UK Microcap | UK smaller companies | (8.5) |

Moves in discounts and premiums

More expensive (LHS) and cheaper (RHS) relative to NAV over October 2024

| Fund | Sector | Disc/ Prem 30/09/24 (%) |

Disc/ Prem 31/10/24 (%) |

Fund | Sector | Disc/ Prem 30/09/24 (%) |

Disc/ Prem 31/10/24 (%) |

|---|---|---|---|---|---|---|---|

| JPMorgan Emerg Europe, ME & Africa | Global emerging markets | 116.2 | 130.3 | JPMorgan Global Core Real Assets | Flexible investment | (12.2) | (25.6) |

| Atrato Onsite Energy | Renewable energy infrastructure | (27.2) | (14.1) | Literacy Capital | Private equity | (0.9) | (11.0) |

| ICG-Longbow Senior Sec. UK Prop Debt Inv | Property – debt | (43.6) | (34.0) | Oryx International Growth | UK smaller companies | (21.1) | (31.1) |

| Livermore Investments | Flexible investment | (38.0) | (29.6) | Tritax Big Box | Property – UK logistics | (13.4) | (22.4) |

| Jupiter Green | Environmental | (20.0) | (12.1) | Foresight Solar | Renewable energy infrastructure | (18.5) | (27.0) |

We discussed JPMorgan Emerging Europe, Middle East & Africa’s discount narrowing above. Atrato Onsite’s move reflects its portfolio disposal. ICG Longbow (which is in windup) announced some encouraging interim results that suggested that although the NAV had fallen, there was some progress towards realisations. Jupiter Green said in July that it was evaluating options for its future, but there has been no new since.

JPMorgan Core Real Assets announced another fall in its NAV during the month, but (as discussed above) has since decided to implement a managed winddown. As discussed previously, Literacy Capital upset some investors with its management fee hike and charity donation cut. Oryx announced a couple of NAV-boosting disposals that are yet to be reflected in its share price. Tritax Big Box and Foresight Solar are casualties of rising bond yields.

Money raised and returned

Money raised (LHS) and returned (RHS) over October 2024 in £m

| Fund | Sector | £m raised | Fund | Sector | £m returned |

|---|---|---|---|---|---|

| Globalworth Real Estate Investments | Property – Europe | 26.3 | Scottish Mortgage | Global | (163.3) |

| JPMorgan Global Growth & Income | Global equity income | 22.7 | Monks | Global | (44.7) |

| UIL | Flexible investment | 10.1 | F&C Investment Trust | Global | (44.0) |

| Law Debenture | UK equity income | 7.1 | Smithson Investment Trust | Global | (39.6) |

| Invesco Bond Income Plus | Debt – loans and bonds | 4.5 | Finsbury Growth & Income | UK equity income | (36.5) |

Globalworth issued shares to satisfy its scrip dividend. UIL’s share issuance was in connection with its acquisition of the minorities in Zeta Resources. JPMorgan Global Growth & Income, Law Debenture, and Invesco Bond Income Plus continue to be able to drip out shares to satisfy demand and moderate their premium ratings.

On the other side of the equation, the shrinkage of the sector continues with buybacks outweighing share issuance by 110 companies and £836m. We said goodbye to Witan and JPMorgan Japan Small Cap Growth and Income as their respective mergers (with Alliance Trust and JPMorgan Japanese) went through. We also lost Gulf Investments.

The funds returning the most money during October were the usual suspects.

Here at QuotedData we spend a lot of time thinking of new ways to get the message across that the best investment companies can make the best long-term investments.

Every year, the industry hands out awards to the managers and trusts that it thinks are doing the best job for investors, but we thought – why not ask investors what they think?

To keep things simple, we asked a panel of industry experts (see below) to whittle down a long list of funds into a shortlist of four nominees in each of 10 categories, so you get the chance to tell us which of the nominees is your favourite.

The process of judging should not take too long for those of you that know these funds well, but for those that do not, there will be links to information on each trust.

As an incentive, we are offering a £5,000 prize to the lucky judge who gets closest to predicting the winners in each of the 10 categories. If there is more than one of these, the winner will be selected at random from all those that got closest.

Major news stories and QuotedData views over October 2024

Portfolio developments

- VH Global completes two solar projects in Australia

- BioPharma Credit gets exposure to spine surgery specialist Alphatec

- Cordiant Digital Infrastructure makes Belgian Data Centre Acquisitions

- Oakley Capital Investments sells Schülerhilfe

- CQS City Natural Resources benefits from substantial discount narrowing

- Schroder Oriental Income navigates weak Chinese market successfully

- GCP Infrastructure hints at big disposal in the works

- Gore Street Energy Storage’s Big Rock secures 12-year RA contract

- International Public Partnerships backs BeNEX to buy Abellio Germany

- Gulf bows out with another good set of results

- Annual results a sign of what’s to come for Seraphim Space Investment Trust

- Fidelity Emerging Markets delivers welcome performance improvement

- Syncona commits another £19.9m to Purespring Therapeutics

- Oakley Capital Fund V snaps up Assured Data Protection

- 3i Infrastructure receives binding offer for Valorem stake

- RTW backs obesity drug firm

- VietNam Holding delivers knockout year with 43% return

Corporate news

- Henderson International Income to top up dividends from capital

- QuotedData’s October 2024 budget day briefing

- Baillie Gifford Japan convinced it can turn its fortunes around

- VinaCapital Vietnam Opportunity new team in place

- Asia Dragon Trust and Invesco Asia Trust to merge

- Good news for Hansa as Ocean Wilsons sells Brazilian business

- JPMorgan Emerging EMEA Securities updates on Russian court order

- Castlenau’s Dignity buys Augmentum Fintech’s Farewill

- AVI Japan Opportunity to offer annual tender offers

- InfraRed Capital Partners to manage Digital 9 Infrastructure

- Newly merged Alliance Witan appoints new stockpicker

- UIL thinking of going private after bout of poor performance

- Atrato Onsite Energy to sell entire portfolio

Property news

- Regional REIT to install solar panels on offices

- PRS REIT puts itself up for sale

- Starwood European Real Estate Finance’s Irish office portfolio impaired by 50%

- Empiric Student Property raises £56.1m for new acquisitions and refurb projects

- Bidding war hots up for Tritax EuroBox

- CEIBA Investments looks to restructure its 10% convertible bonds

- Residential Secure Income to wind down

- Home REIT finally publishes its 2022 annual results

- Ground Rents Income provides strategy update ahead of continuation vote

- PRS REIT reports impressive results as strategic review looms

- British Land raises £301m to part fund retail park acquisition

- Alternative Income REIT targets greater opportunities with change in investment policy

QuotedData views

Visit www.quoteddata.com for more on these and other stories plus in-depth analysis on some funds, the tools to compare similar funds and basic information, key documents and regulatory news announcements on every investment company quoted in London.

Interviews

Have you been listening to our weekly news round-up shows? Every Friday at 11 am, we run through the more interesting bits of the week’s news, and we usually have a special guest or two answering questions about a particular investment company.

Research

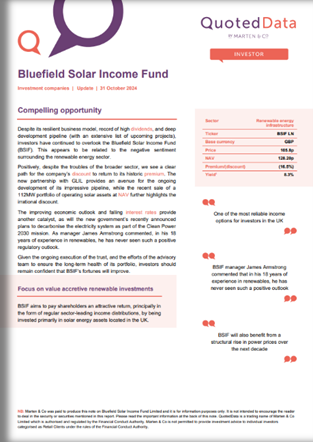

Despite its resilient business model, record of high dividends, and deep development pipeline (with an extensive list of upcoming projects), investors have continued to overlook the Bluefield Solar Income Fund (BSIF). This appears to be related to the negative sentiment surrounding the renewable energy sector.

Positively, despite the troubles of the broader sector, we see a clear path for the company’s discount to return to its historic premium. The new partnership with GLIL provides an avenue for the ongoing development of its impressive pipeline, while the recent sale of a 112MW portfolio of operating solar assets at NAV further highlights the irrational discount.

The improving economic outlook and falling interest rates provide another catalyst, as will the new government’s recently announced plans to decarbonise the electricity system as part of the Clean Power 2030 mission.

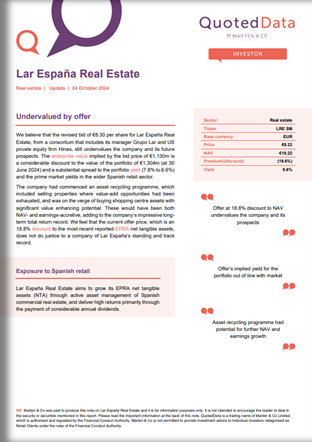

We believe that the revised bid of €8.30 per share for Lar España Real Estate, from a consortium that includes its manager Grupo Lar and US private equity firm Hines, still undervalues the company and its future prospects. The enterprise value implied by the bid price of €1,130m is a considerable discount to the value of the portfolio of €1,304m (at 30 June 2024) and a substantial spread to the portfolio yield (7.8% to 6.6%) and the prime market yields in the wider Spanish retail sector.

The company had commenced an asset recycling programme, which included selling properties where value-add opportunities had been exhausted, and was on the verge of buying shopping centre assets with significant value enhancing potential.

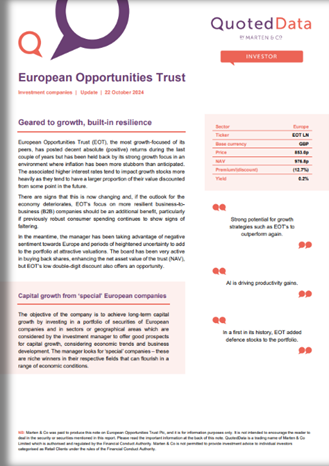

European Opportunities Trust (EOT), the most growth-focused of its peers, has posted decent absolute (positive) returns during the last couple of years but has been held back by its strong growth focus in an environment where inflation has been more stubborn than anticipated. The associated higher interest rates tend to impact growth stocks more heavily as they tend to have a larger proportion of their value discounted from some point in the future.

There are signs that this is now changing and, if the outlook for the economy deteriorates, EOT’s focus on more resilient business-to-business (B2B) companies should be an additional benefit, particularly if previously robust consumer spending continues to show signs of faltering.

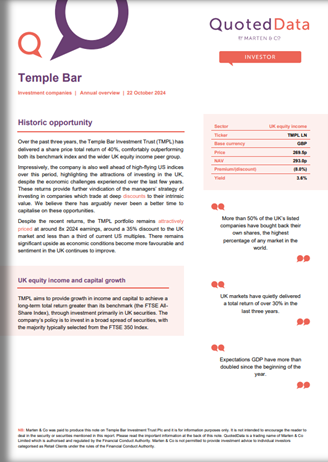

Over the past three years, the Temple Bar Investment Trust (TMPL) has delivered a share price total return of 40%, comfortably outperforming both its benchmark index and the wider UK equity income peer group.

Impressively, the company is also well ahead of high-flying US indices over this period, highlighting the attractions of investing in the UK, despite the economic challenges experienced over the last few years. These returns provide further vindication of the managers’ strategy of investing in companies which trade at deep discounts to their intrinsic value. We believe there has arguably never been a better time to capitalise on these opportunities.

Having delivered impressive returns through 2023, Japanese markets have continued to rise this year, although it has not been entirely smooth sailing for the world’s third-largest economy. A tumbling currency and a 41-year high for inflation set the stage for successive interest rate hikes for the first time in almost two decades. The second of these sent ripples through the stock market, contributing to a historic sell-off for Japanese equities. The recent volatility has been particularly harrowing for yen-sensitive exporters (which benefit from a falling currency), which include some of Japan’s largest companies. Positively, JPMorgan Japanese Investment Trust (JFJ) has very limited exposure to these sectors of the market, focusing instead on high-quality growth stocks that stand to benefit from the structural changes occurring across the economy.

Upcoming events

Here is a selection of what is coming up. Please refer to the Events section of our website for updates between now and when they are scheduled:

- UIL AGM 2024

- Custodian Property Income REIT shareholder presentation 2024

- JPMorgan Asia Growth & Income EGM 2024

- abrdn Asia Focus shareholder presentation 2024

- Partners Group Private Equity shareholder presentation 2024

- abrdn UK Smaller Companies Growth EGM 2024

- CQS New City High Yield Fund shareholder presentation 2024

- Schroder BSC Social Impact EGM 2024

- JPMorgan Global Emerging Markets Income AGM 2024

- JPEL Private Equity AGM 2024

- Warehouse REIT shareholder presentation 2024

- European Opportunities Trust AGM 2024

- JPMorgan Global Growth & Income AGM 2024

- Pacific Horizon Investment Trust AGM 2024

- Fidelity Asian Values AGM 2024

- Invesco Global Equity Income Trust AGM 2024

- Polar Capital Global Healthcare shareholder presentation 2024

- Capital Gearing Trust shareholder presentation 2024

- Mello 10th Anniversary – Derby Conference

- Biotech Growth Trust shareholder presentation 2024

- HICL Infrastructure shareholder presentation 2024

- Rockwood Strategic shareholder presentation 2024

- Tritax Eurobox EGM 2024

- NextEnergy Solar Fund shareholder presentation 2024

- Artemis Alpha Trust EGM 2024

- Polar Capital Global Financials shareholder presentation 2024

- Polar Capital Technology shareholder presentation 2024

- Foresight Environmental Infrastructure shareholder presentation 2024

- Seraphim Space Investment Trust shareholder presentation 2024

- JPMorgan UK Small Cap Growth & Income AGM 2024

- European smaller companies AGM 2024

- Schroder Real Estate shareholder presentation 2024

- Seraphim Space Investment Trust AGM 2024

- DP Aircraft I AGM 2024

Appendix 1 – median performance by sector, ranked by 2024 year to date price total return

| YTD Rank |

Sector | Share price total return YTD (%) | NAV total return YTD (%) |

Discount 30/09/24 (%) |

Discount 31/10/24 (%) |

Change in discount (%) |

Median mkt cap 31/10/24 (£m) |

|---|---|---|---|---|---|---|---|

| 1 | Leasing | 24.4 | 12.6 | (32.4) | (32.4) | (0.0) | 157.1 |

| 2 | Debt – structured finance | 22.2 | 7.6 | (19.5) | (21.0) | (7.4) | 162.8 |

| 3 | Technology & technology innovation | 19.8 | 23.1 | (11.5) | (12.0) | (4.3) | 2,461.8 |

| 4 | North America | 17.1 | 14.0 | (11.9) | (11.2) | (5.4) | 434.0 |

| 5 | Asia Pacific Equity Income | 12.2 | 12.5 | (11.1) | (10.7) | (3.3) | 336.1 |

| 6 | Debt – loans and bonds | 11.2 | 8.6 | (1.8) | (0.4) | (119.7) | 213.0 |

| 7 | Environmental | 9.6 | 4.1 | (20.0) | (12.2) | (39.2) | 286.6 |

| 8 | Global Equity Income | 9.4 | 8.0 | (8.9) | (10.3) | (15.0) | 401.0 |

| 9 | Hedge funds | 9.2 | 3.2 | (12.0) | (9.1) | (23.8) | 197.6 |

| 10 | UK All Companies | 9.2 | 9.3 | (10.7) | (10.3) | (4.4) | 110.7 |

| 11 | Asia Pacific | 9.2 | 12.1 | (12.4) | (14.3) | 15.2 | 269.9 |

| 12 | China / Greater China | 9.2 | 14.3 | (13.1) | (13.2) | 0.6 | 108.2 |

| 13 | Global | 8.9 | 8.8 | (9.0) | (10.1) | 11.9 | 539.0 |

| 14 | Japanese smaller companies | 8.8 | 10.9 | (8.5) | (6.9) | (18.4) | 490.7 |

| 15 | Global emerging markets | 8.3 | 10.2 | (11.6) | (13.9) | 19.8 | 470.3 |

| 16 | Growth capital | 8.2 | 0.0 | (38.2) | (39.6) | 3.5 | 435.5 |

| 17 | UK smaller companies | 8.2 | 7.8 | (11.6) | (11.2) | (2.7) | 359.7 |

| 18 | UK Equity & Bond Income | 7.7 | 7.8 | (7.8) | (9.0) | 14.9 | 137.8 |

| 19 | Asia Pacific smaller companies | 7.5 | 12.4 | (15.2) | (15.0) | (1.1) | 1,021.1 |

| 20 | Biotechnology & Healthcare | 7.5 | 5.9 | (9.7) | (11.3) | 17.2 | 86.7 |

| 21 | Debt – Direct Lending | 7.4 | 2.5 | (15.9) | (17.7) | 11.6 | 331.2 |

| 22 | India/Indian Subcontinent | 7.4 | 16.0 | (13.5) | (16.4) | 21.0 | 354.1 |

| 23 | Insurance & Reinsurance Strategies | 7.4 | 49.9 | (30.3) | (31.2) | 2.7 | 292.8 |

| 24 | UK equity income | 7.1 | 8.3 | (6.9) | (8.1) | 17.6 | 116.7 |

| 25 | Commodities and natural resources | 6.9 | 0.3 | (16.8) | (18.9) | 12.2 | 217.0 |

| 26 | Property – UK Healthcare | 6.5 | 8.2 | (22.2) | (24.6) | 10.9 | 406.5 |

| 27 | Financials & Financial Innovation | 6.3 | 12.5 | (5.9) | (23.8) | 302.9 | 570.4 |

| 28 | European smaller companies | 5.9 | 2.2 | (10.8) | (11.1) | 3.2 | 62.4 |

| 29 | Property – Europe | 5.9 | (8.7 | (33.2) | (32.8) | (1.4 | 790.1 |

| 30 | Infrastructure securities | 5.0 | 0.4 | (13.8) | (10.5) | (23.6) | 90.8 |

| 31 | North American smaller companies | 4.1 | 5.4 | (10.3) | (10.8) | 4.3 | 520.4 |

| 32 | Japan | 3.9 | 8.8 | (12.3) | (15.3) | 23.7 | 80.4 |

| 33 | Flexible investment | 3.2 | 4.9 | (17.1) | (24.8) | 44.7 | 32.9 |

| YTD Rank |

Sector | Share price total return YTD (%) | NAV total return YTD (%) |

Discount 30/09/2024 (%) |

Discount 31/10/24 (%) |

Change in discount (%) |

Median mkt cap 31/10/24 (£m) |

|---|---|---|---|---|---|---|---|

| 34 | Country specialist | 2.4 | 8.0 | (13.1) | (12.5) | (4.5) | 220.4 |

| 35 | Property – UK Commercial | 1.7 | 0.0 | (16.7) | (18.5) | 10.5 | 127.3 |

| 36 | Property – UK Residential | 1.3 | (4.1) | (57.1) | (40.8) | (28.5) | 251.4 |

| 37 | Property – Debt | 1.0 | 1.6 | (27.9) | (23.8) | (14.6) | 205.0 |

| 38 | Global smaller companies | 0.3 | 6.1 | (11.4) | (11.5) | 1.6 | 469.0 |

| 39 | Europe | (0.6) | 1.5 | (10.1) | (11.2) | 10.3 | 595.6 |

| 40 | Infrastructure | (0.7) | 5.3 | (15.7) | (19.7) | 25.7 | 46.4 |

| 41 | Private equity | (1.1) | 0.1 | (34.4) | (34.8) | 1.0 | 936.2 |

| 42 | Property – UK Logistics | (4.1) | 3.5 | (21.3) | (26.8) | 26.1 | 178.2 |

| 43 | Renewable energy infrastructure | (9.4) | (0.2) | (27.3) | (27.0) | (0.9) | 299.6 |

| 44 | Property – Rest of World | (21.0) | (17.8) | (66.4) | (68.1) | 2.5 | 20.7 |

| 45 | Latin America | (26.2) | (24.2) | (12.7) | (13.8) | 8.6 | 96.0 |

| MEDIAN | 7.4 | 7.6 | (13.1) | (13.9) | 3.5 | 276.2 |

Guide

Our independent guide to quoted investment companies is an invaluable tool for anyone who wants to brush up on their knowledge of the investment companies’ sector. Please register on www.quoteddata.com if you would like it emailed to you directly.

IMPORTANT INFORMATION

This note was prepared by Marten & Co (which is authorised and regulated by the Financial Conduct Authority).

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it. Marten & Co is not authorised to give advice to retail clients. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

Marten & Co may have or may be seeking a contractual relationship with any of the securities mentioned within the note for activities including the provision of sponsored research, investor access or fundraising services.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained in this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained in this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.