Short shrift to short seller

An attack by an activist short seller on the fabric of Civitas Social Housing (CSH), coinciding with it falling out of the FTSE 250 index, appears to have driven down CSH’s share price in recent months. CSH has published a strong rebuttal (details of the claims and CSH’s response are on page 5) saying these claims are baseless. The short seller may have made a quick profit, however CSH has had to put a planned capital raise to grow its portfolio on ice and it has impacted the wider sector to the detriment of thousands of people in need of specialist housing.

The manager says that the fundamentals that support growth in the sector remain strong (as detailed on pages 3 and 10). As a result of the short seller attack, CSH’s shares are now trading on a wide discount, while it has increased its dividend target for this year.

Income and capital growth from social housing

CSH aims to provide its shareholders with an attractive level of income, together with the potential for capital growth from investing in a portfolio of social homes. The company expects that these will benefit from inflation-adjusted long-term leases and that they will deliver a targeted dividend yield of 5% per annum on the issue price, with further growth expected. CSH intends to increase the dividend broadly in line with inflation.

Fund profile

CSH has invested £825m to amass a portfolio of diversified supported social housing assets since it launched on 18 November 2016. It raised £350m at IPO and expanded in November 2017, raising an additional £302m through a C share issue (whereby C share investors own a separate class of shares which has its own portfolio). These two pools were merged together in December 2018.

CSH aims to provide an attractive yield, with stable income growing in line with inflation and the potential for capital growth. Its diversified portfolio is let to housing associations and local authorities (referred to as registered providers) on long-term lease agreements, typically 25 years. It buys only completed homes, which includes acquiring new developments on completion, but it does not get involved with forward funding deals (putting up money to finance the construction of new social homes), or the management of social homes directly.

CSH’s portfolio has a low correlation to the general residential and commercial real estate sectors, as the supply and demand demographics driving the social home sector do not move in line with that of the wider real estate market. It is a real estate investment trust (REIT), giving it certain tax advantages. As a REIT, it must distribute at least 90% of its income profits for each accounting period.

The adviser – Civitas Investment Management

CSH is advised by Civitas Investment Management (CIM), previously named Civitas Housing Advisors, a business established in 2016. Many of the 25-strong team have long experience of working in the sector and in specialist healthcare, and collectively, they have been involved in the acquisition, sale and management of more than 80,000 social homes in the UK.

Market outlook

CSH remains a leading UK investor in specialist supported housing, which is an integral part of the healthcare sector in the UK and a key component in facilitating the delivery of care for individuals with significant long-term care needs. It enables such people to live fulfilling lives within the community and close to their families, rather than in a hospital or institutional setting.

Individuals in supported housing properties require some form of care, and mainly include people with learning disabilities, autism, mental health issues and physical disabilities, although demand for supported housing is growing and expanding to cover a wide range of underlying needs faced by people who are battling homelessness, addiction or who are stepping down from the NHS into a more appropriate supportive care environment.

Local authorities are responsible for providing accommodation and funding care for individuals within their jurisdiction. Supported living provides local authorities with a cost-effective solution to housing people in need, with rents being cheaper than residential care placements and inpatient facilities. According to the monetisation calculations completed by the Social Profit Calculator in 2021, CSH’s portfolio generated £75.9m of direct fiscal savings to local and national government per year. The setting also increases quality of life and life outcomes for the residents.

How it works

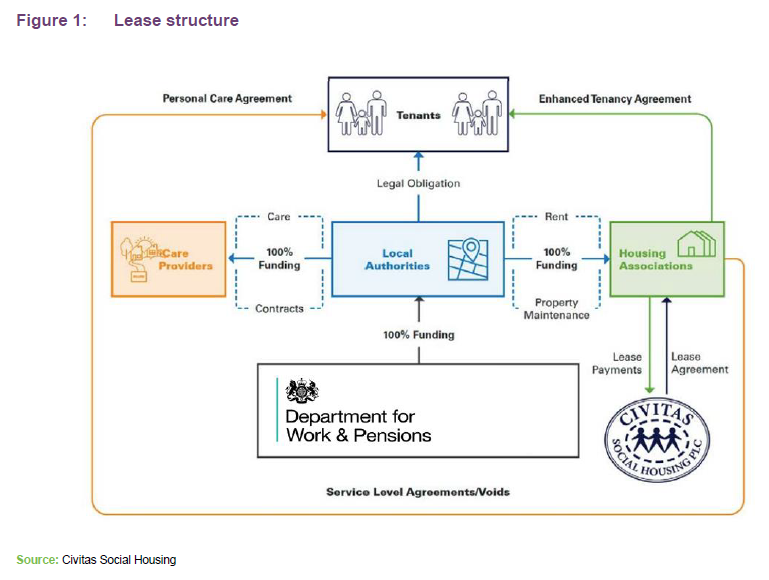

Housing benefit typically provides 100% of the funding of rent and service charge for all supported housing, as shown in Figure 1.

Local authorities enter into care contracts with care providers, who are responsible for the personal care of each individual tenant, and pay them from funding provided by the Department for Work and Pensions.

The care provider in turn enters into a service level agreement with a registered provider, usually a housing association, which has ultimate responsibility for housing provision. Housing benefit is paid by the local authority to the registered provider to cover each individual tenant’s rent and service charge.

CSH owns the property and rents it under a long-term lease, or an occupancy agreement, to the registered provider. The registered provider uses the housing benefit that it receives to cover the rent due and the costs of managing and maintaining the property, as well as seeking to generate a modest surplus.

Of the £264bn spent by the UK government on welfare in 2017, around 10% (£25bn) covered housing benefit, according to the Office for National Statistics. Of the £25bn, supported social housing accounted for roughly 3.5% or £1.4bn. CSH’s annualised rent roll represents roughly 6% of housing benefit spent on supported social housing, highlighting the significant growth opportunity for the company.

Short seller attacks rebuffed

It has been a tumultuous couple of months for CSH that has seen around a quarter wiped off its market cap since early August. The group has come under fire from an activist short seller, ShadowFall, that has made several damaging claims that have negatively impacted CSH’s share price. Below, we have laid out the salient claims by the short seller and CSH’s reply.

Transparency

The short seller’s claims centre around several property investments made by CSH with entities where two directors of the manager, CIM, own a combined 29.98% stake. These, it said, should have been disclosed to shareholders.

For context, a new care provider called Specialist Healthcare Operations Limited (SHO) was setup in 2018 with the help of CIM directors Tom Pridmore and Andrew Dawber. Whilst being an independent care provider (with Paul Hainsworth, a senior executive from Lifeways – one of the UK’s leading specialist care providers – as chief executive and Paul Marriner – formerly chief executive of Lifeways – as chairman) SHO has participated in a small number of OpCo/PropCo split investment deals made by CSH (whereby CSH would acquire the properties and SHO would buy the operating businesses). These were in circumstances where the care provider wanted a clean exit from the entire business and where CSH says it would have struggled to find properties of equivalent quality on the open market.

As REIT rules exclude acquisition of anything but real estate, CSH says it sought to find third-party care providers to make joint bids but said this proved to be difficult. A new care provider was established that would be willing to work alongside CSH on a non-exclusive basis to acquire the care operating businesses and so enabling CSH to acquire the respective real estate assets. Mr Pridmore and Mr Dawber, utilising their sector contacts, brought together suitable investors and professionals to form SHO. CSH says that as originators of the business and to provide alignment with the incoming management team, Mr Pridmore and Mr Dawber each became 14.99% shareholders in SHO, which translates into a 10% economic interest each as a result of the preferential rights and shareholdings of the other SHO shareholders. CSH states that they are not directors and have no involvement in the running of the business. Neither have they received any remuneration or any other form of income from SHO, it adds.

CSH has undertaken four joint tenders with SHO for the purchase of existing built and occupied properties and associated care businesses. Three of the four were the acquisition of the entire care businesses including properties by CSH with an agreed back-to-back sale of the operating businesses to SHO. The fourth was structured so that the properties and the operating business were acquired separately by CSH and SHO on the same day.

CSH says that in order to avoid any conflict-of-interest issues, a buy-side committee, which comprises CIM independent non-executive directors, was established to approve the deals before being submitted for board and AIFM approval.

Prior to any transactions, CSH says that it also sought advice from its sponsor and professional advisers about the related party transaction rules under the Listing Rules and submissions were made to the FCA. The advice received was that these transactions were not related party transactions for the purposes of the Listing Rules as Mr Dawber’s and Mr Pridmore’s aggregate shareholding was below 30% and they would not receive any additional economic benefits, it adds.

CSH says that the deals were not disclosed to shareholders as it considered there was a competitive first mover advantage to the Opco/PropCo arrangements, which would enable CSH to participate in acquisition processes for high-quality properties from their owners. Whilst the OpCo/PropCo concept is common in the property industry, CIM says this was an innovation in the specialist care sector.

OpCo sales price

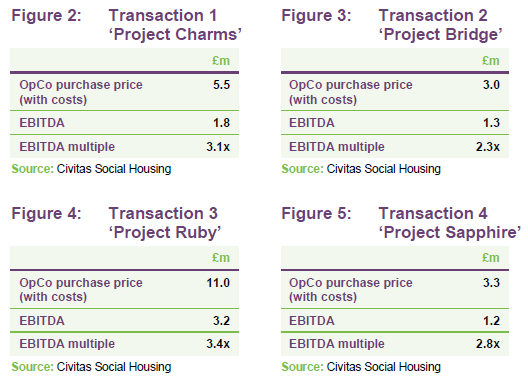

The short seller also queried the price paid by SHO to CSH for the operating companies, implying these transactions had been done on the cheap to the detriment of CSH and its shareholders. It stated that the EBIT multiple paid for the operating companies was as low as 1.3x.

In response, CSH set out the purchase metrics for the four operating businesses acquired by SHO. It said due diligence reports and a formal ‘fair and reasonableness’ assessment had been received by CSH’s board before the transactions. Figures 2 to 5 show CSH’s purchase metrics of the four transactions, showing that the EBITDA multiple was between 2.3x and 3.4x.

In its financial year to March 2021, properties owned by CSH where a SHO entity acts as the care provider represented 14% (£6.9m) of the total annualised rent roll (£50.8m).

Lease lengths

In its open letter to CSH’s board and shareholders, ShadowFall questioned conflicting lease lengths reported by CSH and the registered providers in their respective accounts. The insinuation was that these were inflated by CSH in order to boost NAV and therefore CIM’s management fee.

The discrepancies come in the financial reporting of the lease lengths on the balance sheet of the registered providers. CSH says that the leases it grants to tenants come in two phases – the initial lease term and an extension. Importantly, the extension is exercised at CSH’s sole discretion. Leases may also be granted with a reversionary lease (of 10 to 20 years in length) that automatically commences the date after the initial lease (of 10 to 20 years) expires.

Registered providers may account for the initial (minimum) lease term only for the purposes of their financial reporting, as in theory, the option may not be exercised by CSH at that date. CSH adds that it is for the registered providers to determine the extent to which they recognise lease obligations on their balance sheets. For CSH, the lease has been valued by independent valuers on the normal basis of the full lease term on the premise that it would exercise its option to extend.

100% government backed income

The short seller additionally attempted to cast doubt over the validity of CSH’s “100% government funded” model, stating that CSH had provided substantial lease incentives to tenants and also that two registered providers received loans or rent support from developers – all of which, it said, showed the tenants were financially supported in meeting its rent obligations to CSH.

Lease incentives

Lease incentives are common within the real estate sector and are mainly used to encourage tenants to sign up to long leases at the start of a lease term. Typically, they comprise a rent reduction for an initial period of the lease or some funding support for development of the property.

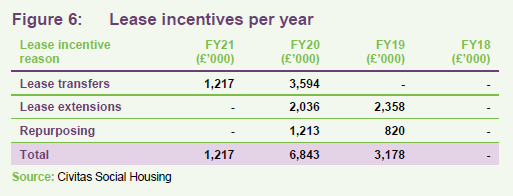

The figure that ShadowFall uses to illustrate rising lease incentives across CSH’s business is £11.2m in the 2021 financial year, up from £6.8m in FY20 and £3.2m in FY19. However, this includes a £10m payment made by CSH that it says was a second instalment for a new-build property development to SHO. CSH states that, as is common practice in funding property developments (so as not to be exposed to any development risk), the project was paid for in two instalments, the first (£12.2m) when building works were complete and the second (£10m), when occupation had been achieved and care and rent packages were approved by the relevant local authorities. CSH says that the second payment is accounted for under IFRS as a lease incentive due to it being a further payment on an existing lease. For all intents and purposes, however, it is a second capital investment to acquire the development project, CSH says.

Therefore, in the financial year 2021 lease incentives totalled £1.2m (which CSH says relates to on-boarding fees in respect of lease transfers). Figure 6 shows CSH’s lease incentives since it launched.

CSH says that it anticipates that the level of lease incentives going forward is likely to be similar to FY21.

Developer loans/rent support

ShadowFall highlighted that two of CSH’s tenants – Encircle and Westmoreland – had been supported by a developer through loans or rent support. Again, CSH says that this is common practice in the real estate sector during the construction or development phase – in other property sectors usually through rent guarantees.

CSH states that developers have a legitimate role in meeting the costs of rental income before a property is fully occupied. During this time the registered provider will receive income to cover the cost of lease payments to CSH (and other landlords) and this will be paid either by the original developer or by the care provider (which could also be the developer). Once a resident is in place all occupation costs are met by the state.

CSH adds that some developers, as part of the range of services they offer, have provided assistance, funding and operational support to registered providers some of which has also been in the form of “in kind” services such as centralised repairs and maintenance and assistance with rent collection from local authorities. This was the case with Westmoreland where Fairhome Group provided support in this regard, CSH says.

Tenant strength

Finally, the short seller questioned the long-term viability of CSH’s rental income with several of its tenants in “financial difficulty”. Since 2018, a number of CSH’s tenants (nine of 17) have been deemed non-compliant by the Regulator of Social Housing for either governance or financial viability or both. Despite this, the impact on CSH has been minimal. It has continued to collect its rents in full throughout and the independent valuer of its portfolio has not seen fit to reduce the value of properties on the basis of the regulator’s judgments on the tenants.

The most recent regulatory notice was on 12 November, which found Falcon Housing Association (CSH’s largest tenant) non-compliant with governance and financial viability standards. It is true that the sector has suffered from growing pains as the sector matures, but CSH states it continues to work closely with all of the registered providers to assist in the strengthening of the businesses. Significant progress has been made, it states, with changes in personnel at both board and executive levels as well as operational enhancements.

In the case of Falcon, the regulator also identified issues around some deals Falcon had entered into with third parties, stating that some involved companies which were at the time linked to directors and shareholders of Falcon. This related to National Care Group, a care provider. CSH says that the presence of directors with outside interests, such as within the care sector or specialist developers, that are correctly disclosed is not unusual within the social housing sector. The origins of what are now large housing associations are often from the care industry, which was the case with Falcon. The two directors in question have since stepped down from the board of Falcon and have transferred ownership of their stake in Falcon to a trust.

Property valuations

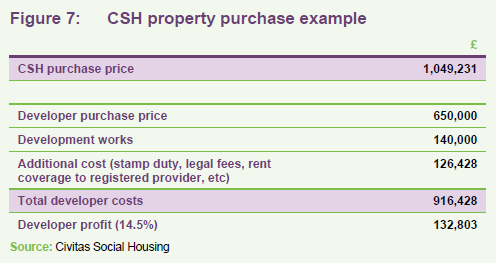

In its letter to shareholders responding to the short seller, CSH also included a section explaining the change in value between what developers/aggregators pay for properties and what CSH pays the developer. Put simply, CSH says that the cost of works to adapt the property from a residential home into a specialist care accommodation with independent apartments is included in the price that it pays. The developer will initially be paid only the value that it has incurred in purchasing the property plus a margin to cover historic costs and an agreed transparent profit (usually around 15%), CSH states. Costs relating to future works will not be paid until the works are completed. The price paid by CSH is supported by independent valuations. By way of example, Figure 7 shows a breakdown of a CSH transaction.

Market fundamentals strong

The demand and supply characteristics in the specialist supported housing sector are compelling, CIM says. There is a severe shortage of properties that are capable of hosting mid-to-higher-acuity care within local community settings, while demand for such properties is high due to the long-standing government policy to seek closure of remote hospitals in favour of community provision.

The trend for community provision has become established in the UK over the past 25 years and reflects much broader societal change in the manner that care is delivered for people of working age with lifelong care needs. What has developed more recently has been the emergence of specialist housing associations that deliver the augmented property services and who, in turn, enter into leases to secure available properties for their underlying tenants.

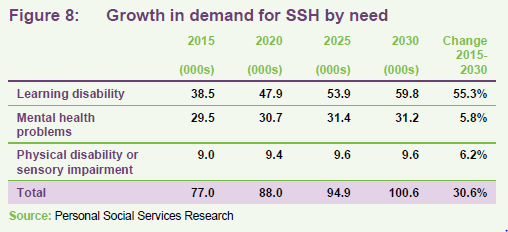

The Personal Social Services Research unit has predicted 30% growth in the demand for SSH housing in England by 2030 and 55% in respect of learning disability alone, as shown in Figure 8. Meanwhile the National Audit Office has forecast a 29% increase in adults aged 18 to 64 requiring care by 2038 compared to 2018.

On the supply side, Mencap states that a significant undersupply of SSH has resulted in a significant number of people with long-term care needs living with elderly parents and over 2,000 people with a learning disability being placed in inpatient units, miles away from their family. The supply of social housing in the UK fell from around 7m in 1980 to 5m in 2018.

Social impact

Investment in supported living is designed with the intention of enhancing the lives of people who, as a result of the homes, are able to benefit from the availability of secure, long-term, high-quality housing, whether of a general nature or as a base for the provision of more specialist housing and care.

Every year, social advisory firm The Good Economy publishes a report examining the social impact of CSH’s investments. The 2021 report found CSH to be an “authentic impact investor” in accordance with the International Finance Corporation Principles for Impact Management. As part of the report, the Social Profit Calculator (SPC) – a social value consultancy that specialises in calculating the additional value of social, economic, and environmental impact – calculated the social value of CSH’s portfolio in monetary terms and found the portfolio to have produced £127m of social value per year (this improves on the £114m calculated in 2019 – it didn’t release a report in 2020 due to COVID). This total social value figure was split between £51.2m of social impact (this is the value of the improved personal outcomes for residents) and £75.9m of fiscal savings generated for public budgets through the reduced cost of care packages. The total figure equates to £3.51 of social value being created for every £1 of annualised investment.

Investment process

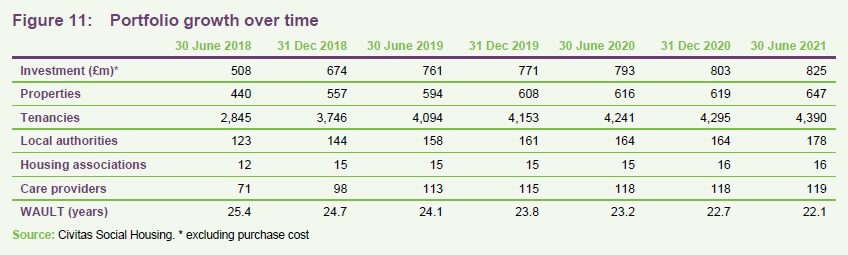

CSH has invested £825m to build a portfolio of 648 properties, as at 30 September 2021. The company’s investment portfolio offers dual exposure to both the social housing and healthcare sectors in the UK. It provides purpose-built and bespoke properties that support the delivery of mid-to-higher-acuity care for working-age adults with long-term care needs. It delivers this in local community settings supported by government-funded care providers and housing associations.

The bulk of the properties have been acquired from housing associations, care providers, developers and private owners, at yields of between 5.5% and 6.5%; mainly on an off-market basis. As the first and largest fund in the sector, CSH has established extensive relationships with developers, care providers and registered providers, which it uses to put in place acquisition agreements. All of the properties that it acquires already have a lease agreement with a registered provider in place, and so are income-producing from day one. It may, from time to time, require the seller to review and upgrade the contracts that it has with various parties before acquisition.

In May 2020, CSH received overwhelming approval from shareholders to expand its investment policy to allow transactions to be undertaken directly with other not-for-profit organisations, including the NHS as well as other entities in receipt of government funding.

CSH makes a detailed assessment of each property to ensure it is fit for purpose before acquisition. It only invests in completed buildings and does not engage in development or forward funding risk.

Due diligence

CSH has followed a detailed due diligence programme with its lease counterparties since launch, which encompasses:

- completion of diligence forms for KPIs, health and safety and finances;

- discussions with the chief executive and finance director of the registered provider;

- site visits to meet management and visit properties;

- standard investigation reports on key individuals for standards of conduct;

- regulatory checks;

- review of available management accounts and business plans;

- physical inspections of properties;

- independent, third-party benchmarking of rent;

- references from all significant care providers; and

- requests for ring-fencing, with segregated accounts or charges for protection of rent and deposits due to CSH.

Promoting best practice

CSH works closely with housing associations to support them and help recruit experienced and knowledgeable non-executive directors onto boards in order to strengthen corporate governance and improve standards of disclosure and asset management.

It has taken its responsibility as the leading player in supported living further with the formation of a not-for-profit community interest company (CIC). The Social Housing Family CIC’s aim is to offer additional support, guidance and management skills to its member housing associations.

The CIC is operationally and financially independent from CSH, is supported by financial contributions from within the social housing sector and has a skills’ commitment from CSH.

Members of the CIC transfer ownership of the housing association to the social housing family, thereby giving CSH enhanced certainty of future rental income as well as further protecting the interests of end users.

Auckland Home Solutions was the first housing association to join The Social Housing Family CIC, and recruitment of additional senior personnel for Auckland has provided further resource and expertise.

CSH has also developed a best-practice protocol to ensure that housing associations are structured for long-term stability.

The protocol contains 10 core principles relating to matters such as financial prudence, conflicts of interest, management and interaction with regulators. In addition, it contains detailed requirements for the on-boarding of new properties. These include:

- independent verification of rent to confirm this is appropriate within the local authority area and represents value for money;

- a minimum ‘on-boarding fee’ paid to the Registered Provider from the proceeds of the sale of the property to CSH, to cover the setup costs of getting the property ready for occupation by a tenant;

- the Registered Provider maintaining segregated accounts/charges for rent and service charges for properties leased from CSH;

- the establishment of a rental protection fund for each tenant, to cover three-to-six months’ rent on every property;

- a sinking fund for each property to cover certain capital and maintenance costs and over-runs; and

- an indexation reserve fund to be set up at the outset of a lease and topped up over its lifetime, with indexation being set with reference to CPI.

Investment restrictions

CSH operates within the following investment restrictions:

- It may only invest in social homes located in the UK.

- It may only invest in social homes where the counterparty to the lease is an approved provider.

- The minimum unexpired term for a lease or occupancy agreement at the time of acquisition will be 10 years (although leases with shorter lengths can be included in an acquisition of a portfolio that has a weighted average unexpired lease term (WAULT) of more than 15 years).

- The maximum exposure to any single approved provider is 25% of gross asset value (once the capital of the group is fully invested).

- The maximum exposure to a group of houses/apartment blocks in a single geographic location is 20% of gross asset value (once the capital of the group is fully invested).

- Only completed social homes will be acquired – forward finance of social homes under construction is not permitted.

- No investment in other investment companies or alternate finance funds.

- No short selling.

Asset allocation

CSH’s portfolio is valued at £940.4m and comprises 648 properties, let to 17 housing associations, with 4,391 individual tenants. The weighted average unexpired lease term (WAULT) on the portfolio is more than 22 years.

Investment activity

CSH’s investment activity has been limited in recent months as it looked to defend itself from the short-seller attack. It bought just one property in the quarter to 30 September 2021, for the delivery of learning disabilities and mental health care services. The manager says that transaction volumes are likely to pick up again in due course and it has an expansive investment pipeline under consideration.

Further enhancing ESG credentials

CSH is pressing ahead with plans to increase the environmental credentials of its portfolio. In June 2021, the company entered into an agreement with energy provider E.ON to undertake environmental enhancements that will help to reduce the carbon footprint across its portfolio.

Initially focussed on 55 properties with lower EPC ratings, the initiative forms part of CSH’s objective to reach carbon neutrality. The project will be part-funded by government grants, including the ECO3 funding scheme, part of the government’s programme to make homes in the UK more energy efficient, and the Domestic Renewable Heat Incentive (RHI), the government’s scheme to support renewable heating costs in homes.

The manager says that it intends to expand the environmental-enhancing schemes across its portfolio over a number of years. As well as having the obvious environmental benefits, improving the energy efficiency of homes should also provide a small incremental increase to the value of the portfolio, the manager believes.

Performance

CSH publishes two NAVs – an International Financial Reporting Standards (IFRS) NAV, which reflects the value of the portfolio if it was sold off on a piecemeal basis, and a portfolio NAV, which is based on the value if it were to be sold as a single portfolio. This is generally higher than the IFRS NAV, reflecting the fact that the properties are held in special purpose vehicles and attract a lower tax charge than selling properties individually.

At 30 September 2021, the IFRS NAV was £672.9m or 108.49p per share. On a portfolio basis, the NAV was £742.6m or 119.74p per share.

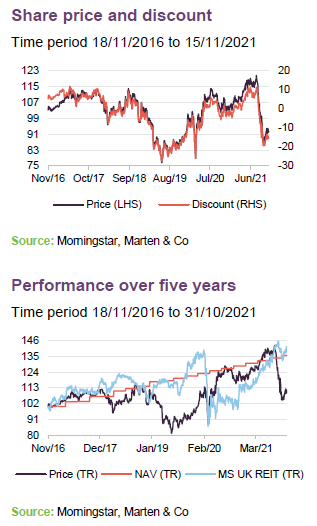

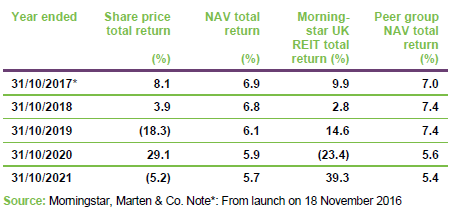

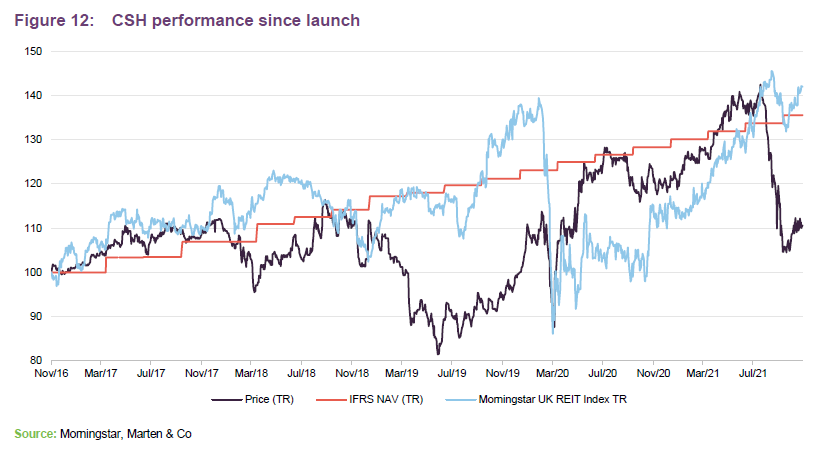

CSH’s share price has fallen sharply since August 2021 as firstly a regulatory judgement on one of its tenants was published, then secondly it was targeted by the activist short-seller. This coincided with the company dropping out of the FTSE 250 index, which saw index trackers sell out of their position in the fund. The share price seems to have turned a corner in recent weeks. It had been on an upward trajectory since June 2019, apart from the COVID-19 induced blip in March 2020 when its share price crashed as part of a wider sell-off due to fears over the pandemic. The share price quickly regained all its losses as investors recognised the strength of its government-backed income. Unlike most other REITs, CSH has not seen a drop-off in its rent collection rates throughout the COVID-19 pandemic. Its NAV has trended upwards since its launch almost five years ago and over the period the NAV total return is 35.1%.

Peer group comparison

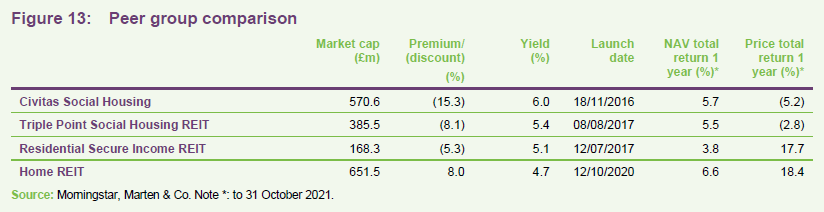

CSH sits within a small group of listed peers comprised of Triple Point Social Housing REIT (SOHO), Residential Secure Income REIT (RESI) and Home REIT (HOME).

RESI’s focus is more on retirement properties and shared ownership housing (without leases), whilst HOME launched in October 2020 and is solely focused on providing homeless accommodation. Therefore, SOHO may provide a better direct comparison. CSH is larger and has a longer track record than SOHO, a greater yield and a comparable performance over one year in both price and NAV terms.

Dividend

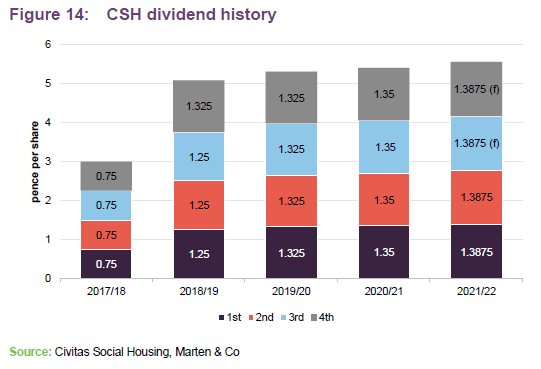

CSH is targeting a dividend for the financial year ending 31 March 2022 of 5.55p per share, continuing its upward progression since it launched five years ago (as shown in Figure 14). This is a 2.8% increase on the 5.4p it paid in the previous year. It declared a second quarterly dividend of 1.3875p on 8 November, which will be paid around 13 December.

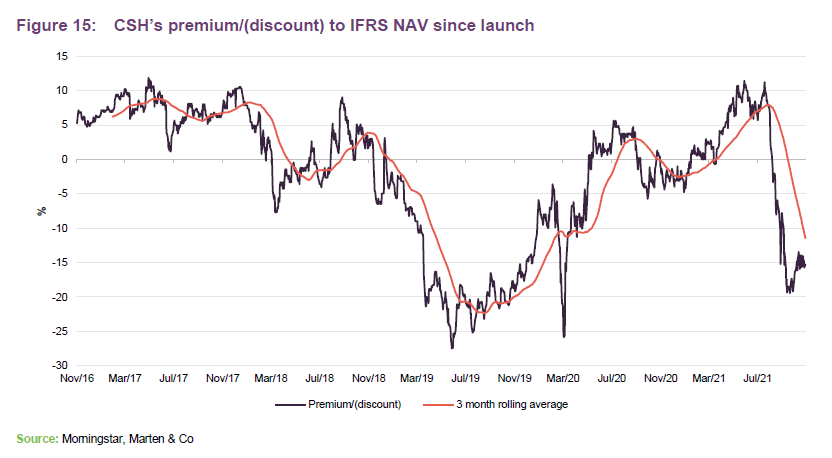

Premium/(discount)

CSH’s shares initially traded at a premium to its IFRS NAV, but moved to trade at a discount due to the concerns that the regulator highlighted regarding some of the housing associations in its portfolio. As the company demonstrated the underlying fundamentals supporting growth in the supported living sector and its leading position in it, the discount narrowed from July 2019. The discount widened dramatically as COVID-19 was declared a global pandemic but quickly narrowed again as the company and the sector proved resilient, helped by secure government-backed income. Following the events mentioned earlier, the premium narrowed from a peak of around 10% to a discount. At 15 November 2021 it was trading at a discount of 15.3%.

CSH is authorised to repurchase up to 14.99% of the issued share capital (renewal of this authority is sought annually at the company’s AGM). Any shares repurchased may be cancelled or held in treasury and later resold. Shares will not be resold from treasury at a discount to NAV unless as part of an offer that is being made to all shareholders on a pro-rata basis.

As at 15 November 2021 CSH had repurchased 5,850,000 shares to be held in treasury since 20 September 2021 at an average price of 90.5p per share and a cost of just under £5.3m. This represents 0.94% of the issued share capital. The share purchases were made with a view to reducing discount volatility following the short-seller attack and are accretive for shareholders.

Fees and costs

CIM is entitled to an annual advisory fee based on a percentage of CSH’s IFRS NAV. This is calculated as 1% on the first £250m, 0.9% on the next £250m, 0.8% on the next £500m and 0.7% on amounts above £1bn. The fee is calculated and paid quarterly in advance. There is no performance fee.

CIM’s contract cannot be terminated before 30 May 2024 and thereafter 12 months’ written notice is required.

Capital structure and life

As at 15 November 2021, CSH had 616,611,380 ordinary shares in issue, with 5,850,000 shares held in treasury.

Debt facilities

Gearing may be used up to an absolute maximum of 40% of gross asset value (i.e. net gearing of 66.7%). Debt has to be secured at an asset level (a property or collection of properties held within a special purpose vehicle) without recourse to CSH. The board has stated that it intends that CSH should have an average leverage of 35% on a gross asset basis. CSH has total bank borrowings of £357.0m, equating to 34.5% of gross assets.

In February 2021, CSH announced it had secured a new seven-year-term, interest-only loan facility of £84.55m from M&G Investment Management, priced at 2.75% above a fixed rate set by reference to the LIBOR swap rate. It is secured by an existing portfolio of specialist supported living assets.

Other debt facilities comprise a £52.5m loan note from Scottish Widows with a maturity in November 2027 and an all-in fixed cost of 2.99%, two revolving credit facilities – a £60m facility with Lloyds maturing in July 2023 and a £100m facility with HSBC maturing in November 2022, and a £60m fixed-rate debt facility with NatWest maturing in August 2024. The NatWest loan can be extended for an additional two years and there is an option of a further £40m accordion.

Life

CSH’s year end is 31 March. CSH will hold its first continuation vote at the AGM in 2022 and every five years thereafter.

Major shareholders

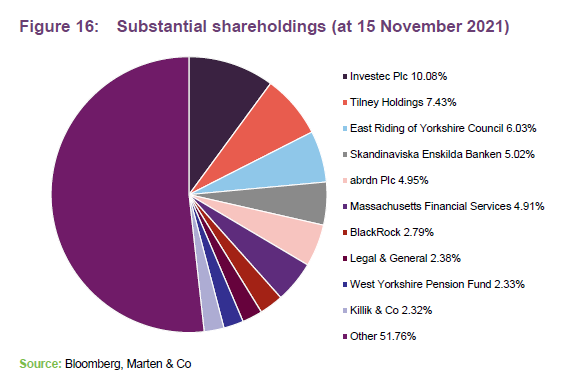

The main change in CSH’s largest shareholders has been the introduction of Scandinavian institutional investor Skandinaviska Enskilda Banken (SEB), which bought a 4.6% stake in CSH in early November and has since upped it to 5.0%.

The investment team

CSH’s investment advisor, CIM, has a proven track record in the social housing sector, combined with many years of experience in the investment industry and financial sector.

Paul Bridge

Paul is CIM’s chief executive (social housing) and joined the company at formation. He has over 20 years’ experience of working at a senior level in the social housing sector. He was chief executive of Homes for Haringey, a registered provider, where he was responsible for 800 staff and 21,000 homes. He has also held a variety of non-executive roles including chairman of Thames Valley Charitable Housing Association and director at Hyde Group.

Andrew Dawber

Andrew is a director and co-founder of CIM. He has been active in the social housing sector since 2012 and was part of the team that founded the private investment company Funding Affordable Homes. He also founded PFI Infrastructure, the first publicly traded social infrastructure fund.

Tom Pridmore

Tom is group director and co-founder of CIM. He is a specialist in real estate and residential development finance and was part of the team that founded the private investment company, Funding Affordable Homes. He is a qualified lawyer with over 19 years’ experience in real estate investment and development, and is responsible for sanctioning all property investment advice and portfolio monitoring.

Dipesh Devchand

Dipesh is chief financial officer of CIM, having previously been managing director, head of fund finance & operations for the FTSE 100 listed alternative asset manager, ICG plc, since 2015. Prior to that he was European finance director for Apollo Global Management for eight years and with GlobeOp Financial Services for just over two years. Dipesh brings a wealth of experience covering financing, regulatory reporting, tax and operational matters pertinent to a variety of alternative asset classes. He is a fellow of the ICAEW, having trained as a Chartered Accountant with PwC’s dedicated investment management team in London.

Eleanor Corey

Eleanor is transactions director at CIM. She has extensive experience in all aspects of real estate management, investment, development and finance from stints at the in-house corporate real estate team at Lloyds Banking Group and a national housebuilder. She previously spent more than 12 years at international law firm CMS Cameron McKenna Nabarro Olswang, where she practised in their real estate team.

Mary Finnigan

Mary is transactions director at CIM. She has worked in the real estate sector for over 20 years. Prior to Civitas, Mary was the head of transactions for WeWork where she led the real estate transaction team in the acquisition and asset management of over 150 buildings in 30 cities in EMEA, including numerous pre-lets in London, Paris and Berlin. During her five years at WeWork, Mary gained extensive experience in the regulatory and legal complexities of the key European markets. Mary is a qualified real estate lawyer and began her career at Jones Day Gouldens before moving to SJ Berwin where she advised major developers, landlords and tenants including The Crown Estate, Axa, British Land, SuperDry and Marks & Spencer. Mary is an active member of Women Talk Real Estate, Real Estate Women and Women on Boards.

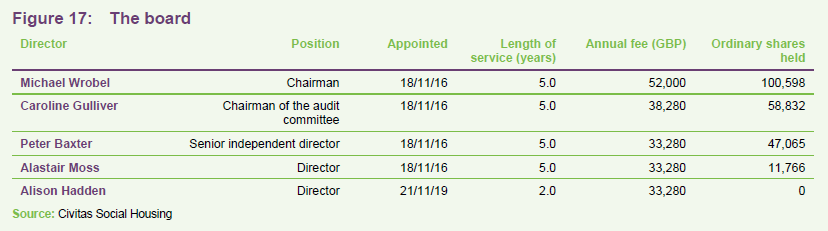

Board

The board is comprised of five non-executive directors, four of whom were appointed on the company’s incorporation in November 2016. All members are non-executive and independent of the investment adviser.

All directors automatically stand for election at the first AGM following their appointment. Thereafter, they are required to stand for re-election at three-yearly intervals, unless they have served for nine or more years, after which they stand for re-election annually. Excluding newly-appointed directors and directors who have served more than nine years, one-third of the remaining directors must retire and stand for re-election by rotation at each AGM.

Michael Wrobel

Michael Wrobel has over 30 years’ experience in the investment industry. He is the non-executive chairman of Diverse Income Trust. He serves as a trustee director of the BAT UK Pension Fund and chair of its investment and funding committee. He is also the chairman of trustees of the Thornton’s Pensions Scheme and Deutsche Bank UK Pension Schemes, a trustee of the Cooper Gay (Holdings) Ltd Retirement Benefits Scheme and acts as an investment adviser to a number of Rio Tinto pension schemes. Formerly, he was a non-executive director of JPMorgan European Smaller Companies Trust and NatWest Smaller Companies. He has served as a director of the Association of Investment Companies, the Investment Management Association and CoFunds. Michael has previously worked at Morgan Grenfell, Fidelity International, Gartmore Investment Management and F&C Management. He has an MA in Economics from Cambridge University.

Caroline Gulliver

Caroline Gulliver is a chartered accountant with over 25 years’ experience at Ernst & Young, latterly as an executive director. During that time, she specialised in the asset management sector and developed extensive experience of investment trusts. She was a member of various technical committees of the Association of Investment Companies and a member of the AIC SORP working party for the revision to the 2009 investment trust SORP (which set out how investment companies should lay out their accounts). Caroline is a non-executive director and audit committee chair for JP Morgan Global Emerging Markets Income Trust, International Biotechnology Trust and Aberdeen Standard European Logistics Income.

Peter Baxter

Peter Baxter has 30 years’ experience in the investment management industry. He is a managing director of Project Snowball, a social impact investment organisation, and a trustee of Trust for London, a charitable foundation. He is also a non-executive director of BlackRock Greater European Investment Trust. Previously he served as chief executive of Old Mutual Asset Managers (UK), and has worked for Schroders and Hill Samuel in a variety of investment roles. Peter holds an MBA from London Business School and is an associate of the Society of Investment Professionals.

Alastair Moss

Alastair Moss is a property development lawyer with over 20 years’ experience and is co-head of real estate at Memery Crystal. He has been a non-executive director of Notting Hill Housing Group (now Notting Hill Genesis) and a member of the audit and treasury committees. He is a former chairman of the investment committee of the City of London Corporation and chaired its property investment board. Alastair is currently chairman of the City’s planning and transportation committee. He is a trustee of Marshall’s Charity and a mentor to commercial directors in government departments, and has also been a board member of Soho Housing Association and was a member of the area board of CityWest Homes. He was a councillor at Westminster City Council for 12 years, including his tenure as chairman of the planning & city development committee.

Alison Hadden

Alison Hadden has over 25 years’ experience in the housing industry. She started her career at Dudley Metropolitan Borough Council and Birmingham City Council, and went on to hold chief executive positions at several major housing associations, including Paradigm Housing, a 13,000-home housing association based in Buckinghamshire. She has also been an executive director at Circle Housing, one of the largest housing associations in the UK. In these roles, she has worked with many of the stakeholders in the industry, including the Regulator of Social Housing. Alison was previously the chair of Housing Plus Group and is currently a non-executive director and member of the audit and risk committee of Yorkshire Housing and a non-executive director and member of the governance committee of Peaks and Plains Housing.

Previous publications

QuotedData has published six previous notes on CSH. You can read them by clicking the links below or by visiting the QuotedData.com website.

Socially beneficial investing – initiation, published 18 June 2018

Regulatory action is positive – update, published 19 February 2019

Targeting full dividend cover – annual overview, published 12 August 2029

Proved its mettle – update, published 15 April 2020

Solid foundations for future growth – annual overview, published 22 October 2020

On firm footing – update, published 17 May 2021

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Civitas Social Housing.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.