Tritax EuroBox

Investment companies | Annual overview | 12 July 2023

Optimism returns

The rapid readjustment of valuations in the European logistics sector has encouraged investors seeking quality assets to return to the market, according to Tritax EuroBox’s (EBOX’s) manager who says that it is optimistic that values are stabilising. The company’s portfolio yield moved out 70bps in the six months to 31 March 2023, but the worst of the declines seem to be over, it adds.

Operationally, the manager says that it is in good shape to take advantage of a strong demand and supply dynamic, having recorded an uplift in annual rent of 5.8% in the six months to March 2023 (10.4% over 12 months). It has recently let a completed development in Germany above ERV and pre-let an extension to an existing building. The manager comments that additional development completions, extensions and inflation-linked uplifts are still to come.

Growth in income and operational savings have meant that the company has been able to fully cover its dividend for the past three quarters. Going forward, the manager expects earnings to continue to cover the dividend, which represents an 8.4% yield.

Bix box logistics in Europe

EBOX invests in a portfolio of logistics assets in continental Europe, diversified by geography and tenant, targeting well-located assets, within or close to densely populated areas. The strategy aims to capture market rental value growth and deliver an attractive capital return and secure income. EBOX is targeting a total return of 9% per annum over the medium term.

Fund profile

The company’s website is tritaxeurobox.co.uk.

Tritax EuroBox (EBOX) invests in and manages a portfolio of logistics assets in continental Europe, diversified by geography and tenant, targeting well-located assets in established distribution hubs close to densely populated areas. The strategy aims to capture market rental value growth, which the manager says is becoming evident in the key distribution markets of continental Europe.

EBOX was launched on 9 July 2018 after raising gross proceeds of €339.3m (£300m) at IPO. Following full deployment of the capital from the IPO into a portfolio of nine continental European logistics real estate assets, the company successfully raised additional gross proceeds of €135m (£119.1m) in a placing on 21 May 2019. In 2021, the group made two substantial capital raises, in March raising gross proceeds of €230m and in September €250m.

Investment in European logistics assets to capture market rental growth.

EBOX’s shares are traded on the premium segment of the London Stock Exchange, with both a sterling and euro quotation. These are the same class of shares and trading line, are fully fungible, and have no impact on overall liquidity of the stock. On 1 October 2021, the group was added as a constituent of the FTSE 250 index. To enhance equity returns, the company uses gearing, with a medium-term target of 45% of gross assets and a maximum limit of 50%.

The manager – Tritax Management

The company’s manager is Tritax Management, part of the Tritax Group. Since 1995, the Tritax Group has acquired and developed more than £6bn of commercial property assets across multiple sectors, including big box logistics assets, industrial properties, office, retail and hotels.

Tritax Group manages more than £7bn of assets (including EBOX), consisting of more than 50m sq ft. Tritax has a particular specialisation in the acquisition and management of logistics portfolios, most notably through Tritax Big Box REIT, a UK FTSE 250 REIT launched in December 2013. Tritax is headquartered in London with over 60 professionals and is authorised and regulated by the FCA.

In 2021, abrdn acquired a 60% interest in Tritax Management. As part of the deal, Tritax now leads abrdn Real Estate’s global logistics team.

In September 2022 the company appointed a new fund manager, with Phil Redding taking over from Nick Preston. Phil joined Tritax in November 2020 as director of investment strategy. Prior to that he spent 25 years at SEGRO Plc, holding the position of chief investment officer from 2011, and was appointed to the board as an executive director in 2013. Phil was responsible for SEGRO’s pan-European investment strategy and implementation, playing an integral role in the company’s repositioning and growth.

Reduction in the base management fee.

In October 2022, EBOX amended its investment management agreement with Tritax Management. The key change was a reduction in the base management fee to 1.00% on NAV up to €1bn and 0.75% on NAV above €1bn. Previously the management fee was 1.3% on NAV up to €500m, 1.15% on NAV between €500m and €2bn, and 1% above €2bn.

Market overview

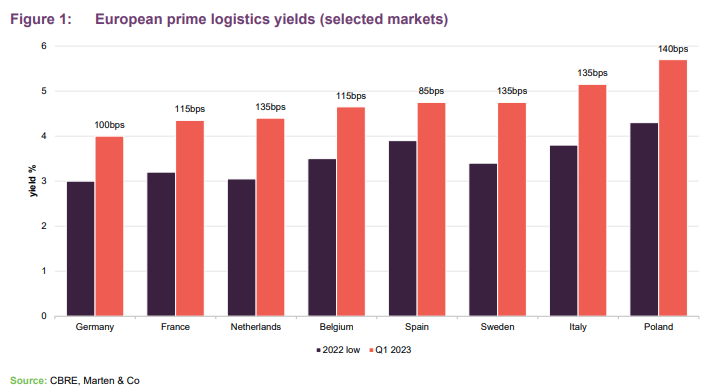

Real estate valuations across Europe have fallen heavily over the last nine months due to the impact of central banks’ quantitative tightening in an effort to bring raging inflation under control. Yield expansion in the real estate sector has mirrored that of interest rate rises. The logistics property sub-sector has seen one of the sharpest value corrections in the sector with prime yields coming off historic lows of 3.5% to reach almost 5%.

The manager says that the rapid adjustment in values is a cause for optimism that price stability is close to being reached – as opposed to a drawn-out decline in values over many quarters. The manager says that investors have returned to the sector at the re-rated asset values, attracted by the continued strong occupier characteristics. The manager notes, however, that investor interest is skewed towards assets that display quality attributes such as strong sustainability credentials, good tenant strength, and located in established distribution hubs.

In fact, EBOX has a disposal in the market at the moment that the manager says has garnered very strong interest from investors – with a dozen strong offers (more details on the sale and reasons behind the asset disposal can be found on page 21). The manager expects the renewed investor activity to grow as the year goes on, which should support the stabilisation of values.

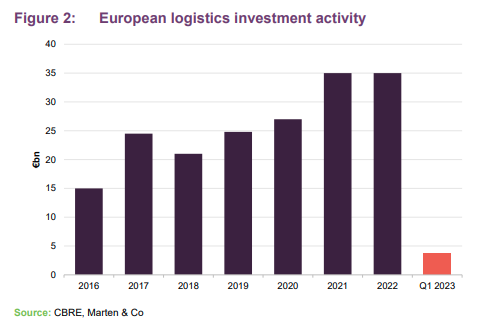

Investment volumes have been subdued so far this year. Just under €4bn was transacted in the first quarter of 2023 across France, Germany, Netherlands, Belgium, Italy, Spain, Poland, Czech Republic, Hungary, Romania and Slovakia, according to CBRE.

Occupier market

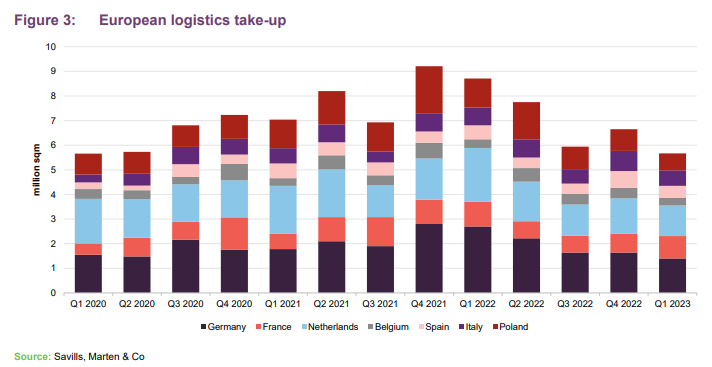

There are signs that macroeconomic caution amongst businesses has started to feed through to occupier take-up of European logistics space. The first quarter of 2023 saw a moderation in take-up numbers across many markets, as shown in Figure 3. However, this should be viewed from the perspective of exceptional levels over the past two years. Take-up in the first quarter was in line with pre-COVID levels.

The manager says that the take-up figures reveal that there was a step up in activity from third-party logistics operators (3PLs), such as DHL, which provider logistics solutions to corporate companies, and manufacturing companies. The latter is evidence that near-shoring, which has been talked about as an occupier trend for three years, is starting to feed through to actual take-up, it adds.

Since the outbreak of the COVID-19 pandemic, manufacturers have shifted their supply chain strategies to avoid the nightmare scenario that they experienced when supply chains were shut down almost overnight, the manager states. Supply chains are becoming shorter, it says, with some manufacturing moving away from the Far East and China and back to Europe. Companies have also adopted a ‘just-in-case’ mentality, as opposed to a ‘just-in-time’ pre-COVID, that has seen inventory increase to help alleviate any future shocks in the supply chain, according to the manager. This, it says, requires more warehouse space.

An occupier trend that the manager expects to grow over the next few years is an increased corporate focus on the sustainability of the buildings that businesses are operating from. Buildings that do not meet sustainability requirements will eventually become obsolete without significant capital expenditure, the manager says. Large multi-national corporate companies have ESG targets that they need to meet, which the manager says should benefit EBOX. The group’s portfolio is highly sustainable, the manager states, adding that it is focused on further enhancements with the roll out of solar panel installations (more details on EBOX’s sustainability and ESG credentials can be found on page 8). The company has been awarded the highest possible industry accolades for the sustainability of its portfolio.

Vacancy still extremely low

Vacancy rate in Europe moved out to 3.5%.

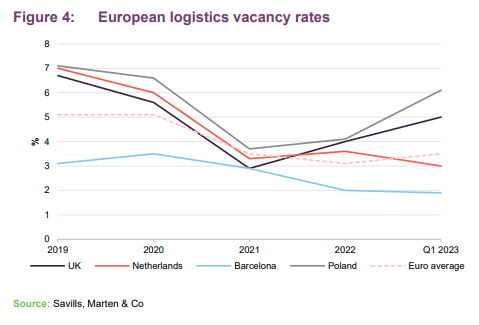

Vacancy rates remain close to historically low levels, despite a slowdown in leasing activity. The average vacancy rate across European logistics was 3.5% at the end of the first quarter, according to Savills, up from a low of 3.1% in 2022 but still one of the lowest levels on record, as illustrated in Figure 4.

Impacting vacancy was the completion of speculative developments that have come onto the market, according to Savills. New development starts are being held back due to the cost of finance, however, it adds. Vacancy rates are likely to rise slightly in the second quarter of 2023 until a slowdown in construction translates into reduced completions later in the year, Savills says.

Figure 4 shows that Barcelona, where EBOX’s largest asset is located, has an exceptionally low vacancy rate of sub-2%. The Netherlands saw its vacancy rate continue to fall in the first quarter of 2023, by 60bps.

Continued rental growth on the cards

The low vacancy rate continues to be supportive of rental growth, the manager says, evident in EBOX’s portfolio where it recorded rental growth of 10.4% on a like-for-like basis to €78.6m in the 12 months to 31 March 2023.

The manager expects that annual rental growth this year will be at a slower pace than in recent years – in the mid-single digits. However, high-quality buildings in locations of limited supply and robust level of occupier demand will continue to perform strongly, the manager adds.

Investment process

EBOX focuses on investment in properties fulfilling a key part of the logistics and distribution supply chain for occupiers including retailers, manufacturers and third-party logistics operators (3PLs). Its portfolio is predominantly made up of large, modern distribution warehouses, with some exposure to urban distribution hubs, which help occupiers fulfil the ‘last mile’ part of the distribution chain.

‘Bottom up’ approach to investment ensures good real estate fundamentals.

EBOX has a ‘bottom-up’ approach to investment, which is focused on identifying good real estate in good locations close to densely populated areas with good transport connections and sufficient labour, power supply and data connectivity and good sustainability credentials. Target assets must also be in locations that the manager deems to display favourable supply and demand characteristics, with limited supply and strong occupational demand.

The company looks to balance the portfolio between stabilised, income-producing assets and exposure to opportunities that enable it to add value through asset management and development activities. It targets and looks to maintain a weighted average unexpired lease term (WAULT) of more than five years across the portfolio, with leases incorporating built-in inflation-linked rent escalators.

EBOX looks to diversify the portfolio by geography (but with an appropriate critical mass in each country to enable economies of scale), building size (but with a focus on larger-scale warehouses), and customer and business sector (with a focus on large, multi-national organisations).

The majority of the company’s portfolio is currently invested in completed, let investments and pre-let income-producing forward funded developments; however, a proportion of the portfolio may be invested in speculative development.

EBOX categorises its investments into four investment pillars:

- Foundation Assets are core low-risk income assets. They typically benefit from long leases to institutional grade covenants in prime locations with index-linked rents, providing the foundation to the portfolio.

- Value Add Assets provide asset management opportunities. These assets are fundamentally strong assets let on shorter leases to financially strong tenants allowing implementation of asset management initiatives to drive value, for example by lease renegotiation or building extension.

- Growth Covenant Assets are fundamentally strong assets in good locations but let to tenants with improving financial covenants. These assets offer the opportunity to add value as the tenant’s financial standing improves and hence improving income security.

- Strategic Land assets are investments in land zoned for logistics use in strong locations and include options over land. These assets offer the opportunity to add value as they are positioned at an earlier stage of the development cycle and so have the potential to become Foundation Assets for the future.

On a long-term fully-invested and geared basis, the company expects that its portfolio would have an equal split between investments in Foundation Assets and value-add investments (incorporating Value-Add Assets, Growth Covenant Assets and Strategic Land).

Developments

An important driver of returns for the company has been developments. EBOX has exclusive partnerships with two specialist logistics developers and asset managers – Dietz AG and Logistics Capital Partners (LCP) – that offer it asset management expertise on its current portfolio and access to their respective development pipelines. EBOX has first right of refusal over the two developers’ pipelines, providing it with acquisition opportunities in some of the best logistics locations across continental Europe, according to the manager.

In the manager’s view, not only have these partnerships provided EBOX with access to a significant quantum of the best quality assets in Europe, but they have also provided them at competitive prices. The manager states that acquisition yields were between 25-50 bps higher on income producing assets, and 100 bps on forward funding developments. This is because developers like to sell assets before construction has started, rather than taking them to market, to provide them with certainty of transaction and allow them to recycle capital into other projects.

EBOX has partnered with a third logistics developer, Verdion, in both Sweden and Germany, although this is not an exclusive partnership as is the case with Dietz and LCP. The manager says that the developers have substantial teams in all of the countries where EBOX operates, with a fundamental understanding of the local markets, knowledge of occupier requirements and relationships with local municipalities.

Sustainability

EBOX’s environmental, social and governance (ESG) policy sets out the group’s approach to managing sustainability covering acquisitions, developments and asset management. The group has recruited a sustainability lead who has developed a long-term strategy to improve sustainability performance.

EBOX works closely with tenants to improve efficiency of buildings.

The manager says that the large, modern warehouses that EBOX invests in are designed to mitigate their impact on the environment, and, unlike other property classes, such as offices, have lower obsolescence and running costs. EBOX works closely with its tenants to undertake environmental initiatives that improve the efficiency of the buildings. The group has obtained operational performance data from the vast majority of its tenants in order to help measure and manage their environmental impact. Examples of sustainability initiatives within the portfolio include the generation of renewable energy through photovoltaic panels on the group’s assets. It plans to commence the installation of PV roof-mounted solar panels on two assets in Germany by the end of the year and follow this with a rolling programme in collaboration with tenants. These two projects will add an additional 6.9MW to the group’s existing generating capacity of 6.7MW. The installation of LED lighting, electric car charging stations, solar carports for power generation, and energy controls are other example of sustainability initiatives implemented by the manager.

Awarded five green star rating by GRESB.

The improvements across its portfolio saw EBOX awarded five green stars rating in the 2022 survey by GRESB (Global Real Estate Sustainability Benchmark) with a score of 88/100. This is a significant improvement on its 2021 GRESB survey score of 82/100 and compares favourably not only against its peer group average score of 79/100 but also against the 74/100 GRESB 2022 average score. It was designated as Leader in ESG for European Industrial Distribution Warehouse Listed Sector by GRESB and also holds an EPRA Gold Level certification for sustainability best practices.

Acquisition due diligence explicitly integrates ESG considerations, including assessing risks such as changes to legislation, contaminated land or flooding, as well as opportunities to improve environmental performance or wellbeing for tenants’ employees. The area surrounding the asset is also considered, including how well it is served by public transport, a ‘walkability’ score and the distance to green space or amenities. Other considerations include internal and external air quality, electric vehicle charging and cycle facilities. Opportunities for improvement are included in the asset management plans and sustainability action plans.

It is EBOX’s long term ambition to have all assets let on green leases, as it works towards achieving net zero carbon across the portfolio by 2040. Currently over 10 green leases have been signed with tenants, incentivising the investment in green initiatives. More detail on the sustainability credentials of some on EBOX’s assets can be found in the asset allocation section from page 10.

The manager says that all new developments will obtain Green Building Certifications and have strong sustainability credentials. EBOX sets ESG standards with its development partners, including a sustainable construction brief and a supplier code of conduct.

EBOX’s social approach focuses on positive relationships with occupiers and providing an environment that encourages employee wellbeing, including introducing nature and wellbeing measures. The group’s local community investment fund supports its tenants’ community engagement initiatives.

Internally, the manager has policies covering equal opportunities, disability discrimination, health and safety, data-protection and whistle-blowing.

The manager says that the strength of the group’s ESG credentials enabled it to issue a €500m ‘green’ bond in May 2021 (details of which are on page 26) that has far more attractive interest rates.

Asset allocation

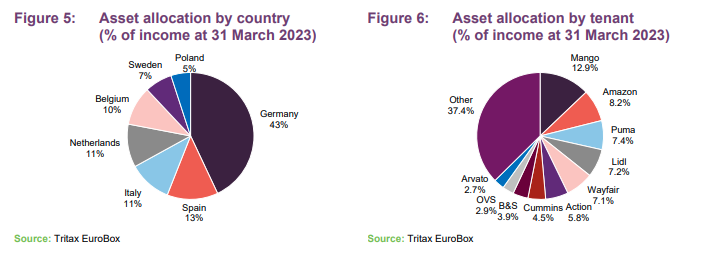

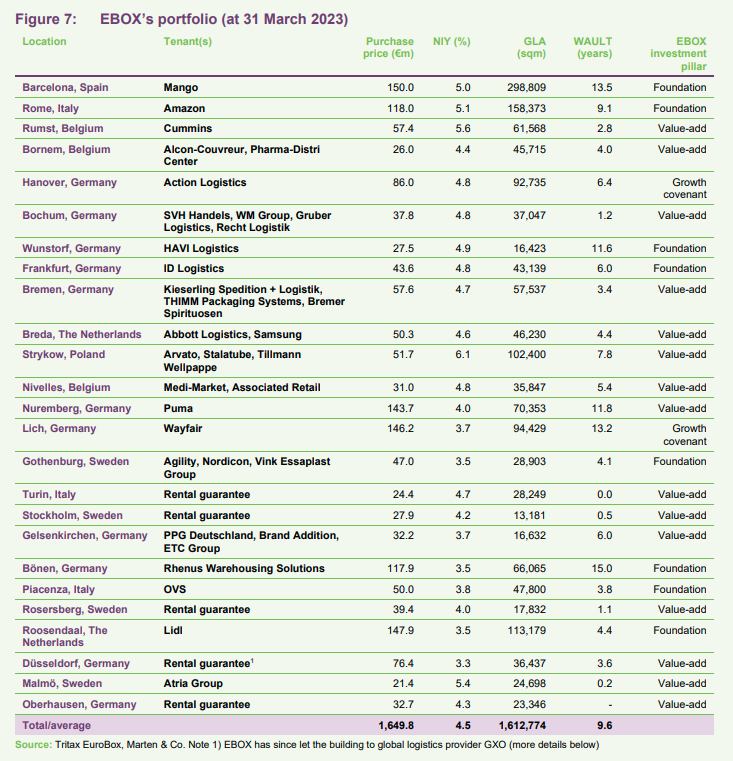

EBOX has a portfolio of 25 assets worth €1.596.7m at 31 March 2023 (down 9.6% from €1,765.6m at 30 September 2022). The portfolio is located across seven European countries.

The portfolio has a WAULT of 9.6 years (7.9 years to break), with a spread of short- and long-term leases, let to 36 tenants. The majority of leases are subject to some form of annual indexation, with 54% linked to uncapped local CPI. 17% of leases have a fixed yearly uplift at an average of 0.9%, while 26% has a combination of inflation linkage (capped at 4%) and a fixed uplift element. Around 3.4% of EBOX’s income is currently through lease guarantees on its development assets.

Barcelona

Purpose-built in 2016, the property is the global distribution centre for fashion retailer Mango. It was acquired in September 2018 for €150m and is the biggest asset in EBOX’s portfolio. In 2021, the company funded a 93,931 sqm extension on the adjacent plot of land, at a cost of €31.5m, which completed in November 2022 bringing the building size to 274,000 sqm, including mezzanine space. The property is let on a 30-year full repairing and insuring (FRI) lease that commenced on 20 December 2016, with a tenant break option in 2036, 2039 and 2042. The rent is subject to annual upward-only indexation.

It is located 25km north of Barcelona and is directly accessible from the motorway network, with Barcelona’s port and airport within a 25-minute drive. The manager says that Barcelona is one of the most supply-constrained logistics markets in Europe, with strong occupier demand. There are no sites available in the greater Barcelona area, due to the landscape, for large-scale logistics development and the manager says there is downside protection in that similar adjacent buildings are leased at higher rents. In the extreme event of the tenant going bust, the property can be sub-divided into up to four units and re-let, the manager adds.

Mango accounts for 12.9% of EBOX’s rental income, as at 31 March 2023. Two months of rent is held in deposit and EBOX has a bank guarantee for 10 months’ rent, that extends to 24 months if certain covenants are not met.

Rome

Acquired from SEGRO for €118m in October 2018, the 158,000 sqm regional fulfilment centre forms a key part of Amazon’s pan-European network and is located in a prime logistics location 35km north east of Rome, with good rail and airport connectivity, according to the manager.

The high-specification logistics facility was purpose-built in August 2017 and has three levels with a maximum eaves height of 14 metres and a site cover of 35%. The building has benefited from significant capital investment from the tenant, the manager adds.

The property is let on a 15-year FRI lease that commenced on 7 August 2017, reflecting an unexpired lease term of just over nine years. At the end of the 15-year lease there are two six-year extension options in favour of the tenant. The majority of the rent is subject to annual indexation.

Rumst

Located in the Brussels/Antwerp corridor in Belgium, the site comprises two modern warehouses with a total gross internal area of 59,000 sqm and an office building of 2,500 sqm. Both warehouse buildings are fully let to Cummins NV, part of Cummins Inc., a Fortune 500 corporation, listed on the New York Stock Exchange with a market capitalisation of $33.6bn. Cummins designs, manufactures, distributes and services a broad portfolio of power solutions globally. Together, these buildings represent a principal distribution hub for Cummins in the EMEA region, the manager says.

There are also two unutilised plots of land, totalling 3.5 hectares that the manager says offers attractive development potential for buildings totalling around 16,000 sqm. The development land has the potential to add substantial value for EBOX, the manager adds, subject to securing the relevant planning permissions.

Bornem

Comprising three warehouses, EBOX’s Bornem asset has a combined gross internal area of 46,000 sqm. The first building is a multi-let warehouse with two interconnected units let to Alcon-Couvreur NV (a world player in eyecare). A new single lease for the two units expires in nine years.

The second building, which was vacant on acquisition in 2018, was let within four months of acquisition to Belgische Distributiedienst NV, part of the BD myShopi NV group, which acts as guarantor to the lease. The lease was agreed for a nine-year term from 1 July 2019, and the rent compounds annually at 100% of the Belgian Health Index.

EBOX developed a new 15,000 sqm facility on the site that completed in 2021 and has let the property to an online grocery retailer on a nine-year lease, with a tenant break options at years three and six, including annual indexed rent of €0.7m per annum. This represented a 14% increase on previous rents secured on the site. The development delivered a yield on cost of 7% and profit on cost of 70%.

EBOX previously sold a small plot of land on the site, which the manager deemed was too thin for a logistics development, at a price 53% ahead of book value.

Hanover

The brand new, purpose-built asset was acquired in October 2018 for €81.6m and was the first for EBOX arising from its relationship with Dietz. It is located in an established logistics area close to Hanover and Brunswick, on the A2 motorway, which crosses Germany, linking Berlin to the Rhine/Ruhr region. The manager says that the area benefits from excellent logistics links and continues to see high occupier demand, a low vacancy rate and limited availability both of logistics buildings and land for development.

The 90,000 sqm property is let to Action Logistics (the logistics arm of discount retailer Action, which is backed by 3i Group) and is classified as a Growth Covenant asset by EBOX. Action has more than 2,300 stores in 11 European countries, with sales of over €6.8bn in 2021. The success of the retailer is underpinned by its logistics network, the manager adds.

Bochum

Acquired in November 2018 for €35.7m, the 37,000 sqm, four-unit asset is strategically located in an established logistics location near Bochum, in the Rhine-Ruhr region of Germany. The area continues to see high occupier demand, a low vacancy rate and limited availability both of logistics buildings and land for development, the manager says.

The multi-let property was acquired with two of the four units, totalling 17,664 sqm, vacant. Within three months of acquisition, EBOX let 9,337 sqm of space to Gruber Logistics (a transportation and logistics service provider in Germany) on a five-and-a-half-year term. The lease is subject to annual CPI uplifts reflecting 100% of the German Consumer Price Index with a floor of 2%.

The second vacant unit, of 8,335 sqm, was let to Recht Logistik (a German logistics and transportation company) in January 2020 on a five-year term at a rent 7% ahead of previous levels. The rent is subject to full annual indexation reflecting 100% of the German Consumer Price Index.

The two original tenants are SVH Handels GmbH (a subsidiary of the Würth Group, a worldwide wholesaler to the trade and craft industry, with annual turnover of over €20bn), which has two years unexpired on its lease, and logistics provider WM Group, whose lease expires at the end of 2023.

Wunstorf

EBOX forward funded the development of this 16,000 sqm urban logistic asset that completed in December 2019. The cold store facility is located 20km from the centre of Hanover and let to HAVI Logistics (a food distributor that supplies fast-food chains across Germany), with security from the parent company, on a 15-year lease.

The asset has a low site coverage of 25%, which the manager says provides it with the opportunity to extend the building by around 10,000 sqm. The manager is in discussion with the tenant, HAVI, regarding an extension. It expects the development land to come with a yield on cost of 7%.

Frankfurt

Bought for €50.6m in June 2019, the 43,000 sqm property is let to ID Logistics. In 2022, EBOX agreed a lease renewal with ID Logistics at a rent 24% above the previous level – growing the annual income from €2.5m to €3.1m. The new seven-year lease includes annual, uncapped CPI-linked uplifts and a tenant option to extend the lease by a further five years (subject to a market rent review at extension).

ID Logistics is servicing an Amazon contract from the facility. The asset is located in the prime logistics location at Hammersbach, near Frankfurt, which the manager says has high occupier demand, a low vacancy rate and limited availability both of logistics buildings and land for development.

Bremen

Located in the prime logistics hub of Bremen, the second-largest metropolitan city in north-west Germany and the largest freight area in the country, the asset comprises two facilities built in 2013 and 2019.

One property is single-let to logistics operator Kieserling Spedition + Logistik on a 10-year lease from February 2019. The second property is multi-let to Kieserling Spedition + Logistik, THIMM Packaging Systems, a packaging and logistics company, and Bremer Spirituosen on shorter leases. The WAULT of both properties is 3.4 years, with rent subject to annual indexation of 85% of the German CPI.

The manager says that the area benefits from excellent road infrastructure as well as national and international transport connections via Bremen International Airport and the high-speed railway network. The location is severely supply-constrained, it adds, with no parcels of land left for development nor plans to zone land for logistics development. This appears to have driven recent rental growth. The shorter leases on the second unit give EBOX the opportunity to capture this rental growth, the manager says.

Breda

Purpose-built in November 2019, the 46,185 sqm property is divided into four units and is half let to Abbott Logistics (part of Abbott Laboratories, a medical devices and healthcare company listed on the New York Stock Exchange with a market capitalisation of $187bn) on a 10-year lease term subject to annual indexation of 2.0% per annum. In December 2020, EBOX signed a green lease on the two previously vacant units with Samsung SDS. The three-year lease is subject to annual uplifts reflecting 100% of Dutch CPI. The green clauses ensure the tenant’s commitment to using the building in a sustainable way, including sharing data on energy and water consumption, waste management and recycling.

The asset is located in an established logistics location along the main east-west logistics corridor in southern Netherlands.

Strykow

The asset, acquired in February 2020, comprises two logistics properties and development land. 61,000 sqm of space is let to Arvato Polska on a new 11-year lease following a re-gear and agreement for the development of an extension. Arvato is an international logistics service company and provides international, third-party logistics services for retailer H&M from this building. The 8,841 sqm extension, which is expected to complete in October 2023, will come at a yield on cost of 7.2%.

The second building is multi-let with 8,942 sqm let until July 2029 to Stalatube (a leading provider of stainless-steel solutions) and 3,287 sqm let to the Polish operations of German packaging company Tillmann Wellpappe until July 2029, with a parent company guarantee.

Nivelles

EBOX acquired the newly built 34,125 sqm logistics facility in Nivelles in January 2021 for €31.2m, reflecting a net initial yield of 4.8%. The asset comprises two units, one of which is let to MediMarket Group on a nine-year lease without a break at a rent, subject to annual indexation, of €803,000 per annum reflecting €44.3 per sqm. The second, slightly smaller, unit was vacant on acquisition and had a 12-month rental guarantee. The company signed a new lease in November 2021 to Associated Retail (trading as Match Supermarkets), a leading Belgian supermarket, for nine years, with a break option at six years, at €793,553 rent per annum, reflecting €44.8 per sqm. The rent will be subject to annual uplifts in line with the Belgian Healthcare Index. This rental level was around 8% above the rental guarantee.

The Nivelles property includes a range of sustainability measures such as LED lighting with motion sensors, insulated exterior walls to achieve good energy performance, cycle storage and a cycle path, along with installation of solar panels to provide tenants with a renewable power source. EBOX negotiated a ‘green lease’ with Match Supermarkets to include specific clauses to ensure the commitment of the tenant to use the building in a sustainable way, sharing data on energy, water consumption, waste management and recycling.

Nuremberg and Lich

EBOX acquired the Nuremberg and Lich properties in the same transaction with its development partner Dietz for a combined €290.9m, reflecting a combined net initial yield of 3.9%.

The 70,353 sqm property in Nuremberg is let to global sportswear manufacturer and retailer Puma. It serves as the European distribution headquarters for Puma, which signed a 15-year lease on the property in April 2020. The property produces an annual rental income of €5.78m, with the lease subject to annual indexation of 100% of German CPI, following a four-year indexation holiday from the start of the lease.

The property is carbon neutral, built to LEED Gold standard, benefits from certified green energy procurement, and has a roof mounted photovoltaic system generating up to 1.5MW of electricity. The 20-hectare site comes with extension potential for an additional 42,000 sqm of floorspace. The manager says that the asset is categorised as a foundation asset by EBOX, due to the low-risk nature of the income. The manager is in discussions with Puma on a 42,000 sqm extension to their global logistics centre, together with an associated lease extension.

The 94,429 sqm distribution unit in Lich, near Giessen, is let to online furniture retailer Wayfair. The distribution centre plays a key role in Wayfair’s European operations, which is focused on Germany and the UK. It signed a 15-year lease on the property that commenced in May 2021 at an annual rent of €5.6m, linked to German CPI, following a three-year indexation holiday at the commencement of the lease. The property is certified to DGNB Gold standard, and it benefits from a range of operational energy reduction measures. The roof has the capacity to support the installation of solar PV panels.

Gothenburg

In June 2021, EBOX acquired its first investment in the Nordic region with the €47m purchase of this asset in the Port of Gothenburg. The asset comprises two purpose-built logistics facilities totalling 28,900 sqm that are fully let to Agility AB, Nordicon AB and Vink Essåplast Group AB, generating a total annual rent of €1.79m (equating to €62.50 per sqm) on leases with a WAULT of 4.1 years. All leases are annually indexed to 100% of Swedish CPI. The manager says that the Port of Gothenburg is one of the most attractive logistics locations in the Nordics and currently has no vacant logistics buildings in the port area. The port is home to Scandinavia’s largest container terminal, which the manager says is forecast to grow over the coming years.

Turin

EBOX completed the forward funding acquisition of the 28,249 sqm asset in Settimo Torinese near Turin in November 2021, for a total consideration of €24.4m. The property is being developed by LCP under a fixed-price development contract. LCP will provide a rental guarantee of €1.277m from completion, based on 12 months’ estimated rental value.

The cross-docked logistics facility is arranged as two equal sized units in one single building, capable of being leased either as a single building or two separate buildings. The facility is expected to achieve a BREEAM Very Good rating and to benefit from roof-mounted photovoltaic panels, which are expected to provide income of €45,000 per annum. The manager states that the Italian logistics market is currently characterised by record levels of occupational take up, particularly in the northern part of the country, as well as vacancy rates at a low level.

Stockholm

The €27.9m forward funding acquisition of EBOX’s second asset in Sweden completed in November 2021. The site, which will host a 13,181 sqm facility, is located in Rosersberg just north of Stockholm and is being developed by Verdion. EBOX will receive an income return equivalent to the net initial yield from completion of the land purchase (which is conditional on receiving the building permit), as well as a 12-month rental guarantee of €1.19m from completion of construction in January 2023.

Rosersberg, which is located close to Stockholm Arlanda Airport, has one of the highest logistics market rents in Sweden, the manager states. Due to the strength of the local leasing market, the manager says that it is confident that it will be able to lease the units quickly and benefit from any increased value that a new lease may create. Verdion will assist with the letting based on pre-agreed leasing criteria with an incentive mechanism and will be retained as asset manager. The developer is targeting a minimum BREEAM Very Good certification.

Gelsenkirchen

EBOX agreed the acquisition of a €32m asset in the Rhine-Ruhr region in Germany in October 2021. The asset has a total gross internal area of 16,632 sqm and comprises three purpose-built logistics facilities. Two of the three units were let on acquisition, with the third let in September 2022. The letting of the third unit, to ETC Group on a five-year lease was agreed at a 6% premium to the rental guarantee level. The asset generates a total annual rent of €1.7m with a weighted average unexpired lease term of six years.

The acquisition price of €32m reflected a net initial yield of 3.7% based on the income from the existing leases and the rental guarantee.

Bönen

In November 2021, EBOX agreed to acquire land and fund the development of a €117.9m asset in the Rhine-Ruhr region in Germany, which is pre-let to the Rhenus Warehousing Solutions SE & Co KG, a global logistics service provider. The property will comprise a single building of 66,065 sqm split into six units and is expected to be completed in June 2023.

EBOX bought the land initially and then funded the construction of the building under a fixed-price contract with Dietz. During the 12-month construction phase, EBOX received from the developer an income return equivalent to the agreed net initial yield of 3.5%. The entire building is pre-let on a 15-year lease to Rhenus, commencing on practical completion of the building. The lease will generate a total annual rent of around €4.1m. The asset has an ERV of €4.7m.

Piacenza

The €49.65m acquisition of the 47,800 sqm asset in Piacenza, Northern Italy, completed in November 2021. The property comprises two units (DC4 and DC5) constructed in 2016 and 2020 and let to Italian fashion brand OVS, which uses the property as its European distribution hub. The lease on DC4 is for a further 7.4 years and on unit DC5 for 6.4 years. Both leases are subject to annual indexation. The gross annual rent of €2.01m reflects an average of €44 per sqm, which the manager says is below the prevailing headline rents in the area.

The asset, which fronts the A1 motorway that connects Milan and Rome and is close to the A21 east to west route linking Turin and Brescia, has obtained BREEAM Very Good and BREEAM Excellent certification and has roof mounted photovoltaic systems installed.

Rosersberg

EBOX funded the development of a 17,832 sqm logistics asset in Rosersberg, just north of Stockholm in Sweden after agreeing a forward funding deal with Verdion worth SEK 402m (€39.4m) in January 2022. The deal reflects a net initial yield of 4.0% based on the income from a 12-month rental guarantee of €1.6m from completion of construction. EBOX also received from the developer an income return equivalent to the agreed net initial yield during the construction of the building, which commenced in June 2022 and is expected to complete in July 2023. The asset has an ERV of €1.9m.

The asset is located adjacent to EBOX’s 13,181 sqm Stockholm property, which it also acquired in a forward funding with Verdion in September 2021. Rosersberg is located close to Stockholm Arlanda Airport, on the E4 motorway to Stockholm city centre and has strong occupier demand characteristics, the manager says. The development is targeting a minimum BREEAM Very Good certification, and the construction will include a range of energy-saving initiatives and staff wellbeing measures, the manager adds.

Roosendaal

EBOX paid €144.3m for this pre-let development from LCP, one of the company’s development partners. The site will comprise a single property, divided into three units, built in three phases, with a total net rentable area of 113,179 sqm. All three units are pre-let to Lidl, the German discount grocer, on a single lease that expires in November 2027. The annual rental income is €5.1m, which will be linked to Dutch CPI. The lease incorporates a rent review and option to extend for a further five years at the end of the lease term, potentially allowing EBOX to capture the prevailing open market level (with a cap of 10% above the rent at that time).

Construction of the first phase completed in December 2021, with the second and third phases completed in December 2022 and February 2023 respectively. During the construction phase, LCP paid EBOX income equivalent to the expected rent until practical completion.

Roosendaal is located in the south-east of the Netherlands, and provides good connections to the ports of Rotterdam, Antwerp and Amsterdam. The property was developed to a BREEAM Very Good certification.

Düsseldorf

EBOX agreed to forward fund the speculative development of this 36,437 sqm property in Düsseldorf in March 2022. It paid Dietz €76.4m for the asset, which reach practical completion in March 2023. Within five weeks of completion EBOX let the property to global logistics company GXO. The tenant, which provides logistics solutions for multinational companies, signed a 10-year lease linked to 100% CPI indexation, reviewed annually.

Dietz had been paying EBOX a rental guarantee reflecting €204,047 per month (€67.20 per sqm per year) during the construction of the property. The annual rent achieved on the new letting was 17.8% above the rental guarantee level, and 6.1% above ERV, increasing the annualised rental income by €0.5m to €2.97m.

A ‘green lease’ clause was agreed with the tenant to encourage the sustainable use of the building along with an obligation to share resource usage data. EBOX is now in discussions to install a substantial solar scheme on the roof of the property.

The site is located between Cologne and Düsseldorf, which is considered one of the principal logistics areas in Germany and where there is a scarcity of available development land and available buildings and strong occupier demand. The developer targeted a DGNB Gold Certificate for sustainability standard.

Malmö

In April 2022, EBOX acquired a site in Malmö for the speculative development of a new 60,700 sqm scheme for SEK 223m (€21.4m). The company, in partnership with Nordic developer MIGS, will embark on its first development project, building the new unit at an estimated cost of €65.3m. It expects the completed building to be worth €115m, based on an annual estimated rental income of €4.4m – equating to an expected yield on cost of 5.1% and an anticipated development profit of 32%.

The site was acquired from the current occupier of the building, Atria Group – a Scandinavian food processing group, which will continue to occupy the current building until February 2024, before relocating. It will pay an annual rent of €1.25m until its relocation. Completion of the new building is targeted for early 2025.

The manager says that the site is located in a prime Swedish logistics market, in the Fosie industrial area south of Malmö, where there is a shortfall of available development land. Demand from tenants is strong, it adds, given the asset’s location between Malmö’s two major ring roads that link to the rest of Sweden and Denmark.

Oberhausen

In September 2021, EBOX signed a deal to forward fund the acquisition of this logistics asset, at a fixed purchase price of €29.9m. Following receipt of the final building permits, the acquisition completed in January 2023. The development of the two-unit, 23,346 sqm building will be undertaken by Verdion. The speculative construction is expected to start in the second half of this year, subject to what the manager says is supportive market conditions and appropriate returns. During the construction phase, EBOX would receive from the developer an income return equivalent to the agreed net initial yield. While on completion, the group will benefit from a 12-month rental guarantee from Verdion of €1.313m (equating to €56 per sqm). The manager says that the assets have the potential to produce annualised rental income of €1.7m when fully let.

Oberhausen, located between Duisburg and Essen, is one of the cities forming the Rhine-Ruhr area, the largest urban area in Germany with a population of over 10 million. The manager says that the Rhine-Ruhr area currently has high levels of occupier demand and very low levels of vacancy for prime logistics real estate. Verdion will assist EBOX with the letting based on pre-agreed leasing criteria with an incentive mechanism.

The developer is targeting a minimum BREEAM Very Good and DGNB Gold certification, and the construction will include a range of energy-saving initiatives and staff wellbeing measures.

Asset management initiatives

Near- and long-term asset management initiatives could add substantial income.

Many opportunities to increase rental income exist within the portfolio, the manager states. The portfolio, it adds, has a reversion potential of 15.3% or an additional €12m of rental growth if assets were relet at estimated rental values (ERV). This is on top of the 5.8% like-for-like rental growth achieved within the portfolio in the six months to 31 March 2023.

Three near-term lease events have the potential to add a further €2.3m to annual income, in the manager’s view. This includes the letting at the group’s recently completed development in Dusseldorf (as mentioned earlier) that was €0.5m (or 17.8%) above the rental guarantee EBOX was collecting from the developer. Secondly, the development in Turin has recently completed, with the developer rental guarantee of €1.277m kicking in. Finally, the small pre-let extension at its Strykow asset (also mentioned earlier) is expected to see an additional €0.5m of rental income on completion in October 2023.

On top of this, the manager expects to capture further rental uplifts through inflation-linked leases throughout the remainder of the year. Of the leases that were linked to full CPI to come up for review in the six months to 31 March 2023, the average annual uplift was 10%. The manager predicts that over the next three years it could capture an additional €5.9m of rent from inflation uplifts, based on Oxford Economics’ average inflation forecast of 4.2% per year.

Rental income could potentially increase further with the commencement of the Oberhausen and Malmo developments (as described above, both are medium-term projects and dependant on market conditions) and the letting up of vacant space above the current rental guarantee levels.

Longer-term, two further potential extensions exist at its Wunstorf and Nuremberg assets in Germany. The manager says that it is in discussions with the tenant at it Wunstorf asset regarding a 10,000 sqm extension and would expect the development to come with a yield on cost of 7%. It has also held talks with Puma regarding a 42,000 sqm extension at its global logistics centre in Nuremberg, along with an associated lease extension, the manager says.

Planned asset sales

Plans to sell at least €150m of assets over 12-18 month period.

In an effort to bring its LTV down to a more conservative level of around 40% (more details on the company’s debt structure can be found on page 26) and maintain its investment grade rating, the manager says that it will make selective asset disposals over the next 12 to 18 months. Some of the proceeds could also fund higher-returning asset management opportunities from within the existing portfolio, if they were accretive to earnings, the manager adds.

The manager says that it is looking to generate sales proceeds of at least €150m over the next 12 to 18 months. These would be on assets where the manager has completed its asset management plan (and therefore further rental income growth was limited) or on assets that the manager believes display some risk – either on the part of the tenant or the building (that did not meet sustainability credentials and would be too costly to implement). It could also mean exiting entire countries where the manager feels that it would be difficult to achieve critical mass in that country.

The company currently has one asset on the market in Germany. The manager says that it has completed its asset management strategy at the building and is looking to crystalise the corresponding uplift in value. It adds that it has been encouraged by the broad group of investor interest in the asset, with 90 expressions of interest received, 50 investors signing an NDA, 12 good offers received and five parties taken into the final stage of the bidding process.

Performance

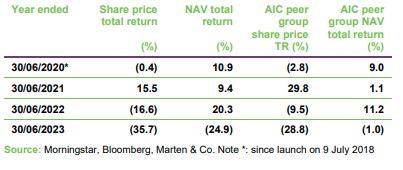

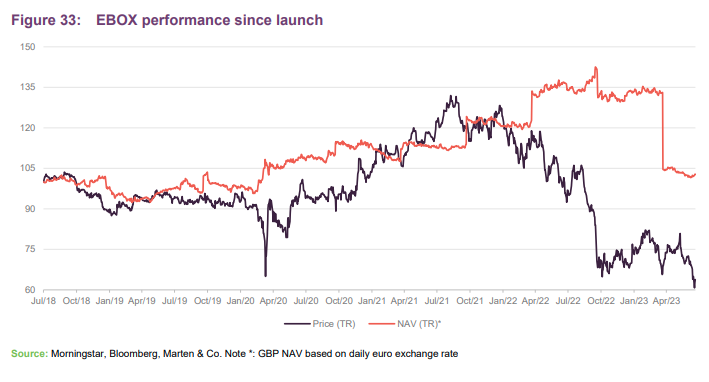

EBOX’s NAV fell 22.7% in the six months to 31 March 2023 due to the impact of a 70bps outward movement in the portfolio’s net initial yield. The NAV had made steady progress from launch and grew significantly with the deployment of the proceeds of equity raises in March and September 2021. EBOX’s NAV is quoted in euro, and the NAV in Figure 33 is the sterling NAV based on the daily exchange rate.

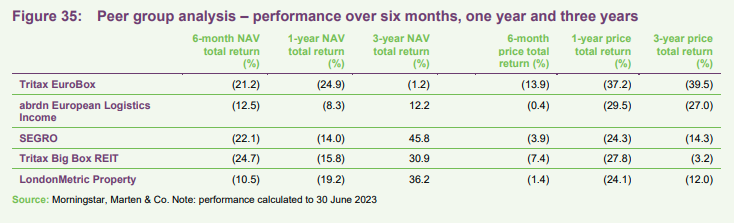

Peer group comparison

Click here for an up-to-date comparison of EBOX’s peer group.

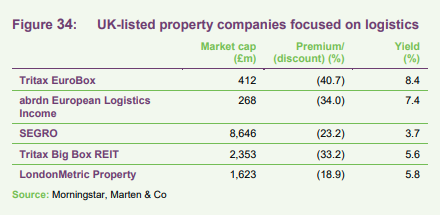

Most property companies investing in European logistics are unlisted funds or subsidiaries of larger groups. The listed peer group we have assembled consists of EBOX’s closest peer, abrdn European Logistics Income (ASLI); SEGRO, which owns a mixture of ‘big box’, urban and industrial space, about a third of which is located in continental Europe; Tritax Big Box; and LondonMetric Property. The latter two are UK-focused.

NAV and portfolio valuation

EBOX publishes its NAV twice a year, based on portfolio valuations, which are approved by the board prior to publication.

Independent international real estate consulting firm CBRE performs the valuation (which recently took over from JLL as part of EBOX’s rotation policy), in accordance with RICS guidance. Each property is unique, and the fair value includes subjective selection of assumptions, most significantly the estimated rental value and the yield. These key assumptions are impacted by a number of factors including location, quality and condition of the building, tenant credit rating and lease length. Whilst comparable market transactions can provide valuation evidence, the unique nature of each property means that a key factor in the property valuation process is the assumptions made by the valuer. CBRE’s valuation methodology also incorporates second-place bids, deals that did not close and other offers for assets on the market.

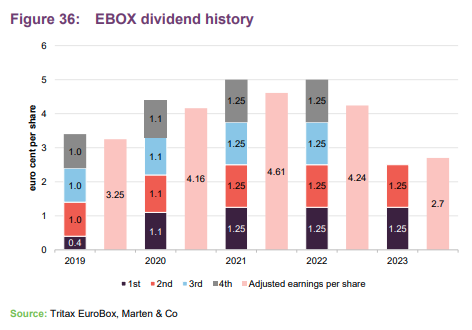

Dividend

EBOX’s quarterly dividend is declared in euros and paid, by default, in sterling (although shareholders can elect to receive dividends in euros). The euro/sterling exchange rate is determined following the dividend declaration.

In the 2022 financial year EBOX paid 5 euro cents per share in dividends, in line with the previous year. The company has maintained the same quarterly dividend level so far in the financial year to 30 September 2023. The dividend per share of 2.50 euro cents in the first two quarters of its financial year was 108% covered by adjusted earnings per share, and the group has now recorded three consecutive quarters of dividend cover (including the final quarter of its 2022 financial year).

Adjusted earnings per share was boosted by rental income growth (from full years’ rent from prior year acquisitions, new lettings and like-for-like rental growth), and lower costs (primarily due to a decrease in the investment management fee – more details on page 25). The board states that it expects the full-year dividend to be covered by adjusted earnings – even with the loss of earnings from any sales and a potential small increase in debt costs (more information on the debt is on page 26).

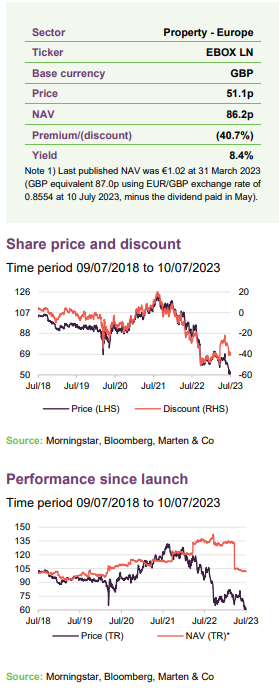

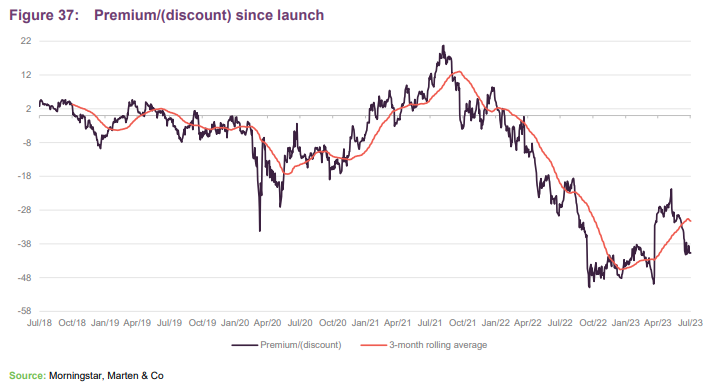

Premium/(discount)

EBOX was trading at a large premium in early 2021, perhaps as the market recognised the structural tailwinds at play in the continental logistics sector, exacerbated by the pandemic, and the work of EBOX’s manager to maximise growth through development. Its premium contracted and moved to a discount after two considerable equity raises in March and September 2021 and significant growth in its NAV.

Over 2022, EBOX’s discount widened significantly, perhaps due to the market pricing in substantial valuation declines across real estate due to higher interest rates, and on 10 July 2023 the company was trading at a 40.7% discount.

EBOX has the authority to buy back or issue ordinary shares to address anomalies in the share price performance, if necessary. In the event that the ordinary shares trade at a discount, EBOX has authority to repurchase up to 10% of its issued share capital. Similarly, should the shares trade at a premium, EBOX has the authority to issue new shares that could be used to satisfy any excess market demand.

The manager says that buybacks are always a consideration at the current discount but believes it can find better returns through investing any proceeds from sales into asset management opportunities in the portfolio. The manager says that it continues to assess development opportunities but recognises the high hurdle for returns in the current share price position.

Fees and costs

EBOX’s management fees were reduced in 2022, effective from 1 August 2022, and are now charged according to the following structure: 1.0% of net asset value up to €1bn; and 0.75% of net asset value above €1bn. It had previously been 1.3% of net asset value up to €1bn, 1.15% between €1bn and €2bn; and 1% above €2bn. EBOX does not pay a performance fee. In the year to 30 September 2022, the manager was paid €11.86m (2021: €7.88m). The manager estimates that the new structure could save an additional €1.1m in the six months to 30 September 2023 (based on the NAV at 31 March 2023).

All costs in relation to core asset management services (which includes fees paid to LCP and Dietz) are paid by the manager from the management fee. Property management services are paid by the company (around €450,000 a year).

The company’s adjusted EPRA cost ratio fell to 25.6% at 31 March 2023 (from 29.5% at 30 September 2022), mainly as a result of the reduced management fees. The sharp fall in NAV in March 2023 will result in a further drop (estimated to be an additional €1.1m) in management fees for the six months to 30 September 2023. The manager expects the adjusted EPRA cost ratio to be within its target range of between 20% and 25% by the end of its financial year (30 September 2023).

Administrative, secretarial and registrar services

Administrative and accounting services are provided by CBRE. EBOX consolidated both the administration and property management services to CBRE in 2019 on the premise that one supplier using the same software and systems would deliver better operational efficiencies.

Company secretarial services are provided by the manager. The registrar is Computershare Investor Services.

Portfolio valuation services

The portfolio valuation services provided by JLL incurred a fee of €124,800 in the year to 30 September 2022 (2021: €75,400).

Capital structure and life

EBOX has a simple capital structure with a single class of ordinary shares in issue and trades on the main market of the London Stock Exchange. As at 10 July 2023, there were 806,803,984 ordinary shares in issue and no shares in treasury.

Debt

EBOX had total drawn debt of €779.0m at 31 March 2023, equating to an LTV ratio of 44.9% (up from 35.2% at 30 September 2022 due to the fall in value of the portfolio). Including capital commitments for development and asset management projects, the group’s proforma LTV was 46.0%. Whilst this is in line with its previously stated medium-term target of 45%, the company is looking to reduce the LTV to around 40% through asset sales (as mentioned earlier).

The majority of the group’s debt is fixed (73%), with its €500m senior unsecured green bond (which has a coupon of 0.95% per annum) maturing in 2026 and a €200m US private placement (which is made up of three tranches with an average coupon of 1.37%) not maturing until 2029. The group’s €250m revolving credit facility (RCF – of which €79m is currently drawn, with a further €33m earmarked for near-term capital commitments) is not fixed, but the company has interest rate caps in place to hedge against a rise in underlying interest rates. The RCF, which matures in 2025, is provided by a group of lenders –BNP Paribas, Bank of America Merrill Lynch, Bank of China and Banco de Sabadell – and has a margin of between 1.2% to 1.9% above the higher of zero or Euribor. The company holds interest rate caps worth €250m that act as a hedge against the RCF, limiting the rise in Euribor to 0.65%. These interest rate caps mature in October 2023. The manager says that it plans to renew a far smaller portion of the €250m caps in place (as it does not plan to increase its use of the RCF). This is likely to be at a higher strike price, it adds, but the smaller portion will negate any material uplift in the overall cost.

The group’s current average cost of debt was 1.22% at 31 March 2023. This would rise to a maximum of 1.46% if the whole of the RCF was drawn. However, the manager says that it expects the majority of the RCF to remain undrawn in the near-term. The impact of the renewal of the interest rate caps on the RCF will have a minimal impact on the overall cost of debt. The weighted average maturity is four years.

EBOX’s primary debt covenants relate to LTV (maximum of 65%), interest cover (minimum of 1.5 times) and gearing ratio (maximum of 150%). Interest cover as at 31 March 2023 was 4.4 times and the gearing ratio was 87%. The value of its portfolio would need to fall by 30% and income to drop by 66% for covenants to be breached (from 31 March 2023 levels), the manager says.

Financial calendar

EBOX’s year-end is 30 September. The annual results are usually released in December (interims in May) and its AGMs are usually held in February of each year. EBOX pays quarterly dividends in March, June, September, and January.

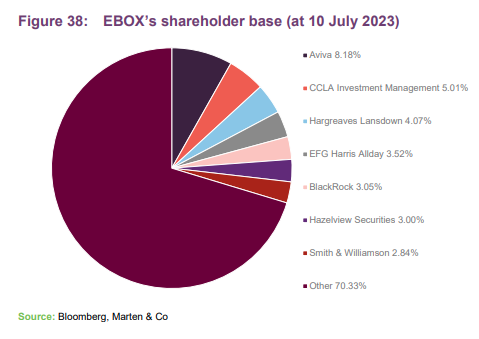

Major shareholders

Management team

The manager has in place an experienced team of investment and asset management specialists. The team has the ability to access off-market transactions in the logistics real estate sector through an extensive and established network across the UK and continental Europe. Key senior personnel include:

Phil Redding – Chief executive

Phil was appointed fund manager in September 2022 and is responsible for leading the group’s fund management function, with overall responsibility for the provision of strategic investment advice to the group. He is chairman of the investment and executive committees. Phil started his career at King & Co (now JLL) where he qualified as a chartered surveyor in its industrial agency and development division in 1992. In 1995, he joined SEGRO plc, holding a number of management positions before becoming chief investment officer and member of the board in 2013. Phil joined Tritax Group in 2020.

Mehdi Bourassi – finance director

Mehdi joined Tritax Group in May 2019. He is responsible for historical and strategic financial matters in relation to the company, including half-year and year-end reporting, transaction structuring, corporate compliance, budgeting/forecasting, treasury management, monitoring of internal financial controls and the company’s wider capital market activities. Mehdi has 10 years’ experience in pan-European real estate finance roles, most recently at Savills Investment Management as finance manager, focusing on executing real estate transactions across Europe. Previously, he worked as financial controller in real estate at Abu Dhabi Investment Authority (ADIA). He began his career at PricewaterhouseCoopers (PwC) in Luxembourg, conducting audit engagements mainly for real estate and private equity clients. Mehdi holds an MSc in Management from IESEG School of Management and an MBA from London Business School.

James Dunlop

James has overall responsibility for identifying, sourcing and structuring investment assets for the company. He is one of the founding partners of the manager, and became a partner at Tritax Group in 2005. He is responsible for identifying sectors and specific properties, negotiating on approved opportunities and handling the disposal of assets in due course. James read Property Valuation and Finance at City University and qualified as a chartered surveyor in 1991.

Henry Franklin

Henry is responsible for the structuring of the Tritax Group funds, providing general legal counsel and overseeing compliance activities. He is a qualified solicitor who completed his articles with Ashurst in 2001, specialising in taxation and mergers and acquisitions. He also qualified as a chartered tax adviser in 2004 before moving to Fladgate in 2005, where he became a partner in 2007. At Fladgate, Henry specialised in the structuring of commercial property funds. He joined Tritax Group in 2008.

Board

EBOX’s board comprises five directors, all of whom are non-executive and considered to be independent of the investment manager. All directors stand for re-election on an annual basis.

Robert Orr (chairman)

Robert is chairman of the group and chairman of the nomination committee. He has extensive board experience at a strategic and operational level in the real estate industry, most significantly as JLL’s European chief executive and currently as a non-executive director of M&G European Property Fund SICAV. He is a qualified chartered surveyor and has an in-depth knowledge of the real estate industry, in particular the European real estate markets. He founded the International Capital Group for JLL in 2005, establishing strong relationships with international investors seeking real estate investment opportunities. Robert is also appointed to the board of APCOA Parking Holdings GmbH, and is a member of the investment advisory committee of EQT Real Estate and a senior adviser to Blue Coast Capital (Lewis Trust Group).

Sarah Whitney

Sarah is senior independent director of the company. She has over 35 years of senior executive experience advising international and UK organisations and boards on strategy, corporate finance, and real estate and economic development matters, as well as complementary non-executive expertise. Sarah’s current non-executive positions include JPMorgan Global Growth & Income plc, BBGI Global Infrastructure S.A. (the FTSE 250 global infrastructure investment company), and Bellway Plc. Previously, she was a non-executive director at St Modwen Properties Plc, until August 2021 when it was acquired by Blackstone. Sarah’s senior executive roles have included roles at PwC, DTZ Holdings (now Cushman & Wakefield), and CBRE. Sarah is a Fellow of the Institute of Chartered Accountants in England and Wales.

Keith Mansfield

Keith is chairman of the audit committee. He is a chartered accountant with extensive experience of leading significant international transactions. He spent 22 years as partner at PwC, where he developed a specialisation in the real estate industry. He served as regional chairman of PwC in London for seven years. He has previously been a board member of Tarsus Group plc, where he was also chairman of the audit committee, and chairman of Albemarle Fairoaks Airport Limited. Keith is currently a non-executive director at DGI9 following its admission to trading on the London Stock Exchange on 31 March 2021, a director at Real Time Sports Bingo Limited and Motorpoint Group plc.

Taco de Groot

Taco is chairman of the management engagement committee. He is a chartered surveyor with significant experience in the real estate and investment funds markets. He was a founding partner of M7 Real Estate in the UK, as well as at GPT/Halverton, Heston Real Estate B.V. and Rubens Capital Partners. Taco has also been chief executive of Cortona Holdings BV, based in Amsterdam, and Vastned Retail NV, a European retail property company listed on Euronext Amsterdam. He is currently a non-executive director of EPP NV, a real estate investment company that operates throughout Poland, and Brack Capital Properties NV, which is listed on the Tel-Aviv stock exchange.

Eva-Lotta Sjöstedt

Eva-Lotta is chairman of the company’s ESG committee. She has extensive experience in global retail, supply chain and digital transformation strategy. She has been chief executive of Georg Jensen, a Scandinavian luxury jewellery and home design brand, and Karstadt, a German premium luxury department store chain. She has also held several senior roles over a 10-year period at IKEA including deputy global retail manager, responsible for the development and implementation of IKEA’s global omnichannel strategy, chief executive of IKEA Holland, and deputy retail manager at IKEA Japan. Eva-Lotta is currently a supervisory board member at METRO AG, a leading international wholesale and food service company, and non-executive director of Elisa Corporation, a telecommunications company registered on the Nasdaq Helsinki.

Previous publications

QuotedData has previously published four notes on EBOX. You can read them by clicking the links below or by visiting our website.

Figure 40: QuotedData’s previously published notes on EBOX

| Title | Note type | Publication date |

| Boxing clever | Initiation | 23 November 2020 |

| Full throttle | Update | 25 May 2021 |

| Fast-tracked | Annual overview | 27 January 2022 |

| Opportunity knocks | Update | 18 November 2022 |

Source: Marten & Co

Legal

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Tritax EuroBox Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it, but in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.