Some commentators appear to have overstated the impact of regulatory concerns on Civitas Social Housing’s (CSH’s) performance. Regulatory notices served on some of its tenants knocked the share price over 2018/2019. However, during the whole period, it collected its rents, paid its dividends and increased its net asset value (NAV).

Recognition of this fact, and the supply and demand fundamentals that support growth in the supported living sector, saw its share price recover and its discount narrow. That momentum, as has been the case in all global markets, has been somewhat curtailed by the coronavirus outbreak. Owing to the strong characteristics of the sector, CSH has been one of the best performing REITs and property companies since the covid-19 pandemic escalated.

The company is keen to expand but has delayed taking on new debt facilities until the markets return to normality. Following the acquisition of a portfolio of properties in March 2020, CSH’s dividend is fully covered by earnings on a run rate basis.

Income and capital growth from social housing

Income and capital growth from social housing

CSH aims to provide its shareholders with an attractive level of income, together with the potential for capital growth from investing in a portfolio of social homes. The company expects that these will benefit from inflation-adjusted long-term leases and that they will deliver a targeted dividend yield of 5.3% per annum on the issue price, with further growth expected. CSH intends to increase the dividend broadly in line with inflation.

| wdt_ID | Year ended | Price total return (%) | NAV total return (%) | EPRA earnings per share (pence) | Dividend per share (pence) |

|---|---|---|---|---|---|

| 1 | 31 Mar 2018 | -0.60 | 10.70 | 1.44 | 4.25 |

| 2 | 31 Mar 2019 | 4.20 | 9.40 | 3.63 | 5.00 |

| 3 | 31 Mar 2020 | 6.60 | 4.30 | 5.30 |

Back on track following turbulent 2019

A wider acknowledgement of the strong foundations that support CSH’s business has been reflected in its share price.

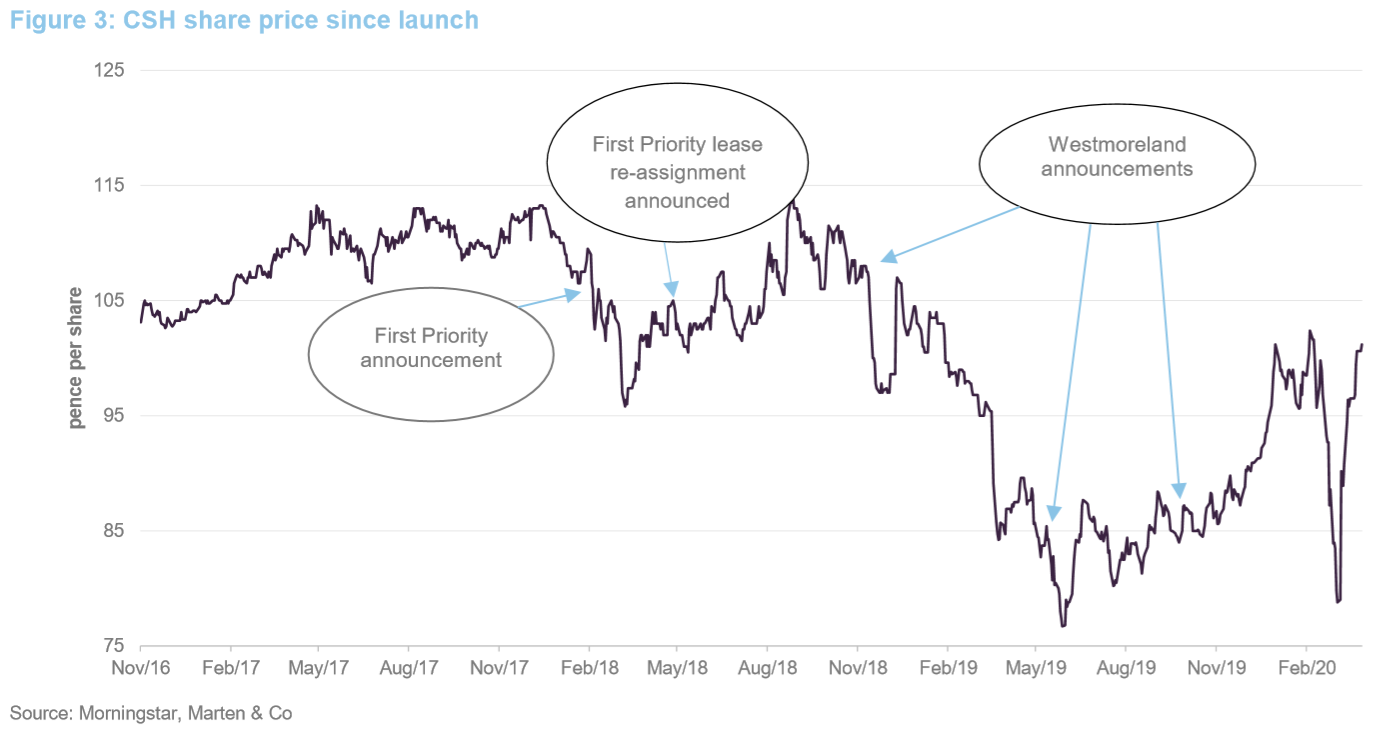

Following a series of regulatory notices on some of the housing associations that rent CSH’s supported living properties, the company’s share price hit an all-time low of 76.7p in June 2019, from an inception price of 103.0p in November 2016 and a peak of 114.0p in September 2018.

But CSH proved that despite the growing pains of the housing associations that lease its properties, it continued to collect its rents, pay its dividends and increase its net asset value (NAV). Its share price bounced back in the second half of 2019 and has continued to track upwards into 2020.

The fundamentals that underpin the supported living sector – namely the chronic shortage in supply of appropriate accommodation, and growing demand; the better health outcomes specialist supported housing brings to occupants; and the substantial cost saving to government – are not going away. In fact, demand is growing at an average of around 5% a year with more than 170,000 people already housed in supported living facilities like those provided by CSH.

We explained the structure of the specialist supported housing market in the UK in our September 2019 annual overview note. To recap, substantial savings are available to local authorities if they can rehome a person in need of supported living from a hospital into a property adapted to their needs. Research has also shown that these tenants then have an improved quality of life and better medical outcomes. Local authorities turn to care providers to manage the day-to-day welfare of the tenant and to housing associations to provide the accommodation. The housing associations lease property on a long-term basis from the likes of CSH.

The sector desperately needs more supply of specialist homes for supported living. The chronic lack of housing led to the launch of a legal challenge in February 2020 against the Secretary of State for Health and Social Care over the repeated failure to move people with learning disabilities and autism into appropriate accommodation.

The Equality and Human Rights Commission said that more than 2,000 people with learning difficulties and autism are detained in secure hospitals, amounting to a systemic failure to protect the right to a private and family life, and a right to live free from inhuman or degrading treatment or punishment.

Central government has always supported the specialist supported living sector. The new Conservative government has made commitments to support the delivery of state funded healthcare and social care, while recognising the cost savings and better personal outcomes for individuals that supported living accommodation offers.

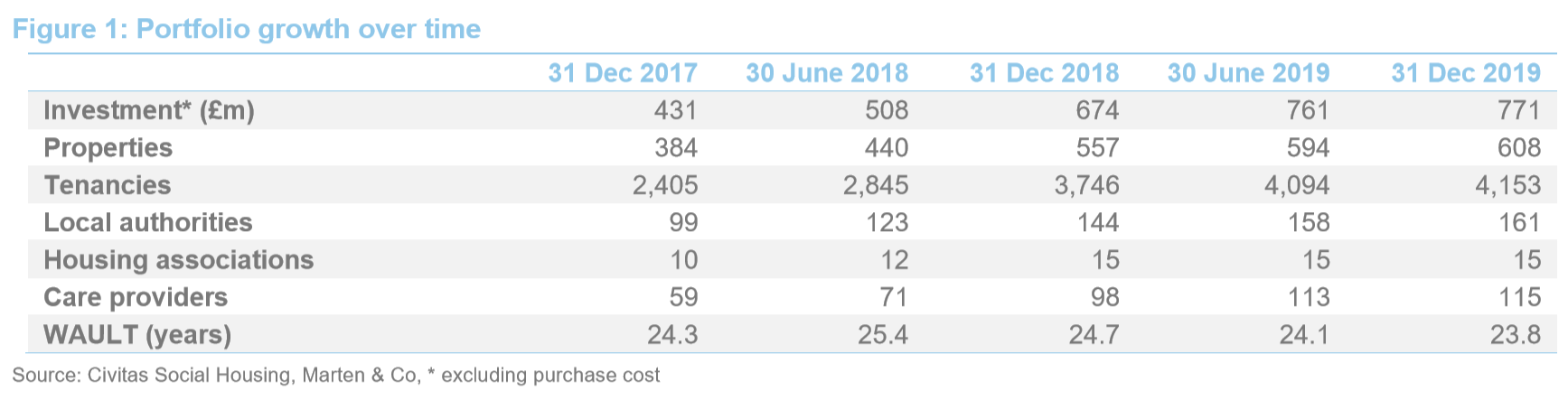

As the biggest and most established specialist supported housing fund, CSH is playing a leading role in growing the sector. It currently owns 616 properties that house more than 4,200 people with long-term health issues.

In March 2020, CSH acquired eight freehold properties for a total of £19.6m, adding 74 tenancies to the portfolio. The properties are leased to housing associations that are existing tenants in its portfolio.

CSH has identified an acquisition pipeline worth more than £200m but needs additional capital to make real in-roads into it. With a current gross loan-to-value (LTV) ratio of around 28%, CSH has ample capacity to leverage further against its LTV target of 35%. With unencumbered properties within the portfolio to a value of around £212m, CSH says it intends to implement its long-term debt strategy over the coming months in terms of additional facilities in a prudent manner taking full regard of prevailing circumstances surrounding covid-19.

With a 100% run-rate dividend cover already achieved (following the acquisitions in March 2020 and including the £12.1m Welsh commitments) further deployment of debt would increase CSH’s rental income, pushing dividend cover further above 100%.

An equity raise is an option for CSH further down the line. It says that it will monitor its share price when markets go back to normal after covid-19 is over, and if its share price recovers to where it was in early March 2020 and its discount narrows further, it may look to the market for equity.

The company wants to broaden its portfolio exposure in the supported living sector to include other areas of government-backed housing, such as facilities for homeless people and accommodation for people stepping down from the NHS. CSH has had a number of conversations with NHS trusts and other providers to develop a pipeline of NHS step-down facilities. These are long-term step-down homes and facilities for those with care needs who are currently housed in hospitals.

CSH would enter into long-term leases with the NHS, which may be structured in the form of specific joint venture arrangements, and also with registered charities. CSH will seek shareholder approval to expand its investment policy at an EGM.

Shareholder approval was received last year to open up CSH’s investment criteria to include Scotland and Northern Ireland, and it has been actively looking at investment opportunities in these countries.

Coronavirus impact

CSH’s share price initially fell following the covid-19 pandemic but regained its losses and is up 14.2% in the month to 14 April 2020.The role of supported living and social care in assisting the NHS during the crisis has been well-publicised in the national media. CSH has said it has received direct and indirect enquiries from the NHS to see if it has any properties that could be made available to them and is working closely with them to provide these.

Although the coronavirus pandemic has delayed some business decisions, such as the new debt facilities, the mid to upper acuity nature of CSH’s portfolio has meant it has been less impacted by the crisis and is in a strong position to grow further when life returns to normal.

Proactive to regulatory issues

The concerns that the Regulator for Social Housing (RSH) had with specific housing associations have been or are currently being addressed. CSH’s leading position in the sector enables it to identify issues at associations early and act quickly and decisively in reassigning leases and minimising impact on its business.

This has been the case with Westmoreland Supported Housing, which has been the subject of several regulatory judgements relating to its governance and financial management (not specific to CSH). Nonetheless, CSH reassigned a significant proportion of Westmoreland’s leases to several other housing associations already in its portfolio on the same terms, while Westmoreland works through its issues. Its exposure to Westmoreland, as measured by rental income, has been reduced to 6.4% from 10.8% at 30 September 2019.

It was a similar story with First Priority Housing Association in February 2018. The RSH published a regulatory notice on the company stating that it did not believe First Priority had sufficient working capital or the financial capacity to meet its debts and highlighted governance concerns. CSH took the decision to reassign the First Priority leases in its portfolio – of which there were 45 – to other providers on similar terms and without any material loss.

The Social Housing Family CIC

CSH is in frequent dialogue with the regulator and works closely with housing associations to support them and help recruit experienced and knowledgeable non-executive directors onto boards in order to strengthen corporate governance and improve standards of disclosure and asset management.

It has taken its responsibility as the leading player in supported living further with the formation of a not-for-profit community interest company (CIC). The Social Housing Family CIC’s aim is to enable the housing associations in CSH’s portfolio to increase their skills and experience and provide funding if required to promote enhanced performance. This should also give additional comfort to the regulator when it assesses the housing association’s governance and financial viability.

The CIC is operationally and financially independent from CSH and is supported by financial contributions from within the social housing sector and has a skills commitment from CSH.

Members of the CIC transfer ownership of the housing association to the social housing family, thereby giving CSH enhanced certainty of future rental income as well as further protecting the interests of end users.

Auckland Home Solutions is the first housing association to join The Social Housing Family CIC, and recruitment of additional senior personnel for Auckland is already under way as a means of providing further resource and expertise.

Performance

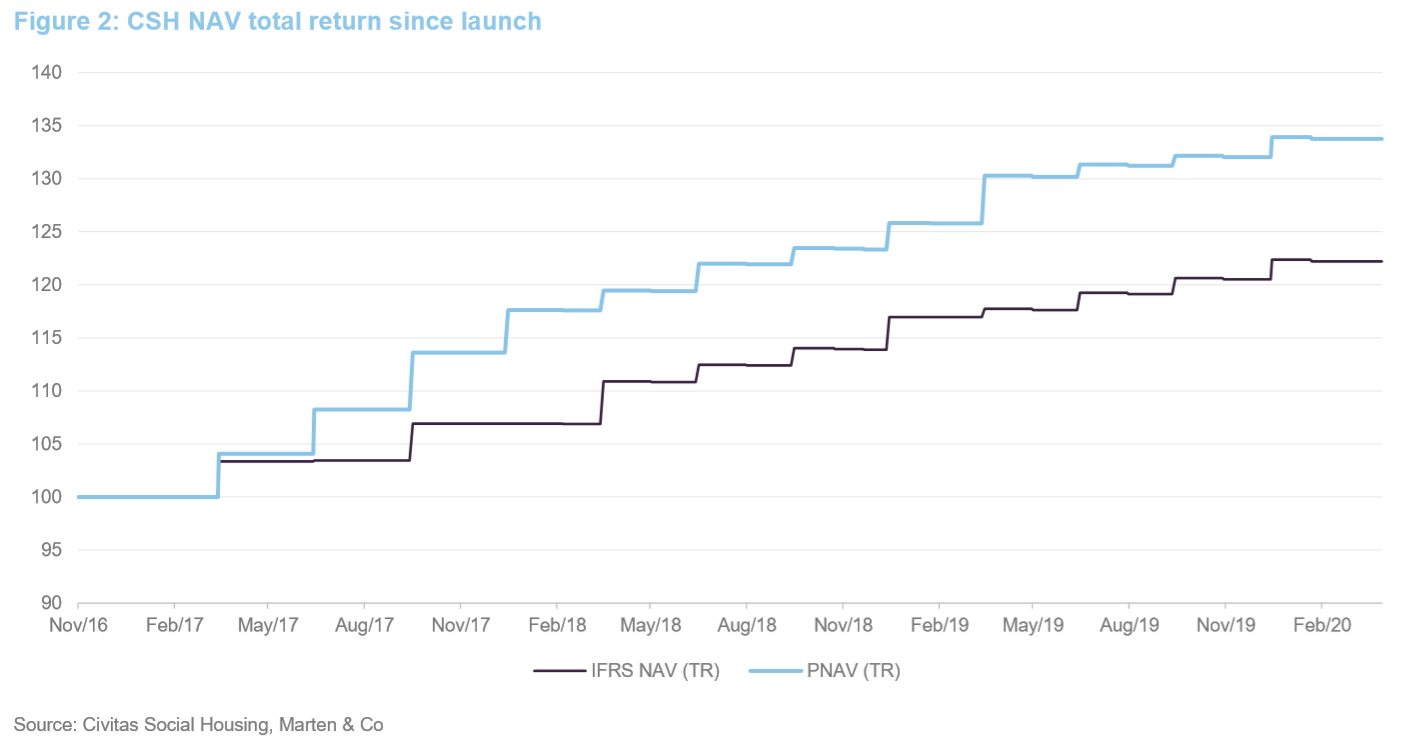

CSH publishes two NAVs – an International Financial Reporting Standards (IFRS) NAV, which reflects the value of the portfolio if it was sold off on a piecemeal basis, and a portfolio NAV, which is based on the value if it were to be sold as a single portfolio. This reflects the fact that the properties are held in special purpose vehicles and attract a lower tax charge than selling properties individually.

At 31 December 2019, the IFRS NAV was £688.6m or 107.55p per share. On a portfolio basis, the NAV was £737.6m or 118.65p per share.

Share price

The second half of 2019 saw CSH’s share price start to recover from an all-time low of 76.7p on 14 June 2019. The share price trended upwards in the second half of 2019 and into 2020 as the market became more comfortable with the fundamentals of the business. CSH’s share price tailed off in March 2020 as part of a wider sell-off due to fears over the spread of covid-19, but regained all its losses.

Peer group comparison

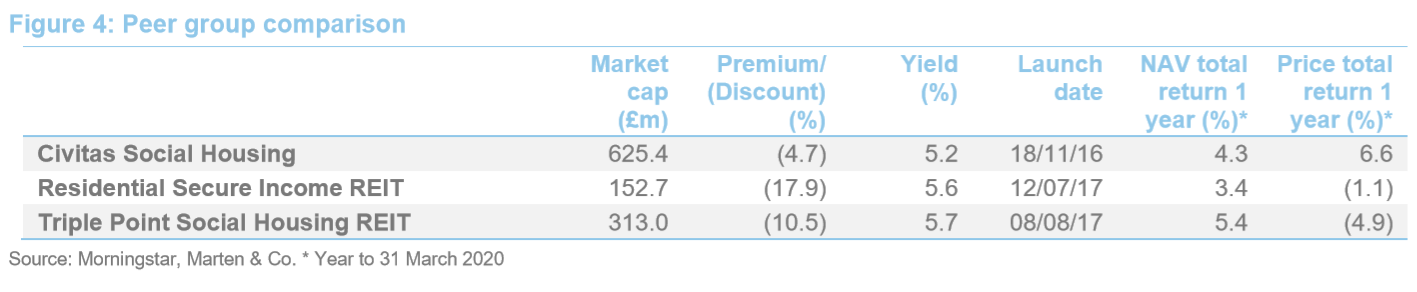

CSH sits within a small group of listed peers comprised of Triple Point Social Housing REIT (SOHO) and Residential Secure Income REIT (RESI). CSH is by far the largest fund in this peer group. RESI’s focus is more on retirement properties and shared ownership housing (without leases), and therefore SOHO may provide a better comparison. CSH is larger and has a longer track record and therefore its superior rating is merited.

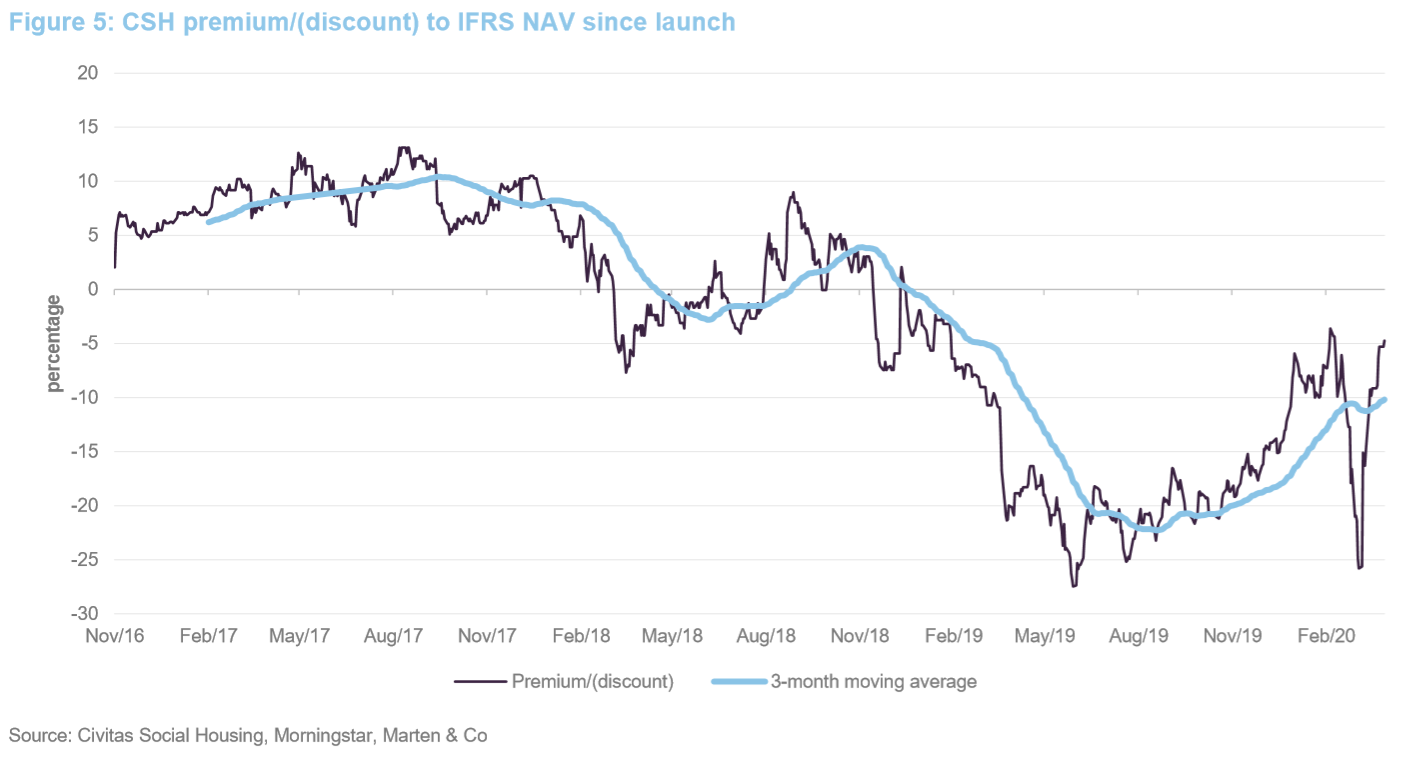

Premium/(discount)

CSH’s ordinary shares initially traded at a premium to its IFRS NAV but moved to trade at a discount due to the concerns that the regulator highlighted regarding some of the housing associations in its portfolio. As the company demonstrated the underlying fundamentals supporting growth in the supported living sector and its leading position in it, the discount has narrowed since July 2019 and was as low as 3.6% in late February. The wider sell-off due to fears over the spread of covid-19 saw the discount initially widen before narrowing again, and at 14 April 2020 it stands at 4.7%.

Fund profile

CSH launched on 18 November 2016, raising £350m at IPO and expanded in November 2017, raising an additional £302m through a C share issue. These two pools were merged together in December 2018.

CSH aims to provide an attractive yield, with stable income growing in line with inflation and the potential for capital growth. Its diversified portfolio is let to housing associations and local authorities on long-term lease agreements, typically 25 years. It buys only completed homes, which includes acquiring new developments on completion, but it does not get involved with forward funding deals or the management of social homes directly.

CSH’s portfolio has a low correlation to the general residential and commercial real estate sectors, as the supply and demand demographics driving the social home sector do not move in line with that of the wider real estate market. It is a real estate investment trust (REIT), giving it certain tax advantages. As a REIT, it must distribute at least 90% of its income profits for each accounting period.

The adviser: Civitas Housing Advisors

CSH is advised by Civitas Housing Advisors (CHA), a business established in 2016. Many of the 20-strong team have long experience of working in the sector and in specialist healthcare, and collectively, they have been involved in the acquisition, sale and management of more than 80,000 social homes in the UK.

Previous publications

Marten & Co has published three previous notes on CSH. You can read them by clicking the link or by visiting the martenandco.com website.

Socially beneficial investing, initiation note, published June 2018.

Regulatory action is positive, update note, published February 2019.

Targeting full dividend cover, annual overview, published September 2019.

The legal bit

This marketing communication has been prepared for Civitas Social Housing by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and if you are not a professional investor, or in any other way are prohibited or restricted from receiving this information you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it but, in practice and in accordance with our internal code of good conduct, will refrain from doing so. Nevertheless, they may have an interest in any of the securities mentioned in this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.