Downing Renewables and Infrastructure Trust says that its NAV for 30 September 2022 rose by 1.5p over the previous three months to 117.7p. The total return for the period, including the 1.25p dividend paid in the period, was 2.6%. The movement in NAV during the period was attributable to several factors:

- financial performance (+1.3pps);

- advantageous fixed pricing arrangements and power price forecasts (+1.6pps);

- foreign currency exchange movements (+4.3pps);

- higher than forecast inflation for the period (future inflation assumptions remain unchanged) (+0.8pps);

- increased discount rates across the portfolio (-4.7pps); and

- other movements including dividend (-1.5pps).

Discount rates

Discount rates used to value the company’s future cash flows when calculating the NAV were increased by 0.5% to 8.0% for the operational levered UK solar and Swedish hydropower portfolios and by 0.3% to 6.3% for the unlevered Swedish wind farm during the period, resulting in an overall increase of the portfolio discount rate to 7.7% from 7.2% and a reduction in the value of the portfolio of £8.7m. The statement says that all of the acquisitions it made in 2022 were accretive to NAV and were made on the basis of base case returns above the revised portfolio discount rates. It feels the same about the projects in its pipeline.

No impact from UK Electricity Generator Levy and EU Price Cap

On 17 November 2022, the UK government announced the introduction of a new levy on excess profits produced by electricity generators. The annual generation forecast for the company’s UK portfolio is below the proposed threshold of 100GWh and therefore it falls outside of the scope of the UK government’s proposed electricity generator levy.

The company’s northern European portfolio is exposed to electricity markets with average prices materially lower than those of central and southern Europe and the UK. Downing Renewables’ price forecasts for its European portfolio fall below €180/MWh from 1 January 2023 and so to the extent that the EU price cap is introduced by the Swedish Government at this level (and the plants do not fall within the various exemptions applicable to hydropower installations), this will have an immaterial impact on the NAV, if any.

Performance

Financial performance of the portfolio for the period was above expectations and contributed £2.4m of the NAV uplift, equivalent to 1.3pps. Solar generation was slightly above budget. Revenue and operating profit from this part of the portfolio were both about 9% above budget.

Operating profit in the wind portfolio was slightly above expectations, supported by strong wind speeds and good levels of availability.

Generation across the hydro portfolio was below budget, mainly driven by low levels of precipitation. However, operating profit was about 30% above budget, with high power prices offsetting low levels of generation.

Power prices and inflation

Medium to long term inflation forecasts were unchanged from June 2022 at 2.75% for the UK in 2023 and 3% thereafter to 2030 and 2% for Sweden from 2023 onwards.

The increase in forecast future power prices and impact of entering into advantageous fixed price arrangements contributed £2.9m (1.6pps) of the NAV uplift.

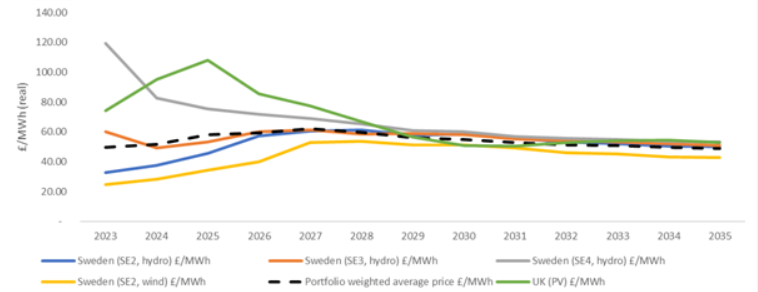

The power price forecasts used in the valuation are set out below in GBP. Where prices are in Euro they are converted back to GBP for the purposes of comparison.

Portfolio update

In line with the original investment case, on 7 October 2022 Downing Renewables repaid the mezzanine debt that was present in the UK solar portfolio when it was bought in 2021. This helps de-risk this part of the portfolio, increases the solar weighting to about 25% of NAV, and cuts overall gearing. After prepayment of the mezzanine debt, gearing across the portfolio stands at 30%.

On 23 November 2022, DORE completed an additional accretive acquisition; that of a 14 GWh hydropower portfolio of seven assets with significant reservoir capacity in Sweden. Six of the sites are located in SE3, and one in SE2. The total investment amount was about £6m and the acquisition increases the hydropower portfolio to 26 plants. The acquisition has been funded on an ungeared basis.

Following the repayment of amounts outstanding under the revolving credit facility in June 2022, the repayment of the mezzanine debt in October 2022 and the most recent hydro acquisition, the company holds cash of £28m, or 13% of NAV.

DORE : No windfall tax hit for Downing Renewables