Bargain hunting

After a strong run of both absolute and relative performance (see

page 16), AVI Global Trust (AGT) faces twin headwinds of widening discounts within its underlying portfolio – as holdings’ share prices move further below their underlying net asset value – and a widening discount on its own shares.

The manager has been cautious on markets, eliminating the trust’s gearing (borrowing) at the end of 2021. That gives it the firepower to take advantage of some of the bargains being thrown up by current events. The manager believes that when markets settle, discounts will start to narrow again to AGT’s benefit.

Our note describes AGT’s investment process, how it is invested currently, and goes into more detail on some of the larger holdings within the portfolio.

Extracting value from discounted opportunities

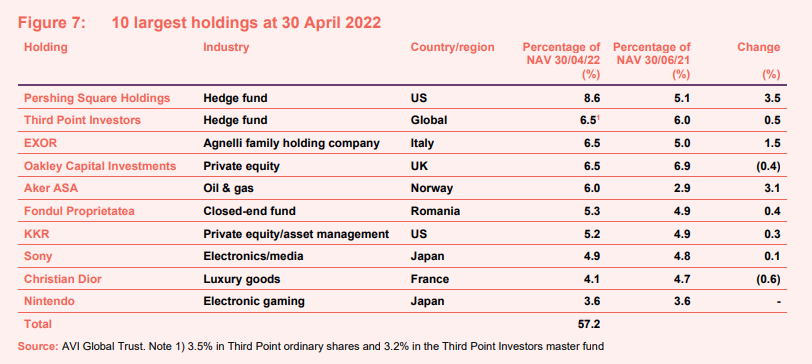

AGT aims to achieve capital growth through a focused portfolio of investments, particularly in companies whose shares stand at a discount to estimated underlying net asset value. It invests in quality assets held through unconventional structures that tend to attract discounts; these types of companies include holding companies, closed-end funds, and asset-backed special situations.

Fund profile

Hear about the fund:

AGT aims to achieve capital growth through a focused portfolio of investments, particularly in companies whose shares stand at a discount to estimated underlying net asset value. It invests in quality assets held through unconventional structures that tend to attract discounts; these types of companies include family-controlled holding companies, closed-end funds, and asset-backed special situations such as asset-rich Japanese operating companies.

For performance measurement purposes, the company compares itself to the MSCI All Country World ex-US Total Return Index, expressed in sterling terms. Whilst it has some US exposure, relative to an unconstrained global index, the trust has a sizeable underweight exposure to the US, primarily because there are fewer opportunities to invest in family-controlled holding companies in that market.

AGT’s AIFM is Asset Value Investors (AVI). AVI was established in 1985, when the trust’s current approach to investment was adopted. At that time, AGT had assets of just £6m and was known as the British Empire Securities and General Trust, later shortened to British Empire Trust. The trust adopted its current name on 24 May 2019.

The manager

Hear about the manager:

Fund Manager Brief: Joe Bauernfreund, Asset Value Investors (AVI)

Since October 2015, the lead manager on the trust has been Joe Bauernfreund, chief executive officer and chief investment officer of AVI. Joe has over 24 years’ experience in the finance industry. After six years working for a real estate investment organisation in London, he joined AVI in July 2002 as an investment analyst. AVI’s head of research is Tom Treanor, who joined the company in February 2011. His previous role was in closed-end fund analysis for Fundamental Data/Morningstar. We talked to Tom when putting together this note.

The investment team continues to grow and now numbers 12. Other members of the team include Scott Beveridge (an investment analyst focused on real estate-backed opportunities and Asian holding companies), Daniel Lee (the lead investment analyst for Japan, Wilfrid Craigie (an investment analyst researching global holding companies and asset-backed special situations), and a Tokyo-based team member, Jason Bellamy, who ensures a constant local presence to AVI’s ongoing engagement efforts in Japan.

As at 30 September 2021 (pre-the share split – see page 22), AVI’s investment team owned 216,372 shares in AGT.

AVI has about £1.2bn of assets under management. In addition to AGT, AVI Japan Opportunity Trust (AJOT) was launched in 2018 and AVI Family Holding Companies Fund was launched in December 2019. Goodhart Partners, a London-based independent “multi boutique” asset manager, has been a minority investor in AVI since 2016, having offered an exit for legacy shareholders in the company. Goodhart helps support AVI with its business development and sales and marketing strategy.

Good quality assets at a discount

AGT seeks to buy assets for less that their fundamental value and then profit as the discount between market value and intrinsic value narrows. AVI will engage with boards and underlying managers to unlock value. Usually, AGT will be a significant investor in the closed-end funds that it holds. It is the availability of value opportunities shapes the portfolio rather than macroeconomic considerations or the composition of any index.

AVI believes that the underlying assets must also represent an attractive investment opportunity in their own right. When it is considering whether to add a potential investment to the portfolio, AVI is looking for a catalyst that will unlock the discount. However, this can take time to come to fruition. AGT should be able to benefit from uplifts in the underlying asset value as well as discount narrowing.

This is especially true of family controlled holding companies, where AGT tends to have less sway. This is why it is important to align the trust with high quality, long-term management and businesses/assets.

Market backdrop

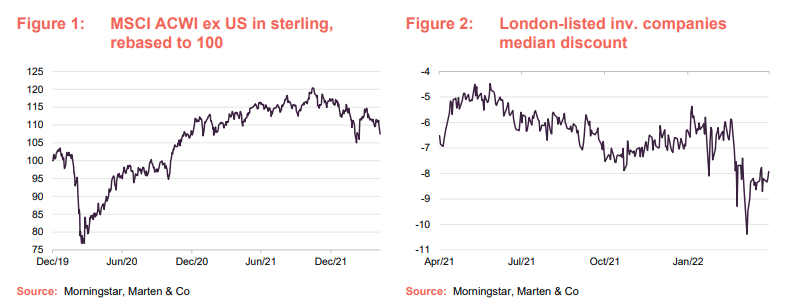

Markets peaked in November 2021 but have since been battered by a number of headwinds including inflation, rising interest rates, the war in Ukraine and new lockdowns in China as it tries to maintain its zero-COVID policy.

Figure 1, overleaf, looks at the performance of the MSCI All Countries (excluding the US) World Index. The returns have been adjusted so that they represent the return a UK-based investor would get in pounds.

AVI thinks that this is a challenging backdrop for markets to make progress. The US central bank (the Federal Reserve or Fed) no longer seems ready to ride to the rescue of falling markets and is instead resolute in its plans to choke off inflation through rate rises and quantitative tightening – the reverse of quantitative easing. The inflation problem has been worsened by the war in Ukraine. In addition, the lockdowns necessitated by China’s rigid adherence to a zero COVID policy are causing new disruption to supply chains. Shortages of food, as well as soaring energy and commodity prices have exacerbated the inflation problem.

The manager believes that at a company level, wage pressures are real. Volatile and significant inflation in the supply chain and disruption causing delays are causing problems for many companies. Some are better-placed than others to get through this, however.

For AGT, a widening of underlying discounts has provided a headwind to returns. Figure 2 shows how the median discount on London-listed closed end funds have moved over the past 12 months. Figure 3 shows how the underlying discount on AGT’s portfolio has moved. The manager feels that this is to be expected in an environment of falling markets. A chart of AGT’s average underlying discount suggests that it reached its narrowest as markets peaked. AVI thinks that the discount widening will start to reverse once markets settle down.

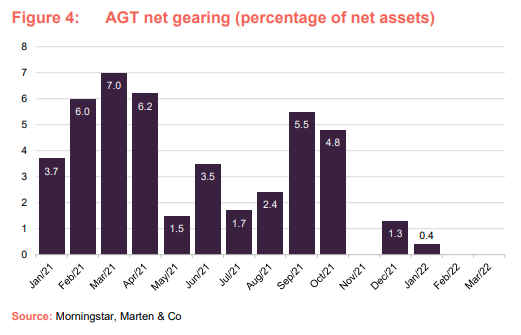

Given the backdrop, the managers are not using gearing (borrowing) at the moment. Gearing was marched downwards at the end of 2021. The managers’ focus has been on maximising returns from existing positions. The trust’s untapped borrowing facilities give the manager the firepower to take advantage of discounted opportunities when it judges that the time is right.

Investment process

The universe of AGT’s potential investments amounts to well over 1,000 stocks: over 100 each of European and Asian family holding companies, over 650 closed-end funds, more than 100 heavily over-capitalised Japanese operating companies with significant cash and/or securities holdings, and over 100 other asset-backed situations.

AVI keeps about 400 of these potential holdings under close scrutiny. Listed assets are valued on a mark-to-market basis. Most listed closed-end funds tend to publish regular NAVs, but the team may maintain its own models for funds that publish less frequently. The team also maintains its own models for valuing unlisted assets.

The portfolio is constructed on a bottom-up basis and without any reference to benchmark weights. Potential investments will be subjected to an intensive due diligence process, which includes meetings with management and an analysis of relevant industries, with help from independent experts where appropriate.

AGT has operated with a fairly concentrated portfolio since 2015, with about 25–35 core positions. In practice, this means about a 3% target position in core holdings.

The team has strong relationships with some brokers and AVI is sometimes offered large lines of stock. With the Japanese part of the portfolio, the manager keeps an eye on trading by insiders (as family members face inheritance tax bills, for example), which can give an indication that there is stock available.

Family-controlled holding companies

The holding companies that AGT invests in should have high-quality portfolios of listed and/or unlisted businesses with the potential for sustained, above-average, long-term NAV growth. The controlling family or shareholder should have a strong track record of capital allocation and have demonstrated that it is capable of generating returns in excess of broader equity markets.

Part of the attraction of investing in these companies is that they operate with a long-term strategic vision; investing for the benefit of future generations, rather than to beat analysts’ short-term estimates.

The manager’s preference is for investment in holding companies where there is a catalyst in place to narrow the discount. By the manager’s own estimate, historically about three-quarters of AGT’s returns from holding company investments have come from NAV growth and one-quarter from discount tightening.

Closed-end funds

AGT invests in closed-end funds globally, but the majority of its investments in this area are listed in London. There are many reasons for this; for example, the manager says that closed-end funds in the US tend to focus on fixed income and yield and, currently, this means that their discounts are tight. In the manager’s experience, corporate governance in the US is also relatively poor; directors are often conflicted, for example, which can be a barrier to unlocking discounts for the benefit of shareholders.

Again, the focus is on the quality and growth potential of the underlying assets. When investing in closed-end funds, the manager places a greater emphasis on an ability to close the discount. Consequently, AGT’s stakes in closed-end funds are usually larger, to give it greater influence. The manager will engage with management, boards and other shareholders. Historically, half of AGT’s returns on closed-end fund investments have come from discount narrowing.

Asset-backed special situations

AGT’s asset-backed special situations largely comprise a number of Japanese investments. These benefit from a tailwind of a revolution in Japanese corporate governance. The manager has been investing in Japan for over 20 years. In 2012, then-Prime Minister Shinzo Abe proposed a stewardship code, which was adopted in 2013. This was aimed at getting institutional investors to fulfil their fiduciary responsibilities and encouraging engagement with company management.

A corporate governance code was introduced in 2015 and strengthened in 2018. This included measures aimed at minimising cross-shareholdings, stressing the importance of companies earning more than their cost of capital, bringing in more independent directors, establishing independent nomination committees for new directors, improving disclosure and encouraging greater dialogue with shareholders, and maintaining a level playing field in the treatment of shareholders. AVI describes this as a scorecard with which it could hold Japanese businesses to account.

The number of activist investors in Japanese securities has increased and the manager sees evidence of rising dividend payout ratios, greater share buybacks, and more independent directors. The managers engage with the boards and management of AGT’s holdings, promoting policies for the benefit of all stakeholders.

With all of its engagement activities, AVI much prefers that these take place in private, although it is willing to put proposals to shareholders if necessary. The vast majority of engagement activity will never come to light, therefore.

A typical stock in this part of the portfolio will be cash-generative, trade on low valuation multiples, and the underlying business will be of sufficient quality such that the manager can afford to take a long-term view.

Hedging

The manager has the ability to hedge positions (by shorting stocks or indices, for example) should it choose, although this is used infrequently, and the manager would not take a net short exposure. The company may use a variety of derivative contracts, including total return swaps, to enable it to gain long and short exposure to individual securities.

Derivatives are valued by reference to the underlying market value of the corresponding security. The gross positive exposure on total return swaps as at

30 September 2021 was £38,396,000 (30 September 2020: £nil) and the total negative exposure of total return swaps was £39,487,000 (30 September 2020: £nil).

Currency exposures have been hedged in the past. Now, as we discuss on page 21, AGT has a multicurrency debt facility, which allows the manager to limit exposure to certain currencies.

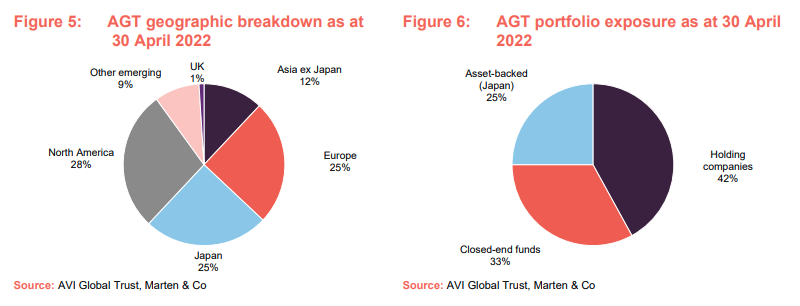

Asset allocation

AGT’s asset allocation is driven by the manager’s stock selection decisions.

Relative to the position at the end of June 2021 (when we last published), AGT has a lower exposure to the UK, Asia and Europe and higher exposure to North America and Japan. The trust’s exposure to property plays has gone, as the portfolio has become more focused on higher-conviction positions.

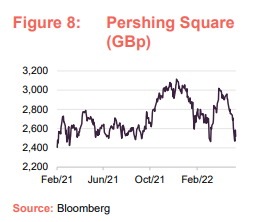

Top 10 holdings

AGT’s portfolio remains relatively concentrated. In our last note, the first entry in the list of the top 10 holdings was ‘Japan special situations’. AVI now prefers to list these separately. Setting aside these, Aker has replaced Godrej Industries in the list of the 10-largest holdings since we last published (using data as at 30 June 2021). Nevertheless, Godrej Industries remains just outside the list and is still a significant investment. As we discuss on page 18, the percentage weighting to Aker has increased as its shares have responded to a stronger oil price.

Looking at some of these in more detail:

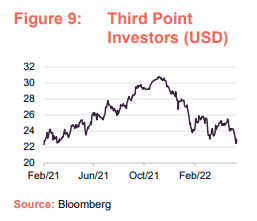

Pershing Square Holdings

We discussed Pershing Square Holdings (PSH) (pershingsquareholdings.com) in our last note. To recap, the hedge fund owns stakes in stocks such as Restaurant Brands (which owns Burger King, Tim Hortons and Popeyes), Agilent Technologies (life science services), Chipotle, Domino’s Pizza, Lowes (DIY stores), Starbucks, Hilton, Howard Hughes (a real estate development company), and mortgage loan companies Fannie Mae and Freddie Mac.

A derivative position initiated in late 2020 has been a significant contributor to PSH’s returns and has offset, to some extent (by about 15 percentage points), the effects of falling markets.

Within the portfolio, Hilton Hotels and Restaurant Brands operate franchise models which cushion them from the effects of reduced demand/higher input costs. Chipotle does own its own stores, and is exposed to the twin problems of higher labour and food costs. However, it was already a relatively generous employer – having introduced a $15/h minimum wage and offering full college education. Its product is positioned towards more affluent consumers, and it has been able to raise prices without affecting demand.

Canadian Pacific Railway was owned by PSH back in the mid-2010s. PSH has been rebuilding the position this year. It is unusual for it to favour capital intensive businesses but there is a strong environmental angle to the growth of the business and shipping by rail is also 75% cheaper than shipping by truck.

A recent investment in Netflix was clearly a mistake. Increased competition and a squeeze on disposable income has led to a well-publicised stall in subscriber growth. However, Tom is heartened by the speed with which PSH recognised the problem and addressed it by selling out of the holding in its entirety, rather than doubling down as it has done in the past.

Universal Music Group (UMG), which AGT also holds directly, derives most of its revenue from subscription-based services such as Spotify, Amazon and Apple. Tom thinks that these are likely to be more resilient than Netflix subscriptions. UMG doesn’t care which of these platforms succeeds, as it offers its product through all of them. Tom thinks price hikes for music subscription services are a possibility (which would also benefit AGT’s holdings in Hipgnosis and Sony).

Third Point Investors

We discussed AGT’s engagement with the board of Third Point in the last note. Since then, two new non-executive directors with significant experience of investment companies have been appointed to the Third Point board. AGT has exchanged 44% of its stake in the listed company, valued at a discount to NAV, into an investment in the underlying Master Fund, which is valued at asset value. That investment was then tied up for six months. Thereafter, AGT can redeem a quarter of the investment each quarter.

Third Point significantly altered its asset allocation over Q1 2022. Exposure to listed equities has fallen to 36% of the portfolio and around a third of that is in energy-related stocks. This may indicate that the manager sees the current environment persisting for some time.

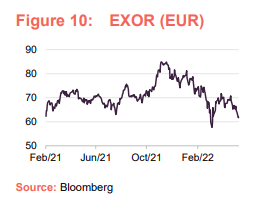

EXOR

Agnelli family holding company EXOR was described in some detail in our last note (see page 11 of that note). In December 2021, EXOR agreed to sell PartnerRe to Covéa for $9bn. Having acquired a 9.9% stake in the business in 2015 for $609m, EXOR bought the balance in March 2016 for $6.1bn. All-in-all, EXOR says its investment in PartnerRe will generate $3.5bn of capital gains.

Ferrari’s revenue rose by 23.4% over 2021 and ended the year with a record order book. Stellantis (the company born from the combination of Fiat Chrysler and Peugeot) continues to build on its ambitions for its electric vehicle (EV) business while extracting synergistic benefits from the merger that created it. Commercial vehicle business Iveco Group was spun out of CNH Industrial and listed on Euronext in January 2022. Iveco’s first quarter sales figures were OK, but supply chain problems impacted on profitability; unfortunately, the share price has halved since its initial public offering (IPO).

Within its listed equity portfolio, EXOR’s investments in uranium-producers Cameco and NexGen Energy were significant positive contributors to its returns over 2021 as the uranium price rose. On the negative side, the Ocado share price was weak; EXOR added to its stake.

Oakley Capital

Private equity fund Oakley Capital Investments (oakleycapitalinvestments.com) published a quarterly trading update covering the first quarter of 2022 recently. The NAV rose by 6% over that period, building on the trust’s good long-term track record. Over five years, Oakley is the second best-performing London-listed private equity trust in both share price and NAV terms.

The trust recently committed to invest a further €400m in Oakley’s limited partnership Fund V. The trust’s discount is languishing at around 29%, having been in single digits in December 2021.

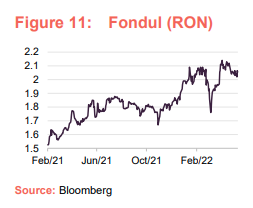

Fondul Proprietatea

Fondul (fondulproprietatea.ro) could be about to benefit from the IPO of its largest holding Hidroelectrica. The only stumbling block, in AVI’s view, is that the Romanian government and the regulator appear to want to restrict the IPO to the Bucharest stock exchange. If that were the case, Hidroelectrica could dominate the exchange, accounting for around half of its market capitalisation. A higher price and perhaps greater liquidity could be achieved through a dual listing in London or New York.

Hidroelectrica is a regulated business and may be subject to extended windfall taxes, but Tom feels that it should fetch an attractive valuation. Fondul says that it plans to sell three-quarters of its stake and return the proceeds to its shareholders.

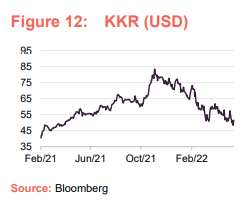

KKR

KKR (kkr.com) is a diversified alternative asset manager, with exposure to credit, infrastructure, hedge funds and real estate, as well as private equity. The manager notes that KKR is operating in growth markets and in asset classes that offer some degree of inflation protection. Its credit strategies have a high degree of floating rate exposure. Higher rates are not generally thought to be good for private equity strategies, but much depends on the deal structure. Tom says that KKR’s portfolio companies tend to be leveraged with fixed-rate debt. He thinks that fundraising for private equity strategies may be harder in the current environment, but KKR’s other business lines may be less affected. In addition, Tom says that investors in limited partnerships are looking to consolidate the number of private equity managers (general partners or GPs) that they deal with, which should work to KKR’s benefit.

KKR’s fee-related earnings for the 12 months ended 31 March were $2.2bn, up 59% year-on-year, and assets under management (AUM) rose by 30% to $479bn. $115bn of that is represented by uncalled commitments (promises to invest that KKR can call upon when needed), so KKR has a substantial war chest to deploy in today’s weaker markets, should it choose.

Tom feels that KKR is priced as though its business is subject to outflows, as an equity manager’s business might, but actually much of its assets under management (AUM) is tied up for the long term. He thinks AUM and fee income will continue to grow from here.

LVMH

We discussed with Tom the potential impact of both China’s slowing economy and the sanctions on Russia on luxury goods businesses, such as Christian Dior’s largest position, LVMH. He notes that Russian share of global luxury spend was a surprisingly low 5% pre-COVID and even lower for LVMH at 2%. Roughly half of that spend happens inside Russia and the rest outside. China represents a much larger proportion of its business – around 35%.

LVMH’s first quarter (Q1) 2022 revenue grew by 29% year-on-year (23% organic). It said that all of its businesses saw double-digit growth barring wines and spirits. Its Asian business grew despite the Chinese lockdowns in March.

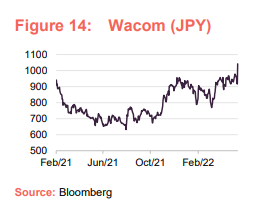

Wacom

Wacom (wacom.com/en-jp) is the largest position within the Japanese small-cap investments held by AGT, some of which are also held by AJOT. Collectively, these accounted for 14.9% of AGT’s NAV at 30 April 2022. At that date, they were valued at an average of 7.7x EV/EBIT and cash/investment securities accounted for an average of 59% of their market caps. Over 2022, a weak yen has weighed on valuations.

Wacom makes digital pens and is the global leader in the field, with a market share of around 60%. Tom says that a relatively new CEO with a strong track record is applying western business practices to the company. He sees the investment as more about operational activism – engaging in a dialogue to help drive best practice – than streamlining the balance sheet. The approach to unlocking value in this part of the portfolio is aided by the increasing depth of resource within AVI’s Japanese research team. Wacom has been open to engaging with AVI, which is now one of its largest investors.

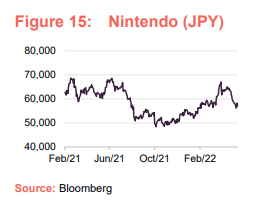

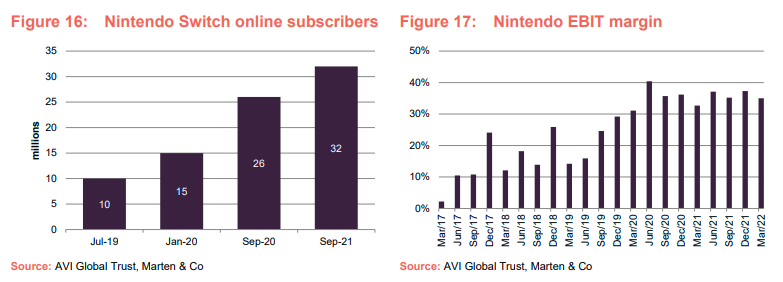

Nintendo

Nintendo (nintendo.co.jp/ir/en) is not an activist investment. Its balance sheet is not efficient – with excess cash – but the attraction of the company for AGT is the shift towards a higher proportion of recurring revenue from its gaming business and better exploitation of its intellectual property. AVI says that around 21% of Nintendo’s revenue is now derived from digital sales versus sub 10% in 2019. By contrast, AVI says that Sony’s digital software, add-on content and network services account for 67% of total revenues, highlighting how far Nintendo still has to grow on this side of the business.

Figure 16 shows the growth in subscribers for its Nintendo Switch online business. AVI notes that a subscriber may represent many users as families will tend to have one account. In line with this trend, Nintendo’s margins appear to be on a rising trend.

Recent trades – investments

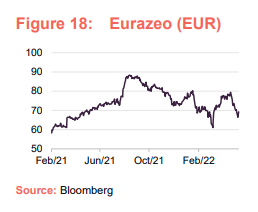

Eurazeo

Eurazeo (eurazeo.com/en) is the Paris-listed holding company for the Decaux, David-Weill, and Richardson families, who own about 38% of the company between them. Eurazeo was a new addition to AGT’s portfolio in December 2021 and one that AGT has continued to build as Eurazeo’s discount has widened since. It is a stock that AGT has owned in the past (AGT sold out in about 2014). The manager believes that Eurazeo’s discount may have widened recently on the back of an overhang of stock.

The attraction of the company is that it is transforming itself from a holding company to an asset management business. At the end of December 2021, Eurazeo had AUM of €31bn (up 42% over 2021) and its NAV was €117.8 per share (up 40% over 2021). Around 80% of its portfolio is invested in about 450, mostly private equity, portfolio companies and the balance represents a stake in the fund management business. AVI believes that both the private equity positions and the fund management business are valued conservatively. It says that Eurazeo’s asset management business is now valued on 20x last 12 months’ (LTM) fee-related earnings + 6x on performance-related income (i.e. carry). AVI notes that several peers trade on materially higher valuations.

The manager suggests that Eurazeo offers the potential for discount narrowing and NAV growth. Eurazeo is aiming to double its AUM by 2025.

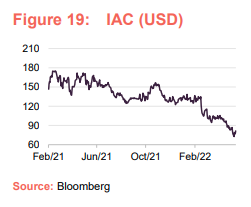

IAC/InterActiveCorp

US internet-focused holding company IAC/InterActiveCorp (iac.com) is a position that AGT was building over the course of 2021. It describes itself as an anti-conglomerate – more of an incubator of businesses than a diversified investment portfolio. It has had some great successes, including Match.com (owner of Tinder), Tripadvisor, and Expedia. IAC is run by Barry Diller (ex-Paramount Pictures and Fox Broadcasting), who controls the voting rights in the company. When a business matures, it is spun out at NAV and so the discount on the existing portfolio – which has been as wide as 40% – should trend towards zero over time.

IAC’s largest investment (29% of IAC’s NAV according to AVI) is Dotdash Meridith a contextual advertising business that AGT thinks can continue to thrive when new restrictions on cookies make targeted marketing harder. Dotdash acquired Meridith in Q1 2022 and is now in the process of integrating it. That process involves streamlining Meridith’s print business, serving up fewer but better targeted advertising on the digital platforms, and combining sales teams.

A recent investment (August 2020) has been a stake (now approaching 15%) in MGM Resorts, a listed casino business. When IAC started to build its stake, MGM had been hit hard by the pandemic. It is unusual that IAC takes minority stakes, but it came with a board seat and AGT thinks that the angle is to increase the company’s revenue from online gaming. MGM Resorts and Entain Plc have a 50:50 joint venture – BetMGM – which already has a significant presence in the North American online casino/betting market. On 2 May 2022, MGM launched a $607m cash bid for LeoVegas AB, a Swedish online casino/betting business, with operations across Europe.

IAC also owns 85% of Angi, a home services/DIY site that links tradespeople and customers. It has been hard to scale the business. The management team has been refreshed and Tom thinks that Angi may have affected sentiment towards IAC.

AVI has valued the components of IAC’s portfolio based on peer group comparisons. Valuing the rest of the company on this basis, its calculations suggest that DotDash Meridith is valued on a very low multiple of about 6x EBITDA.

Recent trades – realisations

As the manager has reduced the number of holdings to focus on higher conviction positions, AGT has exited Pershing Square Tontine Holdings, Naspers, and Associated British Foods among others.

As discussed in our last note, Pershing Square Tontine Holdings was not able to pursue its planned acquisition of a stake in Universal Media Group. It is still effectively a cash shell. Naspers offers exposure to Tencent on a discount. Adverse sentiment towards growth stocks, increased government scrutiny of its business and a weak Chinese stock market have weighed on the stock. Associated British Foods has seen a post-COVID recovery in its sales and profits, but higher input cost inflation is affecting some divisions.

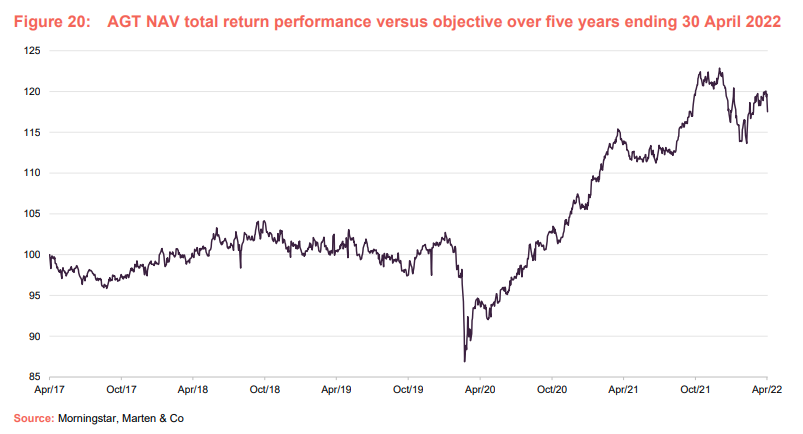

Performance

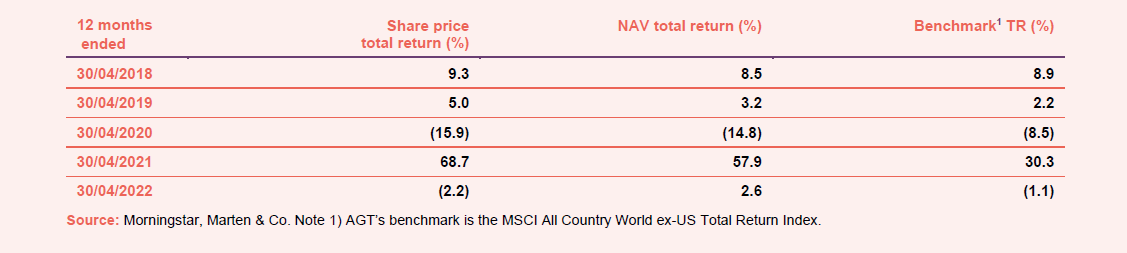

AGT delivered strong relative returns as it recovered from the initial pandemic-related panic in spring 2020. It extended its run of outperformance as markets embraced value propositions in the wake of the good news on vaccines in November of that year. In recent months, however, AGT has been held back by a widening of the underlying average discount on the portfolio (as was illustrated in Figure 3). The manager says that such widening is typical of periods of market stress. However, it enables AGT to sow the seeds for future outperformance by building positions in good quality stocks on attractive discounts.

Peer group

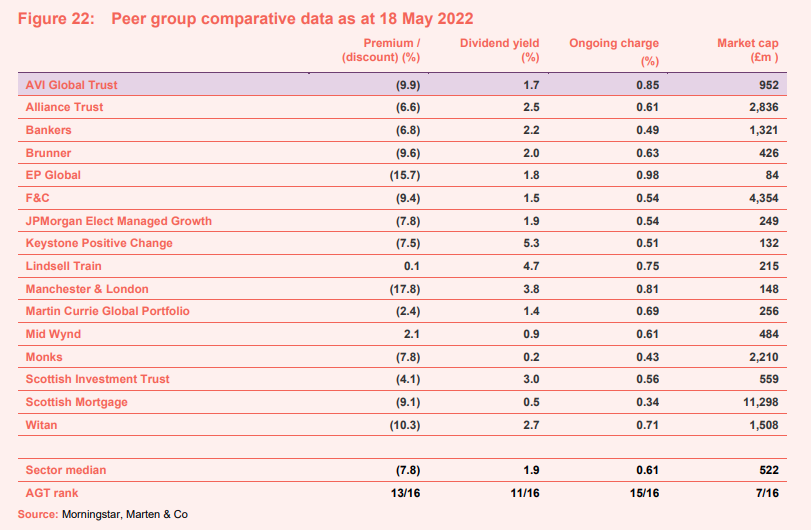

AGT is a constituent of the AIC’s Global sector. For the purposes of this note, we have compared AGT with the other members of this sector (excluding Blue Planet on size grounds). The members of this peer group invest predominantly in listed equities.

AGT’s discount is relatively wide within this peer group. Its yield is about middle of the pack, although none of these trusts invests with the primary intention of generating a high yield. AGT’s ongoing charges ratio is at the higher end of this peer group, but we would argue that none of these figures is particularly high.

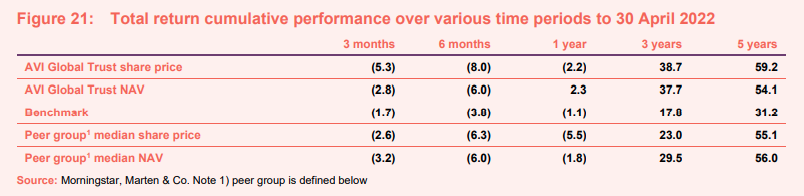

Although widening discounts have weighed on AGT’s NAV, it remains one of the better-performing global investment companies over the past few years.

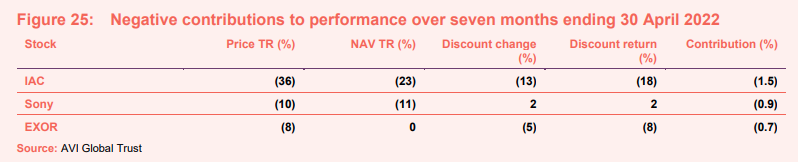

Contributions to returns

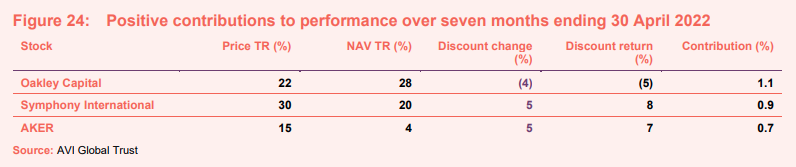

AVI has shared some information on the stocks that contributed to AGT’s returns over the seven months to end April 2022 (AGT’s current financial year to date), which we reproduce in Figures 24 and 25.

Symphony’s (symphonyasia.com) share price has recovered strongly helped by a post-COVID recovery in its hotels and restaurants exposure (largely through its stake in Minor International). It has a recent investment in a Vietnamese logistics business that is trading well. However, the discount remains stubbornly wide.

Aker

AGT does not have much exposure to commodities. However, it does own a stake in Aker (akerasa.com/en), which has significant exposure to rising energy prices through its stakes in Aker BP (a Norwegian continental shelf oil & gas business), Aker Horizons (a renewable energy and green technology business), and Aker Energy (an oil & gas business operating offshore in Ghana). Aker BP is a low-cost producer and one of the largest independent listed oil companies in Europe.

IAC has been hit by the general adverse sentiment towards growth stocks. Sony’s results for the 12 months ended 31 March 2022 were published recently. Revenue rose by 10% and profit before tax has risen by 12%.

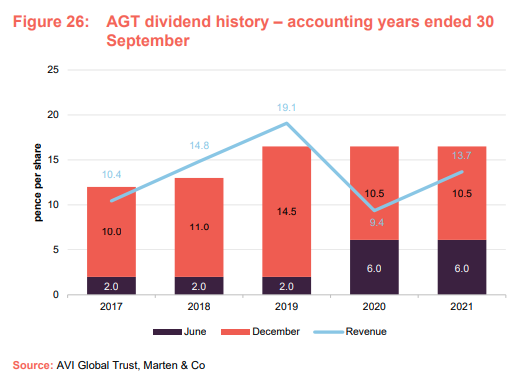

Dividend

AGT normally declares two dividends per year, an interim in June and a final in December.

In the wake of the pandemic, dividend cuts have been commonplace. However, in recognition of the importance of income to many of AGT’s shareholders, the board has opted to dip into revenue reserves to maintain dividends at their level of the previous financial year.

The board does not constrain the investment manager by setting a revenue target. The board’s current intention is to maintain the dividend at current levels. However, the dividend policy remains under careful and regular review.

At the end of September 2021, AGT’s revenue reserve stood at £27.9m, equivalent to 5.6p per share. In addition, AGT’s articles permit the distribution of realised capital gains.

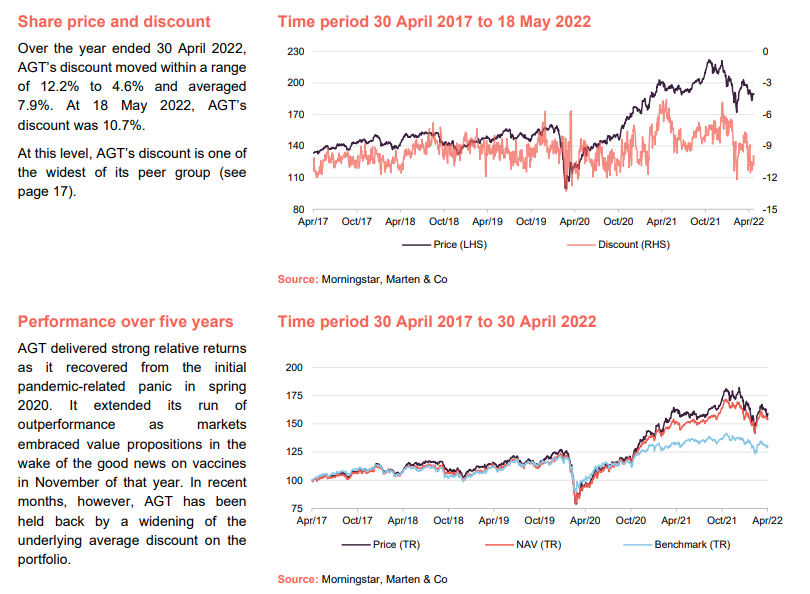

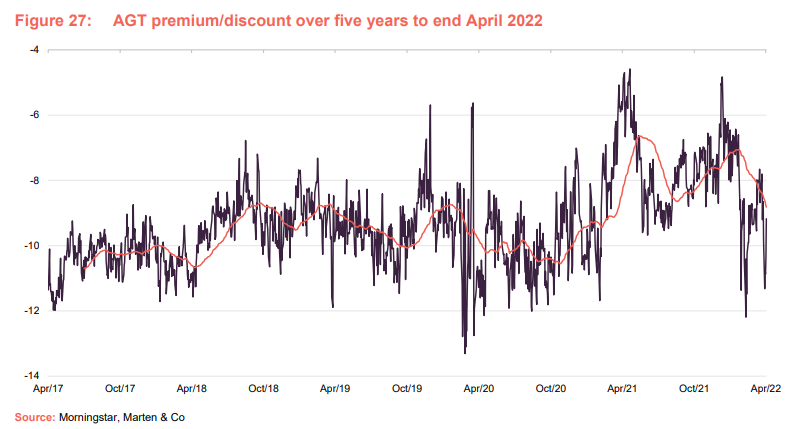

Discount

Over the year ended 30 April 2022, AGT’s discount moved within a range of 12.2% to 4.6% and averaged 7.9%. At 18 May 2022, AGT’s discount was 10.7%.

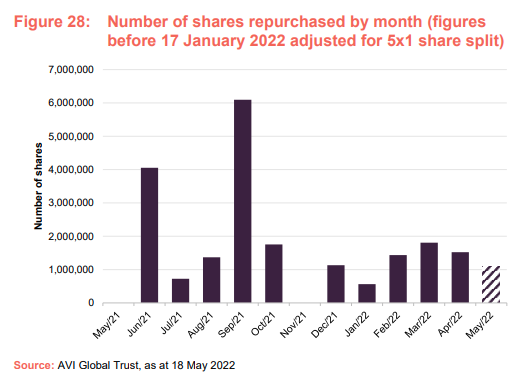

At the annual general meeting (AGM) in December 2021, shareholders approved resolutions empowering the board to buy back up to 14.99% of its then-issued share capital and issue up to a third of its then-issued share capital. A separate resolution granted permission for 5% of the then-issued share capital to be issued without pre-emption.

AGT’s board uses share buybacks with the intention of limiting volatility in AGT’s discount. Over the 12 months ended 30 April 2022, the equivalent of around 20.4m shares were repurchased. Buying back shares at a discount enhances the NAV per share for remaining shareholders, by 0.3% over the course of 2021, according to AVI.

The board also employs a marketing budget (administered by the investment manager) with the aim of stimulating demand for the trust’s shares.

Fees and costs

The investment manager is entitled to an annual management fee of 0.70% of the first £1bn of AGT’s net assets and 0.60% of any net assets above £1bn. The fee is calculated quarterly by reference to the net assets at the preceding quarter end and paid monthly.

The investment management agreement can be terminated on six months’ notice.

For accounting purposes, 30% of the management fee is charged against revenue and the balance against capital.

A breakdown of directors’ fees is shown on page 22. For the year ended 30 September 2021, the only other expenses of note were marketing expenses of £411,000 (FY20: £459,000), advisory and professional fees of £343,000 (FY20: £249,000), custodian fees of £272,000 (FY20: £185,000) and depositary fees of £140,000 (FY20: £120,000).

The ongoing charges ratio (based on the trust’s own running costs) for the year ended 30 September 2021 was 0.83%, down from 0.89% for the prior year. The board argues, and we wholeheartedly agree, that including a proportion of the running costs of the closed-end funds held within AGT’s portfolio within the ongoing charges ratio, but not those of other investee companies may create a perverse incentive for the manager to favour those companies which do not have explicit management fees. It also seems odd to include a share of running costs of closed end funds but not those of businesses held through other corporate structures. However, for the record, were these included, the ongoing charges ratio would be 2.10%.

Capital structure and life

Since we last published, AGT split its shares on a five-for-one basis. As of 18 May 2022, AGT has 546,861,845 ordinary shares in issue, of which 45,600,956 shares are held in treasury. The number of total voting rights is 501,260,889. There are no other classes of share capital.

AGT does not have a fixed life. Its financial year end is 30 September and its AGMs are usually held in December.

Gearing

AGT has a JPY12bn unsecured multicurrency revolving credit facility provided by Scotiabank Europe Plc which runs until 26 August 2024. The interest cost depends on which currency is being drawn as follows:

- Japanese yen 1.025% margin over the Tokyo unsecured overnight rate (TONAR);

- Pounds sterling 1.42% margin over SONIA (sterling overnight index average);

- US dollars 1.25% margin above the secured overnight financing rate (SOFR);

- Euros 1.25% margin above the Euro short-term rate (€ STR).

Undrawn balances below JPY2.0bn are charged at 0.35% and any undrawn portion above this is charged at 0.30%.

Under the terms of the facility, the covenant requires that the net assets shall not be less than £300m and the adjusted net asset coverage to borrowings shall not be less than 4:1.

AGT has also issued three loan notes:

- £30.0m of 4.184% series A unsecured loan notes 15 January 2036;

- £30.0m of 3.249% series B unsecured loan notes 15 January 2036; and

- €20.0m of 2.93% Euro senior unsecured loan notes 1 November 2037.

At 17 May 2022, the effect of valuing the loans at fair value was to reduce the NAV by 0.88p per share.

At 30 April 2022, AGT’s net gearing was 1.0%.

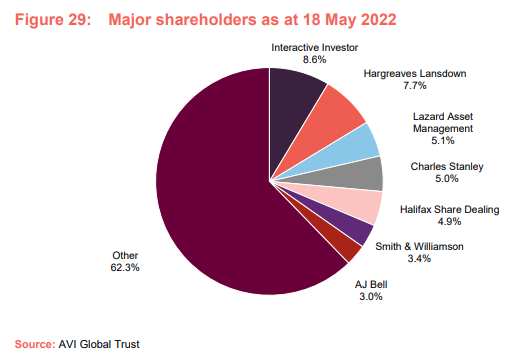

Major shareholders

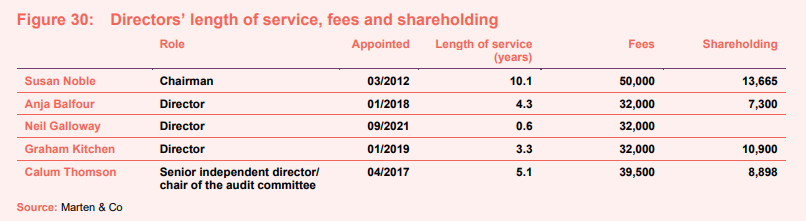

Board

AGT has five directors, all of whom are non-executive, independent of the manager and who do not sit together on other boards.

The chairman, Susan Noble, and senior independent director, Nigel Rich, both joined the board in March 2012. The AGT board decided that it would be advisable not to have two directors retire in the same year and that it would be appropriate to have an orderly succession plan. As a result, Neil Galloway joined the board in September 2021, and Nigel retired from it at the AGM in December 2021. Susan will step down from the board at the AGM in 2022.

Susan Noble

Susan was appointed as chairman of AGT in December 2017. She is a former chair of Alliance Trust Investments, a director of Alliance Trust Plc, an associate director of Manchester Square Partners, and a managing director of Goldman Sachs Asset Management, where she was head of European equities and head of global equities. Susan was also a director and senior European portfolio manager at Robert Fleming Asset Management.

Currently, Susan is chairman of Newton Investment Management Limited.

Anja Balfour

Anja has over 20 years’ experience in managing Japanese and international equity portfolios for Stewart Ivory, Baillie Gifford and Axa Framlington.

She is chairman of Schroder Japan Growth Fund Plc and BMO Global Smaller Companies Plc, a member of the Finance and Corporate Services Committee of Carnegie UK Trust, and a non-executive director of Scottish Friendly Assurance Society. Previously Anja was a trustee of Venture Scotland and a non-executive director of Martin Currie Asia Unconstrained Trust Plc.

Neil Galloway

Neil has 25 years’ experience living and working internationally. Currently based in London, he has spent most of his career working in Asia but also has experience in the Americas, Europe and the Middle East. Following a successful banking career, he has held senior finance and management roles, almost entirely with or for family-controlled companies, overseeing finance, treasury, risk management, legal, IT, projects and business development, with experience in significant business transformation programmes in large and complex businesses.

He was previously an executive director and CFO of Dairy Farm International Holdings Limited based in Hong Kong. His industry experience spans banking, hospitality, retail (mass market, luxury and franchise operations), real estate and services industries.

Neil is executive vice president of IWG Plc.

Graham Kitchen

Graham has over 25 years’ experience as an investment manager at Invesco, Threadneedle and, until March 2018, Janus Henderson, where he was global head of equities. He was previously chair of the investment committee for the Cancer Research Pension Fund and chairman of Invesco Perpetual Select Trust Plc.

Graham is chairman of Perpetual Management UK Limited and Trillium Asset Management UK Limited, and a non-executive director of The Mercantile Investment Trust Plc and Places for People. He is also a member of the investment committee of the charity Independent Age.

Calum Thomson

Calum is a qualified accountant with over 25 years’ experience in the financial services industry, including 21 years as audit partner at Deloitte LLP, specialising in the asset management sector. He has wide-ranging experience in auditing companies in the asset management sector and latterly as a non-executive director and audit committee chairman.

Calum is non-executive director and audit committee chairman of The Diverse Income Trust Plc, The Bank of London and The Middle East Plc, Ghana International Bank Plc, abrdn Private Equity Opportunities Plc, and Baring Emerging EMEA Opportunities Plc. He is also a non-executive director of Schroder Unit Trusts Limited and Schroder Pension Management Limited, chairman of The Tarbat Discovery Centre and a trustee of Suffolk Wildlife Trust.

Previous publications

Readers may wish to refer back to our initiation note – Double discount on quality-focused portfolio – published 25 January 2021 or our last update note – Focused high conviction portfolio – published 5 August 2021.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on AVI Global Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.