Since we last published in January of this year, Pacific Horizon (PHI) has continued with its trend of exceptional outperformance of both its Asia Pacific peer group (where it is comfortably the top-performing trust) and the various indices that it benchmarks itself against.

PHI, with its strong focus on growth, benefitted from a high allocation to technology stocks in the aftermath of the pandemic. However, more recently, the trust has benefitted from timely decisions to reduce its high exposure to China, prior to the various regulatory clampdowns seen this year, reallocating the proceeds mostly to India, a market that has performed strongly year to date.

Reflecting this, PHI continues to trade at a decent premium to net asset value (NAV) and has been issuing a significant amount of stock. Despite this incredible performance, PHI’s manager continues to see strong growth potential for the stocks in PHI’s portfolio and is genuinely enthused about the prospects for these companies.

Focused on Asia ex Japan growth stocks

PHI invests in the Asia-Pacific region (excluding Japan) and in the Indian subcontinent in order to achieve capital growth. The company is prepared to move freely between the markets of the region as opportunities for growth vary. The portfolio will normally consist mostly of quoted securities, although it may hold up to 15% of total assets in unlisted investment opportunities, measured at the time of initial investment.

At a glance

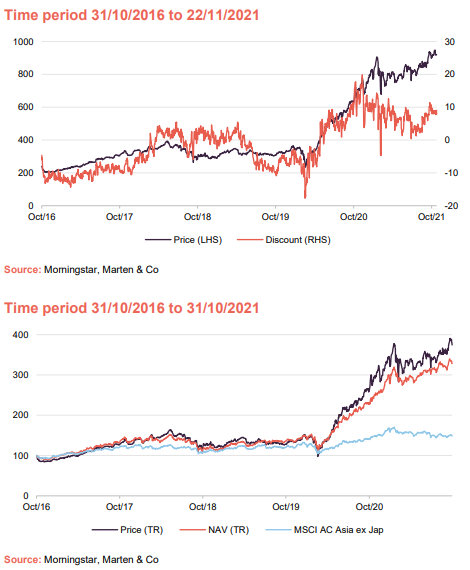

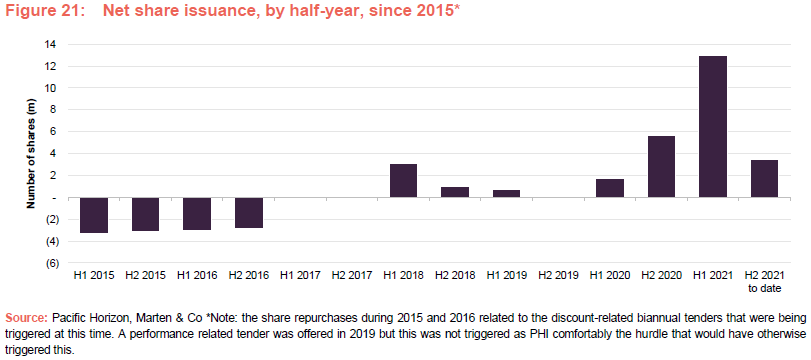

The primary driver of PHI’s premium and the strong demand for its stock is its performance record in recent years. This includes a trend of exceptional outperformance of its Asia Pacific peer group (see pages 21 to 24 for more detail of this in the peer group analysis). The premium has been particularly pronounced since the beginning of June 2020, which has allowed PHI to issue a significant number of shares, particularly during the first half of this year (see Figure 21 on Page 26).

PHI’s performance has seen a marked improvement during the last four years. This initially occurred as PHI successfully rejigged its portfolio in 2018 and PHI has found itself in a performance sweet spot since the COVID-related market collapse of March 2020. This trend of strong outperformance has continued since we last published in January 2021, aided by a timely decision by the manager to slash PHI’s exposure to China.

Fund profile

Pacific Horizon (PHI) is an Asia ex Japan investment trust that specialises in investing in growth companies. Baillie Gifford & Co (Baillie Gifford) has been appointed to manage PHI’s portfolio on behalf of Baillie Gifford & Co Limited, the trust’s alternative investment fund manager. Baillie Gifford has managed PHI since 1992. Baillie Gifford is a long-term growth investor and it believes that there is a significant opportunity to outperform markets over the long term using this approach.

Roderick Snell, who is the lead fund manager for Baillie Gifford’s Asia ex Japan strategies, has day-to-day responsibility for the management of PHI’s portfolio. Roderick had been the deputy manager of the trust’s portfolio since 2013, working alongside Ewan Markson-Brown since the latter’s appointment in March 2014. On 10 June 2021, it was announced that Roderick had become the lead manager following Ewan’s decision to leave Baillie Gifford.

PHI’s board says that Roderick was the obvious choice for lead manager as he has not only co-managed the £3.5bn Baillie Gifford Pacific Fund open-end investment company (OEIC) since 2010, which Ewan also co-managed from 2014, but has attended all of PHI’s board meetings, and has been involved in all portfolio discussions and decisions, since becoming deputy portfolio manager eight years ago.

Roderick has a degree in Medical Biology from Edinburgh University. He has been at Baillie Gifford since 2006 and in addition to managing the Baillie Gifford Pacific Fund since 2010, he is a co-manager on the Baillie Gifford China Growth Trust and co-manager of the emerging markets leading companies strategy.

About the manager

Baillie Gifford has 122 investors/analysts based in its Edinburgh office, with a further three in the US and five in China. It is structured as a partnership and encourages a collegiate approach to managing money, although it allows its portfolio managers the freedom to have the final say about their portfolios. It managed or advised on about US$346.2bn as at the end of September 2021, of which £67.9bn was invested in Asia Pacific equities. PHI and the Baillie Gifford Pacific Fund (its open-ended equivalent) have combined total assets of roughly £4.3bn.

Roderick says that his natural inclination is to take a ‘top down’ macroeconomic view and that considerations of the themes driving economies and industries are always in the back of his mind. However, he thinks that you only really get to see the big picture by looking ‘bottom-up’ (looking first at the attractions of individual stocks). This is very much a stock-picking fund and the portfolio bears very little resemblance to the fund’s MSCI All Country Asia ex Japan Index comparative index (the active share of PHI’s portfolio at the end of October 2021 was 93%).

Roderick spends most of his time in meeting companies and undertaking stock-specific research. He emphasises that the process and philosophy that is used to manage PHI has been the same for the last 30 years.

Market roundup – Asia, remains a relative bright spot

2020 was, without question, a challenging year for financial markets as the impact of the COVID-19 virus was felt around the globe, although the Asia Pacific region fared relatively well. With its experience of similar pandemics, the region was relatively successful at implementing controls to restrict the spread of the virus. Furthermore, as we have discussed in our previous notes, the Asia Pacific ex-Japan region offers long-term structural growth opportunities, and benefitted as investors have refocused their sights on growth opportunities.

Moving into 2021, the Chinese market has suffered as the authorities have clamped down on sectors such as technology, education and housing. In comparison, India – which had a number of hiccups in getting its vaccination programme going – has been a relative bright spot as the government has got a better grip on its handling of the virus, allowing its economy to remain more open.

Manager’s view

The manager’s long-term arguments for investing in growth companies in emerging Asia remain broadly unchanged, and we recommend that readers see our previous notes for more discussion. As we said above, whilst the manager is cognisant of macroeconomic issues and takes long-term structural themes into consideration, the portfolio is very much managed bottom-up. A key summary is as follows:

- China and the broader Asia Pacific ex Japan region offer very strong growth prospects. PHI’s mandate provides it with access to more than 3bn consumers across Asia and pre-pandemic data from the International Monetary Fund forecast that the per capita spending power of Chinese consumers would nearly double in US dollar terms over the five-year period to 2024.

- While the underlying tensions that led to the protests in Hong Kong have been overshadowed by the impact of COVID-19, these are far from resolved. The manager will invest in broader regional companies that are listed on the Hong Kong stock market, but at present has very little appetite for domestic Hong Kong stocks. Retail spending and tourism both suffered during the crisis, which has led to many luxury brands re-considering their strategy for this market (Hong Kong has been a hugely profitable gateway into the mainland, helped by tax-free price differentials).

- The manager continues to like Vietnam, which despite its size and relatively low GDP per capita has been relatively effective in managing COVID. The managers have previously stated that this 95m-population economy should return to brisk growth, and there are signs that this is coming to pass. We observe that Vietnam has a young population, with around 1m people entering the workforce each year; education levels are relatively high, as is female participation in the workforce; and Vietnam is urbanising faster than every other country in Asia, except China. While the trade war risk has lessened, manufacturers are still looking to diversify this risk from China and Vietnam is well placed to benefit.

- While the manager has been reducing exposure to technology as it has emphasised cyclical recovery over duration and pace (the managers thinking behind these themes is explained in greater detail below), digital penetration, technological change and the rise of the Asian middle class continue to be key themes within PHI’s portfolio. These are discussed in greater detail below.

Tilting portfolio away from ‘duration’ and ‘pace’ in favour of cyclical growth

The manager looks to embrace growth in all of its forms and lists three market inefficiencies from which it can add value because growth has been under-appreciated:

- Duration;

- Pace; and

- Surprise.

For the duration theme, the manager is looking for world-class companies, using a long-term time horizon, where it believes these companies have the ability to compound the benefits of high growth for much longer than the market expects. In the manager’s view, analysts’ models are biased towards assuming that growth reverts to a normalised level too quickly, which is why they frequently fail to value this class of high-growth company properly. The approach to profiting from such companies is to hold them and leave them to compound over the long term. The manager cites Samsung SDI as an example of this.

For the pace theme, the manager seeks to identify high-quality companies that are growing rapidly and, crucially, faster than the market expects. In the manager’s view, analysts tend to play safe, and huddle in the 5-15% per annum growth range when building their models. PHI says that there are plenty of instances where 30-50% or more is achievable, but analysts tend to under-appreciate this. The manager highlights SEA Limited, a Singapore-based gaming and online e-commerce company and PHI’s largest holding for some time, as an example of this. Roderick says that these analysts tend to compare it to peers in China when assessing its growth rates, which leads them to undervalue its growth prospects. He says that SEA could compound at a multiple of these. The approach to profiting from such companies is to identify them and hold them for as long as the market fails to under-appreciate their growth, or the growth trajectory flattens so that the manager no longer believes earnings can be doubled over a five-year period.

For the surprise theme, the manager is looking for sudden changes as companies or industries hit inflexion points in their growth trajectories. To profit from these, you need to get in early and wait for the inflexion point to occur. The manager cites PT Vale Indonesia as an example. This is a nickel producer which is a play on electric vehicles, primarily in China. Chinese electric vehicle (EV) penetration is currently around 3 to 4%, but the manager expects this to move to 20 to 25%, over the next few years, and this will create a very tight bottleneck in the market for nickel that is needed for the batteries. On this investment so far, the manager has already made 3-4 times its money back.

The manager says that they have been selling down holdings that fall into the duration and pace themes over the last couple of years, and buying into cyclical growth buckets (this trend really accelerated during the market collapse last year as many cyclicals had fallen 60-70%). The manager cites the example of Tata Motors as being extremely good value and at the beginning of an EV growth cycle.

Chinese clampdown

China has been a significant underweight during the last 18 months, primarily because PHI’s manager was concerned about rising levels of competition, particularly within the e-commerce segment. This meant that PHI was significantly underweight Alibaba, and had no exposure to Tencent or Meituan when the Chinese suddenly tightened regulation on internet companies. This has been significantly positive for its relative performance. The manager said that this shift was both much faster and broader than the market had anticipated, to such an extent that it is now tentatively looking for opportunities. Other sectors to be impacted by shifts in regulation are healthcare, housing and education. The manager says that the influences behind the regulatory clampdown are broad, but can be summarised as follows:

- Geopolitics;

- Demographics; and

- Domestic regulation on tech.

On geopolitics, tension between China and the US has been on the rise, which has impacted US-listed Chinese companies. However, PHI’s manager says that if you look at the Chinese domestic market, this is up and is driving companies to re-list in China (which is a positive for the Chinese authorities), primarily on the ‘H’ share market

On demographics, the Chinese authorities are worried about the low birth rate and what this means for the country’s development going forward. The government sees education, healthcare and housing as being key bottlenecks in advancing population growth and the demographic dividend this could bring. As a result, the real estate sector is coming under a lot of pressure and education can no longer be profit-making. However, PHI does not have direct exposure to either housing or education. It does have some exposure to healthcare, but this has primarily been through Korean biotechnology companies.

On the growing influence of the internet, the manager says that there has been a definite change in the domestic regulation of technology companies. However, he thinks that, despite considerable commentary to the contrary, the regulation is generally quite sensible and punishments are not egregious. Furthermore, the companies that are most affected are not being driven out of business and remain both viable and investable. Nonetheless, this is a clear headwind that is here to stay for some time. It helps that, as discussed elsewhere in this note, PHI has been underweight Chinese technology for some time.

Opportunities in both old and new India

The manager has been reallocating some of the proceeds of its sales of Chinese holdings into what he describes as both old and new India. With regards to old non-tech India, the manager says that it has been able to find some great businesses, that are lowly valued, giving it the potential to make some very high returns. Looking at new India and technology, the manager says that the roll-out of 4G connectivity by Alliance Industries four years ago has brought fast internet to the masses and has really driven the evolution of Indian technology businesses. He thinks that this will be a huge driver of growth for India over the next five years.

Roderick cites examples such as the Daily Hunt, which he describes as the TikTok of India, as well as Zomato (which had its initial public offering (IPO) in July – see page 15), which he describes as the Deliveroo of India (PHI has already made 3 to 4 times its money back on this holding). Rodrick says that the expansion of the Internet in India is leading to real innovation and he expects to see between US$200-300bn of technology company listings over the next three years. He says that PHI, through Baillie Gifford’s private markets team, is very well placed to benefit from this.

Returning to old India, Roderick comments that, following a housing bust around a decade ago, affordability has never been better. However, as a consequence of a liquidity crisis three years ago, the banks curtailed their lending, which has clogged up the housing market. Crucially, it has become practically impossible for developers to pre-sell property to fund development, and many have gone out of business. However, with a resurgent economy and growing population, demand is intensifying. Roderick believes that we are at the beginning of a multi-decade Indian property cycle.

Thematic focus – digitalisation and technology transforming industry

The manager believes that the market’s focus on geopolitics and capital flows can result in it missing the bigger picture of a global rise in digital penetration, technological change and the rise of the Asian middle class. The manager seeks to ignore the noise, focusing instead on long-term growth opportunities. He looks for companies that have the potential to increase revenue and earnings at around 15%-20% per annum over a five-year period or longer, and for opportunities where this potential has not been fully recognised by the market.

PHI’s starting premise is how they think the world and individual countries may change over the next three, five and 10 years plus, in every area of life – economically, socially and politically – and the impact that technology might have on these trends. When looking at a company and thinking about what the market size of its industry might be, the manager assesses what the current rate of growth is, how this industry could change, and whether there are additional opportunities for growth in adjacent markets that the company could enter.

The manager’s feeling is that the rapid development of technology is creating a fundamental change in market behaviour, with digitalisation driving profound changes in economic and political systems, businesses, consumer habits and behaviours. The number of sectors and industries that are becoming digitalised and connected is increasing rapidly. There is growing awareness of these changes across the globe.

Electric vehicles and commodities

Electric vehicles (EV) continue to be a significant theme with PHI’s portfolio. Tata Motors was a new investment for PHI in 2020 (see page 13 of our January 2020 note) although the manager is not necessarily focusing on the EV manufacturers themselves. There is a considerable allocation to companies exposed to the components and materials that Roderick expects will be in demand. The manager thinks that, after a decade of ’informational wins‘, where companies have added value through the development of software, intellectual property (IP) and the like, with investors focusing on asset light businesses, the balance could switch back again. He believes that we now need to make progress with physical components, which is reflected in PHI’s increased exposure to commodities during the last couple of years.

For example, to move to a net zero-carbon economy, we need to build considerable infrastructure to support this (for example EV and grid scale batteries), which will require vastly more commodities than are currently available (mining requires considerable capex just to maintain existing production levels and cash-strapped miners have been curtailing this investment). Reflecting this, mining now accounts for around 10% of PHI’s portfolio. In addition to PT Vale Indonesia, PHI now has investments in: Jiangxi Copper, Korea Zinc, Merdeka Copper Gold (Indonesian miner), MMG (Chinese copper miner), Nickel Mines (Indonesia base metal miner); RUSAL, Vedanta, and Zijin Mining Group Co Ltd H shares (gold and copper miner – note: market (H-shares are listed on Hong Kong’s H-share market, while A-shares are listed on the domestic A-share markets in Shanghai and Shenzhen). The manager is focused on companies with low-cost operational assets, with a strong emphasis on both copper and nickel, and which can grow their production. He thinks that, at present, the market continues to give insufficient consideration to the fact that the value of these companies’ reserves could grow as the value of the end-product increases. Despite the recent spike in commodity prices, the manager thinks that the NAVs of these mining companies could triple from here. There is evidence that the market is waking up to the shortage of commodities that will be required to bring about a greener future. He sees this as a theme that continues to have a long growth runway.

Investment philosophy and process

The underlying approach

Baillie Gifford believes that markets are inefficient at pricing long-term growth, especially over a time horizon of at least five years, and that this creates an opportunity to generate alpha. For this reason, it aims to encourage a culture of long-term thinking within the firm. Baillie Gifford believes there is persistence of good company management, business models and stock prices. This translates into a culture of ‘sticking with the winners’.

The manager uses Baillie Gifford’s own research. The team undertakes much of this, but will often commission research from local research teams, academics and industry experts. Baillie Gifford also subjects some companies to forensic analysis, using the services of investigative journalists and forensic accountants. When it is talking to companies, the conversations with their management teams focus on the long-term prospects of the business.

Roderick is able to draw on the resources of the whole investment team, when analysing companies, and can sit in on meetings with companies outside his geographic remit. This is especially beneficial when he is trying to identify how his companies compare with competitors domiciled in other markets.

Each member of the team is assigned a geographical focus for research, and these responsibilities are rotated every few years. Investment ideas are presented to the group, but the lead portfolio manager makes the final decision. Pre-COVID, Roderick would usually spend four to five weeks visiting Asia each year, and will look to do so again when this is possible.

The OEIC and PHI are run in parallel, with some exceptions. A key driver being the need to keep the OEIC’s portfolio relatively liquid to allow for inflows the funding of redemptions. There is an internal limit of holding no more than 10% of the portfolio in illiquid holdings, but within this constraint, PHI has greater freedom to hold more illiquid investments than the OEIC. The OEIC has ended up with more of a large-cap bias as a result, while PHI has more exposure to small-cap names. There is considerable commonality of the stocks held, although the individual weightings may differ. PHI, unlike the OEIC, also has the option of using gearing (borrowing) and invests in unlisted companies.

Building the portfolio

Gifford is an active investor and does not hold stocks just because they are large constituents of any benchmark. Consequently, there are few limits on country, sector or stock weightings imposed on managers. The initial size of a position will reflect the strength of the manager’s belief in the potential risks and rewards of the investment. One of the guiding principles of investing at Baillie Gifford is to ‘run the winners’ (reflecting the belief in the persistency of good business models). However, PHI has a ‘soft’ upper limit of 10% exposure to any one stock. Roderick looks at the shape of the overall portfolio to ensure that he does not have too many companies exposed to similar thematic dynamics.

The mandate allows the manager to use derivatives to control risk and to alter the portfolio’s exposure to markets. In practice, Roderick is not undertaking such activity. The manager has no plans to use hedging to alter the portfolio’s currency exposure.

Sell discipline

Loss of faith in a company’s management is an instant trigger for a sale. Roderick will also sell if he feels the business model is not working, or if the market has caught up with his expectations.

Portfolio allocation

As at 31 October 2021, PHI held 109 holdings in the portfolio, which is a comparable to the 106 stocks it held at 30 November 2020 (the most recently available data when we last published). PHI believes that it can achieve an appropriate level of diversification for its strategy by holding 40–120 companies, although the current 109 level is close to the maximum number of positions. This reflects the fact that the portfolio has seen an elevated level of turnover during the last 18 months (there were significant shifts in the aftermath of the market collapse last year as the manager saw a lot of value and increased turnover, adding more cyclical exposure and increasing gearing, while reducing exposure to areas such as ‘duration’ and ‘pace’).

The manager has been finding more ideas outside of technology and has continued to shift the portfolio away from China, allocating to India, nickel and non-tech holdings (for example, autos and industrials). As we have previously discussed, this was largely a consequence of taking profits following strong performances, with the manager refocusing the portfolio on what he considered to be stronger opportunities. However, the manager expects that the portfolio will become slightly more concentrated over the next year or so, with the number of holdings coming back down to around 80 to 90 positions, which is more akin to its typical number of holdings in recent years. The manager comments that, if a position is below half a percent, he needs to have a strong view if it is to remain in the portfolio.

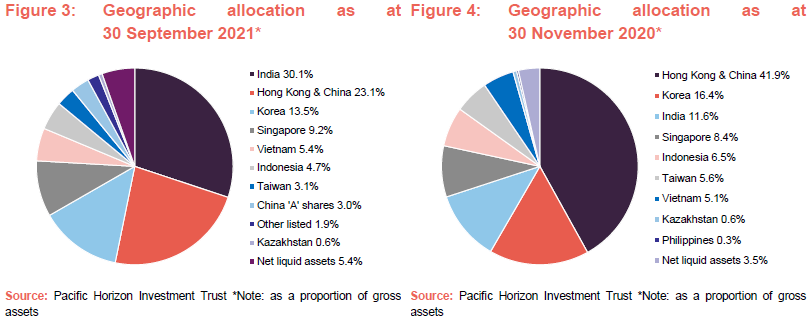

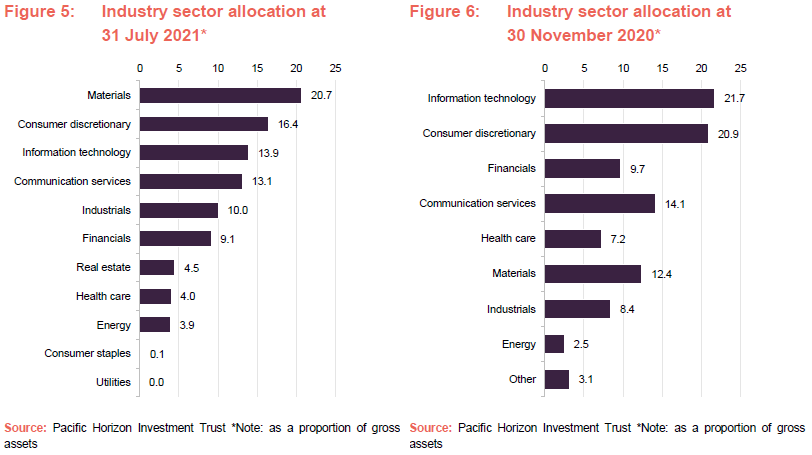

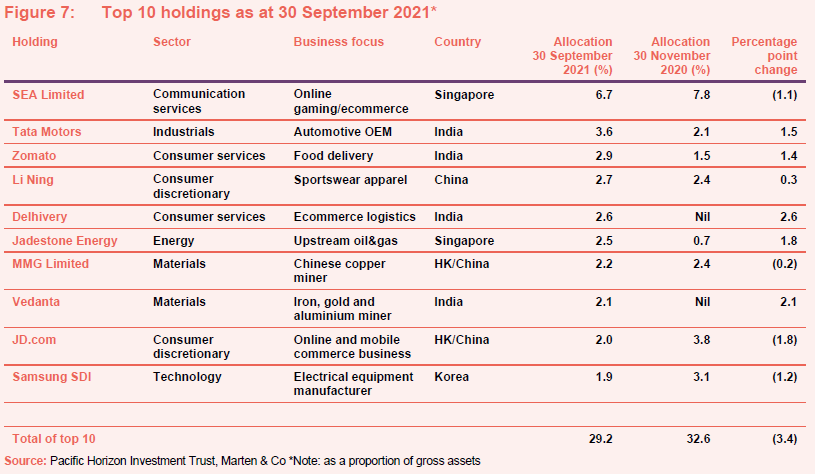

Following the more substantial shifts in allocation that took place last year, which were discussed in our January 2021 note, portfolio turnover has been more modest so far this year. Reflecting this, the changes in PHI’s asset allocation year to date have been driven primarily by relative performance differentials. Comparing Figures 3 & 4 shows a number of changes in the geographic allocations. The massive decrease in the allocation to Hong Kong and China of around 14 percentage points (including the allocation to China ‘A’ shares, which has now been split out as a separate line) reflects both the managers decision to reduce the allocation to this region as well as the relatively poor performance of these holdings in the intervening period (the Chinese government has spooked markets with its clampdown on internet companies, which has impacted the technology sector specifically).

Similarly, the allocation to India has increased markedly (by around 20 percentage points). This reflects both a conscious (and timely decision) by the manager to increase the weight to this region, with PHI also benefitting from its subsequent strong performance. Other notable changes are decreases in the weights to both Korea (19.8% to 13.5%, a fall of 6.3 percentage points) and Vietnam (from 9.8% to 5.4%, a fall of 4.4 percentage points. We commented in our last note that the Korean exposure had been reducing and this trend has continued. The exposure to Vietnam is a useful illustration that the manager constructs a portfolio that is distinctly different to the benchmark, as Vietnam is a non-index country. Another useful illustration is that SEA Limited, PHI’s largest holdings (see the top 10 holdings section below) was, until recently, a non-index position. The manager comments that they have continued to trim SEA Limited over the last couple of years. This has occurred when its strong performance has pushed it towards a 10% allocation within the portfolio and the manager has wanted to moderate its concentration risk. Nonetheless the manager continues to like the company, which he says has significant option value.

It should be noted that the manager is still very constructive on Vietnam and is very bullish on its long-term prospects. He has not been actively reducing the size of PHI’s Vietnamese positions. Instead, it has continued to move down the list due to the strength of performance of other markets. Exposure to Taiwan, already a big underweight, has continued to drift down as the manager has been reducing PHI’s exposure to technology stocks (see below), which includes TSMC (Taiwan Semiconductor Manufacturing Company).

As we have discussed previously, TSMC dominates the Taiwanese market and is a big component of the MSCI AC Asia Ex-Japan Index. Roderick says that, beyond TSMC, he struggles to find opportunities in Taiwan as he sees better investments elsewhere. Similarly, the manager does not see any exciting opportunities in the Philippines. He comments that, while he would look at property, there are much better stories elsewhere (for example in India). PHI has previously held banks in the Philippines, but he thinks that these remain fundamentally challenged and, looking at consumer stocks, they prefer companies elsewhere, such as SEA Limited.

When we last wrote on PHI, we commented that the manager sees an opportunity in the commodities that will be needed to bring about a greener future. At that time, he expected PHI’s commodities overweight to continue to grow, and this has come to pass.

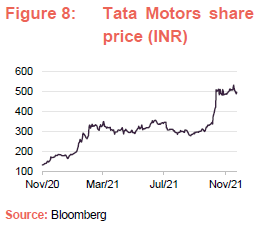

Top 10 holdings

Figure 7 shows PHI’s top 10 holdings as at 30 September 2021 and how these have changed since 30 November 2020 (the most recently available data when we last published). Holdings that have moved into the top 10 are Tata Motors, Zomato, Delhivery, Jadestone Energy and Vedanta.

Names that have moved out of the top 10 are Dada Nexus, Alibaba, Kingdee International, Nickel Mines and Kingsoft Cloud. We discuss some of the more interesting changes in the following pages. Readers interested in other names in the top 10 should see our previous notes, where many of these have been previously discussed (see page 31 of this note).

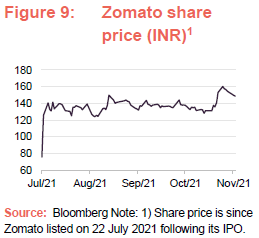

Tata Motors (3.6%) – positioned to reap the benefits of seven years of EV investment

We discussed Tata Motors (www.tatamotors.com) as a new investment for PHI in our January 2021 note (see page 14 of that note). The company, which is the largest automobile manufacturing company in India, plays into the manager’s theme of investing in companies exposed to the structural move away from fossil fuel powered vehicles to electric vehicles. The company, which is part of the Tata Group (an Indian conglomerate that is one of the biggest and oldest industrial groups in India), offers an extensive range of passenger and commercial vehicles including passenger cars, trucks, vans, coaches, buses, sports cars, construction equipment and military vehicles.

As illustrated in Figure 8, Tata Motors has experienced incredible share price growth during the last 12 months. Its domestic business is benefitting from a strong cyclical recovery and the manager believes that it is likely to take market share. However, despite the recent strong performance, the manager believes that Tata Motors has a long growth runway ahead of it.

In February this year, Tata Motor’s JLR subsidiary (Jaguar Land Rover) announced that it was initiating a global restructuring process that would see it trim some 2,000 non-manufacturing jobs from its workforce. This has hit Tata Motor’s bottom line in the short run but should lead to a markedly leaner and more profitable business. PHI’s manager comments that there is a great new line up of products coming through – for example, JLR has also said that its Jaguar brand will be entirely electric by 2025, with electric models of its entire line up launched by 2030. The company’s Land Rover brand is going to launch six fully electric models over the next five years, with the first one coming up in 2024.

As we have previously discussed, Tata Motors has spent several years investing in the development of electric vehicles and, with strong growth expected in its domestic market, is well placed to benefit from the EV trend, which the manager believes to have a positive outlook for the next 1-20 years.

As we have previously discussed, the Modi government has been working to reduce India’s dependency on imports, particularly where the country has a large market (the government’s “Made in India” programme has been a big success) and this provides a structural tailwind to Tata Motors. Roderick believes that if Tata Motors can make this technology work with its high-end Jaguars and Land Rovers, it can do very well. He thinks that the market is slowly waking up to the company’s growth potential, but this trend has a long way to run.

Zomato (2.9%) – the Deliveroo of India

Like Tata Motors above, we last discussed Zomato (www.zomato.com) as a new addition to PHI’s portfolio in our January 2021 note. At that time, we commented that it was PHI’s largest unlisted holding and that it could be described as a pre-IPO investment (PHI had invested US$5m in a fundraising round just before the pandemic broke and was able to add to the holding in November 2020 at the same price). The expectation when we last wrote was that Zomato would list in the first half of 2021. Zomato subsequently listed in July 2021 and, as is illustrated in Figure 9, experienced a strong uplift in its share price following its IPO.

Zomato is an Indian last-mile food delivery company. It operates an online restaurant search, ordering and discovery platform (both through a website and an app) that provides menus, contact details, pictures, directions, ratings, and customer reviews for a range of restaurants. It is among the two largest players in India’s food delivery business (the other is Swiggy, which is being backed by names such as Tencent Holdings, Naspers and DST Global). Zomato has the largest paid membership programme for individuals to receive discounts at restaurants. It is backed by Alibaba’s Ant Financial and Uber.

Both Zomato and Swiggy faced challenging business conditions during the pandemic, as lockdowns shuttered restaurants for walk-in customers, but food delivery was able to recover more quickly as Indians continued to order food via apps (aided by strong growth in smart phone penetration). PHI’s manager believes that home delivery services will continue to grow strongly from here, aided both by the greater exposure and experience developed during the COVID-19 pandemic.

Delhivery (2.6%) – targeting a US$1bn IPO

Delhivery (www.delhivery.com) is an Indian logistics company and one of PHI’s largest investments. Like Zomato, it is a pre-IPO company, having made a filing with the Indian regulator in early November 2021 with plans for an IPO that seeks to raise around US$1bn. Delhivery, which began life in 2011 as a food delivery firm, is now a full suite of logistics services company with operations in over 2,300 Indian cities. In addition to Baillie Gifford, Delhivery is backed by investors such as SoftBank, Tiger Global Management, Times Internet, The Carlyle Group, Steadview Capital and Addition. PHI’s manager observes that a number of Indian IPOs have seen the companies’ share prices quickly double following listing. He expects Delhivery to do well with its IPO.

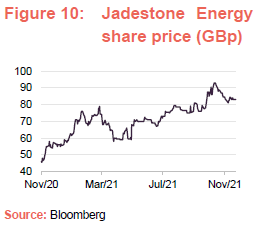

Jadestone Energy (2.5%) – a ‘surprise’ holding

Jadestone Energy (www.jadestone-energy.com) is a holding that falls into the manager’s ‘surprise’ bucket. It is an upstream oil and gas development and production company in the South East Asia-Pacific region. Its portfolio includes producing assets in Australia, Indonesia, Malaysia, Vietnam and New Zealand.

PHI’s manager says that Jadestone has very good geologists and its speciality is acquiring small- to medium-size lots that have been poorly managed by their previous owners (typically State-owned enterprises). Roderick cites Jadestone’s acquisition of a 69% operating interest in the Maari asset, a shallow offshore oil field in the Taranki basin in New Zealand, as an example of the value that the company can create. Jadestone has acquired two producing oil fields from OMV New Zealand Limited in a transaction that sees it receive assets that are worth around US$200m for free, as well as a payment of US$20m to undertake the clean-up operation once the wells are exhausted. The company has predicted an IRR of 100% for the acquisition.

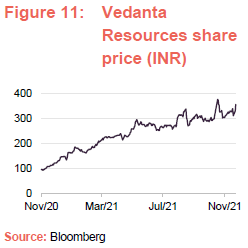

Vedanta Resources (2.1%) – benefitting from a change of alignment

Vedanta Resources (vedantaresources.com) is a new entry to PHI’s portfolio. It is one of India’s largest commodity conglomerates with exposures to zinc, aluminium, steel, copper, oil and iron ore. PHI’s manager comments that Vedanta is a very diverse mining company that is well-positioned to benefit from a new global commodity cycle, which PHI was able to acquire at a very attractive valuation.

PHI’s manager says that Vedanta Resources has suffered from historically poor corporate governance that suppressed its share – its parent company, the Vedanta Group, made a number of attempts to acquire the business at valuations that other shareholders generally felt to be unduly cheap. Baillie Gifford and IPC are the largest shareholders, and pushed back strongly against these advances, which has led to the parent changing its strategic direction. PHI’s manager believes that there is now good alignment between management and external shareholders and that Vedanta Resources’s share price will benefit from renewed efforts to take the business forward and move the share price up.

Performance – exceptional outperformance continues

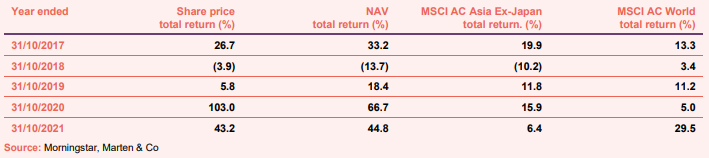

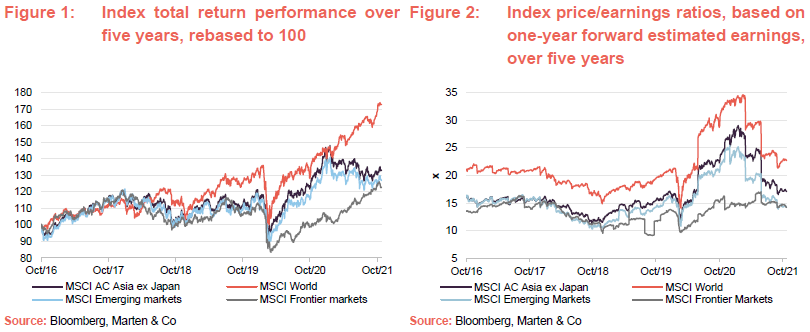

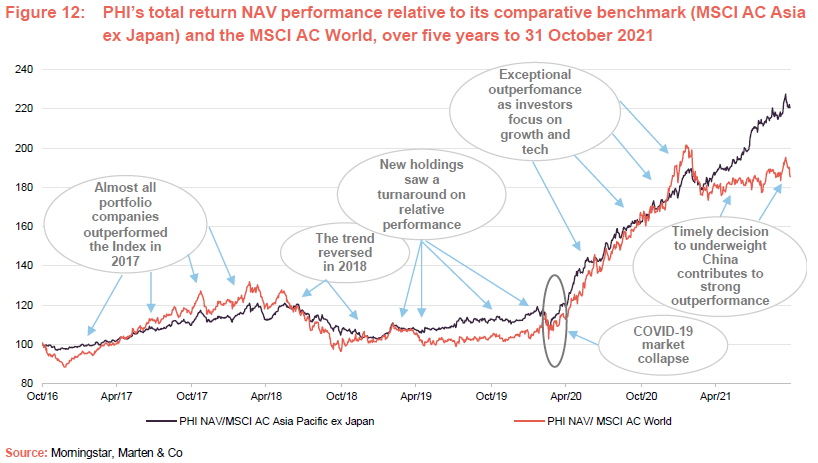

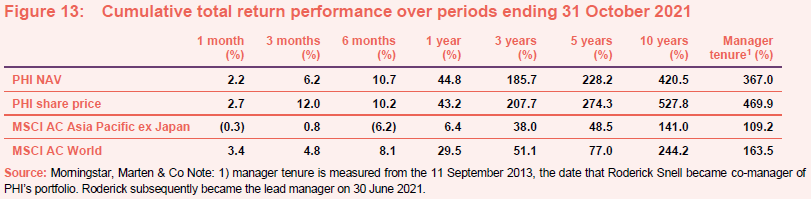

As we have previously discussed, PHI’s performance has seen a marked improvement during the last four years. This initially occurred as PHI successfully rejigged its portfolio in 2018, (which led to a performance-based tender offer in 2019 not being required) and, as is illustrated in Figure 12 above, PHI has found itself in a performance sweet spot since the COVID-related market collapse of March 2020. This trend of strong outperformance has continued since we last published in January 2021, aided by a timely decision by the manager to slash PHI’s exposure to China. PHI’s exceptionally strong performance since the onset of the virus has lifted its performance over all of the time periods in Figure 13.

Performance attribution for the year ended 31 July 2021

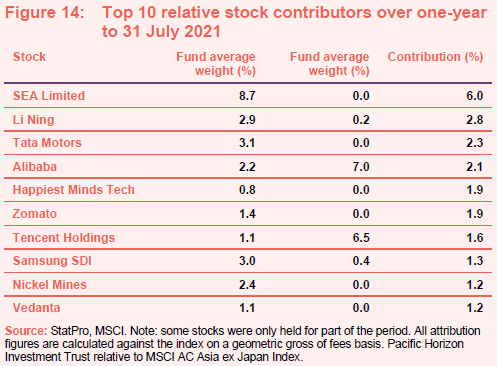

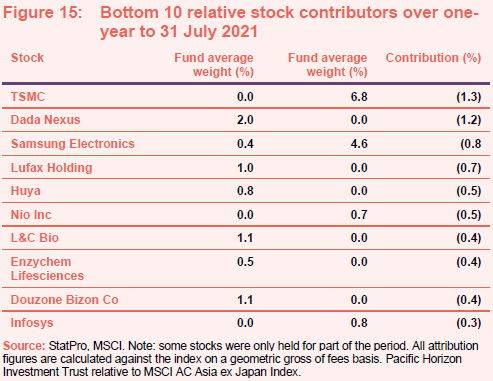

Baillie Gifford has kindly supplied us with some stock level performance attribution data for PHI’s portfolio for the last financial year (for the year ended 31 July 2021). The top 10 and bottom 10 contributors to PHI’s performance are provided in Figures 14 and 15.

The strongest positive contributions have come from:

- SEA Limited – This has been PHI’s largest holding for some time. It is one of South-East Asia’s leading companies in gaming and online e-commerce. It remains an independent company, though it is significantly backed by Tencent. During the period, SEA’s gaming division performed very strongly, with Free Fire becoming the world’s most downloaded game in 2020 and reaching more than 300m monthly active users. SEA’s e-commerce segment aims to grow its market share across much of ASEAN. PHI’s manager thinks that, with its increasing scale, SEA looks set to become the dominant online shopping platform across much of the region in the next 10 years.

- Li Ning – This company is China’s leading domestic branded sportswear retailer. It has continued to benefit from a shift towards local brands by Chinese consumers. Younger Chinese consumers are increasingly turning to fashion to show their individualism, bringing opportunities for manufacturers and retailers in tune to the market, in areas such as athleisure. PHI’s manager believes that Li Ning represents a new breed of Chinese company with the brand power to charge higher prices.

- Tata Motors – This holding was added in the aftermath of the COVID-related market collapse last year (we discussed this in detail our January 2021 note – see page 14 of that note). It was one of a number of cyclical stocks that the manager added at deeply depressed valuations. It also plays into the manager’s theme of investing in companies exposed to the structural move away from fossil fuel powered vehicles to electric vehicles. At the time of investment, PHI’s managers felt that Tata motors was extremely good value and, having spent seven years investing in the development of electric vehicles, they believe it is well placed to capture the rapid growth that this market is expected to see in the years to come. This confidence has been rewarded with very strong share price performance since as both the company and the Indian market have performed strongly.

- Alibaba – previously a significant PHI holding, the trust has benefitted from the manager’s decision to reduce exposure to China and Chinese tech in particular – meaning that PHI’s portfolio has been significantly underweight the stock at a time when it has been performing poorly. Alibaba, along with other significant Chinese technology holdings, has suffered as the government has clamped down heavily on the sector.

The largest negative contributions came from:

- TSMC – PHI has suffered from having zero exposure to TSMC at a time when the stock has been performing very strongly in response to a global semiconductor shortage.

- Dada Nexus – This company is a Chinese ecommerce distributor of online consumer products that came to market with its IPO in June last year (we discussed the newly-acquired holding in our January 2021 note – see page 17 of that note). Along with Alibaba and JD.com, Dada Nexus was given a boost by the pandemic as consumers have switched more and more of their purchasing to online. However, more recently, it has suffered along with likes of Alibaba (discussed above) following the Chinese government’s regulatory clampdown on internet companies.

- Samsung Electronics – PHI suffered from having a significant underweight to Samsung Electronics, which performed strongly during the period, reflecting the strong demand for technology products in the aftermath of COVID.

- Lufax Holdings is a Chinese fintech company that is a non-benchmark holding. It is another holding that has suffered following the Chinese government’s regulatory clampdown on internet companies.

- Huya – This is a Chinese online game streaming company. It is another holding that has suffered following the Chinese government’s regulatory clampdown on internet companies.

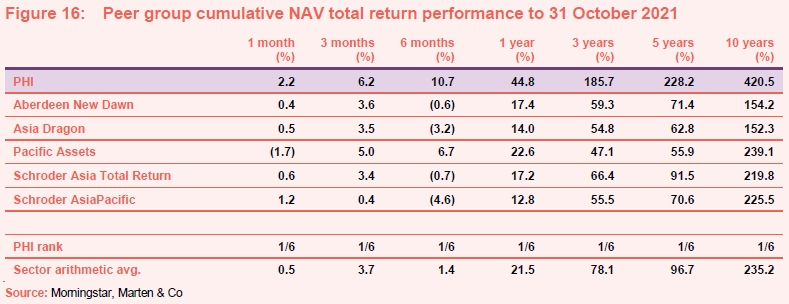

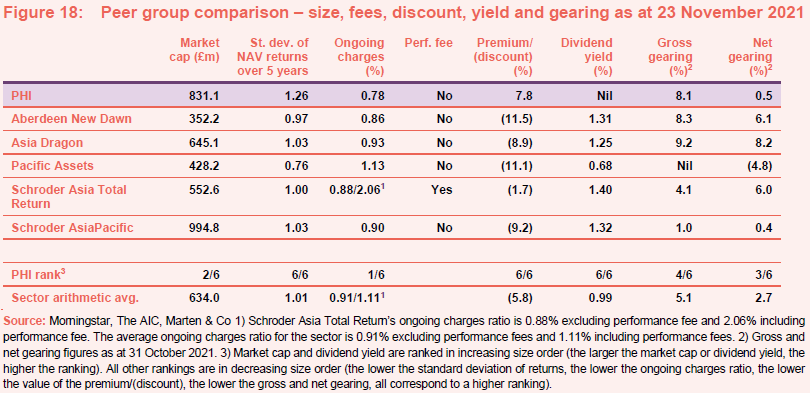

Peer group comparison – Asia Pacific sector

PHI is a member of the AIC’s Asia Pacific sector, which comprises six members. All of these are illustrated in Figures 16 through 18. All of these were members of the peer group when we last wrote about PHI. However, in the intervening period, Invesco Asia Trust has migrated to the Asia Pacific Equity Income sector, reflecting a new focus on income generation. Members of Asia Pacific sector will typically have:

- over 80% invested in quoted Asia Pacific shares;

- less than 80% in any single geographic area;

- an investment objective/policy to invest in Asia Pacific shares;

- a majority of investments in medium to giant cap companies; and

- an Asia Pacific benchmark.

As illustrated in Figure 16, PHI’s cumulative NAV total return performance ranks first out of the entire peer group for every time-period provided. Its strong emphasis on growth has been very successful over the longer term and it benefitted as investors have looked to growth in the aftermath of COVID.

In our last note, we commented that it had underperformed its peers in the very near term and how this reflected the then-recent discovery of a number of vaccines for COVID-19, which had caused markets, and in particular value stocks, to rally. However, we felt that this relief for structurally-challenged companies would likely prove temporary, which appears to have come to pass.

PHI’s performance has also benefitted from a timely move by the manager to reduce the portfolio’s exposure to China, which has seen many tech companies, in particular, significantly impacted by a crackdown by the authorities on their activities there. Not surprisingly, PHI’s NAV performance is markedly ahead of the peer group average, over all of the time periods provided in Figure 16, and particularly over the longer measurement periods.

PHI’s manager emphasises that the trust is very different to other funds in the peer group, with its particularly strong emphasis on growth. The manager wants to be invested in the top 20% of the fasting growing companies in the Asia Pacific region. It explicitly looks for companies that it believes can double their earnings over a five-year time horizon.

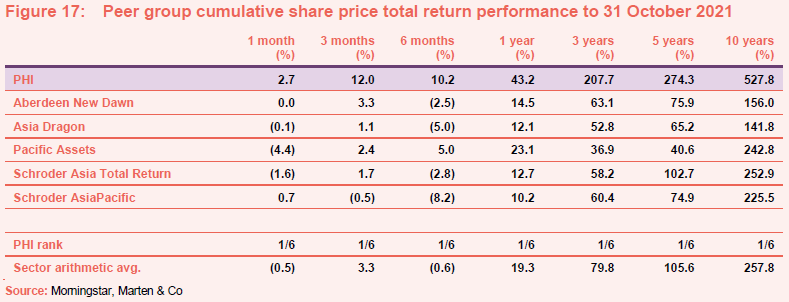

Figure 17 illustrates a similar story for share price total return, with PHI ranking first for all of the periods provided. PHI’s share price total returns are well ahead of the peer group average for all of the time-periods provided. The superior share price performance over the NAV that is evident, particularly in the five- and 10-year periods, reflects the fact that PHI has generally traded on a much stronger rating in recent years.

When we wrote on PHI in October 2019, we commented how it was one of the smallest funds in the sector, but that this was not reflected in its ongoing charges ratio, which was equal to the sector average at that time. Then, in January 2021, we commented that, through a combination of its very strong performance and the significant share issuance that the subsequent premium rating had allowed, PHI had moved up the market cap scale to third – behind Asia Dragon and the then titan of the sector, Schroder AsiaPacific. These trends have continued since January of this year so that PHI has overtaken Asia Dragon and now ranks second to just Schroder AsiaPacific and the latter’s lead has narrowed substantially as it has shrunk while PHI has grown significantly during 2021.

Reflecting this growth, PHI’s ongoing charges ratio has been on a declining trend (see page 27 for more discussion) and is now the lowest in the sector by a margin at 0.78% (the next lowest being Schroder Asia Total Return at 0.88% excluding its performance fee, but 2.06% once its performance fee is included). All things being equal, we expect PHI’s ongoing charges ratio to full further for the current financial year – both as PHI continues to grow and as the trust benefits from the strong asset growth seen in the first half of calendar 2021 applied over a full financial year. Assuming that it continues to grow, PHI’s shareholders should benefit both from PHI being able to spread its fixed costs over a wider asset base and from its tiered fee structure that sees additional assets from here charged at the lowest fee in its tiered structure of 0.55% of net assets.

As illustrated in Figure 18, PHI is the one trust trading at a premium in the sector, which reflects its peer group beating performance that is illustrated in Figures 16 and 17. The next most-highly rated is Schroder Asian Total Return which was trading at a small discount of 1.7%. This is another strongly-performing trust, although its returns are significantly behind that of PHI’s.

Not surprisingly, given its focus on capital growth (PHI has paid dividends to the extent required to maintain its investment trust status – see page 24), PHI’s dividend yield is the lowest in the sector (it is not paying a dividend for the year ended 31 July 2021 and it should be noted that PHI frequently pays no dividend).

In terms of net gearing levels (a measure of indebtedness after allowing for any cash on the balance sheet – calculated by taking any borrowings and deducting cash, and expressing as a percentage of the trust’s net assets), PHI was below the sector average at the end of October 2021. Its NAV returns have shown the greatest volatility, but these are by no means high, and are more than compensated for by its superior performance.

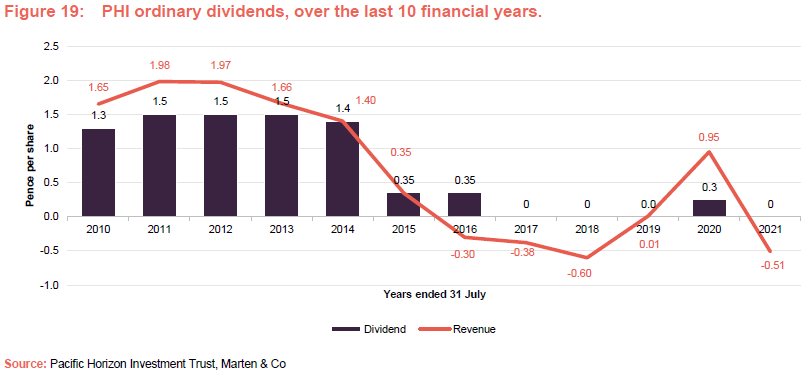

Dividend

PHI’s primary objective is to generate capital growth. Any dividend paid is by way of one final payment per year, following approval at the annual general meeting (AGM). For the avoidance of doubt, PHI’s board has made it clear that investors should not consider investing in the company if they require income from their investment. The board has also said that it does not intend to draw on PHI’s revenue reserve to pay or maintain dividends.

For the year ended 31 July 2021, PHI generated a small revenue deficit of £402k, equivalent to -0.51p per share (2020: a small revenue surplus of £564k, equivalent to 0.95p per share). The revenue deficit for the 2021 financial year means that PHI is not required to pay a dividend, which is in contrast to the 2020 financial year (as illustrated in Figure 19) where PHI declared a dividend of 0.25p per share.

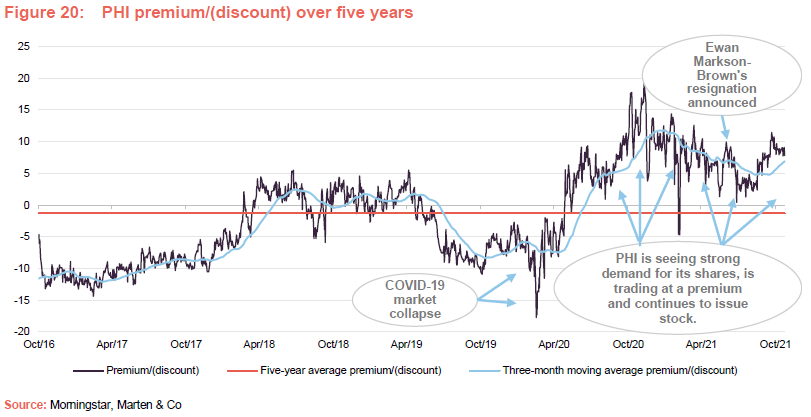

Premium/(discount)

As illustrated in Figure 20, PHI has, for much of the last four years, traded at a premium to NAV. The premium has been particularly pronounced since the beginning of June 2020, which has allowed PHI to issue a significant amount of stock, particularly during the first half of this year, as is illustrated in Figure 21. The primary driver of PHI’s premium and the strong demand for its stock is its performance record in recent years.

Performance-driven premium rating

As discussed in our previous notes, PHI moved to a premium rating in the second quarter of 2018. This occurred as PHI successfully rejigged its portfolio, which led to a marked improvement in performance (it should be remembered that PHI made shareholders a performance-based tender offer in 2019 that was ultimately not required due to a strong improvement in performance coming through – see page 13 of our November 2019 note).

As also discussed in our November 2019 note, the discount widened over the summer of 2019 as risk aversion increased, but narrowed again as markets settled before briefly spiking out to a five-year high of 17.7% on the 17 March 2020 as markets collapsed in the face of an accelerating COVID-19 infection rate. However, as illustrated in Figure 20, this widening proved to be brief as PHI has found itself in a performance sweet spot. As we have discussed previously, in a bid to stabilise the global economy in the face of the virus, governments pumped considerable fiscal and monetary stimulus into the financial system, and investors rotated strongly to focus on growth stocks as the low interest rate for longer narrative was extended even further. Technology and biotechnology/healthcare were massive beneficiaries.

In addition, Asian countries, having previous experience of handling pandemics such as SARS (severe acute respiratory syndrome coronavirus) and MERS (Middle East respiratory syndrome–related coronavirus), were effective in controlling the spread of the virus, allowing their economies to normalise more quickly. All of this was reflected in PHI’s own exceptionally strong performance (in addition to very strong performance, it has markedly outperformed its peers as well as the performance indices it traditionally compares itself against), which has led to strong demand for its strategy from investors.

Premium/(discount) management

PHI has authority to repurchase up to 14.99% of its issued share capital, as well as to issue up to 10% at a premium to NAV. These authorities give the board mechanisms through which it can manage PHI’s discount or moderate any premium that should arise. Shares repurchased can be held in treasury and reissued by the company to meet demand. Any reissue of treasury shares would only be undertaken at a premium to NAV.

As discussed in our January 2021 note, proposals to allow PHI to issue up to 100% of its issued share capital, over a 12-month period, were detailed in a prospectus published on 11 December 2020. Shareholders approved the resolutions relating to these proposals at a general meeting held on 19 January 2021. The measures settled investors’ nerves regarding the scarcity of PHI stock, which helped to moderate its premium.

We welcome PHI’s continued expansion as it benefits all shareholders. All stock is issued at a premium to NAV and is therefore NAV accretive to existing shareholders. Furthermore, expanding the trust allows for greater operational efficiencies and, all things being equal, should lower PHI’s ongoing charges ratio by spreading its fixed costs over a wider asset base. Further share issuance should also lead to greater liquidity in PHI’s shares.

Fees and costs

Baillie Gifford & Co Limited acts as PHI’s alternative investment fund manager and has delegated portfolio management services to Baillie Gifford & Co. PHI’s management fee is calculated on a tiered basis. With effect from 1 January 2019, the annual management fee is 0.75% on the first £50m of net assets, 0.65% on the next £200m of net assets and 0.55% on the remaining net assets.

Management fees are calculated and paid quarterly in arrears and there is no performance fee. The managers may terminate the management agreement on six months’ notice and the company may terminate it on three months’ notice.

Reflecting both its tiered fee structure and strong share issuance during the last few years, PHI’s ongoing charges ratio has been on a declining trend. For the accounting year ended 31 July 2021, it was 0.78%, down from 0.92% for 2020, 0.99% for 2019, and 1.02% the year before that. Baillie Gifford & Co Limited also provides company secretarial services. These services are included as part of the management agreement. PHI’s ongoing charges ratio has been on a declining trend in recent years. This reflects both the reduction in the base management fee that is noted above, as well as the continued strong share issuance which means that PHI’s fixed costs are spread over a larger asset base.

Capital structure and trust life

PHI has a simple capital structure with just one class of ordinary share in issue. Its ordinary shares have a premium main market listing on the London Stock Exchange and, as at 23 November 2021, there were 91,529,961 in issue with none held in treasury.

Each year, the company takes powers to buy back up to 14.99% of its shares at a discount to NAV. It also asks for permission to issue up to 10% of its issued share capital at a premium to NAV. These authorities give the board a means by which they can manager PHI’s premium/discount.

As we noted in our January 2021 note, PHI was able to issue 16.1m shares over the course of the 2020 (representing 27.2% of the shares in issue on 31 December 2019) at a premium to NAV, when demand could not be satisfied from existing shareholders. By issuing shares at a premium, PHI was able to improve liquidity in the trust’s shares, while also providing a boost to the NAV. Increasing the trust’s size also has the effect of reducing ongoing charges, as fixed costs are spread over a wider base. Calendar year to date, PHI has issued 16.47m shares as at 23 November 2021 (equivalent to 21.9% of its issued share capital at the end of 2020).

Gearing (borrowing)

PHI has a one-year £60m multi-currency revolving credit facility (RCF) with The Royal Bank of Scotland International Limited, which expires on 13 March 2022. Gearing parameters are set by the board and the manager operates within these. As of 31 July 2021, the range was set at -15% (i.e. a net cash position) to +10%, although PHI is permitted to go up to +12% due to market movements. PHI’s gross gearing was nil as at the end of October 2021 and it was running a net cash position of 4.8%. These contrast with gross and net gearing levels of 8.8% and 5.5% at the financial year-end, respectively. The main covenants relating to the RCF are that PHI’s borrowings should not exceed 20% of its adjusted net asset value and PHI’s net asset value should be at least £240m.

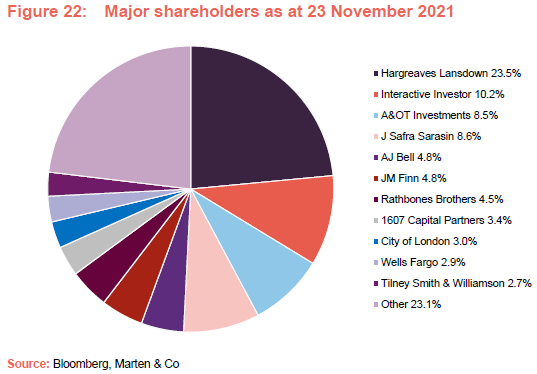

Major shareholders

Five-yearly continuation votes

Shareholders are given the opportunity to vote on the continuation of the company every five years. Most recently, shareholders approved PHI’s continuation at the trust’s annual general meeting on 17 November 2021. Given PHI’s strong performance and the strong demand for its shares, as reflected in both its premium rating and ongoing share issuance, it is not surprising the shareholders approved PHI’s continuation for another five years.

Financial calendar

PHI’s financial year-end is 31 July. It usually publishes its annual results in September (interims in March) and holds its AGMs in October or November. Where applicable, it pays its annual dividend shortly after its AGM.

Board

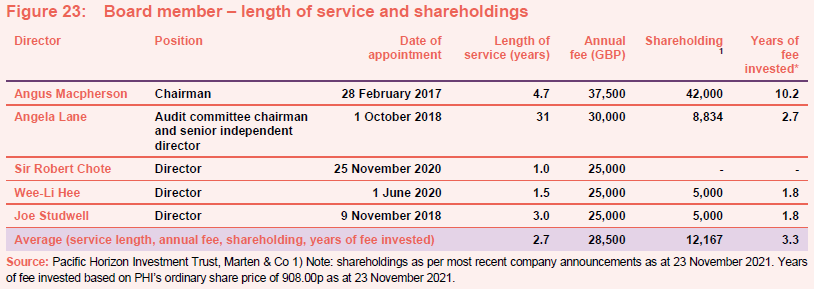

PHI’s board comprises five directors, all of which are non-executive, considered to be independent of the investment manager and do not sit together on other boards. The directors put themselves forward for re-election at the first AGM following their appointment. Thereafter, directors submit themselves annually re-election. Having seen some longer-standing directors retire during the last couple of years, PHI has a relatively young board with an average length of service of 2.7 years.

Directors’ fees

There is a limit of £200,000 for the aggregate of fees paid to directors, which forms part of the company’s articles of association. Shareholders approved the raising of this limit from its previous level of £150,000 at the November 2020 AGM. They would have to vote to approve any further change to this limit. For the current financial year, the chairman’s fee has increased by 8.7% to £37,500 (previously £34,500), the fee for the audit committee chair has increased by 15.4% to £30,000 (previously £26,000) and the fee for other directors has increased by 8.7% to £25,000 (previously £23,000). At these fee rates, the total directors’ fees amount to £142,500, which is well within the £200,000 limit.

Recent share purchase activity by directors

Since we last published in January 2021, Angela Lane has purchased an additional 2,298 shares (in September 2021), Joe Studwell has purchased an additional 1,000 shares (in March 2021) and Wee-Li Hee has made her inaugural purchase of 5,000 shares.

With the exception of Robert Chote, who is the most recent addition to PHI’s board, each of the directors has a significant personal investment in the trust. This is favourable in our view, as it shows significant commitment and helps to align directors’ interests with those of shareholders.

Angus Macpherson (chairman)

Angus was appointed to the board of directors in 2017 and became chairman of the trust on 12 November 2019, following the retirement of Jean Matterson from the board, at the company’s AGM the same day.

Angus was based in Asia between 1995 and 2004 in Singapore and Hong Kong, most recently as head of capital markets and financing for Merrill Lynch for Asia. Currently, he is chief executive of Noble and Company (UK) Limited, an independent Scottish corporate finance business. He is also currently chairman of Henderson Diversified Income Trust Plc, is a non-executive director of Schroder Japan Growth Fund Plc and is the former chairman of JP Morgan Elect Plc.

Angela Lane (audit committee chair and senior independent director)

Angela was appointed as a director on 1 October 2018, and became both the audit committee chair and senior independent director on 10 November 2020, following the retirement of Edward Creasy at the conclusion of PHI’s AGM that same day.

Angela is a qualified accountant and previously spent 18 years working as a private equity investor for 3i Plc. She has held several non-executive and advisory roles for small and medium capitalised companies across a range of industries. She is a non-executive director of Sherborne Schools Worldwide, BlackRock Thorgmorton Trust Plc and Dunedin Enterprise Investment Trust Plc, where she is also chairman of its audit committee. Previously, she held the role of non-executive chairman of Huntswood CTC.

Sir Robert Chote (director)

Robert is an economist, journalist and academic. He became chairman of the Northern Ireland Fiscal Council in 2020 and was chairman of the Office for Budget Responsibility, the nation’s top fiscal watchdog, from 2010 to 2020. He chaired the OECD’s network of parliamentary budget officials and independent fiscal institutions, and currently chairs the external advisory group of the Irish parliamentary budget office. Robert served as director of the Institute for Fiscal Studies from 2002 to 2010, as an advisor to senior management at the International Monetary Fund from 1999 to 2002, as economics editor of the Financial Times from 1995 to 1999, and as an economics and business writer on the Independent and Independent on Sunday from 1990 to 1994.

Robert is chair of the Royal Statistical Society’s advisory group on public data literacy. He is also a member of the Policy Committee of the Centre for Economic Performance at the London School of Economics, the advisory committee of the ESRC Centre for Macroeconomics, and the Council of Westcott House Theological College in Cambridge. He is a governor of the National Institute of Economic and Social Research (NIESR) and a visiting professor at the Department of Political Economy, Kings College London. He also serves on advisory boards at the Warwick Manufacturing Group and is a senior adviser to the governance reform consultancy, FMA.

Wee-Li Hee (director)

Wee-Li is an experienced Asian analyst, fund manager and CFA Charterholder. Brought up in Singapore, she speaks fluent Mandarin and studied in the UK at the University of Leeds and the London School of Economics and Political Science. After graduation, in 2002 she joined First State Investments in Singapore as an analyst, subsequently moving to the firm’s Edinburgh office in 2005. Having co-managed Scottish Oriental Smaller Companies Trust, she became lead manager in 2014, stepping back as a result of family commitments to return to a co-manager role in 2017 and retiring at the end of 2019. She is a non-executive director of Melville Paisley Investments.

Joe Studwell (director)

Richard Frank (‘Joe’) Studwell has spent 25 years working in East Asia as a journalist, independent researcher at Dragonomics and author under the name of Joe Studwell. His published works include Asian Godfathers: Money and Power in Hong Kong and South East Asia and How Asia Works: Success and Failure in the World’s Most Dynamic Region.

Previous publications

Readers interested in further information about PHI, may wish to read our previous notes on the trust, details of which are provided below.

- Powered by technology (our annual overview note published 20 January 2021) discussed how PHI’s focus on growth, and technology and biotechnology stocks in particular, saw it generate a very impressive uplift in its NAV over the course of 2020, as we attempted to adjust to life under the pandemic, which accelerated a number of structural trends.

- 2018 re-calibration paying off (our annual overview note published on 8 November 2019) discussed how the manager’s decision to re-position PHI’s portfolio, by lowering its allocation to technology stocks, as well as excellent returns from stock picks made in 2018, were paying off. At that time, PHI was the best-performing Asia Pacific fund in net asset value (NAV) terms over the year-to-date.

- Pause for breath? (our annual overview note published on 8 November 2018) discussed how, after two years of strong performance, PHI had suffered a reversal of fortune over three months as sentiment swung against both China and the technology sector. The note discussed how this could prove to be short-lived, if China and the US could agree a trade deal.

- Top of the pops! (our annual overview note published on 30 October 2017) discussed how PHI benefitted strongly as both the Asia ex Japan region and technology stockshad rallied. This pushed PHI up its peer-group rankings so that it was first and second, in terms of NAV total return, over one and three years respectively.

- Brave new world (our update note published on 10 October 2016) discussed how PHI’s performance had started to improve, but that the manager thought there is still considerable potential for the portfolio. He believed that some of the themes that PHI’s portfolio was focusing on could radically alter all our lives and that many Asian companies will be at the forefront of this change.

- Invest in Asian growth (our Initiation note published on 21 March 2016) discussed how PHI was suffering as investors were shying away from Asia (weak Chinese growth) and were also focused on defensive stocks for the same reason(technology and biotechnology were not in favour). The note explained that PHI could perform well in an environment where investors were less risk averse.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Pacific Horizon Investment Trust Plc

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.