Ahead of expectations

It is still early in the life of Downing Renewables and Infrastructure Trust (DORE), yet, with an early focus on Swedish hydropower – 51% of the portfolio at the end of March 2021 – complemented by a diverse portfolio of UK solar assets, it can already boast a portfolio that is clearly differentiated from its peers.

DORE’s NAV rose at the end of March, at a time when many other renewable energy funds were announcing NAV falls. It helps that DORE has a new portfolio, but as we explain, its exposure to the Swedish power market proved valuable too, underlining the rationale behind DORE’s policy of building a portfolio that is diversified by both technology and geography.

Assuming that DORE’s intended purchase of a Swedish multi-utility company (see page 8) and a proposed investment in a nearshore, shallow water wind farm – also in Sweden – go ahead as planned, DORE has more than allocated the proceeds from its IPO, well-ahead of expectations. It is intended that the balance will be financed with debt, enhancing DORE’s returns.

The swift deployment of the IPO proceeds supports DORE’s near-term dividend target and may even suggest that this could be exceeded. Yet, despite this string of good news, DORE is one of only two funds in its peer group trading at a discount to net asset value. The manager believes this presents an excellent entry point for investors seeking a diversified alternative to mainstream renewable infrastructure funds.

Diversified renewable energy and infrastructure

Downing Renewables and Infrastructure Trust aims to provide investors with an attractive and sustainable level of income returns, with an element of capital growth, by investing in a diversified portfolio of renewable energy and infrastructure assets located in the UK, Ireland and Northern Europe.

Fund profile

DORE aims to provide investors with an attractive and sustainable level of income returns, with an element of capital growth, by investing in a diversified portfolio of renewable energy and infrastructure assets located in the UK, Ireland and Northern Europe.

The investment manager believes that by investing in a range of renewable energy sources, DORE can reduce the seasonal volatility of revenues and reduce dependency on any single technology to provide more consistent income. There may also be some investments in other infrastructure, whose principle revenues are not derived from energy generation, thus reducing DORE’s exposure to merchant power prices. In addition, diversifying the portfolio geographically should help reduce the portfolio’s regulatory and political risk.

The portfolio will also blend operational projects with projects under construction. The manager says that investment in construction-phase projects offers the potential for higher returns. The amount invested in construction-ready assets or assets under construction will be limited to 35% of gross asset value, as construction projects tend to have more risk associated with them.

DORE is targeting a NAV total return of 6.5% to 7.5% per annum over the medium to long term. The intention is to pay dividends quarterly, targeting a dividend of 3p (3% of the 100p per share initial issue price) for the calendar year ended 31 December 2021, rising to 5p for 2022 and adopting a progressive dividend policy thereafter.

The investment manager is Downing LLP (Downing or the manager), which has AUM of £1.4bn. It has a team of 30 investment and asset management specialists (up from 27 at the time of DORE’s IPO) focused exclusively on energy and infrastructure transactions. Downing has hired a number of senior energy infrastructure specialists based in Sweden and is opening an office there; it has suggested that it would keep Elektra’s Edsbryn office if it succeeds in acquiring that asset (see page 8). The manager has considerable expertise, having managed 119 renewable energy investments and delivered a 9% average unlevered weighted average gross IRR on 55 exits.

The investment proposition – a summary

Our IPO note, which was published on 20 November 2020, set out the thinking behind DORE’s investment approach and explained the investment process in some detail. Readers may wish to refer to that note, but some points are worth reiterating here.

As governments around the world make commitments to achieving net zero greenhouse gas emissions, the scale of investment required in renewable energy generation is vast. A recent report from Bloomberg New Energy Finance (BNEF) said that globally $303.5bn was invested in renewable energy over 2020. It foresees over $12trn of investment in renewable energy generation and batteries over the next 30 years. New demand for electricity will come from the electrification of transport and heating.

DORE’s focus on Northern Europe (UK, Ireland, Norway, Sweden, Finland, Denmark, Iceland, Latvia, Lithuania and Estonia) differentiates it from peers and avoids exposure to countries such as Spain and France which have reneged on subsidies.

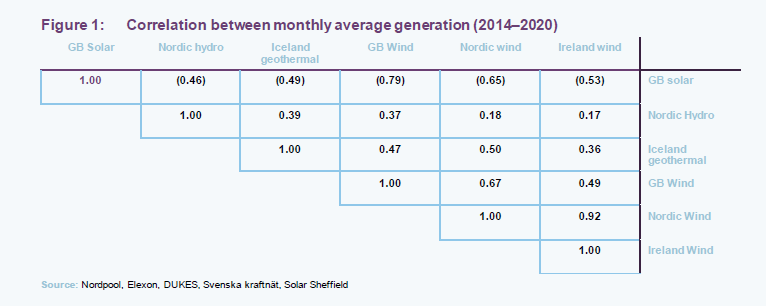

DORE’s policy of diversification by technology and geography reduces resource-related risk. For example, the portfolio returns should not be reliant on wind speeds in a particular location. This also diversifies regulatory risk and reduces the reliance on any one power market (the benefits of which are discussed on page 5).

DORE’s freedom to invest in construction-ready or in-construction assets (up to a cap of 35% of gross asset value at the time of investment) allows it to access higher returns than are available from operational assets.

DORE’s ability to invest into other infrastructure assets should reduce its exposure to merchant power prices.

Downing’s considerable investment of time and money in building its in-house asset management team allows it to optimise DORE’s portfolio. This team works closely with the investment team. The data that the asset management team gathers helps inform investment decisions. Downing cites the example of last year’s introduction of Optional Downward Flexibility Management (ODFM) by the UK’s National Grid. In its role as the Electricity System Operator, National Grid needs to balance supply and demand across its network. ODFM allows it to pay renewable energy generators to stop supplying power to the network at times of excess supply. For the generators, rapid action was needed to meet the rigorous requirements of the scheme and implement any necessary changes to on-site hardware. Downing says this was easier for it due to the degree of control it exerts over its assets through its asset management activities.

Progress to date

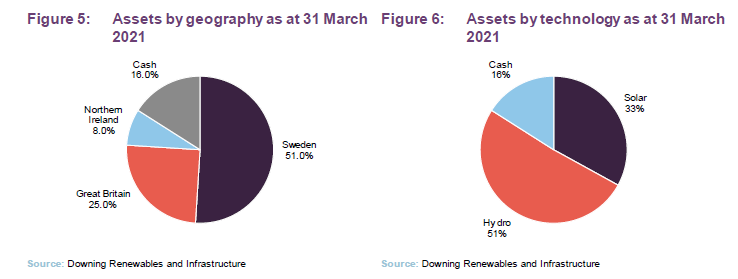

Whilst future investments will undoubtedly change the shape of DORE’s portfolio, as things stand, a clear differentiating factor is its high exposure to Sweden (see Figure 5). As the world strives to tackle climate change, Sweden can already boast over 80% of electricity generation from low-emission sources – nuclear and renewables. However, the country intends to phase out its three nuclear plants (six reactors) by 2040 and is targeting 100% renewable energy generation by that year.

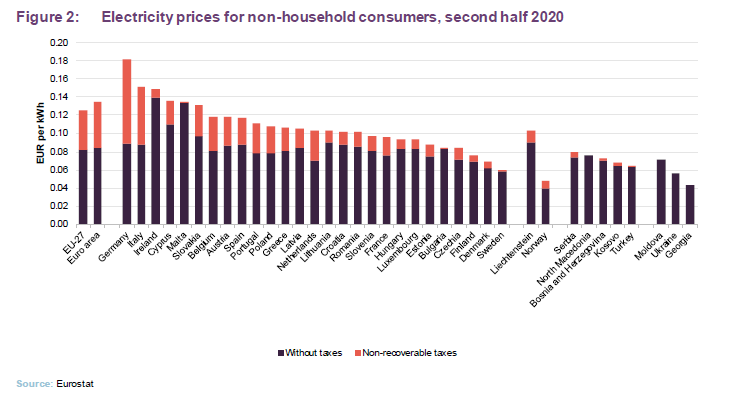

As Figure 2 shows, there is considerable variation in power prices across the EU and a selection of candidate and potential candidate countries. Notably, Sweden and Norway have some of the lowest tax-free power prices of the bloc.

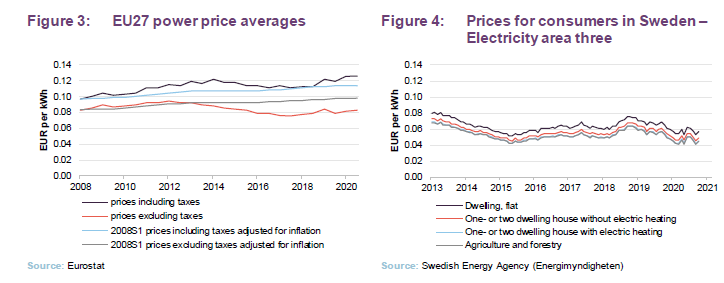

In Figure 3, average tax-free power prices have been trending down in the EU since mid-2012, although even adjusted for inflation, for consumers of electricity, tax increases make it appear that prices are rising.

This is also true in Sweden. In Figure 4 we have used prices for Electricity Area Three, which covers a swathe of the country including Stockholm. However, the manager believes that interconnectors will encourage Nordic power prices to rise towards northern European averages (note in Figure 2 the significant disparity between Swedish and German power prices). The manager also foresees growing demand for power within Sweden, as industrial activity picks up from businesses looking to source renewable power. A good example of this is the EV battery plant that Northvolt is building at Skellefteå in Sweden.

DORE’s latest proposed acquisition – Elektra Nät (see page 8) – offers a model for further expansion within the region. Unlike the UK, the power market is fairly fragmented within the Nordic countries. This offers opportunities to acquire small utilities businesses of about the size that would fit comfortably within DORE’s portfolio as it expands. Regional utilities and district heating schemes form part of Downing’s pipeline. Some of these acquisitions would also reduce DORE’s overall exposure to wholesale power prices as they have revenue derived from RAB-type models.

In line with its strategy of lowering its exposure to merchant power prices, DORE has entered into a number of long-term PPAs in both the UK and Sweden.

In the UK, where a substantial proportion of revenue is derived from government subsidy, 86% of the power produced by the solar portfolio acquired in March (see page 9) is sold under long-term PPAs which have a price floor. Of the remainder, some is sold through private wire arrangements, for example where a rooftop solar installation is used by the building it sits on. The counterparties for the ground-mounted projects are investment grade.

To the extent that it has any uncontracted generation, DORE is able to hedge power prices, should it choose – up to five years in the Nordic market and three years in the UK.

ESG

As might be expected, DORE has strong ESG credentials. Its renewable energy portfolio is forecast to produce enough energy to power 68,312 homes, saving 91,848 tonnes of CO2. It focuses on the environmental health of its assets too and supports local communities with grants. DORE will report to shareholders on matters of sustainability on a regular basis.

Downing LLP is a signatory to the UN Principles of Investment, which means that it:

- incorporates ESG issues into its investment analysis and decision-making processes;

- partakes in ‘active’ ownership policies and practices;

- seeks appropriate disclosures on ESG issues;

- works to promote the principles and enhance their implementation; and

- reports on such activities and progress.

The manager has developed a carbon lifecycle assessment methodology to provide a detailed understanding of the CO2eq emissions of different types of investments. By performing carbon lifecycle assessments, the investment manager intends to use this information to inform its decision making on its choice of suppliers for goods and services relating to its portfolio of investments.

As a signatory to HM Treasury’s Investing in Women Code, the manager is also committed to improving female entrepreneurs’ access to tools, resources and finance.

Pipeline

With much of the IPO proceeds either committed or allocated to projects under exclusivity that are more than sufficient to deploy the remainder, DORE will look to gear the hydro portfolio, which is currently unlevered, and introduce a revolving credit facility. The solar portfolio has £68.9m of long-term debt from Aviva and a further £10.9m from BlackRock. The intention is to introduce a £25m revolving credit facility, equivalent to 10% of gross asset value. Over time, this can help to facilitate near-term investment opportunities, minimising cash drag.

Downing says that it has identified a pipeline of potential investments which is significantly larger than the existing fund. The pipeline encompasses Nordic hydro and wind, UK solar, wind, and Nordic utilities/essential infrastructure investments.

The manager is also exploring co-locating energy storage assets alongside DORE’s generation facilities.

Asset allocation

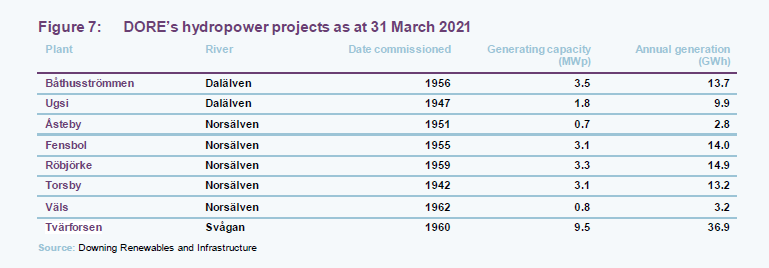

At 31 March 2021, DORE’s portfolio was comprised of eight hydropower assets on three rivers in Sweden and 48 companies owning around 3,250 solar PV installations across Great Britain and Northern Ireland. At that stage, DORE had also signed an exclusivity agreement in relation to a proposed investment in a 100 MW nearshore, shallow water wind farm.

On 28 May 2021, DORE announced that it intended to buy a Swedish multi-utility company (see below). Figures 5 and 6 are as at 31 March and do not incorporate either the proposed wind farm investment or the multi-utility deal.

Hydropower

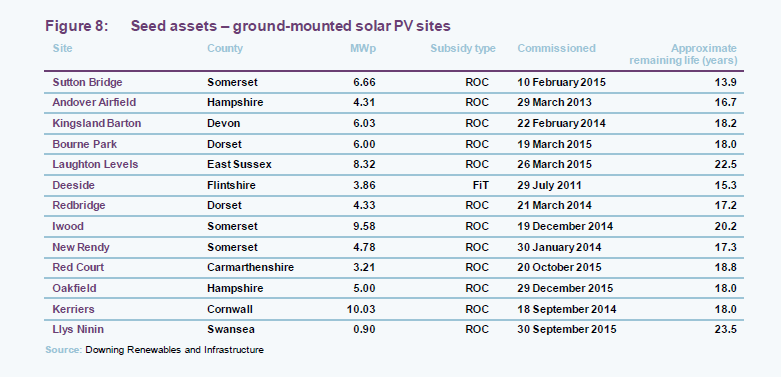

DORE’s hydropower assets are all located on three rivers in Sweden. These have the advantage of storage capacity to help regulate flows. Effectively, these reservoirs act like a battery and this means that their hydro assets can supply baseload power, which differentiates them from usual run-of-the-river hydropower assets.

The eight hydropower plants listed in Figure 7 formed DORE’s first acquisition. The deal was announced on 21 December 2020 and completed on 2 February 2021. The vendor was Fortum Sweden AB and the purchase price was €65m. The assets were acquired without debt. This part of the portfolio has a generating capacity of 25.8MWp and average annual production of about 108GWh. The manager sees the potential to borrow against this portfolio.

The hydropower plants have an extensive operating history, dating back almost 80 years. The manager feels that one of the strengths of hydropower assets is their longevity, which extends well beyond the design-lives of wind and solar assets.

On 28 May 2021, DORE announced that it intended to buy Elektra Nät, the owner of a number of hydropower stations on the river Voxnan near Edsbyn in central Sweden, with total annual generation of about 33GWh, and a local power distribution network.

DORE submitted an indicative bid in excess of SEK 300m (about £25.5m). DORE’s intention is that Edsbyn would be a hub for its investment in the Swedish renewable energy and electricity distribution sectors.

Solar

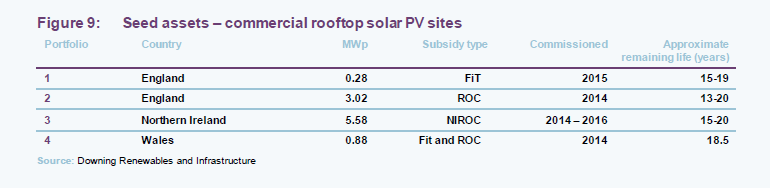

On 22 March 2021, DORE completed the £42m acquisition of a 96MWp portfolio of solar assets. We highlighted these in our IPO note. The 13 ground-mounted solar PV assets listed in Figure 8 have a generating capacity of 73MWp. The four portfolios of commercial rooftop sites amount to 28 assets totalling about 10MWp.

Operations and maintenance functions are contracted with PSH Energy. Asset management is performed in-house by Downing.

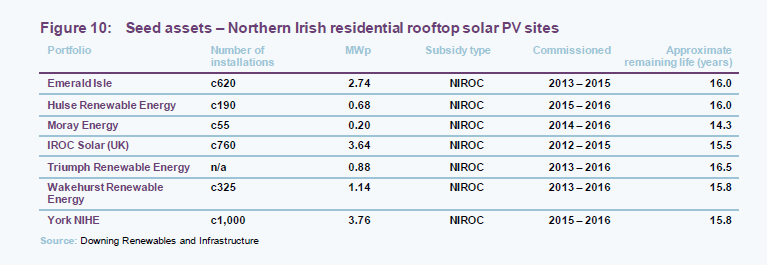

The remaining part of the solar purchase was of seven portfolios of residential rooftop assets in Northern Ireland, with a total generating capacity of about 13MWp.

Operations and maintenance functions are provided by Soventix and Anesco, with asset management performed in-house by Downing.

Wind

On 15 January 2021, DORE announced that it had signed an exclusivity agreement with Bagnall Energy in relation to a proposed investment in a planned 100MW nearshore, shallow water wind farm in Lake Vänern in southern Sweden. The development would be undertaken by Cloudberry Clean Energy AS. Once certain conditions have been met, DORE would have a 40% stake in the project, Bagnall (which is part of the Downing Estate Planning Service, which is managed by Downing) would have 40% and Cloudberry would have 20%. Cloudberry says that Downing will pay about NOK300m (c£25.3m) in two instalments – NOK100m at financial close during 2021 and the balance once the project is commissioned. Downing says that DORE’s share of the total cash outlay required to acquire and develop the site is likely to be about £40m, spread over a number of years.

There is an existing wind farm on the lake, and hence a grid connection is available. The project would comprise 16 turbines with estimate annual production of 350GWh. Cloudberry says that the planned completion is by the second half of 2023.

Performance

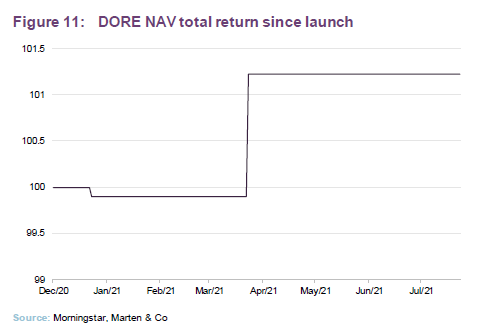

It is very early days in DORE’s life, but it is pleasing to see that its NAV is making positive progress at a time when many other renewable energy funds are announcing NAV falls.

DORE’s NAV uplift reflects its operational performance. For the period from acquisition to the end of March 2021, the hydropower portfolio’s operating profit was 400% up on budget. Largely, this reflects generation well ahead of estimates (a consequence of a delay to the spring floods) coupled with higher-than-forecast power prices in the country. In addition, operating profits for DORE’s UK solar portfolio were 15% ahead of budget, helped by operating cost efficiencies.

Other fund’s NAVs are declining as they factor the UK’s planned corporation tax rise and lower forecasts for long-term UK power prices into NAV estimates. Downing points out that its acquisitions in the UK were already predicated on the higher tax charge.

DORE’s diversification strategy helped, too, as Swedish power prices are trending higher. By contrast, falling gas prices and renewable additions are weighing on UK price forecasts.

Peer group

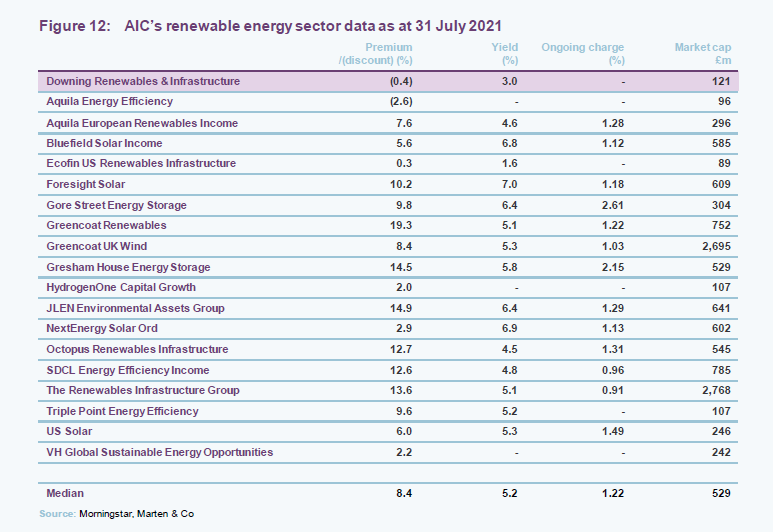

DORE is a constituent of the AIC’s renewable energy sector. There are now 19 members of this peer group, but the sector is increasingly diverse. Two funds – Gore Street Energy Storage and Gresham House Energy Storage – focus exclusively on battery storage assets. These fall within DORE’s remit, but as yet do not feature within its portfolio. Three funds are focused on energy efficiency projects. Two funds –Ecofin US Renewables and US Solar Fund – invest in US projects, which tend to have long-term PPAs. One, the most recent addition to the sector, invests in Hydrogen-related assets. Of the remainder, none has DORE’s current strong focus on the Nordic region or hydropower. There are some others that invest across different technologies – Aquila European Renewables, Bluefield Solar Income, JLEN Environmental Assets, Octopus Renewables Infrastructure, The Renewables Infrastructure Group and VH Global Sustainable Energy Opportunities. This last group are probably the closest comparators.

Within the peer group, DORE is one of the smaller funds, but this is something that we hope will soon be rectified. DORE’s yield (based on the forecast dividend – see below) is targeted to rise in its second accounting period to a level closer to the median of peer group.

Dividend

DORE intends to pay dividends on a quarterly basis, with dividends typically declared in respect of the quarterly periods ending March, June, September and December and paid in June, September, December and March respectively. The first interim dividend is expected to be declared in respect of the period from admission to 30 June 2021 and paid in September 2021.

DORE will target an initial dividend yield of 3% by reference to the 100p issue price in respect of the calendar year to 31 December 2021, rising to a target dividend yield of 5% by reference to the issue price in respect of the calendar year to 31 December 2022. Thereafter, the company intends to adopt a progressive dividend policy.

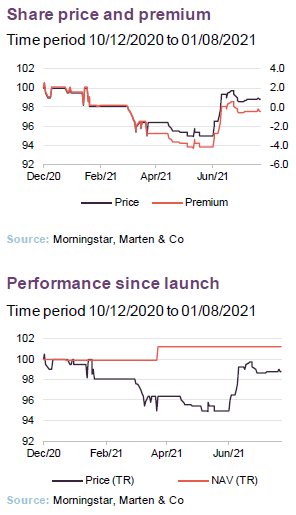

Premium/(discount)

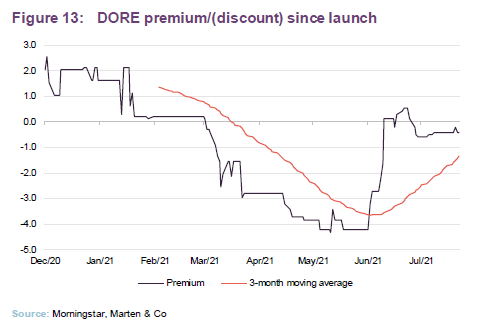

Over the period since launch, DORE has traded in a range of a 4.3% discount to a 2.6% premium. The average discount over this period was 0.9%. At 2 August 2021, DORE was trading on a discount of 0.4%.

It is not obvious why DORE moved to trade at a discount, especially given that it is less exposed to weak long-term UK power prices than its peers. The share price has recovered from its lows. We see no reason why it should not strengthen further.

Previous publications

Readers may wish to refer to our initiation note, published on 20 November 2020 at the time of DORE’s IPO – Targeting attractive and sustainable returns.

The legal bit

This marketing communication has been prepared for Downing Renewables and Infrastructure Trust Plc by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and, if you are not a professional investor, or in any other way are prohibited or restricted from receiving this information, you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.