Confidence rewarded

In mid-December 2020, when QuotedData last published a note on BlackRock Throgmorton Trust (THRG), its manager Dan Whitestone said he was genuinely excited about the prospects for the stocks in its portfolio. That enthusiasm has been vindicated by the strong performance since and the many investors that have embraced the trust over the past year have been well-rewarded.

Dan highlights the breadth of opportunity afforded by the stocks in THRG’s portfolio. His confidence in the outlook for these companies is undimmed and, reflecting this, THRG’s net market exposure is at the high end of its range (see page 8).

Both long and short positions in UK small- and mid-cap companies

THRG aims to provide shareholders with capital growth and an attractive total return by investing primarily in UK smaller companies and mid-capitalisation companies traded on the London Stock Exchange. It uses the Numis Smaller Companies Index (plus AIM stocks but excluding investment companies) as a benchmark for performance purposes, but the index does not influence portfolio construction. Uniquely among listed UK smaller companies trusts, THRG’s portfolio may include a meaningful allocation to short as well as long positions in stocks.

Investors returning to growth and quality

As we explain from page 5 onwards, the composition of THRG’s portfolio is driven by stock selection rather than the manager’s view of the direction of markets or the UK economy. However, it appears as though, since the terms of Brexit were agreed and the UK vaccination programme against COVID-19 gathered pace, international investors are more interested in the UK stock market than they were. Smaller companies have outperformed, the IPO market has opened up – THRG bought some of these, although not all were attractive in Dan’s view – and there are signs that M&A activity is picking up.

Commentators suggest that hope of an end to lockdowns led to a rotation into more cyclical and ‘value’ stocks, which was exacerbated by fears of rising inflation, and a steepening yield curve. Dan cautions against extrapolating too much from the recent spike in inflation, which he attributes to shorter term factors such as supply chain bottlenecks and staff shortages (notably in the leisure industry) which have been exacerbated by furlough schemes. However, a key focus within Dan’s investment process is pricing power, so where there are instances of rising costs, either raw materials or wages, it is imperative those companies can pass these costs on, which Dan thinks his companies are well positioned to do.

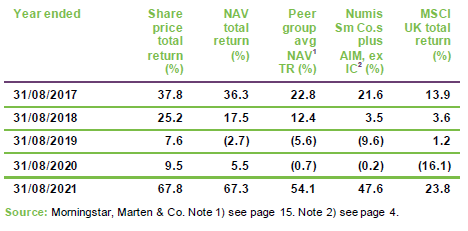

Dan had no intention of attempting to time markets by taking profits from THRG’s growth-focused companies and recycling the proceeds into ostensibly-cheaper value stocks. Consequently, the cyclical/value rally could have been expected to proved a headwind to performance. However, he says that over 2021, individual holdings’ impressive results and earnings upgrades have helped THRG to extend its outperformance of both its benchmark and the average of its peer group (see page 15).

Talking to Dan, he is as excited about the prospects for the stocks in THRG’s portfolio as he was at the end of 2020. For many, he says that the investment case is just getting stronger. He believes that, as economies tried to adapt to lockdowns, the pace of change underway in many industries accelerated. Dan feels that the ‘corporate Darwinism’ that we have discussed in previous notes has been reinforced as technological advances such as the shift to online/cloud-based services disrupts many business models.

Dan feels that the run-up in the share prices of some cyclical/value stocks has already run out of steam. He suggests that cyclical companies may be seeing increased demand, but this is associated with higher raw material and labour costs. However, an inability to pass on these on is leading to disappointment and a re-evaluation of whether investors want to own these businesses, in his view, which is coupled with concerns over the impact of new COVID variants. He concludes that companies experiencing secular growth and those with pricing power, like the ones in THRG’s portfolio, are therefore popular once again.

Fund profile

BlackRock Throgmorton Trust (THRG) aims to generate capital growth and an attractive total return by investing primarily in UK smaller companies and mid capitalisation companies traded on the London Stock Exchange. It uses the Numis Smaller Companies Index (plus AIM stocks but excluding investment companies) as a benchmark for performance purposes, but the index does not influence portfolio construction.

For the period between 1 December 2013 and 22 March 2018, the benchmark was Numis Smaller Companies Index, excluding both AIM stocks and investment companies. There used to be a restriction on the trust’s exposure to AIM companies, but this was removed in March 2018 and, at the same time, the manager was given permission to invest up to 15% of the portfolio in stocks listed on exchanges outside the UK.

UK smaller and mid-capitalisation companies tend to outperform large companies over longer time-frames. In addition, the focus on smaller and mid-capitalisation companies offers exposure to a less-efficient and less-well-researched area of the market, which creates opportunities for an actively-managed fund to add value.

Both long and short positions

Uniquely among listed UK smaller companies trusts, THRG’s portfolio may include a meaningful allocation to short as well as long positions in stocks. Up to 30% of the portfolio may be invested in CFDs, both long and short. Under normal market conditions, the net market exposure will account for 100–110% of net assets.

The manager

BlackRock Investment Management (UK) Limited was appointed manager of the trust in July 2008. Dan Whitestone, head of the emerging companies team at BlackRock, has been sole manager of the trust since 12 February 2018 (he had been co-manager, alongside Mike Prentis, since March 2015). Dan heads a team of five. All members of the team manage portfolios, and between them they manage or advise on a variety of different funds. The team share research responsibilities between them.

Investment process

When selecting long investments for THRG, Dan focuses on identifying two types of opportunity: high-quality differentiated companies and companies leading industry change.

High-quality differentiated companies

Dan believes that high-quality companies have certain characteristics for long-term success, based on:

- management team;

- product;

- industry; and

- balance sheet/cash flow.

In Dan’s view, the most important factor in driving value creation or destruction is the quality of the management team. Its ability to have a vision, execute on strategy and adapt to a changing environment is crucial. The BlackRock team makes a point of meeting not only the top layer of management, but also other key people within a business. Dan believes that a common reason for growing companies experiencing “growing pains” is if they fail to build the infrastructure and depth of team beneath the top management layer.

Meeting management is a core part of the BlackRock team’s approach, and between them they probably have around 750 meetings a year. Usually, they try to have as many of the team in a meeting as possible, to get a diversity of viewpoint.

Dan looks for companies whose products are not purely competing on price, but instead offer solutions to customers’ problems – this gives the company pricing power and persistent demand for its products. It is also important that a company maintains its product’s relevance through R&D.

In Dan’s view, the industry that a desirable company operates in should have structural growth drivers. It should not be capital-intensive, nor cyclical. It should be free from regulatory interference and should not be facing competitors with strong financial support.

Dan avoids heavily indebted companies, believing that the CFO often ends up managing the company for the benefit of the bank rather than investors in these situations. He focuses on cash flow measures of value, as these are less easy to manipulate than profits. Dan looks for indicators of quality such as the conversion of sales into cash – such companies can establish a virtuous circle whereby excess cash can be recycled into sales efforts. A company trading on 25x cash earnings is preferable in his eyes to one on 10x earnings but with no cash flow. The latter are the types of companies that tend to be shorted (see page 7).

On average, THRG’s long investments trade on higher multiples than the short investments. Dan says that this reflects a focus on quality and a desire to avoid value traps.

Industry change

Industry change can provide both long and short ideas. Previously in his career, Dan was a strategy consultant. The experience highlighted the impact of disruptive change on industries and has influenced his thinking since. Dan says that small and medium-sized companies can be a good source of industry disruptors, as they need to do something special, or otherwise innovate, if they are to compete effectively.

He thinks that there are many ways that disruptive change can manifest itself. These include new products, changes to manufacturing that allow products to be sourced more cheaply, vertical integration to improve and extract cost from supply chains, and changes in distribution.

ESG

In recognition of their influence on the success or failure of business models, an assessment of ESG factors is incorporated throughout the research process. It impacts on ideas generation, forms an integral part of the due diligence phase – where ESG issues may be escalated and discussed with BlackRock’s Investment Stewardship team – and ESG conclusions are embedded within the research template that is used to monitor existing and prospective investments. ESG factor risk is assessed as part of regular portfolio reviews undertaken in conjunction with BlackRock’s Risk and Quantitative Analysis (RQA) group.

In conjunction with the Investment Stewardship team, the manager and analysts engage with portfolio companies on any ESG issues that have been identified.

Portfolio construction

Dan does not consider the benchmark when constructing the portfolio; consequently, the portfolio will tend to have a high active share.

Position sizes are driven by liquidity, risk considerations and conviction. Liquidity is important; Dan wants to be able to trade out of a position in the event that something is going against it. He says that he is ruthless about selling positions when the investment thesis is not working. As an aside, Dan says that historical average daily volume is a misleading indicator of future liquidity for small-cap stocks.

The target is to create a portfolio with 120 positions – about 80 long positions and 40 shorts. The number of shorts may seem large, but it is important that the short book is diversified. Dan points out that it is perfectly possible to accurately predict that an industry will suffer long-term decline, then select a stock to represent this, which is then subject to a bid, quite possibly from a competitor. This is because companies in declining industries frequently see consolidation as a remedy, although this may not work as a strategy in the long term. Nevertheless, he says that being short a stock that becomes subject to a bid can be costly. It is therefore better to own a spread of stocks to represent a theme.

The largest position size that Dan would be comfortable with is 5% – there is nothing in the portfolio that is as big as that now. At the low end, he wants to avoid having a long tail of small positions in the portfolio. Individual short positions (see below) are typically sized at about 0.5%–1.0% of net assets.

Essentially, Dan is a growth investor. He therefore believes that the portfolio may underperform in an environment where investors are favouring value stocks. Valuation is secondary to the investment thesis, in Dan’s opinion, but part of the assessment of the merits of a stock is an attempt to identify whether the market appreciates, and is therefore pricing in, the story.

Dan does not believe that mean reversion applies to the types of stocks that he is focused on; winners win big and losers go bust. Therefore, he does not trade stocks based on valuation differentials.

Shorting

About half of short positions represent themes – for example, industries under pressure. Dan cites the examples of pubs and restaurants, and out-of-town retail. These themes are expressed through several stocks in accordance with the approach outlined above. It is not as simple as shorting a basket of stocks in any given industry, however. Even within a struggling sector, there may be companies whose strategy allows them to survive or even thrive.

The rest of the book represents idiosyncratic shorts selected for stock-specific reasons. Companies with questionable accounting are a fertile hunting ground for shorts, although Dan says that sometimes these can take a while to come to fruition.

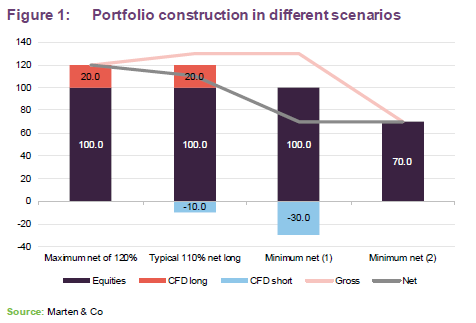

The board has set a maximum limit of net gearing of 20% and, in practice, gearing is provided by the CFD portfolio. The fund operates with an upper limit of 130% gross exposure to equities. Typically, this might comprise 100% in equities, 20% in long positions and 10% in short positions, i.e. a net exposure of 110%.

Cash balances are generally kept low and gearing is flexed by adjusting the size of the CFD book; Dan expects to operate within a range of 100% to 110% net long.

The manager has the flexibility to reduce net exposure to a minimum of 70%. This is more likely to be achieved by using shorts rather than holding cash (as illustrated by minimum net (1) rather than minimum net (2) in Figure 1).

Asset allocation

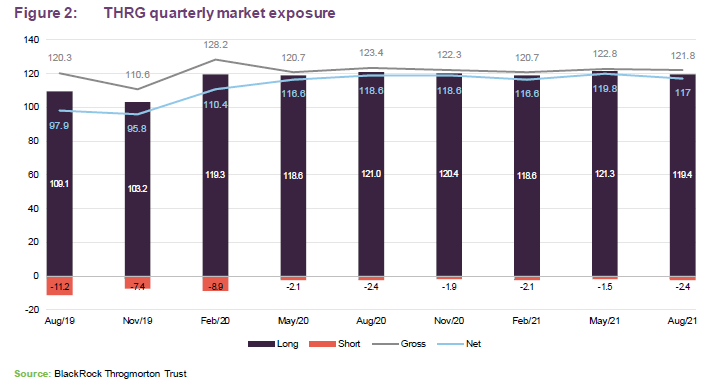

Figure 2 illustrates the sharp reduction in THRG’s short exposure between February and May 2020. The steady rebound in markets from their March 2020 lows vindicated that decision.

The end-May 2021 short position was historically low and has increased since then, but the overall level is still low relative to history. Dan is bullish, driven by an abundance of investable ideas, and added to positions in Q1 2021 in particular. However, Dan notes that there has been an uptick in the number of profit warnings from the types of fundamentally challenged companies that THRG only considers as potential short positions. He also feels that some valuations of cyclical stocks are looking overstretched.

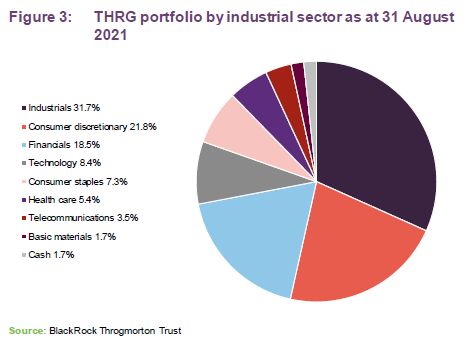

THRG’s sector exposures are driven by the manager’s stock selection decisions and the sector split is not much changed from when we last published.

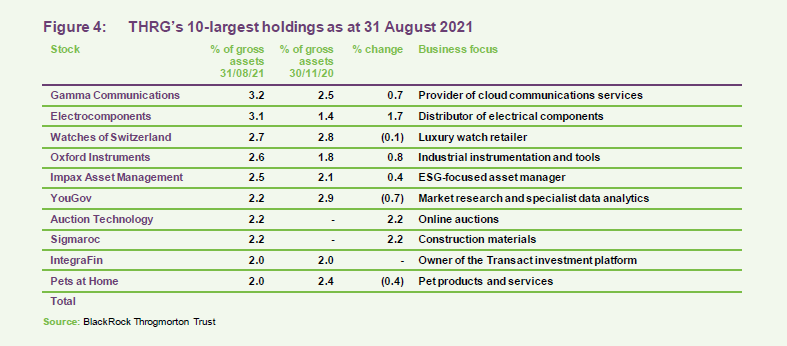

Top 10 holdings

The list of THRG’s 10-largest stock positions looks fairly different to the one we published in our last note – reflecting the sea-change in markets since then.

Games Workshop, Dechra Pharmaceuticals, Breedon Group and Avon Rubber (now renamed Avon Protection) have fallen out of the list and have been replaced by Electrocomponents, Oxford Instruments, Auction Technology and Sigmaroc.

Dan has trimmed some positions that have performed well, but says that there was nothing in the portfolio that was sold because it failed to meet his expectations. Outside of the top 10, IMI Mobile, Codemasters, Scapa and Sanne were all bid for, highlighting the increased levels of M&A activity within the market over the past few months.

Games Workshop

Games Workshop’s share price is close to its all-time high. Dan has both trimmed and added to the position over 2021. He feels that some investors may view the company as a temporary beneficiary of COVID-lockdowns, but he disagrees. The main attraction of the stock is the quality of the management, which was evident in the swift transition of Games Workshop’s sales model.

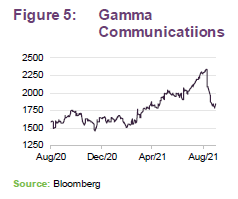

Gamma Communications

Gamma Communications (gammacommunicationsplc.com) provides technology-based communication services to businesses in Europe (but, as yet, the bulk of its business is in the UK). It was a beneficiary of the shift in working patterns driven by lockdown measures imposed last year, but early in the pandemic COVID disrupted its sales too. Revenue for 2020 was 20% higher than in 2019 and EPS 26% higher. The company says that adoption of Unified Communications as a Service (UCaaS) has accelerated markedly since the pandemic.

For Dan, part of the attraction is the prospect of rapid growth in Europe. Gamma Communications made a clutch of bolt-on acquisitions in 2020 (funded from cashflow) that helped expand gross profits in Europe from £9.2m to £22.3m.

Electrocomponents

Electrocomponents (electrocomponents.com) provides access to over 650,000 products, including electrical components. Its online service is taking market share from physical distributors. The market is highly fragmented. Dan believes that breadth of product coverage and ease of use are key reasons why Electrocomponents is taking market share. The business was a COVID-19 beneficiary, but Dan expects it to hold onto the new business it won in 2020.

Oxford Instruments

Oxford Instruments (oxinst.com) makes a wide range industrial instrumentation and tools. Despite some COVID-related disruption to its business, improving margins, driven by its ‘Horizon’ programme – aimed at delivering long-term sustainable growth and margin improvement – drove a 12% increase in EPS for FY21. Its order book is growing in double digits. Dan notes that it has a strong balance sheet and it is keen to make acquisitions.

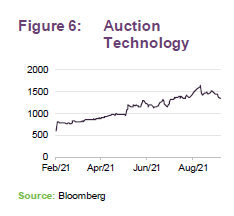

Auction Technology Group

Auction Technology Group (auctiontechnologygroup.com) was acquired at IPO at start of the year. It recently announced what could in Dan’s view be a transformational acquisition. LiveAuctioneers is a North American fine and decorative arts, antiques and luxury goods auction house. The bid is subject to CMA approval.

Auction Technology Group has two divisions – art & antiques and commercial/industrial (e.g. selling off repossessed furniture). It operates a digital marketplace and COVID accelerated the shift towards online trading. This helped drive a 48% year-on-year increase in revenue over the six months ended 31 March 2021 and a 158% increase in EBITDA.

Dan describes a virtuous circle of an increased pool of auctioneers bringing in more product, which attracts more buyers and so on. The company’s strong position in arts & antiques in the UK would be favourably complemented by the proposed US acquisition in his view. The addressable market in the US business is over twice that of the UK and is forecast to grow at 20% per year. LiveAuctioneers also comes with a payments business which, if rolled out to the UK, could improve existing margins.

Outside of the top 10

CVS

CVS (cvsukltd.co.uk) is a provider of veterinary services and products in the UK, Netherlands and the Republic of Ireland. We have discussed the long-term secular growth story around pet ownership in previous reports, focusing on Pets at Home and Dechra Pharmaceuticals (both of which are still held within the portfolio), being accelerated by COVID. CVS is a consolidator in a fragmented market and is also growing organically. It can exploit benefits of scale, given its market share. Dan is encouraged not only by the growth in pet numbers, but also the increased spend per pet. Spending on pets appears to be defensive. Dan also notes that CVS may itself be a target (although that is not the rationale for owning the stock). Mars (a leading pet food manufacturer) has been buying up businesses, and IVC Evidensia (a leading business in the sector), which had intended to IPO, was sold for a much higher price than expected to private equity.

Moonpig

Moonpig (moonpig.group) was an IPO in February this year. It is benefitting from a shift towards digital greetings cards, a trend that seemed to be accelerated by COVID. In recent weeks, the share price has been weak possibly on fears about a fall in customer retention rates as the pandemic eases. Dan says that whilst the company navigated last year well (more than doubling revenue and EBITDA over the year to 30 April 2021), the increase in user numbers since its IPO was less than had been hoped for. Ultimately, he feels that its KPIs are going in the right direction. Moonpig wants to spend more on marketing, which should translate into higher end revenues. However, Dan thinks some investors are overly fixated on the company’s short-term profitability.

WH Smith

Dan has been adding to the position in WH Smith (whsmithplc.co.uk) on weakness. As we have discussed previously, Dan thinks its airport/travel business is an attractive one, but obviously COVID has had a serious impact on this division. Dan says that the management team have done well to recycle cash flow from the high street business into new areas. US domestic travel is returning to more normal levels. WH Smith has been expanding its US operations. Dan says that it helps that the US is much further behind the UK in the effective commercialisation of airport space. Their experience and know-how allows them to bid for contracts more aggressively.

Performance

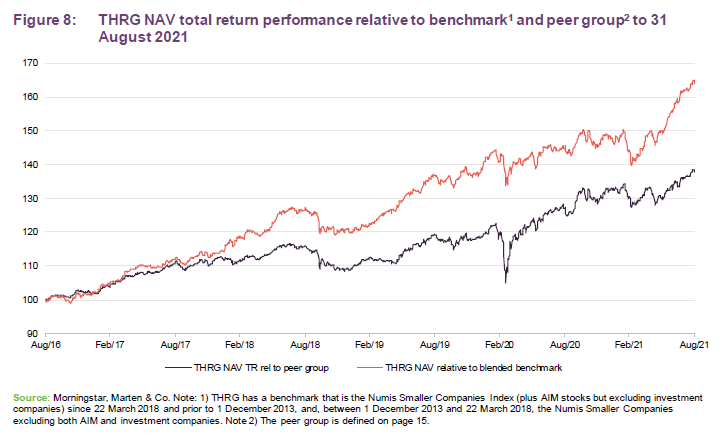

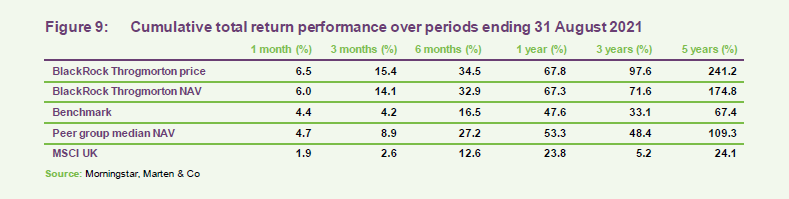

THRG continues to deliver strong outperformance of both its benchmark and its peer group. This has occurred despite the rotation into cyclical and value-style stocks that occurred in November 2020 and persisted for much of H1 2021. Other growth- and quality-focused funds have struggled to keep pace with the market during this period.

The outperformance of smaller companies relative to larger ones is evident in the poor relative performance of the MSCI UK Index in Figure 9.

Drivers of returns

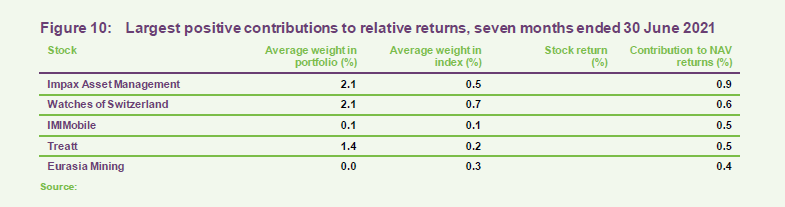

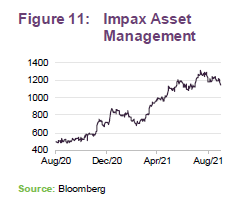

Impax Asset Management

The increased emphasis that investors are placing on sustainability and ESG issues, and the increasing consensus of the need to invest to tackle climate change, have been significant factors in driving growth in Impax Asset Management’s (impaxam.com) AUM. At 31 March 2021, AUM was £30bn, up from £14.4bn at 31 March 2020, and this helped drive an 80% year-on-year increase in profit before tax. Good investment performance has most likely played its part too.

Watches of Switzerland

As discussed in earlier notes, Watches of Switzerland (thewosgroupplc.com) has built a deeper relationship with its main supplier Rolex over the past couple of years. Dan rates the management team very highly. A recent trading update, covering the 13 weeks ended 1 August 2021, showed revenue more than doubling over the previous quarter in constant currency terms with good results from both the UK and US operations. The company is making progress in its ecommerce sales (up 15.9% over the same period year-on-year even though the high street stores re-opened).

A five-year strategic plan, unveiled in July 2021, anticipates the company growing in the UK around 2% faster each year than a market that they expect to grow at 10% per annum compound. In the US, the ambition is investment and acquisitions to drive a 25%–30% CAGR. In addition, the company is exploring ways of expanding into Europe, a market which management believe is “under-invested and under-potentialised”.

Of the others, IMIMobile was bid for by Cisco at a price which was a 48% premium to the previous trading day’s closing share price. Flavour and fragrance business, Treatt, which we have discussed in previous notes, continues to perform well. By contrast, not holding poorly-performing Eurasia Mining was also a factor in THRG’s outperformance of its benchmark.

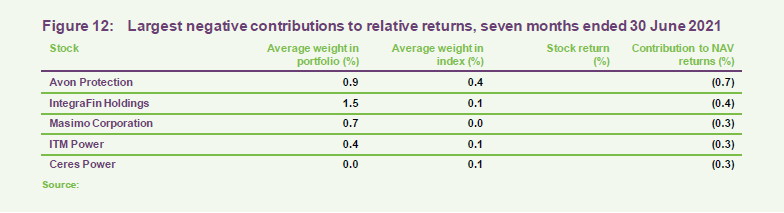

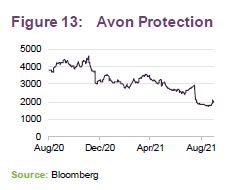

Avon Protection

THRG’s biggest issue in this financial year has been Avon Rubber – now renamed Avon Protection (avon-protection-plc.com). Problems that the company experienced with a US military contract led to downward revisions to earnings forecasts. However, Dan does not believe that this was game-changing for the company. He notes positive updates on its other business and expects that confidence in the stock will return once the issues have been ironed out and the contract is up and running

Jet2

Jet2 (https://www.jet2plc.com/investor_relations/) has struggled with ongoing delays to the full reopening of the leisure travel market. However, Dan thinks that it should achieve market share gains in time, as weaker players leave the industry. TUI, for instance, is in a precarious financial position. The stock is not without risk and the position is sized accordingly.

Of the others, Masimo, which makes devices to measure oxygen levels in blood amongst other things, benefitted from a COVID-19-related surge in business which is now easing off. The two hydrogen plays – ITM and Ceres Power have suffered from profit-taking.

Peer group

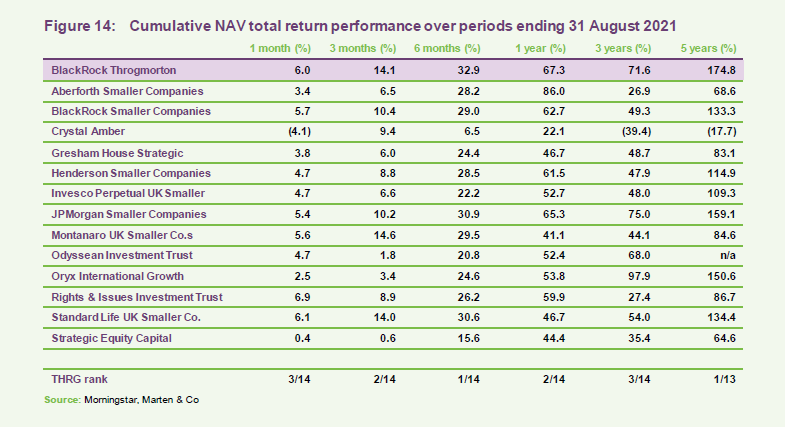

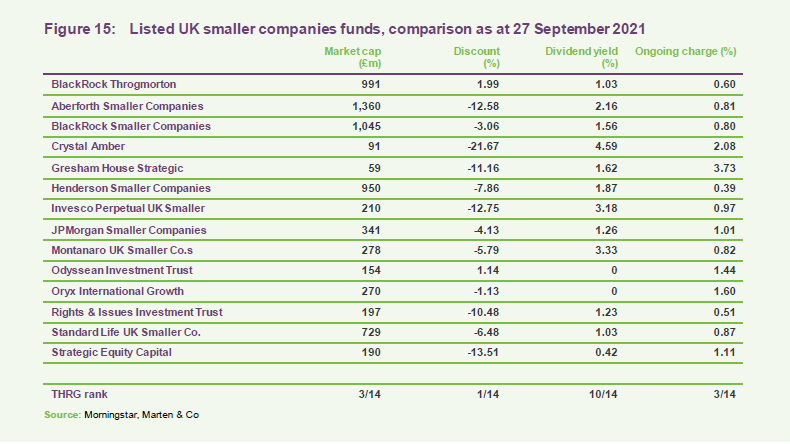

For comparison purposes, we have used a subset of funds in the AIC’s UK smaller companies sector. We have excluded split-capital companies, trusts with a small market capitalisation (below £50m), Marwyn Value Investors (which has a very different investment approach) and those that focus exclusively on micro-cap companies. A complete list is provided in Figure 14.

As Figure 14 shows, THRG ranks close to the top of the table over most time periods and is the best-performing fund over five years.

THRG is close to £1bn in size, but Dan says that there is still scope for it to continue to expand. THRG has been trading at a small premium to asset value and issuing shares to satisfy demand (thereby enhancing the NAV per share for existing shareholders).

THRG is not managed to produce an income, and this is reflected in its relatively low dividend yield.

Its ongoing charges ratio is competitive relative to its peers.

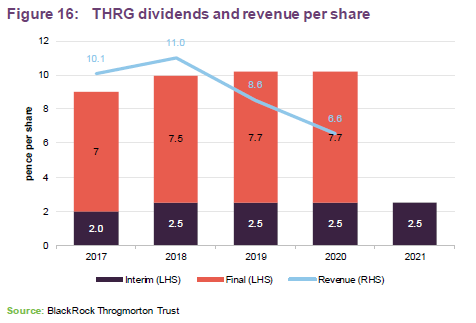

Dividend

Dividends are a by-product of the investment process and THRG’s portfolio is not managed with any income generation objective in mind. Nevertheless, the portfolio may generate reasonable levels of income. The base management fee is charged 25% and 75% to the revenue and capital accounts respectively, while 100% of any performance fee is charged to capital.

Net revenue per share fell to 6.57p for the year ended 30 November 2020, marking the second year that the board has decided to use some of THRG’s revenue reserves to pay the dividend. At the end of November 2020, the revenue reserve stood at £8.8m and this fell to about £5.2m after the payment of the final dividend. However, if needed, the company also has substantial distributable capital reserves.

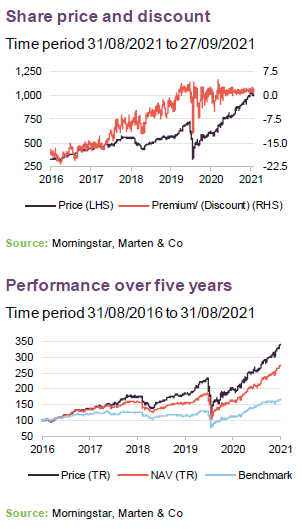

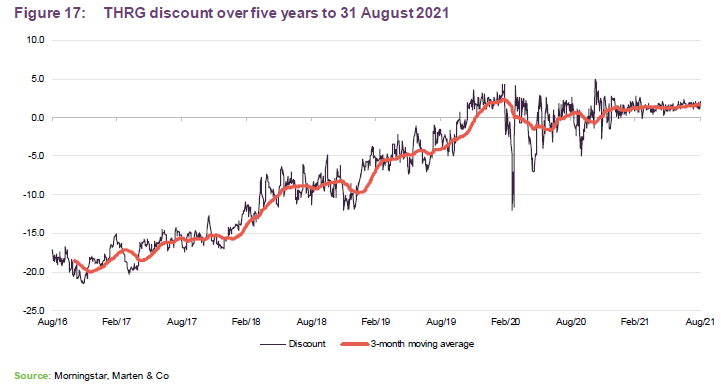

Premium/(discount)

Over the year ended 31 August 2021, THRG’s shares moved between trading at a 5.0% discount and a 4.9% premium and, on average, traded at a premium of 1.0%. On 27 September 2021, THRG was trading at a premium of 2.0%.

The board has said that it believes that it is in shareholders’ interests that the share price does not trade at an excessive premium or discount to NAV. Therefore, where deemed to be in shareholders’ long-term interests, it may exercise its powers to issue or buy back shares with the objective of ensuring that an excessive premium or discount does not arise. Consequently, the board asks shareholders at each AGM for approval to issue up to 10%, and to buy back up to 14.99%, of the THRG’s issued share capital.

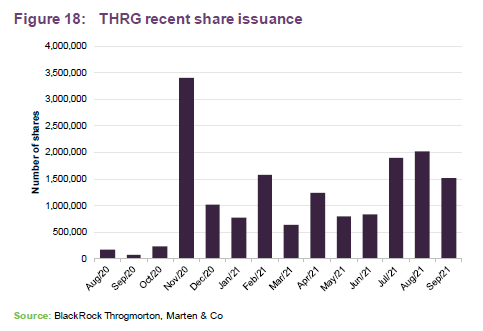

Since August 2020, THRG’s premium rating has allowed it to issue shares, almost 16.2m to date. Share issuance at a premium enhances the NAV for existing shareholders, increases liquidity in the trust’s shares and helps to lower the ongoing charges ratio as fixed costs are spread over a wider base.

Dan pushed hard for the share issuance in November 2020, arguing that he was excited about the prospects for the portfolio. From 30 November to 27 September 2021, THRG’s NAV has risen by almost 43% from 681.23p, vindicating Dan’s enthusiasm.

Fees and costs

BlackRock Investment Management (UK) Limited provides THRG with portfolio and risk management services under a contract that THRG has with BlackRock Fund Managers Limited. That contract is terminable on six months’ notice by either side. BlackRock Fund Managers’ base fee is calculated as 0.35% of gross assets (calculated monthly and paid in arrears). In addition, it can earn a performance fee of 15% of the outperformance of the benchmark index over a two-year rolling period with an effective cap of 0.9% of average gross assets, resulting from a cap on total management fees of 1.25% over a two-year period.

The ongoing charges ratio (which does not include performance fees) for the year ended 30 November 2021 was 0.60%, marginally higher than the equivalent period for the prior year (0.59%). The biggest increase in expenditure appears to have been on stock exchange listing fees. This will have been offset by the uplift in NAV from the result of issuance at a premium. Had performance fees been included in the calculation, the ongoing charges ratio would have been 1.60% (2019: 1.75%).

Capital structure and life

THRG has 99,816,263 ordinary shares in issue and no other classes of share capital. THRG’s board takes powers each year to repurchase up to 14.99% of the trust’s issued share capital (excluding treasury shares) and to issue up to 10%. Shares repurchased may be held in treasury or cancelled, at the discretion of the board. No treasury shares will be reissued other than at prices that represent a premium to the prevailing NAV, thereby ensuring that this action does not have any adverse effect on ongoing shareholders.

The board has set a maximum limit of net gearing of 20%. In practice, gearing is provided by the CFD portfolio. The mechanics of this are described on page 7.

The company’s year end is 30 November and AGMs are normally held in March.

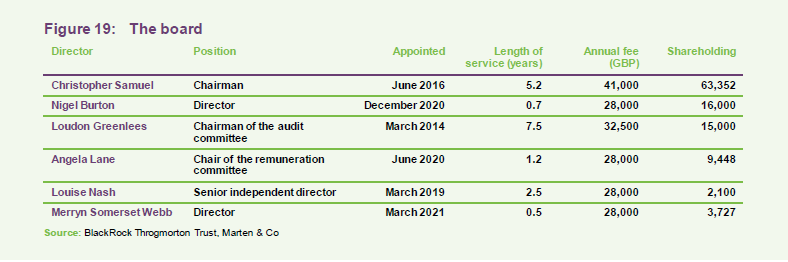

Board

Currently, THRG has six non-executive directors, all of whom are independent of the manager and none of whom sit together on other boards. The size of the board has fluctuated in recent years, but the board felt it important to recruit a sixth director in anticipation of an increased workload as the trust expands.

The composition of the board has changed quite a bit over the past 18 months. Jean Matterson stepped down at the AGM on 24 March 2021; Angela Lane joined the board in June 2020; Nigel Burton was appointed a director in December 2020; and most recently, Merryn Somerset Webb became a director in March 2021. The directors are encouraged but not required to own shares in the company.

Chris Samuel (chairman)

Chris was chief executive of Ignis Asset Management from 2009 until its sale to Standard Life Investments in 2014. He was previously chief operating officer at Gartmore and Hill Samuel Asset Management and was a partner at Cambridge Place Investment Management. Chris is a non-executive director of the Alliance Trust Plc, UIL Limited, its subsidiary UIL Finance Limited and Quilter Plc. He is also non-executive chairman of JP Morgan Japanese Investment Trust Plc and Quilter Financial Planning. Chris graduated from Oxford with an MA in Philosophy, Politics and Economics and he qualified as a Chartered Accountant with KPMG.

Nigel Burton

Nigel spent over 14 years as an investment banker at leading City institutions including UBS Warburg and Deutsche Bank, including as the managing director responsible for the energy and utilities industries. He has also spent 15 years as chief financial officer or chief executive officer of a number of private and public companies. Nigel is currently a non-executive director of AIM listed companies DeepVerge Plc, Microsaic Systems Plc, eEnergy Group Plc and Location Sciences Group Plc. He was formerly a non-executive director of Digitalbox Plc, Corcel Plc, Modern Water Plc, Alexander Mining Plc, Mobile Streams Plc and chairman of Remote Monitored Systems Plc.

Loudon Greenlees

Loudon was chief financial officer and chief operating officer of Thames River Capital from 1999 until 2007 and then commercial director until May 2013. Prior to this, he had been group finance director and chief operating officer of Rothschild Asset Management and group finance director of Baring Asset Management. Loudon qualified as a chartered accountant in 1974.

Angela Lane (chair of the remuneration committee)

Angela spent 18 years working in private equity at 3i, becoming a partner in 3i’s Growth Capital business managing the UK portfolio. Since 2007, she has held several non-executive and advisory roles for small and medium capitalised companies across a range of industries including business services, healthcare, travel, media, consumer goods and infrastructure. Angela is currently a non-executive director of Pacific Horizon Investment Trust Plc and Dunedin Enterprise Investment Trust Plc, where she is also chairman of the audit committee.

Louise Nash (senior independent director)

Louise was a UK small and mid-cap fund manager, firstly at Cazenove Capital and latterly at M&G Investments, which she left in 2015. She now works for family wine business Höpler. She also acts as a consultant to JLC Investor Relations. Louise holds an MA in German and Politics from the University of Edinburgh and the IMRO Investment Management Certificate.

Merryn Somerset Webb

Merryn has significant experience of financial matters through her role as editor-in-chief of MoneyWeek, the UK personal finance magazine, and appears extensively on this subject across radio and television. She brings valuable investment trust-specific experience and is currently a non-executive director of Murray Income Investment Trust Plc, Baillie Gifford Shin Nippon Plc and Netwealth Investments Limited.

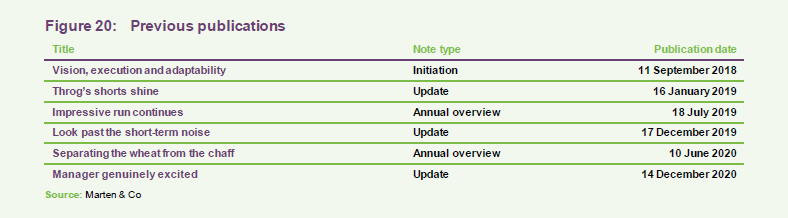

Previous publications

Readers may be interested in our previous publications on THRG, which are listed in Figure 20 below. These are available to read on our website.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on BlackRock Throgmorton Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.