Jockeying for position

Weakened risk appetite among investors as macroeconomic headwinds persist has seen the technology sector suffer. As investors retreated to the sector titans (stocks such as Microsoft and Apple), Polar Capital Technology’s (PCT’s) underweight position in these companies has seen it underperform its benchmark over the 12 months to the end of November, while its exposure to ‘next-generation’ software companies has also been a source of underperformance versus legacy stocks as IT budgets are disproportionately squeezed. PCT’s manager, Ben Rogoff, is undeterred by this and plans to take advantage of valuation compression to double-down on its ‘next-gen’ thematic position and will continue the portfolio’s pivot towards secular growth stocks, focusing on companies with strong balance sheets that can perform well in a more challenging backdrop.

Recent inflation data and a more dovish central bank rhetoric suggests that peak inflation may have been hit, which should result in an easing of interest rate expectations and a raising of investor appetite.

Global growth from tech portfolio

PCT aims to maximise long-term capital growth through investing in a diversified portfolio of technology companies around the world, diversified across both regions and sectors within the overall investment objective to reduce investment risk.

Fund profile

PCT aims to maximise long-term capital growth through investing in a diversified portfolio of technology companies around the world, diversified across both regions and sectors. PCT launched in December 1996 as Henderson Technology Trust and, following a change of manager, became Polar Capital Technology Trust in April 2001.

More information can be found at the trust’s website: www.polarcapitaltechnologytrust.co.uk

Management arrangements

PCT’s AIFM is Polar Capital LLP and the lead manager assigned to the trust is Ben Rogoff, a partner in Polar Capital LLP. He is supported by a team of eight technology specialists, including another partner, Nick Evans. Polar believes that this is one of the best-resourced teams dedicated to this sector within Europe. In addition to PCT, the team also manages two open-ended funds, Polar Capital Global Technology Fund and the Automation & Artificial Intelligence Fund. Collectively, these funds had AUM of $7.8bn at 30 September 2022.

Ben joined the team from Aberdeen in 2003, having started his career in the years running up to the technology boom. The events surrounding the collapse of the tech bubble have influenced the way in which he manages money. One important lesson is that there is limited permanence in the technology sector; it is forever engaged in a process of creative disruption. Change in the sector is a non-linear process. Once-great companies can disappear and minnows can become giants.

Nick Evans joined the team from Framlington in 2007. He complements Ben in that Nick has a more bottom-up approach to selecting stocks, whereas Ben has a bias to a top-down stance.

Market overview – valuation reset

Aggressive quantitative tightening action has continued as policymakers try to get control over persistently high inflation. However, hopes of a central bank pivot or at least a slower pace of rate hikes have increased after the Bank of Canada and Royal Bank of Australia raised rates by less than expected in October and a more dovish rhetoric was used by the European Central Bank during its recent rate hike. The narrative that inflation may have peaked has grown stronger on inflation data in the US, where CPI eased to 7.7% in October, from 8.2% in September and below the 8% forecast.

Despite positive news on inflation in the US, Federal Reserve (Fed) chairman Jerome Powell has indicated that hopes for it to press the pause button on its quantitative tightening policy were premature. However, markets were buoyed by commentary from San Francisco Fed president Mary Daly, who suggested that the time had come “to start talking about stepping down” the pace of rate hikes, while the FOMC meeting in November noted that they will “take into account the cumulative tightening of monetary policy…and economic and financial developments” when determining the pace of future increases. Ben believes that the Fed is coming under increasing political pressure to slow the pace of rate hikes given the lagged effect of interest rate hikes and the risk of causing high unemployment.

A higher interest rate environment and weakened risk appetite among investors has led to a material valuation reset in the technology sector. The manager says that the highest growth software companies have seen their enterprise value (EV)/forward sales multiple compress to 8.9x, below the 17.5x average of the past five years and more than 75% below the highs of 38.5x in February 2021. Valuations are back in line with the five-year average between 2014 and 2018 (8.8x). Companies with high revenue growth (between 15% and 30%) have not been spared, Ben adds. At 5.4x EV/forward sales, they now trade 46% below their trailing five-year average multiple (10x). This is a healthy discount to the average software takeout multiple in 2022 of 7.6x, according to Jefferies, and close to a compelling entry point if a deep US recession is avoided.

We should get a sense of whether the Fed believes that the US has reached peak inflation (and therefore peak interest rate expectations) at its next meeting in December, and if so, investor sentiment should rise. Despite near-term macro and market turbulence, Ben believes that the worst of EV/forward sales multiple compression is likely behind us, and secular tailwinds remain robust.

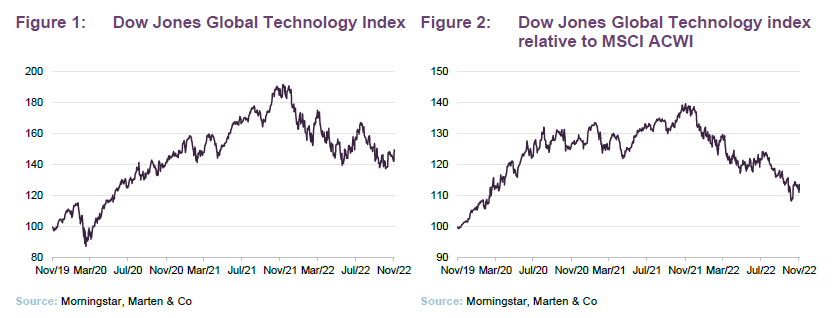

Investor sentiment towards the technology sector has remained extremely negative as central banks tightened financial conditions to contain inflationary pressures, leading to its underperformance of the broader market over 2022, as shown in Figure 2.

Secular growth stocks at reasonable prices

PCT’s manager rotated away from cyclicals in favour of secular growth stocks earlier this year (as we outlined in our update note in May), exploiting the compression in valuations. It says that it intends to use the continued weakness in valuations to further tilt the portfolio towards secular growth stocks, as it returns to a more fully invested position (at the end of November cash and equivalents amounted to 6.0% of the portfolio). Ben adds that this is an interesting opportunity to accumulate growth assets at reasonable prices and it will focus on companies with strong balance sheets that can perform well in a more challenging backdrop. As such, the company has recently purchased several new entry level positions in stocks where valuations had previously been too high for it.

Ben describes the current macroeconomic environment as both highly unusual and very challenging with policymakers focused on restoring credibility and inflation back to long-term averages at a time of full-employment and a relatively robust US economy. However, the risk of a US recession appears to be rising according to the spread between two-year and 10-year US Treasury yields which is currently -82bps – the most negative it has been for at least 30 years. Technology valuations have now reverted back towards five- and 10-year averages, having traded at elevated levels during the pandemic.

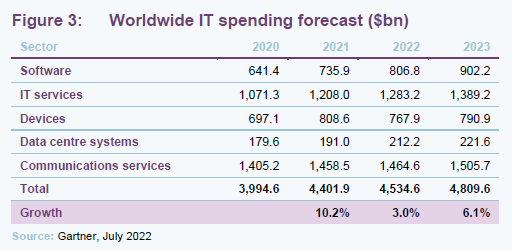

In the meantime, growth in IT budgets has slowed. IT spending is forecast to reach $4.5trn in 2022 representing 3% year-on-year growth, as shown in Figure 3, down from earlier estimates of 5.9% growth. However, the manager says that long-term trends that has seen IT budgets and spending priorities reallocated in favour of new ‘next-generation’ technologies – such as cloud, security, digital transformation, collaboration and AI – at the expense of legacy technologies, appear unchanged.

However, given the macroeconomic backdrop, the share prices of ‘next-generation’ software and other long-duration stocks have suffered heavily. Ben is cautious; he says that a different mentality may be setting in with companies looking to save money on IT budgets, rather than spending on technology to reduce costs. A tighter IT spending environment may be slowing the shift of existing workloads to the cloud given the up-front costs involved. The public cloud saw a slowdown in growth during the last quarter, with the overall market growing 31.5% (down from 36% the previous quarter).

Incumbent, legacy technology companies such as IBM and Oracle have been less affected by a slowdown in IT spending. Large enterprises have not shown much weakness and as yet have not pulled back on IT spend. Ben says that this has slowed the pace of disruption of the incumbents, but adds that disruption is still very much on the cards. The manager won’t buy into legacy incumbents, but will continue to look to add carefully to higher-growth software names that have strong balance sheets and the ability to grow through a more challenging macroeconomic environment. When the macro improves and confidence returns to the market, the manager says that it can meaningfully increase exposure to ‘next-generation’ software companies, such as Bill.com, Confluent, and GitLab.

Many of the largest players in the internet sector have been impacted by weak digital advertising spend. In third-quarter earnings results, Alphabet reported revenue growth of 6% (2% below expectations) due in part to lower advertising budgets, while YouTube declined 2% (against an expectation of a 5% rise), reflecting a pullback in spend in both brand and direct response, as well as competition from TikTok. Meta (Facebook) also reported disappointing earnings results, in part due to a weak advertising market.

Revenue guidance in the semiconductor sector has also been cut, with several industry bellwethers confirming that the semiconductor industry is in a downcycle. Intel lowered its third quarter guidance to the low end of the previously-given range of $15bn-$16bn, as business has “deteriorated”, while Samsung warned: “The second half of this year looks bad, and as of now, next year doesn’t really seem to show a clear momentum for much improvement”.

The semiconductor sector is undergoing an inventory correction that may hit revenue. It has also been hit by the US government restricting the sale of both semiconductors and semiconductor manufacturing equipment into China. This impacts companies such as Advanced Micro Devices, NVIDIA, KLA Tencor and ASML to varying degrees, the manager says. Perhaps the most detrimental rule, according to Ben, is the newly introduced control on ‘US persons’ who are now restricted from specific activities that support the development or production of restricted semiconductors in China without a licence. The aim is primarily to limit China’s access to advanced computing for its military modernisation, including nuclear weapons development, advanced intelligence collection/analysis and surveillance. The manager believes that this will likely have wider ramifications given that the precise end use of such items cannot be determined by the ‘US person’.

Now that third-quarter earnings results are largely complete, Ben hopes that investors will start to focus on compelling 2024 valuation multiples once they have a higher degree of confidence around estimates for 2023. The manager says that it is starting to see attractive opportunities emerging, and if inflationary pressures abate and greater macroeconomic stability returns, it is in a good place to act on it.

Capturing technological change

The technology sector can offer fantastic rewards but can also be unforgiving when you get it wrong. We explored the thinking behind the manager’s approach to stock selection in our initiation note, but to recap:

Avoiding the riskiest stocks and the savage adverse swings in sentiment that accompany missed profit or revenue expectations can make a big difference to long-term returns. For investment managers, it is as much about damage limitation as spotting the next big thing.

Technologies go through cycles, like any other product. New entrants tend to displace yesterday’s winners. Sometimes these big companies can reinvent themselves, but usually not. The best returns can be made as a product or service moves from the early adoption phase to the mass adoption phase. The manager believes that sell-side analysts find it hard to model the near-exponential growth that businesses can achieve as penetration of a product or service shifts from around 5% to around 30%, and this presents an opportunity for active managers. It is also important to exit companies reliant on mature, mainstream technologies. Products and services can see a dramatic collapse in sales and profitability.

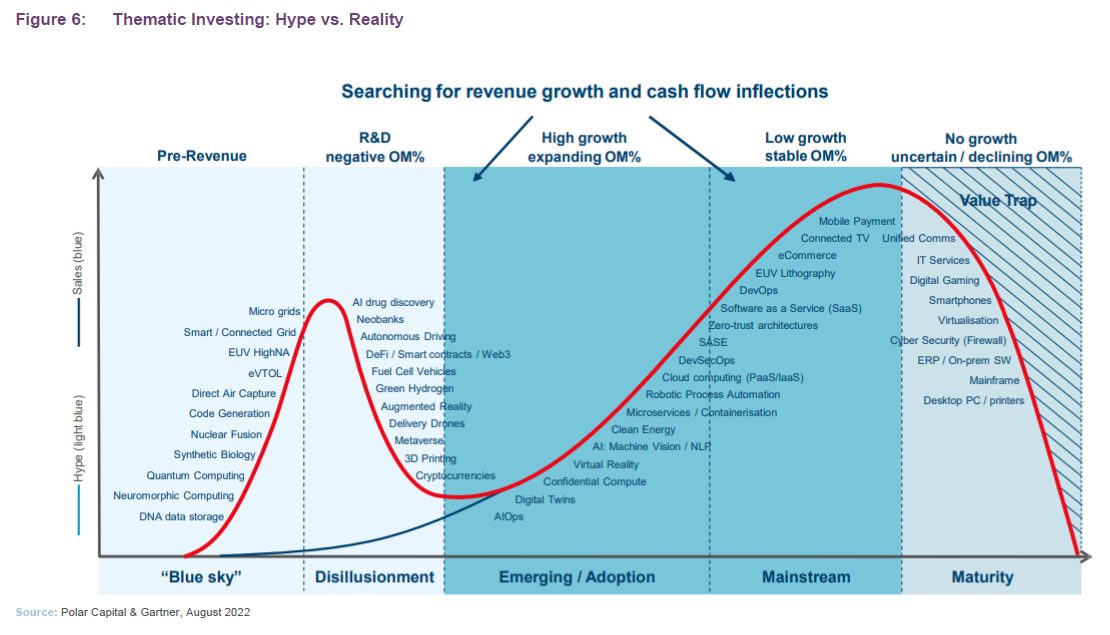

PCT avoids blue-sky and venture-capital-type investments. It also does not invest in businesses that are reliant on securing additional capital – there are points in the cycle when it is much harder for companies to attract funding. Figure 6 provides an illustration of this. PCT’s investment sweet spot is the area shaded in dark blue.

Investment process

PCT’s management team (profiled on page 19) carries out many hundreds of meetings a year, not just with portfolio companies, but also their competitors and suppliers. The team uses surveys and speaks to domain experts to cross-reference what customers think of products, where appropriate.

The manager selects from a universe of more than 4,000 stocks and looks to construct a diversified portfolio with about 100 stocks in aggregate. These should represent the best opportunities within the investment themes that the manager has identified, and should come at the right price. The team looks at the value chain and identifies areas where it is possible to generate super-normal profits (where companies have an unfair advantage) and recurring revenue.

On average, the stocks that are selected for the portfolio should be capable of generating 30%–50% higher growth than the average stock in the benchmark index and the manager is prepared to pay up for this growth – roughly 20%–30% more than the benchmark, on average.

There is little merit in first screening for value, in the manager’s opinion. It is better to think about which companies PCT should have exposure to, and only then about what is the price he is prepared to pay. The team is much more likely to screen for improving business fundamentals or stocks that it may have missed at the periphery of PCT’s investment universe that may not be perceived as tech stocks today, but might be in the future. An important part of this process is to think about the potential downside in a stock. For many of these stocks, missing an earnings forecast can be devastating to their rating.

PCT may miss out on the odd stock as a result, but the manager believes that this is an acceptable price to pay for avoiding the worst of the downside.

Sell discipline

The manager thinks that it is important to run your winners, but also to sell when an investment thesis did not play out as anticipated. Fair value is a moveable target and the potential upside and downside from any position needs to be reassessed regularly. The team has a bull, bear and base case for each stock, with a weighted probability to each of these scenarios.

Holdings will be trimmed as they approach the team’s target price. Sometimes Ben will hold onto a small position in a stock that he feels it is important to stay in touch with. The ability to have exposure to this type of opportunity is a benefit of PCT’s closed-end structure.

Portfolio construction

PCT is managed very much with an eye to risk. It is designed to deliver 3%+ annual outperformance versus its benchmark after fees on a consistent basis, with typical active share of 40–50%. It rarely makes outsized stock-level bets, preferring to add value by avoiding losers (often mature or blue-sky companies) and correctly identifying the most important secular themes (and allocating between them where value is perceived to be most compelling). This means that PCT ends up holding around 100 stocks. Whilst this means that other, less risk-aware funds may perform better over shorter periods, this risk-adjusted/diversified approach should allow PCT to outperform over the medium/longer timeframe.

From time to time, a handful of stocks can dominate the benchmark index. The board allows the manager to take a neutral position in any stock that accounts for more than 10% of the index (up to a maximum of 20% of the portfolio) but PCT cannot have an overweight exposure to these companies.

PCT is emphatically not a closet-tracking fund. If the manager does not like a company, PCT will have no exposure to it, regardless of its weight within the benchmark. This is currently true of Adobe, Cisco and Broadcom, for example (see Figure 11).

Typically, the maximum exposure to a stock will be a 3.0%-3.5% active weighting. The portfolio’s active share has ranged from about 30% to just over 50% max.

Investment in emerging markets is permitted but this is capped at 25% of gross assets. The board has also given the following indicative ranges for PCT’s asset allocation:

- North America up to 85%;

- Europe up to 40%;

- Japan and Asia up to 55%; and

- rest of the world up to 10%.

It has set specific upper exposure limits for certain countries where it believes there may be an elevated risk.

The remit allows investment in unquoted companies (subject to prior board approval and capped at 10% of gross assets) but in practice, this has not been used.

Asset allocation

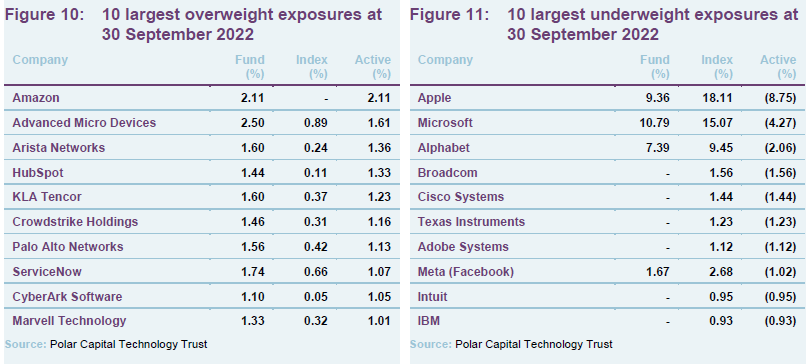

At the end of October 2022, there were 95 stocks in PCT’s portfolio. The portfolio remains benchmark-aware to express the best that the index has to offer and to help manage risk. The portfolio’s active share has trended higher over recent years in part due to higher concentration in the index as well as larger individual stock bets. At the end of September 2022, the active share was 53.9%. Ben feels that, because of their unique market positions and strong cash flow generation, PCT should own some Apple and Microsoft stocks. Nevertheless, at the end of November, these two stocks were still PCT’s largest underweights (see Figure 11). The portfolio may be managed in a benchmark-aware style, but the manager is happy to have zero weightings in index names when he feels that their growth prospects do not merit their inclusion within the portfolio.

Cash and equivalents, which includes puts on the Nasdaq, amounted to 6.0% of the portfolio at the end of November. This reflects the macroeconomic environment, but as mentioned earlier, the manager will look to take advantage of valuation compression and return the trust to a more fully invested position.

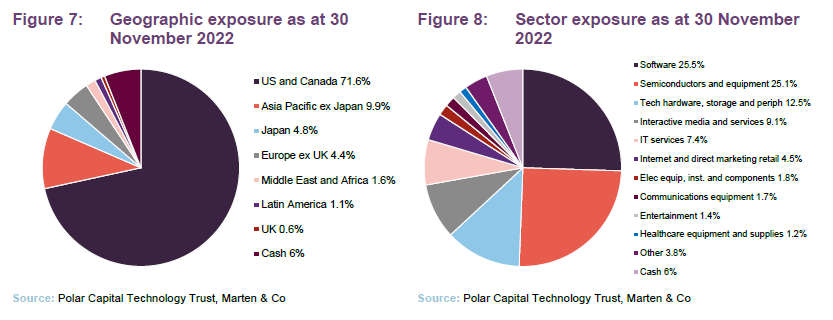

Whilst the manager does not try to add value through geographic asset allocation, he has increased PCT’s exposure to Japan at the expense of Asia Pacific (excluding Japan). He believes that Japan is a world leader in robotics, while the yen should benefit from a normalising macroeconomic environment and weaker dollar. Ben adds that there are several risks to performance in China, including an economic war breaking out with the US (as touched on earlier) and its zero-COVID policy. In Figure 8, the most significant change is a reduction in exposure to interactive media and services. As mentioned earlier, the manager will look to bring its cash position down to a more normalised level for the fund of between 3% and 4%.

10 largest quoted holdings

There has been very little change to the constituents of the top 10 list over the past six months, with KLA Tencor, which supplies process control and yield management systems for the semiconductor industry, being the only new entrant at the expense of Amazon (which is now ranked outside the top 15).

Figures 10 and 11 show PCT’s largest overweight and underweight exposures relative to the Dow Jones Global Technology Index at 30 September 2022.

Amazon had been PCT’s largest overweight exposure at the end of September, but the manager has since reduced its holding to below 1.3%. In recent quarter earnings, the company revealed that growth in Amazon Web Services (AWS) was below expectations at 28% year-on-year (down 500bps on the previous quarter growth and below the 30%-32% market expectation). AWS’s revenue growth for the fourth quarter is expected to be in the mid-20s driven by ongoing cost optimisation and demand weakness in mortgage and cryptocurrency markets. New customer pipeline was healthy, suggesting that long-term drivers remain intact, Ben adds.

ServiceNow, a software automation platform that helps companies manage digital workflows and automate work, now makes up 2.3% of the fund (up 50bps over six months) and is one of PCT’s largest overweight positions against the benchmark. The manager admires ServiceNow’s business model and believes in its future growth potential. Earnings results for the third quarter were stronger than expected, especially in Europe. The company also saw strength in the large enterprise market, with customers paying more than $10m annually growing at 60% year-on-year.

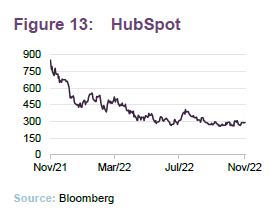

The manager highlights the large market opportunity for HubSpot, which operates a cloud-based customer relationship management platform, that is sized at $45bn today (and only 4% penetrated), growing to $72bn in 2027. The company was ranked as PCT’s 13th largest holding at the end of November.

KLA Tencor is another overweight position. Ben was encouraged by the company’s strong revenue, gross margin and earnings results for the third quarter and its above-consensus estimates guidance for the current quarter, despite the macroeconomic headwinds. China restrictions are expected to have a $600m-$900m negative impact on company revenue, but Ben believes that investors have viewed this as a clearing event.

The underweight exposure to Adobe reflects the manager’s scepticism over the company’s recent M&A activity, which it says could be designed to mask market share loss and/or slowing organic growth in its core business. The manager has exited its position in Adobe following the acquisition of private competitor Figma, a collaborative design platform for designers and developers, which it describes as “highly defensive”.

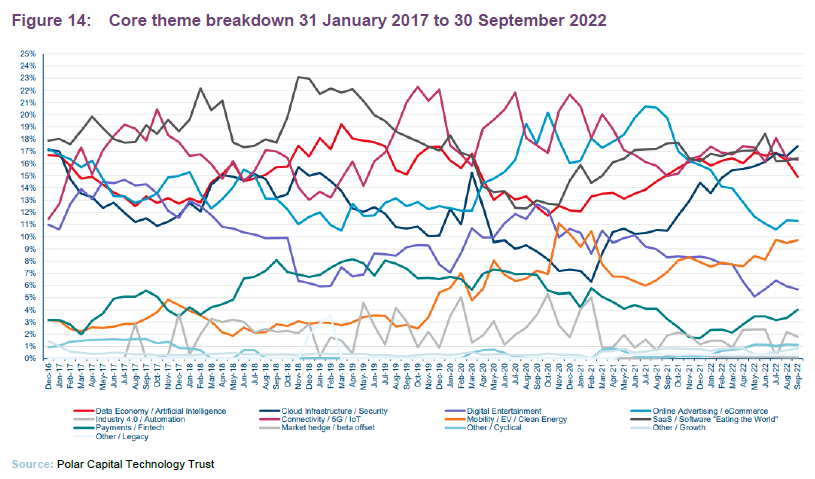

Core themes

PCT’s portfolio is positioned towards stocks that will benefit from six to eight core themes, with a number of secondary themes. The core themes are:

- Software as a service (SaaS);

- Cloud infrastructure/security;

- Mobility/EV/clean energy

- Connectivity/5G;

- Payments/Fintech;

- Data economy/artificial intelligence; and

- Online advertising/ecommerce.

Figure 14 shows how the composition of the portfolio has changed over time.

Cloud infrastructure/security

Cloud infrastructure/security is PCT’s largest thematic exposure at 17.4% at the end of September 2022. The manager says that the war in Ukraine has reinforced demand for cybersecurity due to the elevated risk and instances of Russian-backed cyber-attacks. This has highlighted the threat and the need to spend money on data security. The cost of cybercrime could exceed $10trn by 2025, according to Cyberventures, with cybersecurity playing a vital role in protecting the digital economy. Within PCT’s portfolio are stocks such as Crowdstrike, CyberArk, Tenable and Cloudflare, which could all be big beneficiaries.

SaaS/Software

In the software-as-a-service (SaaS) area, the manager rebuilt PCT’s exposure during the first half of 2021 having cut it as valuations soared in the preceding years. It now makes up 16.5% of PCT’s thematic exposure, and Ben highlights this as an area of focus as he looks to take advantage of valuation compression and return the fund to a more fully invested position.

In the hybrid world of work, software has become crucial for communication, collaboration, workflow automation and orchestration. The total addressable market is further expanding as virtual augments real-world in areas such as business travel, events and online learning. According to Goldman Sachs, SaaS could expand to a $412bn opportunity by 2025 (from $149bn in 2020), representing around 35% of total software spending.

Data economy/artificial intelligence (AI)

The sector has witnessed exponential growth in data generation over the past few years, with more data created in an hour today than in a year 20 years ago. Vast expansion is predicted over the next few years as we continue to move into a more data-centric world. Semiconductor companies are likely to capture 40% to 50% of the total value from this technology stack, Ben says. Adoption of AI is also expected to grow exponentially, requiring a huge increase in data storage and infrastructure spend. By 2025, AI-related demand will account for 20% of total semiconductor demand, according to McKinsey’s State of AI report. PCT’s exposure to this theme is 14.9% through companies like Samsung, NVIDIA, Advanced Micro Devices and Taiwan Semiconductors.

As mentioned earlier, the semiconductor sector is likely to be hit by US restrictions on China. Many of the companies have also reported an inventory correction across the supply chain that could last at least another two quarters, impacting on revenue guidance. Ben notes that semiconductor stocks often begin to start outperforming when they cut their numbers, as investors anticipate the next upcycle.

EV/Mobility

Electric vehicle (EV) sales are expected to account for more than 15% of total global auto sales in 2025, up from 3% in 2020, and 39% by 2030, according to estimates by Morgan Stanley. PCT’s exposure to Tesla has drifted to around 0.6% as its share price suffered recent falls after quarterly earnings numbers fell slightly below expectations. The company recently lowered prices in China, heightening concerns around demand. In the US, the manager expects the Inflation Reduction Act (IRA) to stimulate demand for Tesla cars in 2023. However, it says that there could be an “air pocket” in demand later this quarter as customers hold off taking delivery in anticipation of the IRA rebates starting in 2023.

PCT also has a position in Chinese EV-maker, BYD, which makes a range of passenger and commercial vehicles, including buses and urban rail transit. It has an R&D joint venture with Toyota Motor Corporation and is working with Huawei on automotive intelligent networking and intelligent driving. BYD also has a handset component and assembly business and a presence in batteries and photovoltaics.

Payments/fintech

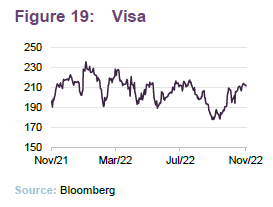

Payments and fintech makes up around 4% of PCT’s thematic exposure but is a sector that the manager is keen on. It has recently bought back into Visa and Mastercard as a way to play the reopening of international travel. The payments total addressable market is rapidly expanding, from around $33trn in 2021 to a potential market worth up to $150trn, according to Bernstein. The pandemic accelerated the decline of cash by three years (with 2020 exceeding prior expectations for 2023, according to WorldPay’s Global Payments Report) and the expansion of the payments sector includes new revenue streams such as business to consumer (B2C) and government to consumer (G2C), as well as growing card penetration rates.

Visa’s recent quarterly results were ahead of expectations, showing only a modest slowdown in credit volumes, while debit volumes held up well. Consumer spending remained stable with volumes ex-Russia growing 16% year-on-year. Ben says that the company’s full-year guidance for 2023 of low-teens revenue growth could prove conservative if the travel recovery continues (although guidance does not bake in the impact of a recession).

Performance

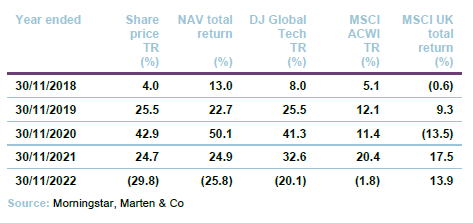

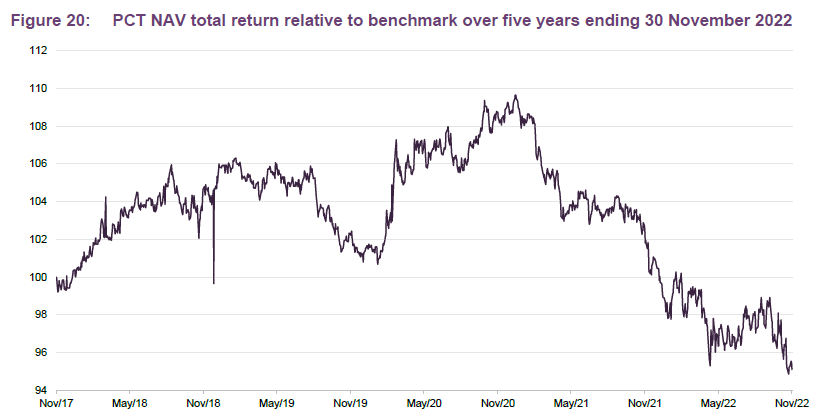

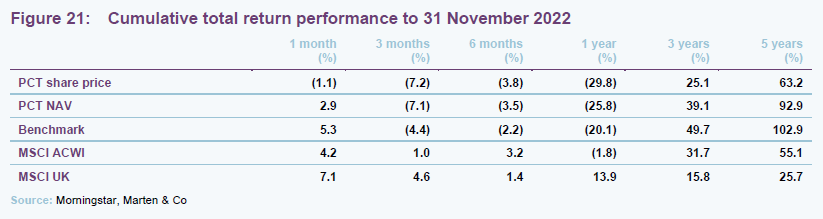

PCT’s underperformance of its Dow Jones Global Technology benchmark since early 2021 has largely been due to the effect of its two largest underweight exposures – Apple and Microsoft – performing reasonably well against a falling technology sector. In the year to the end of November 2022, PCT’s NAV returns were 5.7 percentage points lower. Prior to this, the trust has had a strong run of outperformance relative to the benchmark, but the underperformance from January 2021 has seen its five-year NAV return fall just below that of the benchmark, as shown in Figure 21.

Dividend

PCT historically has not paid dividends, given the nature of its focus on longer-term capital growth. The board reviews this stance on a periodic basis and would declare a dividend if this was needed to maintain the company’s status as an investment trust. Over the years, PCT’s running expenses have exceeded its revenue and therefore the revenue reserve remains negative. To pay a dividend, PCT would need to eliminate its revenue reserve deficit (£126.8m at 30 April 2022).

Premium/discount

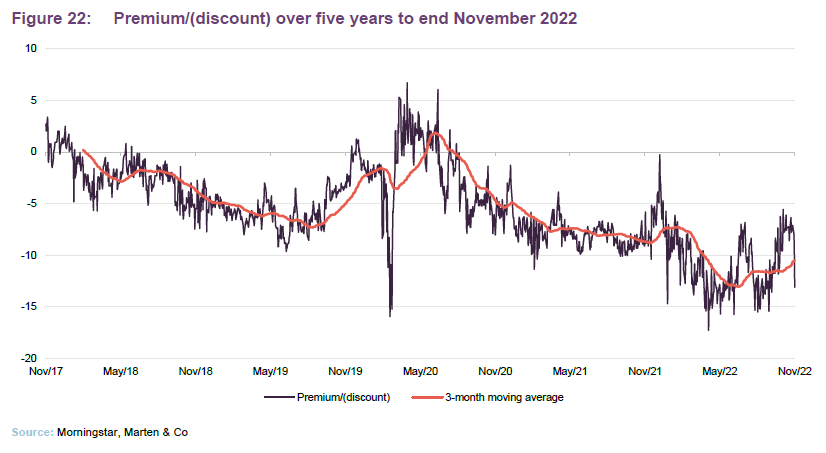

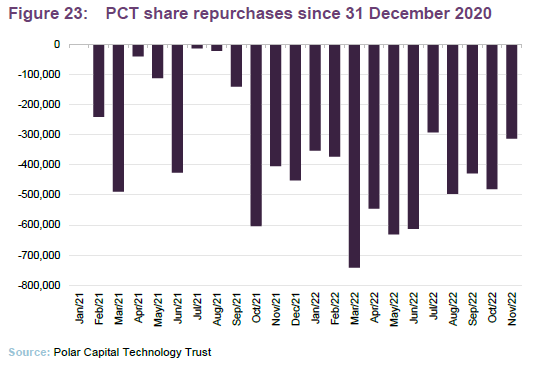

Over the 12 months to 30 November 2022, PCT traded between a discount of 0.3% and 17.3%. The average discount over this period was 10.4%. At 5 December 2022, PCT’s shares were trading at a discount of 7.1%. This feels a little excessive to us, given the upside potential in the portfolio from an easing of interest rate hikes and the action that PCT has taken to moderate its discount, as shown in Figure 23.

PCT issues and repurchases shares with the aim of ensuring that the shares do not trade at excessive premiums or discounts. Shareholders are asked at each AGM to approve the issuance of up to 10% of PCT’s issued share capital and the repurchase of up to 14.99% of its issued share capital. Shares are only issued at a premium to NAV. Shares repurchased may be held in treasury and reissued.

Fees and costs

The fee payable to the manager is tiered. PCT pays 0.8% on the first £2bn of net assets, 0.7% on net assets between £2bn and £3.5bn, and 0.6% on amounts above £3.5bn.

A performance fee of 10% of the fund’s outperformance of the benchmark is payable. The performance fee is subject to a high watermark and a cap of 1% of net assets. No fee is payable if the NAV fails to exceed the high watermark, but outperformance in such years is carried forward to subsequent years. The ongoing charges ratio is 0.84%, which does not include performance fees.

Capital structure

PCT has 129,036,833 ordinary shares in issue and admitted to trading plus a further 8,278,167 shares held in treasury, as at 5 December 2022. There are no other classes of share capital.

PCT’s financial year end is 30 April and AGMs are usually held in September. PCT has an unlimited life, but at the 2020 AGM, shareholders were asked whether they want the fund to continue. Shareholders backed the proposal overwhelmingly (99.8% of those voting). The same question will be put to shareholders in 2025 and every five years thereafter.

The use of gearing and derivative instruments is permitted and overseen by the board.

Derivative instruments such as financial futures, options, contracts-for-difference and currency hedges would be used for the purpose of efficient portfolio management. Any leverage resulting from the use of such derivatives will be subject to the restrictions on borrowings. PCT has no long-term borrowings and, at present, no short-term borrowings either.

Management team

Ben Rogoff

Ben is the lead manager of Polar Capital Technology Trust and is a fund manager of the Polar Capital Global Technology Fund and Polar Capital Automation and Artificial Intelligence Fund.

Ben has been a technology specialist for 25 years. Prior to joining Polar Capital, he began his career in fund management at CMI, as a global technology analyst. He moved to Aberdeen Fund Managers in 1998, where he spent four years as a senior technology manager. Ben graduated from St Catherine’s College, Oxford in 1995.

Nick Evans

Nick Evans joined Polar Capital in 2007. He has 23 years’ experience as a technology specialist and has been lead manager of the Polar Capital Global Technology Fund since January 2008. He is also a fund manager on the Polar Capital Technology Trust and Polar Capital Automation and Artificial Intelligence Fund.

Prior to joining Polar, Nick was head of technology at AXA Framlington and lead manager of the AXA Framlington Global Technology Fund and the AXA World Fund (AWF) – Global Technology from 2001 to 2007 (both rated five stars by S&P). He also spent three years as a Pan-European investment manager and technology analyst at Hill Samuel Asset Management. Nick has a degree in Economics and Business Economics from Hull University, has completed all levels of the ASIP, and is a member of the CFA Institute.

Xuesong Zhao

Xuesong joined Polar Capital in 2012. He has 14 years’ investment experience and is a lead manager of the Polar Capital Automation and Artificial Intelligence Fund. He is a fund manager on the Polar Capital Technology Trust and Polar Capital Global Technology Fund.

Prior to joining Polar Capital, Xuesong spent four years working as an investment analyst within the emerging markets & Asia team at Aviva Investors, where he was responsible for the technology, media and telecom sectors. Previously, he worked as a quantitative analyst and risk manager for the emerging market debt team at Pictet Asset Management and started his career as a financial engineer at Algorithmics, now owned by IBM, in 2005. Xuesong holds an MSc in Finance from Imperial College of Science & Technology, a BA in Economics from Peking University and is also a CFA Charterholder.

Fatima Iu

Fatima joined Polar Capital in 2006. She has 15 years’ investment experience and is a fund manager on the Polar Capital Technology Fund, Polar Capital Technology Trust and Polar Capital Automation and Artificial Intelligence Fund. Fatima is responsible for the coverage of European Technology, Global Security, Networking, Clean Energy and Medical Technology.

Prior to joining Polar, Fatima spent 18 months working at Citigroup Asset Management with a focus on consumer products and pharmaceuticals. She holds an MSc in Chemistry with Medicinal Chemistry from Imperial College of Science & Technology in London. Fatima is also a CFA Charterholder.

Alastair Unwin

Alastair joined Polar Capital in June 2019 as a fund manager and senior analyst. Before joining Polar Capital, he co-managed the Arbrook American Equities Fund. Between 2014 and 2018 Alastair launched and then managed the Neptune Global Technology Fund, and managed the Neptune US Opportunities Fund. Prior to Neptune, he was a technology analyst at Herald Investment Management. Alastair has a BA (1st Class Hons) in history from Trinity College, Cambridge and is a CFA Charterholder.

Paul Johnson

Paul joined Polar Capital in 2012. Prior to this, he helped manage a private investment fund between 2010 and 2012. Paul holds a BA in History and Politics and a Masters in History from Keele University. He has successfully passed all three levels of the CFA programme.

Nick Williams

Nick joined Polar Capital in June 2019 as an analyst on the Polar Capital Technology team. Prior to joining Polar Capital, he worked at Neptune Investment Management as the assistant fund manager on its US Opportunities growth fund. Previously, he worked in academia at the University of Oxford. Nick holds an MChem Chemistry from the University of Oxford.

Patrick Stuff

After graduating in July 2016 from the University of Warwick with a BSc in Economics, Patrick joined Polar Capital as an operations executive, where he provided operational support to all fund management teams at Polar, including the technology team. During this time he successfully passed all three levels of the CFA program first time, and subsequently, after a successful eight months seconded to the Technology team, he joined on a full-time basis in May 2021 as an investment analyst with a focus on small- and mid-cap companies.

Board

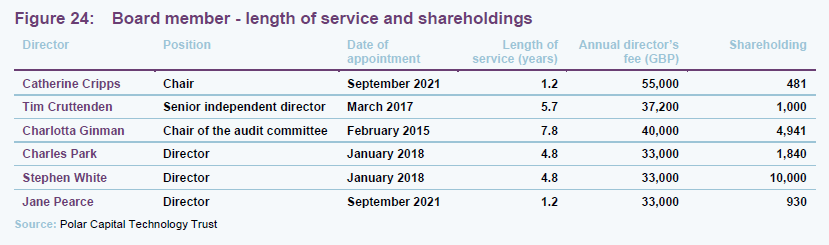

PCT’s board is comprised of six non-executive directors, all of whom are independent of the manager and who do not sit together on other boards. As part of its regular programme of refreshing the board, Sarah Bates retired as chair following the AGM in 2022 and was replaced by Catherine Cripps. Each of the directors stands for re-election at each AGM.

Catherine Cripps

Catherine was appointed to the board in September 2021 and took over as chairman in September 2022. She is a qualified Chartered Accountant with more than 30 years’ senior investment industry experience in a number of trading, risk management and investing roles including investment director and head of research at GAM. Catherine is also a non-executive director of Goldman Sachs International and Goldman Sachs International Bank, where she is chair of the risk committees and a member of the audit committees. Previously, she was non-executive director of CQS Management Limited where she chaired the remuneration and performance management committees and was a member of the audit committee.

Tim Cruttenden

Tim is currently chief executive officer of VenCap International Plc, having been with that company in various positions since 1994. VenCap invests in venture capital funds in the US, Asia and Europe, with a primary focus on early-stage technology companies. He is a non-executive director of Chrysalis Investments Limited.

Charlotta Ginman

Charlotta qualified as a Chartered Accountant at Ernst & Young before spending a career in investment banking and commercial organisations, principally in technology-related businesses. She held senior roles with UBS, Deutsche Bank, JP Morgan and the Nokia Corporation. Charlotta is a non-executive director and chairs the audit committees of Pacific Assets Trust Plc, Keywords Studios Plc and Gamma Communications Plc. She is also a non-executive director of Unicorn AIM VCT Plc and Boku Inc.

Charles Park

Charles has over 25 years of specialist investment experience and was a co-founder of Findlay Park Partners, an investment firm specialising in quoted American equity investments. Prior to this, he was a US fund manager at Hill Samuel Asset Management.

Charles is a non-executive director of North American Income Trust Plc and Evenlode Investments.

Stephen White

Stephen White qualified as a Chartered Accountant at PwC before starting a career in investment management. He has more than 35 years’ investment experience, most notably as head of European Equities at F&C Asset Management, where he was manager of F&C Eurotrust Plc and deputy manager of The F&C Investment Trust Plc. He also held the role of head of European and US Equities at British Steel Pension Fund.

Stephen is a non-executive director and chairman of Brown Advisory US Smaller Companies Trust Plc. He is also non-executive director and chairman of the audit committees of Blackrock Frontiers Investment Trust Plc and Aberdeen New India Investment Trust Plc. Stephen was appointed non-executive director of Henderson EuroTrust plc with effect from 1 December 2022.

Jane Pearce

Jane is an experienced non-executive director and Chartered Accountant with over 20 years’ financial markets experience. She has a number of years’ experience as a technology equity analyst and as an equity strategist at leading investment banks including Lehman Brothers and Nomura International.

Jane is a non-executive director and member of the audit committee of Shires Income plc and a co-opted external member of the audit and risk committee of the University of St. Andrews.

Previous publications

Readers interested in further information about PCT may wish to read our earlier notes. You can read them by clicking on the links below or by visiting our website.

Figure 25: QuotedData’s previously published notes on PCT

| Title | Note type | Publication date |

| Confidence building | Initiation | 12 May 2020 |

| More to go for | Update | 15 December 2020 |

| Exciting times | Annual overview | 7 July 2021 |

| Eyes on the prize | Update | 10 May 2022 |

Source: Marten & Co

Legal

This marketing communication has been prepared for Polar Capital Technology Trust Plc by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and, if you are not a professional investor, or in any other way are prohibited or restricted from receiving this information, you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it, but in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this not.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.