Focused high conviction portfolio

AVI Global Trust (AGT) has had a strong run of performance since last November. Its manager, Asset Value Investors (AVI) has been realising substantial profits from a number of positions where discounts have narrowed significantly or have been eliminated altogether. As we describe on page 8 onwards, the proceeds are being recycled into a more focused, high conviction portfolio of what AVI feels to be good quality companies trading at meaningful discounts to its estimate of their true asset value.

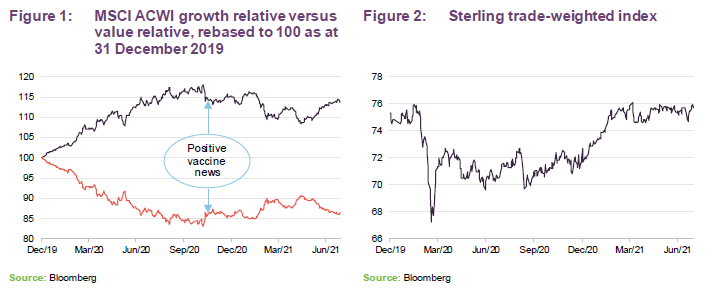

Recent nervousness about new COVID variants appears to have triggered a switch back into growth-focused strategies. AGT has given up some of its outperformance and seen its discount widen in recent weeks. AVI thinks that this is likely to be a short-term phenomenon and thinks that this could be an attractive entry point.

Extracting value from discounted opportunities

AGT aims to achieve capital growth through a focused portfolio of investments, particularly in companies whose shares stand at a discount to estimated underlying net asset value. It invests in quality assets held through unconventional structures that tend to attract discounts; these types of companies include holding companies, closed-end funds, and cash-rich Japanese operating companies.

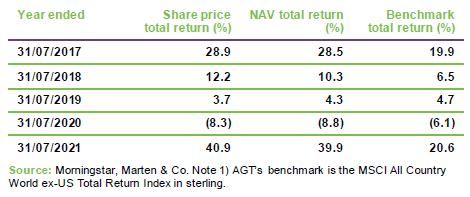

AGT outperforming its benchmark

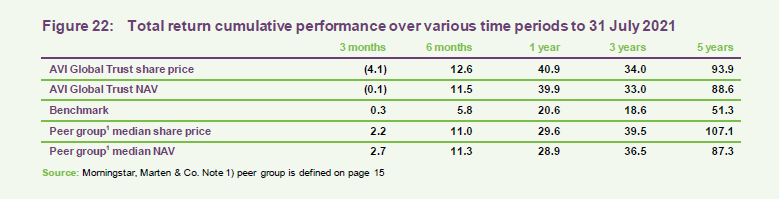

AGT beat its benchmark over H1 (as we show in Figure 22 on page 13). On average, discounts on London-listed funds continued to narrow back towards pre-pandemic levels. However, it is stock-specific success on a number of fronts that has been the biggest driver of returns (see page 14 for more detail). This has allowed the manager to book some profits. Gearing levels in AGT have fallen in recent weeks as a result but AVI says that this is likely to be a temporary phenomenon.

The manager anticipates that AGT’s portfolio will become more concentrated in coming weeks as it focuses on fewer, high-conviction ideas. AVI says that, despite the environment of narrower discounts, there are still enough stocks trading at significant discounts to populate a high-quality portfolio.

COVID-19 and effects of stimulus driving markets

Our initiation note on AGT was published on 25 January 2021 and referenced portfolio data as at the end of December 2020. Towards the end of January, as vaccination rates began to pick up and hopes rose that COVID-19 was under control, investors’ concern seemed to switch to the impact of the substantial government stimulus injected into the global economy. Markets have since appeared to have been influenced by fears of higher inflation and interest rates. This was associated with falls in the values of long-duration assets such as growth stocks and longer-dated bonds.

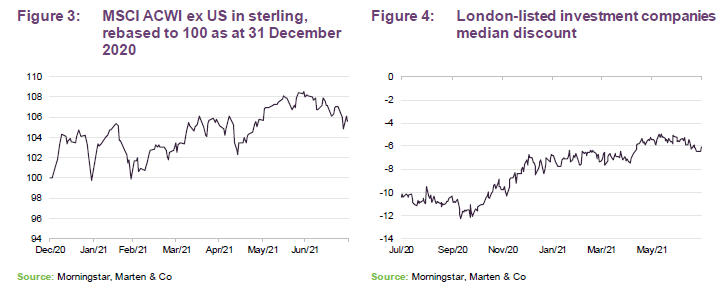

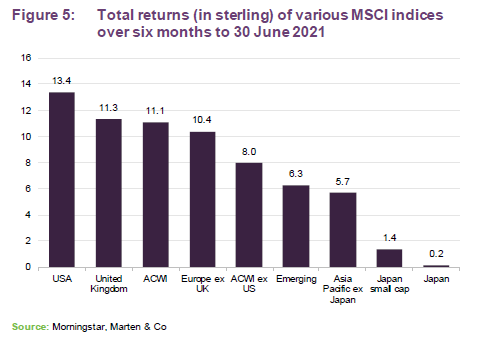

Sterling continued to strengthen, perhaps helped by the Brexit deal as well as the speed of the vaccine rollout. The situation changed once again in June, as the Delta variant triggered new waves of infection, dampening hopes of a return to normality; growth stocks rebounded in response. AGT’s benchmark (MSCI ACWI ex US in sterling) made progress over H1 2021, returning 8.0%.

Japan lagging

From an asset allocation viewpoint, AGT’s overweight exposure to Japan has held it back recently as Japanese stocks have underperformed global indices. In addition, Japanese value stocks did not participate in the global value rally. AVI notes that the companies held by AGT, in particular, are performing fairly well with regard to their underlying earnings and, therefore, the stocks are getting cheaper. It feels that the catalyst for a re-rating would be increased foreign investor interest in the country, on the back of growing evidence that the environment for corporate control and governance is changing.

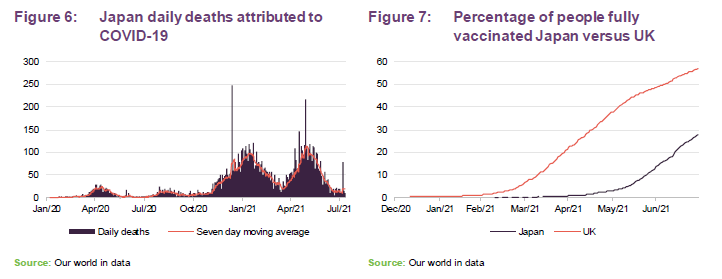

Whilst on many levels Japan’s experience of the COVID-19 pandemic has been relatively good – less than 12% of the number of deaths in the UK while having over 1.8x the population, for example – in one respect, Japan has fallen down. The country was slow to approve vaccines and slow to deploy them. A key to changing foreign investors’ sentiment towards the country could be signs that vaccinations are catching up.

The Toshiba scandal (where it seems the government colluded with the company to put pressure on shareholders not to vote against directors at its AGM and the company did not count some votes) has reignited a debate over the degree to which the government is in bed with the corporate establishment. It could reinforce the old stereotype about Japan being a closed shop to foreign investors. However, AVI notes that the report on the scandal is both detailed and transparent. It feels that this could suggest a change of attitude. CVC made, but later withdrew, an offer for the company in April. If a private equity buyout occurs, AVI thinks that this could be a key catalyst for Japanese markets.

The manager says that changes to Japan’s listing rules in relation to free floats may help improve corporate governance. While some companies may divest stakes in response, it is possible that several Japanese firms decide to delist.

AVI thinks that we could see more MBOs and large companies looking at carve outs, selling to private equity. AVI believes that there is increased interest from big US private equity investors in Japan. KKR and Bain have been there for some time but Apollo recently opened an office in Tokyo and Blackstone has been buying Japanese property.

Asset Allocation

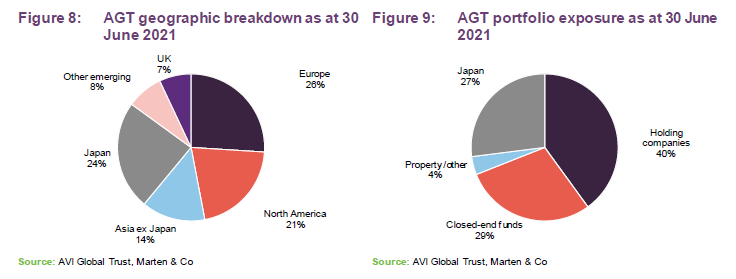

Changes to AGT’s asset allocation are driven primarily by AVI’s stock selection decisions. Over H1, AGT’s exposure to Europe fell to the benefit of North America and the portfolio has a slightly higher exposure to Japan and property and lower exposure to closed-end funds than it did at the end of December 2020.

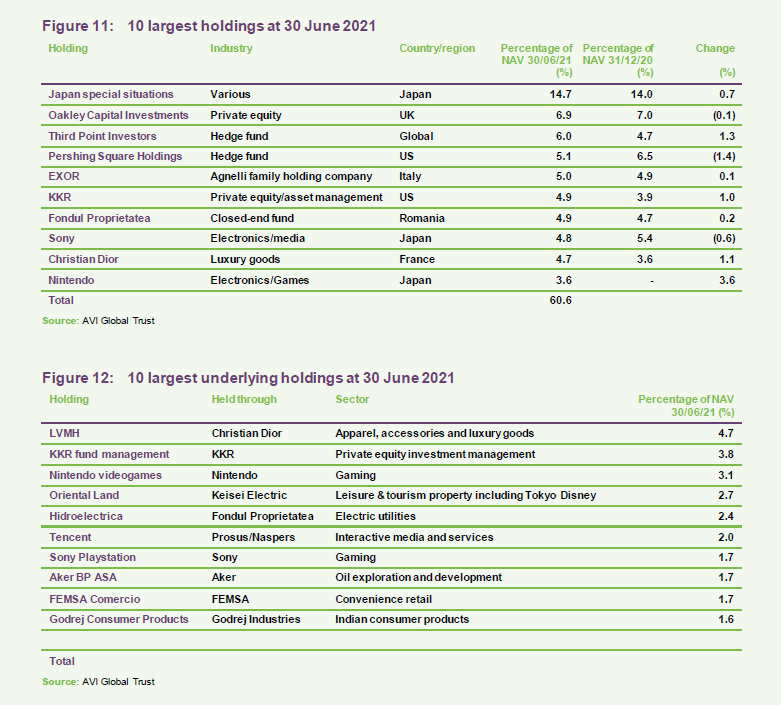

Top 10 holdings

Since end December 2020, Christian Dior and Nintendo have entered the list of AGT’s 10-largest holdings, replacing VNV Global and SoftBank. We discussed AVI’s purchase of Christian Dior in our last note. Nintendo’s gaming business fared well during the pandemic, driving a 34% increase in sales and 86% rise in profit per share over the year ended 31 March 2021. Its share price has drifted off a little this year and AVI has added to the position.

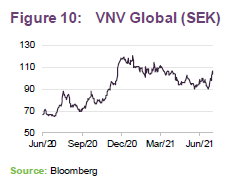

VNV Global performed well, driven largely by the success of Babylon, the digital healthcare company offering online consultations with health professionals. When we talked to AVI, it had cut AGT’s stake in the business by about two thirds. This reflects VNV’s valuation. AVI estimates that it reduced AGT’s position in VNV at about a 17% premium to its estimated NAV, versus about an average 25% discount on purchases.

The position in Softbank was acquired in the depths of the market sell-off last March and its share price (while weak recently) has recovered strongly since then. Again, the position has been cut by about two thirds. AVI says that Softbank’s share buy-back activities helped its rating.

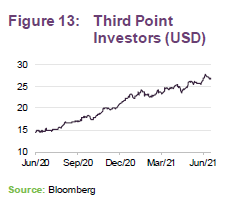

Third Point Investors

AGT’s stake in Third Point Investors (TPIL) was increased over H1 as AVI ramped up pressure on TPIL to tackle its discount. AGT has been a longstanding investor in the hedge fund run by Dan Loeb.

However, the fund has had a persistent discount problem. On 1 April 2021, TPIL proposed:

- the introduction of a discount control mechanism that will set a long-term target discount level of no more than 7.5% and buy-backs to move the discount towards this target;

- an implementation of two discount-triggered tender offers for 25% of NAV, at a discount of 2% to NAV. These will happen, if in the six-month periods ending 31 March 2024 and 31 March 2027, the average discount is more than 10% (for 2024) and 7.5% (for 2027);

- that the company will elect to receive an increased allocation to venture capital and private equity investment opportunities in the underlying Master Fund but only up to 20% of NAV;

- a new intention to employ gearing using a revolving credit facility. This will not exceed 15% of NAV and is intended to facilitate an ability to increase exposure at times of increased opportunity; and

- the creation of an exchange mechanism, pursuant to which qualified investors would be permitted to convert shares of the company for up to an aggregate of $50m of interests in the Master Fund.

AVI responded publicly on 26 May 2021. At that point, clients of AVI – including AGT – held 10.1% of TPIL’s ordinary shares. AVI said that TPIL’s proposals fell “woefully short of the structural changes that we believe are necessary to cure TPIL’s continuing trading discount to NAV problem”. It proposed a quarterly redemption mechanism at a price equivalent to NAV less costs and asked the board to put this proposal to a shareholder vote.

However, the situation is complicated by TPIL’s corporate structure, which includes class B shares owned by Third Point Offshore Independent Voting Company Limited (VoteCo). Those class B shares control 40% of TPIL’s voting rights and, therefore, AVI’s shareholding was not sufficiently large to demand an extraordinary general meeting. AVI appealed to VoteCo’s board to back its requisition. The VoteCo board declined to do so.

On 5 July, AVI came back again, this time with the support of three other shareholders. On this occasion, their combined shareholdings were sufficient to force a meeting. However, the TPIL board rejected the requisition on the grounds that the proposal was structured as an ordinary resolution (requiring a 50% majority to pass) and the law and the company’s articles prevented the company being bound by anything other than a special resolution.

TPIL’s discount had narrowed significantly – hitting around 9% on 5 July – and the fund’s performance has been very strong over the past year. AVI is considering its next steps. We note that TPIL’s discount is now 12.1%.

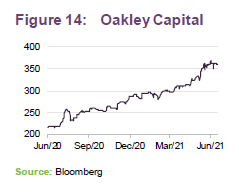

Oakley Capital Investments

Oakley Capital Investment’s performance has been strong over recent years (upper quartile over most time periods). On paper, Oakley’s discount has narrowed significantly over H1. However, it may be wider than it appears as, the last-published NAV was at end December 2020. AVI expects to see an uplift in the NAV at the end of June. The position has been trimmed in recent weeks, but AVI still likes the Oakley proposition. AVI says that the manager is good at repeat and complex deals.

NB: Oakley Capital Investments released an NAV update on 28 July 2021 which we unfortunately did not pick up before this was published. The NAV at end June 2021 was 445p. This compares to a current (9 August 2021) share price of 352p. On that basis, Morningstar estimates that it is trading on a discount of 21%, which is far too wide in our view.

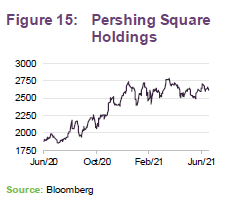

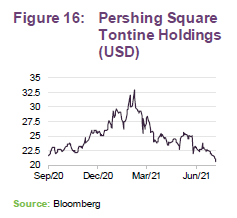

Pershing Square Holdings

AVI has had a position in Pershing Square Holdings (PSH) for a while and recently it also made an investment in Pershing Square Tontine Holdings (PSTH – an NYSE-listed SPAC created and part-financed by PSH).

The stake was acquired after the announcement that the SPAC would be used to fund the purchase of a stake in Universal Music Group as that business is spun out of Vivendi. Vivendi plans to retain a 10% stake in that business, PSTH planned to buy 10%, Vivendi’s other 60% is being spun out to its shareholders.

Other investors in PSTH did not appear to be fans of the proposal. The share price fell sharply – allowing AGT to acquire it at a discount.

However, AVI likes these music businesses. Universal Music forms part of an oligopoly with Warner Music and Sony (which AGT also holds). These firms tend to own recording rights. AVI feels that the scale of these companies gives them important negotiating leverage with artists, but it still expects modest pressure on margins. AGT also has stakes in Hipgnosis Songs Fund and Round Hill Music, which tend to own publishing rights.

Total revenue from recorded music today is 55% lower than it was pre-piracy in 2002 (inflation adjusted). Music-streaming is driving a recovery for the sector. This revenue has the advantage of being higher-quality in that it offers good visibility, low churn and offers consumers good value for money (helped by a much lower distribution expense).

AVI’s assessment of PSTH’s value was based in part on a read-across from Warner Music. Sony Music, buried within the wider business, is of limited use in this regard. However, Warner has a very limited free float and AVI suggests that other streaming/subscription businesses, such as Netflix and SaaS companies, may offer better comparisons.

Pershing’s plans for PSTH have been frustrated by the SEC, which questioned the legality of the proposed deal. PSTH’s rights to acquire the Universal Music stake have been assigned to PSH and Pershing is looking for an alternative initial acquisition for the SPAC (it has an 18-month time limit on this unless PSTH investors agree to extend this). It is possible that whatever deal Pershing comes up with will fire investors’ enthusiasm again and lead to a re-rating of PSTH. While the news was disappointing, AGT also has a top five position in PSH, which will now end up with a larger exposure to UMG. PSH’s ownership of PSTH sponsor warrants could also benefit to a greater extent in any new deal struck by PSTH. AVI believes that the position in PSTH retains attractive optionality.

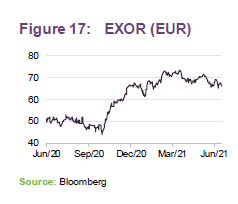

EXOR

EXOR is the Agnelli family holding company. AVI believes that the company trades on a substantial and persistent but unwarranted discount to NAV. Gianni Agnelli’s grandson John Elkann took leadership of the family business in 2003, simplifying the group structure and creating EXOR in 2009. He has subsequentially diversified the business exposure through the acquisition of Partner Re, and unlocked significant hidden value from what was then FIAT.

In 2014, FIAT bought Chrysler for $1. That deal gave it valuable access to the light truck, SUV, and Jeep markets. In 2019, following a failed attempt to merge with Renault, FIAT Chrysler merged with Peugeot to form Stellantis. EXOR retains a 14.4% stake in that business and John Elkann is its chairman.

Stellantis

AVI feels that the €5bn of annual synergistic benefits from that combination are, as yet, unrecognised by the market. Stellantis trades on a 25%–35% discount to GM and Ford (based on P/E and EV/EBIT), yet it is targeting long-term double-digit margins, significantly ahead of previous guidance and potentially making it the world’s most profitable automaker.

Stellantis held its ‘electrification day’ on 8 July 2021. AVI believes that investors have been nervous about the potential impact of measures taken to tackle climate change on the business. Stellantis announced a €30bn investment plan (to be deployed between 2021 and 2025) with the intention that over 70% of its passenger car/light duty truck sales in Europe will be low emission vehicles by 2030. The equivalent target in the US is over 40%. This target will be supported by the development of a number of battery ‘gigafactories’ (more than five by 2030). AVI says that it views the day as an important initial step in changing the narrative on this stock.

However, not only has FIAT/Stellantis been repositioned, its weight within EXOR’s portfolio has been reduced from about 75% of EXOR’s NAV to about 30%.

Ferrari

In 2016, Ferrari was spun out of FIAT as a separate company. Ferrari’s business was slightly dented by the pandemic – a seven-week suspension of production reduced deliveries by 10% and its 2020 revenues ended the year 8.1% below those of 2019. AVI comments that Q1 2021 figures are encouraging, however, with revenue 7.6% ahead of 2019 levels and diluted EPS +16.8% compared to 2019. Ferrari expects to unveil its first all-electric vehicle in 2025.

CNH Industrial

CNH Industrial is another business that was spun out of FIAT. It has a range of industrial, agricultural and heavy road vehicles including brands such as Iveco, New Holland and Case. It recently strengthened its agricultural offering by acquiring Raven Industries. Volumes have recovered from the lows of 2020 and Q1 revenues were 41% up year-on-year and the company predicted revenue growth between 14% and 18% for 2021 over 2020.

CNH is planning to split the business between off-highway and on-highway later this year. AVI thinks that this will help highlight the value within the agricultural business.

PartnerRe

PartnerRe is the fourth significant business within EXOR. This Bermudan-based reinsurance company is benefitting from firmer pricing after the industry was impacted by COVID-19-related losses in 2020.

EXOR’s portfolio also includes a controlling stake in Juventus.

Luxury pivot?

While Stellantis, Ferrari, CNH and PartnerRe dominate, the group’s most recent investments in a 24% stake in Christian Louboutin and SHANG XIA – a Chinese luxury brands brand established in connection with Hermès – have caught AVI’s attention. AVI thinks that John Elkann may be considering a pivot towards luxury goods, and highlights rumours that EXOR is looking at acquiring Armani Group (denied by EXOR on 16 July). AVI thinks that this could have a big impact on the market’s perception of EXOR and help eliminate its sizeable discount to NAV.

Other recent portfolio changes

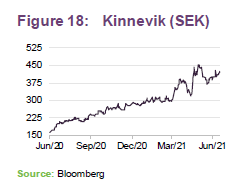

Kinnevik

Kinnevik has been a success story for AGT and is a position that AVI has been taking profits from. After Kinnevik span out its stake in online fashion retail business Zalando, it was trading at a high premium to asset value. AVI also notes that around half of Kinnevik’s assets are listed and therefore the implied premium valuation attributed to its unlisted investments is even higher. AGT no longer holds the stock but it remains on AVI’s watchlist as it thinks that it is a high-quality company.

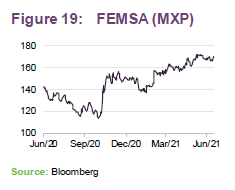

FEMSA

Fomento Económico Mexicano, S.A.B. de C.V. (FEMSA) is a recent addition to AGT’s portfolio. FEMSA is a Mexican conglomerate with stakes in Heineken and Mexico’s Coca Cola bottling company – both of which are listed – and account for about a third of NAV. Its main asset is a convenience store and small format retail business – FEMSA Comercio. Within this is the convenience store business – OXXO – a market leader with expanding margins and attractive returns on capital. FEMSA Comercio is already the largest chain of small-format stores in Latin America, but has ample room to grow in a highly-fragmented ‘mom and pop’-type market. AVI estimates that the implied value of FEMSA Comercio is less than 10x its EBITDA versus a long-term average of 14x.

FEMSA Comercio was affected by lockdowns last year but recent results for Q2 indicate a strong recovery.

In addition, there is some optionality in fintech as the company expands digital payments services within its stores and via a mobile app (“Spin by Oxxo”). This builds on previous initiatives – such as Oxxo Pay, which allows for instore payment of e-commerce purchases – as Oxxo aim to fulfil the needs of Mexico’s large unbanked population. AVI says that success in fintech would have very positive implications for margins and value creation.

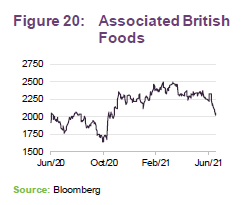

Associated British Foods

AGT is also now invested in Associated British Foods (ABF), which AVI sees as a potential COVID recovery play. The business is dominated by its high street fashion retail business – Primark – and its food ingredients operations, including British Sugar.

Primark does not have an online presence. Its stores were shuttered for an extended period last year and AVI says that investors have punished ABF for this. However, AVI feels that Primark’s business model of permanently low prices would be compromised by the expense of online deliveries and returns, were it to go down the online route. Competition on the High Street has reduced as other players have shut stores – GAP, for example. AVI notes that the queues outside Primark’s stores when they re-opened demonstrated pent-up demand.

AVI says that the rest of the business – ingredients and groceries is low-growth but cash-generative. It does not think that the controlling Weston family want to buy back ABF’s stock, and therefore believes that it is likely that the dividend will be hiked instead. AVI feels that a high dividend supported by strong cashflow should attract dividend investors and drive up the share price.

Berkshire Hathaway

AGT now holds Berkshire Hathaway. AVI feels that it is a beneficiary of the US stimulus. It also thinks that its railroad operations are undervalued. AVI comments that the price multiples that peers are trading on suggest that Berkshire Hathaway may be trading on a high teens discount.

UK property COVID-recovery

AGT has exposure to Capital & Counties (owner of Covent Garden and a stake in Shaftesbury), Shaftesbury (owner of Carnaby Street and China Town) and Secure Income REIT (owner of over 120 Travelodge hotels, a number of properties let to Merlin Entertainments in the UK and Germany and a portfolio of healthcare properties). The attraction in AVI’s eyes is that these are all COVID recovery plays, especially as tourist numbers start to pick up. Valuations may also be reinforced by the bid activity in the sector in respect of companies such as St Modwen, GCP Student Living and even Wm Morrison Supermarkets, where part of the attraction for the bidders is likely to be its extensive property portfolio in AVI’s view.

Performance

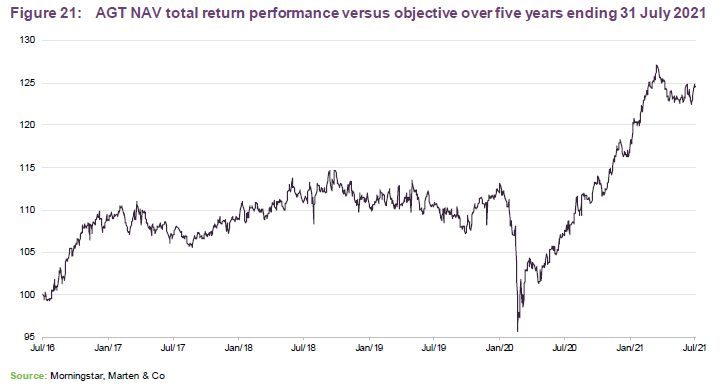

AGT quickly made up the March 2020 COVID-19-related underperformance of its benchmark (which reflected a widespread widening of discounts) and has since powered ahead. Its performance has been helped in part by a resurgence of interest in value stocks from November 2020 onwards.

In June, markets flipped back into focusing on growth stocks once again. This has weighed on AVI’s short-term performance.

Drivers of returns

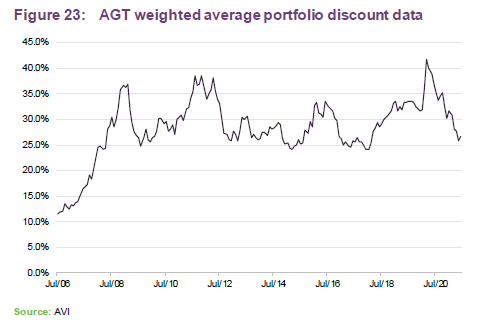

Figure 23 illustrates the substantial narrowing of discounts that AGT has benefitted from since the Spring of 2020.

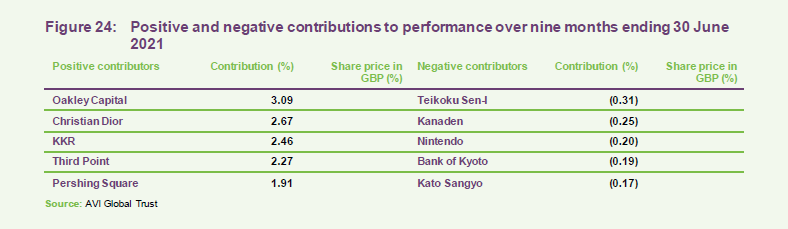

AVI has published some information on the stocks that contributed to AGT’s returns over the nine-month period ending 30 June 2021, which we reproduce in Figure 24.

Strong underlying performance and a narrowing discount helped propel Oakley Capital’s share price higher.

Christian Dior’s LVMH business has just reported H1 2021 revenue up 56% when compared with 2020 and 11% when compared with 2019. The business has largely shrugged off the adverse effects of the pandemic, although travel-related sales are still depressed, affecting perfume and cosmetics sales in particular. Profits soared within its fashion and leather goods division. Tiffany is said to have been successfully integrated within the business and is performing well.

Impressive growth in AUM (a near-doubling over three years) and good returns have boosted KKR’s fee revenues. The business has diversified from a pure private equity to an alternative assets focus and KKR sees considerable opportunity for further growth.

On the downside, Japan’s underperformance of other developed markets contributed to relatively small losses on a basket of Japanese stocks.

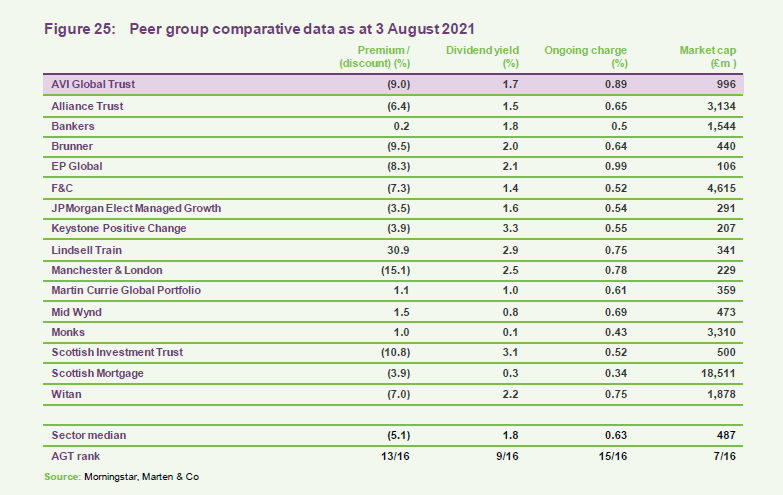

Peer group

AGT is a constituent of the AIC’s Global sector. The members of this peer group invest predominantly in listed equities.

Since we last published on AGT, the sector has expanded with the addition of Keystone Positive Change, which migrated from the UK All companies sector after its management contract was awarded to Baillie Gifford and its mandate changed, and Blue Planet, which has migrated from the financials sector, but which we have excluded from comparative data as it has a market cap of less than £15m.

Whilst comfortably in single digits, AGT’s discount is wider than average within its sector. None of these funds is particularly focused on generating a high dividend yield. AGT’s ongoing charges ratio is on the high side within this peer group. On a market cap basis, AGT is hovering around the £1bn mark.

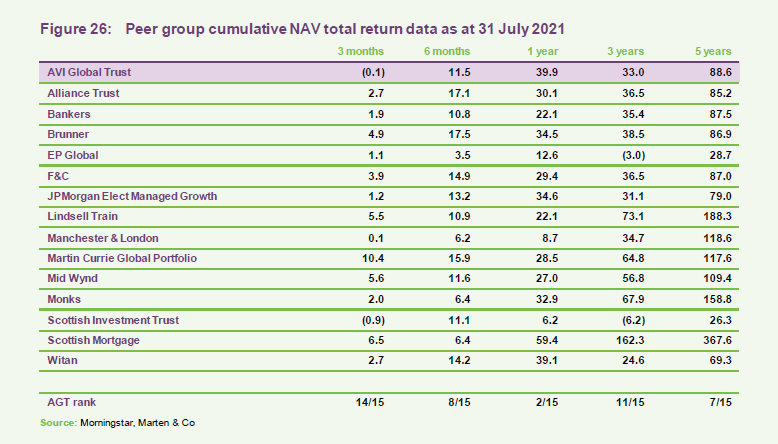

AGT’s strong run of performance towards the end of 2020 propelled it close to the top of the peer group performance tables over one year. More recently, nervousness about new variants delaying a return to more normal levels of economic activity may once again be favouring growth-focused trusts.

We have excluded Keystone Positive Change from Figure 26 as its historic performance reflects its previous UK-focused mandate.

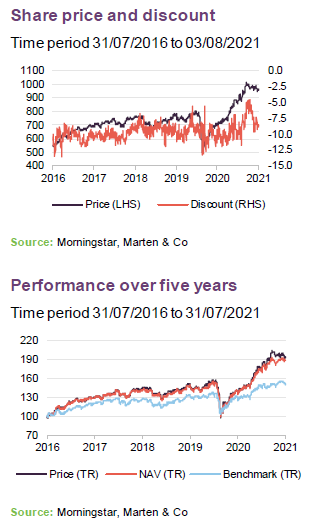

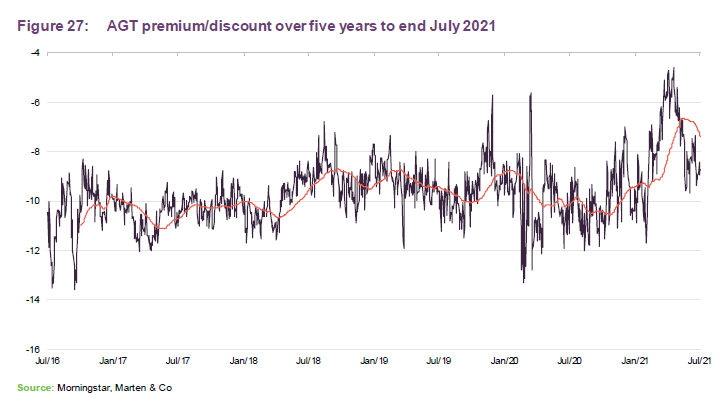

Discount

Over the year ended 31 July 2021, AGT’s discount moved within a range of 12.0% to 4.6% and averaged 8.8%. At 3 August 2021, AGT’s discount was 9.0%.

At the AGM in December 2020, shareholders approved resolutions empowering the board to buy back up to 14.99% of its then-issued share capital (equivalent to 15,761,742 shares) and issue up to a third of its then-issued share capital (equivalent to 35,049,460 shares). A separate resolution granted permission for 5% of the then-issued share capital to be issued without pre-emption.

AGT’s board uses share buybacks with the intention of limiting volatility in AGT’s discount. Over the six months ended 31 July 2021, around 1.5m shares were repurchased. Buying back shares at a discount enhances the NAV per share.

The board also employs a marketing budget (administered by the investment manager) with the aim of stimulating demand for the trust’s shares.

Fund profile

AGT aims to achieve capital growth through a focused portfolio of investments, particularly in companies whose shares stand at a discount to estimated underlying net asset value. It invests in quality assets held through unconventional structures that tend to attract discounts; these types of companies include family-controlled holding companies, closed-end funds, and cash-rich Japanese operating companies.

For performance measurement purposes, the company compares itself to the MSCI All Country World ex-US Total Return Index, expressed in sterling terms. Whilst it has some exposure, relative to an unconstrained global index, the trust has a sizeable underweight exposure to the US, primarily because there are fewer opportunities to invest in family-controlled holding companies.

AGT’s AIFM is Asset Value Investors (AVI). AVI was established in 1985, when the trust’s current approach to investment was adopted. At that time, AGT had assets of just £6m and was known as the British Empire Securities and General Trust, later shortened to British Empire Trust. The trust adopted its current name on 24 May 2019.

Previous notes

Readers may wish to refer to our initiation note, published on 25 January 2021 – Double discount on quality focused portfolio.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on AVI Global Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained in this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained in this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.