BlackRock Throgmorton – AGM update

Investment companies | Flash note | 20 March 2024

Throgmorton’s fuse is lit

In yesterday’s BlackRock Throgmorton (THRG) annual general meeting, manager Dan Whitestone outlined the significant potential for a surge in UK equities, with small and mid-caps outperforming large caps by a sizeable margin, as the macroeconomic outlook in the UK improves.

Dan highlighted that UK companies’ share prices have become increasingly detached from their earnings potential. A combination of political uncertainty thanks to the forthcoming elections, sticky interest rates, strength in overseas stock markets (in particular in a handful of big AI-related US tech names), and consistent outflows of investments in UK-focused funds has weighed on valuations.

Dan believes that the UK small and mid-cap sector is at one of its most attractive entry points in recent memory, based on current share prices. We observe that Dan is not alone in this view, with the UK market being subject to elevated levels of takeover activity.

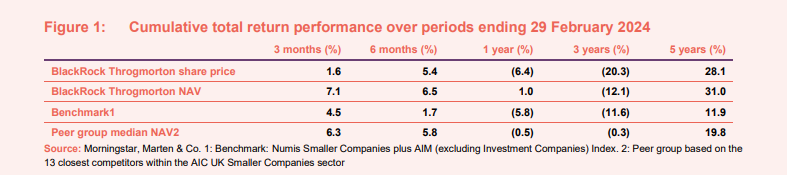

Despite this backdrop, Dan has still been able to demonstrate the merits of good stock picking, having generated strong long-term out outperformance versus his peers and benchmark.

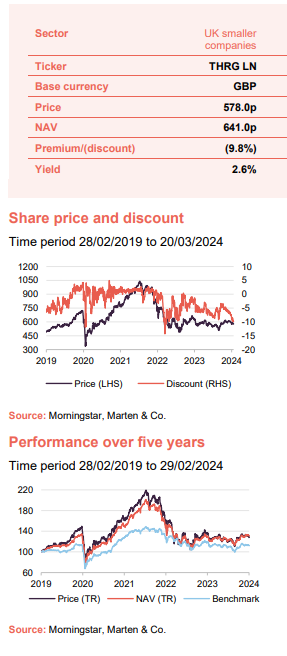

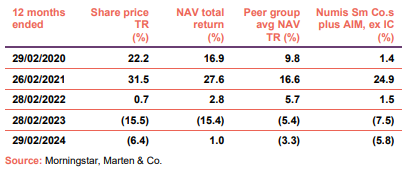

THRG’s board has substantially increased its share buyback activity. Nonetheless, THRG’s discount remains at a historically wide level and may offer investors an attractive way to capitalise on a possible near-term bounce in UK companies.

UK equities markets are ripe for recovery

The UK equity market trades at a wide disconnect from its earnings potential

Following what has been a torrid time for the relative performance of UK equity markets when compared to its developed peers, with the share price performance of UK companies having become increasingly detached from their earnings potential, Dan Whitestone believes that UK markets are ripe for a sharp bounce and feels that could happen very quickly.

Dan’s investment approach favours high-growth, high-quality companies. Nevertheless, he says that the earnings figures for his holdings have often exceeded his own forecasts during the last year, vindicating his increasing bullishness around THRG’s prospects.

Falling inflation and a forthcoming election may be catalysts for a UK rebound

Dan has identified two potential near-term catalysts for a rebound in UK equities, with small cap companies being amongst the strongest beneficiaries. The first is a return to target UK inflation, and the scope that should create for interest rate cuts, and the second is the forthcoming election.

Estimates from the Office for Budget Responsibility indicate that UK inflation will fall further to an average of 2.2% over 2024 and 1.5% in 2025, bringing it below the 2% target of the Bank of England. This, combined with sub 1% GDP growth expectations for the UK, may place sufficient pressure on the Bank of England to cut interest rates, stimulating a recovery. At 3.4%, the latest UK inflation figure (announced today) came in below expectations, adding further pressure on the Bank of England.

Lower inflation, and by extension interest rate expectations, could be very positive for THRG, as it was caught up on the growth-stock selloff of late 2021 and 2022, a result of rising interest rate expectations.

While there appears to be little uncertainty about the outcome of the general election in the UK, policy announcements from the Labour leadership suggest it will be following a fairly centrist and fiscally responsible approach. This suggests that, after an extended period where political infighting, numerous policy missteps and U-turns have provided an excuse to avoid the UK, the election will give way to a period with much reduced political risk.

UK businesses and consumers remain robust

Even without a catalyst for a reversal, Dan believes that much of the negative sentiment around the UK economy is overstated. He notes that UK business confidence has seen a remarkable rebound over 2023, with the Lloyds Bank Business barometer (a metric that tracks business confidence) having reported a net positive of 35%, well above its 25-year average of 28% (a period which filters out much of the recent economic pain).

The UK consumer is also showing signs of sustained strength, with the average UK household income increasing almost consistently over 2023, topping out at a 10% year-on-year increase (based on weekly sampling).

Further evidence of the relative attractiveness of UK valuations is provided by the upsurge of merger and acquisition activity over 2022 and 2023, as larger companies and private equity have pounced on undervalued UK stocks. THRG’s recent performance has already benefitted from the takeover of some of its holdings, with Dechra Pharmaceuticals being one such example.

Meanwhile, UK companies are also net buyers of their own stock, with 13% of large UK companies buying back at least 5% of their shares over 2023, according to research by Schroders. This compares with 9% in the US, which has often been viewed as the major market for buyback activity. Not only have these activities been supportive of THRG’s NAV but they also serve as solid evidence of the opportunity presented by UK companies, given that its current valuations are attracting strategic buyers.

The market has already started to move

THRG has generated both short and long-term outperformance thanks to Dan’s stock picking skill

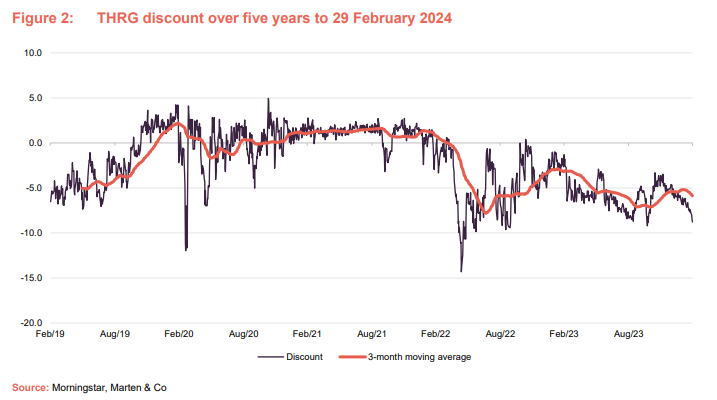

In retrospect, it looks as though the turning point for the market’s recovery may have been the growing realisation in October 2023 that interest rates had peaked. While it has not been a smooth ride since, thanks to a couple of disappointing inflation figures, we have already begun to see a reversal of previous trends, with THRG generating sector and benchmark beating performance since then and over the last 12 months, as can be seen in Figure 1. We note that despite the magnitude of the drawdown during 2022, THRG’s long-term performance remains sufficiently good to place it well ahead of its benchmark and peers over longer time periods.

THRG’s recovery aligns with Dan’s notion that its underperformance during 2022 was primarily the result of the rise in interest rates, rather than structural weaknesses in his companies.

While Dan believes that there are clear near-term tailwinds helping THRG, he has positioned the portfolio to benefit from long-term structural growth trends that he expects will drive the trust’s performance. The majority of THRG’s long-term outperformance (relative to its benchmark) should always be expected to come from successful stock selection and not from gaming the macroeconomic environment.

Anomalous discount, attractive entry point?

THRG’s board has been proactive in buying back shares

THRG’s board has substantially increased its share buy-back activity since the start of 2023. Over the last 12 months THRG’s board has repurchased about 7% of the trust’s outstanding shares. Yet despite this effort, THRG’s discount has not been immune to the general weakness of investment company discounts, trading on a 9.9% discount currently.

THRG’s discount has a 12-month z-score of -2.67 (a score below -2 implies that its discount is more than 2 standard deviations below its 12-month average, a wide level by statistical standards).

We believe that this wide discount, combined with the near-term opportunities in the UK small cap equity market and THRG’s historic out-performance, makes the trust a compelling opportunity for those looking to capitalise on a possible bounce in UK equity markets.

IMPORTANT INFORMATION

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on BlackRock Throgmorton Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.