Dual-use SpaceTech: a strategic shift, not a short-term trend

Rising global defence spending, with many NATO countries now meeting or exceeding previous commitments, has made SpaceTech a higher priority for governments and major contractors. This shift in priorities is feeding directly into the commercial market. Investment in SpaceTech is also rebounding, with $10.4bn raised in the third quarter of 2025, close to the $10.9bn peak in the second quarter of 2021.

Seraphim Space Investment Trust (SSIT) is well positioned in dual-use SpaceTech and has seen strong NAV growth over the last year, helped by valuation uplifts across a number of core holdings. With several of SSIT’s companies showing revenue growth, we believe there could be much more to come. This could help reduce SSIT’s mid-30s discount to net asset value (NAV), which we see as far too wide.

The world’s first listed SpaceTech fund

A diversified, international portfolio of predominantly growth-stage, privately-financed ‘SpaceTech’ businesses that have the potential to dominate their field and are category leaders with first mover advantages in areas such as global security (defence), climate and sustainability, connectivity, autonomous mobility, telecommunication and smart cities.

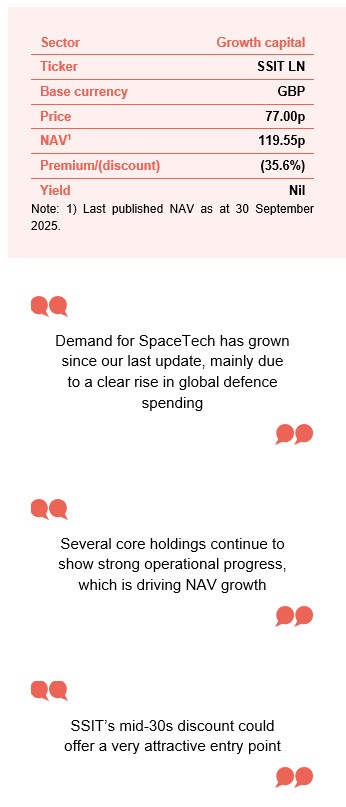

At a glance

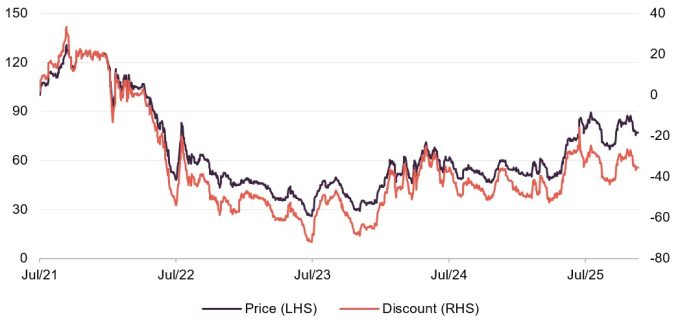

Share price and discount

Over the past year, SSIT’s shares have traded at discounts to NAV ranging from 52.5% to 15.9%, with an average discount of 38.7%. On 1 December, the discount was 35.6%.

Although SSIT’s discount is still large, it has been narrowing gradually. Other growth capital funds also trade at wide discounts, but SSIT stands out due to its focus on space technologies and increased interest in defence spending.

Time period 14 July 2021 to 1 December 2025

Source: Bloomberg, Marten & Co

Performance over five years

SSIT’s portfolio companies do not follow fixed valuation schedules. Instead, fair values are updated after specific events like funding rounds or major developments. This approach reduces unnecessary NAV swings but may mean some holdings show no valuation change for a period.

Time period 14 July 2021 to 30 November 2025

Source: Bloomberg, Marten & Co

| Year ended | Share price total return (%) | NAV total return (%) | MSCI World Aerospace and Defence TR (%) |

|---|---|---|---|

| 30/11/2022 | (59.5) | 1.0 | 20.0 |

| 30/11/2023 | (30.8) | (8.1) | 9.1 |

| 30/11/2024 | 74.3 | (2.6) | 31.0 |

| 30/11/2025 | 29.1 | 27.2 | 35.5 |

Source: Bloomberg, Marten & Co

Fund profile

More information is available on the trust’s website investors.seraphim.vc

SSIT aims to generate long-term capital growth by investing in a diversified international portfolio of SpaceTech companies. These are businesses that use space-based connectivity, navigation, or timing signals, or whose technology is linked to or benefits from the space sector.

Launched in July 2021, SSIT met its fundraising target and began with around £178.4m in cash. By the end of September 2025, total assets had grown to £283.6m.

SSIT’s alternative investment fund manager is Seraphim Space Manager LLP.

Measuring success

SSIT aims for annualised NAV returns of 20% over the long term. While it does not have a formal benchmark, we have used the MSCI World Aerospace and Defence Index for comparison in this note, as does the company itself.

Manager’s view

Demand for SpaceTech has grown since our last update on SSIT, mainly due to a clear rise in global defence spending and changes in procurement. NATO members are now committing to much higher defence budgets, with Germany announcing €34bn for space investment by 2030 – an unprecedented move that shows how quickly space has moved to the centre of national security.

The manager notes that contract activity is picking up, especially in the more established areas of the commercial space market. For example, SSIT’s portfolio company ICEYE has secured six multi-sovereign contracts in six months, some worth over €100m.

This shift in procurement is also reflected in public markets. Major US and European aerospace and defence companies have seen their share prices rise as investors factor in long-term defence projects and the growing importance of space-based capabilities. SSIT’s discount has narrowed with improved sentiment, but the manager warns that this may not last, as some analysts continue to compare the trust to broader private equity funds where discounts remain wider.

The manager believes the investment environment is much healthier than in recent years. Space-sector investment levels are close to previous highs, now with more deals in the $200m–300m range, often focused on defence. China has become a more active investor in SpaceTech, and this is expected to grow over the next three years. Notably, the IPO market has reopened for SpaceTech companies, with Firefly Aerospace planning a 2025 debut. Voyager Technologies’ successful $868m IPO, the largest space IPO to date, is seen by SSIT’s manager as a positive signal for future portfolio exits.

The manager highlights strong demand for Intelligence, Surveillance and Reconnaissance (ISR) and in-space security, especially in Europe. Europe launched only one defence satellite in 2024, compared to over 100 each by the US and China, showing a significant capability gap. As European governments address this, portfolio companies like ICEYE, HawkEye 360 and SatVu are well placed to benefit. There is also growing interest in resilient satellite communications, next-generation navigation (with Xona emerging as a key provider), and long-duration space power solutions from new holding Zeno Power.

Within the portfolio, value growth continues across both private and listed holdings, helped by realisations from Astroscale, AST, Arqit, and Spire Global. Proceeds have been reinvested into new private opportunities more closely aligned with defence demand.

The manager notes some challenges, such as delays in US government payments and contracts, which have slowed progress for some US-focused businesses like ALL.SPACE. However, the outlook is positive, with European and Japanese contracting expected to pick up, more M&A activity likely from defence contractors, and a more open IPO market for quality assets.

Constellation deployments are unlocking the value of high-frequency Earth observation and low Earth orbit (LEO)-based navigation, with large consultancies now promoting these services to corporate clients. Currently, about 80% of portfolio revenues come from defence, but the manager expects this to shift to mainly commercial sources within five years as demand for space data grows.

Overall, the manager believes SSIT is well positioned at the intersection of defence modernisation, AI-driven analytics, and the growing use of space data in industry, with recent contract wins and portfolio resilience supporting this view.

Asset allocation

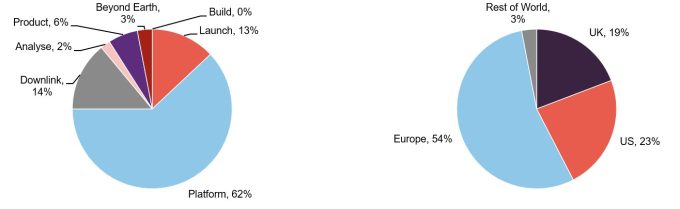

At 30 June 2025, SSIT held 25 direct investments valued at £259.8m, up from £201.5m a year earlier, driven by valuation gains and selective follow-on investments. The portfolio remains concentrated, with the top 10 holdings making up 82.7% of NAV, slightly down from 84.0% at 30 June 2024. As shown in Figure 1, SSIT still offers exposure to a wide range of SpaceTech subsectors. The manager notes the portfolio is focused on leading companies with strong growth potential, rather than taking a broad-brush approach.

The portfolio is built around high-quality, leading companies, with investments spread across different subsectors and countries to reduce risk.

Platform businesses make up 62% of NAV, showing SSIT’s focus on firms developing space-based infrastructure with strong operating leverage, such as ICEYE’s SAR constellation and Xona’s new LEO PNT network. The portfolio also includes product analytics and new “beyond Earth” applications.

As shown in Figure 2, the portfolio remains geographically diverse as of 30 June 2025, avoiding heavy reliance on any single country.

Figure 1: SSIT portfolio by sub-sector as at 30 June 2025

Figure 2: SSIT portfolio by geography as at 30 June 2025

Source: Seraphim Space

Source: Seraphim Space

Recent investment activity

£14.2m invested over FY 2025

SSIT invested £14.2m in new and follow-on investments during the year, including £5.8m more in ALL.SPACE, £4.0m in Zeno, and further funding for Xona, Skylo, ChAI and PlanetWatchers.

£1.5m invested over the first quarter of FY 2026

In the first quarter of FY2026, SSIT made three follow-on investments totalling £1.5m: £1.1m in ALL.SPACE, £0.3m in QuadSat and £0.1m in Taranis. The manager says these targeted investments support promising companies in reaching key milestones.

Full exits of listed holdings – Arqit and Spire Global

SSIT fully exited Arqit (0.9% of NAV at September 2025), selling after a share price rally in October 2025. The sale raised £3.3m, equal to 15% of the original sterling cost. Spire Global (0.8% of NAV) was also sold in October 2025, with proceeds of £2.9m, or 29% of the initial cost.

Portfolio cash runway and SSIT cash burn

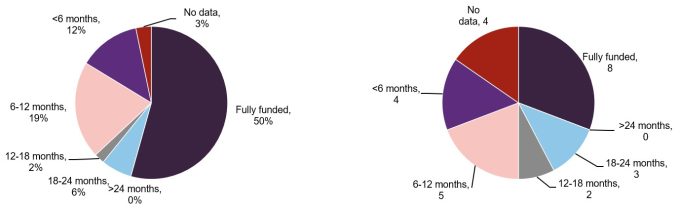

Figures 3 and 4 show SSIT’s portfolio split by funding needs to reach cash-flow break-even, both by value and number of companies, as at 30 June 2025. These are based on the latest forecasts from portfolio company management. In its first quarter FY2026 results, SSIT reported that about half the portfolio, representing 69% of fair value, had a solid cash runway: 58% were fully funded and another 11% funded for at least 12 months from 30 September 2025. At that date, SSIT held £19.4m in cash (down from £21.5m at 30 June 2025), with an extra £8.7m of potential liquidity from listed holdings. SSIT remains disciplined in its spending, making selective follow-on investments to help manage funding risks.

Figure 3: SSIT portfolio by funding duration as at 30 June 2025 (fair value)

Figure 4: SSIT portfolio by funding duration at 30 June 2025 (number of co.s)

Source: Seraphim Space

Source: Seraphim Space

US2.1bn was raised by SSIT’s portfolio companies during FY2025.

In the year to 30 June 2025, portfolio companies raised about $2.1bn, up from around $900m the previous year. Of this, $390m was raised by private companies, with the rest from listed holdings. Among the 10 private companies completing funding rounds, about 60% had strong involvement from outside investors. This highlights ongoing interest in SpaceTech and growing confidence in the portfolio’s commercial progress.

Several core holdings continue to show strong operational progress, with better revenue visibility and clearer paths to EBITDA profitability. With SSIT receiving income and its companies raising capital at reasonable valuations, we believe portfolio funding needs are manageable.

The trust’s balance sheet remains healthy without new equity issuance, supported by disciplined recycling and selective follow-on investments. During the period, some holdings, including ICEYE, moved from last-round or basket-based valuations to multiple-based methods, with ICEYE seeing a notable uplift due to strong bookings, revenue growth, and emerging profitability.

Maturity profile

SSIT is a growth capital fund focused on companies that have progressed beyond the early seed and series A stages. It invests in more established businesses that have commercialised, or are close to commercialising, their products and are moving towards profitability. SSIT uses Seraphim’s venture capital arm to screen out higher-risk, early-stage start-ups. Most of SSIT’s investments are made in the later stages of funding, with about 70% in series C or D rounds, which are typically just before a company goes public.

Top holdings

Figure 5 shows SSIT’s top 10 holdings as at 30 September 2025 and the changes since 31 December 2024, which was the last available data when we previously reported. New entries to the top 10 are Skylo, Zeno, and Tomorrow.io, while AST SpaceMobile, PlanetWatchers, and Seraphim Space Ventures II have dropped out. We discuss some key developments below. More details on SSIT’s holdings are available in our earlier notes, as referenced on page 18.

Figure 5: SSIT 10-largest holdings as at 30 September 2025

| Stock | Subsector | Country | As at 30/09/25 (%) | As at 30/06/25 (£m) | As at 31/12/24 (£m) | Change (£m) |

|---|---|---|---|---|---|---|

| ICEYE | Platform/Earth observation | Finland | 34.7 | 98.5 | 52.4 | 46.1 |

| D-Orbit | Launch/in-orbit services | Italy | 12.1 | 34.2 | 32.4 | 1.8 |

| ALL.SPACE | Downlink/ground terminals | UK | 10.5 | 29.8 | 28.5 | 1.3 |

| HawkEye 360 | Platform/Earth observation | US | 10.4 | 29.6 | 22.0 | 7.6 |

| LeoLabs | Product/data platforms | US | 4.4 | 12.4 | 13.1 | (0.7) |

| SatVu | Platform/Earth observation | UK | 3.9 | 11.2 | 11.2 | – |

| Xona Space Systems | Platform/navigation | US | 3.7 | 10.5 | 6.2 | 4.3 |

| Skylo | Satcoms | US | 1.6 | 4.5 | N/A | N/A |

| Zeno | Space infrastructure | US | 1.3 | 3.7 | N/A | N/A |

| Tomorrow.io | Data platforms | US | 1.3 | 3.7 | N/A | N/A |

| Total of top 10 | 83.9 | 238.1 | 169.2 | 68.9 |

Source: Seraphim Space

ICEYE – accelerating growth as defence demand scales

ICEYE has strengthened its position as a top commercial synthetic aperture radar (SAR) provider with major defence contracts and new products in 2025. Notable developments include a $168m deal with the Finnish Defence Forces for sovereign SAR capability and the launch of a deployable intelligence, surveillance, and reconnaissance (ISR) Cell. ICEYE has expanded its satellite network with six more satellites launched on SpaceX Falcon 9’s Transporter-14. It is investing over €250m to increase manufacturing and develop next-generation SAR technology, backed by a €41.1m Business Finland R&D package.

The company is securing major contracts with NATO-aligned countries such as the Netherlands, Portugal and Japan. Notably, it signed a deal with Japan’s IHI Corporation for four satellites and an image system, with an option for 20 more in the future.

ICEYE’s strong contract pipeline, growing international presence, and ongoing innovation, including its new ‘Tactical Access’ premium tasking service launched in October, position it well for further growth.

D-Orbit – continued progress as in-space logistics expands

D-Orbit is strengthening its role in in-space logistics, especially in last-mile space transport. During the period, it launched its 18th and 19th Orbital Transfer Vehicles (OTVs) on SpaceX’s Transporter-14 mission in June 2025. These OTVs help deploy, reposition, and host payloads for a growing number of satellite customers. As more satellite constellations are launched and operators look for cost-effective orbital logistics, D-Orbit is well positioned to benefit from long-term growth in in-space servicing and mobility.

ALL.SPACE – strengthening its position in resilient multi-orbit connectivity

ALL.SPACE made strong progress in 2025 as demand increased for secure, multi-orbit communications in defence and government sectors. The company secured €3.4m from the European Space Agency to speed up the integration of 5G Non-Terrestrial Networks into its new hybrid terminals, allowing smooth switching between satellite and mobile networks and supporting Europe’s aim for independent communications.

Momentum continued with an agreement with Telesat Government Solutions, enabling ALL.SPACE’s Hydra terminals to be certified for the upcoming Lightspeed LEO network, already used by the US Navy and Army, and designed for reliable connectivity across GEO, MEO and LEO satellites.

Recently, ALL.SPACE expanded its software through partnerships with the European Space Agency and Aalyria, combining its multi-orbit hardware with advanced software to deliver secure, low-latency connections in challenging environments. With advanced hardware and growing software capabilities, ALL.SPACE is well placed to benefit from rising defence demand for reliable satellite communications.

HawkEye 360 – expanding capacity as RF intelligence demand accelerates

HawkEye 360 has expanded its space-based radio-frequency intelligence network, strengthening its role as a signals intelligence provider for government and defence clients. In June 2025, it launched its twelfth satellite cluster, enabling dawn-to-dusk orbital coverage and a Ka-band downlink for greater future data capacity. Cluster 12 became fully operational in September, improving global monitoring for interference detection, maritime awareness, and strategic intelligence. Development of Cluster 13 is underway, with more clusters contracted. SSIT’s manager notes the business is well positioned as global defence budgets rise, especially among NATO countries, where demand for commercial RF geolocation services is increasing.

LeoLabs – strengthening role in space safety and orbital traffic management

LeoLabs is strengthening its position in space situational awareness as governments focus more on space safety and protecting satellites. In August 2025, the company signed a Space Act Agreement with NASA to test how LeoLabs’ detailed tracking data and safety analytics can help prevent satellite collisions and improve orbital traffic management. NASA will review LeoLabs’ radar data, safety products, and its commercial catalogue of nearly 25,000 tracked objects in low Earth orbit, highlighting the growing role of commercial providers in national space safety efforts.

SSIT’s manager notes that as space becomes more crowded and competitive, LeoLabs’ ability to provide tracking accuracy within 10 metres and real-time monitoring puts it in a strong position to meet increasing regulatory and operational needs.

SatVu – advancing thermal intelligence as government traction grows

SatVu has continued to grow in 2025 as demand rises for high-resolution thermal imaging in defence, climate, and infrastructure monitoring. Despite losing its first satellite, the company has shown strong commercial progress. Data from HotSat-1 proved the value of its infrared technology, leading to $6m in pre-orders for HotSat-2, alongside a $10m insurance payout, and manufacturing support from Surrey Satellite Technology Ltd to resolve earlier problems.

Recently, SatVu secured a contract worth up to €3m from the European Space Agency to provide thermal data to the Copernicus programme over three years. SSIT’s manager notes that SatVu has strengthened ties with defence users, providing thermal training to NATO personnel through the APSS initiative. Its technology can detect activities like vehicle movement and energy use, adding valuable insight for intelligence missions.

Xona Space Systems – developing next-generation GPS

Xona Space Systems is expanding Pulsar, its next-generation low Earth orbit navigation satellite network. The company raised $92m in Series B funding led by Craft Ventures, bringing total funding to over $150m, including a $20m award from the US Space Force. Xona has launched Pulsar-0, its first production satellite, moving closer to offering encrypted, spoof-resistant, centimetre-level positioning as a commercial alternative to traditional global navigation satellite systems. SSIT’s manager notes that, with growing concerns about GNSS vulnerabilities, Xona is well placed as a leading provider of secure navigation services.

Skylo – expanding its footprint in direct-to-device connectivity

Skylo has strengthened its role as a leading Non-Terrestrial Network provider, securing several important partnerships in 2025 to expand its global presence. This year, Skylo enabled satellite messaging on Samsung’s latest Galaxy Z Fold7 and Z Flip7 through Verizon, a key move towards mainstream direct-to-device services. The company also expanded its partnership with Garmin, adding satellite messaging and SOS features to the new fēnix 8 Pro watches in the US, Canada, and Europe.

In the IoT sector, Tele2 launched Sweden’s first 3GPP-compliant satellite IoT service using Skylo’s technology, allowing devices to switch smoothly between terrestrial and satellite networks for consistent coverage in remote areas. SSIT’s manager notes that, with a growing network of device, operator, and semiconductor partners, Skylo is well placed to benefit from increasing global demand for reliable connectivity.

Zeno Power – compact nuclear power for extreme environments

Zeno Power is strengthening its leadership in next-generation radioisotope power systems by securing key partnerships and access to essential materials for long-term energy supply. Earlier this year, SSIT joined Zeno’s $50m Series B funding round to support the development of compact nuclear batteries that deliver reliable power for years in space, deep ocean, and polar environments where traditional energy sources are not practical.

Recently, Zeno signed a multi-million-dollar deal with French nuclear specialist Orano to acquire Americium-241, a valuable isotope from nuclear waste with a half-life of over 400 years. This enables Zeno to create higher-power, longer-lasting radioisotope systems for missions such as deep-space exploration and human operations near nuclear sources.

SSIT’s manager believes that with rising demand from government and commercial users for resilient, maintenance-free power, Zeno is well placed to become a key supplier of nuclear energy solutions for challenging environments.

Tomorrow.io – next-generation weather intelligence

Tomorrow.io is strengthening its role as a top provider of real-time, high-resolution weather data, supporting sectors like aviation, defence, logistics, and national resilience. The company is advancing its global weather-satellite network, aiming to improve how often and how accurately weather data is collected for key forecasting needs.

Although there have been no major updates since our last report, SSIT’s manager notes that Tomorrow.io remains a key player in the shift towards space-based climate and operational intelligence. Its hyper-local insights help government and commercial users plan for, reduce, and respond to more volatile weather – an increasing priority for many countries.

Performance

H2 FY2025

As of 30 June 2025, SSIT’s total NAV was £281.1m (118.52p per share), up 17.2% from £239.7m (101.04p per share) at 31 December 2024, and 27.1% higher than £228.1m (96.18p per share) a year earlier. The main driver of this growth was unrealised fair value gains in the portfolio, mainly due to defence and geopolitical trends. The manager expects SSIT to keep benefiting from rising government and commercial spending on space security and modernisation, supporting further NAV growth.

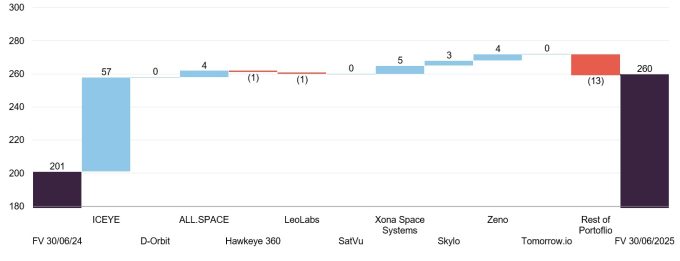

Figure 6: Investment portfolio movements

Source: Seraphim

ICEYE, which doubled in value over the year, was by far the main driver of performance (see Figure 6). SSIT’s manager notes that private holdings continue to meet key milestones, with several achieving strong revenue growth. Many management teams now expect to reach EBITDA profitability before the end of 2025, which could support further NAV growth as these holdings become less risky. The manager attributes this performance to both stock selection and rising demand in the SpaceTech sector.

The manager also highlights that the unrealised gains show the progress made by the portfolio companies. SSIT remains actively involved in helping its holdings realise value through IPOs, M&A, or secondary sales.

Figure 6 shows the changes in fair value of SSIT’s holdings. The total value of the portfolio rose by 28.9% over the year, from £201.5m to £259.8m. Among companies that raised new funds, only D-Orbit saw a lower valuation due to a down-round; three had higher valuations, and six were unchanged. Despite this, D-Orbit’s value at June 2025 was still 288% above SSIT’s original investment. By the end of June 2025, all but two of SSIT’s top 10 holdings were valued above cost, with a median fair value to cost ratio of 108%, ranging from 86% to 288%.

SSIT’s portfolio companies do not follow fixed valuation schedules. Instead, fair values are updated after specific events like funding rounds or major developments. This approach reduces unnecessary NAV swings but may mean some holdings show no valuation change for a period.

First quarter FY2026

On 25 November 2025, SSIT reported its first quarter results for the current financial year. As of 30 September 2025, total NAV reached £283.6m (119.55p per share), up 0.9% over the quarter and setting a new record, following a similar achievement at 30 June. The portfolio’s fair value rose by 1.9% (£4.9m) to £264.7m. This included a £0.4m decrease in unrealised fair value, which was more than offset by a £3.8m foreign exchange gain and £1.5m in follow-on investments.

HawkEye 360’s fair value increased by £9.0m over the quarter, reflecting strong business performance and ongoing corporate activity, though no details were given. ICEYE’s fair value fell by £1.6m to £98.5m, which managers say is to fully reflect the terms of ongoing corporate activity. While details are not disclosed, ICEYE continues to show strong operational progress, and the corporate activity is likely aimed at supporting its growth. The manager notes that both ICEYE and HawkEye360 are currently involved in corporate activity, so their valuations in SSIT’s NAV are not based on the usual multiples method. Instead, they are being priced according to these events. The manager expects both companies to return to the standard multiples valuation within six months and sees further growth for both over the next year.

Portfolio returns

SSIT’s positive NAV growth was driven by unrealised returns

From its launch on 14 July 2021 to 30 November 2025, SSIT delivered a NAV total return of 22.0%. Although its listed equity holdings held back performance, this was outweighed by gains in its unlisted portfolio.

We continue to compare SSIT to the MSCI Aerospace and Defence Index. The index slightly outperformed SSIT’s NAV until October 2023, when it surged following the Israel-Gaza conflict. Ongoing geopolitical tensions and the events of “Liberation day” in April have since accelerated the index’s gains.

Figure 7: SSIT performance from launch to 30 November 2025

Source: Bloomberg, Marten & Co

We believe SSIT benefits from the same positive trends as defence stocks, so the current gap in performance is unlikely to last. In our view, SSIT has strong potential to catch up. We remind readers that SSIT’s manager estimates that around 70% of the portfolio is linked to defence, and says the companies invested in are showing increasing profits.

Figure 8: SSIT performance over periods ended 30 November 2025

| 3 months (%) | 6 months (%) | 1 year (%) | 3 years (%) | Since launch (%) | |

|---|---|---|---|---|---|

| Price | 7.8 | 5.2 | 29.1 | 55.6 | (22.8) |

| NAV1 | 0.9 | 18.3 | 27.2 | 13.9 | 22.0 |

| MSCI World Aerospace and Defence | 0.7 | 8.1 | 35.5 | 93.6 | 115.9 |

Source: Bloomberg, Marten & Co. 1) NAV performance is based on the latest NAV valuation, as of 31 December 2024. SSIT commenced trading on 14 July 2021

Premium/(discount)

Over the past year, SSIT’s shares have traded at discounts to NAV ranging from 52.5% to 15.9%, with an average discount of 38.7%. On 1 December, the discount was 35.6%.

Figure 9: SSIT premium/(discount) from launch

Source: Bloomberg, Marten & Co

SSIT’s discount may make it an attractive entry point given the increased demand from defence sectors

As shown in Figure 9, SSIT briefly traded at a premium after its July 2021 IPO, but the wider growth stock sell-off in 2022, caused by rising inflation and interest rates, pushed it to a discount. This discount peaked at 72% in July 2023. However, as monetary policy eased in developed markets during 2024, the discount narrowed sharply. SSIT’s discount could offer an attractive entry point, especially with rising demand from defence sectors. The ongoing conflict in Ukraine highlights the dual uses of space technology, which has likely added to the downward pressure on SSIT’s share price discount.

Although SSIT’s discount is still large, it has been narrowing gradually. Other growth capital funds also trade at wide discounts, but SSIT stands out due to its focus on space technologies and increased interest in defence spending. We believe the current discount is excessive given these factors.

SWOT analysis

Figure 10: SWOT analysis for SSIT

| A unique investment proposition in the London-listed closed end funds space, SSIT has a laser sharp focus on growth capital investing within the SpaceTech arena. |

| The board and the managers have demonstrated SSIT offers a way for all investors to get exposure to this high growth and otherwise difficult to access sector, for the price of a share. |

| SSIT could suffer periods when absolute and/or relative performance is difficult, particularly when the market backdrop is unhelpful for growth investors, such as when inflation and interest rates pick up. |

| No prospect of a yield, although this should be well understood by shareholders. |

| There are increasing signs that growth investing is coming back into favour, against a backdrop of interest rate cuts, both in the US and globally. The political temperature has risen across the globe and the war in Ukraine has illustrated how important SpaceTech with its dual uses is to modern defence. With Europe rapidly rearming and other nations looking to bolster their defences, some of SSIT’s holdings could have long growth runways. |

| Investors appear to be looking more favourably at SpaceTech, recognising its increasing importance in defence and SSIT looks cheap versus aerospace and defence companies more broadly. |

| The market could once again turn against growth investing, particularly if inflation re-emerges as a threat and nominal GDP growth picks up. However, not only is there a risk of stagflation in more developed markets that could limit the capacity for interest rate rises, the need for nations to bolster their defences will likely outweigh such considerations. |

| Given the concentrated nature of the portfolio, single stock issues could hurt performance. |

Bull vs bear case

Figure 11: Bull vs bear case for SSIT

| Performance | SSIT’s portfolio, which has considerable dual use applications within, has recently been benefitting from strong defence tailwinds, which look set to continue.

Inflation is edging up in the US, but the growth outlook has also deteriorated, limiting the capacity to raise interest rates, which should be positive for growth capital stocks. |

SSIT’s typical investee company requires funding, which has been difficult in an environment of higher interest rates where the IPO window has been shut. The funding environment appears to be improving for higher quality SpaceTech companies, although SSIT could see its performance suffer if this reversed. |

| Dividends | SSIT focuses on capital growth rather than income. It is only likely to pay a dividend to maintain its investment trust status and it would need to recover significant revenue losses first. | Investors should not consider investing in SSIT if they require income from their investment. |

| Outlook | SpaceTech investing appears to be coming into favour with investors, which should suit SSIT. | Growth focused investments generally benefit from subdued inflation and interest rates. Although US inflation has been edging up, the direction of interest rates still looks to be down for now. |

| Discount | The current discount could narrow further or even move to a premium if the outlook for SSIT improves further. | While it remains wide, the discount has narrowed in recent months but could come under pressure if inflation picks up or if the SpaceTech and/or aerospace and defence sectors move out of favour. Size limits ability to undertake buybacks. |

Source: Marten & Co

Previous publications

Readers interested in further information about SSIT may wish to read our previous notes (details are provided in Figure 12 below). You can read the notes by clicking on them in Figure 12 or by visiting our website.

| Title | Note type | Publication date |

|---|---|---|

| Science fiction becoming science fact | Initiation | 14 August 2024 |

| Entering orbit | Update | 7 November 2024 |

| SpaceTech – the critical frontier in modern defence | Update | 25 May 2025 |

Source: Marten & Co

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Seraphim Space Investment Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it. Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.