2018 re-calibration paying off

2018 re-calibration paying off

Moves by Pacific Horizon’s (PHI) manager Ewan Markson-Brown to re-position the portfolio by lowering its allocation to technology stocks, and excellent returns to-date from stock picks made in 2018, are paying off. PHI is the best-performing Asia Pacific fund in net asset value (NAV) terms over the year-to-date. Following a poor 2018, which saw sentiment turn against both China and technology (areas where PHI has significant exposures), the portfolio is now more diversified with a greater focus on a newer wave of growth companies.

PHI’s strong focus on fast-growing companies means that it is clearly differentiated from its peer group. Despite improved recent performance and a relatively low ongoing charges ratio for its size, the trust’s discount is the widest it has been for nearly two years.

Focused on Asia ex Japan growth stocks

PHI invests in the Asia-Pacific region (excluding Japan) and in the Indian subcontinent in order to achieve capital growth. The company is prepared to move freely between the markets of the region as opportunities for growth vary. The portfolio will normally consist entirely of quoted securities, although it may hold up to 10% of total assets in unlisted investment opportunities.

| wdt_ID | Year ended | Share price total return (%) | NAV total return (%) | MSCI AC Asia Ex-Japan TR (%) | MSCI AC World total return (%) |

|---|---|---|---|---|---|

| 1 | 31 Oct 2015 | -4.50 | -7.50 | -14.40 | -4.00 |

| 2 | 31 Oct 2016 | 38.50 | 34.40 | 23.20 | 35.50 |

| 3 | 31 Oct 2017 | 26.70 | 33.20 | 17.70 | 20.50 |

| 4 | 31 Oct 2018 | -3.90 | -13.80 | -8.40 | -9.90 |

| 5 | 31 Oct 2019 | 5.80 | 18.00 | 9.60 | 11.70 |

Fund profile

Pacific Horizon (PHI) is an Asia ex Japan fund that specialises in investing in growth companies. Baillie Gifford & Co (Baillie Gifford), has been appointed to manage PHI’s portfolio on behalf of Baillie Gifford & Co Limited, the trust’s alternative investment fund manager. Baillie Gifford has managed PHI since 1992. Baillie Gifford is a long-term growth investor and it believes there is a significant opportunity to outperform markets over the long term using this approach.

Ewan Markson-Brown (Ewan, or the manager) has day-to-day responsibility for the management of PHI. He took over the management of the portfolio from Mike Gush on 18 March 2014. Ewan joined Baillie Gifford in 2013 from PIMCO, where he had been a senior vice-president in its emerging markets team. Prior to that, he managed Asian funds at Newton Investment Management.

About the manager

Baillie Gifford has 116 investors/analysts based in its Edinburgh office. It is structured as a partnership and encourages a collegiate approach to managing money, although it allows its portfolio managers the freedom to have the final say about their portfolios. It managed or advised on about £206bn at the end of September 2019, of which £67.7bn was invested in Asia Pacific equities. PHI and the Baillie Gifford Pacific Fund (its open-ended equivalent) have combined total assets of roughly £750m.

Ewan says that his natural inclination is to take a macroeconomic view and thematic considerations are always in the back of his mind. However, he thinks that you only really get to see the big picture by looking at the companies themselves, using a bottom-up approach. This is very much a stock-picking fund and the portfolio bears very little resemblance to the fund’s MSCI All Country Asia ex Japan Index comparative Index (the active share of PHI’s portfolio at the end of September 2019 was 84%). Ewan spends most of his time in meeting companies and undertaking stock-specific research.

Ewan is assisted with the management of the fund by Roderick Snell, who has a degree in Medical Biology. Roderick has been at Baillie Gifford since 2006 and has managed the Baillie Gifford Pacific Fund since 2010. He has been deputy portfolio manager of PHI since September 2013.

Market roundup – Asia and US outperforming

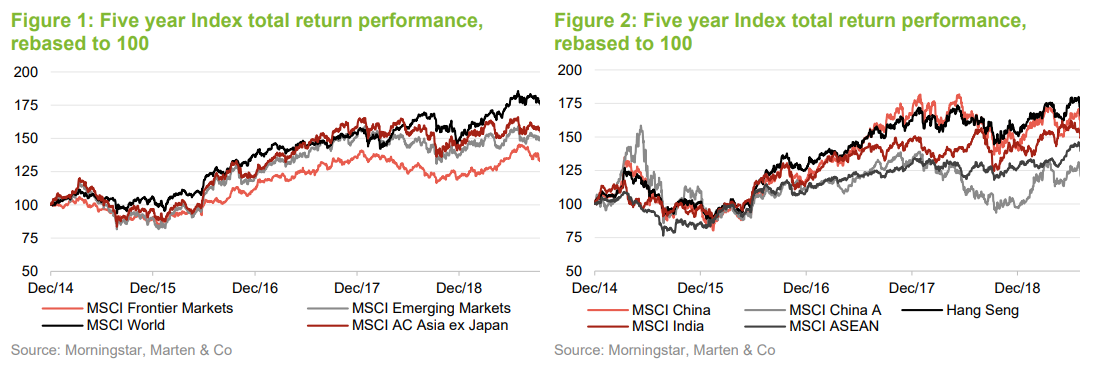

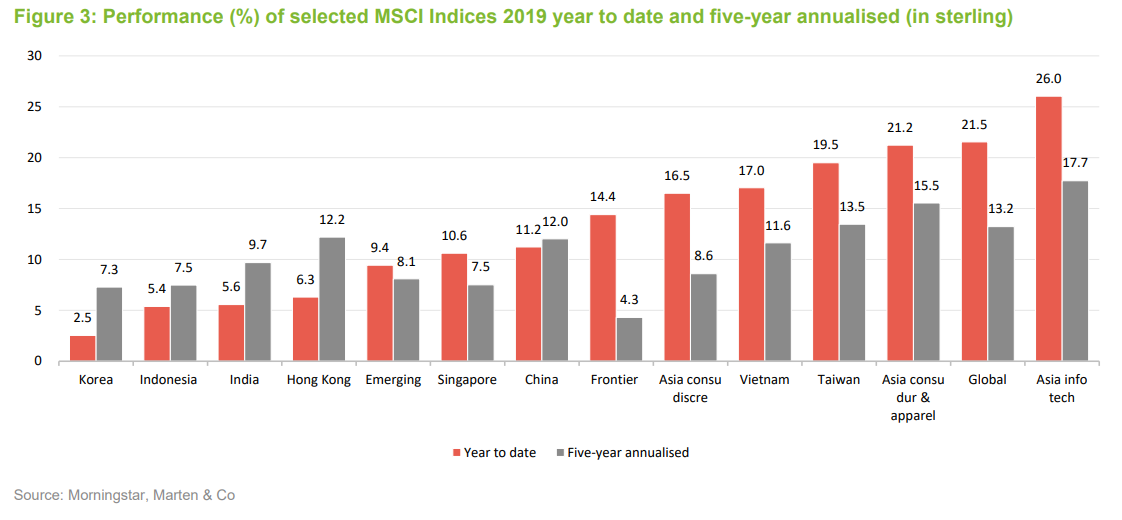

Performance across Asia ex Japan has been a lot better than the wider emerging and frontier universe over recent years. Figure 1 illustrates how the MSCI AC Asia ex Japan Index kept pace with the US-dominated MSCI World Index, until the second half of 2018. A major sell-off in China, notably in technology where the likes of Alibaba and Tencent had previously performed so well, left the US out in front.

It might have been reasonable to speculate that the Federal Reserve’s (the US central bank’s) policy shift earlier this year would lead to some weakening in the dollar, benefitting emerging markets. So far, this has not happened on a global scale, though many Asian stock markets have been performing well. Slowing global growth, emphasised recently by below-par manufacturing output in some key economies, as well as geopolitical tensions and trade wars, have directed flows in the direction of safe-haven assets. Gold is up sharply this year. The US economy remains strong compared to most other major developed economies, while several major Asian markets are growing briskly (see Figure 6).

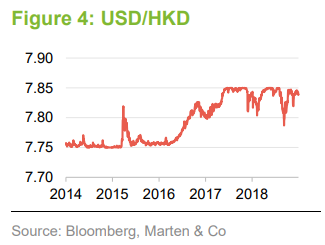

The performance of selected MSCI indices (reflecting PHI’s country holdings and sector allocations) over the year-to-date, is shown in Figure 3. This illustrates how tech and consumer-focused companies have been performing very well across Asia.

Hong Kong protests and the trade war

PHI’s most recent financial year, to 31 July 2019, ended with relations between Hong Kong and the mainland souring to their lowest ebb since China’s resumption of sovereignty in 1996. Hong Kong Chief Executive Carrie Lam’s proposed extradition bill was the catalyst which led to full-blown protests in June. The bill had the potential to undermine Hong Kong’s separate legal system. It is thought that the ferocity of the protests were a culmination of frustration at Hong Kong’s leadership, a lack of career opportunities for young citizens and an unequal society that is compounded by exuberant house prices.

Spending in the retail sector has been falling, probably exacerbated by the impact the protests are having on tourism. Mainland tourist arrivals have fallen sharply and a lot of luxury brands in particular, with stores in Hong King, are treading carefully, not wanting to upset the mainland market. Hong Kong has been a hugely profitable gateway into the mainland, helped by tax-free price differentials. On the currency front, the Hong Kong dollar has been resilient, with significant removal of capital away from Hong Kong largely absent.

PHI says that the most pertinent issue for its markets is the trade war between the US and China. China has not been ceding ground. A weaker Renminbi exchange rate has helped to counter a higher cost base for its exporters, making exports cheaper to foreign buyers. Ongoing trade tensions are likely to weigh on corporate and consumer confidence across the world. Higher tariffs will raise many end-product prices for consumers in both countries, which will likely dampen demand and reduce trade volumes.

The long-term case for Asia

Ewan believes there is significant potential for positive returns from the Asia Pacific region over the coming years. In the near term, he feels that the recent market noise over trade wars, slowing global growth and a rising US dollar are obscuring the underlying reality of strong, consistent economic growth and social opportunity within the region. PHI’s focus is on investment in individual stocks that will benefit from the economic, social and technological changes in evidence across the region. PHI’s mandate allows it to invest to gain exposure to more than 3bn consumers across Asia. Over the five-year period to 2024, illustrated by Figure 6, the per capita spending power of Chinese consumers is forecast to nearly double in US dollar terms.

Vietnam a likely beneficiary from trade war

Vietnam accounts for around 10% of PHI’s country allocation (see the asset allocation section). This is achieved through eight direct holdings as well as PHI’s holding in the Vietnam Enterprise Investments fund (VEIL), which accounts for 2.6% of the portfolio. Vietnam detracted from PHI’s performance over its most recent financial year (see the ‘performance’ section), reflecting liquidity outflows and reduced appetite for frontier exposure over the period. Over the past six months, sentiment has turned with VEIL’s shares up by over 10%.

The country, which is still classified as a frontier market by MSCI, has positively stood out over recent years, a period that has been very challenging for emerging and frontier markets. At close to $200bn, the market capitalisation of Vietnam’s stock market is higher than a lot of other markets classified as ‘emerging market’ by MSCI.

The 95m population economy is growing pretty briskly, with real GDP annual growth averaging 6.6% over 2014–2018, according to the International Monetary Fund’s World Economic Outlook database. The forecast is for a trend rate of 6.5% to be maintained over 2019–2024.

Around 1m people are entering the workforce each year. In terms of the relationship between the numbers entering versus retiring, ‘peak demographics’ are likely in the mid-2020s. Female participation in the workforce is very high. At less than 40%, the level of urbanisation is low for South-East Asia (as examples, Thailand, Indonesia and China are all above 50%). However, no country in Asia, other than China, is urbanising faster than Vietnam.

As a major global exporter, Vietnam is vulnerable to a slowdown in the global economy, though the trade wars taking place present a huge opportunity to bring manufacturing into the country. This is already happening and is a long-term process. China has been actively ‘moving in’. A report by the Asian Development Bank, released in September 2019, noted that exports from emerging Asia to the US increased by 10% year-on-year over the first half of 2019. This was in spite of Chinese exports declining by 12%. Vietnamese exports increased by 33%, and Vietnam took market share in electronics.

Thematic focus – digitalisation and technology transforming industry

The manager believes that the market’s focus on geopolitics and capital flows can result in it missing the bigger picture, of a global rise in digital penetration, technological change and the rise of the Asian middle class. To the extent that he can, Ewan ignores the noise, focusing on thematic opportunities. He looks for companies that he believes have the potential to increase revenue and earnings at around 15% per annum over a five-year period or longer, and for opportunities where this potential has not been fully recognised by the market.

PHI’s starting premise is how they think the world and individual countries may change over the next three, five and ten years plus, in every area of life – economically, socially and politically – and the impact that technology might have on these trends. When they look at a company and think about what the market size of its industry might be, they ask themselves what the current rate of growth is, how this industry could change, and whether there are additional opportunities for growth in adjacent markets that the company could enter. For example, PHI has a circa 5% allocation to nickel related equities (PHI hasn’t held commodities for years) but the managers see long-term demand for Nickel that is correlated to demand for electric vehicles and batteries as we move to a low-carbon world.

The manager’s feeling is that the rapid development of technology is creating a fundamental change in market behaviour, with digitalisation driving profound changes in economic and political systems, businesses, consumer habits and behaviours. The number of sectors and industries that are becoming digitalised and connected is increasing rapidly. There is growing awareness of these changes across the globe. Artificial Intelligence (AI) is now taken for granted, and the concept of electric rather than gasoline-powered cars is now considered as a commercial inevitability rather than a distant vision.

Asymmetric return profile necessary to find ‘winners’

Ewan says that he is comfortable with the underlying portfolio’s asymmetric return profile. A large tail of negative returns reflects the ‘small-cap bias’. Although this leads to uncertainty at the individual holding level, the manager says that it shows the right kind of risk is being taken. Whilst every effort is made to pick the ‘winners,’ Ewan says that it is very difficult, if not impossible, to have any certainty in this strategy. Early recognition of picks that will not perform is important, though, but, arguably, the biggest risk to this strategy is missing out on a ‘winner’ by sitting on the sidelines.

Ewan cites the example of Sunny Optical Technology, PHI’s largest holding at the beginning of 2019, to highlight how a seemingly robust competitive advantage can be quickly nullified. The company’s shares fell 60% from their peak as the arrival of new algorithms removed a need for precision-lenses in smartphone cameras, posing a considerable threat to margins.

Investment philosophy and process

The underlying approach

Baillie Gifford believes that markets are inefficient at pricing long-term growth, especially over a time horizon of at least three years, and that this creates an opportunity to generate alpha. For this reason, it aims to encourage a culture of long-term thinking within the firm. Baillie Gifford believes there is persistence of good company management, business models and stock prices. This translates into a culture of ‘sticking with the winners’.

The company uses proprietary research. The team undertakes much of this, but will often commission research from local research teams, academics and industry experts. Baillie Gifford also subjects some companies to forensic analysis, using the services of investigative journalists and forensic accountants. When it is talking to companies, the conversations with their management teams focus on the long-term prospects of the business.

All the money is managed from Baillie Gifford’s Edinburgh office. Ewan believes that managing the money this way, rather than having regionally-based teams, helps the team keep a sensible detachment from short-term ‘noise’. Ewan is able to draw on the resources of the whole investment team, when analysing companies, and can sit in on meetings with companies outside his geographic remit. This is especially beneficial when he is trying to identify how his companies compare with competitors domiciled in other markets.

Each member of the team is assigned a geographical focus for research and these responsibilities are rotated every 18 months. Investment ideas are presented to the group, but the lead portfolio manager makes the final decision. Ewan spends four to five weeks visiting Asia each year.

The open-ended investment company (OEIC) and PHI are run in parallel, with some minor exceptions. Whilst Ewan is lead portfolio manager on this fund, he is co-manager of the OEIC with Roderick Snell. This does introduce one small element of differentiation between the two portfolios. More significant differences arise because of the need to keep the OEIC’s portfolio relatively liquid. There is an internal limit of holding no more than 12 days’ volume in any stock across the whole firm, but within this constraint, PHI has greater freedom to hold more illiquid investments than the OEIC. The OEIC has ended up with more of a large-cap bias as a result, while PHI has more exposure to small-cap names. There is considerable commonality of the stocks held, although the individual weightings may differ. PHI, unlike the OEIC, also has the option of using gearing and invests in unlisted companies.

There is a small- to mid-cap bias to PHI’s portfolio. This reflects Ewan’s belief that smaller companies grow faster than larger ones, although they exhibit higher volatility. He also subscribes to the view that smaller companies tend to be less well-researched, which means that they are more likely to be mispriced.

Building the portfolio

With over 6,000 stocks in PHI’s universe and a target portfolio size of between 40 and 120 stocks, Ewan focuses on those that he believes are beneficiaries of positive themes such as demographic shifts or technological change.

Ewan is looking for companies that are capable of growing earnings and cash flow faster than market averages. He wants companies to exhibit some or all of the following qualities: good management teams; barriers to entry; positive cash flow; self-funded growth (he wants to avoid companies that need to keep coming back to the market for cash); and a high return on invested capital (around double the market rate). Companies with ‘blue-sky’ technology are only interesting to him if they are fully funded through to positive cash flow.

The managers do not set target prices for stocks, but Ewan is mindful of valuations. He aims to at least capture a company’s earnings growth on the assumption that the price/earnings (P/E) multiple in five years or so, when he is looking to sell, will be at least as high as it is when he makes the investment. There is an obvious problem if you buy on a high P/E multiple; the business case works out but the P/E multiple declines. As an example of this, Ewan would not buy most consumer staples stocks today because he believes that, in the search for companies with stable revenues, investors have bid up valuation multiples to unsustainable levels.

The research process is flexible and can be carried out quickly if necessary – if there is the opportunity to invest in an initial public offering (IPO), for example. Ewan will typically have met the management before investing, and the investment case will always be discussed internally. In addition, he or a member of the team may have produced a brief report, an internal model, a cash-flow projection and/or an extensive internal research note on the company. He will at times canvass analysts and external research providers for their opinion as well.

Baillie Gifford is an active investor and does not hold stocks just because they are large constituents of any benchmark. Consequently, there are few limits on country, sector or stock weightings imposed on managers. The initial size of a position will reflect the strength of the manager’s belief in the potential risks and rewards of the investment. One of the guiding principles of investing at Baillie Gifford is to ‘run the winners’ (reflecting the belief in the persistency of good business models). However, PHI has a ‘soft’ upper limit of 10% exposure to any one stock. Ewan looks at the shape of the overall portfolio to ensure that he does not have too many companies exposed to similar thematic dynamics.

The mandate allows the manager to use derivatives to control risk and to alter the portfolio’s exposure to markets. In practice, Ewan is not undertaking such activity. The managers have no plans to use hedging to alter the portfolio’s currency exposure.

Sell discipline

Loss of faith in a company’s management is an instant trigger for the sale of a stock. Ewan will also sell if he feels the business model is not working, or if the market has caught up with his expectations.

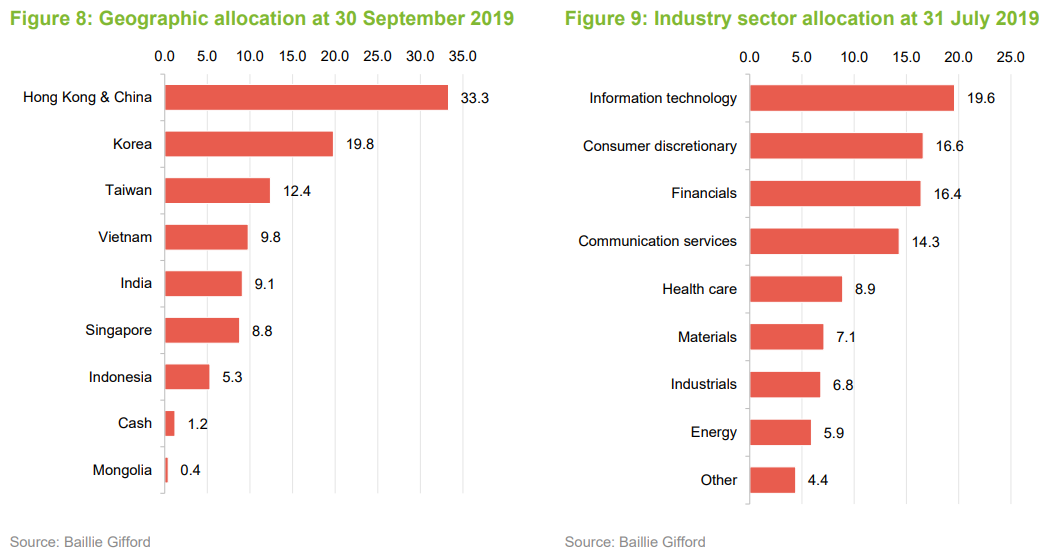

Asset allocation

At the end of September 2019, there were 82 holdings in the portfolio. PHI believes that it can achieve an appropriate level of diversification for its strategy by holding 40-120 companies.

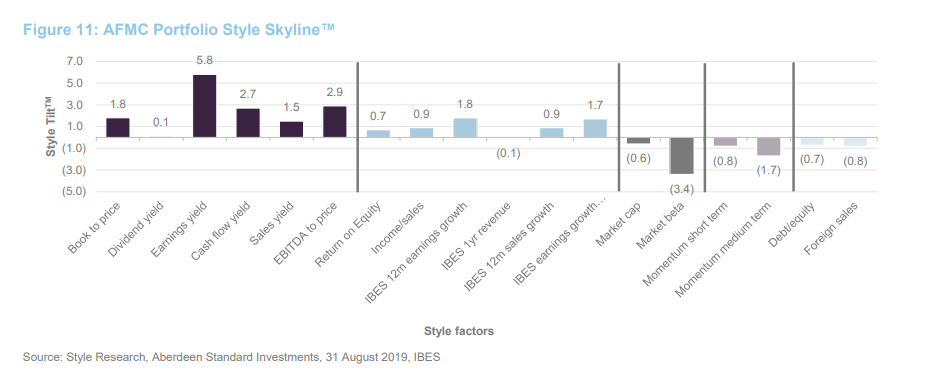

Reflecting its growth bias against the MSCI AC Asia ex Japan Index, Ewan notes that historic earnings growth from current holdings is 18.0%, with one-year forecast growth at 33.1%, compared to 10.7% and 8.5% for the Index. The portfolio’s estimated price-to-earnings ratio for the current year is 18.7x versus 13.2x for the index. The manager is comfortable holding higher value companies based on their growth potential.

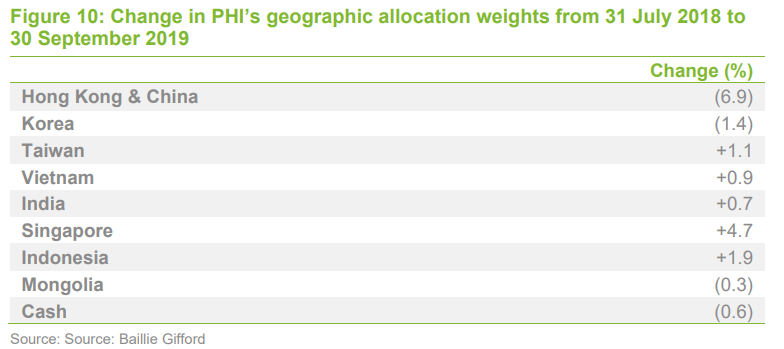

Ewan has reduced the allocation to technology since our last note in November 2018. After peaking at around 52%, technology was down to a re-stated level of 31.5% at 31 July 2019. The re-statement reflected re-classifications made by MSCI, which resulted in some holdings moving from information technology into other sectors, predominantly communication services. PHI’s largest current holding, Singapore-based SEA Limited, was among the companies re-classified to communication services.

Compared to the index, the portfolio has lower exposure to the combination of China and Hong Kong and higher exposure to Vietnam (which is not a constituent country within the Index). Ewan says that the portfolio’s exposure to Korea and Taiwan is dominated by biotech and technology hardware companies, respectively.

Consumer discretionary is the second-largest sector exposure at 16.6%, compared to 20.5% in the previous year. Ewan says that as economic growth within the region recovers, the focus on the Asian consumer should lead to increased interest from investors.

Financials represent the third largest sector weighting at 16.4%. Ewan sold out of Mumbai-based IndusInd Bank after it had performed well over several years.

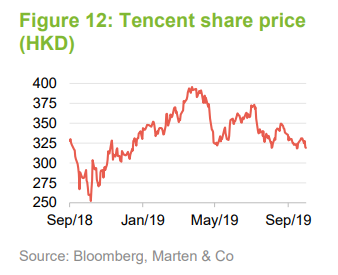

Technology – Reduced role for Alibaba and Tencent

At its peak, Tencent accounted for 12% of PHI’s total assets – it has since fallen to 2.9%. Alibaba’s weighting has not changed as significantly. It is now at 5.1%, down from 6.9% in July 2017. Ewan further reduced the allocation to Tencent over the past year, mainly reflecting concerns that its previous leadership in the WeChat social platform was under threat from ByteDance, while the allocation to Alibaba was broadly maintained over the year.

In QuotedData’s last note, we discussed the marked downward shift in the proportional investments into Alibaba and Tencent. Ewan says that the long-term success of these companies would depend on how their businesses evolve. Just as they disrupted entire industries, they are at risk of being disrupted themselves.

To illustrate the point, the manager says that Tencent and Baidu (sold in 2018) have found that their previously dominant online advertising business have been successfully attacked by new companies. In four years, TikTok went from accounting for less than 2% of China’s social/media advertising budget to 40%-plus this year, surpassing Tencent in this sphere.

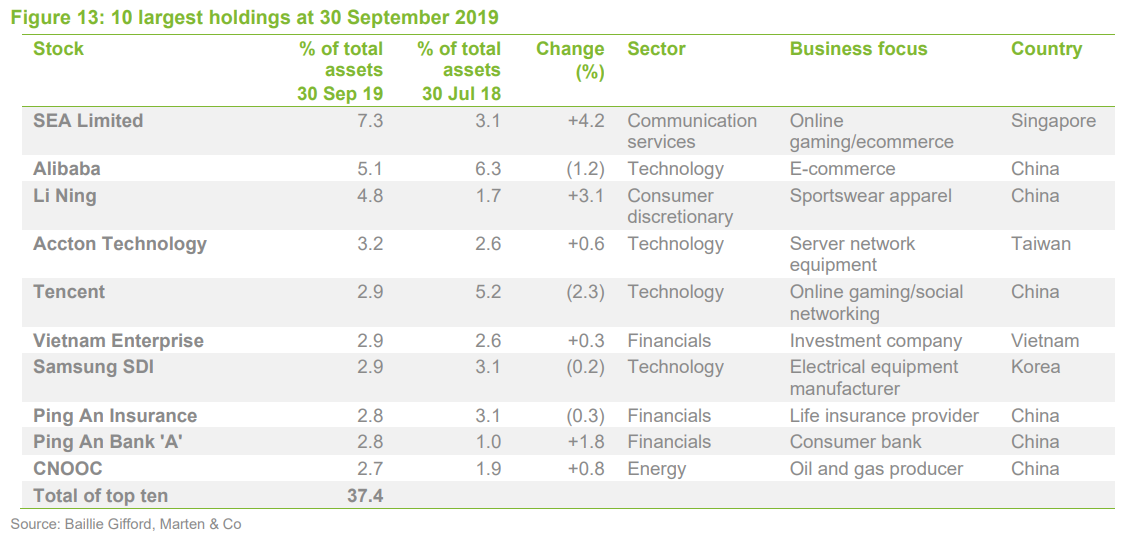

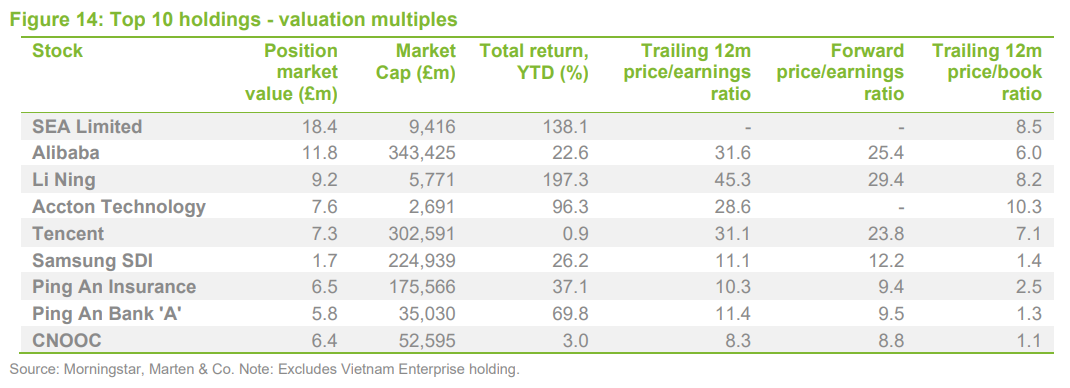

Top 10 holdings – Manager’s 2018 have taken over the mantle

Figure 13 shows PHI’s 10 largest investments at 30 September 2019. There are four additions to the top 10 since our last note: Li Ning, Accton Technology, Ping An Bank ‘A’ and CNOOC. They replace Sunny Optical (China – Optical products), Koh Young Technology (Korea – 3D optical sensors), Geely Automobile (China – car manufacturer) and JD.com (China – online sales).

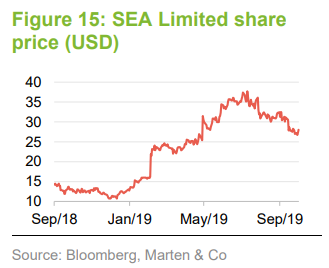

SEA Limited

Based in Singapore, SEA Limited (SEA) (seagroup.com) has usurped Alibaba, Tencent and Sunny Optical (see page 7 in the attached PDF) as the largest holding. Ewan added the company in 2018. SEA is one of South-East Asia’s leading companies in gaming and online e-commerce. It remains an independent company, though it is significantly backed by Tencent. As of 22 October 2019, the shares are up by nearly 140% over the year-to-date. PHI believes that SEA’s markets can potentially grow exponentially over the next 10 years.

Over the course of the trust’s last financial year, SEA launched a new hit game, Free Fire, which took off, quickly reaching 450m downloads and 50m daily active users. PHI says that the game is likely to deliver close to a $1bn of revenue for it in 2019. This has been the catalyst that has driven the share price upwards.

Li Ning

Also added in 2018, Li Ning’s (lining.com) share price has more than tripled over the year-to-date – it is now PHI’s third largest holding. The company is China’s leading domestic branded sportswear retailer. The holding reflects the manager’s belief in the consumer opportunity. Younger Chinese consumers are increasingly turning to fashion to show their individualism, bringing opportunity for manufacturers and retailers in tune to the market, in areas such as athleisure. Li Ning represents a new breed of Chinese company with the brand power to charge higher prices, tapping into the premiumisation trend.

As well as the power of its own brand, the company appears to be benefitting from the US/China trade war, with tariffs potentially posing a threat to Nike’s market-leading position in China. Elsewhere, Li Ning has been further boosted after it sided with China in its recent quarrel with the National Basketball Association (NBA) after the general manager of the Houston Rockets, Daryl Morey, expressed sympathy for the protests in Hong Kong in a tweet. Li Ning is said to no longer be affiliating itself with the Houston Rockets.

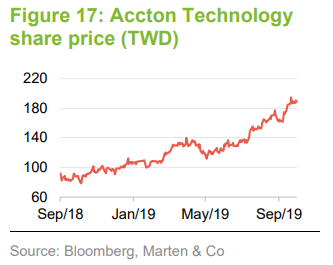

Accton Technology

Taiwan’s Accton Technology (accton.com) is another relatively new addition to the portfolio, which has been performing extremely well. The company researches and manufactures computer network systems. It is a leading supplier of hardware into US data centre companies, where it has worked with Facebook and Amazon. The company is also looking to sell to telecoms companies when they introduce 5G networks.

Elsewhere in the portfolio

Ewan expects there to be plenty of growth ahead in e-commerce across his target markets – he pointed to Indonesia in particular as an opportunity. Software as a service (SAS) is another focus area. PHI owns China-based Kingdee International Software; Ewan says the company is somewhat comparable to Adobe in the US and the industry has an attractive margin profile (at around 20%). Elsewhere in technology, the manager introduced Mitac, a Taiwan-based 5G and ‘internet of things’-focused company.

Finally, in healthcare, the manager bought the Chinese biotech company Zai Lab, with the conviction that it could be a biotech leader within the next five or so years.

New additions to the consumer discretionary bucket included Korea’s Cowell Fashion ‘J-Store’, which is UK-listed but Asia-focused.

Spare capacity for unlisted investments

With ever-increasing access to private capital, companies are staying private for longer and, in many cases, not seeing public listings as an end-goal. In 2018, PHI’s shareholders gave the manager a mandate to invest up to 10% of total assets (calculated at the initial investment point) in unlisted companies. At the time, the portfolio had four unlisted investments, representing 1.6% of total assets. Over the course of the July 2019 year-end, no new unlisted investments were made, whilst one existing holding, NIO, the Chinese electric vehicle developer and manufacturer, listed on the New York Stock Exchange. The other three holdings are:

- Philtown Properties (0.0% of total assets at 30 September 2019), a holding inherited following its spin-out from RFM Corp of the Philippines in 2009.

- JHL Biotech (0.4%), a Taiwanese biotech which was taken private with a view to listing in Hong Kong.

- JHL Biotech Convertible Bond (0.9%) issued as part of its de-listing.

Performance

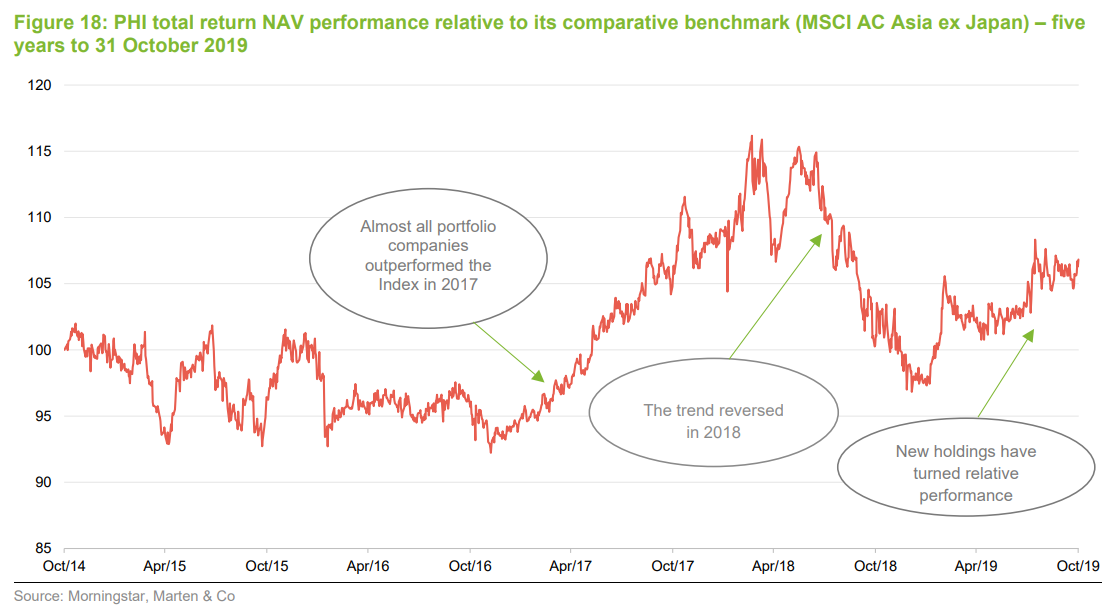

Though PHI is a highly active stock picking fund, performance relative to its benchmark is important – a potential tender offer over 2019, which did not take place, was contingent on relative performance over a three-year period (see the premium/discount section). Since Ewan took over the portfolio on 18 March 2014, total return NAV has increased by nearly 87% to 31 October 2019. PHI outperformed the index over this period, as well as over three and five years.

PHI has been outperforming the index over the year-to-date, pushed on by the SEA Limited and Li Ning holdings. The previous two calendar years were up and down. The manager notes that nearly all holdings outperformed in 2017, before a total reversal in 2018. Many holdings that had previously done very well, were severely affected by global trade wars, a liquidity crunch and technology in transition.

The manager says that, in hindsight, the trust was late in selling several previous winners, including Sunny Optical Technology and China’s Geely Automobile.

Performance attribution – 2018 portfolio moves bearing fruit

Geographically, South Korea was PHI’s worst-performing market over the year to July 2019, falling 20% and detracting 4.5% from the portfolio’s overall performance. Ewan said that trade disputes with China and Japan, weak semiconductor and smartphone sales and negative sentiment towards biotech companies all contributed to performance. Vietnam also detracted, though sentiment has been improving (see the ‘market roundup section’).

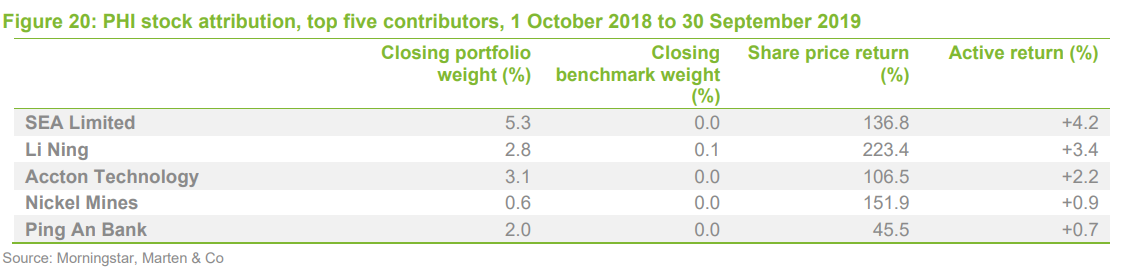

2018 was a year of change for PHI. The manager says that the top five positive contributors to relative returns versus the comparative index over the most recent financial year were all stocks that had either been bought (SEA Limited, Li Ning, Accton Technology, Ping An Bank) or sold (Baidu) in the prior financial year.

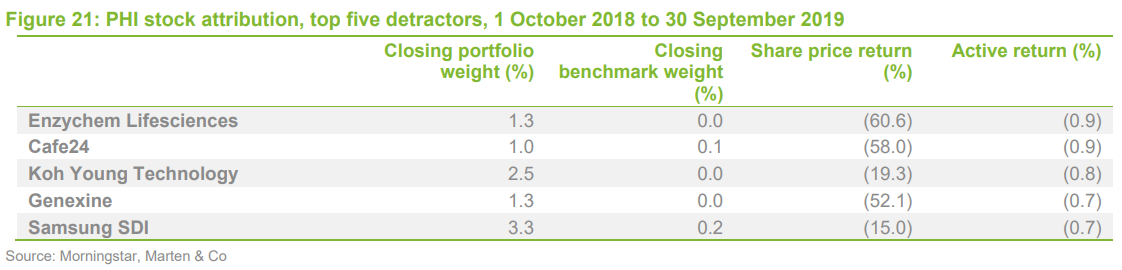

Figures 20 and 21 below list the relative company outperformers and detractors against the comparative index over the one-year period beginning 1 October 2018. Over this period, PHI’s total return NAV outperformed the MSCI AC Asia ex Japan Index by 1.4%, from which the manager’s stock selection contributed 4.2% to active returns and sector allocation detracted from returns by (2.9%). Healthcare was the largest sector detractor.

SEA Limited, Li Ning and Accton Technology contributed a combined +9.8% to PHI’s NAV over the year beginning 1 October 2018.

All five stock detractors were Korea-based. The presence of the healthcare companies Enzychem Lifesciences and Genexine reflected the poor sentiment towards the sector. Ewan’s view of Cafe24 remains constructive. It provides a platform for small firms to transact on its e-commerce platform, with a business model that is somewhat comparable to Shopify in the US.

Peer-group comparison

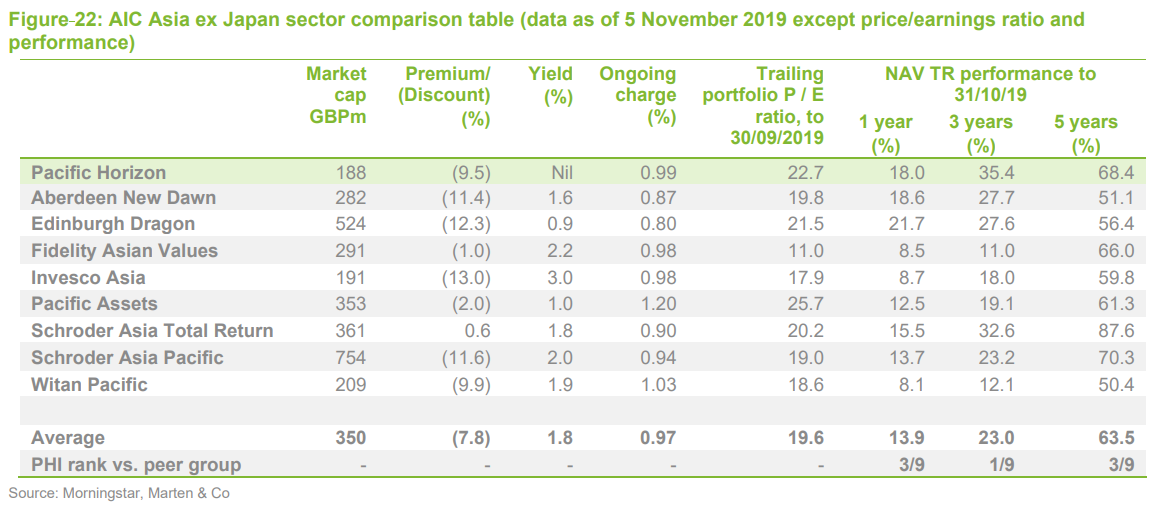

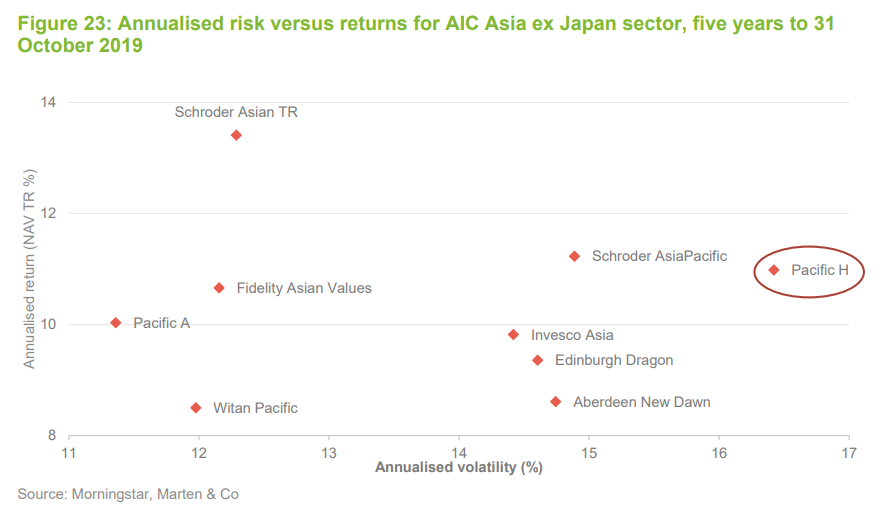

The peer group that we have used for the purposes of this note comprises all the funds in the AIC’s Asia ex Japan sector. As a group, the average total return NAV of sector has increased by 11% over the year-to-date (to end-September). With respect to performance, looking at periods ended 31 October 2019, PHI ranks third out of nine over five years, first over three years, and third over one year. Over the year-to-date (to end-October), PHI ranks first.

PHI is one of the smallest funds in the sector, but this is not reflected in its ongoing charges ratio which is equal to the sector average. PHI is trading at a discount that is wider than the sector average, having most recently traded at a premium over the summer of 2019. If sentiment towards this area improves, the discount could be narrow once more, with PHI potentially trading at a premium again.

Figure 23 looks at risk-adjusted returns for the sector over the past five years. Cumulatively over three and five years, PHI has been among the strongest three performers – recent performance has not been as good, reflecting the portfolio’s underperformance in 2018. PHI had the highest level of volatility over the five years, reflecting an investment approach geared around identifying ‘winners.’

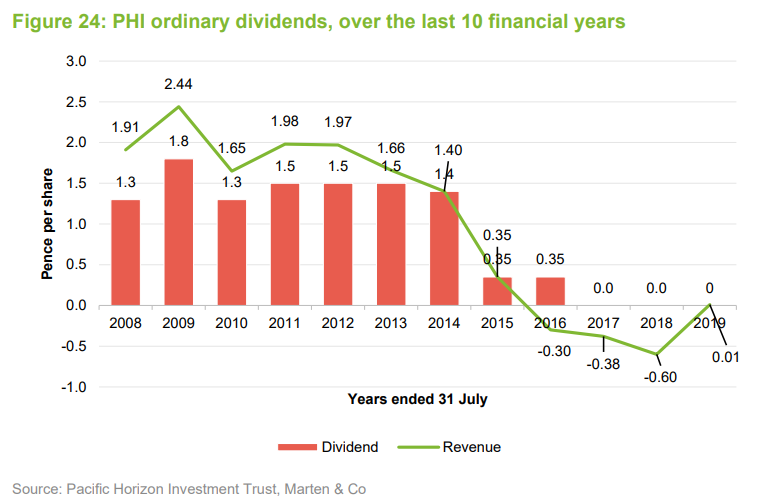

Dividend

For the third financial year in succession, PHI has not declared a dividend. PHI generated a small revenue surplus of 0.01p per share for the year ended 31 July 2019 (2018: a deficit of 0.60p per share). PHI’s primary objective is to generate capital growth and the board’s policy is that any dividend payable in the future will be determined as being the minimum permissible in order to maintain PHI’s investment trust status. This would be paid by way of one final payment per year.

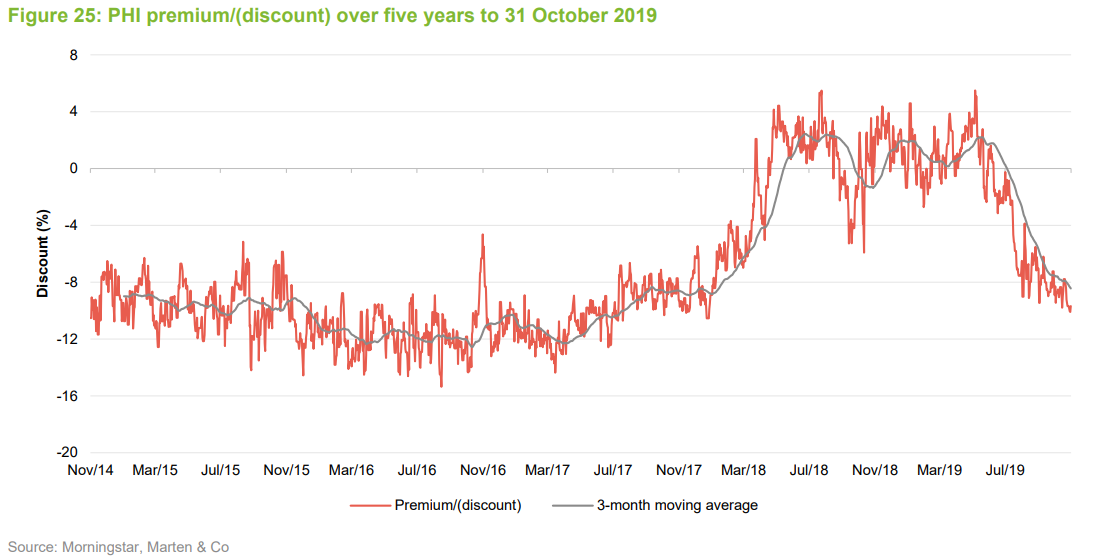

Premium/(discount)

Over the 12-month period to 31 October 2019, PHI’s shares traded between a (10.1%) discount to NAV and a 5.5% premium. The discount has widened since the summer months, reflecting increased risk aversion.

PHI has authority to repurchase up to 14.99% of its issued share capital, as well as to issue up to 10% at a premium to NAV. These authorities give the board mechanisms through which it can manage PHI’s discount or moderate any premium that should arise. Shares repurchased can be held in treasury and reissued by the company to meet demand. Any reissue of treasury shares would only be undertaken at a premium to NAV.

Tender offer off the table as PHI outperforms comparative Index

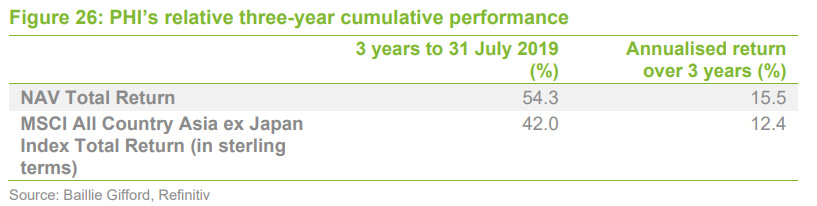

A potential tender offer for up to 25% of PHI’s share capital in 2019, which was approved at the AGM in 2018, will not take place after the trust outperformed its comparative Index (the MSCI All Country Asia ex Japan Index in sterling terms) by more than the requisite level.

The tender was contingent on the trust’s NAV total return failing to exceed the total return of its comparative Index by at least 1% per annum over a three-year period to 31 July 2019 on a cumulative basis. PHI outperformed the Index by 3.1%.

The board met with a number of the trust’s larger shareholders over the summer months, concluding that PHI’s satisfactory longer-term performance meant it would not be in the company’s interests to facilitate another tender process. In the event of underperformance, shareholders will be able to vote on the trust’s continuation as part of the 2021 AGM.

Fees and costs

Baillie Gifford & Co Limited acts as PHI’s alternative investment fund manager and has delegated portfolio management services to Baillie Gifford & Co. PHI’s management fee is calculated on a tiered basis. With effect from 1 January 2019, the annual management fee is 0.75% on the first £50m of net assets, 0.65% on the next £200m of net assets and 0.55% on the remaining net assets. In the periods before 1 January 2019 covered by this report, the fee was 0.95% on the first £50m of net assets, 0.65% on the next £200m of net assets and 0.55% on the remaining net assets.

Management fees are calculated and paid quarterly in arrears and there is no performance fee. The managers may terminate the management agreement on six months’ notice and the company may terminate it on three months’ notice.

The ongoing charges ratio for the accounting year ended 31 July 2019 was 0.99%, down from 1.02% in the prior accounting year, and 1.07% the year before that. Baillie Gifford & Co Limited also provides company secretarial services. These services are included as part of the management agreement.

Capital structure and trust life

PHI has a simple capital structure with just one class of ordinary share in issue. There were 58,990,282 ordinary shares in issue as of 29 October 2019. Each year, the company takes powers to buy back up to 14.99% of its shares at a discount to NAV. It also asks for permission to issue up to 10% of its issued share capital at a premium to NAV.

Over the course of the most recent financial year-end, PHI was able to issue 700k shares (representing 1.2% of the shares in issue on 1 July 2018) at a premium to NAV, when demand could not be satisfied from existing shareholders. By issuing shares at a premium, PHI was able to improve liquidity in the trust’s shares and while also providing a boost to the NAV. Increasing the trust’s size also has the effect of reducing ongoing charges, as fixed costs are spread over a wider base.

Shareholders are given the opportunity to vote on the continuation of the company every five years. The next vote will be at the annual general meeting of the company, to be held in 2021.

PHI’s year-end is 31 July. It holds its AGMs in October or November and, where applicable, pays its annual dividend shortly thereafter.

Gearing

Gearing parameters are set by the board and the manager operates within these. As of 31 July 2019, the range was set at -15% (i.e. a net cash position) to +10%. PHI’s net gearing was 8.9% as at the end of September 2019, compared to 8.3% and 7.9% at the financial year-end and beginning, respectively.

PHI has a £30m multi-currency revolving credit facility with The Royal Bank of Scotland Plc, of which £20m was drawn (split between GBP and USD) at 31 July 2019.

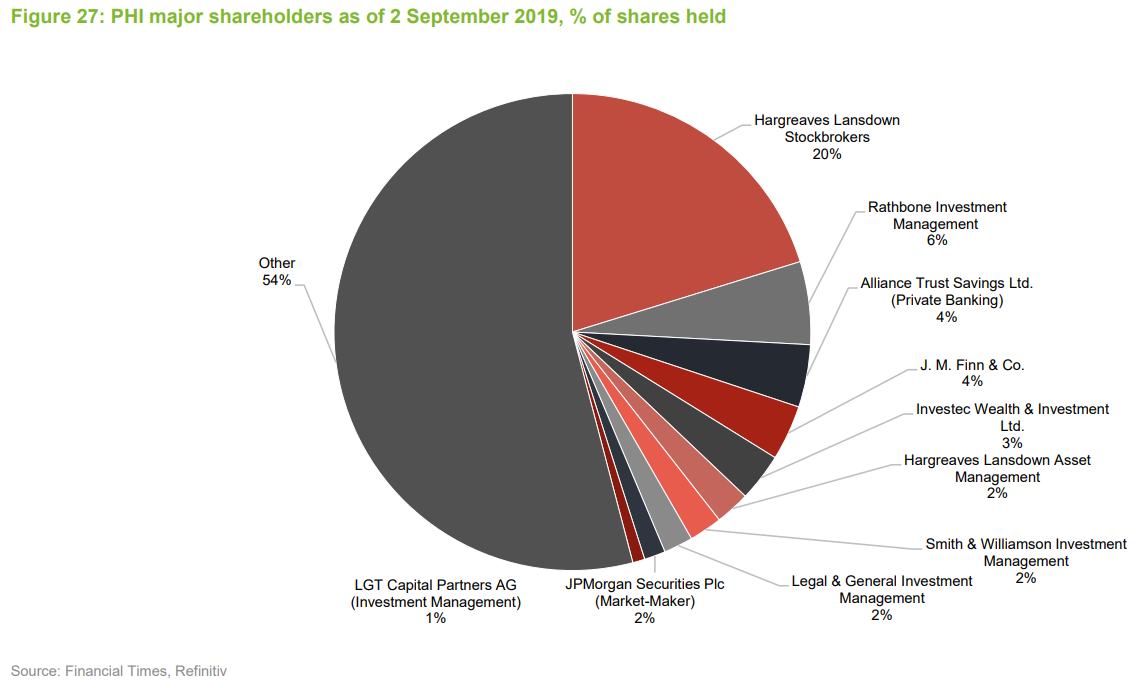

Major shareholders

Figure 27 shows PHI’s major shareholders, as of 2 September 2019.

Board

All of the directors are non-executive, considered to be independent of the investment manager and do not sit together on other boards. The directors put themselves forward for re-election at the first AGM following their appointment. Thereafter, directors submit themselves for re-election every three years. Jean Matterson, who became chairman of the company in October 2010, will be retiring from the board at the conclusion of this year’s AGM. Angus Macpherson will become the chairman of PHI’s board following Jean’s retirement.

Figure 28 includes Angela Lane, who was appointed on 1 October 2018 and whose appointment was ratified by shareholders at the AGM on 6 November 2018. It also includes Joe Studwell, who was appointed on 9 November 2018 – his appointment will fall for ratification at this year’s AGM on 12 November 2019.

There is a limit of £150,000 for the aggregate of fees paid to directors, which forms part of the company’s articles of association. Shareholders would have to vote to approve any change in this limit.

Angus Macpherson (forthcoming chairman)

Angus Macpherson was appointed to the board of directors in 2017. He was based in Asia between 1995 and 2004 in Singapore and Hong Kong, most recently as head of capital markets and financing for Merrill Lynch for Asia. Currently, Angus is chief executive of Noble and Company (UK) Limited, an independent Scottish corporate finance business. He is also currently chairman of Henderson Diversified Income Trust Plc and is the former chairman of JP Morgan Elect Plc.

Edward Creasy (audit committee chair and senior independent director)

Edward Creasy was appointed as a director in 2010. He chairs the audit committee and is the senior independent director on the board. His professional curriculum vitae includes serving as the former chief executive officer of Kiln Plc, a non-life insurer quoted on the London Stock Exchange until its acquisition by Tokio Marine Nichido Fire Insurance Company in 2008. Until January 2011 he was chairman of Kiln Group and chairman of RJ Kiln & Co. Limited. Edward’s other engagement include roles as chairman of Charles Taylor Plc, deputy chairman of W.R. Berkley Syndicate Management Limited and he is also a member of Lloyd’s of London’s supervisory and review committee.

Jean Matterson (retiring chairman)

Jean Matterson was appointed as a director in 2003 and has served as chairman of the board since 2010. She is also chair of the nomination committee. Her professional experience includes a partner position with Rossie House Investment Management, which specialises in private client portfolio management with a particular emphasis on investment trusts. Jean previously spent 20 years with Stewart Ivory & Co, as an investment manager and a director. She also holds directorships with BlackRock Throgmorton Trust Plc, Capital Gearing Trust Plc, Herald Investment Management Limited and HIML Holdings Limited.

Angela Lane (director)

Angela Lane was appointed as a director on 1 October 2018. She is a qualified accountant and has held several non-executive and advisory roles for small and medium capitalised companies across a range of industries. She also holds the role of non-executive chairman of Huntswood CTC, and non-executive directorships at Sherborne Schools Worldwide and Dunedin Enterprise Investment Trust Plc, where she is also chairman of its audit committee.

Joe Studwell (director)

Richard Frank (‘Joe’) Studwell is the most recent appointee to the board (November 2018). He has spent 25 years working in East Asia as a journalist, independent researcher at Dragonomics and author under the name of Joe Studwell. His published works include Asian Godfathers: Money and Power in Hong Kong and South East Asia and How Asia Works: Success and Failure in the World’s Most Dynamic Region.

Previous publications

Readers interested in further information about PHI may wish to read our previous notes (details are provided below).

- Invest in Asian growth – Initiation note – 21 March 2016

- Brave new world – Update note – 10 October 2016

- Top of the pops! – Annual overview note – 30 October 2017

- Pause for breath? – Annual overview note – 8 November 2018

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Pacific Horizon Investment Trust.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.