Top performer as Asia regains momentum

Pacific Horizon (PHI) has rebounded strongly over the past year, outperforming its benchmark and peers as sentiment towards Asia has improved. The trust’s growth-focused approach, which had been out of favour during the period when global interest rates were rising, is once again delivering results.

Despite the obvious challenges, Asian markets have benefitted from resilient domestic demand, easing trade tensions, and renewed confidence in technology-driven growth. With valuations across much of the region still reasonable and PHI’s managers focused on leading companies in areas like semiconductors and artificial intelligence, there could be further upside to come.

Focused on Asia ex-Japan growth stocks

PHI invests in the Asia-Pacific region (excluding Japan) and in the Indian subcontinent in order to achieve capital growth. The company is prepared to move freely between the markets of the region as opportunities for growth vary. The portfolio will normally consist mostly of quoted securities, although it may hold up to 15% of total assets in unlisted investment opportunities, measured at the time of initial investment.

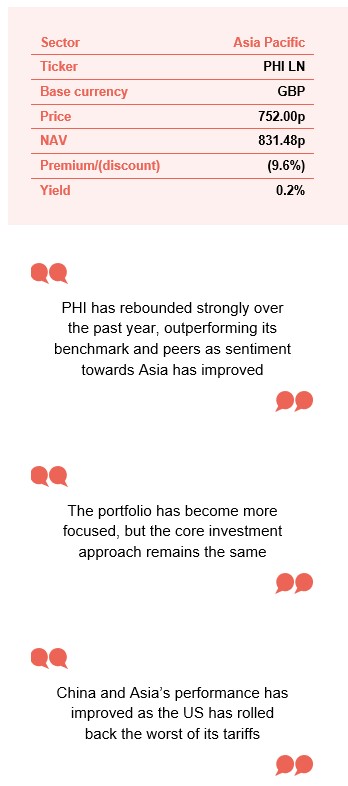

At a glance

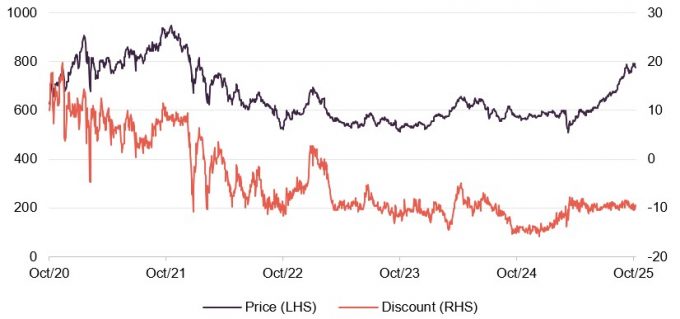

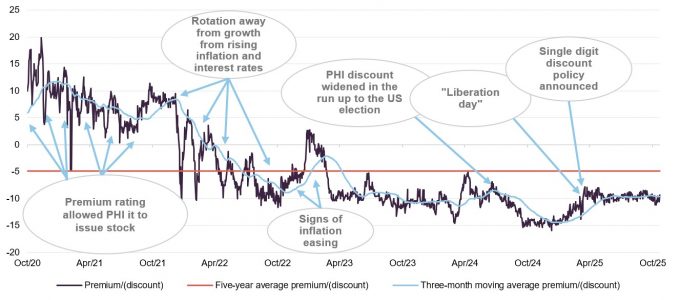

Share price and discount

For several years, PHI has used share buybacks to help reduce its discount. In April, PHI introduced a five-year performance-related tender and stated it would continue buybacks, aiming to keep the discount to net asset value (NAV) in single digits during normal market conditions. This approach has worked, with the discount averaging 9.6% since the announcement and peaking at 11.1%.

Time period 31 October 2020 to 20 November 2025

Source: Bloomberg, Marten & Co

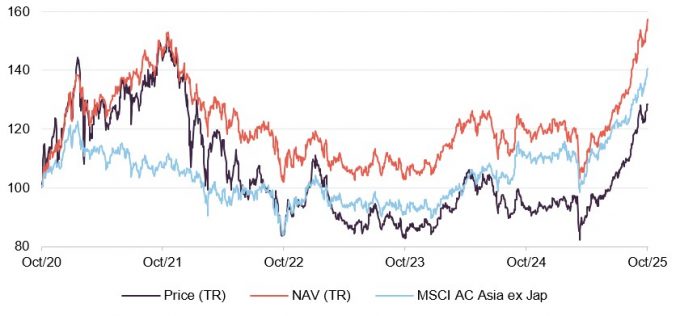

Performance over five years

PHI has a strong long-term track record of outperforming both its MSCI AC Asia Pacific ex Japan benchmark and the MSCI AC World Index, as shown in Figure 9 on page 12. Recent performance has also been strong, with PHI now leading its peer group across all periods shown in Figure 9 and being the top-performing fund in share price total return over most periods (see Figure 10 on page 13).

Time period 31 October 2020 to 31 October 2025

Source: Bloomberg, Marten & Co

| Year ended | Share price total return (%) | NAV total return (%) | MSCI AC Asia ex-Japan total return (%) | MSCI AC World total return (%) |

|---|---|---|---|---|

| 31/10/2021 | 43.2 | 44.8 | 7.1 | 29.9 |

| 31/10/2022 | (41.4) | (29.5) | (21.0) | (4.6) |

| 31/10/2023 | (1.5) | 0.8 | 7.5 | 4.3 |

| 31/10/2024 | 12.4 | 16.4 | 21.4 | 25.4 |

| 31/10/2025 | 36.9 | 30.2 | 26.4 | 20.1 |

Fund profile

Additional information is available at the manager’s website: www.bailliegifford.com

Pacific Horizon (PHI) is an investment trust that specialises in investing in growth companies in Asia ex-Japan. Baillie Gifford & Co (Baillie Gifford) has been appointed to manage PHI’s portfolio on behalf of Baillie Gifford & Co Limited, the trust’s alternative investment fund manager. Baillie Gifford has managed PHI since 1992. Baillie Gifford is a long-term growth investor, and it believes that there is a significant opportunity to outperform markets over the long term using this approach. Pacific Horizon was promoted to the FTSE 250 index in January 2023.

About the manager

Well-resourced investment team.

Baillie Gifford has 145 investors and analysts in Edinburgh, with three in the US and five in China, not counting ESG analysts. The firm is structured as a partnership and promotes teamwork, though portfolio managers have final say over their portfolios. As of September 2025, Baillie Gifford managed or advised on about £213.1bn. PHI and the Baillie Gifford Pacific Fund together had assets of around £3.4bn at the end of September 2025.

PHI is managed by Roderick Snell (lead manager) and Ben Durrant (deputy manager).

Roderick Snell leads PHI’s portfolio as senior fund manager for Baillie Gifford’s Asia ex-Japan strategies, supported by Ben Durrant, deputy manager since January 2023. Roderick says that the team is naturally aware of the political and economic factors affecting Asia, but believes the best insights come from bottom-up stock picking.

PHI is a stock-picking fund that bears little resemblance to the MSCI All Country Asia ex Japan Index comparative index.

PHI is a stock-picking fund, and its portfolio can differ significantly from its benchmark, the MSCI All Country Asia ex-Japan Index. At the end of December 2024, its active share was 74%. The managers focus mainly on meeting companies and detailed research, following the same process and philosophy for the past 30 years.

Market roundup – Asian valuations remain undemanding

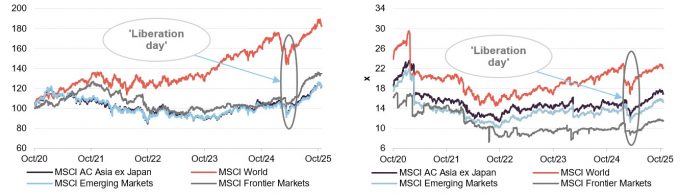

Since our last update in March 2025, global equity markets have seen significant volatility. Markets weakened around “Liberation Day” but have since rebounded as the harshest measures have been rolled back, boosting investor confidence. In this environment, Asia – especially China – has performed strongly, helped by steady domestic activity and improved risk appetite.

Asian equity markets continue to draw investment into sectors linked to long-term growth trends, particularly artificial intelligence and related technologies, where Pacific Horizon has substantial exposure.

Recently, Asia and emerging markets have closed the performance gap with the US, as shown in Figure 1. Valuations have risen across these markets and are now slightly above their five-year averages, though still significantly below their five-year highs.

Figure 1: Index total return performance over five years, rebased to 100

Figure 2: Index F12m P/E ratios over five years

Source: Bloomberg, Marten & Co

Source: Bloomberg, Marten & Co

Managers’ view – Asia remains well-placed to perform

In March, we noted that against a backdrop of a new, vocal US administration and higher market volatility, Asia’s strengths were easy to overlook. PHI’s manager highlights that the region offers low inflation, orthodox economic management, low debt, and, after years of outflows, little speculative money remains. This led us to question why, despite stronger growth prospects, Asian equities still trade at a significant discount to global equities—a trend that continues.

PHI’s managers highlighted two main reasons: China’s economic challenges and a strong US dollar, which was near decade highs against the yuan. However, they believed conditions were shifting in Asia’s favour and an inflection point was near.

Since then, the US dollar has weakened, partly due to US policy, and China is recovering with government support such as subsidies, higher wages, and discounts to boost the economy. Strong exports, some driven by companies stockpiling ahead of tariffs, have helped balance weak domestic demand. Despite ongoing geopolitical risks, PHI’s managers note that most Asian markets have been resilient in the face of these challenges.

On Trump and tariffs

Cost differentials mean large-scale reshoring is not viable.

Trump’s “Liberation day” tariffs initially caused volatility and a sharp sell-off in Asian equity markets as investors reconsidered the impact on trade and supply chains. PHI’s managers now see the longer-term effect as limited. US manufacturing wages are about 10 times higher than in Southeast Asia, so tariffs would need to be extremely high to make reshoring to the US viable. As a result, they believe that labour-intensive manufacturing is unlikely to move back to the US or out of Asia in any significant way.

Despite tariffs, manufacturing unlikely to relocate outside Asia in any meaningful way.

Instead, there has been some diversification within Asia, with countries like Malaysia and Vietnam gaining investment as firms look to reduce reliance on China while keeping access to low-cost labour and established logistics. India was expected to benefit, but new 50% reciprocal tariffs after a dispute over Russian oil imports have dampened that outlook. PHI’s managers remain positive on India’s macro environment, noting both India and China have large domestic markets and are not reliant on US exports. However, they are avoiding Indian IT outsourcers due to US economic challenges and uncertainties from AI.

The main impact of tariffs has been higher import costs for US consumers, reducing their real purchasing power and making US demand more vulnerable to economic slowdowns. This could weigh on Asian exports at the margin, especially as inventories normalise. The only clear structural shift has been at the high end of manufacturing, with companies like TSMC and Samsung Electronics building new semiconductor plants in the US, driven by policy incentives. PHI’s managers see these as exceptions, with Asia’s central role in global manufacturing unchanged.

When we last published, markets were focusing on the reflationary aspects of Trump’s policies, with higher US growth and interest rates expected. While tariffs have raised prices, the growth outlook has worsened, increasing the likelihood of US rate cuts, which generally benefits Asia and growth stocks.

PHI’s managers believe Asian valuations remain attractive despite recent gains. They see the main opportunity in PHI’s portfolio, which includes leading companies in batteries, semiconductors, fintech, gaming, ecommerce, and social networks. As the world becomes more multi-polar, they expect Asia to benefit in the long term.

Investment philosophy and process

The underlying approach

Baillie Gifford believes markets often misprice long-term growth, especially over five years, creating opportunities for outperformance. The firm encourages long-term thinking and focuses on backing strong management and business models, leading to a strategy of “sticking with the winners”.

The company relies on its own research, but also commissions work from local teams, academics, and industry experts. Some companies are examined in detail using investigative journalists and forensic accountants. When speaking with company management, the focus is on long-term prospects.

Managers use the full investment team’s resources and can join meetings with companies outside their usual regions. This helps compare their holdings with competitors in other markets. Each team member has a rotating geographic research focus. Investment ideas are shared with the group, but the lead manager makes final decisions. Roderick and Ben typically spend four to five weeks in Asia each year.

The open-ended investment company (OEIC) and PHI are managed in parallel, but with some differences. The OEIC needs to stay more liquid to handle investor flows, with a cap of 10% in illiquid assets. PHI, within this limit, can hold more illiquid investments and has greater exposure to small-cap companies, while the OEIC leans towards large-caps. Both funds hold many of the same stocks, though in different proportions. PHI can also use gearing and invest in unlisted companies, unlike the OEIC.

Building the portfolio

Baillie Gifford takes an active approach and does not hold stocks simply because they are major parts of an index. There are few restrictions on country, sector or stock weightings, so position size depends on the managers’ confidence in the investment’s risks and rewards. A key principle is to “run the winners,” based on belief in strong business models. Managers also check that the portfolio is not overly exposed to similar themes.

PHI’s managers are allowed to use derivatives to manage risk or adjust market exposure but, in practice, they are not doing so. They also have no plans to hedge the portfolio’s currency exposure.

Sell discipline

A loss of confidence in a company’s management is an immediate reason to sell. Roderick and Ben will also sell if they believe the business model is failing or if the market has already priced in their expectations.

Portfolio allocation

As of 30 September 2025, PHI held 64 companies, up from 62 at the end of 2024. PHI aims for diversification by holding between 40 and 120 companies. Normally, positions below 0.5% of the portfolio require a strong conviction to be kept. At the end of September 2025, 10 holdings were below this level. Over the last financial year, PHI added 15 new holdings and completely sold out of 15 positions.

Portfolio activity

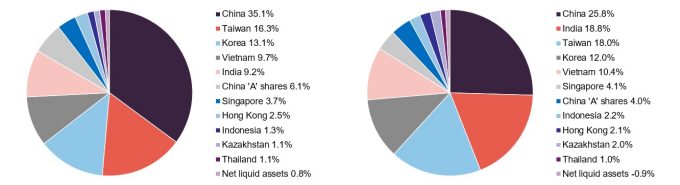

There has been little change in the main themes of PHI’s portfolio since our last note, though exposure to India has continued to fall in favour of China – in part, reflecting the relative performance of these markets. These are the main shifts in geographical allocation (see Figures 3 and 4). While PHI’s managers have been increasing exposure to China, they have also trimmed some Chinese holdings recently, using market movements to diversify PHI’s Chinese stock selection.

The managers have also increased investments in Vietnam, especially in Vietnamese banks, after new pro-growth reforms. They still view Vietnam as Asia’s best long-term growth story. Vietnam has struggled over the past four years due to a government corruption crackdown, which led to a real estate and banking crisis and stalled project approvals. However, the new general secretary, Tô Lâm, is more focused on economic growth and has set ambitious GDP targets, introducing reforms to achieve them.

Figure 3: Geographic allocation as at 30 September 20251

Figure 4: Geographic allocation as at 31 January 20251

Source: Pacific Horizon Investment Trust. Note: 1) As a proportion of gross assets.

Source: Pacific Horizon Investment Trust. Note: 1) As a proportion of gross assets.

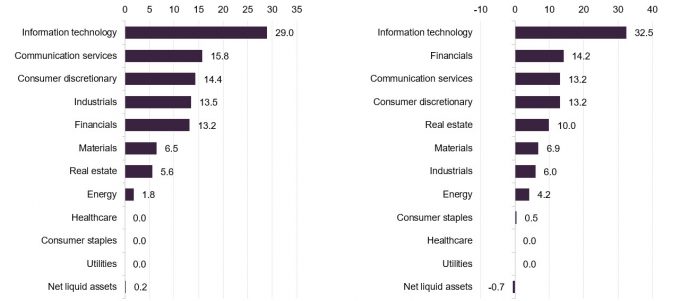

Figure 5: Industry sector allocation at 31 July 20251

Figure 6: Industry sector allocation at 31 July 20241

Source: Pacific Horizon Investment Trust. Note: 1) As a proportion of gross assets.

Source: Pacific Horizon Investment Trust. Note: 1) As a proportion of gross assets.

Korean semiconductor stocks have performed well as AI demand remains strong. The manager notes that Korean inheritance tax laws have kept valuations low, but efforts are underway to address this.

Looking at sector allocations, the biggest change is a 7.5 percentage point increase in industrials exposure. There is also a 2.6 percentage point rise in communication services and a smaller increase in consumer sectors.

Discretionary increased by 1.2 percentage points. The largest reductions were in real estate (down 4.4 percentage points) and information technology (down 3.5 percentage points). There were also notable decreases in energy (down 2.4 percentage points) and financials (down 1.0 percentage point). Changes in other sectors were less than one percentage point.

Top 10 holdings

Figure 7: Top 10 holdings as at 30 September 2025

| Holding | Sector | Business focus | Country | Allocation 30 September 2025 (%) | Allocation 31 January 2025 (%) | Percentage point change |

|---|---|---|---|---|---|---|

| TSMC | Technology | Internet services | China | 11.3 | 10.8 | 0.5 |

| Tencent | Technology | Online gaming/social networking | China | 8.2 | 4.9 | 3.3 |

| Samsung Electronics | Technology | Electrical equipment manufacturer | Korea | 5.7 | 5.6 | 0.1 |

| SK Square | Technology | Electronic components | Korea | 4.2 | – | 4.2 |

| Zijin Mining | Materials | Gold and copper miner | China | 3.5 | 2.7 | 0.8 |

| ByteDance | Communications | Owner of TikTok | China | 3.3 | 3.1 | 0.2 |

| Sea Limited | Communication services | Online gaming/ecommerce | Singapore | 3.3 | 3.4 | (0.1) |

| Alibaba | Technology | E-commerce | China | 3.3 | – | 3.3 |

| MMG | Materials | Chinese copper miner | HK/China | 3.0 | 2.2 | 0.8 |

| EO Technics | Technology | Semiconductor laser markers | Korea | 2.2 | 2.0 | 0.2 |

| Total of top 5 | 32.9 | 28.1 | 4.8 | |||

| Total of top 10 | 48.0 | 42.3 | 5.7 |

Figure 7 shows PHI’s top 10 holdings as at 30 September 2025 and changes since 31 January 2025, the last time we published. New entries to the top 10 are SK Square, Alibaba, MMG and EO Technics, while Equinox India Developments, Daily Hunt, Accton Technology and PDD Holdings have dropped out. The manager has also increased portfolio concentration, as shown in Figure 7.

We highlight some notable changes below. Many other holdings have been covered in previous notes – see page 23 for details. As discussed in the performance section on page 10, PHI’s exposure to AI and technology stocks has supported performance recently. In semiconductors, PHI has benefited from significant holdings in companies such as TSMC, Samsung, SK Hynix (mainly held through SK Square, which trades at a notable discount to its net asset value) and EO Technics remain key holdings. In technology, Tencent, ByteDance (TikTok), and Alibaba have performed well. Alibaba was reintroduced as the managers believe the Chinese government’s stance towards tech firms has improved, and see strong potential in Alibaba’s cloud and AI businesses.

MMG and Zijin Mining have risen on the back of higher copper prices. Exposure to Equinox India Developments was reduced to increase investment in China. Daily Hunt (part of VerSe Innovation) is a private holding whose valuation was cut as its “Josh” video app has not grown as expected. The company has restructured and made layoffs to improve efficiency and aims for profitability.

Other holdings

PHI’s managers note that Meituan, China’s leading food delivery company with about 70% market share, has faced pressure from rising competition as Alibaba and JD.com enter the market. While the next 18 months may be tough, they believe Meituan’s strong cash position and funding will help it withstand the increased competition and it could come out stronger.

The managers have increased their holding in CATL through its Hong Kong IPO, viewing it as a global battery leader with a 40-50% market share. Although battery production is becoming more standardised, CATL’s scale and investment in research, such as its Shenxing Pro battery (which charges to a 478km range in 10 minutes), give it a technological edge. CATL remains profitable while many competitors are not. The managers recently sold CATL H-shares at a premium and switched to the A-shares.

Baidu has been sold due to ongoing stagnation and concerns that its main search advertising business is threatened by AI. Despite heavy investment in AI and autonomous driving, PHI’s managers see rivals like Tencent and Alibaba in stronger positions. They have replaced Baidu with Pony AI, which they believe is better placed in autonomous driving.

Sea Limited, a long-term PHI holding, has performed well, driven by strong growth across its main businesses: e-commerce (Shopee), digital entertainment (Garena), and digital finance (SeaMoney). Improved advertising revenue from Shopee has been a key factor. The business is now profitable and much less risky, with growth in its fintech division and strong results from its mobile game Free Fire. It is also expanding well in Brazil. Managers had doubts about its ability to compete with Mercadolibre, but note it is generating US$250m in EBITDA each quarter. They believe the market is overlooking this part of the business, which could become the most valuable. They see it as the leading consumer-focused stock in Southeast Asia.

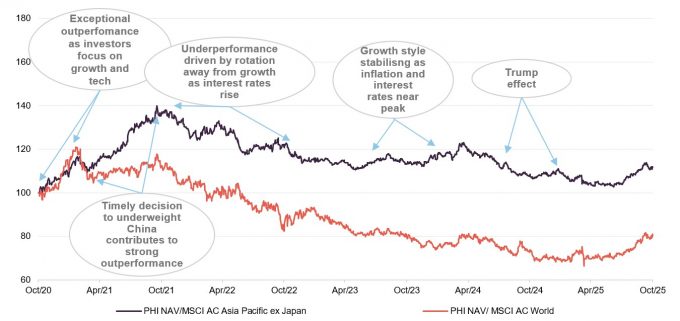

Performance – now benefitting from rotation away from India into China

PHI has a strong long-term track record of outperforming both its MSCI AC Asia Pacific ex Japan benchmark and the MSCI AC World Index, as shown in Figure 9. Recent performance has also been strong, with PHI now leading its peer group across all periods shown in Figure 9 and being the top-performing fund in share price total return over most periods (see Figure 10 on page 13).

Figure 8: PHI’s total return NAV performance relative to its comparative benchmark (MSCI AC Asia ex Japan) and the MSCI AC World, over five years to 31 October 2025

Source: Bloomberg, Marten & Co

PHI’s performance benefited from well-timed decisions to reduce its exposure to China in 2021 and increasing exposure to India and then, in 2024, to reduce China in favour of India.

Trump’s tariff announcements in early 2025 initially hurt growth stocks, but markets rebounded strongly from May. Chinese stocks and Korean semiconductor companies have since performed well.

PHI’s managers expect continued volatility but believe their holdings will outperform companies with limited growth in the long run. The portfolio has become more focused, but the core investment approach remains the same.

Figure 9: Cumulative total return performance over periods ending 31 October 2025

| 1 month (%) | 3 months (%) | 6 months (%) | 1 year (%) | 3 years (%) | 5 years (%) | 10 years (%) | Manager tenure1 (%) | |

|---|---|---|---|---|---|---|---|---|

| PHI NAV | 7.4 | 22.3 | 42.0 | 30.2 | 52.8 | 55.9 | 374.7 | 402.8 |

| PHI share price | 5.7 | 21.1 | 40.1 | 36.9 | 51.7 | 27.2 | 360.6 | 406.2 |

| MSCI AC Asia Pacific ex Japan | 7.1 | 13.9 | 31.9 | 26.4 | 65.1 | 39.6 | 166.8 | 179.8 |

| MSCI AC World | 4.8 | 9.3 | 23.6 | 20.1 | 57.2 | 94.9 | 243.5 | 296.2 |

| Peer group NAV2 | 6.7 | 13.9 | 29.3 | 17.9 | 47.8 | 47.8 | 243.4 | 282.2 |

| Peer group share price2 | 5.7 | 13.5 | 30.4 | 23.3 | 48.3 | 37.4 | 237.7 | 279.1 |

Peer group comparison – Asia Pacific sector

PHI is a member of the AIC’s Asia Pacific sector, which comprises four members, all of which are illustrated in Figures 10 and 11. All four were members of the peer group when we last published. Members of the Asia Pacific sector will typically have:

- over 80% invested in quoted Asia Pacific shares;

- less than 80% in any single geographic area;

- an investment objective/policy to invest in Asia Pacific shares;

- a majority of investments in medium to giant cap companies; and

- an Asia Pacific benchmark.

Please click here for an up-to-date peer group comparison of PHI versus its Asia Pacific peers.

It is worth noting that, whilst the peer group is fundamentally capital-growth-focused, the Baillie Gifford approach has traditionally been characterised by a particularly strong emphasis on growth.

Peer group performance

As mentioned in earlier notes (see page 23), PHI’s focus on growth stocks has benefited it over the long term, although this approach has recently faced significant headwinds. When interest rates started rising in 2022 to combat higher inflation, growth companies struggled but, this year, sentiment has improved. Trump’s “Liberation Day” tariff announcement initially led to a short-term increase in business activity as companies stockpiled in anticipation of higher costs. Now, markets expect that slower global growth will lead central banks to cut rates, which would support growth stocks. PHI has benefited from this environment, ranking first out of four for NAV total return in all periods shown in Figure 10, except for the three-year period, which reflects much of the earlier growth sell-off.

We believe longer-term periods are more appropriate for assessing a long-term strategy like PHI’s. PHI’s managers aim to invest in the top 20% of growth companies in Asia Pacific and look for businesses they believe can double earnings over five years.

Figure 10: Peer group cumulative NAV total return performance to 31 October 2025

| 1 month (%) | 3 months (%) | 6 months (%) | 1 year (%) | 3 years (%) | 5 years (%) | 10 years (%) | |

|---|---|---|---|---|---|---|---|

| PHI | 7.4 | 22.3 | 42.0 | 30.2 | 52.8 | 55.9 | 374.7 |

| Pacific Assets | 5.9 | 6.2 | 12.0 | (1.1) | 15.0 | 41.5 | 145.6 |

| Schroder Asia Total Return | 6.6 | 12.8 | 30.7 | 18.1 | 61.7 | 50.7 | 250.9 |

| Schroder AsiaPacific | 7.1 | 14.2 | 32.6 | 24.5 | 61.6 | 43.1 | 202.5 |

| PHI rank | 1/4 | 1/4 | 1/4 | 1/4 | 3/4 | 1/4 | 1/4 |

| Sector arithmetic avg. | 6.7 | 13.9 | 29.3 | 17.9 | 47.8 | 47.8 | 243.4 |

The average market cap for the peer group is now £620.3m, up 17% from £530.2m at the last update. PHI remains the second-largest fund by market capitalisation.

PHI’s ongoing charges ratio has risen slightly over the past two years but was falling for several years before that. At 0.75%, it is still the lowest in the sector, with the next lowest being Schroder Asia Total Return at 0.88%. The peer group’s average ongoing charges ratio has edged up from 0.90% to 0.91%.

All funds in the group continue to trade at a discount, though the sector average discount has narrowed slightly from 9.7% to 9.6% as of 20 November 2025. PHI usually trades at a small premium to the sector average, likely due to its strong long-term performance and the board’s share buybacks. PHI’s current discount is 1.1 percentage points above the sector average, which may present an extra opportunity.

As noted before, PHI’s dividend yield remains the lowest in the sector, reflecting its focus on capital growth. PHI pays dividends only as needed to maintain its investment trust status.

Figure 11: Peer group comparison – size, fees, discount, yield and gearing as at 20 November 2025

| Market cap (£m) | St. dev. of NAV over 5 years | Ongoing charges (%) | Perf. fee | Premium/ (discount) (%) | Dividend yield (%) | Gross gearing (%)2 | Net gearing (%)2 | |

|---|---|---|---|---|---|---|---|---|

| PHI | 626.2 | 17.80 | 0.75 | No | (9.6) | 0.20 | 7.4 | 7.4 |

| Pacific Assets | 425.1 | 12.99 | 1.10 | No | (10.0) | 1.08 | Nil | (4.4) |

| Schroder Asia Total Return | 527.5 | 15.16 | 0.90/1.501 | Yes | (0.7) | 2.04 | 6.5 | 5.3 |

| Schroder AsiaPacific | 868.3 | 14.17 | 0.88 | No | (11.0) | 1.89 | 4.0 | 4.2 |

| PHI rank3 | 2/4 | 4/4 | 1/4 | 3/4 | 4/4 | 4/4 | 4/4 | |

| Sector arithmetic avg. | 611.8 | 15.03 | 0.91/1.061 | (7.8) | 1.30 | 4.5 | 3.1 |

PHI’s net gearing has increased from one of the lowest in the sector to the highest, showing the managers’ confidence in the opportunity. However, at 6.8%, its gearing remains modest. PHI’s NAV returns are still the most volatile among peers, but this volatility is not high and is balanced by its strong long-term performance.

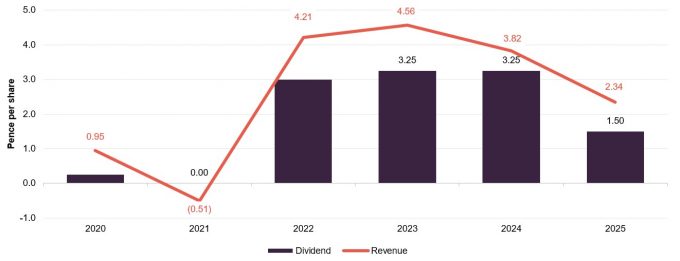

Dividend

Capital-growth-focused; any dividend is the minimum required to maintain PHI’s investment trust status.

PHI’s main aim is capital growth, not income. Any dividend is paid once a year after AGM approval. The board has made it clear that investors should not consider investing in the company if they require income from their investment (in four of the last 10 years – 2017, 2018, 2019 and 2021 – PHI did not pay a dividend at all). In years with a revenue shortfall, PHI is not required to pay a dividend and does not plan to use reserves to maintain payouts.

For the year ended 31 July 2025, PHI reported a revenue surplus of £2.1m or 2.34p per share, down 38.7% from £3.6m or 3.82p per share the previous year. As a result, the board proposed a final dividend of 1.50p per share, to be paid on 1 December 2025. This represents a dividend yield of 0.20% based on a share price of 752.0p as at 20 November 2025, and is 53.8% lower than last year.

Figure 12: PHI ordinary dividends over the last five financial years (ended 31 July)

Source: Pacific Horizon Investment Trust, Marten & Co

Premium/(discount)

PHI aiming to maintaining discount in single digits

For some years, PHI has used share buybacks to help moderate its discount. In April, PHI introduced a five-year performance-related tender and stated it would continue buybacks, aiming to keep the discount to NAV in single digits during normal market conditions. This approach has worked, with the discount averaging 9.6% since the announcement and peaking at 11.1%.

As of 20 November 2025, PHI traded at a 9.6% discount, narrower than its one-year average of 11.1%, close to its three-year average of 9.7%, but wider than its five-year average of 4.9%. Over the past year, the discount ranged from 7.8% to 15.9%.

As noted in previous reports, broader macroeconomic factors have typically had a bigger impact on PHI’s discount than company-specific ones. The discount tends to widen when markets expect higher inflation and interest rates, which weigh on growth stocks, and narrows as sentiment improves. Periods of risk aversion, especially concerns over Asia, have also led to a wider discount. The new policy should help limit further widening during market downturns.

Many of the events affecting the discount have been covered in earlier notes, but we previously highlighted the potential for the discount to narrow, especially if Trump’s tariffs turned out to be less severe than expected and if an improvement in China and Asia’s performance came through. Broadly speaking, this has come to pass, helping to narrow PHI’s discount and that of its peers. With signs that US interest rates may need to fall to support its weakening economy, there could be further gains to come and PHI, with its strong focus on growth, looks well placed to benefit. We expect this could lead to the discount narrowing further, and if China and Asia outperform as PHI’s managers anticipate, PHI could move to a premium rating and resume issuing stock.

Figure 13: PHI premium/(discount) over five years

Source: Morningstar, Marten & Co

Performance-related conditional tender offer in 2030

On 16 April 2025, PHI announced a 25% tender offer for shareholders in 2030 if the trust underperforms the MSCI All Country Asia ex Japan Index (total return in sterling) between 31 March 2025 and 31 March 2030. This conditional tender is expected to encourage managers to outperform and offers shareholders reassurance of a partial exit near NAV if performance lags over the next five years.

Structure

Fees and costs

Baillie Gifford & Co Limited is PHI’s alternative investment fund manager and has delegated portfolio management to Baillie Gifford & Co. PHI charges a tiered management fee: 0.75% on the first £50m of net assets, 0.65% on the next £200m, and 0.55% on any amount above that.

Management fees are calculated and paid quarterly in arrears, with no performance fee. The managers can end the agreement with six months’ notice, while the company can do so with three months’ notice. Baillie Gifford & Co Limited also provides company secretarial services as part of the management agreement.

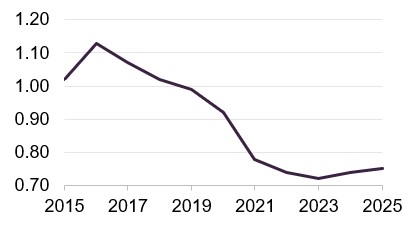

Figure 14: Ongoing charges ratio (%)1

Source: Pacific Horizon Investment Trust Note: 1) For financial years ended 31 July.

PHI’s ongoing charges ratio had been falling due to its tiered fee structure, a lower management fee, and strong share issuance up to the end of 2021. However, it has risen slightly by 3 basis points over the last two years, from 0.72% in FY2023 to 0.75% in FY2025. PHI’s net assets have recovered strongly in the last six months, which should help reduce the ongoing charges ratio again. PHI still has the lowest ongoing charges ratio in its peer group, at 16 basis points below the sector average.

Capital structure

PHI has a simple capital structure with one class of ordinary share in issue.

PHI has a straightforward capital structure with only one type of ordinary share. These shares are listed on the London Stock Exchange’s main market. As of 20 November 2025, there were 92,074,961 shares issued, with 8,892,711 held in treasury, leaving 83,182,250 shares with voting rights.

Each year, the company seeks approval to buy back up to 14.99% of its shares at a discount to NAV and to issue up to 10% of its share capital at a premium to NAV. These powers help the board manage PHI’s share price premium or discount.

Gearing

PHI has a £60m multi-currency revolving credit facility.

PHI has a £60m multi-currency revolving credit facility with The Royal Bank of Scotland International, expiring in March 2026. The board sets gearing limits, currently from -15% (net cash) to +15%.

At the end of October 2025, PHI’s gross and net gearing were both 7.4%, up from 5.2% and 3.1% at the end of February 2025. The main loan conditions are that borrowings must stay below 30% of adjusted net asset value, and net asset value must be at least £300m. There is a 0.4% fee for unused amounts.

Major shareholders

Figure 15 shows PHI has a strong retail presence, with major platforms making up over 40% of its share register. Wealth managers hold more than 20%. Since our last update, Swiss private bank J. Safra Sarasin, known for its focus on sustainability, has increased its holding.

Figure 15: Major shareholders as at 30 October 2025

Figure 16: Percentage point changes in shareholdings since 12 March 20251

Source: Bloomberg, Marten & Co

Source: Bloomberg, Marten & Co. Note: 1) The date of the shareholder data used when we last published on PHI.

Five-yearly continuation votes

The next continuation vote is due at the 2026 AGM.

Shareholders can vote on whether the company should continue every five years. The last vote at the 2021 AGM approved PHI’s continuation. The next vote will take place at the 2026 AGM.

Financial calendar

PHI’s financial year ends on 31 July. Annual results are usually published in September, with interim results in March. The AGM takes place in November, and any annual dividend is paid soon after.

Management team

Roderick Snell joined Baillie Gifford in 2006 and became a partner in 2023. He has managed the Baillie Gifford Pacific Fund since 2010 and has led PHI’s portfolio since June 2021, after serving as deputy manager from 2013. Before joining the emerging markets team, he worked in the UK and European equity teams. He also co-manages the emerging markets leading companies strategy. Roderick holds a BSc (Hons) in Medical Biology from the University of Edinburgh.

Ben Durrant joined Baillie Gifford in 2017 and has worked in the UK, global discovery, and private markets teams before moving to emerging markets. Before this, he was at RBS in group strategy and corporate finance. Ben is a chartered accountant, a CFA charterholder, and has a BSc (Hons) in Mathematics from the University of Edinburgh. He has co-managed the Baillie Gifford Pacific Fund since 2021.

Board

All directors submit themselves for re-election annually.

PHI’s board has five non-executive directors, all independent from the investment manager and not serving together on other boards. Directors stand for re-election at the first AGM after their appointment and then each year. Angela Lane is the longest-serving director with seven years, and the average director tenure is 5.3 years.

Directors’ fees

The company’s articles of association set a £200,000 cap on total directors’ fees, and any increase would need shareholder approval. This year, directors’ fees rose by 3.5% compared to last year, bringing the total to £178,540, well within the set limit.

Figure 17: Board member – length of service and shareholdings

| Director | Position | Date of appointment | Length of service (years) | Annual fee (£)1 | Share-holding 2 | Years of fee invested3 |

| Roger Yates | Chairman | 13 March 2024 | 1.7 | 46,580 | 15,000 | 2.4 |

| Angela Lane | Audit committee chairman and senior independent director | 1 October 2018 | 7.1 | 38,810 | 8,923 | 1.7 |

| Sir Robert Chote | Director | 25 November 2020 | 5.0 | 31,050 | 500 | 0.1 |

| Wee-Li Hee | Director | 1 June 2020 | 5.5 | 31,050 | 10,000 | 2.4 |

| Joe Studwell | Director | 9 November 2018 | 7.0 | 31,050 | 5,000 | 1.2 |

| Average (service length, annual fee, shareholding, years of fee invested) | 5.3 | 35,708 | 7,885 | 1.6 | ||

Recent share purchase activity by directors

Since our last update in March 2025, directors’ holdings have not changed. All directors have personal investments in the trust, with an average fee investment of 1.6 years. We view this positively, as it shows commitment to PHI and aligns directors’ interests with shareholders.

Roger Yates (chairman)

Roger was chief executive of Henderson Global Investors from 1999 to 2008, after earlier fund management roles at Invesco/LGT and Morgan Grenfell Asset Management. He is currently senior independent director at Mitie Group, chair of British Biotech Trust, and a non-executive director at Jupiter Fund Management. Previously, he was senior independent director at St James’s Place and IG Group, chair of Electra Private Equity, and a non-executive director at JP Morgan Elect.

Angela Lane (audit committee chair and senior independent director)

Angela became PHI’s audit committee chair and senior independent director on 10 November 2020. She is a qualified accountant with 18 years’ experience as a private equity investor at 3i Plc. Angela has held various non-executive and advisory roles with small and mid-sized companies across different industries. She is currently a non-executive director and audit committee chair at BlackRock Throgmorton Trust Plc and Seraphim Space Investment Trust Plc. Previously, she was non-executive chairman of Huntswood CTC and a non-executive director and audit committee chair at Dunedin Enterprise Investment Trust Plc.

Sir Robert Chote (director)

Sir Robert is an economist, journalist and academic. He became chairman of the Northern Ireland Fiscal Council in 2021 and will become President of Trinity College, Oxford, in November 2025. He has chaired the UK Statistics Authority since 2022 and will step down in September 2025. Previously, he was chairman of the Office for Budget Responsibility from 2010 to 2020, director of the Institute for Fiscal Studies from 2002 to 2010, advisor to the International Monetary Fund from 1999 to 2002, and economics editor at the Financial Times from 1995 to 1999. He is a visiting professor at King’s College London’s Department of Political Economy and serves on advisory boards at the Warwick Manufacturing Group and the Centre for Economic Performance at the London School of Economics.

Wee-Li Hee (director)

Wee-Li is an experienced Asian analyst and fund manager, and a CFA Charterholder. Raised in Singapore, she speaks fluent Mandarin and studied at the University of Leeds and the London School of Economics. She joined First State Investments in Singapore as an analyst after graduating in 2002, then moved to the Edinburgh office in 2005. She co-managed the Scottish Oriental Smaller Companies Trust Plc, becoming lead manager in 2014 before returning to a co-manager role in 2017 for family reasons. She retired at the end of 2019 and is now a director at Melville Paisley Investments.

Joe Studwell (director)

Richard Frank (“Joe”) Studwell has spent over 25 years working in East Asia as a journalist, independent researcher at Dragonomics, and author under the name of Joe Studwell. His published works include Asian Godfathers: Money and Power in Hong Kong and South East Asia and How Asia Works: Success and Failure in the World’s Most Dynamic Region.

SWOT analysis

Figure 18: SWOT analysis for PHI

| A sharp focus on growth investing within the Asia ex-Japan region, providing investors with exposure to high-quality growing companies. The managers take a long-term view and do not waver even if market conditions are unfavourable. |

| The board and the managers have demonstrated a clear prioritising of shareholder interests, such as through the five-year performance-related tender offer in 2030 and the single-digit discount control policy. |

| PHI suffers from periods when absolute and/or relative performance is difficult, particularly when the market backdrop is unhelpful for growth investors, such as the period of higher inflation and interest rates from late 2021. Asia tends to suffer when interest rates rise in the US, for example. |

| Low income yield, although this should be well understood by shareholders. |

| There are increasing signs that growth investing is coming back into favour, against a backdrop of interest rate cuts, both in the US and globally. |

| Investors appear to be looking more favourably at Asia and at growth investing more generally. After a difficult couple of years, China is recovering, while policy and fiscal uncertainty in the US has been driving a rotation away from that market to other regions. |

| The market could once again turn against growth investing, particularly if inflation re-emerges as a threat and nominal GDP growth picks up. However, there is a risk of stagflation in more developed markets. This could limit the capacity for interest rate rises, and Asia would likely benefit from this scenario. |

| Single stock issues could hurt performance, given the unapologetically bottom-up nature of the fund. |

Bull vs bear case

Figure 19: Bull vs bear case for PHI

| Performance | Absolute performance has been positive over all time periods and PHI’s NAV total returns are top of its peer group for all periods, with the exception of three years – a period where inflation and interest rates have been elevated, particularly in developed markets. Inflation is edging up in the US, but the growth outlook has also deteriorated, limiting the capacity to raise interest rates, while China has also been recovering. PHI looks well-placed for further outperformance. | PHI has had a difficult few years of relative underperformance. This has largely been due to growth investing being out of favour against a backdrop of rising inflation and interest rates. Decisions to increase the exposure to China and semiconductors early in 2024 also weighed on PHI’s performance last year, but this has since reversed. |

| Dividends | PHI focuses on capital growth rather than income and the annual dividend is paid purely to maintains its investment trust status. | PHI’s board has made it clear that investors should not consider investing in the company if they require income from their investment. |

| Outlook | Asia and growth investing appear to be coming into favour with investors, which should suit PHI. | Growth investing generally benefits from subdued inflation and interest rates, while capital flows in and out of Asia tend to be sensitive to US interest rates. Although US inflation has been edging up, the direction of interest rates still looks to be down for now. |

| Discount | The board has a control mechanism to keep the discount in single figures, which has already had a material impact. The current discount could narrow or even move to a premium if the market environment is positive for PHI and its stock picks look like making a comeback. | The discount could widen further and the control mechanism come under pressure if inflation picks up, pushes up interest rates, and this leads to a renewed period of underperformance for growth investing. |

Previous publications

Readers interested in further information about PHI may wish to read our previous notes (details are provided in Figure 20 below). You can read the notes by clicking on them in Figure 20 or by visiting our website.

| Title | Note type | Publication date |

|---|---|---|

| Invest in Asian growth | Initiation | 21 March 2016 |

| Brave new world | Update | 10 October 2016 |

| Top of the pops! | Annual overview | 30 October 2017 |

| Pause for breath? | Annual overview | 8 November 2018 |

| 2018 re-calibration paying off | Annual overview | 8 November 2019 |

| Powered by technology | Annual overview | 20 January 2021 |

| Blistering performance | Annual overview | 25 November 2021 |

| Convergence opportunity | Annual overview | 8 December 2022 |

| Consistent growth and quality bias | Annual overview | 6 December 2023 |

| Inflection point approaching? | Annual overview | 19 March 2025 |

IMPORTANT INFORMATION

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Pacific Horizon Investment Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it. Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.