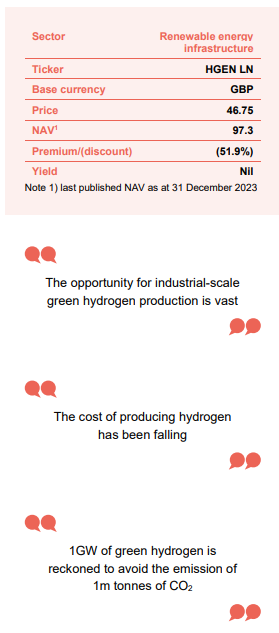

HydrogenOne Capital Growth

Investment companies | Initiation | 3 May 2023

Funding a green revolution

HydrogenOne Capital Growth (HGEN) is the only pure play green (renewables-powered, no carbon dioxide produced) hydrogen fund available on the London listed market. It offers diverse exposure to nine exciting private hydrogen investments and a hydrogen production facility that is being developed in Germany.

Spurred on by the need to tackle climate change and improve energy security, globally, governments are devoting considerable resources to jump-starting the green hydrogen industry. HGEN is well-positioned to benefit as investee businesses scale rapidly over the coming years. The investment adviser has around £500m worth of additional opportunities available.

HGEN should be seen as a long-term investment. However, in the short-term, more risk-averse (some might say panicky) investors have driven a sharp, and we feel unwarranted, fall in HGEN’s share price. With the shares at an 51.9% discount, new investors are being presented with an attractive entry point.

Diversified green hydrogen exposure

HGEN aims to deliver an attractive level of capital growth by investing, directly or indirectly, in a diversified portfolio of hydrogen and complementary hydrogen-focused assets whilst integrating core ESG principles into its decision making and ownership process.

Fund profile

More information is available on the trust’s website: hydrogenonecapitalgrowthplc.com.

HGEN is the first London-listed fund investing in clean hydrogen for a positive environmental impact. It aims to deliver an attractive level of capital growth by investing, directly or indirectly, in a diversified portfolio of hydrogen and complementary hydrogen-focused assets whilst integrating core ESG principles into its decision-making and ownership process.

HGEN compares its NAV performance to the Solactive Hydrogen Economy Index.

HGEN’s AIFM is FundRock Management Company (Guernsey) Limited (formerly Sanne Fund Management (Guernsey) Limited). It is advised by HydrogenOne Capital LLP, whose lead managers are JJ Traynor and Richard Hulf. More information on the advisers is available on page 24.

HGEN can hold both listed and unlisted (private) investments, however the majority of the portfolio is invested in unlisted hydrogen assets. In both cases, HGEN aims to be a long-term investor. The early portfolio was established with a liquidity reserve of cash and listed hydrogen assets, with the intention of giving investors exposure to the sector from day one.

HGEN holds its unlisted investments through a 100% stake in a limited partnership, HydrogenOne Capital Growth Investments (1) LP.

The market for green hydrogen

The opportunity for industrial-scale green hydrogen production is vast…

With the potential to eventually replace fossil fuels in many applications, the opportunity for industrial-scale green hydrogen production is vast, particularly in hard to decarbonise sectors of the market such as power generation and transport. While estimates vary, some 20bn tonnes per annum of greenhouse gas emissions could be addressed with clean hydrogen over time, which is over one third of all greenhouse gas emissions today.

…but billions of dollars of investment are needed.

Reaching such lofty targets will require billions of dollars of investment over the next few decades; however, the industry has already advanced rapidly over the last few years. Production costs are falling and technologies already available today utilise hydrogen to produce, store, move and use energy to reduce greenhouse gas emissions.

Governments recognise the urgent need to decarbonise the hydrogen sector.

Governments recognise the urgent need to decarbonise the hydrogen sector. In addition to the environmental benefits, energy market upheaval stemming from the war in Ukraine has also provided a new imperative to fund alternatives to Russian natural gas and oil, and to improve energy security.

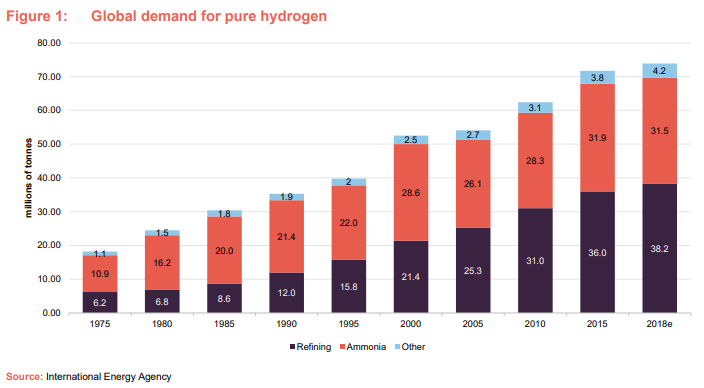

Hydrogen is currently used extensively across industrial applications, predominantly in oil refining and the production of fertilisers – however, its use extends across a wide range of end markets including steel and cement production, artificial fibres, glass, electronics, and metallurgy. It is light, storable, reactive, can be readily produced at industrial scale, and contains more energy per unit of mass than natural gas or gasoline, making it attractive as a transport fuel.

Although out of date, Figure 1 shows how the demand for hydrogen has grown over since 1975 and breaks down the main uses of the hydrogen produced.

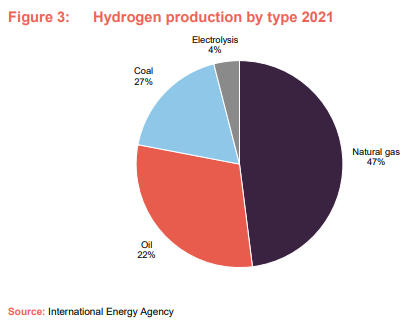

The existing market for hydrogen is estimated to be worth $175bn annually.

The existing market for hydrogen is estimated to be worth $175bn annually. Crucially, almost all of this is so-called grey hydrogen, which is produced by steam methane reforming (SMR) powered by coal and natural gas, generating around 830m tonnes a year of greenhouse gases (for reference, the United Kingdom generated about 500m tonnes in 2021).

Currently, only around 1% of global hydrogen production is derived from renewable energy, which is known as green hydrogen, so the first challenge is to transform existing generation from grey to green (which will be discussed in more detail below). Green hydrogen can replace dirty (grey) hydrogen as the major energy source for existing industrial processes as well as be integrated into new end markets where it is proving difficult to meaningfully reduce greenhouse gas emissions, such as long-haul transport, chemicals, and iron and steel manufacturing.

Hydrogen can be used as a form of energy storage.

Hydrogen will also play a crucial role in the ongoing development of the wider renewables sector as one of the leading options for energy storage, helping to address the current variable output issues associated with solar and wind generation – one of the major issues with renewable energy currently is being able to effectively store excess production of energy for long periods of time. The diversion of excess production of renewable energy at times of peak supply (when intraday power prices are exceptionally cheap) into hydrogen generation offers another form of energy storage that can be held indefinitely (unlike traditional battery storage) and used to fuel peaking power plants (power plants that generally run only when there is a high demand for electricity, traditionally powered by natural gas or coal).

Hydrogen is capable of being produced using a range of fuels including renewables, nuclear, and biomass (renewable organic material that comes from plants and animals). It can then be transported as a gas via pipelines, or in liquid form by ships and other forms of heavy transport. This flexibility should help support production economics as cost curves improve to match market prices for grey hydrogen and other polluting fuels.

The colours of hydrogen

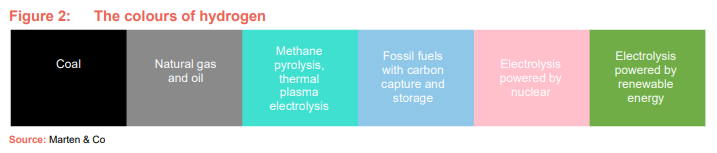

The principal behind hydrogen as a fuel source is relatively simple. The traditional method of production splits out hydrogen from natural gas (through the process of steam methane reforming mentioned above), releasing a large amount of carbon dioxide into the atmosphere in the process. Once the hydrogen has been separated, it can then be used in a similar fashion to fossil fuels; however, power is generated through a chemical reaction rather than combustion, producing only water and heat as biproducts. The end result, then, is much more environmentally friendly – however, the immediate challenge we face is to produce this hydrogen without the associated emissions. At present, there are several methods of producing hydrogen, the various types tend to be identified by colour, but these are not always used consistently across the industry. Our chart shows black, grey, turquoise, blue, pink and green hydrogen.

As touched on above, the current market is dominated by dirty hydrogen including “black”, “grey” and (not shown) “brown” hydrogen which refers to production from coal, natural gas and lignite, respectively. “Blue” hydrogen refers to the production of hydrogen from fossil fuels with CO2 emissions reduced by the use of carbon capture, utilisation and storage. While blue is theoretically a more carbon-friendly alternative, research has suggested that its total carbon footprint may actually be worse than simply burning natural gas or coal during some applications, particularly when it is used for heating.

Green hydrogen, produced from the electrolysis of water, could be a nearly limitless source of energy.

Hydrogen produced by electrolysis involves splitting water into oxygen and hydrogen. This production process emits no CO₂, although at present it remains expensive and energy intensive. Where the power source for electrolysis is nuclear, the output is known as “pink” (or sometimes “purple” or “red”) hydrogen. Where the power comes from renewable energy, the output is known as green hydrogen. Using water makes it possible that hydrogen could become a nearly limitless source of energy for all of us in the future.

“Turquoise” hydrogen, formed by methane pyrolysis or thermal plasma electrolysis, involves heating (and in the thermal plasma case, passing an electric current through) methane until it decomposes into carbon and hydrogen. HiiROC, within HGEN’s portfolio, is making hydrogen using thermal plasma electrolysis – applying an electrical field to methane, splitting it into hydrogen and carbon black (see

page 14). Where the methane used is biomethane, the net effect is to sequester carbon from the atmosphere. HiiROC refers to this as “golden” hydrogen.

Today’s coalition of voices in favour of hydrogen includes renewable electricity suppliers, industrial gas producers, electricity and gas utilities, automakers, oil and gas companies, major engineering firms and the governments of most of the world’s largest economies.

Cost comparison

The cost of producing hydrogen has been falling.

The cost of producing hydrogen has been falling. However, fluctuating fossil fuel prices are a complicating factor for comparisons across technologies. HGEN quotes a price range of $1.5–$2.3 per kg in the US for grey hydrogen. Blue hydrogen is relatively expensive, coming in at about $3–$11 per kg. Green hydrogen is estimated to cost $1–$6 per kg although subsidies introduced by the Inflation Reduction Act (see below) are thought to reduce that range to $1–$5 per kg.

Technology – let’s talk electrolysers

The process of using water electrolysis and fuel cells for energy is not a new one. In fact, it was used to fuel the first internal combustion engines over 200 years ago. Despite its long history, the sector has failed to fully develop as a long term, sustainable industry, until now. Initial optimism in the ‘70s faded, as oil price shocks resolved to a new era of cheap, polluting energy, stymying further investment in hydrogen technology. Similar attempts were curtailed through the ‘90s and again in the 2000s once again due to the resurgence of cheap oil, which drastically increased the opportunity cost of hydrogen investment. However, much has changed over last 10 years, driven by the declining cost of renewable energy, the need to tackle climate change and the increasing efficiency of electrolysers; production costs are now expected to decrease by around 50% by 2030.

There are three main types of electrolysers that exist today: alkaline electrolysis (ALK), proton exchange membrane (PEM) electrolysis, and solid oxide electrolysis cells (SOECs). The technology for alkaline and PEM electrolysis have been around for decades, while SOECs remain more in the development phase, attracting significant investments from companies such as Ferrari and Shell.

All three offer various pros and cons, with alkaline electrolysis known for its durability and low operating costs. PEM is seen as providing much greater efficiency; however, it requires expensive electrode catalysts (platinum, iridium) and membrane materials, and their lifetime is currently shorter than that of alkaline electrolysers. The majority of new investment into the sector has flown into PEM projects over the last few years. However, it is hoped that SOECs can also work in tandem with the other systems, providing a cheaper, more efficient alternative to the established technologies through the use of ceramics as the electrolyte.

SOECs have to operate at high temperatures (about 700–800°C) although their efficiency can be increased by more than 100% when powered by industrial waste heat. PEM and alkaline electrolysers do not have that requirement (about 70–90°C and under 100°C, respectively).

Alkaline electrolysers are currently the dominant technology, making up about 75% of global manufacturing capacity, and PEM making up about 25%. SOECs currently account for a very small amount of early-stage manufacturing.

HGEN has a particular focus on diversifying its exposure to different technologies and geographies. As an example of this, the company has invested in solid oxide, alkaline and PEM producers of electrolysers.

Government support is delivering on the promise of green hydrogen

1GW of green hydrogen is reckoned to avoid the emission of 1m tonnes of CO2.

1GW of green hydrogen is reckoned to avoid the emission of 1m tonnes of CO2. The various use cases for green hydrogen have the potential to avoid the emission of 20 gigatonnes of greenhouse gases.

Globally, governments have accepted the need to accelerate the transition to green hydrogen and are providing significant support to this. In the US, the Inflation Reduction Act contained $9.5bn of funding for hydrogen to subsidise production tax credits of up to $3 per kilogramme. The US Department of Energy added a further $400m to a program seeking to reduce the cost of clean hydrogen by 80% to $1 per kilo over the next decade. In addition, the Bipartisan Infrastructure Law set aside $750m to fund research, development, and demonstration efforts to dramatically reduce the cost of clean hydrogen.

In Europe, the EU strategy on hydrogen was adopted in 2020. In May 2022, the EU published its REPowerEU plan, which is designed to find alternatives to Russian fossil fuels and has increased EU hydrogen targets for 2030 by a factor of four. Its ambition is to produce 10m tonnes and import 10m tonnes of renewable hydrogen in the EU by 2030. In Japan, the 2030 target is 3m tonnes per annum. In the UK, the government is aiming for 10GW of hydrogen, again by 2030.

While these policies are undoubtedly positive, there has been some controversy surrounding the rollouts. On the continent, translating ambition into action has proved easier said than done; for example, it has taken more than two years to obtain the necessary exemptions for increased public aid for the hydrogen sector. This lack of action has been put into sharp relief by ground-breaking US legislation. Large subsidies and tax credits for US-manufactured renewables products have raised eyebrows relating to free trade and competition policy, and have led some manufacturers to consider shifting production. The EU have returned serve, announcing large scale public funding for green projects from their state aid programme. The outcome, for investors appears to be an even more aggressive regulatory tailwind which had already reached levels well ahead of what many would have thought plausible.

Projects are being built.

The upshot of these and other initiatives is that the false dawns for the hydrogen sector over recent years should now be behind us. While the operational base of green hydrogen is just 0.8GW today, 6.0GW is under development and 1.2TW of projects are proposed. For reference, the UK requires around 300TWh of electricity annually.

There is already new demand beyond the one-for-one substitution of grey hydrogen.

For the next few years, there is more than enough demand from customers looking to switch away from grey hydrogen to justify the construction of these new plants. However, the alternative use cases are already being developed. For example, in the UK, National Gas’s Future Grid project is testing the effect of blending hydrogen with natural gas in the existing transmission network. Snam (an Italian energy infrastructure company) in Italy has already tested a 10% blend, and in Germany, the town of Oehringen in the southwest of the country is trialling a 30% blend.

In aggregate, the potential market for green hydrogen is estimated to be $2.6trn.

Despite such a multitude of tailwinds, we remain in the early innings of the transition away from dirty hydrogen, and, as has been the case across the entire renewables sector, costs remain the major barrier in the short term. The biggest issue lies with renewable energy capacity which, at present, is far too small. Today, total annual hydrogen production is around 70Mt. If all this was to be produced using renewable energy it would require more than the entire generation capacity of the European Union. The good news is that renewable energy capacity continues to accelerate. In many cases, wind and solar power is now cheaper than fossil fuel equivalents and the world is set to add as much renewable power in the next five years as it did in the previous 20 years, overtaking coal to become the largest source of global electricity by 2025. The recent success of solar, wind power, and electrical vehicles in particular have shown that the combination of political and technological innovation have the power to build global clean energy industries, with green hydrogen likely to be a significant benefactor. The total addressable market for green hydrogen is thought to be $690bn by 2030 and $2.6trn by 2050.

The investment process

HGEN is designed to offer exposure to a diversified portfolio of hydrogen and complementary hydrogen-focused assets in the OECD. The private hydrogen assets that form the bulk of the portfolio are expected to be mainly in the form of equity (although investments may be made by way of debt and/or convertible securities), will be held for the medium to long term, and may include controlling stakes in companies (although, as we show in Figure 8 on page 12, all of HGEN’s existing positions represent minority stakes). The advisory team will seek to ensure that HGEN’s investments come with minority protection rights (which can grant a minority shareholder a ‘veto’ over specified actions of the company) allowing it to monitor the underlying companies’ activities to ensure that they comply with HGEN’s investment policy.

The advisory team have built up a network of contacts within the hydrogen industry and have good connections with existing players in the space. HGEN is often investing alongside large industrial companies, as well as other specialist ESG investors and venture capitalists.

HGEN is an Article 9 climate impact fund.

HGEN is an Article 9 climate impact fund under SFDR, with 89% of its activities aligned to EU taxonomy. The maintenance of Article 9 status is central to the investment approach adopted by the advisory team. An analysis of ESG aspects is a critical part of HGEN’s due diligence, therefore, and ongoing monitoring of these issues is an important part of the adviser’s role.

Potential investments need to be material and scalable. HGEN is not an early-stage investor. Investee companies will tend to have physical infrastructure in place and a pool of staff. The advisers are targeting NAV returns of between 10–15% on average over time, factoring in their estimation of the likely exit multiple of the investment.

Candidates for inclusion within the portfolio are subjected to an intense due diligence process. In addition to the resources of the investment adviser, HGEN has access to the knowledge of the advisory board (see page 24 and 25), and a due diligence team at professional services firm Arup. Typically, the due diligence process takes about six weeks. As an aside, the team says that the due diligence costs associated with establishing the initial portfolio have been inflating HGEN’s expense ratio.

The investment adviser is responsible for determining which assets make it into the portfolio and the position sizes. However, potential deals need to be signed off by the AIFM, and the board also gets to review prospective investments before they are made.

Investor protections and governance

Wherever possible, HGEN’s investments are structured in such a way as to embed downside protections.

Wherever possible, HGEN’s investments are structured in such a way as to embed downside protections. At the end of December 2022, all of the assets in the private hydrogen portfolio benefitted from downside protections such as anti-dilution and liquidation preferences ( which protect equity holders from dilution from subsequent equity issuances) In addition, around two thirds of this portfolio was invested against delivery milestones.

HGEN has also secured representation on each private hydrogen investment board.

Restrictions

In its prospectus, HGEN promised to abide by the following investment restrictions:

- no single private hydrogen asset will account for more than 20% of gross asset value (GAV);

- private hydrogen assets located outside developed markets in Europe, North America, the GCC and Asia Pacific will account for no more than 20% of GAV;

- at the time of an investment, the aggregate value of the company’s investments in private hydrogen assets under contract to any single off-taker will not exceed 40% of GAV;

- no single listed hydrogen asset will account for more than 3% GAV, with a targeted average stock weighting of 1.5% of GAV;

- the portfolio of listed hydrogen assets will comprise no fewer than 10 listed hydrogen assets at times when the company is substantially invested;

- listed hydrogen assets must derive at least 50% of their revenue from hydrogen and/or related technologies;

- listed hydrogen assets and related businesses held in the liquidity reserve must:

- consist of larger hydrogen companies, companies in the industries that support these manufacturers and project level companies; and

- have a market capitalisation (at the time of investment) of at least US$1bn; and

- in the liquidity reserve, no single listed hydrogen asset or related business will account for more than 7% of GAV (with a targeted average stock weighting of 2.5% of GAV).

Hedging

Currently, HGEN’s non-sterling exposures are hedged using forward foreign exchange contracts, but the company may decide to discontinue this in the future.

Realisations

Existing hydrogen producers may be prepared to acquire promising companies even before they become established.

Whilst the approach is a medium- to long-term one, the advisers believe that HGEN could achieve its first exit within two to four years of its launch. They note that existing hydrogen producers may be prepared to acquire promising companies even before they become established. The advisers will weigh up potential offers against their view of the risk/reward opportunity presented by such investments.

Asset allocation

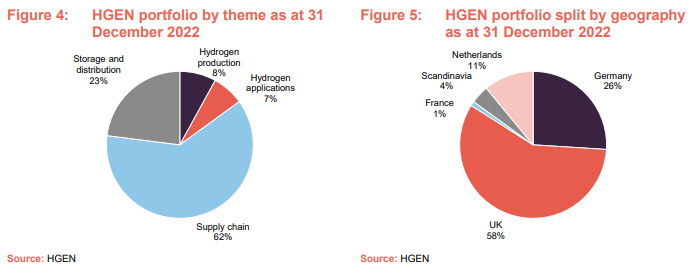

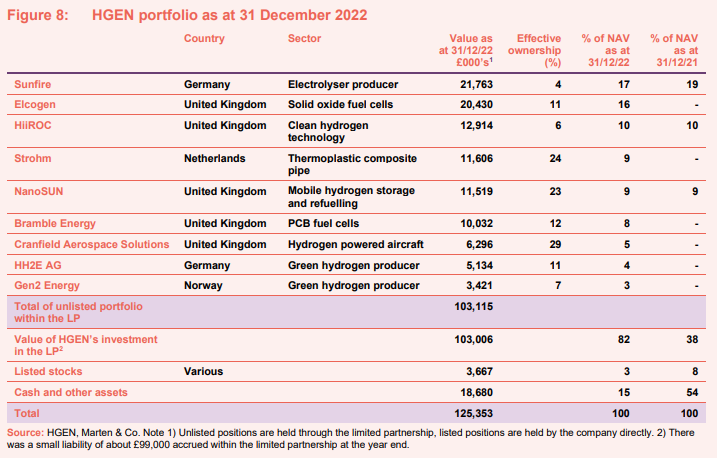

At 31 December 2022, HGEN had invested £103m in private hydrogen assets, had £3.7m in listed assets and a further £18.7m of cash.

Since the end of 2022, HGEN has invested an additional £1.4m into Cranfield Aerospace Solutions (the final tranche of the £7m commitment that HGEN made to that company) and announced its first investment of £2.5m in a green hydrogen project, at Thierbach in Germany.

Seven of the private investments, representing 89% of the invested portfolio by value, are revenue-generating. The aggregate revenue from these investments was about £33m for 2022, more than double that of 2021.

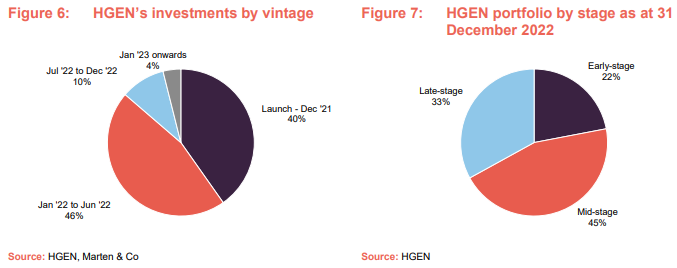

The advisers have classified HGEN’s portfolio by “stage”. Roughly, early-stage companies are those with forecast annual revenues for 2024 of less than £20m, this currently includes companies such as Bramble, Cranfield Aerospace and HH2E. Mid-stage companies are those with revenues between £20m and £60m; this includes HiiROC, Elcogen and NanoSUN. Late-stage companies, such as Strohm and Sunfire, have revenues in excess of £60m.

The hydrogen production companies – Gen2 and HH2E – represent about 8% of the portfolio. The advisers believe that both these companies ae capable of generating material cash flow from the middle of the decade as projects come online.

The advisers suggest that the forecast holding period for late-stage companies might be less than three years, between three and five years for mid-stage companies, and over five years for early-stage companies.

The advisers suggest that the average revenue growth of the portfolio as a whole might be 21x between 2021 and 2024, which is a compound annual growth rate (CAGR) of 174%.

Sunfire

Sunfire: manufacturer of alkaline and solid oxide electrolysers.

Sunfire (sunfire.de) makes electrolysers used to manufacture both hydrogen and synthetic gas. It makes electrolysers in both alkaline and solid oxide varieties (discussed on page 7 and 8). It also makes off-grid power supply technology – based on its solid oxide fuel cells.

Sunfire employs about 500 people in Germany and Switzerland. In addition to HGEN, it is backed by several investors including Neste, SMS Group and Amazon. Revenues have grown over 10x since HGEN first invested, albeit from a low base.

Sunfire’s products are being used in a 30MW pressurised alkaline electrolyser for German energy giant Uniper, a 20MW plant in Finland for P2X, and a test plant at Lingen in Germany run by RWE. In its nearby Solingen plant, Sunfire is optimising its factory, with the help of Vitseco Technologies, to produce alkaline electrolysers at scale. It is targeting 500MW in 2023, which will grow to a multiple of this over time. Sunfire recently installed 12 solid oxide electrolysis modules at Neste’s renewable products refinery in Rotterdam. Capable of producing 60kg of hydrogen per hour, this is the world’s largest high-temperature electrolysis system (2.6 MW) installed in an industrial environment.

Elcogen

Elcogen: amongst the world’s most advanced solid oxide specialists.

Elcogen (Elcogen.com) is the second-largest holding in the HGEN portfolio, accounting for 16% of the fund’s total NAV. It is amongst the world’s most advanced solid oxide specialists, focusing on fuel cells and electrolysers and its technology can be applied to a broad range of residential, industrial and commercial applications. The company, which is based in Estonia and Finland, has developed a unique, reversible ceramic technology that can convert hydrogen into emission-free electricity and vice versa, providing long-term, high-capacity energy storage. Its products have two major advantages: they operate at lower temperatures and are significantly more efficient than competitor products, and these benefits have driven strong commercial demand despite the relative infancy of the sector. At present, the company has an established base of over 60 industrial customers worldwide.

HGEN’s total stake in the company is £20.5m. The capital is being used to fund the expansion of Elcogen’s facilities in Tallinn to create a new, automated production line for solid oxide fuel cells, initially scaled at 25MW/year, rising to 50MW/year (equivalent to 100MW–200MW in electrolysis mode). It will also allow the company to further invest in research and development to continue progressing solid oxide technology and fuel cells. Other Elcogen investors include Biofuel OÜ, and VNTM Powerfund II. The company has also received funding from the European Union’s Horizon 2020 research and innovation programme.

HiiROC

HiiROC: thermal plasma electrolysis.

HiiROC (hiiroc.com), founded in 2019, has developed an innovative new patented technology as an alternative to existing methods of electrolysis called thermal plasma electrolysis (TPE). The company is currently in the development stage with pilot units contracted for deployment through 2023 across a range of hydrogen use cases.

HiiROC’s TPE converts natural gas, flare gas and biomethane into hydrogen and solid carbon black. This results in zero CO2 “turquoise hydrogen” at a comparable cost to steam methane reforming, but without the associated emissions and using only one fifth of the energy required for the electrolysis of water. The carbon black biproduct can then be used in multiple commercial applications such as tyres, rubbers, plastics, building materials and as a soil enhancer.

HiiROC has strong growth potential right across the hydrogen economy, from grid injection and electricity generation to decarbonising industry by replacing natural gas, flare mitigation and synthetic fuels. Initial projects include a 400kg/day hydrogen facility in Germany, recently announced by Wintershall Dea and VNG as well as at EPi’s biomethane pilot plant in Chelmsford, and with Northern Gas Networks as part of its hydrogen programme.

HGEN’s initial investment from November 2021 totalled £10m, joining multinationals Centrica, Hyundai and CEMEX on the shareholder register. Since the initial investment, HiiROC has gone from strength to strength, winning the KPMG Global Tech Innovator 2022 award, overcoming fierce competition from over 1,250 applicants across 22 countries and jurisdictions during the national stages. It was also awarded the FT’s Tech Champion for Energy 2022.

HiiROC has grown its revenues by a factor of 10 since HGEN’s initial investment. It has also entered an MOU with Egypt’s EGAS for flare gas mitigation, and won the first UK project to inject Hydrogen at Brigg Gas Fired Power station, as part of the Net Zero Technology Centre’s £8m Open Innovation Programme.

Strohm

Strohm: leading manufacturer of fully bonded Thermoplastic Composite Pipe.

Strohm (strohm.eu) is the first and leading manufacturer of fully bonded Thermoplastic Composite Pipe (TCP), a lightweight, flexible, and high-strength pipe. Its pipes do not corrode or embrittle when in contact with water, carbon dioxide, hydrogen or hydrogen sulphide. TCP has about a 50% lower carbon footprint than metal.

Strohm’s initial business was focused on the oil and gas industry. However, it is rapidly expanding its renewables business. Strohm is the industry leader in offshore hydrogen pipelines, whereby green hydrogen generated at offshore wind turbines can be transported to shore via Strohm’s subsea pipe infrastructure. Its pipes also have applications in carbon capture, utilisation and storage.

Generating hydrogen at the site of the offshore turbine and transporting that by pipe rather than transmitting electricity by cable, can transfer up to 10 times more energy, while avoiding curtailment and grid charges, providing considerable cost and operational benefits (watch an explanatory video here).

HGEN’s initial investment totalled £8.4m and it has added a further £1.7m for a total stake of £9.5m, worth 8.7% of total NAV. HGEN’s co-investors include Shell Ventures, Chevron Technology Ventures, Evonik Venture Capital, and ING Corporate Investments. The proceeds from its latest round of funding enabled Strohm to accelerate the expansion of its manufacturing operations to 140km of pipe per annum. The company expects revenues from renewable energy to account for over 50% of the total by 2025. It sees the total market expanding to £700m by 2030, and acerating to more than £1.7b by 2040.

The company has seen considerable commercial success over the past year singing with ECOnnect to provide more than 11km of TCP for the TES Wilhelmshaven Green Gas Terminal in Germany. Strohm also secured its largest commercial agreement in history from ExxonMobil for its offshore operations in the Americas. Company revenues have more than tripled since HGEN’s initial investment, reflecting the positive growth that the company is experiencing.

NanoSUN

NanoSUN: supplier of mobile hydrogen storage and refuelling systems.

NanoSUN (nanosun.co.uk) is a supplier of mobile hydrogen storage and refuelling systems to hydrogen consumers. The company’s novel technology provides a flexible and low-cost connection between hydrogen customers such as truck stops, and concentrated hydrogen supply sources. NanoSUN’s Pioneer units are filled with hydrogen at source, and transported to customer sites, where they provide storage and refuelling facilities, all in a single, re-fillable system. By combining distribution and dispensing equipment into a single unit, the resultant offering to customers is more flexible and lowers structural costs by some 60% compared to traditional systems.

HGEN’s total investment of £9.1m joins other investors, including Germany’s Westfalen Group, with the proceeds going toward the expansion of manufacturing capacity and the development of next generation refueler units. The company has also received significant funding from the Department for Business, Energy & Industrial Strategy.

The company has seen several positive developments in recent months, including the completion and delivery of its enhanced Pioneer Mobile hydrogen refuelling stations, and the signing of an agreement with Hydrogen Systems to deliver hydrogen refuelling solutions to central Europe. Revenue has grown over 60x since HGEN’s initial investment while the company has also identified substantial demand for the Pioneer product, developing a strong order book for 2023–2024 with clients such as Westfalen, and Octopus Hydrogen.

Bramble Energy

Bramble Energy: printed circuit board fuel cell solution.

Bramble Energy (brambleenergy.com) is pioneering revolutionary fuel cell design and manufacturing techniques. Its printed circuit board fuel cell solution (PCBFC) manufactures low cost, scalable and recyclable fuel cell modules that can be made at any PCB factory world-wide. The advisers feel that the real value in the patented PCBFC is the cost reduction potential of 100kw+ fuel cells used in the automobile sector. Bramble is working closely with Tier 1 auto companies in the US and Japan to adopt Bramble technology/IP on a licensed basis.

HGEN’s £10m investment in Bramble formed part of a £35m fundraising round, including existing Bramble investors IP Group, BGF, Parkwalk and UCL Technology Fund. The money is being used to scale the company’s product offering.

Over the past 12 months, the company has reached a number of significant milestones, winning the Scale-up Readiness Validation, SuRV, competition while also receiving funding from the Department for Business, Energy & Industrial Strategy (BEIS) as part of the £40m Red Diesel Replacement competition.

Cranfield Aerospace

Cranfield (cranfieldaerospace.com) is an aerospace market leader in the design and manufacture of new aircraft design concepts, complex modifications to existing aircraft and integration of cutting-edge technologies to deliver hydrogen-powered turboprop flight.

Phase one of the company’s zero emissions aircraft roadmap is the conversion of a Britten-Norman Islander 9-seat aircraft from conventional fossil fuel to that of gaseous hydrogen propulsion. This development is set to deliver the world’s first fully certified, truly green, passenger-carrying aircraft using hydrogen fuel cell technology. The end solution will deliver emissions-free commercial air travel and is planned to be certified for passenger flight in 2026.

Just prior to publishing, Cranfield and Britten-Normen announced a merger to improve the efficiency of the business model with the goal to create the world’s first fully integrated, zero-emissions sub regional aircraft. The move is a positive development given how closely the two companies work together and should generate a number of synergies.

HEGN originally invested £7.0m in the company, along with co-investors Safran Corporate Ventures, the UAE-based Tawazun Strategic Development Fund, and Motus Ventures. As part of the deal to create the newly merged company, HGEN has injected a further £5m into the combined business as part of a £10m funding round.

Cranfield continue to tick off milestones, having achieved preliminary design targets in 2022, it expects to conduct test flights in 2024. Strong execution to date has seen strong order book growth, with the company signing numerous commitments for modification kits to convert Britten-Norman Islanders to hydrogen-electric power.

The company has 90+ staff and is one of very few aerospace SMEs globally to have both whole aircraft design capability, and to hold a range of regulatory approvals for the design and manufacture of modifications to existing aircraft. Cranfield is a long-established aircraft company with a customer base that has included Boeing, Airbus, and Rolls Royce (amongst others).

HH2E

HH2E: German developer of green hydrogen production facilities.

HH2E (hh2e.de/en) is a specialist in developing projects to decarbonise industry, using green hydrogen, with associated energy storage and hydrogen power generation facilities, with the intention of providing 24/7 clean energy for customers. Its technology-mix, a combination of battery and alkaline electrolysers, enables near-constant production using the cheapest hours of renewable electricity supply. This transforms a variable input of sun or wind energy into a constant flow of price-competitive green hydrogen, heat and carbon-free electricity, to supply local industries and municipalities

HH2E has already identified multi-billion and multi-gigawatt investments over several projects in Germany, including the Thierbach project (discussed in more detail below).

Over the next few years, the company’s emphasis will be on decarbonising existing industrial sites, but over time, HH2E also intends to develop greenfield projects.

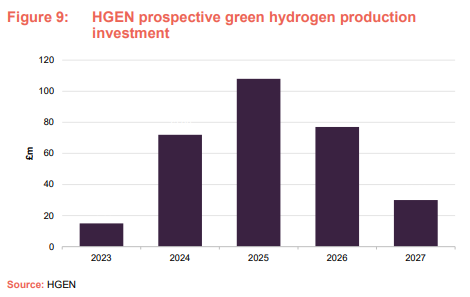

HGEN has invested £5m alongside funds managed by Foresight Group LLP, and both companies have signed a framework agreement giving the right to co-invest in HH2E’s projects directly. This will provide a substantial part of the development and construction capital covering five large projects. These projects are expected to be at industrial locations across Germany and will cost in excess of £300m to fully develop (see page 17).

Along with the successful development of projects throughout the year, HH2E has signed a purchase agreement with Nel for a 120MW electrolyser and has also continued to invest in technology, committing €1m into Stoff2, an early-stage technology firm developing a combined battery-electrolyser product which HH2E could deploy from 2026 onwards.

Gen2 Energy

Gen2 Energy: Norwegian developer of green hydrogen production facilities.

Gen2 Energy (gen2energy.com) was HGEN’s first step into hydrogen supply projects. The Norwegian company manufactures green hydrogen utilising the abundant, low-cost renewable power which is being generated in excess of market demand in the region. Hydroelectric power, the key constituent in the power mix in Norway, has the additional advantage of very high uptimes compared to green electricity from wind and solar sources, meaning that Gen2’s electrolysers could operate virtually 24/7, with lower unit costs of hydrogen as an outcome.

By converting this electricity to green hydrogen, and where necessary transporting the hydrogen to industrial customers by sea, the company aims to become a regional supplier of low-cost clean fuel and feedstock. Gen2 has a series of projects in its pipeline, totalling an estimated 700MW, in Norway to begin with, which could commence production in 2024–2026.

Over the past year, the company has developed a number of hydrogen development projects with an initial focus on a 100MW plant at Nesbruket in Mosjøen. Its long-term goal is to establish production capacity at large-scale for green hydrogen based on 100 percent renewable energy, and to operate a reliable and efficient logistics network.

HGEN has invested £3m in Gen2 alongside HyCap, while existing industrial backers include Vitol, Höegh LNG, and the Knutsen Group.

Thierbach

Thierbach: an industrial-scale green hydrogen production plant.

The Thierbach Project is a development for the construction of an industrial-scale green hydrogen production plant that will serve customers across the energy, transportation and industrials sectors in Germany. As noted above, the project will be built and operated by HH2E as part of a consortium comprised of HH2E, Foresight Group, and HGEN. The project will harness HH2E technology, combining alkaline electrolysers with a high-capacity battery, to address the challenges of volatile renewable energy production enabling the constant production of cost-competitive green hydrogen without a permanent supply of power.

The projected is expected to have the capacity to produce around 6,000 tonnes of green hydrogen per year during phase 1. Further expansion phases could increase this to more than 60,000 tonnes in the medium term, which could result in over 10m tonnes of greenhouse gas emissions avoided over the life of the project.

Thierbach is in Saxony and its prospective customers are said to include large-scale energy and industrial consumers such as the chemical industry and commercial air and road transport operators.

Along with the £5m investment in the developer, HH2E, HGEN will invest a further £2.4m in the Thierbach Project, alongside other institutional investors.

Future investments

HGEN’s advisers say that they have significant pipeline of over £500m of potential investments. The potential capex requirement to fund Gen2 Energy and HH2E’s investment programme alone runs to in excess of £300m.

The £500m figure encompasses 34 potential deals of which 10 – worth about £100m – were live at the time of the publication of HGEN’s annual results.

Valuation

The entire private portfolio is revalued on a quarterly basis. This is reviewed and approved by the AIFM and board before publication. KPMG audits the valuation annually.

The investment adviser values the private hydrogen assets according to IPEV guidelines, which incorporate the use of:

- discounted cash flows (DCF);

- multiples (of revenue or earnings, for example);

- industry valuation benchmarks; and

- available market prices.

For the private hydrogen assets, the appropriate valuation methodology varies, depending on the availability of suitable data. DCF may be used where appropriate forecasts are available. The valuation process will also consider any recent transactions, where appropriate.

For those assets where a trading multiples approach can be taken, the methodology factors in revenue, earnings or net assets as appropriate. This approach can only be applied to companies that are consistently generating profits or, failing that, revenues. The valuation approach uses the last 12 months of earnings or revenue.

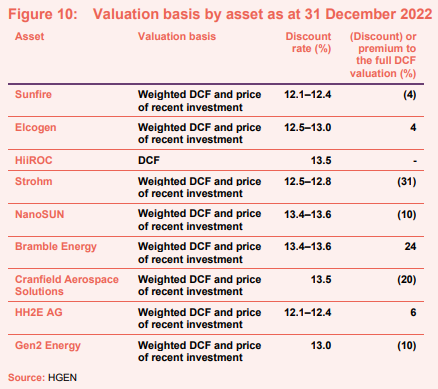

HGEN discloses the valuation basis for each asset, which we reproduce in Figure 10. In the final column, a negative percentage denotes that the weighted valuation is at a discount to the full DCF valuation; whilst a positive percentage denotes that the weighted valuation is at a premium to the full DCF valuation. The weighted average discount rate at the end of December 2022 was 12.9%, up from 12.5% at the end of December 2021.

Based on the portfolio as at the end of December 2022, the directors estimate that a 1% increase in the discount rate would reduce the NAV by £6.515m and a 1% fall would add £7.815m to the NAV.

The advisers say that the year-end valuation implies a forward revenue multiple for 2024 of about 5.5x and say that this is about 40% lower than listed multiples. Looking further out – to 2026 – the gap narrows to 20%.

Performance

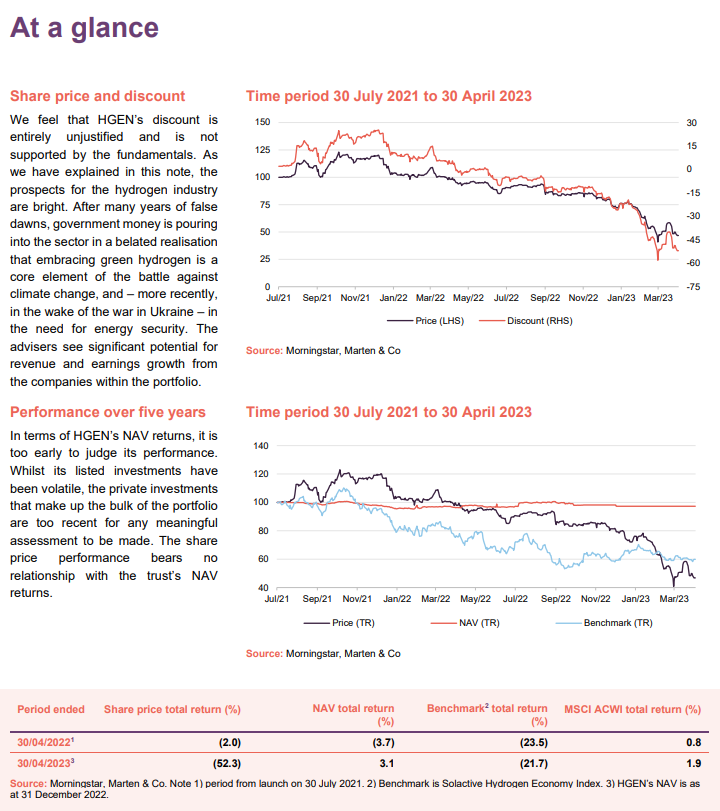

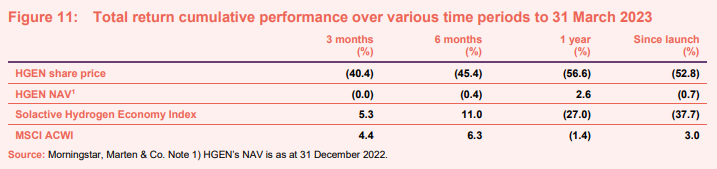

In terms of HGEN’s NAV returns, it is really too early to judge its performance. Whilst its listed investments have been volatile, the private investments that make up the bulk of the portfolio are too recent for any meaningful assessment to be made. Nevertheless, within this section we have included some information drawn from HGEN’s recent annual results.

The share price performance bears no relationship with the trust’s NAV returns. We discuss the emergence of the discount on page 21.

HGEN’s NAV increased by 1.6% to 97.31p over the course of 2022, driven by increases to valuations of some of HGEN’s private hydrogen assets, which added 3.94p to the NAV, offset by expenses of 2.15p per share.

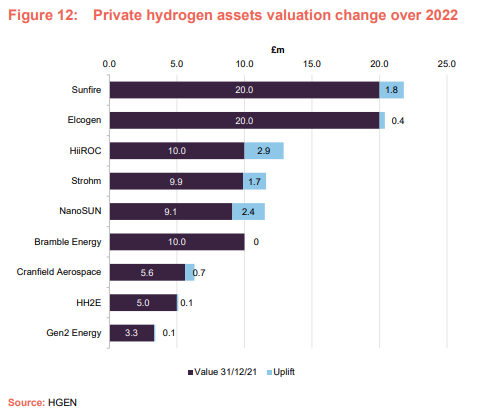

HGEN has broken down the portfolio’s contributions to the NAV uplift by company.

Offsetting these uplifts was a net £4.5m fall in the valuation of HGEN’s listed assets.

The emission of 42,716 tonnes of CO2e was avoided thanks to HGEN’s investment activities.

Dividend

HGEN would pay any dividends necessary to maintain its investment trust status, but the nature of the companies that it is backing is likely to mean that returns come from capital growth rather than income for now. For the year ended 31 December 2022, HGEN generated a negative revenue return per share of 1.14p and the balance on its revenue reserve at the end of that period was negative £2.21m.

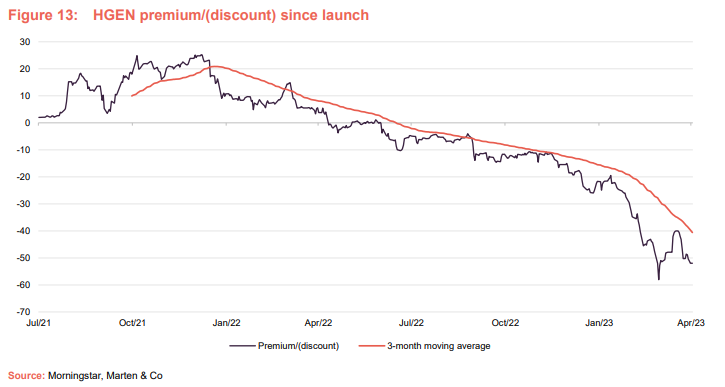

Premium/(discount)

Around 12 months ago, HGEN’s shares moved from trading at a premium to trading at a discount and the trend has been of discount widening since, with a marked lurch downwards in the share price in the first quarter of 2023.

We feel that HGEN’s discount is entirely unjustified and is not supported by the fundamentals. As we have explained in this note, the prospects for the hydrogen industry are bright. After many years of false dawns, government money is pouring into the sector in a belated realisation that embracing green hydrogen is a core element of the battle against climate change, and – more recently, in the wake of the war in Ukraine – in the need for energy security. The advisers see significant potential for revenue and earnings growth from the companies within the portfolio.

We feel that HGEN’s de-rating has been driven by share price falls for listed companies in the hydrogen sector. Many of these have been stock-specific – a run of profit warnings from ITM Power linked to problems scaling its business (in contrast to Sunfire), for example. Much of it, though, represents a dramatic shift in sentiment away from growing but unprofitable companies, which has been triggered by rising interest rates.

Each year, the directors ask shareholders for permission to issue up to 10% of HGEN’s issued share capital and repurchase up to 14.99%.

Fees and costs

The investment adviser charges a fee of 1.5% on the NAV of any private hydrogen assets owned by HGEN, whether these are held directly or indirectly through the limited partnership.

Initially, HGEN’s listed hydrogen assets formed part of its liquidity reserve (cash on hand) – used to fund private investments as they became available. For the first 18 months of HGEN’s life (to 30 January 2023) the adviser agreed to cap its fees on the liquidity reserve at 0.5%.

Going forward, the investment adviser is entitled to an advisory fee of 1.0% of the net asset value of the listed hydrogen assets up to £100m, and 0.8% on the remainder of the value of any listed assets.

The adviser can also earn a performance fee – in the form of carried interest partner fees – under the limited partnership agreement. This is calculated as 15% of any realised cash profits on private hydrogen assets above an 8% per annum compound return. 20% of any carried interest partner fees would be used to buy HGEN shares in the market and these shares would then be subject to a 12-month lock up.

The adviser’s fees are calculated quarterly and payable in advance.

The other expenses for the year in excess of £100,000 were: administration and secretarial fees of £193,000, directors’ fees of £173,000, audit fees (to KPMG) of £118,000, PR and marketing fees of £212,000, and capital transaction costs of £219,000. That latter expense was buoyed by the volume of new investments during the period.

HGEN’s ongoing charges ratio for the year ended 31 December 2022 was 2.51%, up from 2.06% for the prior period.

Capital structure

HGEN has 128,819,999 ordinary shares in issue and no other classes of share capital. No ordinary shares are held in treasury.

At launch, HGEN raised £107.35m gross with the issue of shares at 100p per share. In April 2022, it then raised a net £21m of additional capital through the issue of 21,469,999 shares at 100p per share. This share issue was supported by both existing and new investors.

HGEN’s accounting year end is 31 December, and its next AGM is being held on 23 May 2023.

HGEN has an unlimited life. However, at the AGM in 2026 and every fifth AGM thereafter, shareholders will have an opportunity to vote on the continuation of the company.

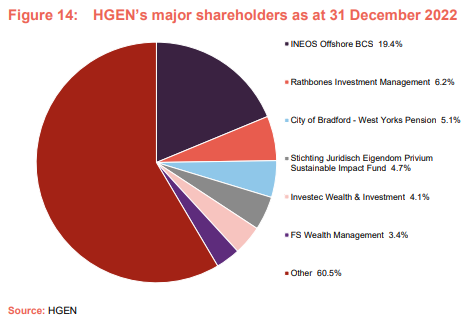

Major shareholders

INEOS Energy’s initial stake was subject to a 12-month lock-up. It is entitled to nominate a non-executive director to HGEN’s board. INEOS Energy also has a right of first refusal to acquire up to 100% of co-investment opportunities offered to HGEN in connection with the private hydrogen assets held by the limited partnership. The INEOS Energy stake was passed across to INEOS Offshore BCS Limited on 31 October 2022.

Gearing

HGEN currently has no debt outstanding. However, it is able to take on debt for general working capital purposes or to finance investments and/or acquisitions, provided that at the time of drawing down (or acquiring) any debt (including limited recourse debt), total debt does not exceed 25% of the prevailing GAV. That limit applies on a look-through basis across the wider HGEN group as well as the top company, but excludes debt within companies that HGEN does not control (although the board will monitor debt exposures and will determine the appropriate course of action). Debt will be utilised in the project financing for the HH2E and Gen2 projects mentioned on p16-17.

Advisory team

Dr JJ Traynor

JJ has extensive experience in energy, capital markets, project management, and M&A. He has held a series of senior energy and banking sector positions, including executive vice president at Royal Dutch Shell, where he led investor relations and established the company’s ESG programme; managing director at Deutsche Bank, where he was the number one ranked analyst in European and global oil & gas; and geologist at BP, in the North Sea, West Africa and Asia Pacific. He has a Geology BSc from Imperial College and a PhD from Cambridge University. He attended the INSEAD Advanced Management Programme and is a fellow of the Geological Society of London.

Richard Hulf

Richard is a fund manager with a corporate finance and engineering background. Richard has 30 years of experience in the utilities and energy sectors and is a chartered engineer, originally from Babcock Power and latterly Exxon. In addition, his financial experience spans stock broking, corporate finance and fund management with Henderson Crosthwaite, Ernst & Young and Artemis Investment Management, where he invested into renewables companies. He has an MSc in Petroleum Engineering from Imperial College.

At 31 December 2022, JJ Traynor and Richard Hulf each held 100,000 shares in HGEN.

The advisory board

Giles Morland

Giles has over 35 years’ investment banking, asset management, private banking and private wealth management experience.

He was a former managing partner at Mirabaud et Cie, chairman and chief executive of Mirabaud Securities, vice chairman (formerly chairman) and executive director of Mirabaud Asset Management and is ACA qualified.

Andy Arnold

Andy is an experienced commercial and business development manager with 35 years’ experience in the international energy industry. Former positions include commercial director and business development manager at Schlumberger and Ophir Energy, BG, BHP, ExxonMobil, and a secondment to the UK Government’s DTI (now BEIS).

Andy qualified as an accountant with KPMG, and is currently a director of Northbrook Energy Advisory Ltd.

Katriona Edlmann

Katriona is the Chancellor’s Fellow in Energy at Edinburgh University and is a world-leading academic in low carbon geo-energy and the geological storage of CO2 and hydrogen.

The advisers say that Katriona brings a science-based perspective to investment decisions.

Mazen Masri

Mazen has decades of operational experience in the energy industry in the Middle East and Africa and possesses pioneering entrepreneurial skills, and an expansive network of relationships. He owns and manages an energy services group operating since the 1970s in over 20 countries. The EDG Group has partnered over the years with the likes of Schlumberger, Baker Hughes and GE as well as BP, ENI, Bechtel, Technip and others.

Mazen is focused on transitioning to more sustainable and greener energy through developing and introducing proven technologies worldwide. The advisers say that he brings extensive international operational and technical knowledge to the HGEN team.

Caroline Cook

Caroline has 30 years of experience in energy and sustainable investing and is currently a sustainability specialist at a large UK asset manager.

Caroline was a former NED and audit chair in the small-cap E&P sector, managing director at Deutsche Bank as No.1 rated analyst, and initiator of cross-sector energy transition research. She also has significant consulting experience across the global energy sector.

Board

HGEN’s board is composed of four directors, all of whom are independent and do not sit together on other boards.

The board’s policy is that all directors, including the chairman, shall normally serve no longer than nine years on the board. The board may deviate from the policy if it feels there are circumstances where service beyond nine years would be in the best interests of the company and its shareholders.

Roger Bell, who was a director and INEOS Energy’s nominated director from 20 May 2021, stepped down from the board on 4 May 2022 and was replaced by David Bucknall. David is not a member of the board committees – audit and risk, remuneration, management engagement, or nomination, and valuation – but may attend these by invitation. David recuses himself from any decision relating to a transaction by the company or any member of the group with INEOS Energy or any of its associates.

Caroline Cook, who was a director from 20 May 2021, stepped down from the board on 7 April 2022 but remains on the advisory board (see above).

Simon Hogan (chairman of the board and nomination committee)

Simon has significant capital markets, legal and management experience. He was previously a managing director of Morgan Stanley and chief operating officer across their commodities, fixed income and equity divisions. He has held multiple board positions and was a member of the FCA Practitioners committee.

Afkenel Schipstra (chairman of the audit and risk committee and the valuation committee)

Afkenel has over 19 years’ experience in energy in Europe and Sub-Sahara Africa. She was previously SVP of hydrogen business development for the Netherlands at ENGIE, and held senior positions at Gasunie, Shell, and NAM.

Abigail Rotheroe (chairman of the management engagement committee and the remuneration committee)

Abigail has over 20 years of investment experience and was previously investment director at Snowball Impact Management, a sustainable and impact-focused asset manager. She was a director of Threadneedle Investment, following positions at HSBC Asset Management and Schroders and has experience of institutional and retail investment. Abigail is a non-executive director of Baillie Gifford Shin Nippon Plc and Templeton Emerging Markets Investment Trust Plc.

David Bucknall (non-executive director)

David is currently chief executive officer of the INEOS Energy group of companies and has been nominated as the board representative of INEOS Offshore BCS Limited. He brings a wealth of commercial experience through his role held at INEOS Energy.

Legal

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on HydrogenOne Capital Growth Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it, but in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.