Out in front

In both total net asset value (NAV) and share price return terms, Jupiter Emerging & Frontier Income (JEFI) has been the pacesetter within its peer group since the November 2020 vaccine announcements. Manager Ross Teverson and the team’s long-held view that stocks were priced more attractively outside of China has been paying off, led by its Taiwan-based holdings in particular.

JEFI’s bottom-up approach, which combines value and growth elements, has matched well with the shift away from growth stocks. A portfolio comprising predominantly of stocks with above-average dividend yields, the absence of reliance on China and India, and a mandate that allows investments into both emerging (EM) and frontier (FM) markets makes JEFI a unique proposition (see page 14). Despite its smaller size, it is trading at one of the tightest discounts within its peer group. A return to the pre-pandemic premium share price to NAV rating would allow JEFI to grow by raising capital and broaden its attraction to institutional investors.

Long-term capital and income growth

JEFI aims to generate capital growth and income over the long term, through investment predominantly in companies exposed directly or indirectly to emerging markets and frontier markets worldwide.

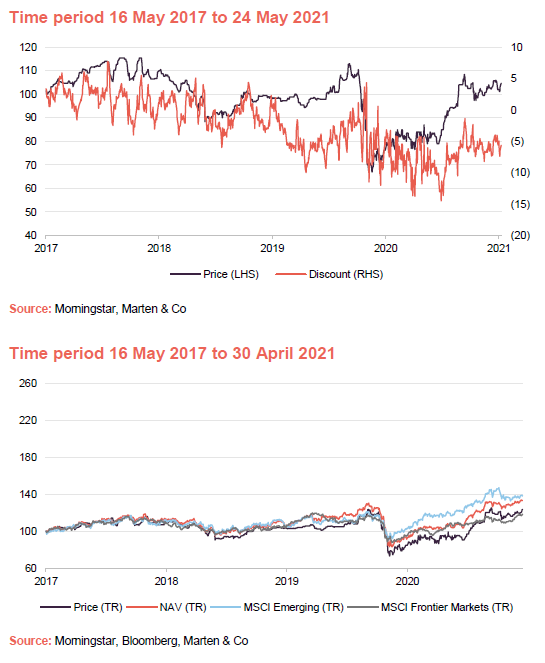

JEFI’s discount has narrowed since we last published, though it will need its shares to return to their pre-pandemic premium to NAV for it to grow by issuing new shares. There has been far less impact on the capacity of the portfolio holdings to pay dividends than we saw in the developed world over 2020.

JEFI’s relative performance has improved considerably since our last note in November 2020, with the subdued performance of China-based stocks (the key driver of the MSCI Emerging Markets Index) and a wider return to prominence for small-cap and value stocks working in its favour. As we discuss in the peer group section, JEFI’s strategy is distinct and there are potential catalysts in place for the recent relative outperformance to extend.

Focus shifting away from COVID and back to fundamentals

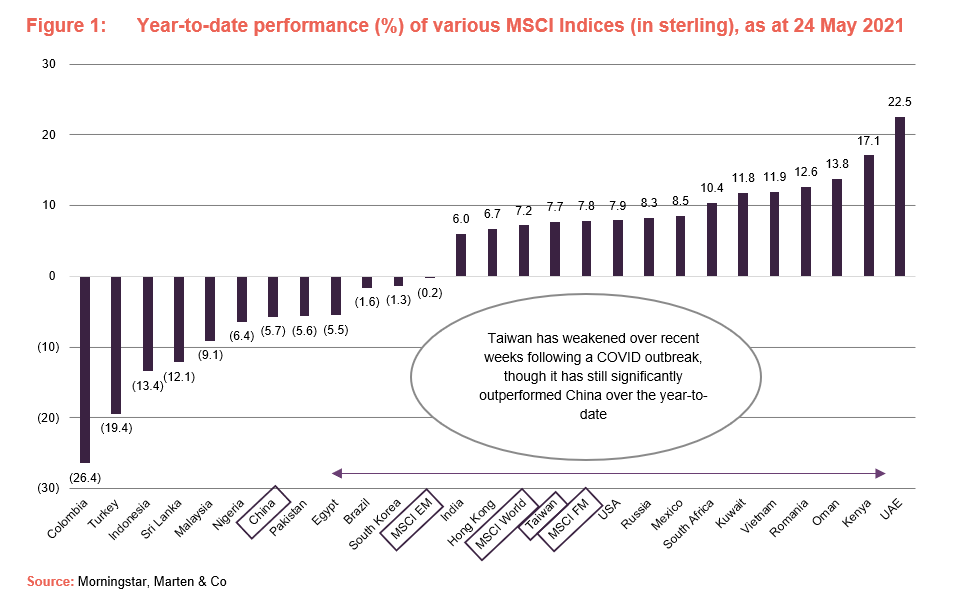

At times over 2020, it felt like China was carrying the baton for global emerging markets (it accounts for over 35% of the MSCI Emerging Markets Index), with its stock market well out in front as it completed a remarkable turnaround, having been the initial epicentre of the COVID-19 pandemic. As Figure 1 illustrates, it has been a different story so far this year, with China taking more of a backseat.

The November 2020 vaccine developments precipitated a shift towards value and small caps (market capitalisations below $2bn), which has worked to JEFI’s advantage. Ross continues to allocate a much lower proportion of JEFI’s portfolio to China (and indeed India), compared to many of its peer funds, as discussed in the performance section. JEFI’s stock-picking approach means country allocation is a by-product of its fundamental analysis of companies. This has naturally steered JEFI away from China and towards Taiwan in particular, which provides access to technology enablers (companies playing a critical role in the major technological changes taking place) at a discount to the those on the mainland.

More broadly, at the country level, Ross believes the market has been shifting its focus away from COVID-19 and back towards emphasising longer-term fundamentals. Given that many frontier markets have still yet to see their equity markets recover, despite quietly returning to normal levels of economic activity, there continues to be scope for a degree of catch-up (to emerging and developed markets) on a valuation basis especially. Sadly, some of the largest countries, notably India, continue to be severely impacted by the pandemic.

Financial inclusion theme remains undervalued

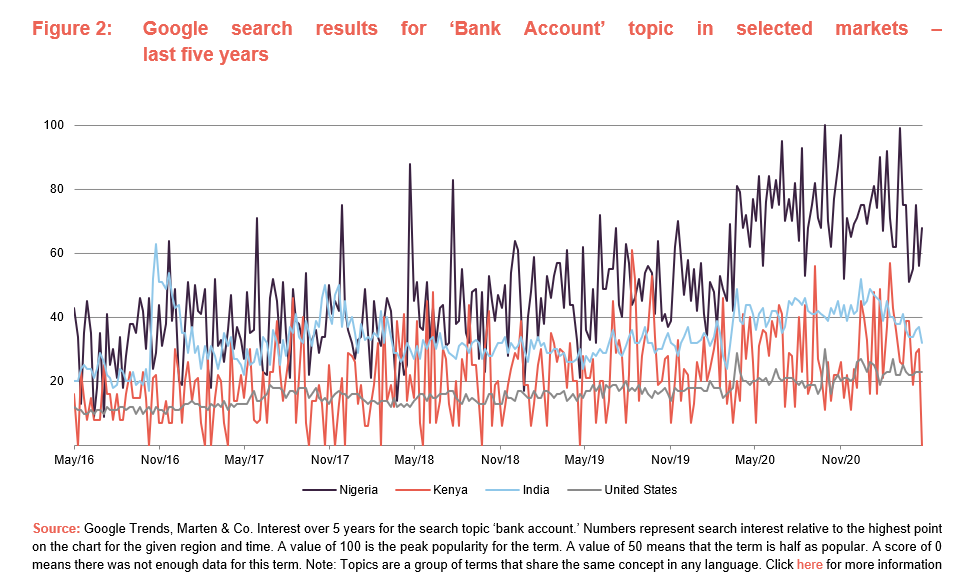

The financial inclusion structural change theme, described by Ross as the process of bringing the previously unbanked into the financial system and ultimately gaining access to basic financial products and services, is second only in its portfolio importance to the predominantly South Korea- and Taiwan-based holdings in tech-enabling companies like Mediatek and Chroma Ate (see the asset allocation and performance sections). Ross believes that opportunities in financial inclusion continue to be under-appreciated. He observes that JEFI holds several well-capitalised (the balance sheets are in good shape), high-profit-margin-generating and domestically dominant banking positions that continue to trade at significant discounts, and in cases below book value (accounting as opposed to market value) per share. Whilst fintech companies are typically described as ‘disrupters,’ Ross says that for the likes of Kenya and Nigeria, the incumbent financial companies are using fintech technologies to enhance their propositions.

Figure 2 compares the popularity of the ‘Bank Account’ search topic (‘topics’ are a group of terms that share the same concept in any language) in Nigeria, Kenya, India, and the US (the US is used as a broad control group for developed markets). Using this high-frequency data proxy, we can see a significant increase in search activity in Nigeria over the past 12 months. Nigeria’s leading banks, including JEFI-held Guaranty Trust Bank, are making a sustained push to develop products for the financially excluded (some 60m Nigerians remaining unbanked).

In addition to Guaranty Trust Bank, JEFI also has exposure to Kenya’s KCB bank (whose one-year share performance is shown in Figure 3), Pakistan’s UBL, Bank of Georgia, and Turkey-based AvivaSa (which provides private pension and life insurance products).

![]()

Asset allocation

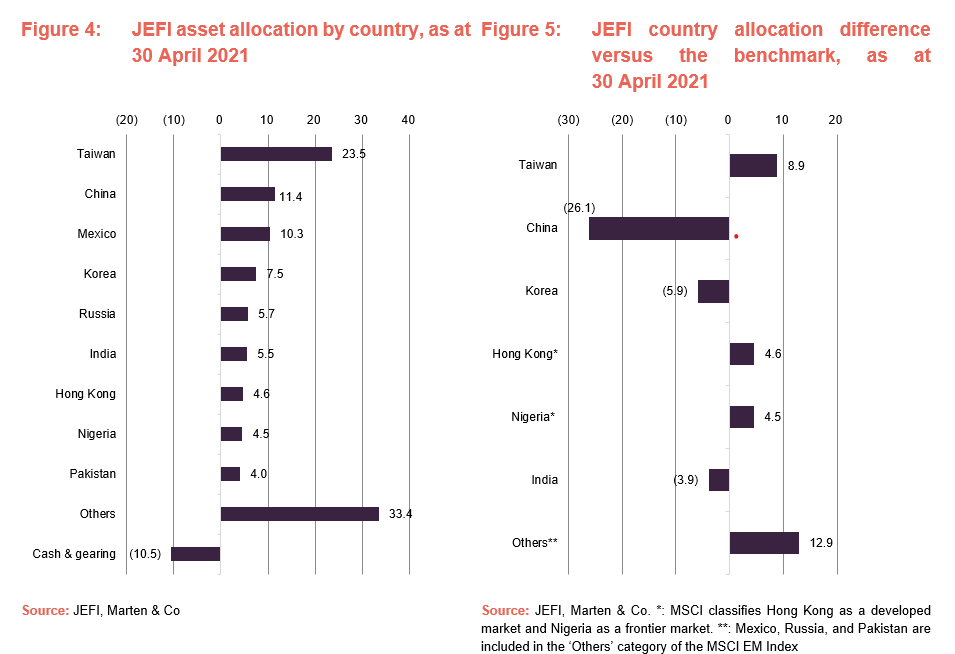

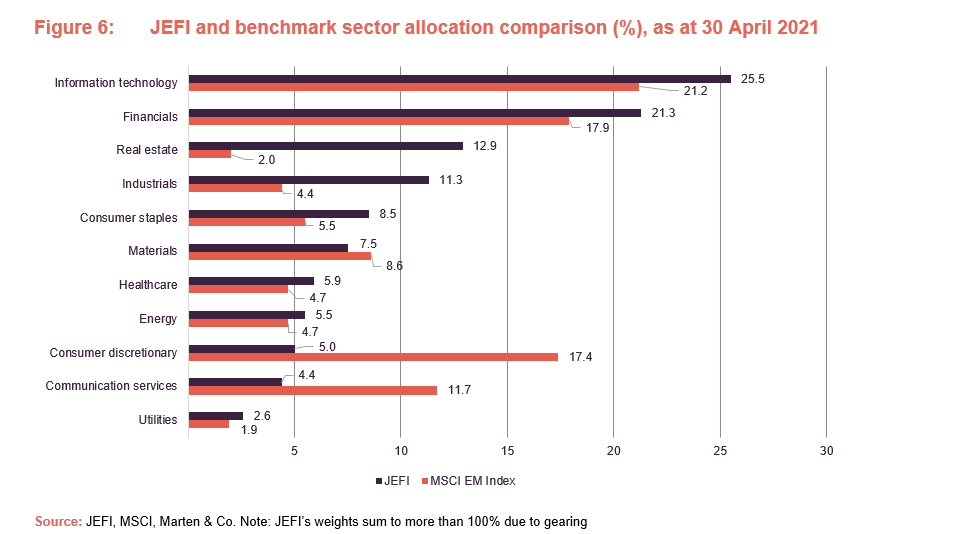

The stock-picking style favoured by JEFI’s manager means that the portfolio only loosely resembles the benchmark. As illustrated by Figure 5, this continues to be most clearly embodied by the fund’s much lower allocation to mainland China. The most recent (as at 30 April 2021) relative difference in weight was (26.1%). As at 30 April 2021, the relative difference between JEFI’s exposure and that of the benchmark was (26.1%). The decrease in the underweight from (32.6%), based on 31 October 2020 figures used in our last note, is mainly attributable to the subdued performance of Chinese stocks so far this year.

As a result of performance and portfolio activity by the manager, changes to the geographical make-up of the portfolio since we last published include:

- A 1.5% increase in Taiwan’s weight;

- a (1.7%) reduction in Hong Kong’s weight;

- a (1.2%) reduction in Nigeria’s weight; and

- Brazil moving from a 5.5% weight to no longer figuring in JEFI’s top 10 markets.

Particularly in technology, Taiwan is home to several companies that are well aligned with some of the structural change drivers Ross is looking for. Some of these holdings are not household names, yet they are integral to the global supply chains of companies such as Apple. Ross cites Mediatek as an example, noting that the company is a global market leader in handset chips and that its technology has significantly contributed to the decline in handset prices.

At 25.4% of the portfolio, technology is JEFI’s largest sector allocation – this is slightly higher than we last published (24.1%). Financials are also well represented, reflecting the manager’s views around financial inclusion, which we discussed on page 5. Elsewhere, real estate and industrials continue to be well represented, while the portfolio is much less aligned to the consumer discretionary and telecommunication sectors than the benchmark.

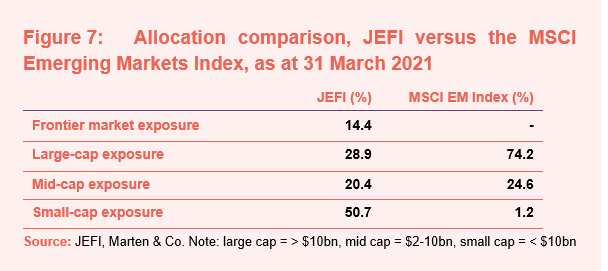

As well as providing exposure to many of the structural growth drivers discussed in this note, JEFI’s near 15% allocation to frontier markets serves as a useful diversifier. With so many asset classes increasingly moving in lockstep, the fact that stock markets in the likes of Kenya and Vietnam tend to be driven by country-specific forces is a point of distinction between JEFI and most of its peer group.

Top 10 holdings

Ross did not significantly increase trading in the portfolio over 2020, as he felt comfortable in the abilities of balance sheets of companies across the portfolio to withstand the initial impact. None of the financial sector holdings have had to raise equity capital (by issuing new shares), while around a third of the portfolio companies hold net cash (that is, after deducting their total liabilities) on their balance sheets. We also note that dividend payout ratios (dividend per share as a percentage of earnings per share) tend to be lower outside developed markets, which provide some additional headroom compared to situations where a much higher proportion of earnings are distributed as dividends.

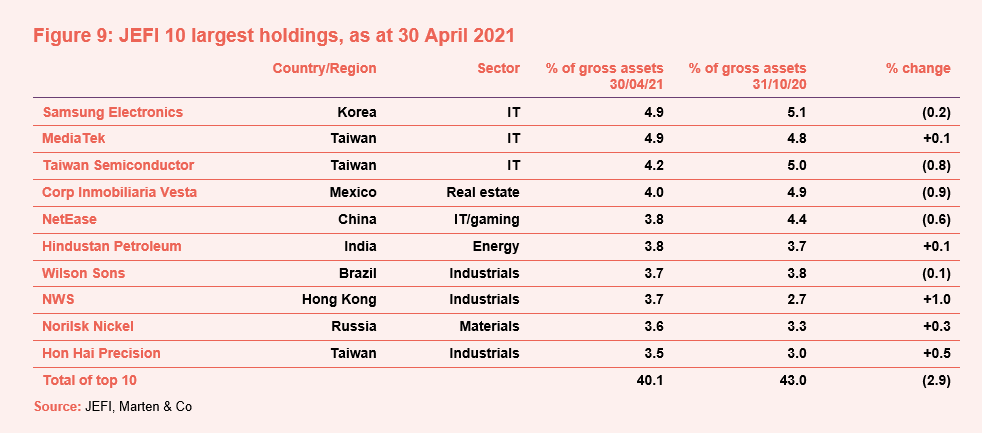

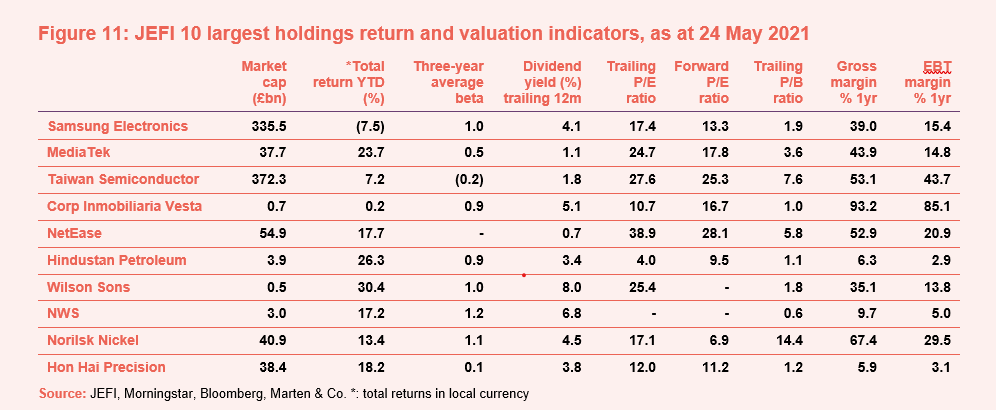

Compared to the 31 October 2020 figures used in our last note, there have been three changes to the line-up of top 10 holdings with Guaranty Trust Bank, KCB bank, and Chroma Ate (all three remain in the portfolio) replaced by NWS, Norilsk Nickel, and Hon Hai Precision. Whilst Guaranty Trust Bank and KCB bank do not figure in the top 10 this time around, the financial inclusion theme that they provide access to remains a key area of attraction for JEFI, as discussed earlier in the note.

MediaTek and Norilsk Nickel are covered in the attribution section below, while many of the remaining top 10 holdings have been discussed in earlier notes, which you can access through the previous publications section by clicking here.

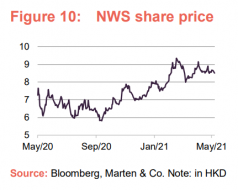

NWS, a Hong Kong-listed conglomerate with operations spanning toll roads to aircraft leasing is having a strong year, with its shares up 17.9%, as shown in Figure 10. The company is an example of how JEFI is able to augment its exposure to China through Hong Kong, where Ross notes that many companies trade at discounts to their peer group on the mainland.

Taiwan’s Hon Hai Precision is also having a good year and, similarly to NWS, its business is built around economies of scale, with much lower gross and operating margins than many of the other holdings in the top 10. Hon Hai is the largest assembler of iPhones for Apple, as well as being a major electronic components manufacturer and an emerging player in the contract manufacturing of electric vehicles.

Portfolio activity over the past year

Over the 12 months to 13 April 2021, Ross brought five new companies into the portfolio. They are AvivaSa (Turkish insurance company), Kunlun (Chinese gas distributor), Elan (Taiwanese semiconductor design company), Crédit Agricole Egypt (Egyptian retail and commercial bank), and Obour Land (Egyptian consumer staples). AvivaSa, Kunlun, and Crédit Agricole Egypt were profiled beginning on page 13 of our most recent annual overview note.

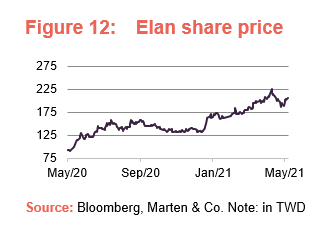

Elan Microelectronics

The manager looked to Taiwan once more in growing the technology stable with the addition of Elan Microelectronics (www.emc.com.tw). The company provides exposure to the integrated circuits (ICs) and microcontrollers industry, where it is involved in research, development, manufacturing, and sales processes. Its products include biometric solutions, microcontrollers, and pen & touch input solutions. The company is a key partner for companies such as Microsoft and Google in the development of touch-screen protocols and security standards. It is currently trading at a trailing 12-months price/earnings (P/E) multiple of 13.3x, which is in keeping with the relative value provided by many Taiwanese technology companies.

Obour Land

Egypt’s Obour Land (www.obourland.com) manufactures a range of popular dairy products, from milk to white cheeses. It is a well-established brand in the Middle East and North Africa region’s largest market for consumer staples, with Egypt’s population of around 100m providing opportunities across mass-market and premium channels. As with many listed consumer-focused companies operating in the region, Obour Land trades at a modest valuation, with its shares trading at a P/E multiple of 8.3x last year’s earnings and below sales per share (price/sales ratio of 0.9x).

Performance

JEFI’s relative performance against the benchmark MSCI Emerging Markets Index has improved significantly since our last note was published in November 2020. Given the benchmark’s over-35% weighting to China, a level JEFI is very unlikely to ever approach, significant deviations in relative performance are to be expected. Just as the relative strength of Chinese equities over 2020 weighed on JEFI’s relative returns, a subdued 2021-to-date has worked in the fund’s favour.

We argued in our November 2020 note that JEFI would benefit if valuations in some of the other well-positioned neighbouring Asian markets (like Taiwan, for example) were to move closer into line with China, with its bottom-up fundamentals-led approach well-suited to a shift away from growth stocks.

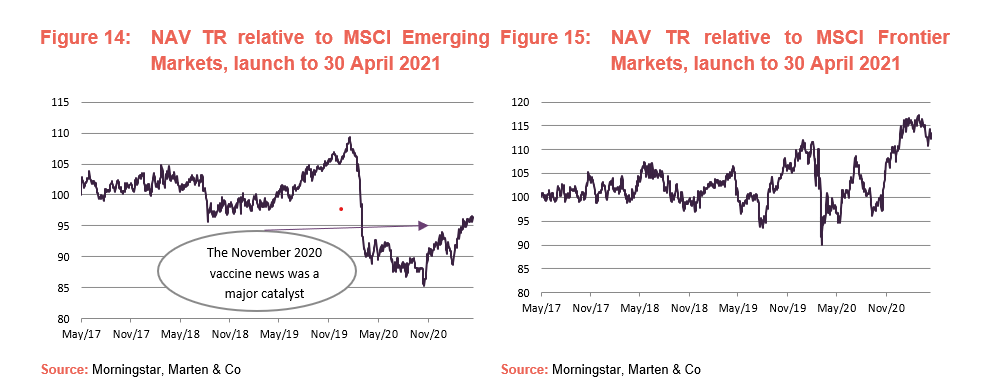

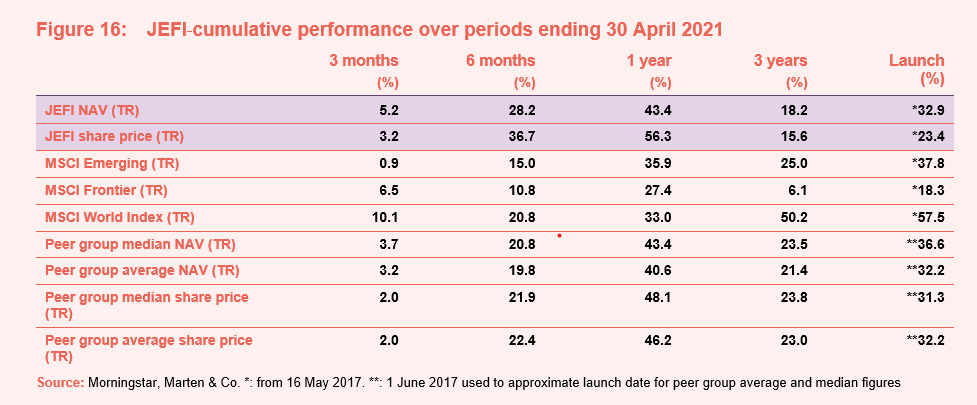

As illustrated by Figure 16, JEFI has performed very well over the past six months, with performance since the November 2020 early vaccine developments coming in well above its peer group and the MSCI World, Emerging, and Frontier comparative indices. Relatively low exposure to hard-hit countries, like Brazil and India, has also helped to steer relative performance, while the 15% allocation to frontier markets could provide a further catalyst for outperformance going forward, as more capital is allocated to the likes of Kenya, Nigeria, and Vietnam. JEFI’s performance against the MSCI Frontier Markets Index (shown in Figure 15) has been impressive of late as well.

We note that the peer group shown in Figure 16 includes all the funds in the AIC’s global emerging markets sector, with the exceptions of Africa Opportunity and Gulf Investment Fund, which are not global funds. We have also omitted Barings Emerging EMEA Opportunities from the table, on the basis that its broadened remit has only taken effect over recent months.

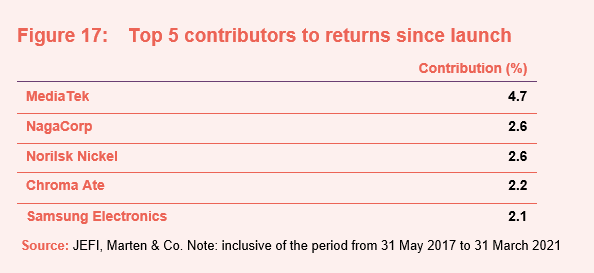

Performance attribution – positive contributions led by MediaTek

JEFI’s manager has provided a performance attribution breakdown since its launch on 15 May 2017, with the positive contributors illustrated by Figure 17.

MediaTek has been held since launch and has been going from strength to strength. In addition to cementing its position as the second-largest manufacturer of chipsets for mobile phones behind Qualcomm, it has been expanding its chipset business and is now well-entrenched into the supply chains of Amazon and Google. Ross notes that MediaTek has narrowed the technology gap with Qualcomm, with its new line of 5G chips contributing to what he believes will be a sustainable increase in gross margins. We note that the company continues to trade a discount to its US peer group.

NagaCorp, the Cambodia-based hotels and casino operator, had an exceptionally strong 2018 and 2019 in share price terms. Ross subsequently sold the position to create room for higher conviction ideas elsewhere. Since our last note, Ross has added to the position in Russia’s Norilsk Nickel. The company is the largest global producer of palladium and a major producer of nickel and copper, all of which are set to play an integral role in the clean energy transition.

Like Qualcomm, discussed above, Chroma Ate is another Taiwanese hardware enabler; it manufactures precision electronics testing components. Ross believes the company has strong pricing power, while noting that around 30% of its revenues are based around electric vehicles, with the company producing a lot of the testing equipment used.

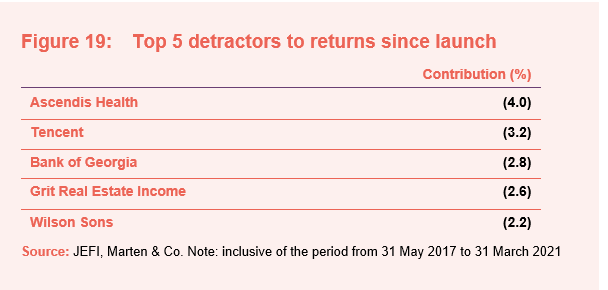

Detractors

The main detractors are illustrated in Figure 18 below. Ascendis Health is no longer part of the portfolio, while China’s Tencent has historically been a large part of the MSCI Emerging Markets benchmark. While it has performed very well over most of the past 18 months, as we have noted earlier, JEFI’s approach naturally steers it away from many of the richly valued Chinese technology companies. We note that Bank of Georgia, Grit Real Estate Income, and Wilson Sons remain in the portfolio, with the manager believing that the investment cases remain intact.

Peer group comparison – distinguishing traits coming to the fore

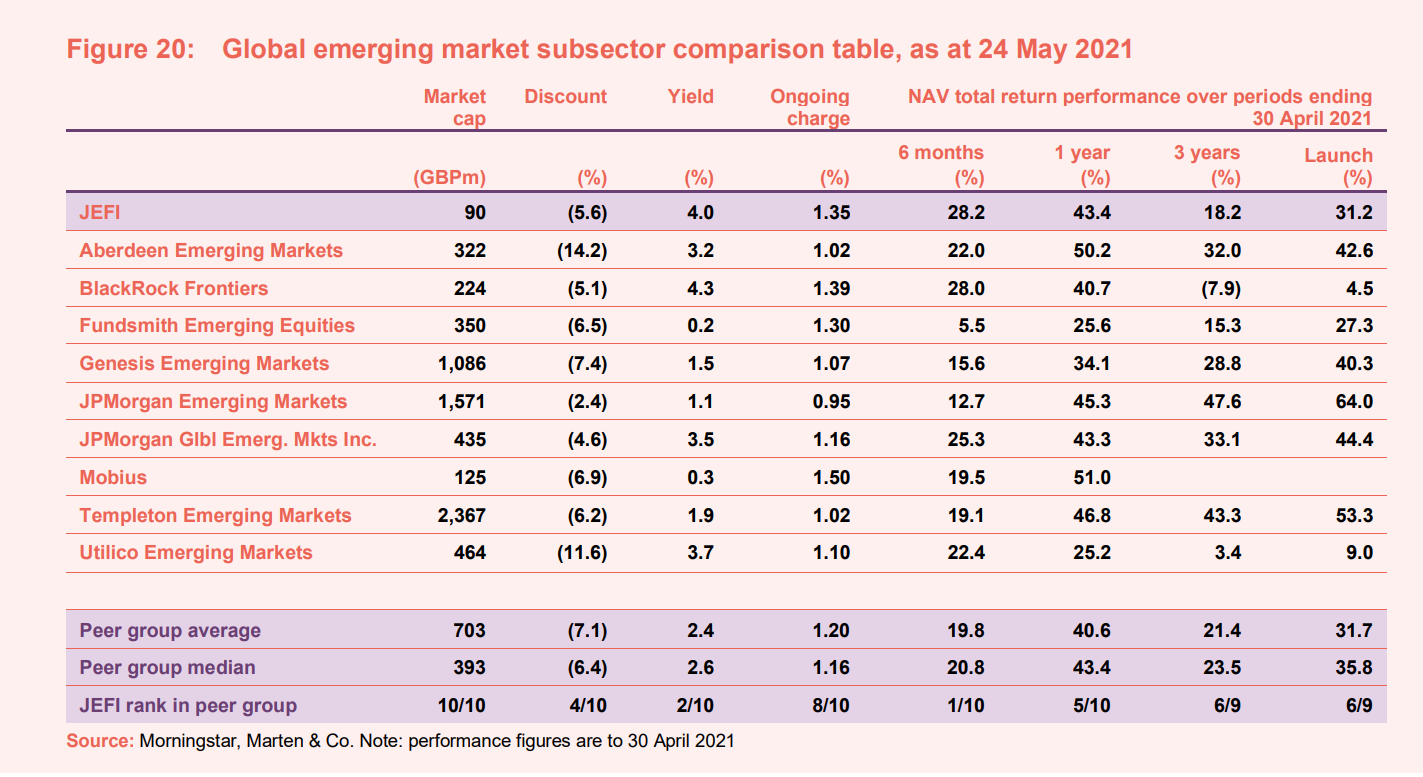

JEFI’s distinguishing traits include a portfolio approach that combines value and growth elements, the holding of companies with predominantly above-average dividend yields, a mandate that allows investments into both emerging market and frontier markets, and relatively low exposure to China and India compared to many of its peers. These traits have come to the fore recently when comparing JEFI to its peer group. Its excellent relative performance over recent months is mapped out in Figure 20.

The market’s recognition of this can be recognised by the fact that despite being the smallest fund by some distance, and the inevitable effect this has on ongoing charges when compared to much larger funds, JEFI was the fourth most expensive fund (at a discount of 5.6%), on a relative basis, as at 24 May 2021.

Relative performance has been helped by the challenges faced by Brazil and India so far this year and the tailing off in China’s stock market surge. Many of the funds listed in Figure 20, including Aberdeen Emerging Markets, JPMorgan Emerging Markets, and Templeton Emerging Markets, have much greater exposure to China. Where this is not the case, exposure to India is often high, as in the case of Fundsmith Emerging Equities, where India was 44.5% of the fund, as at 30 April 2021.

As we have previously noted, out of the subset of the AIC’s global emerging markets funds shown, only Mobius allocates to both emerging and frontier markets. However, the similarities largely end there. Mobius is also almost entirely growth-focused, with Brazil, China, and India accounting for close to 55% of its portfolio, as at 30 April 2021. By comparison, China and India combined were 16.9% of JEFI’s portfolio, and Brazil is no longer one of its 10 largest country allocations.

JPMorgan Global Emerging Markets Income (JEMI) is the only other fund to invest in a portfolio of largely above-average yielding companies. JEMI also counts Taiwan Semiconductor and Samsung amongst its largest holdings. However, JEMI does not invest in frontier markets, which – as we have discussed previously – appear to still be providing some deeply discounted opportunities, especially in financials.

JEFI and BlackRock Frontiers continue to be the highest-yielding funds, though BRFI is capital growth-focused and its frontier-only approach means it cannot hold companies in emerging markets such as Taiwan, a market that has performed very well for JEFI since its launch.

Dividend

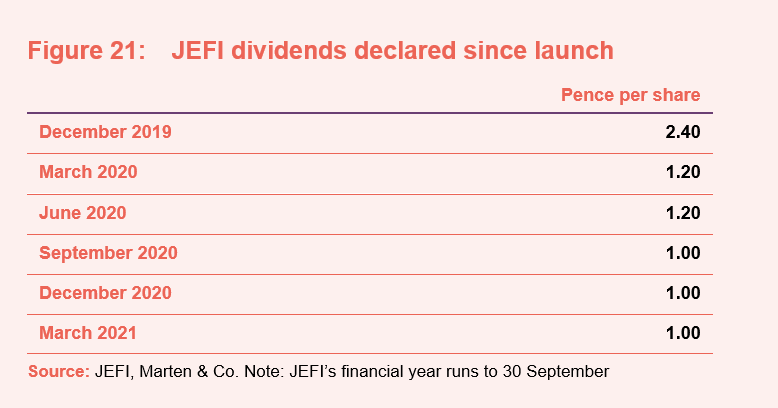

JEFI’s manager targets a dividend yield that is at least 20% higher than its benchmark’s. Four payments are made per year, in April, July, October, and January. At launch, JEFI said it would target a minimum annualised dividend of 4%. As of 27 May 2021, JEFI’s shares were yielding 3.9%.

For the financial year-end to 30 September 2020, the first interim dividend of 1.2p was paid on 17 April 2020. On 3 June 2020, JEFI declared a further interim dividend of 1.2p which was paid on 3 July 2020 – both distributions were fully covered by earnings.

The pandemic’s initial impact led to JEFI reducing its expectations for dividend income growth for the financial year, though as Ross points out, the early suspension of dividend payments by banks was the result of regulatory intervention. We note that Kenya’s KCB bank has returned to paying dividends. Ross adds that Bank of Georgia is expected to re-instate distributions over 2021 while in Pakistan, Indus Motors and United Bank have returned to a normal level of dividend payments.

Premium/(discount)

Over the year to 30 April 2021, JEFI’s shares moved within a discount range of 14.5% to 1.4%, with an average discount of 7.4%. As at 27 May 2021, JEFI was trading on a discount of 4.3%. JEFI’s discount has narrowed significantly since our last note and were the shares to move to a premium to NAV over the coming months, this would provide an opportunity to grow the fund by issuing shares.

JEFI’s board and manager remain keen to expand the trust, which would help improve liquidity in the shares and lower the ongoing charges ratio. The shares were valued at a premium to NAV in the period leading up to the pandemic, as Figure 22 illustrates.

We note that JEFI’s asset base (total assets of £95m, as at 30 April 2021) remains towards the lower end of the minimum size preferred by many asset managers, so it is likely to take on the opportunity to expand, particularly given the strong relative performance drivers outlined in the performance section.

JEFI operates a discount control mechanism using share buybacks and new issues of shares intending to ensure that, in normal market conditions, the price of its shares will closely track the underlying NAV. Since its formation in 2017, JEFI has issued 4m additional shares at a premium to NAV.

We also note that the fact JEFI provides an annual redemption facility at NAV. Readers interested in finding out more about this can refer to page 20 of our November 2020 annual overview note.

Fund profile

Launched in May 2017, JEFI invests in stocks that provide exposure to emerging and frontier markets (any country that is not classified as developed). The aim is to generate both capital growth and income over the long term, using an investment approach that is benchmark agnostic, unconstrained and focused on identifying positive change.

Investment manager

JEFI’s portfolio is managed by Ross Teverson, of Jupiter Asset Management (Jupiter), who subcontracts the job of managing the portfolio from the AIFM, Jupiter Unit Trust Managers Limited. Ross is now the sole manager of JEFI with the departure of Charles Sunnucks in June 2020, following Jupiter’s acquisition of Merian. The emerging markets team has approximately £1.1bn under management. The manager can also draw on the expertise of Jupiter’s wider pool of asset managers and analysts. Ross works closely with Matthew Pigott and Colin Croft, as well as the broader 8-person emerging markets equity team.

Ross Teverson

Ross has been managing an unconstrained emerging markets portfolio since 2012. He joined Jupiter in 2014 as head of strategy, Global Emerging Markets. Before joining Jupiter, Ross worked for 15 years at Standard Life Investments, where he managed a global emerging markets equity fund. Ross spent seven years in Standard Life Investments’s Hong Kong office, where he managed an Asian equity fund and was a director of the business. He is a graduate of Oxford University and is a CFA Charterholder

Previous publications

Readers interested in further information about JEFI may wish to read our earlier notes. You can read the notes by clicking on the links below:

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Jupiter Emerging & Frontier Income Trust.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.