And now for something completely different

On 28 February 2025, BlackRock American Income (BRAI) announced a significant change. The company asked shareholders to approve a new investment objective and policy, announced a new enhanced dividend policy, reduced management fees, and offered shareholders a 20% tender at a 2% discount to NAV (after costs).

The proposals were approved by investors, with more than 99% of those voting giving their approval on 16 April 2025. The tender offer was undersubscribed, with 16.15% of BRAI’s shares validly tendered.

In its new form, the trust is following an investment approach that appears to be distinct from other investment companies listed in the UK, investing using a systematic active equity approach devised by BlackRock. This note explains BRAI’s new approach and the corporate structure that supports it. Historical performance data is included for reference in the charts on this page. The note focuses on BRAI’s returns since the strategy change.

Attractive income and growth from US value stocks, using a systematic active equity approach

BRAI aims to provide long-term capital growth, whilst paying an income of 1.5% of NAV per quarter, around 6% of NAV per annum. BRAI follows a systematic active equity approach that aims to provide outperformance of the Russell 1000 Value Index (the benchmark).

More information is available on the trust’s website

How does new BRAI differ from old BRAI?

- The portfolio’s focus on deriving income and capital growth from US value stocks remains unchanged. This focus on value stocks may provide diversification for portfolios that are otherwise concentrated in a small number of mega-cap US tech stocks.

- There has been a change to the method by which investments are selected, which is described in more detail below.

- The maximum active position in a stock is 1.5%. The number of stocks in the portfolio increased from about 60 to 232 at end September 2025, which may have reduced the portfolio’s exposure to stock specific risk.

- The previous investment policy excluded certain stocks on ESG grounds. Under the new policy, BRAI has a wider opportunity set.

- Costs have been reduced, with a halving of the base management fee and the introduction of a new tiered structure (see page 11).

- Dividends have increased to 1.5% per quarter or about 6% per annum (see page 9 for more detail).

- Regular, performance-triggered exit opportunities have been introduced and an exit opportunity will also be provided if the trust does not grow (see page 10).

What is systematic active equity?

Data-derived insights to spot mispriced stocks

BlackRock’s Systematic Active Equity (SAE) team states that it uses data-derived insights to identify and exploit market inefficiencies (mispriced stocks). At the end of September 2025, BlackRock was managing over $313bn using this approach across a variety of global and regional portfolios; long only, partial short, and hedge fund structures; and a London-listed investment company, which the firm describes as the first of its kind.

BlackRock has a team of over 100 investment professionals, based in San Francisco and London, dedicated to SAE.

The approach draws on over 40 years of insights into practices that have been observed in active investment management.

BRAI’s universe is no longer constrained by ESG criteria

BRAI’s universe is no longer constrained by ESG criteria, as it was in its previous guise, but ESG analysis is incorporated within the research process.

Continuous innovation

The SAE team is making ongoing changes with the aim of optimising the outcome for investors. Quant-driven strategies have been in use for a long time, but the amount of information available to the managers has increased. The managers are responsible for identifying which data may provide useful insights, determining when to use these, assessing whether certain datasets provide useful insights only when they are used together or at certain points in the economic cycle, and deciding the weighting given to each set of insights when making investment decisions.

Few asset managers have the scale to succeed in this area

The SAE team was an early adopter of AI and machine learning

Collating and processing the information appears to require significant resources, particularly computing power. It appears that relatively few asset managers have the scale that may be necessary to operate in this area.

In addition, the managers observe that the largely-numeric fundamental value data that was available early on came in a structured and relatively easy-to-analyse format. However, many of the datasets that are available to the team now are unstructured and often in the form of text. The SAE team states that it was an early adopter of AI and machine learning as it sought ways to interpret that data in a useful and practical way.

While an analysis of a company’s fundamental value is incorporated within the process, the SAE team also draws on multiple independent data sets. For example, analyst reports and newspaper articles are scanned for information regarding sentiment towards a company’s products or services. The SAE team also collects data on areas such as internet search trends, transaction volumes, footfall data, and app usage statistics.

The SAE team reviews an average of 10 new sets of data each month.

The analysis also incorporates macroeconomic indicators, using “now-casting” techniques to assess current economic conditions.

Insights are tested for their ability to predict fundamentals and returns consistently and reliably. These evaluations are conducted using tools that run a five-year back test in less than two seconds.

The managers have the authority to make final decisions and may, for example, delay the execution of trades in the event that there is a major market shock.

The SAE approach generates higher portfolio turnover (roughly 100%–200% of the portfolio each year). According to BlackRock, the impact of the cost of trading is factored into each investment decision and a proportion of trades are crossed or matched within BlackRock, which may reduce transaction costs.

The output

The analysis produces insights into aspects such as:

- How attractive are a company’s fundamentals?

– Examining areas such as profitability, growth, financial strength, valuation, and management characteristics.

- Market sentiment

– Assessing sentiment towards a company based on views from analysts, investors, and management, as well as flows of investors’ money in and out of funds and strategies; and

– Considering whether the broader market environment appears supportive of the stock by evaluating similar businesses, customer and supplier information, and other potential indications of a supportive environment.

- Macroeconomic themes

– Looking at themes across industries, countries, and styles.

- ESG

– Is a business exposed to ESG risks, and how is it mitigating these?

– How does it treat its staff, customers, and suppliers?

– The company could be affected by the transition to a carbon-neutral world, depending on its industry, operations, and adaptation strategies.

Once the managers have a set of signals that they believe is providing useful information, the scores from these signals are blended to give a view on each stock in the universe. Higher scores are associated with higher return expectations, and this informs portfolio construction, which aims to achieve a trade-off between risk and return net of transaction costs.

The portfolio will typically contain between 150 and 250 large- and mid-cap stocks.

BRAI will still, in theory, be permitted to invest up to 20% of its assets outside the US. However, in practice, its portfolio now appears more likely to be 100% committed to US equities.

The macroeconomic backdrop

Markets have recovered from the selloff associated with Liberation Day

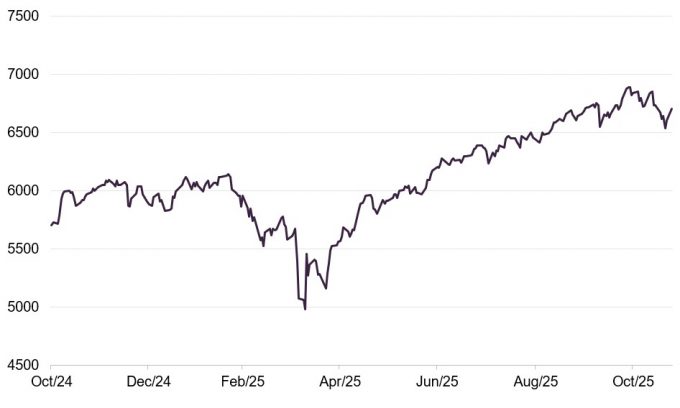

One influence on markets globally has been President Trump’s policy agenda. A central aspect of this has been his tariff policy. Tariffs were imposed on imports from Canada and Mexico, followed by the announcement on 2 April 2025 of tariffs on almost all imports. The market appeared to react negatively to this, which was followed by a reduction in tariffs on a temporary basis to 10% in most cases. Markets then appeared to recover, and announcements of various trade “deals,” not all of which are confirmed, may have contributed to a renewed risk-on environment.

The AI trade, which appears to have gained momentum in March 2023 with the release of ChatGPT-4, experienced a setback in January 2025 following reports of DeepSeek’s development of a new large language model (LLM), which the company stated had been developed at a lower cost compared to equivalent US models. This was followed by a sharp selloff of the Magnificent Seven stocks, as well as increased flows into other US stocks and out of the US into other markets. Mega cap US technology stocks were also affected by the Liberation Day declines in markets. The pace of capital expenditure into AI infrastructure did not appear to slow, and this may have contributed to a recovery in confidence in the trade.

BRAI offers a way of diversifying US exposure away from the Mag 7

Now, these US mega-caps represent a significant portion of the S&P500 once again. For investors who wish to gain exposure to the US market but seek diversification, BRAI may provide an alternative.

Figure 1: S&P 500 Index over 12 months to end October 2025

Source: Bloomberg

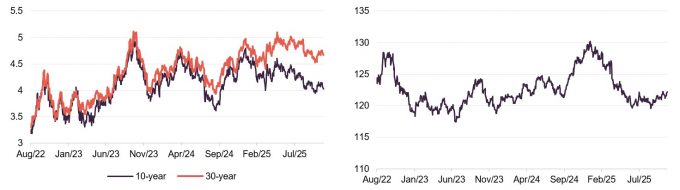

The US president has argued for lower interest rates, but the Federal Reserve has, to date, maintained its position, citing concerns over the inflationary effects of tariffs, for example. Calls for the dismissal of Fed board members and its chair could undermine confidence in US bond markets. Inflation numbers in the US have been increasing.

Another consideration for debt investors is the potential long-term effect of the One Big Beautiful Bill (OBBB), which is projected to add trillions of dollars to the US deficit. If this is combined with higher government borrowing costs, it may present challenges.

Figure 2: US long-term government bond yields

Figure 3: US dollar trade-weighted index

Source: Bloomberg

Source: Bloomberg

These factors have likely combined to weaken the US dollar. On a trade-weighted basis, the dollar has fallen from its February peak. However, this process may continue if flows out of US assets increase.

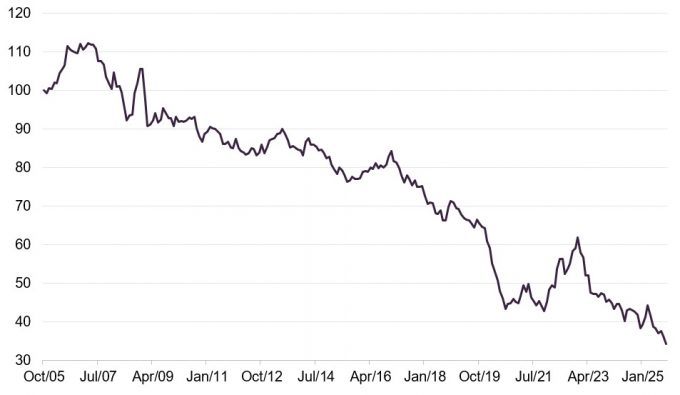

Figure 4: Value versus growth in US market

Source: Bloomberg (based on MSCI US value and growth total return indices)

For BRAI, a key consideration is the performance of value stocks (its universe) relative to growth stocks. As Figure 4 shows, value stocks have declined relative to growth stocks over the past two decades. The extended period of low US interest rates that followed the global financial crisis in 2008 may have contributed to this trend.

Late in 2021, expectations of rising interest rates, which were later confirmed, appeared to trigger a rally in value. However, the relative peak set at the end of 2022 was followed by a resurgence of growth, which may be partly attributable to the success of AI. Liberation Day appeared to halt another emerging value rally.

The managers observe that in some ways, unpredictable policy shifts by the US administration may make their job more difficult. They also note that this appears to be causing shifts in investor behaviour, which they believe could create more mispriced securities.

The portfolio

New portfolio in place from 22 April 2025

The realignment of the portfolio to fit the new strategy was completed by 22 April 2025. The manager contributed towards expenses, and there was an NAV uplift associated with the tender offer, which meant there appeared to be no cost to ongoing shareholders.

At the end of BRAI’s last financial year (ahead of the realignment), the trust had almost 10% of its portfolio invested in non-US stocks; currently, the entire portfolio is invested in US stocks.

Marked shifts in sector and stock exposures

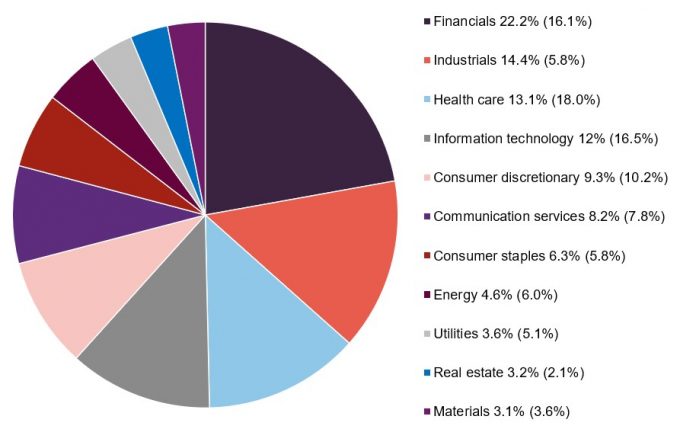

Figure 5 shows the split of BRAI’s portfolio by industry sector as at 30 September 2025. The figures in brackets represent the percentage of the portfolio in each sector as at the end of BRAI’s last financial year (31 October 2024), before the adoption of the new investment approach. There have been shifts in sector allocations, with higher exposure to financials and industrials, and lower exposure to health care and information technology. The net effect is that, on a sector basis, the portfolio is much closer to the benchmark. This suggests that, in terms of alpha generation, stock selection appears to be the primary contributing factor.

Figure 5: BRAI asset allocation by sector as at 30 September 2025 (and as at 31 October 2024)

Source: BRAI

There is minimal overlap between BRAI’s 10 largest positions at the end of its last financial year (31 October 2024), before the new investment approach was adopted, and the largest positions in the portfolio at the end of September 2025.

Figure 6: Top 10 holdings as at 30 September 2025

| % as at 30/09/25 | % as at 31/10/24 | Change | ||

|---|---|---|---|---|

| JPMorgan Chase | Financials | 3.2 | – | 3.2 |

| Berkshire Hathaway | Financials | 2.8 | – | 2.8 |

| Walmart | Consumer staples | 2.6 | – | 2.6 |

| Amazon | Consumer discretionary | 2.6 | 1.7 | 0.9 |

| Bank of America | Financials | 2.3 | – | 2.3 |

| Alphabet | Communication services | 1.9 | – | 1.9 |

| Morgan Stanley | Financials | 1.9 | – | 1.9 |

| Johnson & Johnson | Health Care | 1.8 | – | 1.8 |

| Charles Schwab | Financials | 1.7 | – | 1.7 |

| Pfizer | Health Care | 1.6 | – | 1.6 |

| Total | 22.3 |

Performance

Building a track record of outperformance

Analysis of BRAI’s returns before the strategy change may not considered relevant to this note. Figure 7 shows how BRAI has performed in both share price and NAV terms versus its performance benchmark, and against the S&P 500 Index since the strategy change.

The data suggest that BRAI has outperformed its objective to date. The S&P 500 Index has likely been influenced by the performance of mega-cap, AI-related companies. BRAI’s performance benchmark appears to be more diversified, although the trust has some exposure to the AI theme. The trust has generated returns over the past six months without a significant allocation to the mega-cap AI theme.

It may be too early to draw conclusions about the volatility of these returns, but this will be considered in our future reports.

Figure 7: Total return performance data for periods to end October 2025

| Calendar year | 1 month (%) | 3 months (%) | 6 months (%) | Since 22 April 2025 (%) |

|---|---|---|---|---|

| BRAI share price | 2.3 | 8.6 | 17.7 | 16.6 |

| BRAI NAV | 3.6 | 8.1 | 17.2 | 21.4 |

| Russell 1000 Value | 2.9 | 5.9 | 15.1 | 18.5 |

| S&P 500 | 4.9 | 9.0 | 25.6 | 32.3 |

Dividends

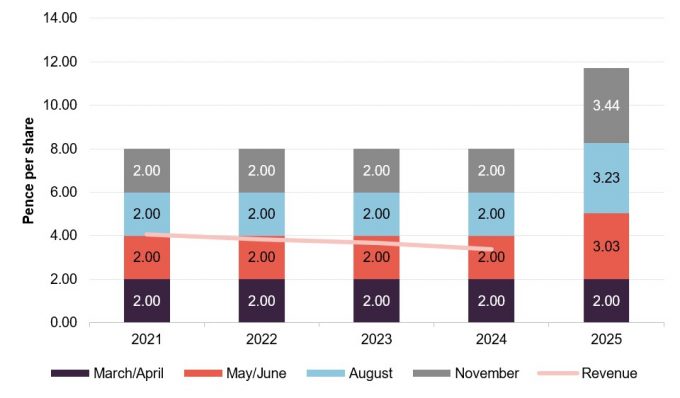

New enhanced dividend policy roughly 6% of NAV each year

With effect from 17 April 2025, BRAI adopted a policy of paying a quarterly dividend equivalent to 1.5% of NAV (approximately 6% annually). The x-axis labels show historic ex dates for BRAI’s dividends. Going forward, the intention is to pay the dividends in April, July, October, and January.

Figure 8 shows BRAI’s dividend history over the last five years. The final column reflects the shift to paying a dividend based on 1.5% of NAV.

To facilitate the payment of its enhanced dividends and share buybacks if needed, BRAI had distributable reserves of £105.7m at the end of April 2025. The payment of enhanced dividends is not a new feature for the trust; its dividends have not been covered by net revenue earnings since FY 2017. Without the constraint of having to hold high-yielding stocks to generate its income, BRAI may invest across the US market with the aim of maximising total returns.

Figure 8: BRAI five-year dividend history for financial years ending in October

Source: BRAI, Marten & Co

Premium/(discount)

Over the 12 months ended 31 October 2025, BRAI’s shares traded at a discount to NAV between 11.9% and 1.0% and averaged 6.3%. At 26 November 2025, the discount was 5.4%.

The discount widened over 2023 as the Magnificent Seven dominated markets and value stocks underperformed. After an initial increase last summer, BRAI’s rating began to improve in October last year, which may have been influenced by anticipation of the tender offer, and is now at a higher level. The board has stated that it would like to see investors support the new approach and for the trust to grow.

Conditional tender offers

If BRAI does not exceed its benchmark net of fees by an average of 0.5% per annum over three-year periods, the first of which ends on 30 April 2028, the company has committed to offering shareholders a 100% tender offer at a 2% discount to NAV less costs.

In addition, the 100% tender offer may also be triggered if the net assets of the company are less than £125m at the end of those three-year periods.

Figure 9: BRAI’s premium/(discount) over the five years ended 31 October 2025

Source: Bloomberg, Marten & Co

Structure

Capital structure

BRAI’s issued share capital comprises 95,361,305 ordinary shares, of which 38,949,167 are held in treasury. The number of shares with voting rights is 56,412,138.

BRAI’s financial year end is 31 October, and its AGMs are typically held in March. The board is planning to announce the trust’s next set of annual accounts in January 2026.

Shareholders approved the continuation of the company at this year’s AGM. Another continuation vote is scheduled for 2028 and every three years thereafter.

Fees and costs

With effect from 17 April 2025, BRAI has a tiered management fee, based on NAV, of 0.35% on the first £350m and 0.30% on any balance. There is no performance fee.

The ongoing charges ratio for the year ended 31 October 2024 was 1.06%, based on a management fee of 0.70% on NAV. Following the fee cut, this ratio may be lower in this and future years. The board has estimated that over a full 12-month period of the new fee, the ongoing charges ratio is expected to fall to approximately 0.70%–0.80%.

The managers

BRAI’s AIFM is BlackRock Fund Managers Limited. BlackRock Investment Management (UK) Limited acts as BRAI’s investment manager and company secretary.

BRAI’s lead managers are Travis Cooke and Muzo Kayacan.

Travis Cooke

Travis is head of the US portfolio management group within BlackRock’s systematic active equity (SAE) team. He is responsible for the management of the US long-only, partial long-short, and long-short equity strategies within SAE.

Travis joined Barclays Global Investors (BGI) in 1999, and that firm merged with BlackRock in 2009. At BGI, he was a portfolio manager for various developed market strategies within its alpha strategies group.

Travis has a BA degree in Business Economics from the University of California at Santa Barbara in 1998, and an MSc in Finance from London Business School in 2008. Additionally, he has been a CFA charterholder since 2001.

Muzo Kayacan

Muzo is a portfolio manager and head of EMEA product strategy in the SAE division. He is responsible for managing US, global, and European funds as well as overseeing the EMEA product strategy team, which provides a link between investment teams and clients.

Prior to joining BlackRock in 2010, Muzo was a senior associate portfolio manager at AllianceBernstein, where he was responsible for implementing investment decisions in global developed and emerging markets institutional equity portfolios, as well as implementing active and passive currency hedging strategies. From 2005-2007 he completed a graduate training scheme with M&G, followed by a role in the product development team. Before joining M&G he was a futures trader.

Muzo holds a Bachelor’s degree in Psychology from Warwick University, obtained in 2003. He has been a CFA charterholder since September 2009.

The board

BRAI has four directors, all of whom are non-executive and independent of the manager. Alice Ryder stepped down as chair and as a director following the last AGM and David Barron succeeded her as chair. Gaynor Coley is the most recent appointee and has taken on the role of audit committee chair from David Barron.

Figure 10: Directors’ length of service, fees, and shareholding

| Role | Appointed | Length of service (years) | Fees(£) | Shareholding | |

|---|---|---|---|---|---|

| David Barron | Chairman | 22/03/2022 | 3.7 | 45,000 | 11,677 |

| Gaynor Coley | Chair of the audit committee | 25/06/2025 | 0.4 | 39,000 | 10,000 |

| Solomon Soquar | Senior independent director | 21/03/2023 | 2.7 | 32,500 | 10,000 |

| Melanie Roberts | Director | 01/10/2019 | 6.2 | 32,500 | 10,000 |

Source: Marten & Co

David Barron

David spent 25 years working in the investment management sector and was until November 2019 chief executive officer of Miton Group Plc, following six years with the firm. Prior to this he was head of investment trusts at JPMorgan Asset Management for more than 10 years, having joined Robert Fleming in 1995. He is currently chairman of Baillie Gifford European Growth Trust Plc and (until its planned merger with AVI Japan Opportunity Trust Plc completes) a non-executive director of Fidelity Japan Trust Plc.

Gaynor Coley

Gaynor Coley is a chartered accountant with over 30 years of experience in private and public sector finance, including experience of governance, compliance, and risk management. She is a non-executive director and chair of the audit committee of Foresight Enterprise VCT Plc and Lowland Investment Co Plc, and chair of the grants committee and a trustee of the Duchy Health Charity.

Solomon Soquar

Solomon Soquar has over 30 years of experience in investment banking, capital markets and wealth management. He has worked with several financial institutions, including Goldman Sachs, Bankers Trust, Merrill Lynch, Citi and Barclays. His most recent executive role was as CEO of Barclays Investments Solutions Limited. In recent years he has held a portfolio of roles, including non-executive director of Ruffer Investment Company Limited; chair of the Africa Research Excellence Fund; and business fellow at Oxford University, Smith School of Economics and Enterprise.

Melanie Roberts

Melanie Roberts is a partner at Sarasin & Partners LLP. She has 29 years of investment experience. She joined Sarasin & Partners in 2011 and in January 2023 was appointed head of charities, continuing to focus on strategy, stewardship, and client service for charity portfolios. Prior to joining Sarasin & Partners, she spent 16 years at Newton Investment Management as a fund manager of charity, private client and pension fund portfolios.

IMPORTANT INFORMATION

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on BlackRock American Income Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it. Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.