As inflation recedes across the bulk of the world’s developed economies, all eyes turn to the path of interest rates and the speed with which these come down in the coming months. Several major central banks have already cut their interest rate, including the Bank of England (BoE) which reduced its base rate to 5% on 5 August, the first reduction in over four years.

While markets generally view these cuts as a positive, it’s important to consider the fundamentals driving these decisions. In the context of the UK, falling inflation and better than expected growth has allowed the BoE a degree of flexibility to cut on its own terms. In contrast, US cuts appear predicated on the strength of its labour market, which has weakened considerably in recent months, with US unemployment hitting its highest level since October 2021.

Falling interest rates in the UK are also set against a backdrop of historically low equity market valuations, which stands in contrast to the US.

“Once again we have the contradiction of an expensive US equity market expecting both strong EPS growth over the coming years yet accompanied by significant interest rate cuts to stave off recession. Both cannot be right.” – Andrew Lapthorne, Société Générale.

However, it was the knock-on effect of the Bank of Japan’s end of July decision to increase its key interest rate to 0.25% – which led to a sharp recovery of the yen – that may have triggered a sell-off in markets early in August (as investors unwound trades financed with yen denominated debt), especially as it coincided with the poor US jobs data mentioned above.

Elsewhere, China continues to grapple with deflation amid an ongoing domestic demand crisis, while election outcomes in Germany and France add to a growing sense of unease across the EU.

Greater stock market volatility is the long-term friend of the active investor.

Pershing Square Holdings

Markets will need to reassess what constitutes a ‘normal’ policy rate going forward, which may well be significantly higher than the pre-Covid period.

F&C Investment Trust

The recent pick up in M&A activity in the UK market suggests investors are beginning to recognise the value on offer.

JPMorgan Claverhouse

At a glance

| Exchange rate | 31 August 2024 | Change on month % | |

|---|---|---|---|

| Pound to US dollars | GBP / USD | 1.3127 | 2.1 |

| Pound to Euros | GBP / EUR | 1.1882 | 0.1 |

| US dollars to Japanese yen | USD / JPY | 146.17 | (2.5) |

| US dollars to Swiss francs | USD / CHF | 0.8496 | (3.2) |

| US dollars to Chinese renminbi | USD / CNY | 7.0913 | (1.9) |

Source: Bloomberg, QuotedData

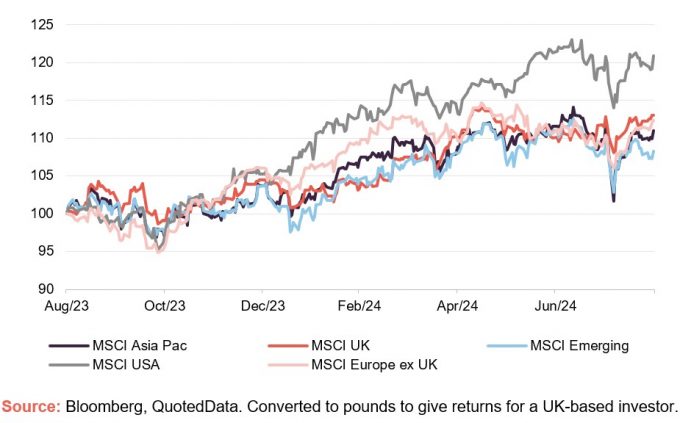

MSCI Indices (rebased to 100)

Market returns were modest across the board in August, however this masks a brief period of panic as weak macro data in the US helped spark a global volatility shock.

On average, the MSCI indices faced a peak to trough dip of over 6%. While these losses were recovered over the course of the month, the scale of the move highlights the vulnerabilities of the US centric, global market. This uncertainty is reflected in the steep drop in US treasury yields and the ongoing rally in gold, as well as the market volatility we have seen in early September.

MSCI Indices (rebased to 100)

| Indicator | 31 August 2024 | Change on month % |

|---|---|---|

| Oil (Brent – US$ per barrel) | 78.80 | (2.4) |

| Gold (US$ per Troy ounce) | 2503.39 | 2.3 |

| US Treasuries 10-year yield | 3.90 | (3.1) |

| UK Gilts 10-year yield | 4.02 | 1.1 |

| German government bonds (Bunds) 10-year yield | 2.30 | (0.2) |

Source: Bloomberg, QuotedData

Global

Beatrice Hollond, chairman, F&C Investment Trust, 1 August 2024

While the fundamental backdrop is constructive and US recession has been avoided, global equity markets, dominated by the US, continue to trade at historically elevated valuation levels. Strong growth in earnings has propelled most of the so-called “Magnificent Seven” group of stocks to new highs but elevated valuations and market concentration remain a concern, with optimistic earnings expectations presenting an additional challenge if investment in AI fails to translate to sustained growth in earnings. Politics will remain an area of focus for investors in 2024 and, while a Labour government with a significant majority may present a more stable backdrop for UK assets, the US and Europe face a period of political uncertainty in the months ahead. This, in conjunction with signs of moderating US growth after a strong period, presents some near-term risk for equity markets.

There remain grounds for optimism, however, including for international equities that have struggled to beat the technology-heavy US market for many years and which potentially stand to benefit from a broadening out of the equity rally. Improving economic prospects and earlier interest rate cuts may provide a near-term tailwind for European and UK equities, while corporate governance reform means that Japan continues to look attractive from a longer-term structural perspective. In addition, there are now signs of progress (in terms of valuation uplifts and increased pace in realisation of investments) in the private equity sector, helped by a pickup in merger and acquisition activity, which should provide further support.

. . . . . . . . . . .

Paul Niven, fund manager, F&C Investment Trust, 1 August 2024

Recent equity market performance has been robust – inflation is trending lower, cuts in interest rates are on the horizon, growth has been more resilient than expected and earnings have surpassed expectations. Market pricing now assigns a low probability to a recession and the industry consensus expects a healthy growth in earnings for the S&P 500 in 2024. However, with the ten largest stocks in the S&P 500 now accounting for more than 35% of the market’s total capitalisation, and almost 30% of its net income, equity markets are vulnerable to slowing momentum in this segment of the market. It is notable that the major winners of the broader AI theme, at least so far, are the infrastructure vendors, or ‘enablers.’ This includes cloud platform providers like Google, Microsoft and Amazon and graphics processing unit (GPU) producers like Nvidia and others. AI is still at an early stage of adoption overall and, while in the longer term there are likely to be significant benefits, most companies today lack the foundational building blocks that enable AI to generate value and productivity gains at scale. Moreover, signs of a weaker US consumer, including a sharp drop in home sales and an uptick in consumer delinquencies, and a potentially highly consequential US presidential election in November, present additional near-term risks for equity markets. Furthermore, if a ‘soft’ landing has been achieved with interest rates at current levels, then markets will need to reassess what constitutes a ‘normal’ policy rate going forward, which may well be significantly higher than the pre-Covid period.

. . . . . . . . . . .

Managers, RIT Capital Partners’, 1 August 2024

We face a mixed economic backdrop ahead and although we see inflation continuing to taper, the risk of an economic slowdown remains. Many consumer-facing companies in the US have highlighted weakening consumer demand, the lack of discretionary spending and a general malaise. Amidst this mixed macroeconomic backdrop, we continue to focus on specific top-down themes and bottom-up individual investments, seeing opportunities across our pillars.

Within Quoted Equities, we are finding compelling opportunities in SMID-cap companies, especially in Europe and the US. Among larger companies, we remain very selective in those that we believe are misunderstood by the market, and our bias remains towards quality, given slowing economic data and uncertainty driven by elections. Regionally, we continue to favour Japan which offers attractive valuations, resilient earnings revisions as well as a fertile stock picking ground.

Across Uncorrelated Strategies, we believe returns on our credit portfolio should remain healthy, as the historically high yields on offer in specific individual companies are compelling. As part of ensuring we have a resilient portfolio, we will continue to use our gold exposure as a helpful diversifier in times of heightened geopolitical tensions, or should rates fall more sharply than expectations on the back of a rapid downturn in growth.

On our private investments, we are optimistic that the recent uptick in transactions will build momentum in the second half of the year. M&A volumes on the public side have increased so far in 2024, normally a good lead indicator for IPOs. We believe we may well see increasing signs of recovery as the year progresses and into 2025.

. . . . . . . . . . .

Managers, Murray International, 9 August 2024

While the first half of 2024 showed signs of economic resilience and recovery in places, several factors contribute to a cautious outlook for the global economy. The recovery has been uneven, with significant disparities between regions and sectors. Corporate earnings have been strong, particularly in the technology sector, which has benefited from advances in AI and increased productivity. However, the reliance on a few key industries and companies raises concerns about market concentration and the sustainability of growth. Any setbacks in these sectors could lead to broader market corrections.

Inflation remains a concern. Although inflation rates have moderated in some regions, they are still above the targets set by central banks, which are trying to navigate the delicate balance between controlling inflation and supporting growth. The inflationary environment of the last few years has eroded purchasing power in many regions, affecting consumer spending. Although labour markets have stabilised, wage growth has not kept pace with inflation in many areas, potentially limiting consumer driven economic growth.

Geopolitical tensions are another significant risk. The ongoing war in Ukraine, the conflict between Israel and Palestine, and broader political tensions between East and West have the potential to disrupt trade, impact inflation, destabilise the global economy and severely weaken investor sentiment. The political landscape in the United States remains highly charged as the presidential election approaches. The division between Democrats and Republicans is deepening, and if this political turmoil deteriorates further, it could worryingly test American democracy and impact its international standing.

In summary, while there are positive signs of economic recovery and growth in specific sectors, the global economy faces several significant risks and uncertainties. Inflation, geopolitical tensions, market concentration and consumer confidence are all factors that could derail equity markets trading at lofty levels and lead to increased volatility. Policymakers and businesses must navigate these challenges carefully to sustain growth and stability in the coming months.

. . . . . . . . . . .

Andrew Ross, chairman, Witan Investment Trust, 13 August 2024

Investors have largely shrugged off disappointments in the timing of interest rate cuts, unwelcome developments in global conflict hotspots and uncertainty generated by 2024’s wide swathe of national elections. Notwithstanding a sharp bout of volatility in early August, equity markets as a whole seem to have taken the view that, whatever flies there may be in their proverbial soup, they are focused on the substance, not the swimmer.

This insouciance, complacency to some, is helped by the increased proximity of easier monetary policy, after the prospect of rate cuts retreated for much of early 2024. The European Central Bank, with a relatively weak continental economy, has led the way, followed by the Bank of England in early August. The US Federal Reserve, while holding rates steady at the end of July, indicated that a September cut was on the cards, as long as the incoming data on inflation and the labour market remained supportive.

Whilst politics remain in flux in some countries in Europe and ahead of the US presidential election, resolution of the uncertainty in the UK has been greeted by a positive initial reaction. The pre-election tendency for the news to highlight every problem as a half-empty glass has abated, while the absence of fiscal room for manoeuvre aligns the country’s need for improved productivity with the incoming government’s need for resources to fund reforms to public services, from health to defence. If the government lives up to its “New New Labour” credentials the low valuation of the UK market could find the catalyst it needs to be more positively rated.

. . . . . . . . . . .

UK

Neil Hermon, manager, Henderson Smaller Companies, 1 August 2024

Whilst global inflation has fallen significantly over the last year, it remains above official targets. Hence central banks, led by the US Federal Reserve, have retained their generally hawkish stance. However, it is clear we have reached the end of the monetary policy tightening cycle and the next movement in rates will be downwards. What is not clear is the timing of when rates start to fall and the speed of their descent. So far in 2024, economic data, particularly services and wage inflation and labour market activity, has surprised negatively, pushing expectations of interest rate cuts further into the future. In the meantime, the delayed transmission mechanism of rising interest rates and their impact means that economic conditions are likely to remain challenging in the short term. Notwithstanding this, the prospect of a monetary easing cycle is likely to support global equity markets and allow valuation multiples to expand.

Geopolitics remain challenging, with the ongoing conflicts in Ukraine and the Middle East and heightened tensions between China and the US. The longer-term economic implications of this are material. There is an urgent need to reduce European dependence on Russian oil and gas supplies and a requirement to decrease China’s influence on the global supply chain through investment in nearshoring capability. In addition, domestic politics are likely to be an area of volatility. Up to half the global population is going to the polls in 2024 with key elections in the UK, USA, France, India, Mexico, South Korea and the EU. In the UK, a surprise early election has resulted in the expected Labour landslide win, mostly due to dissatisfaction with the incumbent Conservative Government rather than enthusiasm for the Labour Party. The strong majority should allow for a stable government, and one that is less reliant on the fringes of their party. We see this result as a clearing event for the market and expect the political premium associated with the UK to reduce over time. We welcome Labour’s commitment to ‘boost investment’ and in particular their pledge to ‘increase investment from pension funds in UK markets’. Any incremental flow into the UK could breathe life into a generally under-owned and, more importantly, undervalued UK equity market.

In the corporate sector, we are encouraged by the fact that conditions are intrinsically stronger than they were during the Global Financial Crisis of 2008-2009. In particular, balance sheets are more robust. Dividends have recovered strongly post-pandemic and we are seeing an increasing number of companies buying back their own stock.

The IPO market has been exceptionally quiet as equity market confidence has diminished. There are some signs that this is likely to improve in the short to medium term, with the recent successful float of Raspberry Pi providing evidence that the UK equity market remains open for attractive, growing businesses. M&A activity has remained robust as acquirors, particularly private equity, look to exploit opportunities thrown up by the recent equity market falls. We expect this to continue in the coming months as UK equity market valuations remain markedly depressed versus other developed markets.

In terms of valuations, the equity market is trading below long-term averages. In addition, smaller companies are trading at a historically high discount to their larger counterparts. A sharp rebound in corporate earnings following the pandemic-induced shock in 2020 has now faded. Weak economic activity led to subdued corporate earnings growth in 2023 compounded by rising interest costs and a higher corporate tax burden. The outlook for 2024 looks more favourable as cost pressures ease and demand remains generally robust.

. . . . . . . . . . .

Matt Cable, manager, Rights and Issues, 6 August 2024

As discussed in our last annual report, inflation has continued to moderate in the UK, broadly in line with market expectations. This in turn has increased investor confidence in interest rate cuts later in the year which should be positive for economic activity and hence equity returns. A notable feature of the first half has been a divergence between such expectations for the UK and the US, where there remains greater uncertainty.

The UK general election was called towards the end of the period and held on 4th July and, as expected, the Labour party won with a large majority. This outcome was widely anticipated so is unlikely to have a short-term impact on markets. Over the coming months we will be watching closely as government policy becomes more apparent, especially in areas such as labour policy, tax and international relations.

Following a challenging period for UK equities the macroeconomic backdrop appears to be improving, with inflation under control and the potential for lower interest rates. This should create better conditions for equity investors. At the same time, the UK election allows for a period of greater political stability which should mean businesses can plan with more certainty and investors can build confidence in the outlook.

Clearly macroeconomic risks remain, from the ongoing conflict in Ukraine to uncertainty around the US election. However, we approach the remainder of the year with a degree of optimism and continue to look for attractively valued investment opportunities in our market.

. . . . . . . . . . .

David Fletcher, chair, JPMorgan Claverhouse, 9 August 2024

The geopolitical climate remains a significant concern for investors. Tensions between Russia and the NATO countries are simmering as the war in Ukraine drags on, the conflict in the Middle East shows little sign of resolution, and Sino-US relations remain fraught, despite a flurry of high-level, relatively congenial meetings earlier this year. There is a risk that the outcome of November’s US presidential election will escalate tensions on all these fronts and spark fresh bouts of market volatility. In the short term the recent decision by US President Biden not to run for re- election in November will increase market uncertainty.

In the UK, the market environment is more positive, and we share the managers guarded optimism about the prospects for the market and the company. The likelihood of imminent decreases in UK interest rates, combined with rising real wages, has boosted business and consumer confidence. On the political front, the prospect of a more stable political climate following the general election last month has been welcomed by investors.

Despite these favourable developments, UK equity valuations remain attractive in absolute terms and relative to other markets. The recent pick up in M&A activity in the UK market suggests investors are beginning to recognise the value on offer, but there is scope for further significant gains, as and when corporate earnings prospects improve and investors’ confidence in this market increases. Meanwhile, investors, both in the UK and abroad, have a rare opportunity to access the attractive dividend yields on offer in the UK at historically low valuations.

. . . . . . . . . . .

Managers, The Diverse Income Trust, 20 August 2024

We are optimistic and think that a UK-quoted multicap equity income strategy has excellent prospects: The UK stock market itself stands on a low valuation, having been outpaced by others during globalisation. ‘The smallcap effect’. As UK-quoted smallcaps are standing on absurdly low valuations currently, their upside potential appears to be even greater than mainstream stocks. The UK stock market has recently broken out of its 1999 trading range on the upside. This is significant in our view because it has occurred at a time when local investors continue rapidly to sell down their local holdings.

The notion of the UK stock market becoming a global leader may appear remote. But this is usual at recovery points and has happened previously. Between 1965 and 1985 for example, the UK stock market greatly outperformed the US stock market. We believe it is set to do so again.

Given that the UK stockmarket is starting from what appears to be a very undemanding valuation, and few global investors have a weighting in it, when it recovers it has the potential to outperform international markets for a long period, maybe a decade or two.

. . . . . . . . . . .

Richard Wyatt, chairman, Temple Bar Investment, 20 August 2024

The UK stock market enjoyed a positive first half of the year, supported by an increase in M&A activity and in companies buying back their own shares; both a reflection of the perceived value offered by current valuation levels.

With the election of a new government in a landslide result, the UK offers the increasingly rare attraction of political stability. Combined with the continued appealing valuations offered by UK equities, particularly when compared with the valuations seen in certain overseas markets and sectors, the outlook for UK equities is positive.

. . . . . . . . . . .

Asia

Ian Cadby, chair, abrdn Asian Income Fund, 15 August 2024

The potential return of Donald Trump as US President has caused uncertainties in markets across Asia. Given Donald Trump’s actions in his previous term, investors are justifiably concerned about the risk of tariffs and a renewed trade conflict with Asia. Such measures, if implemented, would weigh on currencies, businesses, consumer sentiment, economies and risk appetite in general. However, this potential impact should be weighed against the likely boost from the expected easing of interest rates by the Federal Reserve in the latter months of 2024. While we would expect uncertainty to persist through to the election in November and beyond, we would see any potential impact from US policy and political developments as a nuanced one, with differing impacts across different economies, sectors, businesses and the consumer.

In China, the Third Plenum, a major meeting held roughly once every five years to map out the general direction of the country’s long-term social and economic policies, has just concluded. There was an emphasis on discussing near-term issues, reflecting some urgency following a disappointing second-quarter of GDP growth. While there were few details on reforms, the tone and focus remained unchanged, with a balance between security and development goals. Post the Plenum, there has been incremental stimulus, starting with the cutting of policy rates by the central bank and the easing of demand and supply conditions in the bond market.

Over the longer term, we continue to view Asia as one of the most compelling regions for investors looking for growth and income potential. The region is clearly more than just China, with opportunities abounding across the broader area. Asian markets have been tarnished by investor concerns over China, but we believe this overlooks the excellent progress the broader Asian region has made in recent years in strengthening its economies, shoring up its currencies, creating employment, adopting technology and driving innovation.

More than 50% of Asian equity total returns now come from dividends and dividend growth. Companies in Asia have less geared balance sheets than their global peers and free cash flow generation cover on dividends has been increasing, both of which highlight the potential for increasing payout ratios in the region. Today, we believe little of this significant progress is priced into markets, with the MSCI Asia Pacific ex Japan Index trading on just 13xPE, compared to the S&P 500 Index on nearly 21xPE. We believe that the often-overlooked dividend credentials of Asian equities will become ever more attractive, with investors increasingly recognising the income potential of some of the world’s most exciting companies.

. . . . . . . . . . .

Europe

Sam Morse, manager, Fidelity European, 2 August 2024

The COVID-19 global pandemic — a “once in a century” event — has set off a long-lasting chain reaction that is unpredictable and makes fools of forecasters (including the Company’s Portfolio Managers!). We thought the rapid and steep monetary tightening which followed the pandemic would end in recession, as it so often does, following an inversion of the yield curve. That has not, to date, been the case. Indeed, the global economy has been much more resilient than anticipated and corporate earnings have held up well supporting stock markets around the world. As highlighted above, many stock markets are reaching all-time highs. However, we are now seeing some signs of consumers reining in their spending, particularly in the US. Consumption is the main growth engine of developed economies. Is this an early warning sign that the dreaded recession is upon us just as the optimists declare victory? To add to this, there is considerable geopolitical uncertainty expected post the US elections, not least the potential changes in US foreign policy when it comes to the tragic Ukraine war. In the event of a downturn, stubborn inflationary pressures could prevent a rapid easing in monetary policy. Continental European governments remain heavily indebted and are already running substantial budget deficits so fiscal easing would also be constrained. Valuations no longer discount an economic malaise. So, in short, we are cautious and see the stock market as being vulnerable if the outlook worsens and sentiment shifts to be more negative.

Whatever the constitution of the new French government following the result of the French parliamentary elections, we have little optimism regarding the short or long-term outlook for the French domestic economy for the same reasons that we are gloomy about the outlook for the domestic economies of Europe (which represent about one third of the sales and profits of continental European companies). Ageing populations, low productivity, high and growing levels of government debt, etc., will mean that growth is likely to remain anaemic. Thankfully, domestic France represents a relatively small percentage of sales and profits for continental European companies.

. . . . . . . . . . .

Stuart Paterson, chair, European Assets Trust, 8 August 2024

Following the invasion of Ukraine and the impact on energy prices and inflation, central banks underestimated the inflation problem forcing them to raise interest rates rapidly. Tighter monetary policy is now taking effect and inflation is falling. European economic growth is gradually improving, although manufacturing continues to lag the services sector.

After these falls in inflation, the interest rate environment in both Europe and the US appears more benign. The European Central Bank has begun to ease monetary policy, as have Switzerland and Sweden; the US Federal Reserve is expected to follow suit later this year. Lower interest rates have historically benefited smaller companies to a greater extent than larger companies. The improvement in the interest rate environment should benefit European smaller companies which are currently valued at historic lows.

A recession can be avoided, although this is a delicate balancing act for central banks. Global geopolitical tensions are a concern, as are the possible repercussions for energy prices. There is also some political uncertainty, including November’s presidential election in the US. The second round of voting in France has resulted in a hung parliament, averting a hard-right victory.

In European small and mid-cap equities, there are reasons to remain optimistic. Earnings have been resilient despite higher interest rates and, over the longer-term, share prices tend to follow earnings. Good companies continue to grow, and we see opportunities in the current market.

. . . . . . . . . . .

North America

Jonathan Simon, manager, JPMorgan American, 15 August 2024

There will always be some risks and uncertainties for investors to consider, and for us, at this moment, one such risk is the labour market, which we expect will continue to slow. While the overall employment market is still experiencing excess job openings, in some key sectors, including construction and retail, job openings are now below their five-year averages. If this trend broadens out, it may create a headwind for consumer spending growth over the remainder of this year and beyond. Investors are also watching developments in the US presidential race, which may increase uncertainty regarding the outcome. The result could possibly aggravate existing geopolitical tensions between the US and China, while also complicating America’s relations with its western allies. Any such outcomes could increase market volatility both in the run up to the November vote, and in its aftermath.

However, with economic growth solid, unemployment low, most of the journey back to 2% inflation completed, and rates set to decline, the US economy should continue to provide a rising tide to support most investment boats for the rest of this year and into 2025.

. . . . . . . . . . .

Bill Ackman, manager, Pershing Square Holdings, 15 August 2024

The stock market has increasingly been characterized by a growing percentage of the market capitalization of companies being held by effectively permanent owners, principally index funds. We believe that the growing index ownership as a percentage of stock market float has increased the impact that short-term, highly leveraged investors can have on price discovery as they now comprise a growing percentage of the market cap and daily trading of companies, and are important marginal buyers and sellers of a security. These shorter-term investors – which include so-called market-neutral and quantitative funds – use large amounts of margin, derivative, and total return swap leverage in their strategies. As highly leveraged market participants, these investors’ tolerance for mark-to-market losses is small, which contributes to stock price volatility as they can become effectively forced sellers when companies disappoint, even in the short term.

Equity markets have exhibited an enormous amount of single-name stock price volatility for even the largest companies when they surprise investors with even minimally below-expectation overall results or small misses on certain closely followed business metrics. Markets are also exhibiting an enormous amount of volatility when macro data surprises occur.

Greater stock market volatility is the long-term friend of the active investor with permanent capital who seeks to identify high quality companies which are not dependent on the capital markets to implement their business strategies. While an earnings’ miss or other business metric disappointment in a quarter could reflect the beginning of deterioration in fundamentals, in many cases the impact of the disappointment has only a marginal effect on long-term intrinsic value. Market overreactions to short-term bad news can drive business valuations to levels well below long-term intrinsic value and create buying opportunities coupled with a high degree of liquidity.

. . . . . . . . . . .

Managers, JPMorgan US Smaller companies, 23 August 2024

The performance of the US economy is crucial for smaller companies, as they tend to generate more of their earnings domestically than larger cap companies. Small cap companies also tend to be more exposed to the economic cycle and high interest rates, relative to larger caps, which tend to have stronger balance sheets and lower gearing.

Despite some recent slowing in growth and a weakening in labour market conditions, we expect the economy to remain in good shape, supported by eventual rate cuts and ongoing strong consumer demand. Households, that make up 70% of US GDP, continue to be in good shape with solid earnings power, which benefits corporate America. This should benefit consumer and business spending and provide support for small cap earnings, which appear poised to grow faster than large cap earnings, after two consecutive years of declines. Furthermore, small cap valuations are currently at historic lows relative to large caps, and institutional investors remain under allocated, so any improvement in sentiment towards this sector may encourage institutional investors to increase their exposure. In all, we see several reasons to be optimistic about the outlook for US small caps.

However, there is some risk that the US economic backdrop will become more volatile, especially given the forthcoming US presidential election. While we do not construct our portfolios based on top-down forecasts of macro or geopolitical factors, as these are beyond our and the investee companies’ management teams’ control, we are evaluating the impact that certain political decisions could have on company fundamentals. We will also continue monitoring incremental risks, which may create headwinds for US equities.

. . . . . . . . . . .

Global emerging markets

Maria Luisa Cicognani, chairman, Mobius Investment Trust, 2 August 2024

Uncertainties remain as we move into the second half of the year. Key issues such as inflation, interest rates, geopolitical tensions, elections and China’s slower-than-expected recovery will continue to shape the landscape. However, we believe emerging markets are poised for significant growth in the medium-term, driven by a favourable macroeconomic backdrop, structural and cyclical growth stories and attractive valuations. The rise of artificial intelligence is a key investment driver, with companies that supply major tech companies benefiting significantly from this trend, including a number of MMIT’s holdings.

We would argue, that the US market poses some challenges with its high valuations and concentrated structure, while European equities are less attractive due to concerns about an economic slowdown. Emerging markets offer a compelling diversification opportunity with strong growth potential and attractive valuations. The growing economic links between emerging markets will continue to boost inter-emerging market trade and reduce their dependence on developed markets.

The board is always mindful of the risks. The outlook for US growth, inflation, Federal Reserve rate cuts and the US dollar remains critical for emerging market assets. Chinese policy developments also require close monitoring. Geopolitical risks are inherent in emerging market investing, especially in an election year. The US elections could have a significant impact on the US dollar and foreign policy. Global geopolitical tensions, such as the war in Ukraine and the conflict in the Middle East, pose significant risks, potentially affecting energy prices and driving inflation. With the share of the democratic world shrinking and with 40% of the world living in what the EIU defines as “autocratic” states1 there will be challenges to maintain a steady state of development and growth.

. . . . . . . . . . .

Commodities and natural resources

Richard Horlick, chair, Riverstone Energy Limited, 21 August 2024

The energy demand and supply picture continues to change. The Russian invasion of Ukraine has already forced a major re-balancing as European countries successfully reduced their reliance on Russian energy, seeking new sources of supply to meet their needs. Russia, in turn, has shifted its focus to find new outlets and markets for its energy. Additionally, the impact of the transition to renewable energy is significant and has created a very dynamic market environment. It is one that requires focus, expertise and careful management.

At REL, we continue to believe in running a portfolio with both conventional and decarbonisation assets at its core. The world needs to transition but it also needs a consistent supply of energy which today can only be met by harnessing both conventional and renewable energy. The focus on a reliable and secure energy supply favours both conventional energy that is produced closer to end markets where the energy is being consumed and locally produced renewable energy. In addition, the longer tail for conventional energy use will continue to support these assets.

In the oil market, low inventories and risks to supply, driven by the tensions in the Middle East and restrictions in OPEC+ oil production growth, are likely to be somewhat offset by production growth outside of OPEC+. With continued growth in global consumption, the environment for oil remains relatively supportive. In natural gas, reductions in production may help to decrease the inventory overhang but a lot will depend on the outlook for the winter and the resulting forecast for demand.

In decarbonisation there undoubtedly remains a huge opportunity ahead. There are also, inevitably, a number of challenges in such a vast and fast-moving market. Improving energy efficiency across the system is a key area but progress on storage solutions, despite a rapid decrease in battery costs, has not been as rapid as required. Public and private solutions need to be found and governments have a critical role to play in helping develop a supportive environment for investment, reduce friction in the system and help speed up progress in the delivery and efficacy of renewable energy. The benefits of the Inflation Reduction Act and the Bipartisan Infrastructure Act are feeding through, reflecting and accelerating similar policies and regulations in the EU. In addition, 37 per cent. of the EU’s post-Covid recovery plan are being spent on climate initiatives as will 30 per cent. of the total expenditure for the long-term EU budget (2021-27), notwithstanding recent EU elections.

. . . . . . . . . . .

Charles Goodyear, chairman, BlackRock World Mining Trust, 23 August 2024

Looking ahead, market volatility is unlikely to abate. 2024 marks a significant year for elections worldwide bringing uncertainty on the policy and geopolitical front. China, one of the most important economies for commodity demand, has also fueled concerns for the growth outlook and there is the potential for mounting geopolitical risk, primarily in the Middle East. Although inflationary pressures are easing, a measured approach by each central bank would indicate potential interest rate cuts in Europe and Asia and an increasing likelihood of a rate cut in the US.

However, there are reasons for optimism for the commodities sector. The mining industry is key to delivering the materials required for infrastructure investment, including the investment required to support the transition to a low carbon energy environment. This transition is expected to drive materials demand for many years to come. Artificial intelligence (AI) systems depend on minerals and metals in several ways and the investment in AI data centres and power grids is also set to bolster metals demand. Despite the pick-up in M&A activity, we are pleased to see mining companies continue to show strong capital discipline, which should ensure that there is an appropriate split of available cash flow between shareholder distributions and growth.

. . . . . . . . . . .

Managers, chairman, Golden Prospect Precious Metals, 30 August 2024

As previously discussed, we have a positive outlook for the miners as higher precious metal prices feed through to earnings, whilst we believe cost inflation pressures should lessen going forward enabling stronger returns. We are hopeful the sector will remain disciplined, allowing more dividends and buybacks which should attract generalists back to the sector. Many of the drivers of precious metal pricing should remain, such as Central Bank demand, whilst its use as portfolio protection should continue to support flows. ETF holdings have recently shown additions, which should that remain, can further tighten global balances. Stocks are at low earnings multiples so have room for expansion with improving sentiment on their ability to execute, even without a better gold/silver price. We are hopeful that they can demonstrate this over the next few quarters.

. . . . . . . . . . .

Environmental

Glen Suarez, chairman, Impax Environmental Markets, 12 August 2024

Political momentum for decarbonisation is gaining traction globally, with several key regions embracing ambitious climate goals. In the US, UK and EU, policies are increasingly aligned with green initiatives, reflecting a strong commitment to reducing carbon emissions. Notably, China’s third plenum has, for the first time, pledged to pursue decarbonisation, signalling a significant policy shift for the world’s largest emitter.1 Meanwhile, Australia is making strides in renewable energy investment and policy frameworks.

With ongoing cost reductions and favourable policies, renewable energy’s economic appeal is growing, accelerating the shift to sustainable energy. Recent examples include Indian energy production offering ongoing (rather than intermittent) solar power at lower rates, reflecting the sector’s increasing cost-competitiveness, while in the U.S., Texas stands out for having the largest renewable market share without state subsidies, highlighting the sector’s market viability. The cost reductions in renewables are driven by economies of scale, improved supply chains and technological advancements.

It is encouraging to learn that according to Bloomberg NEF, the world may have hit a pivotal milestone by reaching peak carbon emissions last year. This suggests that emissions from energy and industry in particular have likely topped out, setting a precedent for a downward trend. This peak is a significant marker in the fight against climate change, indicating a shift towards greener energy sources and more sustainable practices. It reflects the cumulative impact of worldwide efforts in renewable energy adoption, energy efficiency improvements and stringent environmental policies.

. . . . . . . . . . .

Infrastructure securities

James Smith, manager, Premier Miton Global Renewables – 1 August 2024

The market has reassessed both the timing and pace of the current interest rate cycle, pushing back the date at which the major western central banks will begin to ease monetary policy. High levels of government spending, wage pressures, and residual liquidity from Covid stimulus programmes have combined to keep core inflation high, despite headline inflation easing somewhat as energy prices moderated.

The performance of renewable energy companies has been highly correlated to interest rate expectations, with fundamental company performance being relegated to a secondary factor. This has however, had positive implications for company valuations as earnings have continued to grow in many holdings even while share prices have fallen.

The operational environment has become increasingly positive as the half year progressed. Gas and electricity prices fell over the first few months of the year, before strengthening again over the second quarter. The market price of European carbon permits followed a similar pattern. Capital costs for new renewable energy projects have stabilised, although with continued downward pressure on solar costs due to over-capacity in the supply chain. Several holdings made positive comments about the availability of attractive returns on new investment.

An emerging positive trend is the outlook for power demand from data centres, and in particular from artificial intelligence.

Despite recent poor performance, we believe the UK listed renewable energy investment companies remain attractive investments. Discounts to NAVs are at high levels. Dividend yields remain high, typically between 7.5% and 10.0%, with dividends being well covered by cash flows. Several companies are buying back shares, both absorbing excess supply and providing a modest boost to NAV per share in the process.

We hope to see the beginning of long-awaited monetary easing in the second half of 2024. Given that higher rates have had a very negative impact on sector valuations, we believe it reasonable to hope that the opposite is also true.

Irrespective of interest rate driven market sentiment, the sector is continuing to invest and grow earnings. The current commodity price environment is relatively benign which may reduce the earnings volatility seen in some companies in recent years. A period where earnings growth is more reflective of underlying business growth, rather than commodity price movements, would be welcome.

We have recently seen a step-up in demand for renewably generated power from technology companies and data-centres. Long term technology trends such as the use of artificial intelligence, are likely to lead to higher electricity demand in future. It is also illustrative of the fact that large corporate power buyers are increasingly prioritising the purchase of renewably generated electricity over that generated from fossil fuels.

. . . . . . . . . . .

Technology

Tim Scholefield, chairman, Allianz Technology – 8 August 2024

The shorter-term outlook for the technology sector is, as always, difficult to predict with any great precision and we can safely assume that monetary policy, geopolitics and election outcomes will be significant determinants of market direction over the next six to twelve months. While it is the case that inflation is finally within or approaching central bank targets, and hence that there are reasonable grounds for anticipating that monetary conditions will ease over the next twelve months, there is the potential for disappointment over the timing and magnitude of interest rate reductions. The valuation of ‘growth’ sectors such as technology is particularly sensitive to changes in interest rate expectations which in turn gives rise to a risk of heightened near term volatility. Nevertheless, we remain excited by the technology sector’s long-term potential and confident that secular themes such as the development of AI, cyber security and the continued move from legacy IT infrastructure to the cloud will ultimately reward patient investors with a focus on the mid- and large-cap segments of the technology sector.

The macro outlook appears to be more constructive for those borrowers seeking refinance as 3 and 5 year yields have fallen due to market expectations on the likely timings and trajectory of interest rates. This is helpful although set against this we expect credit spreads to widen so all in funding costs could remain neutral.

. . . . . . . . . . .

Debt

Rhys Davies and Edward Craven, Invesco Bond Income Plus, 15 August 2024

After a strong rally to end 2023, bonds, broadly defined, delivered near-zero returns in the first half of this year. Credit markets performed relatively well (delivering income and a modest degree of capital return), while government bonds struggled (with income more than offset by price falls).

Looking first at the parts of the market most represented in our portfolio, high yield corporate bonds (ICE BofA European Currency High Yield Index, GBP-hedged) returned 3.9% and subordinated bank capital instruments (ICE BofA Contingent Capital Index) returned 5.3%. Investment grade corporate bonds (ICE BofA Sterling Corporate Index) returned -0.1% and gilts (ICE BofA UK Gilt Index) -2.9%.

Market yields for high yield and subordinated banks did not change much but spreads over government bonds tightened (from 411bps to 363bps and from 378bps to 327bps respectively).

The better performance for credit-risk assets reflected changing investor perceptions of the key macroeconomic drivers – growth and inflation. Data on economic activity has generally been a bit stronger than predicted, increasing confidence in corporate earnings and the consequent ability of companies to repay. Inflation data was less encouraging, particularly in the US in the first quarter. Along with a more hawkish tone from the major central banks, this meant that expectations for interest rate cuts have been significantly pared back, notwithstanding some better data in Q2 and actual rate cuts from the ECB and several other G-10 central banks. In January, the market was pricing in seven 0.25% rate cuts from the Bank of England in 2024. By the end of June, this had reduced to less than two.

As credit markets have rallied, supply has been stronger. High yield corporate issuance (for European currencies) was a gross €65 billion in the first half of 2024, already above the €58 billion and €32 billion totals for 2023 and 2022. On the whole, there have been plenty of buyers to absorb these new bonds. In many cases, deal terms have tightened to take advantage of the strength of demand.

Total levels of yield in the corporate bond markets remain quite attractive and we think there are still good opportunities to buy bonds which will provide good levels of income. However, we are conscious that yields have come down and that much of the yield is coming from interest rates, not credit spread.

Partly because of the importance of interest rates in yields, the markets have been very sensitive to inflation and growth data. We expect this to continue.

Inflation data has been bumpy, but we think it is on a downward path to levels consistent with the targets of the central banks. There have already been some rate cuts and we think there will be room for more over the rest of the year. We are comfortable holding more interest rate risk. Current yields are satisfactory and there is potential for capital return as interest rate expectations evolve.

Although interest rates should fall from here, we do not expect that they will reach the low levels seen before 2022. At the same time, there is potential for economic activity to weaken. This poses a challenge to corporates, who could face a difficult re-financing environment along with weaker earnings. The balance sheets of more leveraged or weaker businesses may come under strain in these conditions.

We have reduced our exposure to credit risk in this environment while also maintaining liquidity so that we can take advantage of opportunities that may arise in such weaker market conditions.

. . . . . . . . . . .

Managers, RM Infrastructure Income, 19 August 2024

Government bond yields have traded in a range during the Period and overall have remained largely unchanged. We have seen the first interest rate cut by the Bank of England during July and it is highly likely that base rates will be lowered further from the current level of 5.00% during the second half of the year. This is a supportive backdrop for borrowers when it comes to facilitating refinancing as the overall cost, affordability and the availability of credit for those portfolio borrowers who are seeking a refinance.

Credit spreads hae been largely steady with the Markit iTraxx Europe Crossover index opening at 310 and closing the Period marginaly wider at around 320. Our base case forecasts are that there will be credit weakness to follow through in the second half of the year, specifically as we see stress within the Commercial Real Estate “CRE” market. Despite Bank of England moving rates on a lower trajectory, the current level of base rates are still putting extreme pressure on CRE loan metrics for historic transactions, especially those originated during the post Covid-19 period.

. . . . . . . . . . .

Private Equity

Managers, Pantheon International – 1 August 2024

As a result of the current macroeconomic environment, many of our managers are holding on to their companies for longer than usual while they wait for the right time to commence a sales process. Indications are that the average holding period has increased from around five years in 2019 to around six years in 20231. More generally, the slowdown in M&A transactions over the past two years means that private equity deal flow was lower in 2023, compared to 2022 and 2021, although add-on acquisitions continued apace as private equity managers executed on their “buy-and-build” strategies, snapping up smaller, synergistic companies at attractive valuations to bolt on to their platform companies.

We are hopeful that we will start to see increased deal activity as more certainty returns to the inflation and interest rate environment, and the opening of the initial public offering (IPO) market accelerates. Although PIP is not dependent on its portfolio companies going public for exits, healthy IPO markets boost overall market confidence and support both private equity and strategic/ trade buyer activity. Both we and our managers are unable to predict the timing of a resurgent M&A market, but there are very early signs that the tide may be starting to turn, which means that several of PIP’s portfolio companies, which are already being prepared for exit, will be ready for sale as the outlook improves. Indeed, deal activity does seem to be picking up – for example recently released data shows that new transactions in Europe increased markedly in Q2 2024, with newly recorded deals increasing by 5% by number, and by 73% by aggregate deal value2.

In addition to more confidence returning to the overall M&A market, there are record levels of dry powder (c.US$1.5tn3) in our industry, which is capital that has been raised and is available to invest but has not yet been deployed, however a majority of this is concentrated among the largest buyout funds. This capital sitting above us at the mega end of the market is positive for PIP as these managers can, and often do, buy our smaller portfolio companies to take them onto their next stage of development. The most recent European deal data appears to point to greater activity by the large and mega buyout focused managers, who are under pressure to deploy capital.

. . . . . . . . . . .

Managers, Partner Group – 22 August 2024

The transaction environment for global buyout is showing signs of gradual improvement in 2024. On an annualized basis, the value of transactions returned to 2019/2020 levels. This comes as accessibility to financing is improving with, in particular, the reopening of the bank-led syndicated

loan market. As a result, while the Federal Reserve has not yet started cutting rates, the renewed competition with and amongst private credit lenders has driven financing spreads lower. Once this is complemented by Federal Reserve rate cuts later this year, the financing backdrop should further improve

This, alongside, a continued gradual reopening of the IPO market should enable a further narrowing between buyers’ and sellers’ price expectations. Given the high levels of dry powder and unrealized value, we therefore expect moderate improvement in transaction activity over the remainder of 2024. Uncertainty remains, however, with geopolitical events still a key risk. For this reason, we maintain our disciplined underwriting for prospective investments while reiterating our strong conviction in our transformational and hands-on approach for existing investments.

. . . . . . . . . . .

Hamish Mair, manager, CT Private Equity Trust – 29 August 2024

The private equity market in most of our significant markets is showing signs of improvement. This is clearly the case in the UK where this has been underlined by our recent significant exits which have been completed at or above target valuations and within the expected timescales. Some of the Northern European geographies, such as Germany and the Nordics, are more cautious, but parts of Southern Europe are more overtly optimistic.

For the last eighteen months the private equity market has been adjusting to a different economic environment with higher prevailing interest rates. This has resulted in a slowdown in M&A activity with some connected pricing and valuation multiple adjustments. The fundamentals of most of our investee companies have continued to make progress with revenue and profits growth continuing. As the underlying growth of the companies offsets the adjustment in valuation multiples, overall asset values will once again move back towards the longer term positive trend. A key determinant in this will be business confidence which is difficult to measure in real time and is susceptible to external global events. Despite this, from our recent discussions with our investment partners, we can identify an improving trend and we expect that this will, in due course, lead to further good growth in shareholder value in the remainder of 2024 and beyond.

. . . . . . . . . . .

Property

Colin Godfrey, chief executive of Tritax Big Box REIT:

The first half of 2024 saw 11.7 million sq ft of take up across the UK, up from 10.0 million sq ft in H1 2023. Leasing deals continue to take time to complete, but second quarter activity (7.3 million sq ft of take up across 25 deals) was particularly strong with several large commitments closing.

Market activity remains broad-based across both building size and occupier type. Occupier demand is diverse with retailers (both online and omnichannel) and 3PLs (third-party logistics operators) active in the market. Manufacturing demand remains prominent, accounting for 25% of activity in the last 12-months.

Alongside the increase in take up, both space-under-offer and requirements (which reflect potential near-term demand) remain healthy. CBRE reported 12.1 million sq ft under offer at Q2 2024, up from 11.1 million at Q4 2023. Savills’ requirements index has increased with an uptick in enquiries for large units. Meanwhile, our own occupier enquiry hub remains close to record levels with a mix of interest by size, sector and location. Companies continue to look to evolve their supply chain networks. In doing so, they are generating new and additional demand for logistics buildings.

In addition to the structural drivers (growth of ecommerce, supply chain resilience and optimisation, and ESG) that continue to support our sector, the improving macroeconomic backdrop is expected to lead to increased levels of take up going forward. The new government’s ambition is to kickstart economic growth and focus on housebuilding. This has the potential to positively impact us as firstly, logistics will be an important enabler of UKs economic growth and secondly, with Savills research suggesting new housing creates additional demand for logistics space, and the UK government aiming to deliver 1.5 million new homes over the next five years, we believe this could further support demand in the sector.

Market vacancy, which reflects ready-to-occupy space, stood at 5.6% at the end of the period, up from 5.1% at Q4 2023. Vacancy comprises both second-hand space and developments that complete on a speculative basis. Here, the trend remains positive with speculative space under construction declining further across H1 2024 and new speculative starts remaining well below 2021/2022 levels.

Total space under construction, which also includes build-to-suit projects, stood at 18.9 million sq ft at H1 2024, down from 21.4 million sq ft at Q4 2023.

Prime headline rents increased across the period but at a lower rate than in recent years. MSCI UK Distribution Warehouse ERVs increased by 2.0% in H1 2024 (H1 2023: 4.0%).

CBRE prime market yields remained flat across the period at 5.25%, but Savills have in recent weeks moved their prime yield in by 25bps to 5.0%. H1 2024 transaction volumes totalled £2.5bn (H1 2023: £4.1bn). Market activity picked up in Q2 2024 following a quiet first quarter, but there has been a general lack of stock available to purchase and an absence of large or portfolio deals. Investor conviction in the sector remains high with surveys continuing to highlight logistics as a favoured destination for capital. Existing owners are, however, choosing to hold onto logistics assets given their ongoing conviction in the sector and attractive returns available following a period of repricing.

. . . . . . . . . . .

Duncan Garrood, chief executive of Empiric Student Property:

Student accommodation continues to be highly sought after by both existing and new investors, with UK purpose-built student accommodation (PBSA) specifically attracting interest from global capital interest. Relative to 2023, investment in PBSA has bounced back in the first half of the year, with CBRE reporting £2.1bn of investment into the sector in 2024 to date, three times higher than the same period in 2023. The abolition of Multiple Dwellings Relief (MDR) came into effect on 1 June 2024 and has resulted in pricing for some assets being impacted by up to 4.0% by virtue of increased stamp duty charges. This will likely impact pricing of transactions into the second half of 2024.

The supply of new beds is forecast to increase in 2024, with best estimates indicating the delivery of circa 12,500 beds on average over the next four years. In the medium term, new supply remains heavily constrained with construction cost viability remaining challenging in all but the strongest markets, impacted by land value, planning, enhanced building safety standards and higher debt costs. The constrained supply is also being compounded by the falling number of Houses of Multiple Occupation (HMOs) with a range of factors forcing private landlords from the market. Since 2016, the stock of private rental properties has decreased by almost 10%, with the UK’s HMO supply decreasing by 146,000 beds over the past four years.

Demand for UK higher education is normalising post pandemic but remains very strong. UCAS, which represents around 90% of total applications, recently published application data to June 2024 in respect of the 2024/25 academic year. Applications for higher tariff institutions, to which we are primarily aligned, have continued to grow, increasing 0.4% year-on-year. Lower tariff institutions have experienced a further decline in applications, dropping 3.7%, further demonstrating a continued flight to quality.

International applicants have fallen by 1.9%, with the largest declines seen in applicants from Nigeria and India, a large constituent of this decline arising from dependant applications. This follows a tightening of rules for dependant family visas for masters students, a change which has not impacted us due to the single occupancy nature of the majority of our sites. Applications from China, the USA, Canada and the UAE continued to report modest increases. Non-EU international applicants remain 40% higher than their pre-pandemic level.

Domestically, applications have reduced by 1.6% compared to 2023, driven by a 4.9% decline in mature student applications. Applications from 18-year-olds are up 0.6% and are forecast to continue growing until 2030 due to the increasing size of the qualifying cohort.

The UK remains within the top four most-favoured international destinations for students originating from the USA, China and India and continues to perform well on relative affordability when compared with many other sought-after international destinations for higher education. Demographically, to date, we have experienced an increase in demand from international students which does demonstrate the resilience of the UK’s international student market.

These strong trends contributed to sector wide rental growth of 8% for the 2023/24 academic year, with Glasgow experiencing the strongest rental growth of all the major markets at 19%. For the 2024/25 academic year, expectations for continued rental growth, in addition to anticipated cuts to the base rate of interest, have held prime regional yields stable across the sector during the first half of 2024.

. . . . . . . . . . .

Richard Shepherd-Cross, investment manager of Custodian Property Income REIT:

After a period of stabilisation, the trajectory of valuations appears to be turning positive and the company, together with its peers, has a more optimistic outlook.

Investors in listed real estate have reason to be optimistic with falling vacancy rates, rental growth and discounted share prices creating generous dividend yields and room for share price recovery. Along with the recent cut in interest rates which we expect to support valuations further, we believe this could be a very opportune time for investors to re-engage with real estate.

LSH’s recent UK Investment Transactions report recorded a 12% increase in UK transaction volumes for the six months to 30 June 2024, albeit this is still below the five-year average. CBRE’s UK Mid-Year Market Outlook reported stronger signs of a turning point for real estate noting inflation is on target and cost of living pressures have moderated, creating space for consumer demand to rebound. Overall, according to this report, the economic backdrop is positive for both occupiers and investors.

. . . . . . . . . . .

Paul Williams, chief executive of Derwent London:

The UK economic environment continued to improve through the first half of the year (H1) having begun to recover late last year. With inflation now in line with the Bank of England’s 2% target following a substantial reduction from its peak of 11% in October 2022, the UK base rate was cut by 25 basis points in August to 5.0%, and there are further cuts on the horizon.

The five-year swap rate has responded favourably and is now 3.6%. Further declines in the cost of debt and improving availability should be expected to encourage a recovery in investment activity. At £1.9bn, transaction volumes in H1 were 65% below the 10-year H1 average. However, since the start of H2, enquiry levels are picking up with CBRE reporting £19.2bn of global equity targeting London offices.

In February, we highlighted with our 2023 full year results that “valuations are now approaching this cycle’s lows”. In H1, the pace of MSCI capital value declines slowed to 2.1%. Looking forward we expect a recovery in capital values, principally driven by rental growth.

The central London office market has strengthened further with the key occupier themes continuing to be quality, location and amenity. At the same time, existing supply that satisfies these requirements is limited and the market development pipeline is constrained, driving rental growth for the best space.

The imbalance between supply and demand across the London office market remains pronounced. Grade A vacancy is 1.8% and there are only 7.3m sq ft of speculative development completions due by the end of 2027. While leasing transactions are taking longer, the increase in space under offer suggests the lower take-up in H1 should be temporary.

Overall vacancy has levelled off at 8.3%, with the West End at 4.5% and the City at 10.8%. According to CBRE, lower quality, second-hand space comprises over two-thirds of supply. The Grade A vacancy rate in the West End is only 1.2% and in the City is 2.1%. The central London development pipeline is constrained, with 12.6m sq ft of space under construction and due to complete by 2027. Of this, 42%, or 5.3m sq ft, is pre-let or under offer, rising to 54% for projects due to complete in H2 2024. In line with longer-term trends, pre-letting levels in the West End (23%) are below the City (62%).

Take-up in the second quarter, which was 20% higher than Q1, benefited from some large financial pre-lets in the City, and since the start of H2 the West End has seen some of the space under offer convert with the completion of several substantial pre-lets, including BDO. Occupier enquiry levels remain high across a broad range of sectors backed up by active demand rising 14% through H1 to 11.2m sq ft, 56% above the five-year average.

Liquidity across the market has been focused on smaller lot sizes where there is less of a requirement for leverage. With £1.9bn of transactions completing in H1, below the long-term average, the average lot size was only £29m. The availability of debt has begun to improve in recent months. The first cut in base rates saw the five-year swap rate fall back to 3.6%. In a global context, London continues to enjoy a reputation as a safe haven. As a result, sentiment is improving and a rising number of investors are switching from a ‘wait and see’ approach to being more acquisitive.

Prime yields were unchanged in H1. At 4.0%, West End yields have increased 75bp compared to June 2022 while City yields have moved out 200bp to 5.75%.

. . . . . . . . . . .

Fredrik Widlund, chief executive of CLS Holdings:

There are signs of improvements in the real estate investment market and leasing activity continues to be positive as occupiers are increasingly prepared to commit to the right locations and buildings. The bifurcation seen in the last few years has carried on with stronger demand for centrally located and/or higher quality offices, while more peripheral office locations or lower quality buildings continued to decline.

The investment market improved in the first half of 2024, albeit from historically low numbers, but an increase compared to the same period last year and certainly the second quarter of 2024 was more active with buyers slowly returning to the market. As we have seen in past cycles, the UK entered the downturn earlier and is now ahead in its recovery while Germany and France are a bit further away.

. . . . . . . . . . .

IMPORTANT INFORMATION

This note was prepared by Marten & Co (which is authorised and regulated by the Financial Conduct Authority).

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it. Marten & Co is not authorised to give advice to retail clients. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

Marten & Co may have or may be seeking a contractual relationship with any of the securities mentioned within the note for activities including the provision of sponsored research, investor access or fundraising services.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.