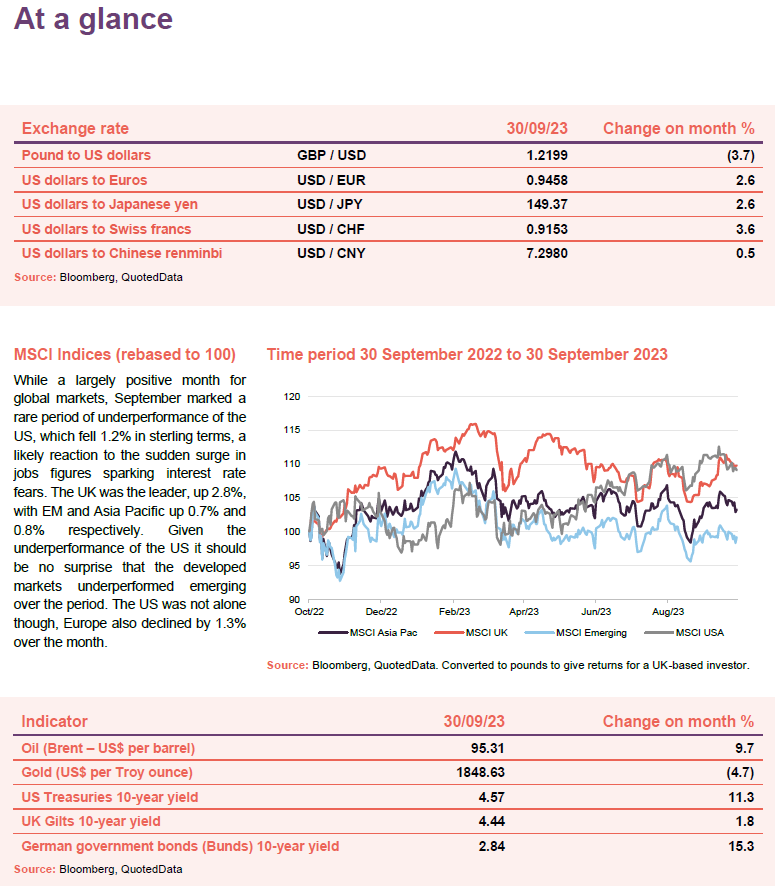

Economic and Political Monthly Roundup

Investment companies | Monthly | October 2023

Reading the headlines, it still feels that we are trying to walk across a frozen lake. While none have yet to fall though, cracks are starting to appear, and some are certainly closer to making it to the other side than others. In practical terms we have seen another month of mixed news for economic growth, with the US leading the charge while the rest of the world tries to dodge stagnation, interwoven with concerns by businesses around the fragility of the economic outlook.

“The only function of economic forecasting is to make astrology look respectable.” – JK Galbraith

One of the biggest surprises has been the exceptionally strong jobs data the has come out of America, with 336,000 jobs added in September, almost twice the consensus estimates for the month. This is a doubled edged sword however, as it places greater pressure on the Fed to raise rates again this year, with at least one more rise being the markets expectation (this was reflected in a jump in bond yields over the month). Ultimately the US is increasingly looking like the bright spot in the global economy, with the economic activity continuing to remain very robust in the face of rising interest rates.

The story elsewhere is not as rosy. While the UK did revise its Q1 GDP estimates upward (implying a greater post-COVID rebound than originally thought) September’s PMI fell to 46.8, indicating that business had become gloomier on the UK’s outlook. However, a recession is not a certainty, as a weakening outlook may finally give the BoE pause for thought. Despite the impact of high rates and cost of living increasingly weighing on the markets minds, the UK consumer was more confident in September, with retail sales having rebounded in the month.

The world’s second largest economy continued to show signs of stagnation over September, with China’s exports falling YoY once again (though not as much as pundits thought). Chinese inflation came in at 0% in September, which indicates that the risk of deflationary pressures is a real one, often a sign of declining economic activity. The Communist party has got the ball rolling on supportive measures however, having proposed establishing a stock market stabilisation fund to boost market confidence.

Global

(compare global and flexible investment funds here, here, here and here)

David Seligman, chairman, British and American Investment Trust – 29 September 2023

With the many political, social, economic and indeed climatic uncertainties facing the world today, both in the immediate future and in the longer-term, it is difficult to be very positive about the investment climate going forward. Inflationary pressures, while reduced, remain unconquered. Counter-inflationary interest rate measures may not have peaked and, if shortly to do so, might last longer than originally expected. The war in Ukraine, together with its effect on world energy and food prices, is likely to enter a third year and this year has brought numerous examples of disruptive and destructive weather patterns world-wide which can only be expected to worsen over the coming years. While the attempts to control the generationally high levels of inflation have so far resulted in a generally softer landing than originally feared, much of the higher than expected economic activity, particularly in the retail, hospitality and travel sectors could be the result of pent up demand following the Covid period and the drawdown of savings built up during this latter period which may soon come to an end.

. . . . . . . . . . .

Manager, Manchester and London – 27 September 2023

After more than 525bps of US rate hikes over the past couple of years, the range of potential outcomes for the next 12 months now appears somewhat narrower. Advanced economies are expected to experience slower growth and inflation remains a key factor influencing monetary policy. China has shifted from a growth engine for the world to a deflation engine. We see geopolitical risks remaining between the US and China and continuing de-risking of supply chains.

Most major central banks are near the end of their rate tightening cycles. In the more medium term, inflation is expected to fall, and there are even signs of future disinflation in parts. While risks remain, the possibility of 10 year Treasury yields falling with improving inflation prints provides optimism for stock returns. The US economy’s situation is unique, and while recession risk exists, the outturn may well be much better than previously anticipated. We do believe that our portfolio of long duration assets may be more interest rate sensitive than it is sensitive to a mild recession.

The primary challenges to equities remain inflation, recession, regulation, energy prices and war. Central banks aim to prevent entrenched price changes, but it is difficult to calibrate monetary policy to prevent transitions to high inflation regimes. The Fed’s preferred measure, the PCE price index, has fallen but history has seen reversals before. We are hopeful that, over time, productivity gains can assist in reducing inflation.

Recession risk is always a concern when the Fed has been so active in attempting to slow the economy but we would remind readers that the areas of technology that we are invested in are often considered more defensive. Geopolitical risks, such as the conflict in Ukraine and US-Sino relations, also pose very material concerns. China, Iran, N Korea and Russia are all bad actors that can cause numerous horrific events that could cause material downside for the markets. We are constantly watching the oil price with anxiety.

. . . . . . . . . . .

Zehrid Osmani, Manager, Martin Currie Global Portfolio Trust – 27 September 2023

An important focal point during the second part of the year will remain the inflation trend, with inflationary pressures likely to continue to ease, but with the risk of inflation remaining stickier and longer lasting. Inflation is likely to be driven by technological fragmentation, near-shoring trends which will increase production costs, and elevated wage inflation. The latter is likely to be the most important determinant of inflation in the medium term.

Inflation trends will continue to feed into monetary policy expectations – we predict that the peak in interest rates is getting very close now, which should in itself be supportive for the quality growth style that we invest in. However, we do not subscribe to the market view that monetary policies will reverse in the first half of 2024 because we envisage inflation rates preventing central banks cutting interest rates.

The economic cycle will continue to be an important focal point with an ongoing uncertain outlook, given the sizeable interest rate increases that we have seen in the past 18 months across key geographies. Our central scenario remains a sharp slowdown rather than recession for the world as a whole and the US in particular. For Europe, our central scenario remains stagflation. We maintain our probability of a global recession at 30-35%, despite a broad consensus view that a recession is a high likelihood in 2023. China’s economic momentum remains key to the global economic cycle and we expect ongoing recovery in the services sector in China in the remainder of 2023. There is a rising risk of recession in the US in 2024, however, which could be an important focal point for investors.

The corporate earnings cycle is already in recession following downgrades and with the risk of further downgrades in the rest of 2023. Equity valuations are now less supportive but, within this, EU and Asian equities are relatively attractive. In this continuing uncertain environment, we believe that focusing on fundamental assessments and picking undervalued stocks that have strong fundamentals and operate in industries with favourable dynamics for value creation will serve our shareholders well over the longer term.

. . . . . . . . . . .

Managers, JPMorgan Global Growth & Income – 27 September 2023

Overall, we are relatively sanguine about the year ahead. While we hope that AI could lead to a technology-led growth opportunity within the broad economy, we see headwinds in the form of: higher interest rates; a depleting consumer cash balance; and record profit margins at risk of returning to pre-pandemic levels. So, while broad market valuations trading slightly above historical averages look neither compelling nor particularly demanding.

This year has seen several key themes emerge, some of which we believe will have longevity, while others will be temporary. We see AI as an opportunity that could change the way companies operate over the next decade, from both an efficiency point of view and a quality-of-service perspective, with social media stocks seeing this as a core part of their infrastructure and business. Over the coming year we will undoubtedly see many companies claim to be AI winners, just as we saw many companies claim to be internet winners in the early 2000’s. Our core objective is being able to separate which of these companies will be able to monetise AI from those that will purely implement it without seeing a long-term lift to earnings. Given AI’s data requirements, we see Nvidia as the key beneficiary of this growth opportunity, with demand outstripping supply for the foreseeable future. As the clear market leader, Nvidia has a great starting place from which to monetise the technology, but other types of barriers to entry are just as important to consider. For instance, despite many new companies talking about their ability to deliver AI-generated images, for legal reasons their customers cannot use these images due to litigation risk. Hence, we see Adobe as having a real edge with their image library and their leading image software. We see AI as a great opportunity to not only increase pricing but also tap into new smaller businesses that historically were outside of Adobe’s addressable market. With holdings in Microsoft, Amazon, Meta, Nvidia and Adobe, we believe we are well positioned in companies that will have the ability to monetise AI.

Over the coming year, there is a reasonable chance many companies will be incorrectly considered as AI winners; however, we believe that our emphasis on the barriers to entry will stand us in good stead in the long term.

. . . . . . . . . . .

Peter Burrows, chair, UIL – 25 September 2023

Several themes continue to dominate global events: heightened geopolitical tensions, the outlook for inflation and interest rates, climate change, technology and Artificial Intelligence (“AI”).

As anticipated at the time of announcing UIL’s half-year report, Covid-19 has receded and we do not expect it to be an issue going forward. China’s reversal of its zero tolerance policy earlier this year was a positive. However, weak Chinese consumer confidence is a headwind to a full recovery by China.

The war in Ukraine has gone on longer than expected and today there continues to be no clear way forward. Both sides have been drawn in further, but once they reach a neutral position, a negotiated outcome would be expected.

The ongoing friction between the USA and China continues to deepen and it is now difficult to see how this reverses direction. Given the USA and China are the two largest economies globally this must pose significant risks at some point in the future, especially for technology businesses on each side of the Pacific Ocean.

Inflation moved markedly for most economies over the year. Nearly all central banks responded with significantly higher interest rates. We now see major differences between three key regions: the Western economies where we expect inflation to reduce gradually; Asia, where we see China heading for deflation; and Latin America (“LatAm”), where inflation has already halved. Against this backdrop we expect Western economies to hold interest rates higher for longer, China to reduce rates further while LatAm is expected to reduce interest rates sharply lower.

The one unknown in our view continues to be the response of the labour force especially in the West. Labour markets remain tight and the number of unemployed are at record lows in many economies. If this continues, then the shortage of the work force will drive up wages and in turn feed inflation.

An ever increasing factor for investors is climate change. It has clearly had devastating impacts on a number of communities from wildfires in Hawaii to floods in Germany. We are seeing whole ecosystems being impacted from prolonged droughts to record temperatures. As investors we need to prepare for these outcomes to continue across our portfolios.

There is a very perceptible shift to embrace AI by most businesses and as with most technological developments, those without legacy businesses benefit the most, but eventually all businesses will need to adapt or risk failure. This has been our experience in the Fintech sector. UIL has a number of investments with significant exposure to AI, Blockchain and Quantum Computing.

The outlook for worldwide economies increasingly rests with global leadership, both political and central bankers. The central banks perhaps have the easier task as inflation looks to be receding in most major markets. We assume interest rates will stay higher than expected and we expect this will be a headwind to economies and commodities are likely to remain soft. The same cannot be said of geopolitical leadership which remains challenging. The rising pressure to meet social expectations and the impact of climate change, natural disasters and conflict will be difficult to navigate. We remain focused on reducing risk and helping investee companies navigate through these challenges and emerge stronger.

. . . . . . . . . . .

Victoria Muir, chairman, North Atlantic Smaller Companies Investment Trust – 15 September 2023

Global supply chains have returned to some normality and as a consequence in developed markets the momentum of increasing inflation appears to be weakening. Forward looking indicators suggesting that inflation is likely to moderate, as it has already in the US where it is on a downward trajectory. Central banks are walking an interest rate tight-rope, as they balance inflation control with maintaining economic growth. In Emerging Markets, the inflation picture is mixed with a chance of China going into deflation and inflation levels improving elsewhere.

UK equities, in general, have experienced a prolonged period of being rather unwanted, unfashionable and unloved, and share prices have been affected by a significant withdrawal from this market. Their value is being very gradually recognised and we expect an uptick in M&A. In the US, it has been striking to note how narrow the market has been, with performance concentrated across a handful of names and a marked difference between the S&P 500’s returns versus that minus its seven dominant stocks. We are starting to see some signs of this normalising.

. . . . . . . . . . .

Russell Napier, chair, CT Global Managed Portfolio – 7 September 2023

The savers who own the shares of our Company are seeking to both protect and grow the purchasing power of their wealth. This involves securing positive nominal returns but also, over the long-term, securing returns higher than the rate of inflation. Over the very long-term equities have provided such returns but sometimes it has taken more than a decade for the initial investment in equity indices to result in positive real total returns. If, as Mr Buffet famously said, ‘price is what you pay, value is what you get’, then it is possible to pay too much even for the highest quality companies. Assessing the sustainability of corporate returns and the correct price to pay for future returns is the skill and partially the art of investment. Our shareholders have benefited from the skills of our previous managers in selecting high quality companies that can produce sustainably high returns and in investing in those companies at what proved to be attractive valuations. Our Company will continue to pursue such an investment policy under our new managers.

Investing in companies that can both produce high returns on capital and also reinvest their cash flows at similarly high returns is an approach that is likely to be particularly attractive in an age of higher inflation. While none of us can forecast the peak level that inflation might reach in any business cycle, the structural changes underway in the world do seem to augur a materially higher level of inflation than we have been used to over the past decades. To defend savings from the erosion of purchasing power that comes with higher inflation one approach will be to invest in companies that can invest and reinvest their cash flows for returns that very significantly exceed the rate of inflation. Our new manager, Lazard Asset Management, will invest in such companies. Their skill, demonstrated since they began this High Quality Growth strategy, will be in accurately forecasting where corporate returns can remain sustainably high and of course in not paying too much for such high returns. It is a skill they have been deploying for over a decade and since the inception of this approach, in February 2011, that has produced a net outperformance relative to our comparator index of 2.4% per annum. The shares of companies that can invest and reinvest at rates of return well above the rate of inflation are likely to remain in strong demand in an era of high inflation.

The steep rise in interest rates since 2020 has not produced the scale of economic deceleration and perhaps even financial distress that might have been expected. Such a reaction to higher interest rates in 2008 caused a contraction in economic activity, bank collapses and huge losses for equity investors. Despite record high levels of debt, relative to GDP, both the public and the private sector have, so far, been able to service their debts and debt defaults have remained constrained compared to other economic downturns this millennium. This resilience probably primarily reflects a move by many debtors to extend the duration of their borrowing and lock in low interest rates in the period of very low interest rates that pertained up to 2020. Even so debt is always maturing and as it is refinanced the higher costs of servicing that debt will lead to greater strains for those seeking to service their debts. The clock is thus ticking for debtors as their debts are refinanced at higher rates of interest. The data on private sector debt service ratios, which show the proportion of private sector income currently needed to service debts, indicate that many countries, are at a level where historically their private sectors have defaulted on their debt obligations and these ratios will continue to deteriorate as debt is refinanced. Perhaps surprisingly the private sector debt service ratios of the United States, United Kingdom and Japan are reasonable but for some large and important countries, such as France and China, a dangerously high level of private sector income is being diverted to service debts. The impact from rising interest rates on economic growth, financial stability and equity prices has been benign but as time ticks on and debts are refinanced at higher interest rates this is likely to change. Investing in those corporate cash flows that can remain robust even in such circumstances can protect investors from the worst effects of any economic contraction that may come as the impact from higher interest rates hits the private sector. Companies with high returns on capital and low debt levels should be better placed to weather economic contractions when they come.

It is not easy to discern the major trends that are developing during a period of rapid short-term changes and general volatility. One trend though is becoming more apparent. That is that governments are intervening to create outcomes that they believe should not be left to market forces. That is a trend that involves both the socialisation of private sector risk, as we saw with the significant government support for the private sector during the COVID-19 crisis, but also in the form of governments co-opting or cajoling corporations to assist in delivering their political goals. This is a trend that is very likely to continue as governments react to what are the growing list of ‘crises’ confronting the electorate – climate change, war in Europe, a cold war with China, higher cost of living etc. While such intervention may mitigate the extremes of the business cycle it comes at a price for savers in the form of greater government interference in the allocation or private capital / savings. History suggests that such government interference rarely results in higher returns on capital for the companies so co-opted by governments. A well-chosen portfolio of equities may be one of the few places for investors to hide in such a world particularly by investing in the high-quality companies that can continue to produce high returns on capital even during such shifts in the balance between markets and governments.

Savers face new challenges but rarely are they unique challenges. History provides some guidance to the future and it suggests that well managed companies, producing high returns on capital and bought at good valuations will provide positive real total returns.

. . . . . . . . . . .

UK

(compare UK funds here, here, here and here)

Marwyn Value Investors – 25 August 2023

Despite a challenging global market landscape, we are optimistic about the prospects that lie ahead. Our portfolio is exceptionally poised to capitalise on forthcoming opportunities, and we eagerly anticipate witnessing the growth and evolution of our portfolio companies. We are immensely grateful for your continued trust and investment in Marwyn Value Investors Limited.

We have maintained a cautious stance towards the markets and company valuations in recent years, a strategy that seems increasingly justified given the prevalent speculation and a somewhat unrealistic expectation regarding a return to ultra-low interest rates. We perceive the burgeoning sovereign debt issue and a contracting money supply as significant forces that will necessitate a recalibration of market expectations and valuations. We are beginning to observe early signs of these necessary adjustments taking place.

. . . . . . . . . .

Managers, Strategic Equity Capital – 27 September 2023

The Investment Manager’s core planning assumption is that continued geopolitical and macroeconomic uncertainty will drive market volatility throughout the remainder of 2023. The shift to a period of higher inflation and higher interest rates has fundamentally impacted asset markets and equities in particular. It is likely that increasing focus on company fundamentals and valuation discipline will be required to outperform in this environment which plays to the strengths of the Company’s investment strategy and the Investment Manager’s approach.

The elevated levels of corporate activity within the UK equity market continue to play out and the volume of takeover activity amongst smaller companies has not been seen since H2 2019, despite overall UK takeover volumes (of all sizes) remaining marginally below H1 2022 levels. Bid premia in the period were also elevated, providing further evidence of attractive valuations amongst UK smaller companies despite the higher cost of capital environment today. The investment process and private equity lens across public markets enables the identification of investment opportunities with potential strategic value that could be attractive acquisitions for both corporate and financial buyers.

. . . . . . . . . . .

Simon Gergel, Manager, Merchants Trust – 26 September 2023

In our opinion, the UK stock market offers exceptional opportunities for investors. According to Goldman Sachs, the UK stock market is trading close to its lowest absolute valuation in the last 20 years, in terms of price to earnings ratio, at the same time that the USA is trading close to its highest level. That is unusual in itself. But, in addition, the dispersion of valuations across the UK stock market (the gap between growth and value stocks) is around the widest it has been in 50 years, according to Morgan Stanley. These are conditions, that I don’t remember seeing before in my career. Many sound businesses are trading on depressed valuations, offering the potential to make very healthy capital and income returns. To understand why this is the case, and why conditions may change, it is worth discussing the circumstances that have led to this unusual situation.

Since the Brexit referendum in June 2016, the UK stock market has been out of favour with international investors, and it has gradually de-rated. Initially, this was driven by fears over the economic impact of Brexit itself, and this was exacerbated by the tortuous political wranglings with the EU during Theresa May’s and Boris Johnson’s premierships. Political uncertainty increased, when Jeremy Corbyn, a hard-left leaning politician looked like he could win the general election in 2019. Then, just as the Brexit and political uncertainty started to fade, following Johnson’s emphatic election win in 2019, the Covid pandemic hit in early 2020, and the UK seemed to suffer especially hard, providing another reason for foreign investors to stay away. Next, as the pandemic was fading into the rear-view mirror, the Russian invasion of Ukraine caused a huge inflationary spike that particularly affected Europe, giving global investors reason to stay clear of the whole continent. Further political uncertainty ensued when Liz Truss became prime minister for a brief period in 2022 and unsettled the financial markets with what were perceived as unfunded tax cuts. Finally, more recently, as discussed above, the UK’s inflation rate has been higher and more sticky than the rate in the US and the EU, creating a narrative that the UK has a more challenging outlook.

These concerns about the UK, have led to steady outflows from UK equity funds in recent years. This comes on the back of a structural, forty-year period, where domestic pension funds and institutions have gone from owning around half the UK stock market, to only 4%. The selling has largely been due to the increasing maturity of defined benefit pension funds, and accounting rules which encouraged funds to sell equities and buy bonds. This selling pressure has exacerbated the de-rating of the stock market, and widened the gulf between those companies that are popular with global investors – typically the large multi-nationals and the higher growth / higher return companies – and the rest. It has often felt like there were no buyers for some of the medium sized and smaller companies, and it not surprising that we have seen a step-up in the number of portfolio companies buying back their own shares, to take advantage of the bargain prices available.

Whilst some people may see this set of circumstances as a reason to shun UK equities, we see the glass as half-full. The selling pressure by domestic pension funds and institutions really cannot go much further, as they own very few UK equities. Furthermore, the government is keen to promote the UK stock market, and to get domestic savers and institutions to support investment and innovation. This may take time to have any effect, but the relentless selling should be nearly finished. The latest inflation numbers suggest that the UK is nearing the peak of the inflation cycle and any visibility on peak interest rates could lead to a significant change in depressed investor sentiment. UK politics seems to be becoming less polarised, with the policy gap between Rishi Sunak and Sir Keir Starmer quite narrow, removing one of the often-cited reasons for avoiding UK investments. Most importantly, the valuations of many UK companies are compelling, especially compared to their peers overseas, despite the majority of sales of UK listed companies actually coming from abroad. We would expect to see a resurgence in takeover activity, as companies and private equity funds look to take advantage of this situation. The cost of debt and volatility of interest rates may keep some of these investors on the sidelines for a while longer, but once the interest rate cycle looks more supportive, sentiment could change rapidly.

. . . . . . . . . . .

David Barron, chair, Dunedin Income Growth Investment Trust – 21 September 2023

The economic challenges to global growth continue to build, following rapid and sustained interest rate increases from central banks across the world, coupled with a Chinese economy facing significant headwinds. Despite some signs of easing, inflationary pressures remain significant in most economies and supply constraints are placing upward pressure on many commodity prices. In the UK, inflation remains too high and growth too low, albeit there are indications that a trough has been reached and perhaps somewhat ahead of other major economies. For equity markets, there remain reasons to be cautious and the next 18 months are likely to be a tough period for corporate earnings development. It is that very unpredictability of world and economic events that makes us concentrate on the companies within the portfolio and their ability to navigate the environment ahead of them.

Our objectives remain to meet investor needs for capital and income returns over the medium and long term. We have again made good progress in this period. Whilst the global outlook is far from propitious, we believe our strategy of focussing on a concentrated and actively managed portfolio of high quality companies from across the UK and European markets with leading sustainability characteristics sets us up well to navigate conditions ahead.

. . . . . . . . . . .

Steve Tatters, investment manager, Aurora Investment Trust – 21 September 2023

The UK is, in so many ways, mired in its own gloom. Anyone visiting even with a neutral perspective will soon find themselves infected by the negativity that pervades life in the UK. Although there are plenty of negative things occurring, and some of them have been big, like the implications of Brexit, when one thinks about it in the context of what the future holds for the world, there is reason to be particularly optimistic.

Take technology; Charles Babbage is considered to have built the first computer, Ada Lovelace to have written the first computer programme, Alan Turing is the founding father of modern computing and Artificial Intelligence, Tim Berners-Lee is the person who started what became the internet we know today, Geoffrey Hinton who recently stepped down from Google and is considered the father of AI and Demis Hassibis the new head of AI at Google is the co-founder of Deep Mind that has made great breakthroughs in AI. These people are all from the UK and were actually all born in London. This is not coincidence, the British, although they rarely acknowledge it themselves, have a culture that produces creative and inventive people, and we are in an era when that will be highly valued.

The best-selling writer of all time is Shakespeare, but in the modern era it is JK Rowling. In fact, 3 of the 5 best-selling books of all time were written in the UK. The same goes for music where 4 of the top 8 selling artists of all time are from the UK. We could go on, but the picture is the same, the UK is unusually creative in a way that has global appeal.

Machines reduced the manpower needed in food production and robots and AI are doing the same in manufacturing, logistics and administration. As people work less, they put more time and money into leisure and entertainment. That is having a big impact in games and sports and once again, the UK is uniquely placed.

Football is the world’s most watched sport with the English Premier League the most watched and most valued in the world. Next it is cricket. The most valuable sport according to Forbes is Formula One, which also originated in the UK and 70% of the teams are based here. As we write another game originated in the UK, Tennis, the most watched single person match sport in the world, is having its annual tournament in Wimbledon, SW London.

This creative and playful inventiveness is not just an intrinsic cultural characteristic, it is also the product of an education system that encourages individuality. Again, the UK has four universities ranked in the Top 10 in the world, the same number as the US, a country with 5 times the population.

Brexit may impact where companies decide to locate their factories, but there is a reason why Apple and Google have recently opened such big HQs in London.

The past 25-year period has been a miserable one for investors in the UK stock market when compared to their global peers. Some of this has been justified but a lot has been due to the devaluing of businesses listed here. As we write, the value of Apple now exceeds the whole of the FTSE 100.

These are the moments when value investors retire, get fired or alternatively double down, maximise their upside value and wait. Buffett says that when it is raining gold put out a bucket not a thimble. In 1999, in our first full year, we lagged the market by 25%, and value investing felt like a lonely place to be as everyone was enjoying bumper returns in the market. What we learned then and have again and again, is that in the end value wins, it can be a long wait, but ultimately value shines through.

. . . . . . . . . . .

Charles Luke and Iain Pyle, managers, Murray Income Trust – 20 September 2023

Recent data points provide a less than clear picture around current conditions and future direction. However, in most developed economies growth appears to be more robust than might be expected in light of the meaningful monetary policy tightening over the past 12 months. On the other hand, the momentum of China’s reopening has faded and more stimulus is likely to feature. Underlying price pressures have been sticky reflecting excess demand across various sectors and economies prompting central banks to remain hawkish. We believe that the current tightening cycle will ultimately restrict economic growth with the resulting downturn in demand helping to engineer a relatively rapid fall in inflationary pressures allowing significant interest rate cuts over the next 18 months.

Companies with pricing power, high margins and strong balance sheets are better placed to navigate a more challenging economic environment and emerge in a strong position.

The valuations of UK-listed companies remain attractive on a relative and absolute basis. Apart from the global financial crisis, the UK’s market multiple is nearing its lowest point for 30 years. It is cheap in absolute terms, relative to history and also relative to global equities. Investors are benefitting from global income at a knock-down price. Moreover, the dividend yield of the UK market remains at an appealing premium to other regional equity markets. In summary, we feel optimistic that our long-term focus on investments in high quality companies with robust competitive positions and strong balance sheets, which are led by experienced management teams will be capable of delivering premium earnings and dividend growth.

. . . . . . . . . . .

Sir Laurie Magnus, chair, City of London Investment Trust – 19 September 2023

Over two-thirds of revenues earned by the companies in City of London’s portfolio comes from overseas. Whilst this diversification is helpful given the relative economic weakness of the UK, prospects for the global economy remain very uncertain. The war in Ukraine has no end in sight, there is continuing tension with China, the outcome of the increasingly fractious US election campaign remains in doubt and recent climatic events across the world have demonstrated the severe risks of climate change.

A further uncertainty arises from the coordinated actions by central banks to use the levers of monetary policy, and most directly higher interest rates, to curb inflation. The implications of this will take some time to show their effect, but it is already clear that a return to the cheap lending rates that have prevailed for the last 15 years will not recur. Households will experience a significant increase in interest costs as their fixed rate mortgages are rolled over, as will businesses when their existing debt matures. Over time, although the rate of inflation should continue to fall as increases in energy prices drop out of the annual calculation, this will affect the behaviour of consumers, with consequences for corporate profits and investment.

UK listed shares in general continue to trade at lower valuations relative to comparable businesses overseas. The reasons for this include continuing investor scepticism concerning the benefits of Brexit, the preponderance of “value” stocks (such as banks and energy companies) relative to “growth” stocks (such as technology including AI), the lack of domestic support because many UK investment institutions favour fixed interest in their asset allocations and the prospect of a more interventionist Labour government. These lower comparable valuations, however, offer potential rewards for City of London as both private equity firms and overseas businesses take advantage of opportunities to use the UK’s open markets to secure attractive acquisitions. It remains the case that UK equities offer compelling dividend yields relative to the main alternative equity markets and, on this basis, UK investors can reasonably take the view that they are being “paid to hold on” until valuations improve.

. . . . . . . . . . .

Georgina Brittain, Katen Patel, managers, JPMorgan Mid Cap Trust – 19 September 2023

The trajectory of inflation and interest rates is clearly key for the outlook. While we had expected a mild recession in the UK in the second half of 2023, the economy may avoid this – but UK growth prospects are pedestrian at best. Following the encouraging inflation figures in July we believe inflation has peaked in the UK, and we foresee a significant further decline from the current levels over the course of 2023, which will hopefully bring the UK more in line with other developed markets. Interest rates at 5.25% have risen significantly and we believe they are very close to peak levels. Consumer confidence had staged a significant recovery from its abject lows – largely, we believe, due to continuing very low unemployment rates and the wage increases that have been seen this year – although the very recent spike in mortgage rates has caused a setback in what had been an upward trend.

Clearly the UK stock market is currently focused on the macro-economic outlook. Evidence of this can be seen in the sharp one day upward move of 4% in the FTSE 250 Index when July’s inflation figures proved a positive surprise. However, as always, our focus is on the companies themselves. Overall the message we are hearing from them is a positive one. The FTSE 250 is a broad and diverse index, and we continue to find exciting and undervalued investment opportunities, some of which we have described above.

This leads us to valuations. While the environment remains difficult for businesses and consumers to navigate, a lot of this is already reflected in valuations. At the time of writing, the FTSE 100 is on a forecast P/E for 2024 of 10.5x, and FTSE 250 is similar on a 10.8x forecast. The Mid Cap index premium has almost completely disappeared; and 10.8x compares to a 20 year P/E average of 13.7x (source: Investec). The Bank of America chief investment strategist, Michael Hartnett, has called out UK mid cap stocks as being at their cheapest versus global stocks since 2003. As we have said before, acquirors of UK businesses are recognising this and M&A is set to continue.

. . . . . . . . . . .

Amanda Yeaman, Abby Glennie, Investment managers, abrdn Smaller Comapnies – 13 September 2023

The markets continue to be dominated by macro conditions, predominantly the pathway of inflation and interest rates, globally. The UK still stands out in terms of inflation, in that whilst many countries are battling with high inflation environments, the UK appears to be showing stickier inflation. Whilst energy prices have stepped back, we are seeing areas such as food inflation in the UK remain at high levels; and wage inflation as well as a strong labour market continue to support consumer spending. Without a recession, there remains the challenge of how inflation gets controlled; interest rates having already been increased significantly, but often taking some time to have an impact. China is the region where Covid-19 and the re-opening still remains uncertain, with other countries having returned to some ‘normality’. The combination of these factors creates a very uncertain environment, which continues to drive market challenges.

We would also remind investors of the geographic exposures of the portfolio companies’ revenues. At the time of writing, 51% of revenues are generated in the UK, with 49% overseas. This is similar to the exposure within the Company’s benchmark. Many of the companies in the portfolio, as has been true through time and a result also of our investment process, have strong international growth exposure. Some are global leaders in what they do. One challenge in the upcoming period for overseas earners is the current strength of Sterling, which, if it continues, may cause some currency headwinds for these businesses.

In a recessionary environment, or continued low economic growth, we believe the market will move towards quality, resilience, reliability, visible revenue streams and strong balance sheets. We have seen these characteristics fundamentally demonstrated by the portfolio companies over this period, clear also through the dividend strength. In that economic situation, where growth becomes scarcer, the growth that remains tends to become more valuable.

In a recovery phase, small and mid-cap stocks tend to lead that market recovery, and the outlook for the asset class should be attractive. Small and mid-caps in the UK have still lagged large companies in the market moves since the start of 2022. In that environment, we believe the small-cap asset class can produce some attractive return potential, as markets recover and the disparity to large-cap narrows. Encouragingly, the Company outperformed in the sharp market recovery in Q4 2022, with quality growth companies performing well.

We continue to believe there are opportunities for quality growth businesses, which deliver well on earnings expectations, to outperform. The valuations currently being paid for growth companies in UK small mid-cap markets remain significantly below historic levels, whereas in other regions the market is now paying a ten-year median valuation for growth businesses again. As such, many quality UK growth companies currently trade on undemanding valuations.

. . . . . . . . . . .

Jeremy Rigg, chair, Henderson High Income – 13 September 2023

In the near term the outlook for markets will be driven by inflation expectations and the impact this will have on monetary policy. There are certainly some signs that inflation is easing a little, particularly in the US and across Europe. However, inflation in the UK is proving more problematic, and although the Bank of England has increased interest rates significantly in the first half of 2023, the expectation in the market is that they may have to rise a little further.

The UK corporate sector is in the midst of the interim results season and whilst there are certainly pockets of weakness, corporate results are for the most part holding up well. In particular, UK banks have announced positive updates showing relatively little sign of corporate and personal sector weakness, and capital levels within the banks are at very positive levels. In addition, the UK housing market, which is very important to the UK economy, is holding up reasonably well at this stage.

UK companies still appear to be relatively attractively valued in a global context.

. . . . . . . . . . .

Investment managers, Onward Opportunities – 7 September 2023

We believe the market’s implied base case global outlook is for an economic slowdown. Negative forward indicators include inverted yield curves, declining energy and industrial material prices, falling producer prices and a faltering Chinese recovery. As a result, most large investors remain cautiously positioned with lower-than-normal risk asset exposure and higher-than-normal cash holdings, meaning illiquid risk assets such as UK small-caps remain attractively valued.

It was disappointing but perhaps unsurprising that investors did not view UK equities as a safe haven in this period. Although various bodies including the OECD, IMF and OBR have upgraded assessments of the UK’s economy, the UK market has remained sluggish with all indices falling.

One feature of these market conditions has been the impact of private equity backed bids for UK listed companies, as the first quarter flurry of bids faded. EQT’s substantial offer for Dechra Pharmaceuticals and offers for Medica and Alfa Financial Software highlighted how other investors will recognise value if public markets don’t. With Japan at long last re-rating, the UK does look increasingly isolated as the final value play among developed equity markets.

Many less liquid smaller UK companies now resemble the “cigar butts” of Warren Buffet’s much quoted quip – “like picking up a discarded cigar butt” astute value investors should look for companies that have been overlooked but still have value in them. The AIM segment is our preferred investment hunting ground, and we look forward to today’s value becoming tomorrow’s accepted recovery and momentum plays. We are very conscious that the timing of sentiment transition is always unknowable, but believe that the end of rate increases will be a positive catalyst.

. . . . . . . . . . .

Asia

(compare Asian funds here)

What of the outlook for ASEAN economies and stock markets? To us it feels like a mixed bag, economies are probably not completely stuck in a middle income trap but there are significant challenges to drive stronger growth. Educational attainment in India and the ASEAN region, whilst improving on the United Nations Development Programme’s (“UNDP’s”) Education Index, has a long way to go to catch up with developed Asia, and 50% of children in the region still only get primary-level schooling.

Other indicators also suggest economies in ASEAN face hurdles to significantly accelerate growth. The transparency international surveys of corruption perceptions suggest little relative improvement in the region outside of Vietnam, whilst the Heritage Foundation Economic Freedom Index also indicates large gaps in policy-making remain to create dynamic capitalist economies in ASEAN countries (admittedly the Heritage Foundation is a US conservative think tank and may be biased however, stock markets without functioning capitalism and strong property rights etc don’t work as any frontier fund investor knows).

Going back to stock markets in ASEAN, they face a lack of dynamism too. New Economy (technology, internet etc.) stocks are a very small part of the indexes in ASEAN, and R&D spending relative to GDP is very low. This has tended to mean both the economies in the ASEAN region and stock markets exhibit a lack of dynamism which limits their potential. This is not all bad as the ASEAN stock markets can be quite defensive but for your portfolio managers if we want to be defensive, we would prefer to buy the high-yielding stocks listed in the developed Asian stock markets as discussed earlier.

Of the four ASEAN stock markets, we are currently more optimistic on Indonesia and the Philippines. Malaysia and Thailand both appear to be stuck in classic middle income traps, with poor policy-making and politics in Thailand in particular messy. Neither stock market has much bottomup attraction at the current time. Indonesia is the most interesting market. Policy-making and stability has generally improved under President Jokowi and the country should undoubtedly benefit from the “green” transition given its exposure to key commodities like nickel. Upcoming elections in 2024 are key but we are hopeful we will see a continuation of current better policies. We are likely to use any dips in the market on election worries to add to our weighting in Indonesia.

India we do however view somewhat differently from the ASEAN economies and stock markets. On current policy settings the potential for an acceleration in the sustainable growth rates is high. India has a young population, and many structural dynamics are in its favour – whether that is better infrastructure provision, improved educational attainment, digitalisation of the economy, stronger property rights and bankruptcy laws, rising financialisation and urbanisation as mortgages become widely available.

. . . . . . . . . . .

Europe

(compare European funds here and here)

Alexander Darwall, investment manager, European Opportunities Trust – 22 September 2023

Investor sentiment regarding Europe is not good. Europe has been a structurally lower growth region than North America and Asia. This pattern is unlikely to change soon. Indeed, Europe remains vulnerable to further energy shocks. The EU’s target, as set out in its ‘Fit for 55′ is the reduction of EU emissions by at least 55% by 2030. The corollary is that renewable energy should reach 45% share of the total energy mix by 2030. Reaching these goals has an economic cost. Accordingly, we select companies that have a global reach, tapping into faster growing regions, and companies where energy costs are a lower component of the overall cost base.

The European economy has proved to be surprisingly resilient, buoyed by robust consumer spending. Driven by the joint impacts of monetary and fiscal stimulus, the post-pandemic period has been one characterised by abundant liquidity and a resilient consumer. However, as the ECB’s asset purchases continue to unwind and consumers deplete their pool of excess savings, we see a different dynamic unfolding, a less resilient economy and more subdued consumer spending.

Our companies, typically, have lots of intellectual property (IP) and innovate extensively, meeting customers’ needs. New technologies will continue to drive innovation and create new business opportunities. Most prominent of these emergent technologies is Artificial Intelligence (AI). In our view, the biggest beneficiaries of this development will be those companies that have proprietary, monetisable data, and those that provide infrastructure to accommodate significant computing applications, fitting exactly the profile of our investee companies. These same IP intensive, innovative businesses have pricing power and discipline, a crucial factor in softer economic conditions. We remain confident in our strategy and in the positioning of our portfolio. Our lower exposure to consumer spending and input cost dependency positions us well. Moreover, the strong balance sheet and profitability profiles of our companies positions them well not only to survive in more challenging conditions, but to thrive as competitors lack the cash flows to invest through the cycle and as new M&A opportunities emerge.

. . . . . . . . . . .

Japan

(compare European funds here)

Masaki Taketsume, investment manager, Schroder Japan Trust – 29 September 2023

We believe that the Japanese equity market currently provides one of the most attractive opportunities, particularly for long-term investors. Several developments that are unique to Japan should combine to support sustained corporate earnings growth and increasing valuation multiples in the years ahead.

From an economic perspective, we should see a continued cyclical recovery following the lifting of Covid restrictions. More importantly, after more than two decades of deflationary pressure, the emergence of “positive” inflation, led by wage growth, is immensely encouraging. Not all inflation can be viewed as positive, but Japan is experiencing lower rates of inflation than in many other parts of the world. This suggests that the re-emergence of inflation in Japan can be viewed as an opportunity rather than a threat.

Indeed, the implications of this positive inflation should not be under-estimated for corporate Japan. This is an environment in which Japanese companies can regain pricing power (the ability to raise prices in response to inflation) which, when coupled with improved consumer purchasing power through wage increases, should drive healthy levels of corporate earnings growth. An element of these higher profits can then be recycled back into the economy through further wage increases, driving a positive cycle of broader economic progress that has been largely absent from Japan for a generation.

Meanwhile, corporate governance reforms are likely to remain a structural driver of the Japanese equity market in the years ahead. Historically, the structure of corporate Japan has been dominated by the keiretsu system of cross-shareholdings and close relationships between customers, suppliers, their banks and competitors. This system has been increasingly criticised from a governance perspective because it can lead to inefficient capital allocation and poor decision-making. In recent years, however, we have begun to see meaningful change, with companies, investors and regulators such as the Tokyo Stock Exchange, working together to raise corporate governance standards, with the aim of improving returns and growth prospects. The success of these initiatives is reflected in the level of dividends and share buybacks from Japanese companies. These have been rising steadily in recent years and currently stand at record levels, but there remains scope for considerable further positive progress as the corporate governance revolution unfolds.

The Japanese stock market has reached multi-decade highs in recent months in response to these positive domestic developments. Nevertheless, the equity market as a whole looks attractively valued when compared to other regions’ markets and in the context of history. Many listed Japanese companies continue to trade below their book value despite the ongoing corporate governance movement. This suggests the market is not yet fully reflecting the progress that many businesses are making to improve returns. We are confident we can continue to find selective opportunities for businesses to transform both their growth prospects and their market rating through better capital allocation and by considering the needs of all their stakeholders, shareholders included. These opportunities remain concentrated at the lower end of the market cap spectrum, where valuations are also even more attractive, despite the high quality of many businesses and their superior growth potential.

To conclude, there are many reasons to believe that we may be entering a period of sustained outperformance from the Japanese stock market. We are seeing renewed appetite for Japanese equity from global investors and this demand should continue to grow as the positive domestic story becomes better understood. This represents a fertile environment for active, high conviction stock pickers, and we are excited at the opportunity that lies ahead for investors in the company.

. . . . . . . . . . .

Manager, Baillie Gifford Shin Nippon – 22 September 2023

The first half of this year saw a bifurcation in performance within the Japanese market. Mature large cap stocks in capital intensive and cyclical sectors did very well in share price terms, helping lift the broader Japanese indices to record highs. Their strong performance was largely due to improvements in corporate governance and shareholder return policies. A key driving factor for this has been the pressure applied on management teams by both domestic and overseas activist investors who have taken large stakes in many of these businesses. In addition, Yen weakness has helped inflate profits as most of these companies are exporters. In this environment and amid a complete lack of investor interest, high growth small cap stocks continued to languish.

At a macro level, rising interest rates, inflation, and US-China tensions continue to sour investor sentiment on growth stocks. A slowing Chinese economy and signs of excess inventory in critical sectors like semiconductors and industrial equipment are further dampening market confidence. In this context, it is perhaps unsurprising to see weak operating results being reported by many of our manufacturing holdings exposed to these end markets. More encouragingly and contrary to their weak share price, most of our internet holdings continue to perform admirably well in operational terms.

. . . . . . . . . . .

Joe Bauernfreund, investment manager, AVI Japan Opportunites Trust – 15 September 2023

The Japanese Yen weakness was driven by a cautious tone from Kazuo Ueda, the newly appointed Bank of Japan (“BoJ”) governor, which disappointed those anticipating an imminent end to the BoJ’s Yield Curve Control (“YCC”) policy. Latest data for June showed a 4.2% increase in core inflation (excluding food and energy) which is starting to flow through to higher wages. We think it isn’t a matter of if we will see material adjustments to YCC, but when – which would be a boon for the Yen.

Over the period however, small-caps lagged, with the MSCI Japan Small Cap Index returning only +15.4%. With the rally led by large-cap value, the MSCI Japan Value Index appreciated +22.8% (both in JPY). During a period of strong foreign flows into Japan, it is typical to see early capital allocated towards large cap names. As the rally is sustained, however, we would expect there to be a trickle-down effect as capital seeks out smaller and better valued opportunities. Given AJOT’s portfolio has an average market cap of £675m, we are well placed to benefit.

The Tokyo Stock Exchange (“TSE”) followed through on its announcement at the end of last year calling on companies to address low valuations. This is mostly aimed at the 1,800 companies in Japan that trade on a price to- book ratio of less than 1x. Companies will need to determine why the market evaluates their shares so lowly and disclose plans to improve the valuation. It is an encouraging step, highlighting regulators’ intentions to continue using their powers to promote governance reforms.

It feels that the stars are starting to align in Japan. Our approach to engaging with undervalued, high-quality companies is bearing fruit and, particularly if we see a reversal in Yen weakness and increased flows into small caps, we could be in for a period of strong NAV growth.

. . . . . . . . . . .

North America

(compare North American funds here and here )

Managers, Middlefield Canadian Income–21 September 2023

We believe cyclical value sectors are poised to outperform in H2 and that Canadian equities are uniquely positioned to benefit from this setup. The recent strength in commodity prices supports our view that the Canadian dollar should appreciate relative to the British Pound in H2 after depreciating 3.3% in H1. Our highest conviction sectors are real estate and energy, as reflected by the Fund’s current asset allocation. Both sectors have historically acted as effective hedges against inflation which is expected to remain elevated over the medium-term. Growth stocks that demonstrated market leadership during H1 are starting to screen as expensive, especially with monetary policy expected to remain restrictive for longer. The relative value that Canadian cyclicals currently offer further strengthens our conviction. Canadian companies have returned record amounts of capital to shareholders recently in the form of dividends and share buybacks. This is a trend we expect to continue in H2 as earnings outlooks improve due to better-than- feared economic conditions.

. . . . . . . . . . .

Stephen White, chair, Brown Advisory US Smaller Companies – 18 September 2023

So far in 2023, both the US economy and the US stock market have defied expectations on the upside. Despite major headwinds comprising a huge jump in interest rates, persistent inflation, the depletion of pandemic era savings, concerning geopolitical tensions and a minor regional banking crisis, the US consumer has remained resilient and continued to drive the American economy.

As a result, the recession forecast by many a year ago has failed so far to materialise. The stock market has responded positively, and it has been supported further by hopes that the peak in interest rates is within sight.

Given the market’s rise to date, some setback should not, of course, be ruled out. While the Federal Reserve may have paused its rate increases in June, this was done merely in order to take stock and assess the impact so far. With the resilience of the economy and still high inflation numbers, the trajectory for interest rates remains upwards in view of the Federal Reserve’s determination to bring inflation back into its target range. The difficulty for the Federal Reserve is in determining at what point the rise in rates will achieve this, without putting the economy severely at risk. With the Federal Reserve putting inflation restraint before economic activity, there is a risk that investors underestimate the extent and duration of tightening potentially to come.

At the same time, the geopolitical concerns remain, the economy may slow if the consumer finally becomes more cautious and corporate earnings may be impacted.

As we look further out, we become more optimistic. We expect the Federal Reserve’s tough medicine to work and for the inflation numbers as we enter the autumn to trend lower, allowing interest rates to ease back too. Although possibly somewhat softer, we still expect the domestic US economy to hold its own, with demand supported by recent wage growth and still high levels of employment. We see this as a generally favourable background for the US smaller company sector which should again draw investors given its attractive valuations and extended period of underperformance relative to its larger peers.

. . . . . . . . . . .

Emerging Markets

(compare emerging market funds here)

Managers, BlackRock Latin American Investment Trust – 29 September 2023

The outlook for the Mexican economy remains positive as it is a key beneficiary from the re-shoring of global supply chains. Mexico remains defensive as both fiscal and the current accounts are in order. While our view remains positive, we have taken profits after a strong relative performance, solely because we see even more upside in other Latin American markets such as Brazil. In addition, we believe that the Mexican economy will be relatively more sensitive to a potential slowdown in economic activity in the US in response to rising interest rates there.

We continue to have a very positive view on Brazil, even though our thesis of slowing inflation and sound fiscal policies has partially played out already. While the market is now pricing in interest rate cuts, these have not yet started, and the positive economic impact is yet to come. In addition, while international investors have moved capital to Brazil, local equity flows have continued to be negative year-to-date as equity markets struggle to compete with a risk-free rate of return of close to 14%. We therefore see Brazil as very early stage in its positive economic cycle and continue to see further upside over the next 12-18 months. We have significantly scaled back our positions after the strong performance, but domestic Brazil remains a dominant bet in the portfolio.

Political uncertainty has been the overriding market sentiment in other countries in Latin America. We believe this will continue to impact market performance, and we have a cautious view on Chile, Colombia and Peru. However, despite the political headwinds in Colombia, we are seeing a slow improvement in macroeconomics and believe it can become an attractive market again once the political climate stabilises.

In a global context, we remain optimistic about Latin America as a whole. Central banks have been proactive in increasing interest rates, which has now resulted in falling inflation. Thus, we will likely see a monetary easing cycle in most countries in Latin America, which should support both economic activity and asset prices. In addition to this normal economic cycle, the whole region is benefitting from being somewhat isolated from global geopolitical conflicts. We believe that this will lead to both an increase in foreign direct investment and an increase in allocation from investors across the region. As such we are optimistic about the outlook for Latin American stocks over the next 12-24 months.

. . . . . . . . . . .

Aidan Lisser, chair, JPMorgan Emerging Markets Investment Trust – 27 September 2023

Developments in China were one of the main factors impacting emerging markets over the past year. With demand for exports weakening and the heavily indebted property market under severe pressure, near-term economic growth is likely to remain well below pre-pandemic levels.

However, it is important to stress that our Portfolio Managers are focused on the bottom-up fundamentals of the high-quality businesses that they own or target, and the growth prospects of those companies over the long-term. Whatever the country’s near-term economic prospects, the Chinese market will still offer appealing investment opportunities capable of generating excess returns for the Company’s shareholders. Furthermore, while the Chinese market continues to face challenges over the coming year, it is evident that many other emerging markets have done well – inflation pressures are less extreme, their currencies have been strengthening and companies have performed strongly. Opportunities in these markets will remain plentiful.

In addition, the long-term case for emerging markets remains robust – based on superior economic growth, favourable demographics, increasing consumption and the presence of high-quality companies and managements.

. . . . . . . . . . .

Managers, Gulf Investment Fund – 25 September 2023

The outlook for the GCC in 2023 remains positive, driven by benign inflation, giga & mega infrastructural projects, and continuous reforms across social and economic policies. The IMF projects GCC to grow by 2.9 per cent and 3.3 per cent in 2023 and 2024, respectively; after growing at 7.7 per cent in 2022 from a lower base. This compares to World GDP growing at 2.8 per cent in 2023 and 3.0 per cent in 2024.

The IMF expects CPI inflation in the GCC to be 2.9 per cent and 2.3 per cent in 2023 and 2024 vs 4.7 per cent and 2.6 per cent for the advanced economies, respectively. The lower inflation in the GCC economies gives the necessary bandwidth to the GCC governments to continue and/or increase their fiscal spending at a time when the contribution from oil is expected to decline driven by production cuts by Opec+ and a slowdown in global economy.

The pace of structural reforms in the GCC was maintained during the covid period of 2020-2022 due to which growth in the non-oil GDP is expected from fixed investments, private consumption, and high government spending ensuring diversification and unabating increase of the non-oil share in the economy.

The global economy is under an overhang of an ongoing invasion of Ukraine by Russia, and an economic softness due to high-interest rates. Against such a backdrop, the GCC is a bright spot on the global map where the above-mentioned headwinds are positively offset by domestic public and private spending.

. . . . . . . . . . .

India

(Compare India funds here)

Managers, India Capital Growth Fund – 21 September

Whilst the ongoing conflict between Russia and Ukraine is having an impact on the supply and cost of energy and agricultural commodities for many of the world’s economies, the Indian economy has been less impacted than most others: India’s dependency on imported oil remains but the overall economic impact has been offset by the increasing value of India’s IT exports and the government no longer directly absorbs the cost of rising oil costs. Indeed, India has been the beneficiary of a global corporate trend to diversify supply chains, with many corporates having realised the risk of been overly dependent upon Chinese manufacturers.

India’s inflation is not driven by weak monetary policy, wage pressure or the expectation of wage increases, and India is self-sufficient in agricultural commodities meaning the risk of high inflation having a detrimental impact upon the Indian economy is much less than in many other countries.

. . . . . . . . . . . .

South Korea

(compare country specialist funds here)

Managers, Weiss Korea Opportunity Fund – 19 September 2023

On a year-to-date basis ending 30 June 2023, the benchmark Korea Index returned 14.4% and the KOSPI 200 Index returned 16.1%.21 To contextualise these returns, Korea was one of the best performing markets in Asia alongside Taiwan and Japan.39 Looking into daily trade flow and volume, foreign investors were the largest net buyers, accumulating more than 12.3 trillion KRW net in the first half of 2023, according to the Korea Exchange.40 However, unlike previous market cycles, the stock market gains were not evenly distributed across a wide range of sectors. While the information technology (including memory semiconductors) and materials (including EV batteries and other materials) sectors outperformed the Korea Index, the utilities, healthcare, financials, and consumer staples sectors generated negative returns. Foreign net buying was also concentrated in select sectors and names. For instance, out of the 12.3 trillion KRW in net buy flow by foreigners, 12.08 trillion KRW (roughly 98%) was focused on one issuer: Samsung Electronics.41

More broadly, the South Korean economy finally began to exhibit signs of a rebound during the second quarter of 2023. Korea’s exports posted a meaningful rise during the final two months of the quarter, even escaping a trade deficit for the first time since February 2022.42 The improvement in the balance of trade was led by trade exports, which grew 7.9% and 13% in month-over-month terms in May and June, respectively.43

Focusing exclusively on rebounding exports and the surge in a few risk asset prices, however, would present an incomplete view of the South Korean economy. As Governor Rhee noted at the most recent Bank of Korea Monetary Policy Board meeting on 13 July 2023, other macroeconomic indicators still require careful attention, such as persistent high core CPI inflation and significant household debt.44 For instance, while year-on-year CPI increases moderated to 2.7% in June 2023 from a high of 6.3% in July 2022, core CPI increases remained in the 4% range in June 2023 from a high of 5% in January 2023, according to Statistics Korea.45 Household debt remains at 103% of GDP, which is an area that the Bank of Korea is “closely monitoring”.

As we noted in the 2022 Annual Report, we continue to observe early but positive signs in the realm of corporate governance in South Korea. The source of activist demands, volume of requests and success rates of adding board members to target boards all appear to exhibit positive directionality. We have also witnessed the Korean government more actively pursuing corporate governance reforms as described later in the report.

Much of the support in favour of reform is now originating within Korea, particularly from domestic activist funds and the Korean government. This is new, as historically such support mostly arose from non-Korean investors and organisations which were ineffectively attempting to exert shareholder-friendly pressure. According to Insightia, which publishes regular reports on the state of shareholder activism in Asia, approximately 75-80% of activism campaigns launched in South Korea in 2022 were “by funds based in Korea or run by Korean fund managers,” which is an increase from the 60% Insightia reported for 2019.58 We believe this dynamic is likely to make companies more agreeable to positive reforms.

We are also encouraged by the volume and success of activist campaigns seeking to add board members to the boards of targeted companies. The absolute number of campaigns increased more than 480% from 2019 to 2022. The success of these campaigns is also increasing; in 2020, no activists were successful in putting one or more of their nominees on the target company’s board, whereas in 2022, 10 campaigns succeeded on this measure.

. . . . . . . . . .

Vietnam

(Compare country specialist funds here)

Vu Huu Dien, Investment managers, Vietnam Enterprise Investments – 13 September 2023

The performance of the VN Index in the first six months of 2023 was characterised primarily by two factors: (1) the repricing of market valuations, in which sectors and stocks that were oversold and hit multi-year low valuations have been readjusted upwards; and (2) the initial optimism that the Government’s policy actions will start to have a material impact in the economy from the second half of 2023. From a macro perspective, external factors have, so far, not had the same impact as in previous years. Barring black swan type events, external factors are unlikely to alter the current course of Government policy, focusing on easing monetary policy and stimulating the domestic economy via public and private investments. Against this macro backdrop, sectors that tap into the recovery theme should fare well in the latter half of the year.

At the end of 2022, VEIL had anticipated 2023 to be a year of consolidation and rebuilding for Vietnam. The story thus far has matched that expectation. Earnings growth in 2023 won’t be as exciting as previous years, for a high growth country such as Vietnam. Nevertheless, VEIL is expected to see an improvement in quarterly earnings and, so far, this has been the case. For the full year 2023, Dragon Capital’s Top80, which represents 69% of the VN Index, is projected to deliver 3.9% in EPS growth. More exciting growth is currently expected for 2024 at 24.4% EPS growth and only at an undemanding forward Price-to-EPS ratio of 8.1x. For VEIL, 2023 serves as an important steppingstone in further realigning the portfolio to better capture the structural growth expectations of Vietnam.

. . . . . . . . . . .

Biotech and Healthcare

(compare Biotech and Healthcare funds here)

Investment managers, RTW Biotech Opportunities – 13 September

Pharma went shopping in the first half of the year. Total deal value of US$93 billion puts sector M&A activity on track to be at the highest level since 2019. 2019’s US$328 billion total was driven by two large deals, Bristol-Meyers’ US$74 billion for Celgene Corporation and AbbVie’s US$63 billion for Allergan plc, both focused on diversification and cost savings. In contrast, recent deals have been about innovative assets that can deliver growth. Deal highlights include Pfizer’s US$43 billion for Seagen Inc., Merck’s US$11 billion for Prometheus, Novartis’ US$3.2 billion for Chinook Therapeutics, Sanofi’s acquisition of Provention Bio for US$2.9 billion and Lilly’s US$2.4 billion for Dice Therapeutics. Premiums ranged from 30% for Seagen up to 270% for Provention Bio and proxies tell the story of competitive processes. Of the three large cap pharma companies we have highlighted as most in need of patent cliff revenue replenishment (Bristol, Pfizer, and Merck), only Pfizer has addressed a significant part of its exclusivity losses this decade, not to mention the potential impact of the Inflation Reduction Act (IRA) on small molecule portfolios. With attractive valuations for midcap biotech companies and record (and growing) cash piles on large cap pharma balance sheets, we think these deals will continue.

Despite the strong pick-up in M&A, the biotech sector’s burgeoning recovery from the second worst bear market in its history flattered to deceive in the first half of the year. From the low in mid-May last year to the end of January this year, the Russell 2000 Biotech Index rallied over 40%, but then finished the first quarter -7.3%. It rallied back slightly in the second quarter to finish the first half +5.3%, but it was the only sector index to finish the half in meaningfully positive territory. The pharma heavy Arca index was +0.7%, the large cap heavy NBI was -3.2%, and the most commonly traded small cap index, the XBI, was +0.2%. At US$85.00, the XBI is trading at approximately the same level as it was in 2015 and only marginally above last year’s lows when adjusting for subsequent take-outs and transformational clinical data. As a result, sector valuations remain attractive. The NBI is trading at 5.8x price to sales, which is still only 29% above Global Financial Crisis lows. At the smaller end of the spectrum, 180 of the 578 companies with less than US$10 billion of market capitalisation are trading at less than the cash on their balance sheets.

We suspect that some negative sector headlines might have impacted sentiment in the short term (without impacting fundamentals too much). The FTC Chair Lina Khan’s push to expand the definition of anti-competitiveness beyond portfolio overlap likely dampened excitement about M&A. In the FTC’s lawsuit to block Amgen’s acquisition of Horizon Therapeutics, Khan introduced theoretical product bundling of non-overlapping products as an argument to block the deal. While we think the odds are low, should courts decide in favour of the FTC, agreements not to bundle across products seem a straightforward remedy in the same way that there were no pharma deals in the last decade that were blocked due to portfolio overlap – any issues were solvable with the divestiture of overlapping products.

The banking crisis in the first quarter also likely weighed on sentiment, especially with “biotech bank”, Silicon Valley Bank (“SVB”), featuring so heavily. This was made moot by the deposit backstop, and SVB’s orderly wind-down should have no material impact on biotech funding. However, it did conceal two significant M&A deals that happened on the same weekend: Pfizer-Seagen was the biggest deal since 2019 and Sanofi-Provention was the biggest premium paid so far this year.