Unfazed by market turmoil

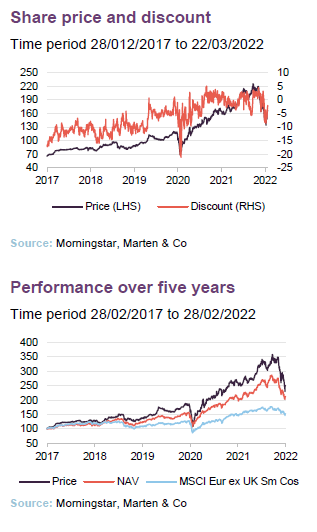

Montanaro European Smaller Companies (MTE) has built up an enviable track record by backing high-quality growing companies for the long-term. In recent months, fears of rate increases (in response to rising inflation) have triggered a sharp reversal of sentiment towards growth stocks. The Ukrainian war has made investors more risk averse, and some have sought safety in large cap stocks. MTE’s shares have moved from trading at a small premium to trading on a single-digit discount.

What we will not see in response to this situation is any change in the way in which MTE is managed. MTE has experienced many periods where low-quality stocks outperform or investors retreat to so-called defensive (usually low-growth) stocks. The manager may take advantage of the situation by adding to favoured stocks at attractive prices, but MTE will stick by its portfolio and wait for markets to come back to its way of thinking. The current discount may represent a buying opportunity.

Continental European smaller companies

MTE aims to achieve capital growth by investing principally in Continental European quoted smaller companies. The benchmark index is the MSCI Europe ex UK Small Cap Index (in sterling terms).

Fund profile

Montanaro European Smaller Companies Trust (MTE) aims to achieve capital growth by investing principally in smaller, quoted, Continental European companies (those within the European Union, Norway and Switzerland) but is not restricted from investing in smaller companies quoted on other European stock exchanges. The benchmark index is the MSCI Europe ex UK Small Cap Index (in sterling terms).

The original company dates back to 1981, but Montanaro Asset Management Limited (MAML) took on the management of the trust in September 2006 and the European small-cap investment approach dates from then.

The manager

MAML was established in 1991 and is chaired and 95% owned by Charles Montanaro and family. Head of investments Mark Rogers owns 5%. However, the wider team has options over about half of the equity. The CEO is Cédric Durant des Aulnois, the lead manager on MTE is George Cooke (who is also head of fund management at MAML), and Stefan Fischerfeier acts as George’s back-up. Charles, Mark and George are all members of the investment committee, which also includes Alex Magni (see page 17 for more detail on the team).

They are supported by what MAML believes is the largest and most experienced team in Europe, specialising in researching and investing in quoted small and mid-cap companies. The investment team now numbers 15, as MAML has continued to invest in its business. The team is multi-lingual and multi-national. All but two of the fund managers also have research responsibilities.

In addition to MTE, the team manages a range of funds focused on UK and European equities, the Montanaro Better World Fund (an open-ended fund investing in small and mid-cap companies supporting the UN Sustainable Development Goals), and two recently-launched global equity funds. MAML has about £5bn of assets under management.

Sharp reversal of sentiment after good run

George says that 2021 was a good year for MTE; in his words – the stars aligned. The emergence of new variants of COVID unnerved some investors and the market favoured the solid growing businesses that are typical of MTE’s portfolio over cyclical stocks and structurally-challenged but lowly-valued opportunities.

However, as the year progressed, investors became increasingly worried about inflation. Expectations grew that central banks would raise interest rates in response. The ECB was a laggard in this regard but appeared to capitulate early in February 2022. Higher rates mean higher discount rates applied to valuations of growth stocks. This triggered a sharp rotation from ‘growth’ to ‘value’.

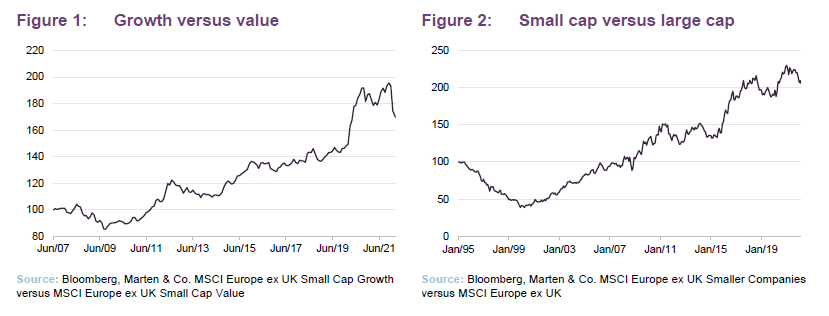

The outbreak of war has exacerbated shortages of some commodities and threatens to prolong the period of high inflation. However, fears are growing of a simultaneous recession – in other words stagflation. Smaller companies, which – as Figure 2 shows – have a good long-term track record of outperformance of large caps, and growth stocks appear to have been hit particularly badly.

Part of MTE’s investment approach, which we detail below, is to back companies for the long term, and avoid being distracted by gyrations in markets and economics, consequently turnover remains low. The easing of COVID restrictions is making an important difference in one respect, however; the team expects to do a lot more company visits now, as it has done historically.

George observes that MTE’s high-quality portfolio is well-placed in the event of a slower economy. MTE does not own any loss-making companies, and 44% of portfolio companies have net cash on the balance sheet. The approach favours businesses operating in areas of structural growth, which should be less affected, and perhaps sometimes benefit from a recessionary environment.

The portfolio should also be resilient to the effects of inflation. A core indicator of the quality of a company is its ability to pass on price increases.

Investment approach and process

MAML avoids trying to time macroeconomic shifts, preferring to focus on the long term.

It wants to invest in:

- simple businesses that it can understand;

- niche businesses in growth markets (non-cyclical companies, growing organically rather than businesses that tend to focus on acquisitions);

- market leaders (strong, defensible market positions and pricing power);

- companies with high operating margins and high returns on capital (barriers to entry/a sustainable competitive advantage);

- profitable companies trading at sensible valuations; and

- good management that it trusts (aligned to shareholders and demonstrating sound ESG practices).

This could be summed up as investing in high-quality businesses at sensible prices. Furthermore, MAML believes it is important to:

- do the work yourself (rather than relying on brokers);

- be passionate; and

- learn from mistakes (humility goes a long way).

In addition, MAML believes that it is easier to add value through stock selection for a small-cap portfolio, especially given the relative paucity of research available on these companies. MAML observes that some large companies are covered by 50 or more brokers, while many European smaller companies have little or no coverage. Firm evidence for the success of this approach is provided in Figure 2.

Sifting through the universe

The constituents for MTE’s portfolio are drawn from a universe of about 4,000 companies listed in Europe. The focus is on those with a market cap between €100m and €5bn (about 2,300) and, as described below, unprofitable companies are excluded which reduces the pool to about 1,700 stocks. The benchmark index currently includes stocks with market caps of up to about €7bn.

MTE is a true stock-picking portfolio; index-weightings play no part in forming its portfolio construction. MAML has always generated its own investment ideas rather than relying on external analysts. There are many good reasons for this, but it is also fortunate as the availability and quality of external analysis – which MAML believes has been on a declining trend for some time – was exacerbated by MiFID II. This gives MAML a competitive edge, which is sharpened by the strength and depth of its research team.

The size of the team allows for some theoretical research, and lateral creative thought is encouraged. MAML is an entrepreneurial boutique with a flat structure that allows for quick decision-making and avoids the politics that bog down more bureaucratic large asset managers. MAML does not encourage the development of ‘star’ fund managers, but is focused on staff retention, including the granting of staff options over MAML equity. MAML’s ‘back office’ functions are carried out in-house rather than being outsourced (as they are in many smaller investment management boutiques).

Research responsibilities are distributed amongst the team on a sector, global basis. Emphasis is placed on being well-prepared for meetings, which is possible as the research team is well-resourced. MAML’s analysts can then set the agenda, challenge management and get the information that they need. Site visits are encouraged (another perk of having a large team is that it is not desk-bound).

On average, each analyst will seek to identify 20 stocks within their sector coverage worthy of closer scrutiny. These will form the pool from which portfolio constituents are drawn. The first part of the process is to eliminate poor-quality companies. These stocks are identified by applying a quantitative screen to the wider universe. Loss-making companies, those with poor cash flow and highly indebted businesses are rejected. Stocks that fit structural growth themes that the team has identified may be prioritised. Each company within the universe is assigned a quality rating.

The analysts then build a financial model and conduct a proprietary checklist for each stock. They also check whether a stock meets MAML’s ESG criteria (see below). Then the idea is put before MAML’s investment committee, who challenge assumptions and ask for more information if they feel this is warranted. Stocks that pass these quality thresholds may then go on to an approved list of approximately 270 companies. No fund manager can buy a company that is not on the approved list.

Various valuation tools are considered (primarily discounted cash flows) but include P/E, free cash flow yield, dividend yield and relative to peers and the team operates with a time horizon of five to 10 years. The ideal investment should provide a margin of safety in excess of 25% over its intrinsic value. Analysts will also look at risk factors. Analysts will then assign a recommendation to each stock. These will be presented to the whole team at weekly meetings and the fund managers will then decide which stocks make it into portfolios. Once a stock makes it into a portfolio, it will usually remain there for many years.

Portfolio construction

MTE’s investment policy is more fully described in its annual report. It only invests in listed securities and MAML says that unquoted companies are not eligible for consideration.

Some other rules apply:

- MTE does not hedge its currency exposure;

- MAML will hold no more than 10% of the voting rights in any company (across all funds managed by MAML); and

- no more than 10%, in aggregate, of the value of its total assets at the time of investment will be invested in other investment trusts or investment companies admitted to the Official List of the UK Listing Authority. Currently, MTE has no holdings in other investment trusts, nor does it expect to ever do so.

Typically, the target weighting for a position will be between 1% and 3.5%, depending on both the strength of conviction that the manager has in the stock, and its liquidity. The total number of holdings is typically around 50. There is no obligation to sell a company if its market cap exceeds €5bn, but these will be gradually recycled into lower market cap companies. The manager will ensure that a single position does not exceed 7.5% of the portfolio.

ESG analysis

MAML’s focus on quality is supported by its commitment to ESG principles, which have been ingrained within its investment approach for many years. It believes that there is a clear correlation between how well a business fares on ESG grounds and the value it creates for its shareholders.

Christian Albuisson chairs an internal sustainability committee of seven, which meets quarterly and oversees MAML’s efforts in this area. The team includes a dedicated ESG and impact specialist, Kate Hewitt. MAML also has its own handbook, policies and checklists. It votes the shares it controls, and it engages with companies. MAML expects the companies that it invests in to improve their ESG awareness and it monitors their progress.

Some sectors are excluded from portfolios on ESG or ethical grounds. MAML portfolios will not contain tobacco companies; companies manufacturing weapons, facilitating gambling or manufacturing alcohol; companies engaged in oil-, coal- and gas-related E&P; companies involved with pornography; companies making high interest-rate loans; or companies engaged in animal testing unless it is required by law. Corporate governance checks include an assessment of a company’s remuneration policy.

MAML’s attention to ESG issues extends to its own business. Following an extensive evaluation process, it was made a Certified B Corporation in June 2019 (more information is available at bcorporation.net). Early in 2021, MAML joined the Net zero asset managers initiative (more information at netzeroassetmanagers.org), supporting the goal of net zero greenhouse gas emissions by 2050 or sooner. MAML is a member of the GFANZ taskforce (see gfanzero.com) and sits on the real economy transition workstream group.

Sell discipline

Stocks exit the portfolio for a variety of reasons – for example, when they become significantly overvalued, if they become too big, or due to takeovers.

Furthermore, stocks may leave the portfolio if the analysts identify unfavourable changes in the fundamentals of the business or an unfavourable management change.

Stocks will also be sold if they no longer pass MAML’s quality threshold, or if a new opportunity comes along that offers better prospects.

Asset allocation

There were 58 holdings in the portfolio at the end of February 2022.

Net gearing is low – zero at the year-end (following the issue of some shares just ahead of the month-end), and just 2.9% at the end of February. This was a reflection of a lack of attractively priced investment opportunities rather than any call on the macroeconomic picture.

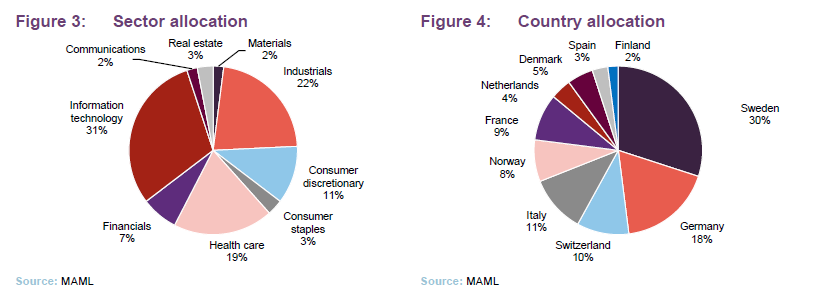

Geographic and sector allocations are determined by stock selection, but MTE has had a long-term overweight exposure to healthcare and technology companies relative to its benchmark.

Notably, MTE has negligible exposure to materials and energy – two sectors that have risen strongly since Russia invaded Ukraine – and to cyclical financials, which have been rising in anticipation of higher interest rates.

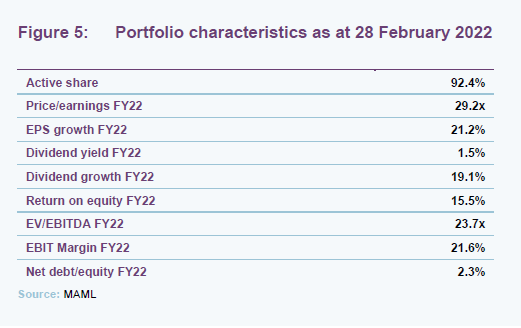

As Figure 5 shows, MTE’s portfolio has a high active share, 92.4% at the end of February 2022. Portfolio companies tend to trade on higher valuation multiples but offer faster revenue, earnings and dividend growth than the average stock. MTE’s portfolio companies also tend to have robust balance sheets, higher returns on equity (helped by the portfolio’s bias away from highly capital-intensive businesses) and higher margins.

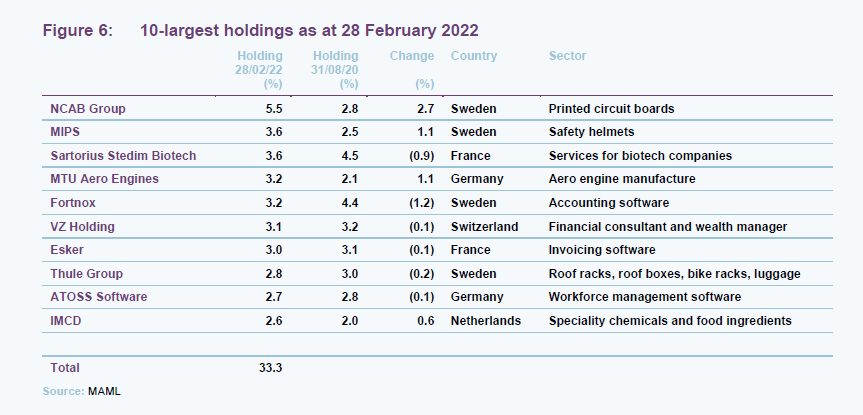

10-largest holdings

Evidence, if it were needed, of MAML’s long-term approach to investment is that since we last published on MTE, using portfolio data as at 31 August 2020, just three stocks – Nemetschek, Tecan and Hypoport – have dropped out of the list of the 10-largest holdings to be replaced by MIPS, IMCD and MTU Aero Engines that are also longstanding positions in the trust. Many of these stocks were discussed in previous notes.

Nemetschek

Nemetschek (nemetschek.com) is a stock that has been exited on valuation grounds. The manager also felt that the company’s main competitor was beginning to open up a technological lead over the company. Nemetschek would need a lot of investment to catch up and combine its point solutions into a unified suite.

Hypoport

Hypoport (hypoport.com) is a technology company operating in the credit, insurance and real estate sectors. The position was trimmed in March 2022, as its relative valuation became less attractive, but the stock is still held within MTE’s portfolio.

MIPS

MIPS (mipscorp.com) was discussed in our last note. The company makes inserts for helmets that help absorb some of the impact of accidents on the brain. The 2021 calendar year was a good one for the business, with organic sales growth of 72%, a near doubling of operating profit and earnings per share, and MIPS solutions implemented in 883 helmet models (up from 729 a year earlier). The company is building on a strong presence in sport and motorcycle helmets, with a push into safety helmets.

IMCD

Speciality chemicals and food ingredients business IMCD (imcdgroup.com) saw its share price rise by almost 90% over the course of 2021. The company delivered a 63% increase in earnings per share over the year, helped by a number of bolt-on acquisitions and a recovery in demand as customers benefited from the easing of COVID restrictions.

NCAB

NCAB (ncabgroup.com/en/investors) has become the largest holding within the portfolio on the back of strong share price performance. MAML first started building a position in the stock for MTE in March 2019. At the time, MAML envisaged that the share price would at least double. In April 2020 the company raised money via a placing of shares and MTE supported this.

NCAB’s focus is on printed circuit boards (PCBs). MAML feels that the company has made some good acquisitions, cementing its market-leading position. There has been a significant rise in demand for PCBs, but supply has been constrained. Most PCBs are sourced from China. NCAB leverages its buying power by amalgamating orders on behalf of customers. It oversees everything from design, prototyping, and production to quality control. Clients value the product as it has a low error rate – helped by NCAB being close to its customers. George feels that the valuation is still not excessive.

NCAB generated 39% organic growth in revenue (in US dollar terms) for 2021 over the prior year, and, including the effect of acquisitions, a 93% increase in the size of its order book.

NCAB halted all deliveries of PCBs to Russia on 28 February 2022. The company suggests that this will take about 5% off its EBITDA (based on 2021 numbers).

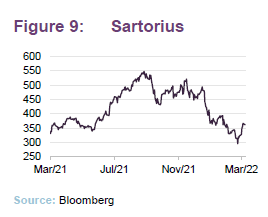

Sartorius Stedim

Sartorius (sartorius.com/en) makes equipment needed to produce biologics and biosimilars, such as vaccines and monoclonal antibodies. The position was trimmed in July 2020 but has been maintained since then. The company was a beneficiary of COVID in that it supplied equipment and services to over 200 companies that were developing vaccines. Its sales and profits numbers for 2021 were very good, therefore, but the breakdown published by the company suggests that COVID was far from the only factor working in its favour. Sales growth for the year was 51% and pandemic-related effects were 18 percentage points of that. Similarly, the order intake grew by 54%, of which pandemic-related orders accounted for 13 percentage points.

Vitrolife

Vitrolife (vitrolife.com) is a stock that MTE has held for some time. It made a strong positive contribution to MTE’s returns over 2021. It makes products and supplies services that support the IVF process. Demand for IVF is rising, and the success rate is increasing. Vitrolife’s products are consumables and are only a small part of the overall cost, but quality of the product is paramount.

The company has augmented its product offering by addressing the need to check on the progress of fertilised eggs within incubators on a regular basis. Vitrolife can create a time-lapse film by positioning a camera over the incubator and taking pictures at regular intervals. This saves a great deal of time and is much more efficient.

Vitrolife delivered sales growth of 35% over 2021 (30% organic sales growth), as the IVF industry recovered from the effects of COVID.

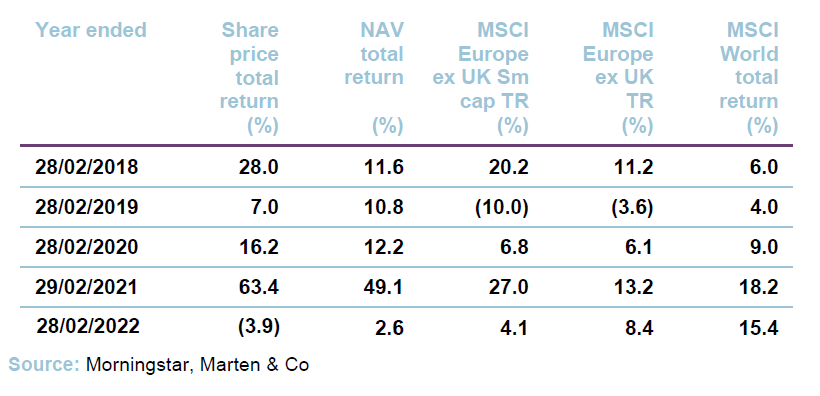

Performance

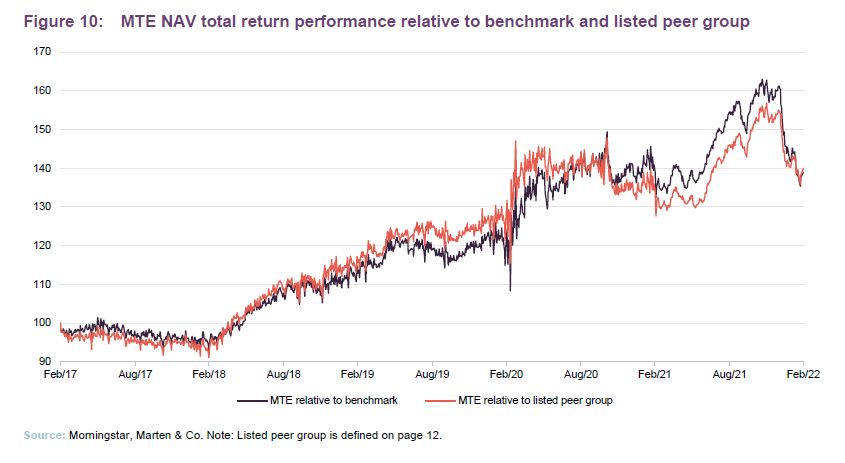

Notwithstanding the recent pull-back in its NAV and share price, MTE has delivered strong absolute and relative performance over the past five years (and before that). The resilience of most portfolio companies in the face of COVID-related lockdowns and the associated acceleration of many structural growth trends to which the portfolio is exposed were drivers of outperformance. The cyclical recovery as the vaccines took effect provided some headwind from November 2020. However, on average the portfolio continued to generate good growth in revenue and profits.

The recent pull-back in valuations of growth companies comes as investors have become concerned with inflation and the prospect of higher interest rates. Russia’s invasion of Ukraine has served to exacerbate and prolong the inflation problem, unnerve investors and raise the threat of stagflation. We would echo George’s comments on page 4 – operationally, MTE’s companies ought to hold up relatively well in these scenarios.

Peer groups

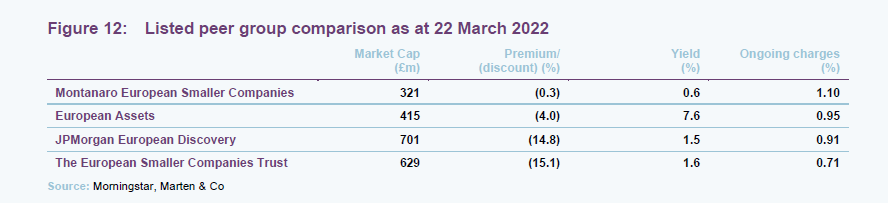

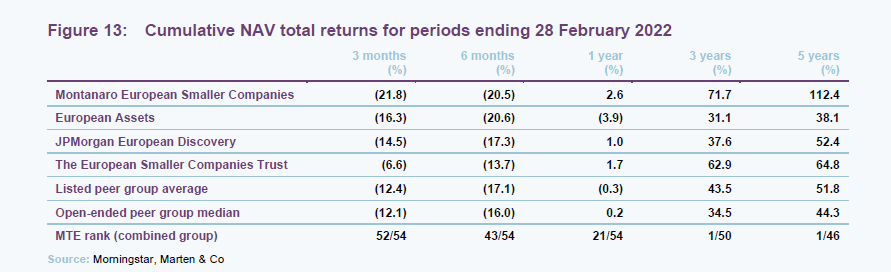

For the purposes of this note, we have compared MTE with the other trusts in the AIC’s European smaller companies sector. Although a respectable size, MTE is the smallest of these. It also has the lowest yield, reflecting the focus on growth companies. MTE’s ongoing charges ratio is in line with funds of an equivalent size. Even after the recent share price fall, MTE trades on the narrowest discount, which is most likely a reflection of its superior performance record.

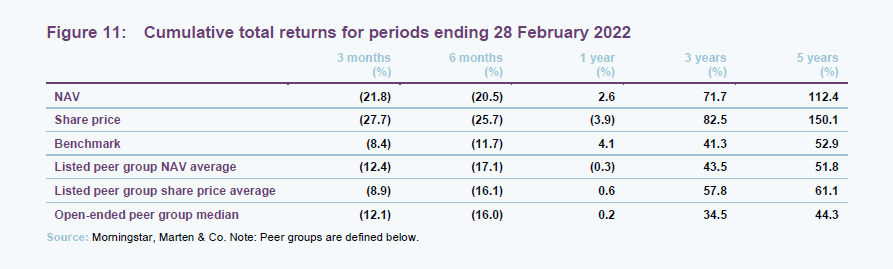

In Figure 13 below, we have also included data from MTE’s open-ended peers – a group of 50 funds available for sale in the UK and European Union. MTE beats the peer group averages over longer-term time periods and, if we combine both peer groups, MTE is the best-performing fund over three and five years.

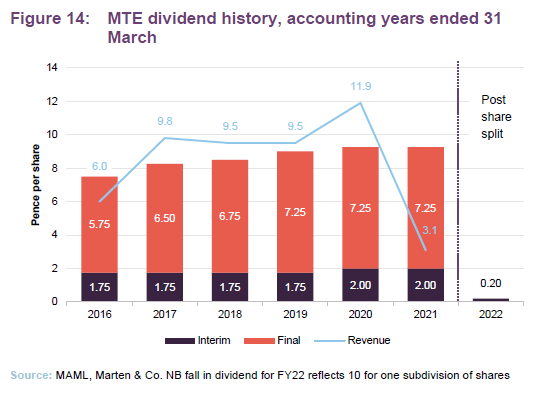

Dividend

MTE’s primary aim is to deliver capital growth to its shareholders, and its dividend yield is modest, 0.6% as at 22 March 2022. However, over the long term, growth in dividends of the companies in which it invests has allowed MTE to grow its dividend while also building a substantial revenue reserve. In the face of a COVID-19 related reduction in revenue, the board opted to dip into that reserve in the accounting year ended 31 March 2021. The reserve stood at £3.2m at the end of March 2021 (March 2020 £4.3m), equivalent to 1.7p per share.

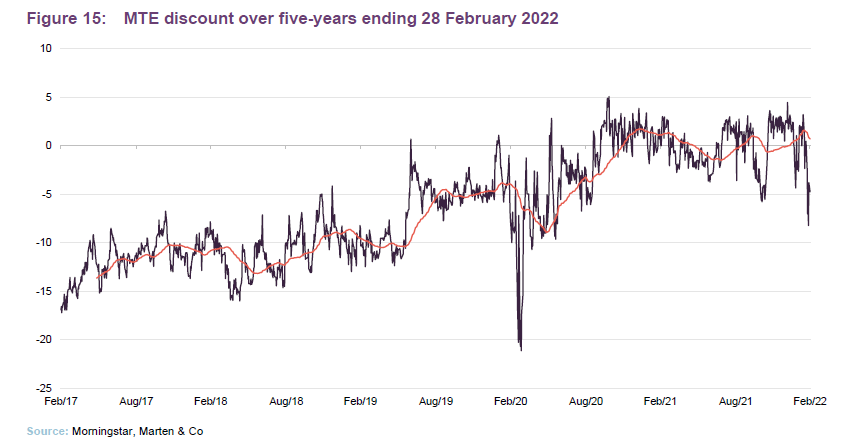

Premium/(discount)

Over the 12 months to the end of February 2022, MTE’s shares traded within a range of an 8.2% discount to a 4.4% premium and an average discount of 0.1%. At 22 March 2022, the shares were trading at a discount of 0.3%.

MTE’s strong long-term performance helped drive down the discount and move the shares to trade on a premium to asset value. However, the sharp swing in sentiment against growth stocks and heightened uncertainty about the impact of the war in Ukraine have contributed to a widening of the discount in recent weeks.

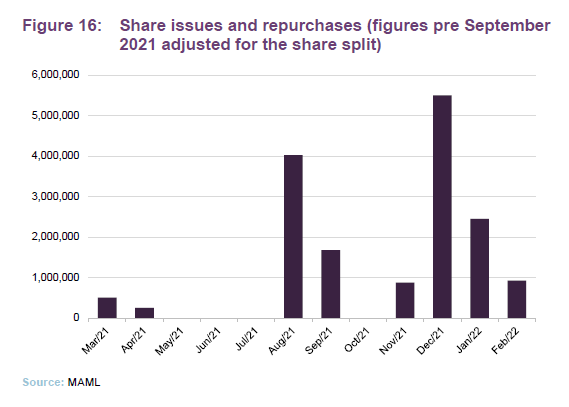

MTE has powers to issue and buyback shares, which it renews regularly at the AGM. Shares repurchased can be held in treasury and may be reissued. The board has said that these would only be reissued at a higher absolute price than the weighted average purchase price of the shares in treasury, and at a premium to NAV at the time of reissue or at a discount, provided this discount was lower than the weighted average discount at the time the shares were repurchased.

The net effect of this should be that purchasing the shares and reissuing them again is profitable for ongoing shareholders.

The board has stated that it will consider a buyback of shares where the discount of the share price to the NAV per share is greater than 10% for a sustained period of time and is significantly wider than the average for similar trusts. The board will take into consideration the effect of the buyback on the liquidity of the company’s shares.

In addition, the board encourages the manager to market the company to new investors.

Fees and costs

MAML is the company’s investment manager and AIFM. It is entitled to receive a management fee of 0.9% of the first £500m of MTE’s market capitalisation and 0.75% of the balance up to £750m and then 0.65% on any amount above £750m, payable monthly in arrears. Charging the fee on market capitalisation incentivises the manager to keep the company’s discount narrow. The tiered structure of the fee (introduced with effect from 1 April 2021) will help to lower the trust’s ongoing charges ratio, in time.

MAML is also entitled to a fee of £50,000 a year for acting as the AIFM. There is no performance fee. The management contract can be terminated by either side on six months’ notice. MTE charges 35% of the management fee against revenue and the balance against capital. The same methodology is applied to the accounting treatment for interest on MTE’s borrowings.

Link Company Matters Limited provides company secretarial services and Link Alternative Fund Administrators provides general administrative services. Equiniti Limited acts as Registrar and The Bank of New York Mellon (International) Limited as the company’s Depositary and Custodian. The company’s auditor is Ernst & Young.

The company’s ongoing charges ratio for the year ended 31 March 2021 was 1.2%, unchanged from the previous year, but the estimate at the half-year mark was 1.1%, reflecting the growth of the trust.

Capital structure and life

MTE has 189,427,600 ordinary shares in issue and no other classes of share capital. No shares are held in treasury. The company has an unlimited life.

Following shareholder approval, MTE split its shares on 14 September 2021 such that shareholders received 10 new ordinary shares in exchange for each existing ordinary share that they held.

MTE’s accounting year end is 31 March. Annual accounts are published around the end of June/beginning of July and the AGM is usually held in August or September.

Gearing

The board has set a maximum limit on borrowing, net of cash, of 30% of shareholders’ funds at the time of borrowing. The board, in discussion with the manager, regularly reviews the company’s gearing strategy and approves the arrangement of any gearing facility. The board believes that the ability to use gearing offers a strong competitive advantage over alternative open-ended investment funds. Therefore, it strongly encourages the active use of gearing by the manager.

MTE has a €10m secured loan maturing on 13 September 2023 that carries a fixed rate of interest of 1.33%, and a €15m revolving credit facility until 13 September 2023, both provided by ING Bank NV. Drawdowns from the revolving credit facility are charged at a margin over the relevant EURIBOR rate.

At the end of January 2022, MTE had net gearing of 2.4%.

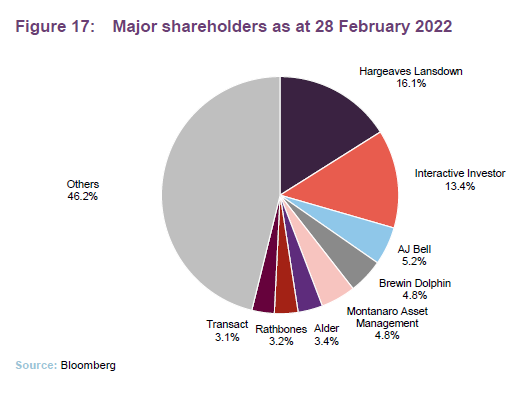

Major shareholders

Management team

George Cooke

George joined MAML in July 2010. He graduated from the University of Nottingham in 2005 with an undergraduate degree in Management Studies. He spent a further year of study there, at the end of which he was awarded a Masters (with Distinction) in Corporate Strategy & Governance. Immediately following this, he joined the graduate scheme at Aon Benfield (formerly Aon Re). Having completed this scheme, George settled as an analyst within the ReSolutions department, where he specialised in assisting with the capital and runoff issues of insurance and reinsurance companies. During his time at the company, George received a Diploma in Insurance. He is also a CFA Charterholder.

Stefan Fischerfeier

Stefan joined MAML in 2007. He holds a B.A. in Business Administration from the University of Cooperative Education in Mannheim (1995) as well as a Diplom-Kaufmann (MBA equivalent) from the University of Mainz (1998). He graduated from the London Business School with an MSc in Finance (2006). After graduating from University of Mainz, Stefan spent more than six years at Accenture in Germany, Switzerland, France, and the UK as a management consultant for European banks and asset managers. He then worked as an analyst at Nordwind Capital, a Munich based private equity company, analysing the automotive industry, and as an investment consultant for a property fund in Romania assessing real estate investment opportunities in Eastern Europe.

Board

The board consists of three directors, all of whom are independent of the manager and who do not sit together on other boards. Each director offers himself or herself up for re-election at each AGM.

Richard Curling

Richard was appointed to the board in 2015 and became chairman in 2018. He has over 30 years’ experience as a fund manager and is currently an investment director at Jupiter Fund Management Plc. He also has extensive experience of investment trusts. Richard is also chairman of the nominations committee.

Gordon Neilly

Gordon was, until the end of August 2020, chief of staff at Standard Life Aberdeen, prior to which he was global head of strategy at Aberdeen Standard Investments and was responsible for developing the group’s strategy and overseeing its implementation as well as overseeing all corporate activity for the Group and its closed end fund business. He joined Aberdeen in 2016 from Cantor Fitzgerald, where he held the position of joint CEO. Gordon is currently a non-executive director of Personal Assets Trust Plc.

Caroline Roxburgh

Caroline is a Chartered Accountant with over 30 years’ experience in finance and audit across a number of industries and sectors, and was formerly a partner at PricewaterhouseCoopers LLP until her retirement in 2016. She chairs the audit committee and is the senior independent director. Caroline also holds a number of other board positions, including a non-executive directorship of the Edinburgh Worldwide Investment Trust Plc.

Previous notes

Readers interested in further information about MTE may wish to read our other notes. Click the links in the table or visit the QuotedData website.

The legal bit

This marketing communication has been prepared for Montanaro European Smaller Companies Investment Trust Plc by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and, if you are not a professional investor, or in any other way are prohibited or restricted from receiving this information, you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.