News

- Home

- QD view – The inflation trade – an early Christmas present?

2022 has been a tough old year, with investors being visited by their own kind of Ghost of Christmas Past. One whose name is inflation, a long-forgotten spectre.

2022 has seen, for some countries, a truly parabolic growth rate of inflation. While pundits had predicted that the post-COVID rebound in activity would be a possible driver, none could have predicted the sudden and brutal war in the Ukraine. A war which sent energy prices skyrocketing and put a strangle on the world grain supply (a major contributor to the rising cost of food). Even without the war, 2022 saw us contend with supply chain bottle necks, China’s draconian COVID-19 response, tight labour markets across the US and UK, and in many countries the impact of an increasingly strong dollar, all of which added to global inflation.

The fight against inflation, as we all know, leads to rising interest rates, with central banks doing their best to try to engineer a ‘soft landing’, ideally curtailing the rapid increase in inflation without tanking their economies in the process. Rising rates lead to, almost without exception, lower asset valuations, as they lead to a rising discount rate which asset valuations are based on.

Yet investors may have received an early Christmas present, with an opportunity to tap into the ‘peak-inflation’ trade. US annual inflation figures have fallen month-on-month since their September peak and, here in the UK, the CPI eased slightly in November. This suggests that, hopefully, much of the pain of rising rates has now been priced into asset values, as declining inflation suggests that monetary policy is (hopefully) working.

The question is, have the downside risks finally yielded to the upside potential of lower discount rates? (this is especially pertinent for stocks in the highly valued growth sector, which was hit hardest by rising rate expectations), or are the current risks still too great to be able to call the bottom of the market? This is a topic our analysts intend to debate in this article.

David Johnson (DJ): Inflation is, for reasons good and bad, a far less terrifying thought than it was at the start of the year, and what matters more than anything is the expectation of future inflation, as it is through such factors that interest expectations are formed. The implication is that, if we are past the inflation peak, then interest rate expectations should begin to dampen, as less aggressive monetary policy is needed to curtail future inflation.

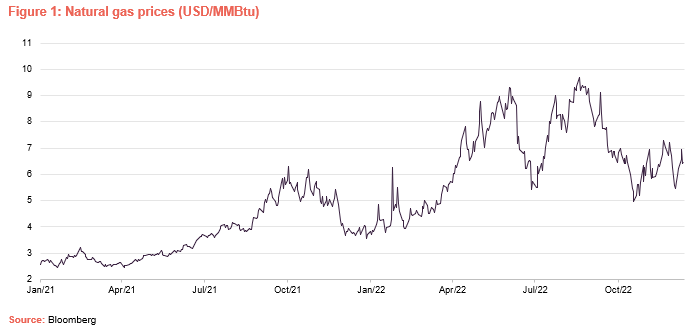

But why would we be past peak inflation? The most obvious factor is that the energy-crisis seems to have subsided somewhat, as advanced economies have made sufficient adjustments to ensure that supply is not materially disrupted over the winter. Natural gas prices have fallen sharply as economies adapt their consumption and storage policies to the recent supply reductions. As can be seen by Figure 1, natural gas prices are back down to their ‘post-COVID’ peak – a level seen in October 2021 when the world was in the blissful grip of post-lockdown consumption.

While bill payers everywhere should breathe a sigh of relief, it is the Europeans who will be the most relieved, as they were not only faced with higher natural gas prices but also practical restrictions in their supply. Could this be a turning point for trusts such as Montanaro European Smaller Companies (MTE), which is 37% off its September 2021 peak, largely as its growth-focused portfolio de-rated.

James Carthew (JC): I fear that David’s optimism about an end to the squeeze on gas prices may be overoptimistic. Recent weakness seemed to me to be more a product of full storage ahead of winter demand and unusual warm weather in Europe. If we fast forward a few months, the picture may look quite different. That bodes well for Gulf Investment Fund (GIF), which although it doesn’t have direct natural gas production exposure, will benefit from a buoyant Qatari economy and its stake in Qatar Gas Transport.

DJ: The country that one could argue is past the highest peak is the UK. Not only does it benefit from a fall in energy prices, but it also has the unfortunate benefit of having a recession combined with fiscal tightening. Both of these are powerful deflationary forces, as they reduce the level of economic activity in the UK, directly constricting the demand for money. This could be associated with weak sterling, which flatters a large portion of the UK equity market that derives most of its revenue from overseas.

There are signs that a UK recession may be more of a pin prick than a car crash, with investment manager David Smith, manager of the UK-focused Henderson High Income Trust (HHI), highlighting that a forthcoming recession is likely to be a mild one (i.e. a loss of c.1% GDP per annum) thanks to a strong UK consumer, tight labour market, and robust corporate balance sheets. Reflecting the strength of his conviction, David has gone as far as to increase HHI’s allocation to miss-valued UK cyclicals as a result, though HHI’s value tilt has already seen it generate an attractive, positive, 12-month NAV return.

Even prior to 2022, the UK was one of the cheapest developed markets, with the Brexit-discount weighing heavily on company valuations. Nevertheless, it can boast many high-growth companies of the type that were once the darlings of the market. One great example of a fund focused in this area is BlackRock Throgmorton Investment Trust (THRG), a high-growth mid-and-small-cap strategy which prior to the start of 2022 was the best-performing UK small and mid-cap trust. THRG’s manager, Dan Whitestone, raises a strong argument behind growth investing in the current environment; that well-run, good-quality, high-growth companies, are less exposed to the impact of rising interest rates and recession, and their business models can continue to capture disruptive sectoral trends unabated.

JC: I like THRG too but more for its portfolio’s ability to weather the recessionary storm than as a bet on falling UK interest rates. The Bank of England is still keen to stress its hawkish tendencies. The proliferation of strike action suggests a real pressure on employers to raise wages, which may help entrench inflation. I cannot see a return to last year’s very low interest rates any time soon.

Value players, funds such as Temple Bar (TMPL), stress the attractions of their strategy in this environment. The key to their success will be sidestepping value traps – companies that look cheap but are cheap for very good reasons. One thing I am keen to see play out in 2023 is how the banking sector fares. Higher rates are boosting net interest margins, but fears of higher debt defaults are weighing on share prices. Polar Capital Global Financials’ (PCFT) managers think that these concerns are overdone.

DJ: Ultimately, the inflationary elephant in the room is the US, as whatever happens in Europe, the UK, or elsewhere, the overwhelming factor in determining the potential of the ‘peak inflation’ trade is the views of the Federal Reserve around the trajectory of US inflation. In my mind, while the Europe and the UK could be described as ‘cost-push’ inflation – driven primarily by the rise of input costs – the US is ‘demand-pull’. With a robust economy, generous fiscal expenditure, a strong consumer, and the aftermath of a post-COVID bounce in consumption, it is clear that America’s inflation is more driven by higher consumption than it is in Europe.

This is not to say that it hasn’t felt the heat from rising energy prices, with the US’s car-heavy society meaning that their consumers felt the pinch at the gas pumps. Biden’s Inflation Reduction Act is designed to reduce US inflation in the long term by reducing the economic exposure to volatile fossil fuel prices, while also reducing the deficit.

US gas prices are dropping and are approaching $3 a gallon, a psychological break point, well below the $5 peak they hit during the energy price crunch. The New York Federal Reserve (which is not the rate-setting body), has reported a fall in consumer inflation expectations, with the median one-, three-, and five-year-ahead expectations decreasing to 5.2 percent, 3.0 percent, and 2.3 percent, respectively; compared to the 7.1% annualised figure printed in November. Which itself was down from October’s 7.7% level.

JC: North American Income Trust (NAIT) has been the North American sector’s success story this year. Its manager is relatively upbeat as he looks to the trust’s healthy income account. In the absence of a return to a more risk on mindset, income may be an important part of investors’ returns next year. Notwithstanding an easing of headline inflation figures, Jerome Powell’s comments after the latest 0.5% hike in US rates put paid to any notion that the inflation monster has been slain. He said “it’s good to see progress, but let’s just understand we have a long way to go to get back to price stability”.