Tomorrow’s winners

Edinburgh Worldwide (EWI) aims to invest in some of the world’s most exciting companies, many of which would otherwise be hard for investors to access. It seeks to identify tomorrow’s winners when they are still relatively small, and hang onto them as they become successful. The manager acknowledges that not every company will make it, but expects that the profits accruing to EWI from those that succeed more than make up for those that fall by the wayside.

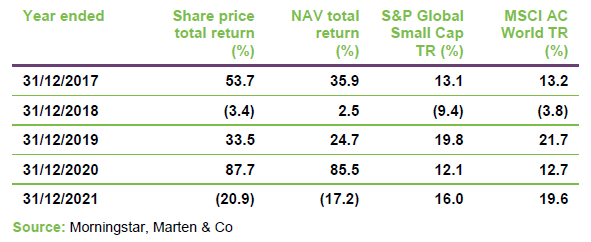

After a period of strong absolute and relative performance in 2020, sentiment appeared to switch against high-growth companies. EWI gave back some of its considerable outperformance. The manager is a long-term investor, however. EWI’s five-year numbers remain well ahead of indices and peers. A small discount has opened up in recent weeks.

Capital growth from entrepreneurial companies

EWI aims to achieve capital growth from a global portfolio of initially immature entrepreneurial companies, typically with a market capitalisation of less than $5bn at time of initial investment, which are believed to offer long-term (over at least five years) growth potential.

Fund profile

EWI is an investment trust which invests globally in a portfolio of primarily listed companies. It aims to profit from a global portfolio of initially immature entrepreneurial companies, typically with a market capitalisation of less than S$5bn at the time of initial investment, which are believed to offer long-term growth potential.

The board chooses to compare the trust’s performance to the S&P Global Small Cap Index (total return in sterling). However, the composition of the index has no bearing on the manager’s choice of stocks or position sizes. As evidence of this, the active share at the end of December 2021 was about 99%.

Up to 15% of the portfolio (at the time of investment) may be invested in unlisted securities. The board is proposing that this limit be increased to 25%, as discussed below.

With the aim of spreading risk, the portfolio should have between 75 and 125 holdings and have exposure to at least six countries and 15 industries. No more than 5% of the portfolio will be invested in a single security (at the time of acquisition).

The trust was launched in 1998, but did not adopt its current strategy until 31 January 2014.

EWI’s AIFM is Baillie Gifford & Co Limited, a wholly-owned subsidiary of Baillie Gifford & Co.

Douglas Brodie is the lead manager on the trust and its open-ended equivalent Global Discovery. He is supported by two deputy managers – Svetlana Viteva and Luke Ward – and a five-strong team of analysts. Collectively, they make up the eight-strong global discovery team within Baillie Gifford. Some more biographical details are provided on page 20.

The wider firm had £346.2bn of AUM at 30 September 2021 and the global discovery team were managing £5.5bn of that.

Exposure to unlisted securities

EWI has invested in 18 private companies since it adopted its new investment approach in 2014. At the end of December 2021, EWI had 13.3% of its portfolio in unlisted securities, some of which are discussed from page 12 onwards. The board and the manager believe that for EWI to gain access to immature entrepreneurial companies, increasingly it must look to purchase unlisted companies. They reason that technological advances have lowered the initial capital requirement needed to establish and scale many companies.

They say that the quantum of funding available to promising private companies is considerable, and entrepreneurs may never need to turn to public markets for growth capital, instead choosing to use an IPO as a means to provide liquidity for backers once the business is large and mature.

As an indication of the size of the opportunity, EWI cites a figure of 923 private companies with values in excess of $500m at the end of 2020, collectively worth more than $2.2trn. This compares with 18 companies worth a total of $18bn in 2006.

The board is asking shareholders to increase the maximum exposure to unlisted companies (at the time of investment) to 25% of the portfolio. The proposal will be voted on at the upcoming AGM scheduled for 2 February.

A single unlisted investment may be represented by multiple holdings in different share classes. The new wording of the investment policy will also replace ‘holdings’ with ‘companies’ with respect to the target number of positions.

Philosophy and process

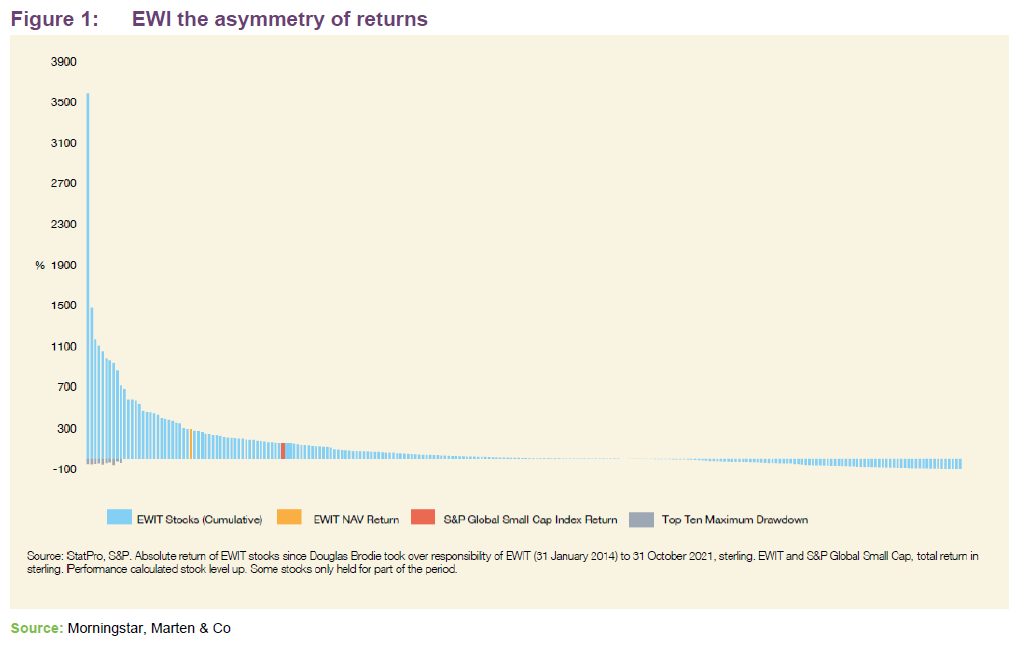

The philosophy that drives the construction of EWI’s portfolio is common to other Baillie Gifford trusts and is based on the manager’s observation of the asymmetry of returns. The manager believes that only a few stocks have the ability to become global leaders in their fields and sustain that position and the rewards that accrue to them are considerable. By contrast, they suggest that most companies will struggle to outperform and, as is especially the case with the younger, more immature companies that EWI focuses on, quite a few will fail. They say that it is important that investors in EWI understand this.

The manager says that tools and technology have levelled the playing field. Advances such as the internet, cloud computing and online payments are enabling even relatively small businesses to scale fast and address a global market. The implication is that, if the market is global, differences in country and regional macroeconomic and political environments are much less relevant.

EWI, therefore, represents a true stock-picking portfolio, constructed without reference to index weights or to reflect the views of an asset allocation committee. The portfolio has a bias to technology, but as the manager points out, technology is everywhere.

Potential investments should have a market cap of no more than $5bn at the time of investment. Nevertheless, the emphasis is on identifying the winners and running with them and EWI may end up with holdings in far larger companies (Tesla, for example). EWI can act as an incubator of companies that grow to become large enough to be included in Baillie Gifford’s larger-cap strategies and identify up and coming disrupters. However, it can retain exposure to these; the manager is not compelled to sell companies on market cap grounds. At 31 October 2021, funds managed by the global discovery team were invested in 137 stocks. 99 of those were also held in other Baillie Gifford strategies.

This is not a venture portfolio – the manager tends not to consider companies less than $300m–$400m in size – but these are relatively immature companies on the frontiers of change. The manager feels that the uncertain outlook for these businesses makes it hard for the market to value them properly. This is especially true for those companies that are expected to become significantly profitable some years in the future. The manager believes that most of these stocks are poorly understood and that creates the space for bottom-up research to add value. The universe is vast – perhaps 30,000 companies – but most of these will not have the characteristic traits that they are looking for and some entire sectors are not a fit.

The manager seeks to assess the potential of the business model and the risk that it does not succeed. Companies need to have a scalable business model and a clear competitive advantage. Credibility of management is very important as is an alignment between the interest of management and investors. Only a very small numbers of stocks fit their criteria. The manager says that the sector is full of companies that are small and will stay that way.

The manager believes that, if it is to deliver transformational growth, a business needs to have a culture of innovation which allows it to identify and solve problems for their customers, and that it often helps if they are starting with a clean sheet of paper rather than simultaneously managing the decline of an incumbent business. EWI is often a provider of growth capital, sometimes just pre-revenue (as is the case with many of the trust’s healthcare investments, for example). For the companies, the manager believes that EWI’s evergreen structure is an advantage. It means that its investments can be made for the long term without having to be bound to the normal 10-year cycle of private equity LP funds.

Generally, the manager is not keen on situations where a number of companies are competing in the same niche. However, he may consider buying small positions in a few competing companies if it is not yet clear which might have the winning formula for success. This is true of the trust’s oncology-focused stocks, for example.

EWI’s board and manager take their stewardship role seriously. However, the company will not seek to influence the strategic direction of the companies that it invests in.

EWI may end up holding a significant stake in a business (Baillie Gifford has informal caps on the size of the stakes held across all funds), especially early in a business’s life. However, the manager is mindful of the daily liquidity in listed stocks and factors that into position sizes. A typical new position will start life in the portfolio as a 0.5%–1.5% position. Where the risks associated with the business model are binary, the position size will be smaller. One of the largest new positions in the portfolio in recent times was Tesla, where the manager invested about 1.6%–1.7% in the company once cars were rolling off the production line and that element of the business plan had been de-risked.

Sales are triggered once it is clear to the manager that the investment case is flawed. M&A activity is also a source of involuntary sales – often companies end up being taken over for less than the manager thinks they could be worth. In addition, positions will be re-evaluated and may be sold if the manager feels that the upside is limited.

ESG and Stewardship Principles

Baillie Gifford & Co is a signatory to the United Nations Principles for Responsible Investment and the Carbon Disclosure Project and is also a member of the Asian Corporate Governance Association and International Corporate Governance Network.

EWI’s natural bias towards capital-light businesses contributes towards the portfolio’s lower-than-market-average carbon intensity (88.1% lower than the S&P Global Small Cap Index).

We reproduce the company’s stewardship principles (taken from its most recent annual report) below.

We encourage company management and their boards to be ambitious and focus their investments on long-term value creation. We understand that it is easy for businesses to be influenced by short-sighted demands for profit maximisation but believe these often lead to sub-optimal long-term outcomes. We regard it as our responsibility to steer businesses away from destructive financial engineering towards activities that create genuine economic value over the long run. We are happy that our value will often be in supporting management when others do not.

We believe that boards play a key role in supporting corporate success and representing the interests of minority shareholders. There is no fixed formula, but it is our expectation that boards have the resources, cognitive diversity and information they need to fulfil these responsibilities. We believe that a board works best when there is strong independent representation able to assist, advise and constructively test the thinking of management.

We look for remuneration policies that are simple, transparent and reward superior strategic and operational endeavour. We believe incentive schemes can be important in driving behaviour, and we encourage policies which create alignment with genuine long-term shareholders. We are accepting of significant pay-outs to executives if these are commensurate with outstanding long-run value creation, but plans should not reward mediocre outcomes. We think that performance hurdles should be skewed towards long-term results and that remuneration plans should be subject to shareholder approval.

We believe it is in the long-term interests of companies to maintain strong relationships with all stakeholders, treating employees, customers, suppliers, governments and regulators in a fair and transparent manner. We do not believe in one-size-fits-all governance and we recognise that different shareholder structures are appropriate for different businesses. However, regardless of structure, companies must always respect the rights of all equity owners.

We look for companies to act as responsible corporate citizens, working within the spirit and not just the letter of the laws and regulations that govern them. We believe that corporate success will only be sustained if a business’s long-run impact on society and the environment is taken into account. Management and boards should therefore understand and regularly review this aspect of their activities, disclosing such information publicly alongside plans for ongoing improvement.

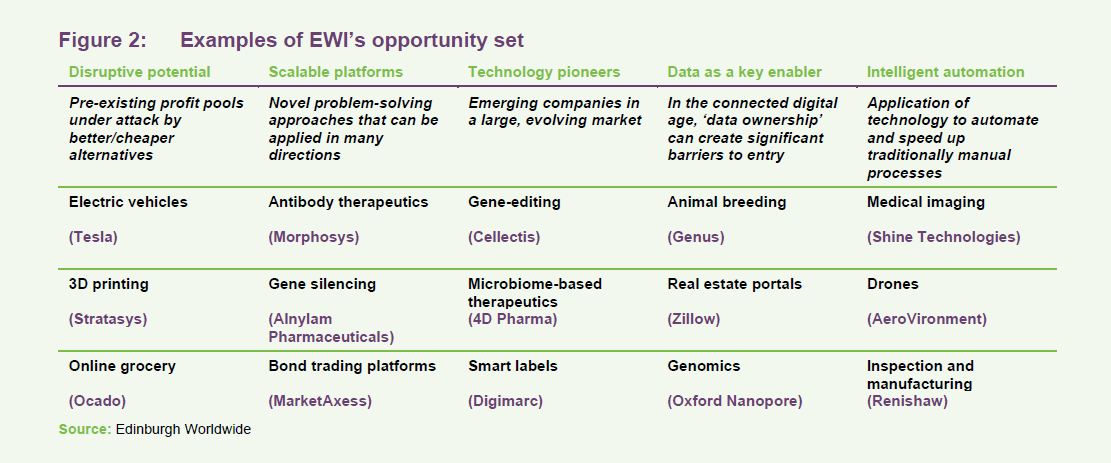

The opportunity set

As an illustration of the opportunity set available to EWI, the manager has identified a wide range of themes that the fund is backing currently. Within each category, the fund is targeting unique businesses with strategic value.

Asset allocation

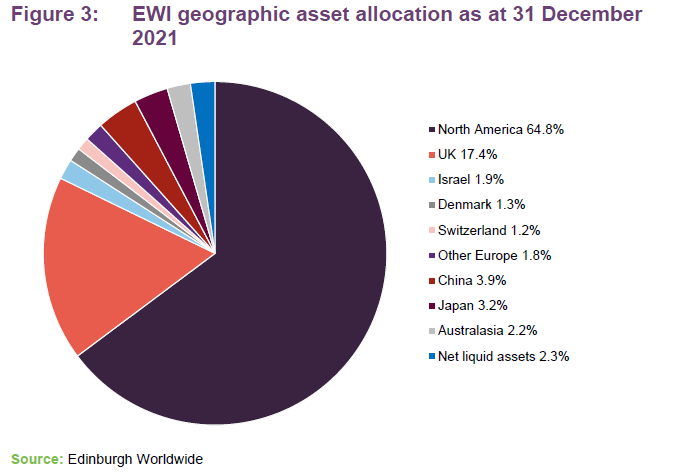

EWI’s asset allocation is driven by the manager’s stock selection decisions. The portfolio is global, but has a distinct bias towards North America, which accounts for about two-thirds of the fund, and relative to its benchmark index has an overweight exposure to North America and the UK, and has an underweight exposure to Japan.

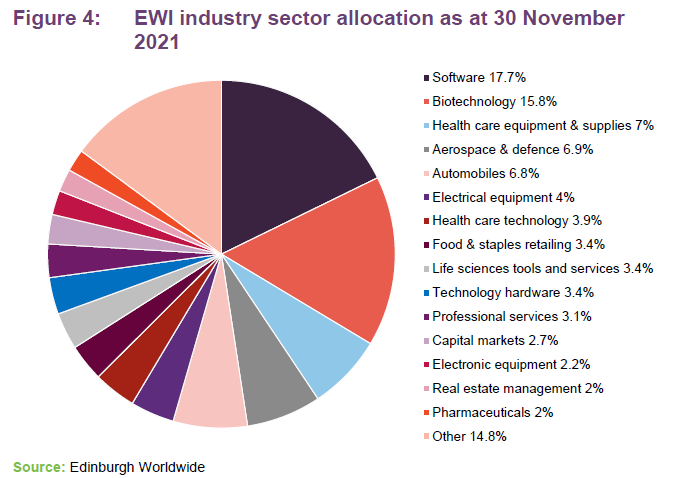

On an industry basis, much as one might expect, the portfolio has a significant exposure to sectors such as software and biotechnology and an underweight exposure to sectors such as financials, materials and consumer goods and services.

The long-term approach that the manager takes is reflected in the low level of turnover within the portfolio. For the 12-month period ended 31 October 2021, turnover was 9.1% (FY20 8.4%).

One notable disposal in 2021 was of Dexcom (investors.dexcom.com/), which makes real-time blood glucose monitoring systems used by diabetics. This has been a successful investment for EWI, having been a significant position within the portfolio since 2014. The stock price has risen more than 10-fold since then.

Top 10 holdings

Below we look at a selection of these and a couple of newer positions, Sprout Social and ITM Power, that the manager highlighted to us:

Tesla

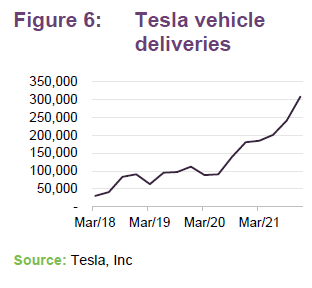

Figure 6 shows how deliveries of Tesla’s (ir.tesla.com) cars have been ramping up over the past three years. Semiconductor shortages, transport bottlenecks and COVID-related restrictions have impacted on production levels in recent years. Tesla achieved record revenue and profit in Q3 2021, achieving an operating margin of 14.6%.

New capacity is being added in Shanghai, Berlin and Texas. However, the manager thinks that there is much more to go for, believing that we are at the early stages of the electrification of transport. Incumbent OEMs have mostly accepted that the transition is happening and are working to address that but most have a long way to catch up, in his opinion. The manager also thinks the software component of the product offering – autonomy and entertainment – could be a significant revenue earner over and above EV sales.

Having a $1trn company as the largest position may seem to some to be out of line with EWI’s brief. However, Tesla is the perfect example of the manager running his winners. Tesla was one of a handful of companies that were retained within the portfolio when the new investment policy was adopted in 2014. The stock price was $36.28 at the time. Today, despite the falls of recent weeks, it is just over 26x that. There will come a time when this is no longer in the portfolio, but not yet.

Alnylam Pharmaceuticals

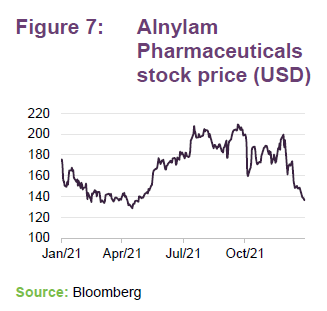

Alnylam Pharmaceuticals (investors.alnylam.com) uses gene silencing (RNA interference) technology to block certain genes that cause a range of diseases. The company has three approved products tackling rare diseases and an extensive pipeline of over 20 clinical programmes which includes therapies for haemophilia, liver disease, hypertension, gout, Alzheimer’s, and Hepatitis B.

Baillie Gifford highlights Alnylam’s relatively good track record with drug discovery. Alnylam says that 64.3% of its candidate therapies have succeeded to date, compared with an industry average of 10.3%. Technological advances have reduced the ‘hit and miss’ element of the process, to the benefit of the company’s profitability. Alnylam is adopting a responsible approach to drug pricing in recognition of that.

Alnylam is still loss-making, reflecting its heavy investment in R&D, but had $2.4bn in cash at the end of 2021 and says 2021 revenue was 83% higher than in 2020. It hopes to secure FDA approval for its Vutrisiran therapy for hATTR Amyloidosis-PN later this year and to secure readouts for a number of trials that are currently underway. The company is targeting more than 40% compound growth in revenue through to the end of 2025.

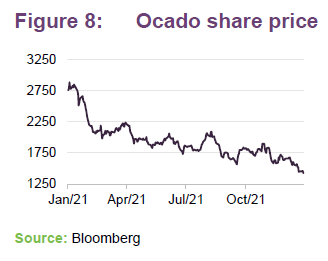

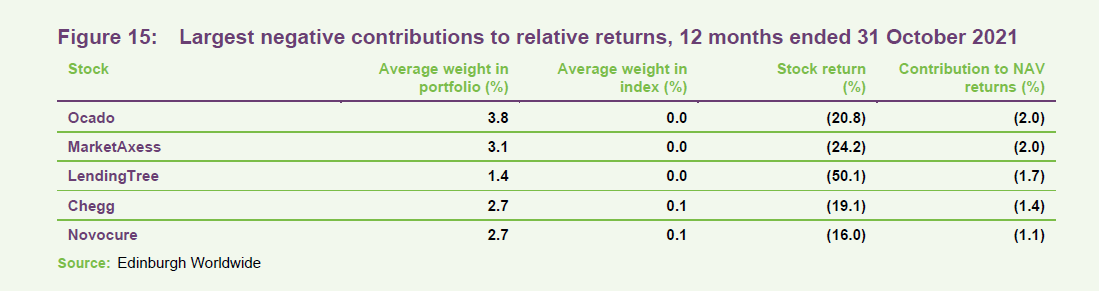

Ocado

Ocado (ocadogroup.com/investors) has been at the forefront of fulfilment for online groceries for some years. Its OSP platform combines software solutions and robotics and is used by retailers with combined global sales of £210bn. Its UK-based online grocery business is now part of a 50:50 joint venture – Ocado Retail – with Marks & Spencer. This is now the fastest-growing grocer in the UK.

At the half-year stage, the business was still loss-making, but losses were lower than for the equivalent period in 2020.

COVID drove a strong uplift in demand for online shopping, which was expected to fall back again as lockdowns were eased. In the event, Ocado Retail appears to have been able to maintain growth in customer numbers but has seen a fall in average order sizes. Labour shortages have had an impact on revenue growth and profitability. For Q4 2021, average orders were up 8.5% year-on-year, while revenue was down 3.9%.

Investors have taken profits over 2021 and the share price has fallen back. Baillie Gifford are looking through this short-term setback.

Oxford Nanopore Technologies

Oxford Nanopore (nanoporetech.com/) was a significant constituent of EWI’s portfolio of unlisted investments until its end September 2021 IPO. The company has been owned by EWI since 2015 and had already been marked up in value substantially ahead of its listing. The shares rose sharply from the 425p IPO price but have fallen back recently alongside other growth stocks and are 538p today. The company offers real-time and mobile DNA and RNA sequencing, which is used in applications such as genetics, food safety and identifying/monitoring pathogens.

On 7 January 2022, it said that it expects revenue from its life science research tools to increase by 83% for 2021 over 2020, ahead of expectations. It had previously guided towards sales of around £140m in 2022 and £180m in 2023.

Codexis

Codexis (ir.codexis.com) engineers enzymes to be used as biocatalysts in the production of pharmaceuticals and fine chemicals, with applications in food and nutrition as well as pharmaceuticals and industrial biochemistry. The company believes that its products have widespread potential – they cite a McKinsey Global Institute study from May 2020 that suggested that as much as 60% of the physical inputs to the global economy could, in principle, be produced biologically.

The company has over 1,800 patents and patent applications globally, and is working with partners such as Novartis, Allergan and Tate & Lyle on some of its products.

Revenue is growing at a fast pace (100% year-on-year in Q3 2021), albeit from a low base. At 30 June 2021, 17 products were licensed and producing revenue, and a further 61 were in pre-commercial development.

Sprout Social

The manager feels that companies may need to have a presence across many social media platforms if they are to access customers. Sprout Social’s (investors.sproutsocial.com) cloud-based SaaS allows content to be distributed and managed across a number of platforms. At end September 2021, Sprout Social had over 30,000 customers in more than 100 countries. Annual recurring revenue was $204m (up 46% year-on-year), 99% of which was subscription-based. High gross margins (around 75%) mean that the company is close to profitability despite considerable investment in its growth.

ITM Power

ITM Power (itm-power.com) was a new holding in 2021. Its technology uses electrolysis – it designs and manufactures PEM (proton exchange membrane) electrolysers – to produce hydrogen. This is a company that the team has followed for a while, given its longstanding position in Ceres Power. As the shift to renewables accelerates, a fundamental problem remains – how to tackle the intermittency of renewable power generation. Baillie Gifford believes that we will see an overbuild of capacity in renewables. At times, we will have more energy than we need. It makes sense, therefore to store it and release it when it is needed. Alkaline batteries are useful but can only discharge over a period of up to two hours. A solution that can release stored power over days, if necessary, is needed. ITM Power’s technology can use excess energy to make hydrogen from water, which can be stored, and perhaps distributed using existing natural gas infrastructure.

It is early days for the business – revenue for the six months ended 31 October 2021 was just £4.1m. At 16 December 2021, the company had work in progress totalling 62MW and an order backlog of 499MW (both up significantly on the prior year). Supported by a recent fundraise, it has commenced work on a new ‘gigafactory’ and a second with capacity for 1.5GW per year is planned, reinforcing its market-leading position.

EWI also has exposure to solid-state lithium power storage technology through QuantumScape.

Unlisted positions

At the end of October 2021, EWI held 12 unlisted investments, which accounted for 10.8% of the portfolio. Across the firm, Baillie Gifford held 73 unlisted companies worth £4bn at end October 2021.

Looking at a selection of EWI’s unlisted positions:

Space Exploration Technologies (SpaceX)

SpaceX (spacex.com) has attracted a number of headlines in recent years, notably securing a contract with NASA to land the next generation of lunar astronauts on the Moon.

The manager notes that the company is operating in an industry with real cost challenges, and is seeking to address these. He believes that government agencies tend to be risk averse and their R&D budgets have been constrained. Private capital could approach problems in novel ways and bring greater capital discipline.

From its first space-faring flight in 2008 with Falcon 1, the company has developed rapidly. The Falcon 9 proved in 2015 that reusable rockets were a practical option. It has become a workhorse, launching 134 times. In 2018, the Falcon Heavy made its first flight; it is for the moment the world’s most powerful operational rocket. In 2019, the Dragon docked autonomously with the International Space Station, and in 2020, it delivered astronauts to the station as NASA certified the Falcon 9 and Crew Dragon spacecraft for human spaceflight. Starship, the new prototype, will be used for lunar missions and there is ambition to go to Mars. However, it also offers a lower-cost alternative for satellite launches.

SpaceX is building out its Starlink constellation of low-orbit satellites, with around 2,000 in orbit now and up to 42,000 planned, providing what it describes as low-latency (as low as 20ms), high-speed (100Mb/s–200Mb/s) internet access anywhere on the planet. The manager suggests that it could grow to be the first truly global utility.

PsiQuantum

Quantum computing, which uses entangled particles in place of electrical circuits, could theoretically be far more powerful than conventional computers. However, entangling electrons – the typical approach to building quantum computers – is complex and advances in this area have been slow. PsiQuantum (psiquantum.com) takes a different approach; its machines use entangled photons. The company believes that “uniquely [it has] a clear path to building a useful quantum computer”.

A $450m series D funding round in July 2021 brought the total raised by the company to $665m since its launch in 2016. The manager says that it still has hurdles to overcome before it has a commercial product. However, it is already working with potential customers to devise algorithms that would run on the devices.

Akili Interactive Labs

Akili Interactive (akiliinteractive.com) uses specially-designed computer games to treat various cognitive impairments such as ADHD. Akili’s products are designed to deliver sensory and motor stimuli to selectively target and activate specific cognitive neural systems in the brain. The proprietary technology is engineered to directly generate physiological changes in the brain to improve cognitive function. The company’s EndeavorRx therapy has been approved by the FDA for the treatment of ADHD.

In May 2021, it received $160m in funding – $50m of debt and $110m in Series D equity funding – to scale its EndeavorRx product and support the development of other therapies through clinical trials.

Performance

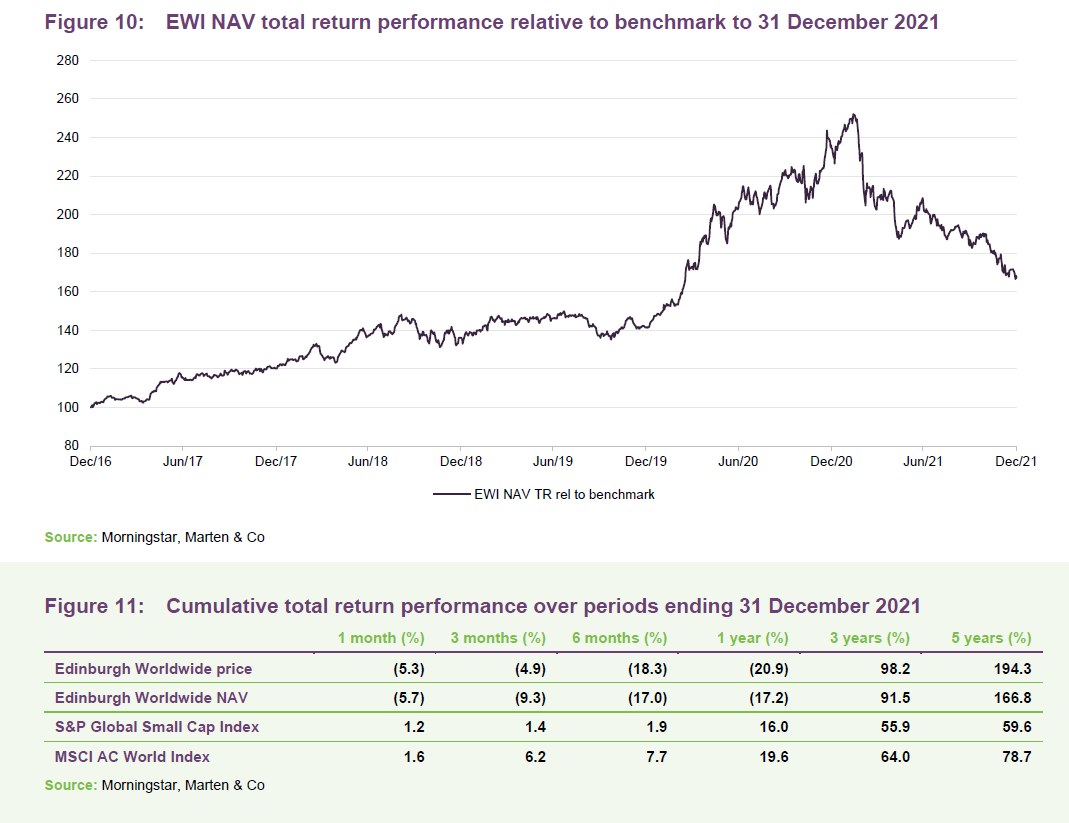

EWI underperformed its performance benchmark over the accounting year ended 31 October 2021, giving back some of the outperformance of earlier years, and that trend continued up to the end of December 2021. However, the objective is to outperform over five years and the record of outperformance over the long term is intact.

Over five years, small caps have lagged large caps, but EWI has delivered 2.8x the return of its performance benchmark in NAV terms and even more in share price terms as the discount has narrowed over that period (see page 19).

Drivers of performance

As Figure 10 shows, the change in EWI’s fortunes comes around the middle of February 2021. This coincided with a jump in US treasury yields associated with higher inflation and an expectation of higher interest rates. Companies such as the ones in EWI’s portfolio whose profitability is skewed towards the long-term tend to suffer disproportionately when long-term interest rates rise as the discount rate used to value future cash flows rises. It may also be true that investors took some profits after the considerable outperformance of many of these stocks in 2020 and switched money into cyclical stocks that they felt would benefit as COVID restrictions were eased. In addition, there were some business models – such as those that enabled working from home or supported online retail – that were seen to be beneficiaries of COVID-19-related lockdowns. For some investors there may have been an expectation that revenue/profit would take a hit once normality was restored.

The manager feels that, setting the macroeconomic influences aside, in time, the superior growth achieved by the winners within the portfolio is what drives long-term returns. It is more instructive, therefore, to look at attribution data on a stock-by-stock level.

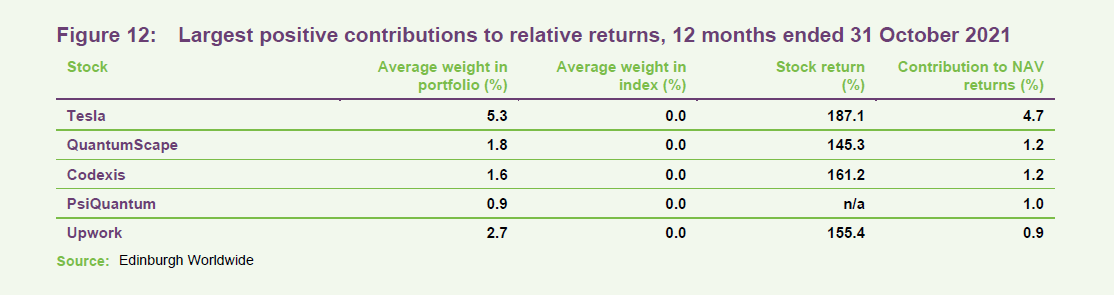

EWI has published some performance attribution data which covers the 12 months ended 31 October 2021.

Just outside this list is Oxford Nanopore Technologies, which contributed 0.7 percentage points to EWI’s relative return over this period.

QuantumScape

We discussed Tesla, Codexis and PsiQuantum above. QuantumScape (ir.quantumscape.com) makes solid-state batteries for electric vehicles and it is excited about the growth of the EV market. It feels that its batteries are a better alternative – in terms of energy density, charging time and safety – than lithium-ion batteries of the type used by Tesla.

QuantumScape has a 50:50 joint venture with Volkswagen to accelerate the commercialisation of the QuantumScape battery. Plans are underway to develop a factory or factories with a 2GW capacity. The output would not be exclusive to VW. Vehicle testing is scheduled for 2023 and full commercialisation is targeted for 2024/25.

The share price rose strongly after the business received a $680m cash injection following a merger with a SPAC.

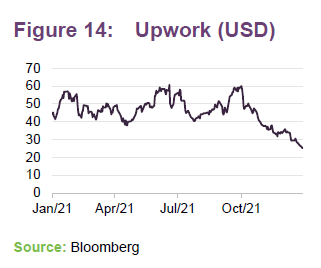

Upwork

Upwork is an online freelancing and recruitment services marketplace, connecting website and app developers, creative and design, finance and accounting, consulting and even some operations staff, with a wide range of businesses.

The stock price rose in the wake of good Q3 2020 figures. The Q3 2021 statement showed 32% year-on-year revenue growth on 25% client growth.

On the negative side, again we have already discussed Ocado.

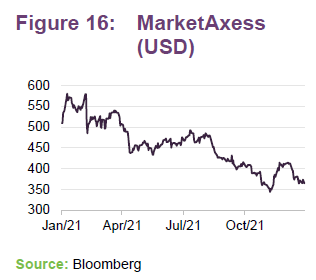

MarketAxess

Corporate bond trading site MarketAxess (investor.marketaxess.com) saw a fairly steady decline in its stock price over 2021. The bond market is gradually shifting towards electronic trading and MarketAxess feels that this will drive a considerable increase in market volume. It has been building its business through bolt-on acquisition and is expanding into other market segments such as muni bonds.

The business is cash-generative and has been returning cash through buybacks and dividends. However, revenue growth stalled in 2021 and quarterly earnings per share has been trending downwards. The company attributes this in part to low spreads and low volatility in the US market.

LendingTree

Online lending marketplace LendingTree (investors.lendingtree.com) found that its consumer loans division was hit hard by COVID. Volumes here and in its Home division have grown strongly over 2021 – revenue up 107% and 42% respectively, year-on-year for Q3 2021. Now, however, it is seeing a dip in revenue and profitability in its insurance division.

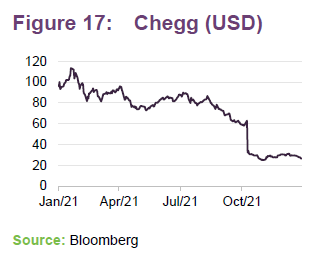

Chegg

Online education business Chegg (investor.chegg.com) saw a sharp drop in its share price following the announcement of third-quarter figures. Q3 numbers were not bad – 12% year-on-year revenue growth on 17% year-on-year growth in subscribers. However, the company said that in the US and Canada, learning sites and apps – both free and paid-for – experienced significantly reduced traffic from the start of the ‘fall semester’. Subscriber numbers fell by about 9.5% over Q3. The company’s projections for Q4 were well below analysts’ expectations. The company attributes this in part to the end of the pandemic and a shift from study to employment as the US labour market tightened.

Novocure

Novocure (novocure.com) is an oncology company seeking to treat solid tumours through the application of alternating electric fields tuned to specific frequencies – tumour treating fields (TTF). It has FDA approval for the use of TTF in three indications and has late-stage clinical trials underway in a number of others.

The company is targeting revenue in excess of $500m for FY21 and had almost $1bn in cash at the year end. Slowing revenue growth appears to have unnerved investors.

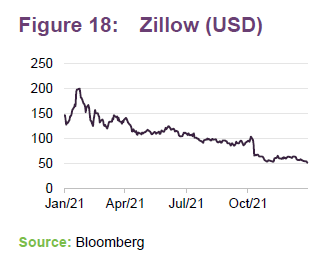

Zillow

Early in November, the price of Zillow (the US online real estate portal, which accounted for 3.6% of the portfolio at the end of October 2021) fell sharply. The stock moved from $105.72 at 31 October to $54.11 by end November, implying about a 1.8% hit to EWI’s NAV. The company’s results fell well short of expectations and it announced that it would discontinue its ‘Offers’ business line which bought and sold houses. The stock was $50.24 at 21 January 2022.

Peer group

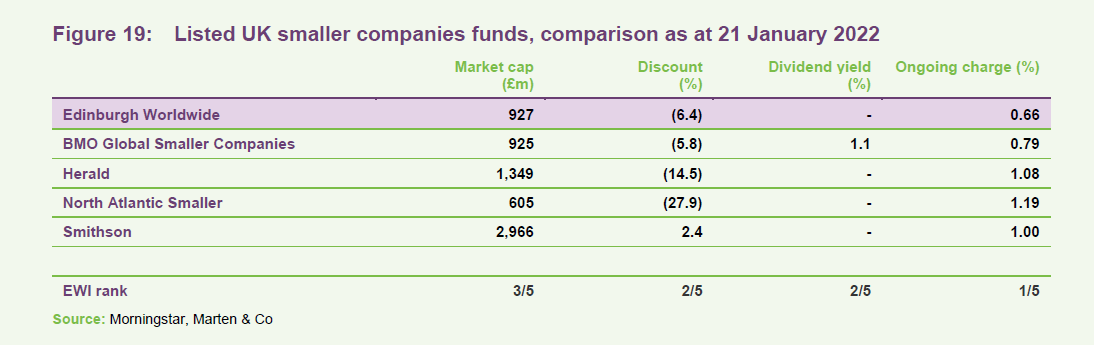

EWI is a constituent of the AIC’s global smaller companies sector.

Each of the funds in the sector is a reasonable size. EWI is the second-highest rated fund in the peer group. The focus of the funds in this sector is capital growth and none of these offers much by the way of a dividend yield. EWI has the lowest ongoing charges ratio of any of these funds.

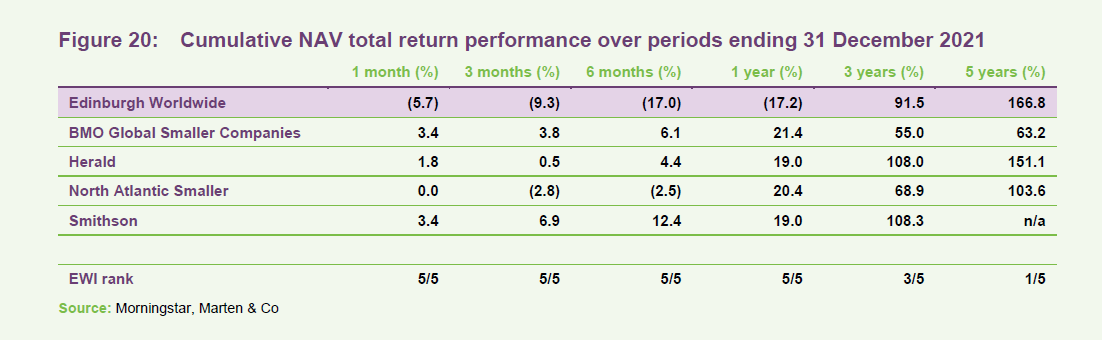

EWI’s short-term performance setback is evident in Figure 20. Nevertheless, the long-term (five-year) returns targeted by the manager remain the best of the peer group.

Dividend

EWI’s focus on capital growth tends to mean that there is insufficient net revenue to fund dividends. Indeed, the company has not declared a dividend since 2014, the year that the new strategy was adopted.

For the accounting year ended 31 October 2021, EWI’s net revenue per share was -0.62p, down from -0.46p for the prior year. The revenue reserve is negative (a net revenue loss of £4.1m) and this would have to be eliminated before EWI declared a dividend. If circumstances change, the board would pay the minimum permissible dividend consistent with the fund retaining investment trust status.

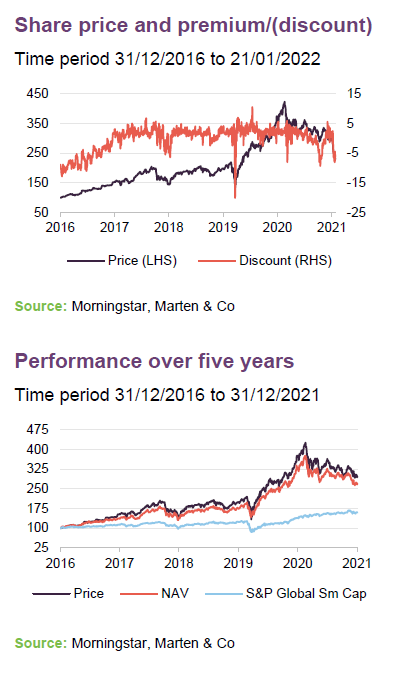

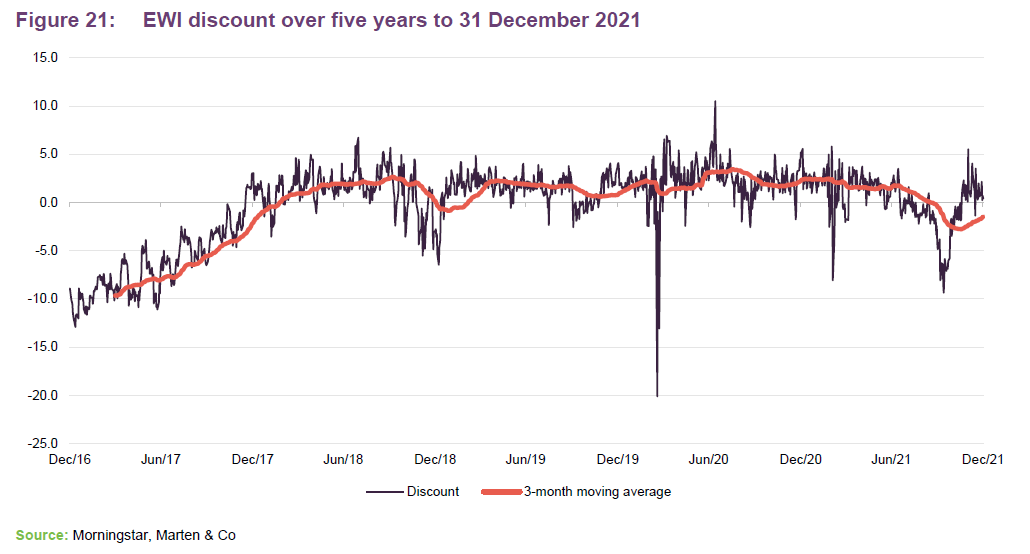

Premium/(discount)

Over the 12-month period ended 31 December 2021, EWI’s shares traded within a range of a 9.4% discount and a 5.8% premium to NAV and averaged a 0.4% premium. At 21 January 2021, the discount was 6.4%.

The main driver of the recent widening in EWI’s discount might perhaps be its short-term performance record.

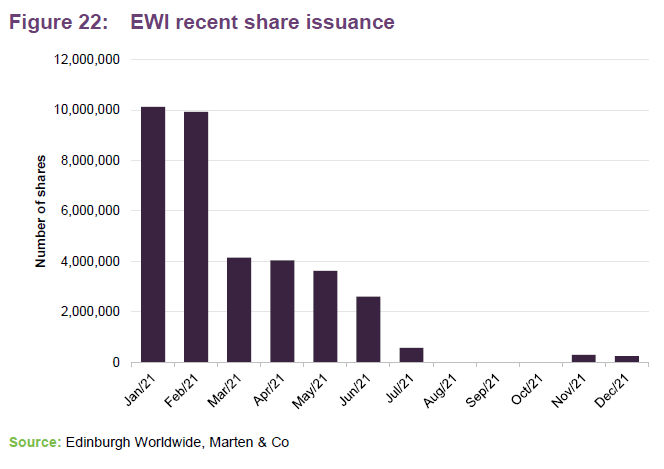

Each year, the board asks shareholders for permission to buy back up to 14.99% and issue up to 10% of EWI’s issued capital. Repurchased shares may be held in treasury and reissued when demand returns. Shares will only be issued or reissued at a premium to asset value, thereby enhancing the NAV for existing shareholders. Figure 22 shows the pattern of share issuance over 2021, which reflects the change in sentiment towards growth stocks and the emergence of a small discount in the second half of the year.

Fees and costs

The annual management fee is 0.75% on the first £50m of net assets, 0.65% on the next £200m and 0.55% on any remaining net assets. The management fee is calculated and payable quarterly. The management agreement can be terminated on three months’ notice.

The ongoing charges ratio for the accounting year ended 31 October 2021 was 0.66%, down from 0.72% for the prior year.

Capital structure

EWI has 405,753,695 ordinary shares in issue and no other classes of share capital. There are no shares held in treasury.

The trust’s accounting year runs to end October and its AGMs are typically held early in the new calendar year – the next is scheduled for 2 February 2022.

EWI does not have a fixed life and does not hold regular continuation votes.

Gearing and derivatives

The company recognises the advantages of long-term gearing and the investment policy allows gearing up to 30% of net assets. In practice, however, gearing has tended to be in single digits in recent years. Gearing levels are discussed at each board meeting.

EWI has a £100m five-year multicurrency revolving credit facility which is provided by The Royal Bank of Scotland International Limited and expires on 9 June 2026. In addition, there is a £26m multicurrency revolving credit facility provided by National Australia Bank Limited and an expiry date of 29 June 2023 and a £36m multicurrency revolving facility provided by National Australia Bank Limited with expiry on 30 September 2024.

At the end of October, EWI’s gearing was in the form of drawings in euros, dollars and sterling.

Derivatives can be used either as a hedge or to exploit an investment opportunity. In practice, they are not normally used.

Management team

Douglas Brodie

Douglas joined Baillie Gifford in 2001 and is head of the Global Discovery Team. He became a partner in 2015 and is a CFA Charterholder. Douglas graduated with a BSc in Molecular Biology & Biochemistry from the University of Durham in 1997 and attained a DPhil in Molecular Immunology from the University of Oxford in 2001.

Svetlana Viteva

Svetlana joined Baillie Gifford in 2012 and is an investment manager in the Global Discovery Team. She is a CFA Charterholder. Svetlana graduated with a BA in Economics and a BA in Business Administration from the American University in Bulgaria in 2008, MSc in Investment Analysis in 2009 and PhD in Accounting and Finance in 2012, both from the University of Stirling.

Luke Ward

Luke joined Baillie Gifford in 2012 and is an investment manager in the Global Discovery Team. He graduated with an MEng (Hons) in Mechanical Engineering from the University of Edinburgh in 2012.

Board

EWI’s board is comprised of six directors, each of whom is non-executive and independent of the manager. There are no changes expected in board composition over the coming year although Donald Cameron has indicated that he is unlikely to stand for re-election at the 2023 AGM.

Total directors’ fees are currently capped at £200,000 per year. However, to give the board flexibility to hire a new director ahead of Donald Cameron’s retirement, the board is asking shareholders to increase the limit to £250,000 at this year’s AGM.

Henry Strutt

Henry was appointed chairman on 24 January 2017. He qualified as a chartered accountant in 1979, following which he spent over twenty years with the Robert Fleming Group, seventeen of which were in the Far East. Henry is a non-executive director of New Waves Solutions Limited.

Donald Cameron

Donald is an advocate at the Scottish Bar (non-practising) and is also a qualified barrister in England and Wales. He was elected a member of the Scottish Parliament in 2016. Donald is a non-executive director of Murray Income Trust Plc.

Helen James

Helen is the former CEO of Investis, a leading digital corporate communications company. She was also previously head of pan-European equity sales at Paribas. Helen is the group chief operating officer of Brunswick Group.

Caroline Roxburgh

Caroline is a qualified Chartered Accountant and was a partner at PricewaterhouseCoopers LLP until 2016. She is a non-executive director and chair of the audit committee of Montanaro European Smaller Companies Trust Plc, a non-executive director and chair of the audit and risk committee of Edinburgh International Festival Society, a non-executive director of the Royal Conservatoire of Scotland and a publicly appointed member of the board of directors and chair of the audit and risk committee of VisitScotland.

Jonathan Simpson-Dent

Jonathan has spent the majority of his career running entrepreneurial private equity and listed mid-cap international growth businesses across multiple sectors, being a former CEO of Evander Group, Cardpoint and WLT (EMEA), CCO of Cardtronics Inc and CFO of HomeServe Plc and General Healthcare Group. He has also previously worked at PricewaterhouseCoopers LLP, McKinsey & Company and PepsiCo. Jonathan is the chair of Bromford Housing Group Ltd and a Fellow of the Institute of Chartered Accountants.

Mungo Wilson

Mungo is a former solicitor and is associate professor of finance at Saïd Business School, University of Oxford. He is also an associate member of the Oxford Man Institute of Quantitative Finance.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Edinburgh Worldwide Investment Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.