Investment Companies Monthly Roundup

Kindly sponsored by abrdn

December 2022

Monthly | Investment companies

Winners and losers in November 2022

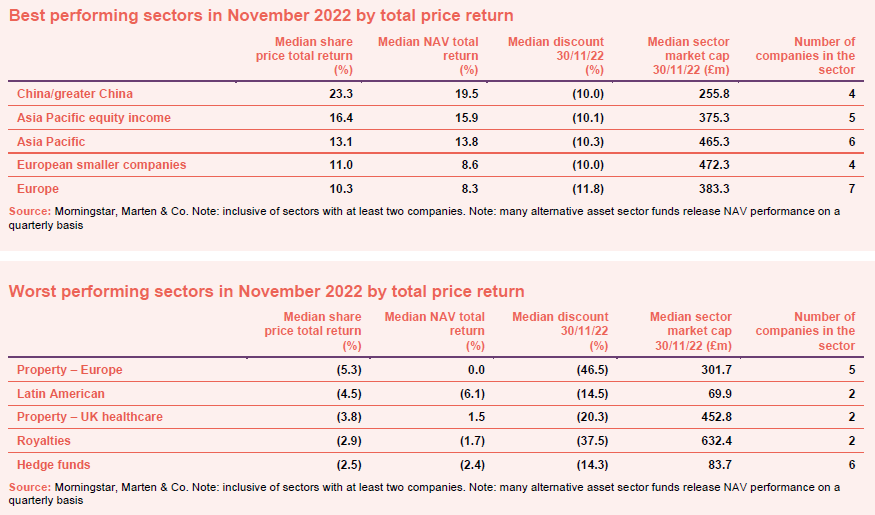

As discussed in this month’s economic and political roundup, lower US inflation triggered a fall in the US dollar and drove equity markets higher over November. The big surprise was the resurgence of Chinese markets on the hope of an easing of its zero-COVID policy, in spite of a rapid rise in cases. We would be cautious about a return to lockdowns in the country given poor vaccination rates/vaccine efficacy. Rising Chinese markets boosted Asia Pacific funds too. Warm weather has helped Europe build its gas reserves and eased power prices, helping those economies.

Higher interest rates are a problem for property companies – many have been hit by rising borrowing costs and valuation yields. Latin American funds gave back some of the gains that they have made recently. A weaker dollar hit the royalties funds, which derive a substantial proportion of their revenue from the US, and also a number of dollar denominated hedge funds.

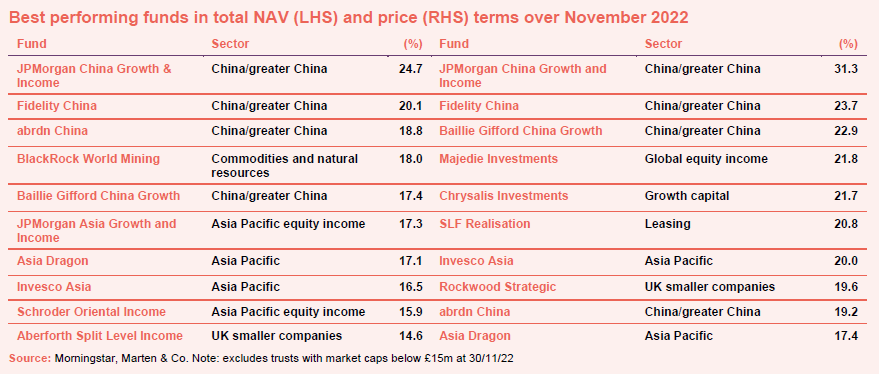

The hope of easing of zero-COVID policies is responsible for almost all of the sizeable jumps in NAV of funds exposed to China, Asia Pacific and even BlackRock World Mining, which is up on hopes that China’s economy will grow and suck in more industrial metals. abrdn China lagged its peers, it tends to have a more conservative approach to its stock selection.

Aberforth Split Level Income is the exception. Its NAV returns are amplified (in both directions) by its split capital structure. UK small cap recovered from the worst of the impact of ‘Trussnomics’ over the month. Some companies and private equity funds have been taking advantage of the turmoil in the UK market, bidding for listed stocks. This is also helping sentiment.

Generally, share prices moved up faster than NAVs in the China/Asia sectors, narrowing discounts. Majedie did well as it announced another change of manager.

Chrysalis is recovering too. A recent capital markets day showcased some of the exciting businesses within its portfolio. A presentation by its independent valuation committee may have also helped reduce scepticism abouts its NAV. SLF Realisation announced a return of capital.

Rockwood Strategic is a beneficiary of the bounce in UK small caps. Its interim results, announced in the month, were well received by investors. The board hopes to be able to grow the company.

Worst-performing

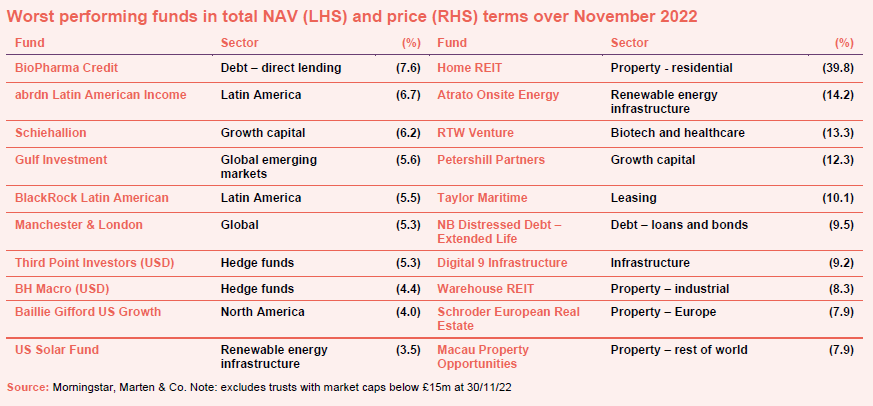

On the negative side, the major influence on NAVs is the weaker US dollar. That affected BioPharma Credit, Schiehallion, Manchester & London (which has almost all of its portfolio invested in the US), Third Point Investors, BH Macro, Baillie Gifford US Growth and US Solar Fund. A weaker oil price weighed on Middle Eastern markets, hitting Gulf Investments.

The fall in Latin American funds may be related to the election of Lula in Brazil – the market has fallen since the result was confirmed. Weaker commodity prices may be having an impact here too.

Looking at share price falls, Home REIT tops the list with a precipitous, almost 40% drop, in its share price. The company was attacked by a short seller and, despite rebutting the claims, the REIT’s share price remains depressed (in fact it has come under attack from a new direction since the end of the month).

Atrato Onsite Energy published results during the month, revealing that its dividends were uncovered by earnings – mainly because it has been slow to get its IPO proceeds invested.

RTW Venture has experienced a marked widening of its discount recently. It is changing its US tax status, but this has no impact on investors outside the US, so this might represent some temporary indigestion as US investors react to the news.

Petershill issued a trading statement on 22 November. Net management and advisory fees have fallen year-on-year, but the share price move might be related to the completion of its share buyback programme. Taylor Maritime won control of Grindrod Shipping during the month, but there’s nothing to indicate why its shares would be weaker. Digital 9 Infrastructure has lost its management team.

Moves in discounts and premiums

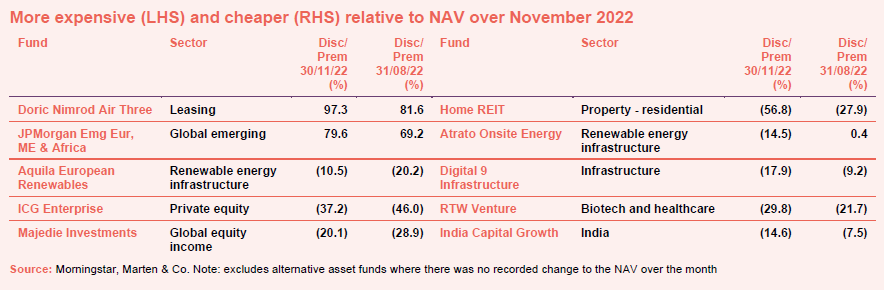

The aircraft leasing funds have been in greater demand since Doric Nimrod Air One announced that it had agreed to sell its A380 to Emirates. JPMorgan Russian got shareholders’ approval to adopt its new investment policy and changed its name to JPMorgan Emerging Europe, Middle East and Africa Securities. The premium rose as investors were reassured that the company would not issue stock. Aquila European Renewables also changed its name (from Aquila European Renewables Income Fund – no we aren’t sure why it bothered either), but the narrower discount might reflect good news from its Norwegian wind farm project, where 95% of the turbines are now in operation. We have been puzzling as to why private equity discounts are so wide for some time now, it was good to see ICG Enterprise’s move in the right direction. As stated above, Majedie’s new management arrangements pleased investors.

We have discussed most of the funds that experienced discount widening over November above. India Capital Growth is, by some distance, the best-performing Indian fund over the past six months. However, as the Indian market keeps hitting new highs, investors appear to be nervous, and discounts have become more volatile. The trust’s discount has narrowed since the month end.

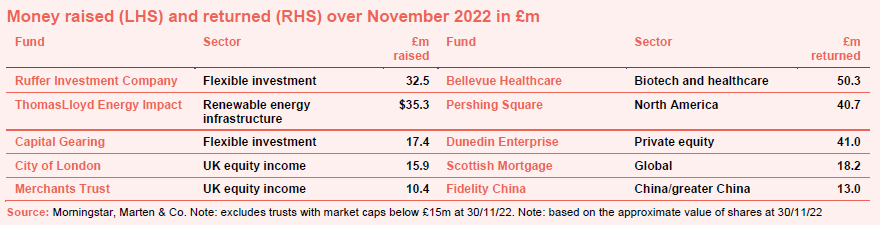

Money raised and returned

This month we said goodbye to Fundsmith Emerging Equities (now in liquidation) and Independent Investment Trust (merged with Monks). There has been very little fundraising within the sector in recent months, but three new funds are trying to get off the ground. We have published an IPO note on Conviction Life Sciences, James Carthew wrote an article about AT85 for Citywire and Long Term Assets was discussed on our weekly show on 18 November.

However, it looks as though we may be losing Starwood European Real Estate Finance and NB Global Monthly Income.

Issuance and shrinkage in the above table largely reflect tap issues (dripping stock into the market to match ongoing demand) and share buy backs. ThomasLloyd Energy Impact is worth a mention. When it launched its recent placing, it said it had demand from certain European investors who had been unable to come into the fund at the time of the IPO. Support from this area may have been a factor in its $35m fundraise. The outflow from Bellevue Healthcare came from its annual redemption opportunity. Holders of 5.2% of the trust opted for redemption of their shares.

Major news stories and QuotedData views over November 2022

Upcoming events

Here is a selection of what is coming up. Please refer to the Events section of our website for updates between now and when they are scheduled:

Interviews

Have you been listening to our weekly news round-up shows? Every Friday at 11 am, we run through the more interesting bits of the week’s news and we usually have a special guest or two answering questions about a particular investment company.

| Friday | The news show | Special Guest | Topic |

| 30 September | BSIF, discount rates | Masaki Taketsume | Schroder Japan Growth |

| 7 October | VNH, SONG | Simon Farnsworth | Life Science REIT |

| 14 October | TMI, HEIT | Jonathan Maxwell | SDCL Energy Efficiency |

| 21 October | HICL, DORE | Ross Driver | Foresight Solar Fund |

| 28 October | JPE, JRS | Joe Bauernfreund | AVI Japan Opportunity |

| 4 November | ROOF, CYN, PEY | Jason Baggaley | abrdn Property Income |

| 11 November | MAJE, TLEI, CRS | James de Uphaugh | Edinburgh Investment Trust |

| 18 November | Long Term Assets, Renewables | Jeff O’Dwyer | Schroder European Real Estate |

| 25 November | Renewables, DGI9, NBMI, HOME | Bruce Stout | Murray International |

| 2 December | CHRY, SYNC | Rhys Davies | Invesco Bond Income Plus |

| Coming up | |||

| 9 December | Stuart Widdowson | Odyssean | |

| 16 December | Richard Aston | CC Japan Income and Growth | |

| 6 January | Andrew McHattie | Review of 2022 | |

Guide

Our independent guide to quoted investment companies is an invaluable tool for anyone who wants to brush up on their knowledge of the investment companies’ sector. Please register on www.quoteddata.com if you would like it emailed to you directly.

Research

There has been a distinct shift in sentiment towards financials stocks and Polar Capital Global Financials Trust (PCFT) since Spring 2022. As fears of economic recession grew, initial enthusiasm about the positive effects of rising interest rates on banks’ profit margins gave way to concern about the prospect of higher loan defaults. However, these have not materialised, and PCFT’s managers think it is likely that they will not.

Dan Whitestone, manager of BlackRock Throgmorton (THRG), remains steadfast in his commitment to the most-attractive, highest-quality growth opportunities within the UK small cap sector, despite the apparent headwinds facing this strategy.

Whilst THRG has lagged its benchmark and peers recently, having been caught up in the wider growth-stock selloff, the vast majority of Dan’s investee companies continue to demonstrate the same fundamental strength and resilient business models, albeit now at much more attractive valuations. In fact, several companies have posted stronger results over 2022, despite the difficult circumstances that they face.

Conviction Life Sciences Company (CLSC) has a target issuance of up to 100m ordinary shares at 100p per share as part of the company’s initial issue, equal to an initial market cap of up to £100m.

CLSC is being launched to capitalise on two avenues of return presented by the global life sciences and medical technology markets, the first being the inherent structural growth opportunities which are presented by the sector, and the second being what the directors believe is a materially undervalued sector, particularly outside of the United States. CLSC’s addressable markets will include, for example, novel therapeutics (both large- and small-molecule), medical technology (including devices and diagnostics), pharmaceutical services, and digital health.

Even considering the particularly challenging markets we have seen during the last couple of months, Ecofin Global Utilities and Infrastructure Trust (EGL) has posted a very respectable performance and has been issuing shares. This most likely reflects the long-term strong structural growth drivers, inflation linkages and the defensive (less economically sensitive) nature of its investments, in an environment where the global economy is slowing down and tipping into recession.

The share prices of many logistics-focused real estate investment trusts (REITs), including Tritax EuroBox (EBOX), have been hit as interest rates have risen and the investment market has cooled. Inevitably, valuations in the low-yielding logistics property sector will fall (and property yields rise) as the higher cost of debt chokes off investment.

However, the occupier market is still a landlord’s market, with record low supply and robust demand putting owners in an advantageous position, meaning rental growth is very much in the picture. This will have an offsetting effect on softening (rising) property yields. EBOX has announced a number of leasing deals at significant uplifts to previous rents and with superior terms, such as annual uncapped inflation-linked uplifts.

More than five years after it refocused its global equity portfolio, Alliance Trust (ATST) has proven the merits of blending different expertise across different investment styles. Its manager, Willis Towers Watson, has been able to demonstrate the benefits of its balanced, multi-manager strategy. By eschewing a single investment style bet (such as ‘growth’ or ‘value’) in favour of a focus on stock picking, ATST has been able to provide handy outperformance of the majority of its peers over 2022.

ATST has also implemented a new dividend policy, which has substantially enhanced its pay-outs. The trust now has a 2.4% yield, and the board aims to extend its 55-year track record of increasing the dividend every year.

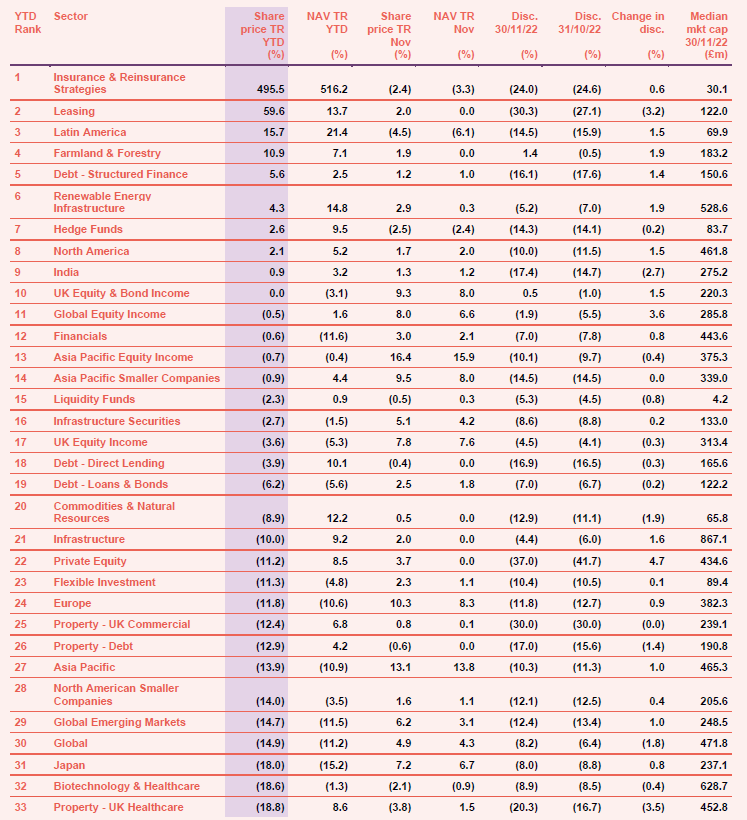

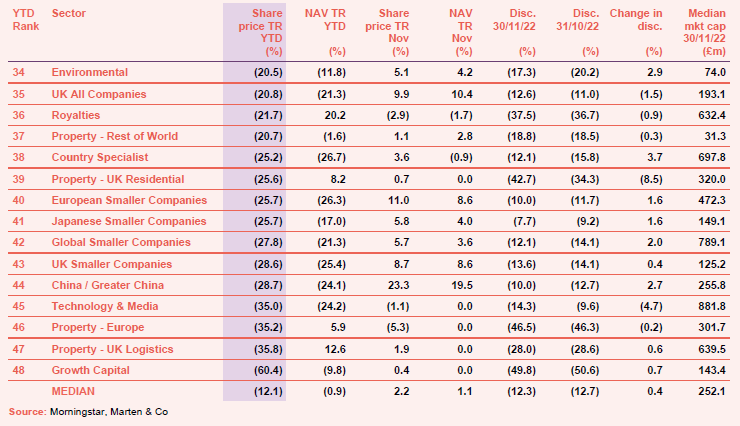

Appendix 1 – median performance by sector, ranked by 2022 year to date price total return

The Legal Bit

This note was prepared by Marten & Co (which is authorised and regulated by the Financial Conduct Authority).

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

Marten & Co may have or may be seeking a contractual relationship with any of the securities mentioned within the note for activities including the provision of sponsored research, investor access or fundraising services.

The analysts who prepared this note may have an interest in any of the securities mentioned within it.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.