Hi Fidelity!

AVI Japan Opportunity (AJOT) has published proposals for a combination with Fidelity Japan Trust (FJV) that would improve liquidity in AJOT’s shares, lower its ongoing charges ratio, and give the manager greater resources to unlock value in the companies it invests in.

For FJV shareholders the deal offers the chance to switch into a much better-performing trust, with improved discount control. While a cash exit is available as part of the proposal, AJOT’s also offers shareholders the option to redeem shares each year – the next opportunity is due soon – so investors will continue to have the opportunity to exit easily in the future, and it seems reasonable to us that the cash option would be undersubscribed.

In addition, AJOT has no shortage of potential investments, and the managers see plenty of upside from the existing portfolio.

Unlocking value in Japanese smaller companies

AJOT aims to achieve capital growth in excess of the MSCI Japan Small Cap Index by investing in a concentrated portfolio of over-capitalised small-cap Japanese equities. Asset Value Investors (AVI) leverages its four decades of experience investing in asset-backed companies to engage with company management and help to unlock value in this under-researched area of the market.

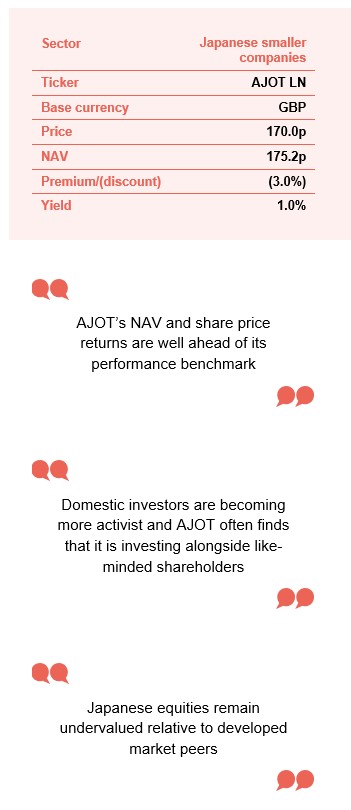

At a glance

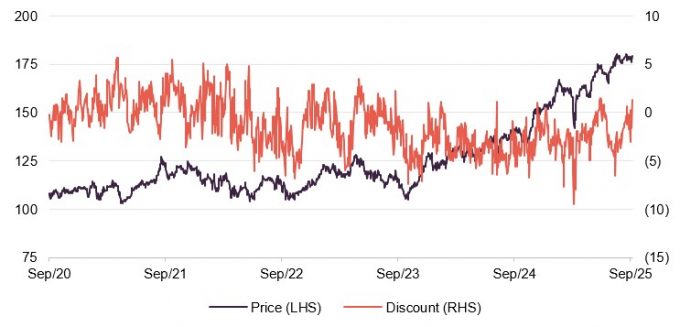

Share price and discount

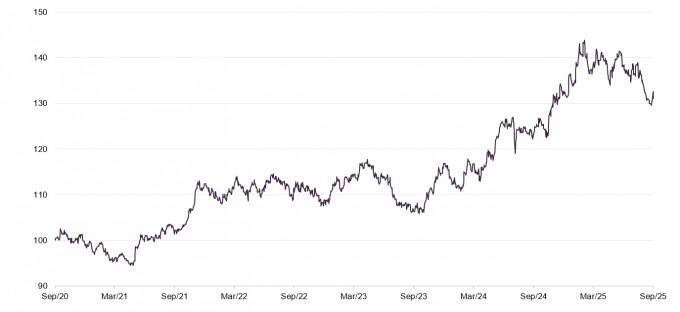

Over the 12 months ended 30 September 2025, AJOT’s shares traded between a 1.5% premium and a 9.5% discount to net asset value (NAV). The average discount over the period was 2.6%. By contrast, the range for FJV was 1.6% premium to 18.6% discount and an average of 9.9%.

At 22 October 2025, AJOT was trading at a 3% discount to NAV.

Time period 30 September 2020 to 22 October 2025

Source: Bloomberg, Marten & Co

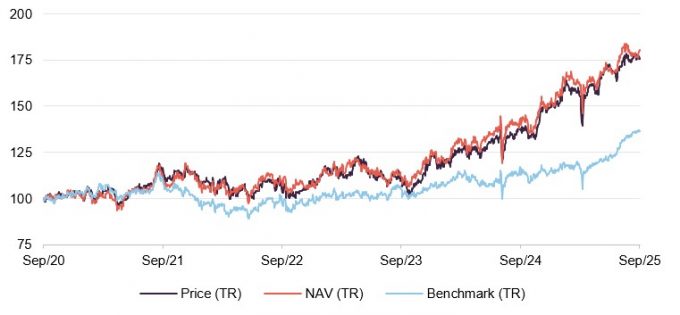

Performance over five years

Although the short-term periods have been more difficult, AJOT’s NAV and share price returns are still well ahead of its performance benchmark, the MSCI Japan Small Cap index, over most time periods.

The nature of AJOT’s investment approach means that returns are driven by the manager’s stock selection and the success of its campaigns to unlock value.

Time period 30 September 2020 to 30 September 2025

Source: Bloomberg, Marten & Co

| 12 months ended | Share price total return (%) | NAV total return (%) | MSCI Japan Small Cap TR (%) | MSCI AC World total return (%) |

|---|---|---|---|---|

| 30/09/2021 | 16.8 | 12.0 | 10.2 | 22.8 |

| 30/09/2022 | (11.5) | (4.3) | (12.0) | (3.6) |

| 30/09/2023 | 7.7 | 4.1 | 8.1 | 10.7 |

| 30/09/2024 | 22.9 | 26.3 | 9.0 | 20.5 |

| 30/09/2025 | 29.5 | 27.3 | 19.7 | 17.3 |

Fund profile

More information is available at the fund’s website www.ajot.co.uk

AJOT is an investor in Japanese companies. Its focus is on good-quality small- and mid-cap listed companies that have a large portion of their market capitalisation in cash, listed securities or other realisable assets (assets that are easy to convert into cash without significantly impacting their value). AJOT’s manager seeks to engage proactively with these companies to unlock their value potential. Further detail on AJOT’s investment philosophy and approach was included in our last note on the trust, a link to which is provided on page 14.

AJOT’s AIFM and investment manager is Asset Value Investors Limited (AVI). The lead manager working on AJOT’s portfolio is Joe Bauernfreund, one of a seven-strong team focused on Japan, one of whom is based permanently in Japan, and the majority of whom are Japanese-speakers. There is a plan to continue to grow the team in the near future.

AVI and its employees are aligned with shareholders

AVI was established in 1985 to manage what is now AVI Global Trust (AGT) and has total assets under management of about £2bn. AVI began investing in Japan over four decades ago and AJOT was launched in October 2018 to focus on the opportunities presented by that market. At the end of September 2025, AVI and its employees owned over 3.3m shares in AJOT (suggesting a good alignment of interests between the manager and other shareholders).

AJOT compares its performance to the MSCI Japan Small Cap Total Return Index, expressed in sterling terms. The index does not influence AJOT’s portfolio construction. AJOT has a very high active share relative to the performance benchmark.

The merger

S110 combination with FJV, 50% cash exit at 1% discount for FJV shareholders who want it

On 12 August 2025, AJOT announced that it had entered into non-binding heads of terms (a preliminary agreement setting out the main commercial points of a proposed deal) with the board of Fidelity Japan Trust (FJV) in respect of a proposed combination of the two trusts’ assets. The structure of the deal involves a s110 reconstruction and members’ voluntary winding up of FJV (a mechanism that allows investment companies to merge by liquidating one and transferring its assets to the other in return for shares or cash). Under the proposals, new AJOT shares will be issued to FJV shareholders on the basis of the ratio of the formula asset values (NAV less costs) of the two trusts. A cash exit facility is available for FJV shareholders who want it, priced at a 1% discount to NAV, and capped at 50% of FJV’s issued share capital.

Costs offset against uplift from providing cash exit at a discount and AVI contribution

The costs of the transaction that are attributable to the FJV rollover into AJOT shares will be capped at £1m. An amount equivalent to the cash exit charge – that is, the cash that is equivalent to the 1% discount to NAV that is applied to shareholders who opt for the cash exit – will be set against costs. 1% of half of FJV’s net assets at the time of publication would be about £1.3m. Depending on the size of the rollover (and hence the cost contribution from this source), AVI will also make a contribution, capped at £1m, towards the costs of the deal.

Shareholders of both trusts will get the chance to vote on the deal at meetings to be held on 6 November 2025 (AJOT), and 7 November 2025 and 27 November (FJV).

The AVI team has set out the benefits of investing with AJOT in a video, which can be viewed here. As we discuss below, there are a number of reasons why we think FJV and AJOT shareholders should be supportive of the deal.

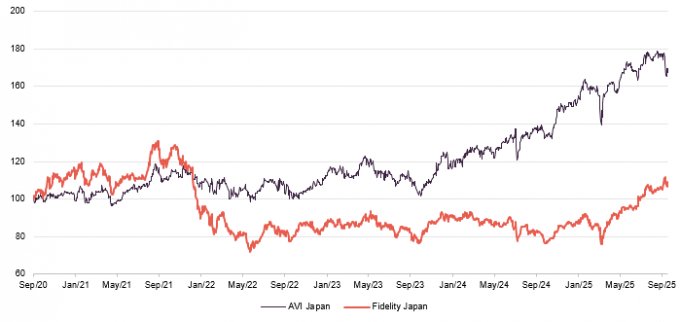

Track record and prospects

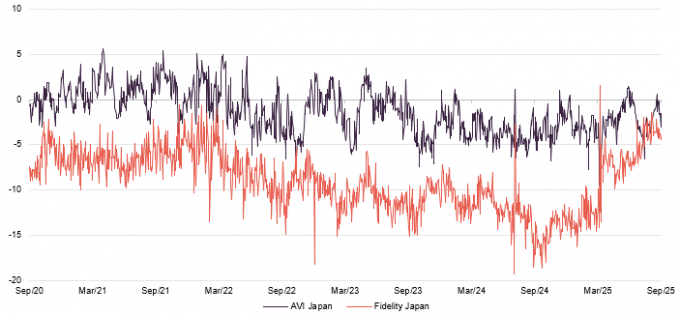

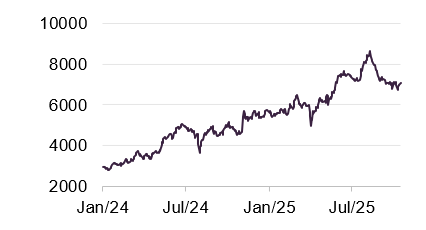

Figure 1: AJOT and FJV share price total returns over five years ended 30 September 2025

Source: Bloomberg, Marten & Co

The gap between AJOT and FJV’s returns to shareholders over the past five years is significant. Had investors in FJV held AJOT instead, they would have been more than 50% better off.

However, this begs the question, is AJOT’s run of good performance sustainable?

No shortage of potential investments; Cash from FJV rollover could be redeployed within 10 weeks

AJOT’s managers would argue that there is no shortage of potential investments for the trust, and they are increasingly pushing on an open door when it comes to engaging with companies with the aim of unlocking value and improving returns. The manager estimates that the extra resources that a merger with FJV would bring could be deployed within 10 weeks and would allow AJOT to take larger and more influential positions in some target companies.

The opportunity persists, in part, because the pool of stocks in the investment universe is deep (there are around 4,000 listed companies in Japan) and these stocks often have little or no analyst coverage, so mispricing can persist longer than it otherwise would.

Attitudes towards corporate governance are shifting

Initiatives that the government, regulators, and the stock exchange have taken to improve corporate governance are bearing fruit. The culture is shifting, and companies are recognising that change is needed. Buybacks and dividends are increasingly prevalent. Domestic investors are becoming more activist and AJOT often finds that it is investing alongside like-minded shareholders.

Japanese equities are undervalued relative to peers

Japanese equities remain undervalued relative to developed market peers. Foreign investors have an underweight exposure to what is, based on MSCI index weightings, the second-largest market in the world.

The Japanese economy is changing too in the face of stubborn inflation and rising interest rates (a reversal of Japan’s historic low-inflation, low-rate environment). Domestic investors, who have long sat on sizeable cash piles, now have a good incentive to switch some of that into stocks. Wages are rising, which could in time boost consumer spending. The tourism sector is thriving as well.

Trump’s tariff policies did cause some setback in the market earlier in the year, but a trade deal was agreed in the summer.

The choice of Sanae Takaichi as the new leader of the LDP, the senior party in Japan’s governing coalition, was well received by the market, albeit the subsequent collapse of that coalition provided a temporary hit to confidence. Now the LDP has built a new coalition without the more “pacifist” Komeito, that should be supportive to Japan’s resurgent defence sector.

It feels to us as though Japan is an attractive place to invest, and AJOT has opportunities to continue to add value for its investors.

Tighter discount

The AJOT board recognises that it is in the interests of shareholders to maintain a mid-market price for its ordinary shares that is as close as possible to NAV. The board monitors the share price discount to NAV over rolling four-month periods and will buy back stock if the average discount exceeds 5%. The discount should also be limited by the annual exit opportunity (see below).

Figure 2: AJOT and FJV premium/discount for the five years to 30 September 2025

Source: Bloomberg, Marten & Co

Over the 12 months ended 30 September 2025, AJOT’s shares traded between a 1.5% premium and a 9.5% discount to NAV. The average discount over the period was 2.6%. By contrast, the range for FJV was 1.6% premium to 18.6% discount and an average of 9.9%.

The discounts on both trusts have been volatile – largely as a consequence of macroeconomic events such as “Liberation Day”. However, AJOT has done a good job of keeping its discount in check, whereas FJV’s only really started to narrow in April 2025, after AJOT expressed an interest in merging with it and then it failed its continuation vote (a vote by shareholders on whether a trust should continue to operate in its current form).

At 22 October 2025, AJOT was trading at a 3% discount to NAV.

Scale benefits

Even if the cash option is taken up in full, AJOT is expected to end up with assets of about £360m (based on assumptions made around the time of the announcement), making it roughly 50% bigger than it is today. All things being equal, that should help improve the liquidity in AJOT’s shares, as well as lowering the ongoing charges ratio (as discussed below).

Lower fees for AJOT shareholders

AJOT’s management fee is currently 1% of the lower of market capitalisation and net assets. This will shift to a new tiered fee – still based on the lower of market capitalisation and net assets – but where the fee on the first £300m will be 1.0%, 0.95% on the next £50m, and on assets above £350m, 0.90%. AVI will continue to invest a quarter of its fees back into AJOT shares.

The AJOT board estimates that the ongoing charges ratio post the deal will be 1.25% on a normalised basis.

100% exit opportunity available

AJOT has an unlimited life; however, shareholders have a regular opportunity to exit the company at a price close to NAV. The most recent opportunity was announced in October 2024 and took the form of a tender offer for 100% of shares in issue at NAV (after costs associated with providing the tender) less a 2% discount. 3,637,759 shares were tendered at 152.37p per share. These shares were repurchased and cancelled.

In 2024, the board amended the 100% exit opportunity schedule, increasing the frequency from biennially to annually. Details of the next opportunity will be announced soon, and it should be available within the current quarter. We think that this part of AJOT’s structure gives greater comfort for FJV shareholders considering whether to take cash now or rollover into AJOT shares.

Asset allocation

At the end of September 2025, AJOT’s gearing (borrowing) was 7.2%, marginally higher than it had been seven months earlier. The gearing came via JPY6.6bn of drawings on a revolving credit facility that comes at a cost of TONAR+1.55% (TONAR is the Tokyo Overnight Average Rate).

Reflecting the manager’s high-conviction approach, on 30 September 2025, AJOT had 21 holdings, four fewer than at the end of February 2025.

The average stock in the portfolio is valued on just 8.8x EV/EBIT (enterprise value divided by earnings before Interest and tax: a valuation metric) and has net cash as a percentage of market cap of 12.8%. Based on the manager’s assessments, over 44% of the average stock’s market cap was accounted for by net cash, investment securities and stakes in other companies that were not needed for the business.

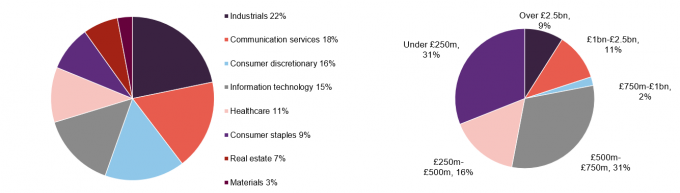

The split by sector reflects AVI’s stock selection decisions. Compared to when we last published (using data as at 28 February 2025) the exposure to consumer discretionary has fallen sharply (from 33% to 16%) and exposure to communication services and consumer staples has risen (by nine and seven percentage points, respectively). The split by market cap indicates a continued shift towards smaller companies, as flagged in previous notes; although the managers have also taken advantage of opportunities amongst some companies towards the top end of AJOT’s target range.

Figure 3: AJOT sector breakdown as at 30 September 2025

Figure 4: AJOT portfolio split by market cap as at 30 September 2025

Source: AVI Japan Opportunity Trust

Source: AVI Japan Opportunity Trust

10 largest holdings

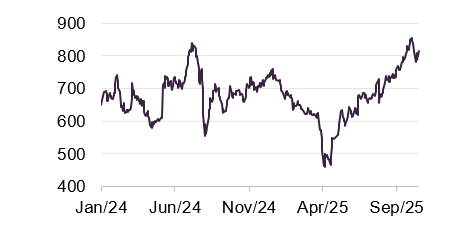

Since we last published, using data as at end February 2025, four positions – Beenos, TSI Holdings, Tecnos Japan, and Konishi – have exited the top 10, to be replaced by Wacom, Rohto Pharmaceutical, Mitsubishi Logistics, and Broadmedia.

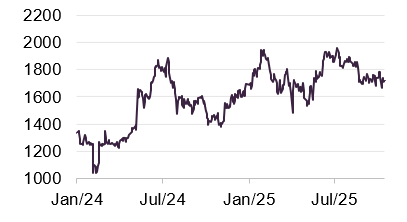

Figure 5: TSI Holdings (JPY)

Source: Bloomberg

As discussed in our last note, Beenos was bid for and AJOT exited its position in May 2025, crystallising a 127% profit for the trust, which was achieved in less than 18 months. TSI Holdings was sold to a 16% share buy back in July, crystallising a return on investment for AJOT of 92%. The managers had been pleased to see the business sell surplus real estate earlier in the year (triggering the big spike in the share price that is evident in Figure 5). TSI then made a JPY28.3bn acquisition that absorbed much of its cash pile.

Konishi was another stock that was sold to a buyback during the summer. It had been held by AJOT since the inception of the trust and was a successful investment, making a 74% profit for AJOT.

Tecnos Japan is an IT services company that is benefitting from the increasing digitalisation of businesses in Japan. In February, Ant Capital Partners offered a 39% premium to the prevailing share price to acquire AJOT’s stake. In total, AJOT made a 61% profit on its investment.

Figure 6: 10 largest holdings at 30 September 2025

| Holding | Industry | AVI ownership (%)1 | EV/EBIT(x)1 | NFV as % of market cap1 | ROI in JPY(%)1 | Percentage of NAV 30/09/25 | Percentage of NAV 28/02/25 | Change(%) |

|---|---|---|---|---|---|---|---|---|

| Raito Kogyo | Construction groundworks | 4.7 | 7.1 | 33 | 34.5 | 10.9 | 4.9 | 6.0 |

| Wacom | Digital pens | 12.9 | 7.5 | 12 | 12.9 | 10.3 | ||

| Eiken Chemical | Diagnostics | 6.1 | 22.6 | 13 | 36.9 | 9.9 | 8.1 | 1.8 |

| Rohto Pharmaceutical | Pharmaceuticals | 2.8 | 11.3 | 11 | 5.5 | 9.8 | ||

| Mitsubishi Logistics | Logistics | 2.4 | n/a | 183 | 4.0 | 8.1 | ||

| Atsugi | Apparel, stockings | 22.1 | n/a | 112 | 23.0 | 7.8 | 5.9 | 1.8 |

| Kurabo Industries | Conglomerate | 4.8 | 4.9 | 62 | 74.2 | 7.8 | 9.5 | (1.7) |

| Aoyama Zaisan Networks | Wealth management | 8.0 | 11.3 | 11 | 37.2 | 7.3 | 7.3 | – |

| SharingTechnology | Service matching platform | 14.5 | 12.5 | 12 | 28.7 | 7.3 | 6.2 | 1.1 |

| Broadmedia | Online education | 29.1 | 10.9 | 40 | 8.0 | 6.3 | ||

| Total | 9.02 | 463 | 85.5 |

Source: AVI Japan Opportunity Trust. Note 1) data in these columns is as at 31 August 2025. Note 2) for the whole portfolio the figure was 8.8x as at 30 September 2025. Note 3) for the whole portfolio the figure was 44.1% as at 30 September 2025.

Wacom

Figure 7: Wacom (JPY)

Source: Bloomberg

Wacom (investors.wacom.com) was at one time AJOT’s largest holding (see our February 2022 note, link on page 14). It is a leading manufacturer of digital tablets and pens.

AVI has been engaging with Wacom’s board for some time. In May this year, it launched a public campaign – Draw Wacom’s Future – which included setting out some recommendations for turning around Wacom’s branded business, enhancing governance, optimising Wacom’s capital allocation policy, and improving investor relations. AVI also put forward a number of resolutions at Wacom’s annual general meeting (AGM). These called for:

- the appointment of one outside director with capital markets background;

- the establishment of a Transformation Plan Supervisory Committee;

- an amendment to the Articles of Incorporation regarding the handling of acquisition proposals based on the ‘Guidelines for Corporate Takeovers’ by the Ministry of Economy, Trade and Industry;

- granting general meetings of shareholders the authority to determine dividends of surplus earnings;

- conducting a JPY5bn share buy-back in FY2026; and

- defining that total shareholder return (TSR) shall be used as an indicator for the stock-based compensation for internal directors.

A 100+ page presentation on a dedicated website sets out AVI’s thinking on this. You can read this here.

In September, another activist declared a stake in the company, which may help AVI achieve its agenda.

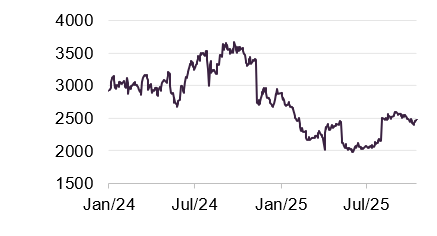

Rohto Pharmaceutical

Figure 8: Rohto Pharmaceutical (JPY)

Source: Bloomberg

We covered Rohto Pharmaceutical (rohto.co.jp) in our last note, observing that the share price fall evident in Figure 8 had made it one of the largest detractors to AJOT’s performance over the second half of 2024. In April 2025, AVI launched another of its public campaigns – Awakening Rohto – in which it called for the company to focus on its core business rather than allocating resources to its unsuccessful regenerative medicine business, and to engage with shareholders more constructively to comply with the Tokyo Stock Exchange’s request for management that is conscious of the cost of capital and stock price.

Again, AVI has prepared a detailed explanation of its stance, which you can read here.

In May, Rohto published its medium-to-long-term growth strategy, covering the period from 2025 to 2035, which included targets for sales growth and margins. This included an increase in its dividend payout ratio to at least 30% and a dividend on equity ratio of 3.5%.

Mitsubishi Logistics

Figure 9: Mitsubishi Logistics (JPY)

Source: Bloomberg

Mitsubishi Logistics (mitsubishi-logistics.co.jp) stood out in Figure 6 as the cheapest of AJOT’s current top 10 holdings, based on a comparison of its market cap and its net financial value. It is one of the major logistics distribution companies in Japan, and AVI thinks that the operational side of the business is well-run. It comes with some sizeable real estate that includes both the logistics and distribution warehouses from which it operates and a separate real estate investment portfolio.

The properties tend not to be revalued in the company’s accounts, so AVI has done a lot of work, with the aid of third-party valuers, to come up with its estimate of their true value. The upshot is that it believes that the real estate assets are worth almost twice the current share price.

Given that Japanese companies are being told that they should be trading above book value, and that there is another value-driven investor on the register, it seems likely that Mitsubishi Logistics will give serious consideration to monetising its surplus property portfolio.

Encouragingly, the company realised JPY11.5bn from the sale of cross-shareholdings earlier this year (a common feature of Japanese corporate structures), indicating that it is open to change.

Broadmedia

Figure 10: Broadmedia (JPY)

Source: Bloomberg

Broadmedia (broadmedia.co.jp) is primarily an online education business, although it does have some ancillary businesses, including a fishing channel. Broadmedia’s Renaissance High School Group offers courses in non-mainstream areas such as eSports, entertainment, and beauty.

AVI says that there are two other activist investors on Broadmedia’s share register. AVI would like to see Broadmedia rationalise its conglomerate structure to focus on education, which it thinks has great potential. Initial meetings with management have been positive.

Performance

Up-to-date information on AJOT and its peers is available on our website

Although the short-term periods have been more difficult, AJOT’s NAV and share price returns are still well ahead of its performance benchmark, the MSCI Japan Small Cap index, over most time periods.

Figure 11: Total return cumulative performance over various time periods to 30 September 2025

| 3 months(%) | 6 months(%) | 1 year (%) | 3 years(%) | 5 years(%) | |

|---|---|---|---|---|---|

| AVI Japan Opportunity share price | 2.6 | 14.1 | 29.5 | 71.4 | 77.1 |

| AVI Japan Opportunity NAV | 5.5 | 11.2 | 27.3 | 67.4 | 79.4 |

| Comparator benchmark | 11.5 | 17.8 | 19.7 | 41.2 | 36.9 |

Source: Bloomberg, Marten & Co

The nature of AJOT’s investment approach means that returns are driven by the manager’s stock selection and the success of its campaigns to unlock value. There will be periods where AJOT’s returns diverge meaningfully from the index, and therefore its performance is best considered over the long term.

Figure 12: AJOT NAV total return performance relative to MSCI Japan Small Cap index for the five years to 30 September 2025

Source: Bloomberg, Marten & Co

Performance attribution

AVI provided us with data on the leading contributors and detractors from AJOT’s returns over 2025 up to the end of August. Happily, the detractors had a relatively minimal influence on returns.

Figure 13: Leading contributors and detractors from AJOT returns 2025 year to end August

| Contribution (GBP %) | Share price return (%) | Contribution (GBP %) | Share price return (%) | |||

|---|---|---|---|---|---|---|

| Kurabo Industries | 3.57 | 33.0 | Aichi | (0.36) | (10.9) | |

| Raito Kogyo | 3.08 | 49.6 | Konishi | (0.30) | (4.6) | |

| TSI Holdings | 2.10 | 9.5 | Jade Group | (0.21) | (9.7) | |

| Tecnos Japan | 1.79 | 45.7 | SK Kaken | (0.16) | (6.8) | |

| SharingTechnology | 1.37 | 23.8 | Helios Techno | (0.11) | (13.1) |

Source: AVI Japan Opportunity Trust

Kurabo Industries

Figure 14: Kurabo Industries (JPY)

Source: Bloomberg

Kurabo Industries (kurabo.co.jp) was also the leading contributor to returns over the second half of 2024, which we discussed in our last note. It is a conglomerate that started life as a textile company and now has a presence in chemical products, advanced technology, food and services, and real estate. AVI was attracted by its strong core business and overcapitalised balance sheet (holding more cash or assets than is needed to run the business efficiently).

Whilst the share price has come back a bit from its peak, this might reflect the completion of a JPY6bn share buyback programme that it initiated in November 2024.

AVI was pleased to see the company announce in March that it would close its most unprofitable textile plant and then, in May, announce plans for a 4% dividend on equity target and a new JPY20bn share buyback.

Raito Kogyo

Figure 15: Raito Kogyo (JPY)

Source: Bloomberg

Raito Kogyo (raito.co.jp) is focused on the specialist construction sector, with core operations and large market shares in slope construction and ground improvement (accounting for about 70% of sales orders between them). Trading has been good, with results coming in ahead of market expectations.

AVI is asking the company to improve its capital efficiency (a measure of how effectively a company uses its financial resources to generate profits or revenue), corporate governance, and shareholder communication.

Previous publications

Readers interested in further information about AJOT may wish to read our previous notes listed below. You can read them by clicking on the links in Figure 15 or by visiting our website.

Figure 16: QuotedData’s previously published notes on AJOT

| Title | Note type | Date |

|---|---|---|

| Progress on a number of fronts | Initiation | 20 July 2021 |

| The tortoise triumphs | Update | 15 February 2022 |

| Maintaining its firepower | Annual overview | 21 October 2022 |

| Good governance, better returns | Update | 19 July 2023 |

| The sun has risen | Annual overview | 20 February 2024 |

| Pushing on an opening door | Update | 6 August 2024 |

| Reforms at a tipping point | Annual overview | 24 March 2025 |

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on AVI Japan Opportunity Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it. Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.