An ESG leader in Asian equities

Despite the difficulties of COVID-19, Aberdeen New Dawn (ABD) has provided very strong absolute and relative returns during the last 12 months. Specifically, its returns are markedly ahead of its benchmark, the wider Asia Japan region and global equity markets more generally. Asia is emerging from the pandemic in a position of relative strength and ABD’s manager thinks valuations are at attractive levels relative to global equities.

Until recently, ABD had also benefitted from a narrowing of its discount. However, ABD’s shares now trade on the widest discount in its sector. This widening (into double digits) does not appear to be consistent with either ABD’s absolute or relative performance. It might therefore present an opportunity for investors as markets settle as economic growth gathers pace this year.

ESG considerations play an increasingly important role in stock selection and ABD’s portfolio now merits a AA score from MSCI’s ESG rating system, classifying it as a ‘Leader’ on Environmental, Social, and Corporate Governance (ESG) issues.

Capital growth from Asia Pacific ex Japan

ABD aims to provide shareholders with a high level of capital growth through equity investment in the Asia Pacific countries, excluding Japan. The trust holds a diversified portfolio of securities in quoted companies spread across a range of industries and economies. ABD is benchmarked against the MSCI All Countries Asia Pacific ex Japan Index (in sterling terms).

Fund profile

Aberdeen New Dawn (ABD) aims to provide shareholders with a high level of capital growth through equity investment in the Asia Pacific countries, excluding Japan. ABD holds a diversified portfolio of securities in quoted companies spread across a range of industries and economies. Investments may also be made through collective investment schemes and in companies traded on stock markets outside the Asia Pacific region, provided that over 75% of their consolidated revenue is earned from trading in the Asia Pacific region, or they hold more than 75% of their consolidated net assets in the Asia Pacific region.

ABD is benchmarked against the MSCI All Countries Asia Pacific ex Japan Index (in sterling terms). We have also included comparisons against the MSCI AC Asia ex Japan index, the MSCI AC World Index and its peer group within this report.

The manager is Aberdeen Standard Fund Managers Limited, which has delegated the investment management of the company to Aberdeen Standard Investments (Asia) Limited (Aberdeen or the manager). Both companies are wholly-owned subsidiaries of Standard Life Aberdeen Plc.

Aberdeen’s approach is to manage money using a team approach. We met James Thom, a senior investment manager in the team, for the purposes of preparing this note.

Market roundup – Asia, a relative bright spot

2020 was, without question, a challenging year for financial markets as the impact of the COVID-19 virus was felt around the globe. However, although the virus originated in China and quickly spread to the rest of the Asia Pacific region and beyond, many parts of the region have fared relatively well. The region has, with its experience of similar pandemics, been successful at implementing controls to restrict the spread of the virus (in comparison, more developed markets have generally struggled to get to grips with the virus). Furthermore, as we have discussed in our previous notes, the Asia Pacific ex-Japan region offers long-term structural growth opportunities – although, as with all emerging markets, it tends to exhibit greater volatility along the way.

As is illustrated in Figures 1 and 2, Asia Pacific ex Japan has since the beginning of 2020 outperformed broader global markets, emerging markets and frontier markets. However, Figure 1 also illustrates the considerable variation that can be seen within the region.

Late cycle to early cycle in six months

We have previously commented on how a strong US dollar tends to lead to outflows from emerging Asia. One effect of the pandemic is that it appears to have turned the tide on the global economic cycle, moving us from late cycle to early cycle in around six months. Hawkish monetary policy and the prospect of interest rate rises in more developed markets look a long way off, which should act as a tailwind for emerging Asia for some time.

Furthermore, it seems reasonable that the chaotic policy moves of the Trump presidency are now largely behind us and there is the possibility of a less-combative approach from the US administration in engaging with China and the wider region.

Manager’s view

The manager’s long-term arguments for investing in growth companies in emerging Asia remain broadly unchanged, and we recommend that readers see our previous notes for more discussion. It should be noted that, whilst the manager takes a macro view and long-term structural themes are factored into its thinking, the portfolio is very much managed bottom-up.

James Thom says that he is really positive on the outlook for Asian markets. He acknowledges that some areas of the market are a little frothy and have been boosted by improvements in liquidity, and he expects that there is more of this to come following the approval of President Biden’s stimulus package in the US. However, Asia continues to have a very good handle on dealing with the pandemic, which is feeding through to an improving growth outlook.

Asia – slowly getting back on track

ABD’s manager says that, overall, the economies of the Asia Pacific ex Japan region are getting back on track and are starting to see growth. James says that, for example, China has posted GDP growth of around 2%, while Taiwan and Vietnam have posted growth in the region of 3% each, all of which is feeding through to growth in corporate earnings. James now thinks that the contraction in corporate earnings in 2020 is not as bad as was initially expected. Furthermore, James is expecting to see sharp increases in earnings for 2021, possibly an average of 25%, across the region, while earnings growth of 20 to 21% is readily achievable, in his view.

James says that, despite the recent set back in share prices as markets have paused in the face of increasing long-term interest rates, the conversations the ASI team are having with companies are increasingly positive, even in hard-hit markets such as India. With respect to valuations, James thinks that these were not particularly stretched, even prior to the setback, which has provided an extra layer of comfort given an otherwise brightening outlook. James says that for now, he is focusing on price-to-book ratios as these are more meaningful in the current environment than P/E ratios, and whilst these are generally a bit above the longer-term averages, they are not unduly so. Nonetheless, Asia Pacific ex Japan in his view looks cheap relative to global and US equities, and he expects to see this Asian discount narrow as investors rotate more fully back into Asian equities as the outlook continues to improve.

Malaysia – difficult macro compounded by poor handling of COVID-19

A key exception to Asia’s generally-good handling of the COVID-19 pandemic has been Malaysia, which was forced to institute a lockdown in January, although the signs are that the government is now gradually easing these restrictions. As we have previously discussed, ABD has not held any exposure to Malaysia for some time as the manager considers that against a poor macroeconomic backdrop, the risk-reward ratio for prospective portfolio candidates is not currently compelling. Malaysia, along with other markets in the region, has suffered from the US-China trade war, but it also has the additional burden of a very large debt pile left behind by its former government.

Indonesia and the Philippines have also struggled in the handling of the pandemic, while Taiwan, Korea, and Vietnam have been able to avoid mass outbreaks and have been successful in keeping their coronavirus-related deaths low.

Investment philosophy and process

ABD’s portfolio is managed by ASI’s Asian equities team. There was very little impact on the makeup of the team following the merger between Aberdeen Asset Management and Standard Life that formed Standard Life Aberdeen. However, there is an increased emphasis on individual team members having responsibility for researching a specific sector rather than managing research along geographic lines.

Stock selection is key to portfolio construction, but thematic insights (such as technological developments) and structural changes to industries influence stock selection. The core tenets of the Aberdeen approach to managing money are as follows:

- a, long-term, buy and hold strategy;

- a research-intensive process with an emphasis on meeting management; and

- a bias towards high-quality companies (where quality is determined by an assessment of management, business focus, the health of the balance sheet and corporate governance).

A preference for and the promotion of good corporate governance is an important part of the approach. In recent times, Aberdeen has broadened this to include an evaluation of both the environmental and social impacts of a potential investment. However, the importance of ESG considerations has seen a marked uplift during the last 12 months as the ASI team has expanded the resources that it is allocating to this area (see below). ESG analysts continue to be embedded within the investment management team. Aberdeen is not an activist investor, but sees the value of engaging with companies.

No stock is bought unless the manager has met management and follow up meetings are held at least six-monthly. The team had over 1,600 meetings with companies last year.

Any member of the team can put forward a new investment idea, but initial research tends to be carried out by the relevant sector and geographic specialist. Ideas are circulated internally and discussed at team meetings until a consensus has been reached.

With respect to assessing the potential reward available from a stock, an analysis is made of key financial ratios, the market that the company operates within, the peer group and the company’s business prospects.

Risk assessment is focused on ensuring that the portfolio is adequately diversified (on a range of metrics) rather than formal sector or geographic controls. Little attention is paid to market capitalisation, but an evaluation of liquidity does have a role.

New additions to the portfolio tend to be introduced at a 0.5% weighting and will be increased only after they have been tracked for a while and the investment thesis appears to be working. Thereafter, position sizes are driven by conviction and the manager’s assessment of portfolio diversification.

In the day-to-day management of the portfolio, the manager seeks to take advantage of anomalous price movements to either top-up or top-slice positions. This typically accounts for the bulk of turnover activity. Sales are often also triggered by M&A activity; the manager believes that its emphasis on high-quality companies results in selecting stocks for portfolios that are also likely targets for takeovers. Sales will also be made when the manager’s investment thesis does not go to plan.

The trust’s current gearing level is around 7% and it uses gearing conservatively where opportunities arise. ABD does not hedge currency risk on a continuing basis but may, from time to time, match specific overseas investment with foreign currency borrowings.

Markedly superior ESG credentials versus benchmark

James Thom has advised that, over the course of the second half of 2020, the ESG rating of ABD’s portfolio, as scored by MSCI, has improved from a rating of A to AA. The benchmark, in comparison is BBB. More information on MSCI’s rating system can be found at msci.com/our-solutions/esg-investing/esg-ratings; however, to summarise:

- Companies rated as AA and AAA are defined as ‘Leaders’ – a company leading its industry in managing the most significant ESG risks and opportunities;

- BB, BBB and A are defined as ‘Average’ – a company with a mixed or unexceptional track record of managing the most significant ESG risks and opportunities relative to industry peers;

- CCC and CC are defined as ‘Laggards’ – a company lagging its industry based on its high exposure and failure to manage significant ESG risks.

With ABD’s portfolio moving from the top end of average up to a leaders rating, this illustrates that the manager is making significant progress on ESG issues. James Thom also says that the carbon intensity of ABD’s portfolio looks good and is well below that of the benchmark.

The ASI team has been improving the ESG processes and data collection. As illustrated above, it now has access to MSCI’s ESG data. James says that the team still does its own ESG work, but will then use MSCI’s system to compare and contrast and highlight where there may be differences in their analysis that would benefit from additional work. ASI also now purchases carbon data and analytics from Trucost (trucost.com/capital-markets/eboard-data-analytics) through which it can analyse its portfolios and potential investments. Trucost offers a “verified and complete 10-year time-series carbon emissions data and disclosure metrics across company operations and supply chains representing 93% of global markets by market capitalisation”. This is enhanced by in-depth energy data from coal power production and fossil fuel reserves to energy transition, carbon price risk exposure, physical risk impacts and ”2-degree” alignment assessment.

ASI has also been developing its own ESG in-house scoring system, and every analyst can now drill into this database. This allows the analyst to see both the score and any issues that have been highlighted with the company.

It is worth noting that Aberdeen has historically held strong corporate governance of investee companies at the heart of its process, as it sees this as being key to companies’ commercial success and for shareholders receiving the benefits of that commercial success. However, it has been advancing its ‘E’ and ‘S’ credentials, and, with the improvement in the portfolio rating in the MSCI ESG scoring system, there is clear evidence that this improved approach to ESG is impacting both research and portfolio construction. As noted above, now that the portfolio has an ESG score, James gives consideration to how portfolio adjustments will impact this ESG score, when he is looking to make changes to the portfolio.

Asset allocation

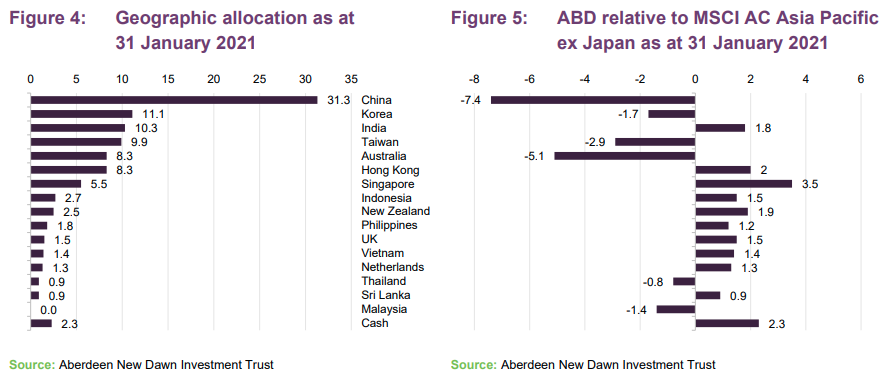

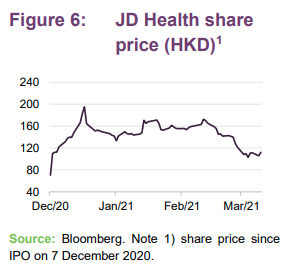

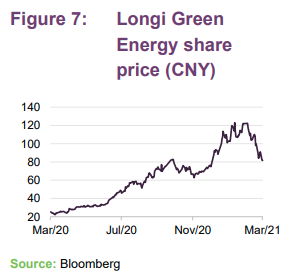

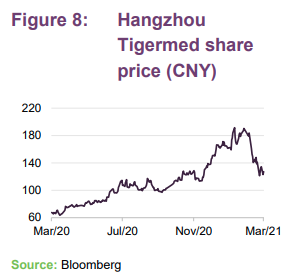

As at 31 January 2021, ABD held 54 holdings in the portfolio, which is an increase over the 52 stocks it held at 30 June 2020 (the most recently available data when we last published). Previously, we have commented that ABD’s manager had been increasing the trust’s exposure to China. More recently, the overall Chinese exposure has held steady at around 31%, but the manager has been reducing exposure to the China A-share Fund and rotating this into direct equity holdings. James says that China has been a healthy hunting ground recently, and this is why several new names have been added to the portfolio. In each case, the manager has started with a small position, which it is gradually building. It has generally been broadening the portfolio in sectors where they already have exposure, such as the internet, healthcare and green energy stocks. Examples include Alibaba (see top 10 holdings section below), JD Health International, Longi Green Energy Technology, Yunnan Energy New Material, China Tourism Group Duty Free and Hangzhou Tigermed. A new position has also been added in Fisher & Paykel Healthcare of New Zealand.

JD Health International

JD Health International (ir.jdhealth.com/en) was established as a subsidiary of JD.com (along with Alibaba, which is discussed below, JD.com is one of two massive B2C e-commerce platforms in China). The company, which is China’s largest online retail pharmacy, had its IPO on the Hong Kong Stock Exchange in December, in which ABD participated. JD Health issued 381.9m shares, pricing these at HKD70.58 per share and, as is illustrated in Figure 6, the shares have surged following listing. Even after the recent setback, they remain significantly above the issue price. ABD’s manager says that the company has a differentiated anchor position in this market, and with plans to go into online consultations, it is very well positioned to capture the growth in this particular sector. However, James also believes that is very well placed to benefit from the fast-growing healthcare market in China.

New renewable energy holdings

China has recently pledged to be carbon neutral by 2060 and it has said that it will be at peak carbon in 2030. ABD’s manager believes that renewable/clean energy will feature very heavily in China’s next five-year plan and is expecting to see a lot of investment in this space, with considerable opportunities in solar and wind generation, as well as nuclear. Reflecting this, the manager has added Longi Green Energy Technology (en.longi-solar.com) to the portfolio. The company is the world’s largest manufacturer of solar wafers and, according to ABD’s manager, is very cost-competitive in this market. The manager believes that the company is very well positioned to capture growth in both its domestic market and internationally.

The manager also added a position in a Yunnan Energy New Material Co, which is a chemical company that is primarily focused on the production of critical battery components, where ABD’s manager says it is a market leader. This differentiates it from LG Chem, another ABD holding, which makes whole batteries and primarily services European auto manufacturers, whereas Yunnan Energy is primarily servicing Chinese manufacturers.

New healthcare holdings

The manager has established new positions in Hangzhou Tigermed and Fisher and Paykel Healthcare. Hangzhou Tigermed is listed in both the A-share and H share markets, and ABD holds both. The manager says that the company is similar to Wuxi Biologics (see page 12) in that it provides contract services to the biotech sector, which is booming in China. James says that Hangzhou Tigermed conducts more clinical trials and has good relationships with hospitals, which helps it to facilitate these.

Fisher and Paykel Healthcare is a New Zealand company that is the global market leader for respiratory systems sold into hospitals. It has seen a big rise in demand as a result of the pandemic. However, this is leading to an increase in consumables, and so ABD’s manager is expecting to see a sustained increase in revenues, rather than just a one-off uplift.

China Tourism Group Duty Free

The manager has also initiated a position in China Tourism Group Duty Free on share price weakness. ABD’s manager says that Chinese tourism has been driving duty-free spending globally, but from a domestic Chinese perspective, China has struggled to capture this. However, there is a lot of domestic tourism within China and the government is keen to try and keep some of revenue from this consumer spending at home. James says that the ASI team is expecting to see a change in the regulation to effectively bring this spending back onshore. He thinks that China Tourism Group Duty Free is the company that is best-positioned to capture the most benefit from these changes in the regulations.

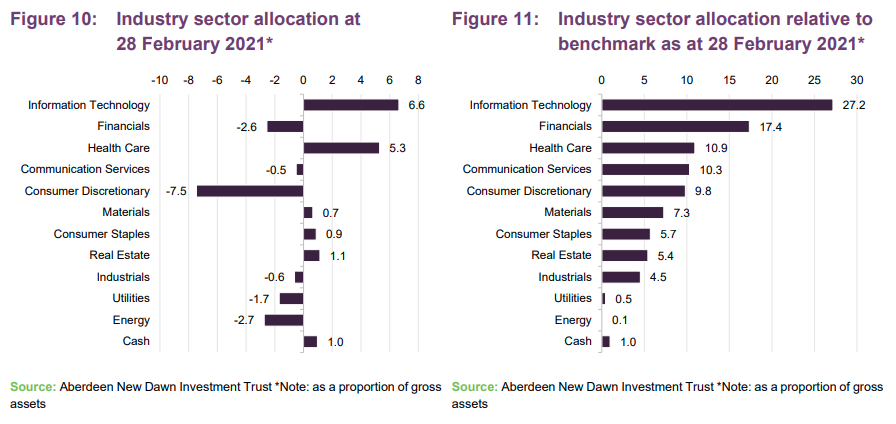

Relative to the benchmark, ABD has a notable underweight exposure to consumer discretionary, as well as underweights to energy and utilities and financials. Instead, the manager has a preference for structural growth opportunities within technology and healthcare, which are key themes within the portfolio. The internet is still seen as a positive force, with Tencent providing the primary exposure.

Top 10 holdings

Figure 12 shows ABD’s top 10 holdings as at 31 January 2021 and how these have changed since 30 June 2020 (the most recently available data when we last published). Holdings that have moved in to the top 10 are Alibaba and Wuxi Biologics. Names that have moved out of the top 10 are Bank Central Asia and Ayala Land. We discuss some of the more interesting changes in the following pages. Readers interested in other names in the top 10 should see our previous notes, where many of these have been previously discussed (see page 25 of this note). We have discussed some of the more interesting changes below.

Alibaba (2.4%) – Added to ABD’s portfolio on weakness in Q4 2020

Alibaba (alibaba.com) is the largest e-commerce company in China. Headquartered in Hangzhou, the company is also present in the e-commerce market through its ownership of the Taobao, Tmall, and Alibaba1688 websites, all major e-commerce platforms in China. ABD’s manager initiated a position in Alibaba in Q4 2020, having not held it previously on corporate governance concerns, although it otherwise liked the business.

James Thom says that Alibaba has made a lot of progress in terms of corporate governance during the last two to three years. With Jack Ma stepping back from the business, key man risk has been reduced and, crucially, Alibaba is now less tied to Jack Ma and his associates. There has also been a change in the variable interest entities (VIE) ownership structure that had previously given the manager concerns.

James also says that the Aberdeen team is now getting better access to management, including senior individuals (having previously struggled with this). The team has found management to be very open to engagement. James says that they now have a lot more insight into the accounts, aided by the ANT Financial IPO process. Although this IPO was subsequently pulled, Aberdeen‘s managers were able to drill down into the prospectus, which they found to be very useful, and the ASI team concluded that Alibaba had now cleared their quality hurdle. James says that, prior to the announcement of the probe in the fourth quarter, Alibaba had been going from strength to strength.

James said that they began to build the position prior to the ANT Financial IPO being pulled, but were then able to increase the position significantly on weakness. James says that he remains cautious on Alibaba, which is why it is an underweight position, but expects this to increase as he gains confidence.

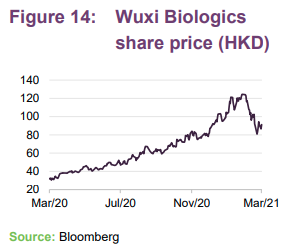

Wuxi Biologics (2.3%) – positive tailwind from COVID-19

Wuxi Biologics (wuxibiologics.com) has been a constituent of ABD’s portfolio since June 2018. The company works as a sub-contractor to a number of biotech companies that wish to outsource part of their R&D work and/or manufacturing process. It assists biotech companies with the discovery, development and manufacture of biologics. It has operations in the US, Ireland, Germany and Singapore in addition to China, and has received EMA and FDA approval for its Chinese facilities.

When we first discussed Wuxi in our October 2018 initiation note (see page 10 of that note), we said that the manager believed that the company was becoming a national ‘champion’ in this area and had demonstrated a good track record of business execution. ABD’s manager still considers this to be the case and, as we discussed in our August 2020 note, the company, somewhat unusually, published a positive profits warning – telling investors that its profit for the first half of 2020 would be more than 58% ahead of the prior year, with work that it was doing to tackle COVID-19 contributing to this. This continues to be a tailwind for the company, which has moved up into ABD’s top 10 holdings on the back of very strong performance. However, as illustrated in Figure 14, the stock has retrenched recently as investors have rotated away from growth stocks.

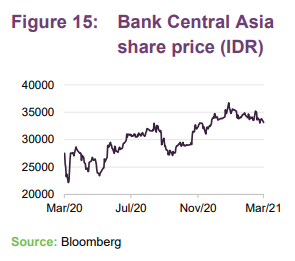

Bank Central Asia – further recovery potential from here

Bank Central Asia (bca.co.id/en) is the largest privately owned bank in Indonesia. It is a full-service bank, with a strong presence in the country, where it has over 1,100 branches and 17,000 ATMs. It is a long-term constituent of ABD’s portfolio – the manager says that, in addition to the advantages of its strong presence and scale, the bank benefits from a low-cost funding base and the ability to pick and choose who it lends to (like many emerging market privately owned banks, it is less susceptible to state interference than its state-owned peers).

As is illustrated in Figure 15, its share price has recovered well since the lows of March last year and, while it has shifted out of ABD’s top 10, James says that it is on the cusp of being a top-10 holding, the bank has no real issues and they haven’t cut the portfolio’s holding. Indonesia is one of the countries that has been more heavily affected by the pandemic, but with its broad exposure to the Indonesian economy, the manager sees strong potential for the bank to continue to recover from here, as the Indonesian economy recovers.

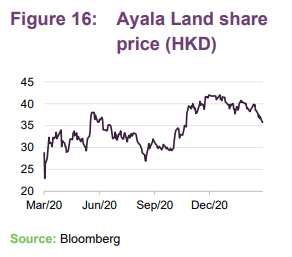

Ayala Land – manager confident of recovery prospects

Ayala Land (ayalaland.com.ph) is a family-controlled property company in the Philippines that has been a long time holding in ABD’s portfolio. Originally formed as a subsidiary of Ayala Corporation, the company was spun out in 1998 and listed on the Philippine Stock Exchange in 1991. The company’s core businesses are strategic landbank management, residential development, shopping centres, corporate businesses, and hotels & resorts. It also has interests in construction and property management.

The Philippines has struggled to get a grip on the pandemic and, along with Indonesia, has been one of the laggards in the Asia Pacific region (a slow roll out of testing, contract tracing and quarantine measures, along with ineffective leadership have been cited as key issues in the Philippines poor performance). As we commented in our August 2020 note, Ayala Land has suffered as a result (the company has seen a sharp drop in revenue and earnings since the crisis started). However, the company has a solid balance sheet, which has given the manager sufficient comfort to maintain the position. As is illustrated in Figure 16, Ayala’s share price has moved up strongly in the fourth quarter of 2020 as positive news on vaccine development emerged. The ASI team says that it still likes the company and while the position size has not been changed, Ayala Land has slipped down ABD’s rankings as it has been overtaken by stronger performing holdings. However, it still remains a significant position and is just outside ABD’s top 10. James believes that Ayala Land it is still a high-quality company and that it will recover given time.

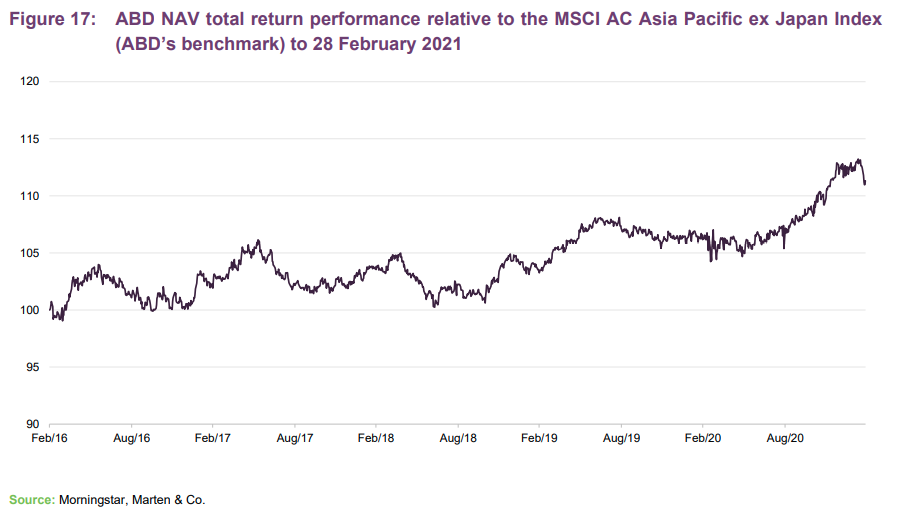

Performance

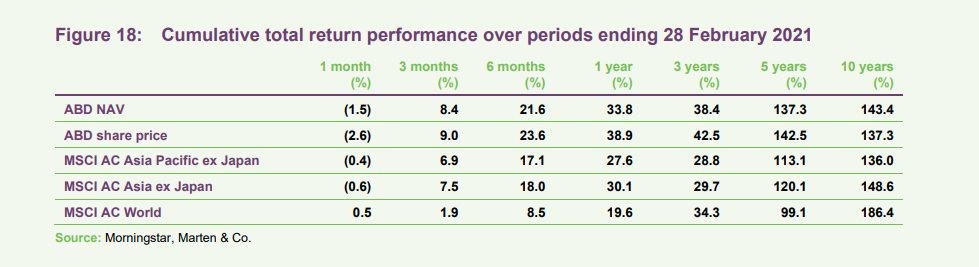

As is illustrated in Figure 17, ABD has, in NAV total return terms, outperformed its performance benchmark over the last five years. This overall outperformance is also illustrated in Figure 18, where ABD has outperformed the benchmark over all of the period’s provided, with the exception of the one-month period. The same pattern is seen for ABD’s share price total return performance, which exceeds that of the benchmark for all periods except the one-month period. ABD has also outperformed both the MSCI AC Asia ex Japan Index and the MSCI AC World Index for all periods up to and including five-years (see Figure 18).

A broad trend of modest outperformance accelerated in the first half of 2019, when the portfolio’s bias to quality stocks made it defensive in falling markets, and again in H2 2020. The recent sell-off in growth stocks, triggered by a steepening yield curve in the US, seems to have dented returns a little, but this may prove temporary.

The recent widening of ABD’s discount is a key reason why ABD’s NAV total return performance modestly exceeds that of its share price performance for all of the periods provided in Figure 18.

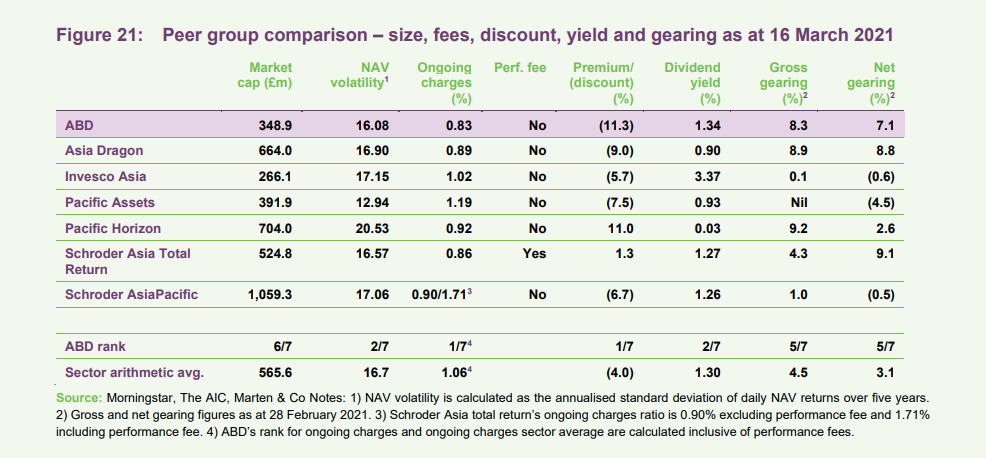

Peer-group comparison – Asia Pacific sector

ABD is a constituent of the AIC’s Asia Pacific sector. The Asia Pacific sector is comprised of seven members, which are detailed in Figures 22 to 23.

Members of Asia Pacific sector will typically have:

- over 80% invested in quoted Asia Pacific shares;

- less than 80% in any single geographic area;

- an investment objective/policy to invest in Asia Pacific shares;

- a majority of investments in medium to giant cap companies; and

- an Asia Pacific benchmark

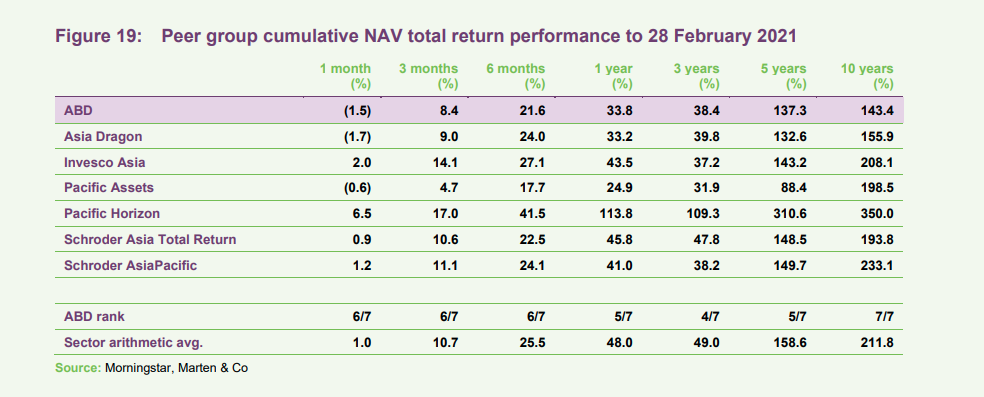

As illustrated in Figure 19, ABD’s cumulative NAV total return performance ranks in the lower half of the table over most of the time periods provided. As we discussed in our initiation note, the performance of ABD and its stablemate, Asia Dragon, relative to their peers, was held back by the manager’s more cautious approach to China and the corporate structures that allowed access to that country’s leading technology companies. Reflecting this, the manager had a long-standing conviction that it would not invest in companies such as Tencent and Alibaba that were only accessible to foreign investors through structures known as ‘variable interest entities’. These structures had been established to bypass Chinese government restrictions on foreign ownership of internet licences. The manager has progressively relaxed this stance (Tencent was added to the portfolio towards the end of 2017 and, more recently, the decision was made to add Alibaba to the portfolio (see pages 11 and 12).

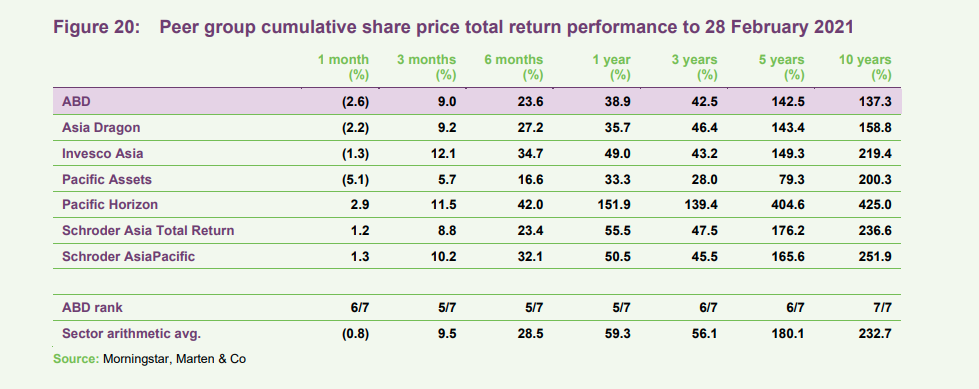

The delay in adding Alibaba was due to the manager continuing to have some reservations about its corporate governance, which have been overcome more recently. As the manager has reduced the Chinese underweight, ABD has been able to participate in the strong relative performance of that market. However, it still remains underweight relative to peers, which has held back performance more recently as that market has moved up strongly. As we have previously noted, the success of the Chinese A share fund, that we highlighted on page 19, demonstrates that the manager can outperform in this market. As illustrated in Figure 20, a similar pattern of relative performance can be seen for ABD’s share price total return performance, relative to its peers.

A further consideration is that the performance of the peer group average has been dragged up significantly by the exceptional performance of Pacific Horizon (PHI) during the last twelve months. Pacific Horizon’s investment approach is very heavily growth-focused, with considerable allocations to technology and healthcare, which have been key to the very strong returns it provided in 2020. However, as can also be seen in the peer group section, all of the peers have been left behind by PHI, which illustrates the extent to which it offers a different proposition and is therefore not an ideal comparator for the rest. Our analysis shows that, if PHI is excluded from the peer group, ABD’s NAV performance is otherwise comparable to the peer group average over all periods provided up to five years, although it is markedly behind over 10 years for the reasons discussed above.

With a market cap of £348.9m as at 16 March 2021, ABD is a decent size, although as is illustrated in Figure 21, it is still the second-smallest within this peer group. Its ongoing charges ratio is nonetheless very competitive, being the lowest within the peer group (see page 20 for more detail). As an aside, ABD, like the overwhelming majority of its peers, does not incur a performance fee. The only exception in this regard is Schroder Asia Total Return, which charges a performance fee of 10% of the excess annual NAV total return of the fund above a 7% hurdle, subject to a high water mark. As is also illustrated in Figure 21, ABD has exhibited one of the lowest NAV volatilities in the peer group, ranking second to Pacific Assets.

As is illustrated in Figure 23 on page 18, ABD’s discount appears to have widened out again recently and continues to be one of the widest in the peer group. This is possibly a reflection of its NAV performance relative to peers. In absolute terms, ABD’s yield is modest, reflecting its focus on capital growth and because – unlike a couple of its peers – it does not make distributions from capital. Nonetheless, its yield is the second highest in the sector and because the sector is relatively low yielding (which brings the sector average yield down), ABD’s yield is broadly in line with (slightly above) the sector average.

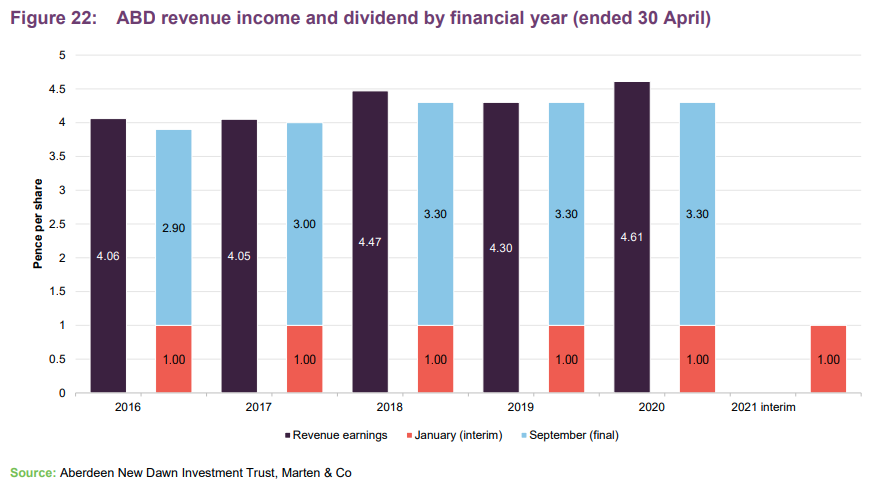

Biannual dividends

ABD’s focus is on generating capital growth rather than income. It pays two dividends a year, an interim in January and a final in September, from surplus income (unlike some of its peers, which pay a large part of their dividend from capital). As illustrated in Figure 22, ABD’s revenue return per share has generally been on an upward trend during the last five years, although there has been some volatility.

For the year ended 30 April 2020, revenue income returned to its trend of growth and surpassed the previous peak in 2018 of 4.47p per share, coming in at 4.61p per share. Roughly speaking, ABD would need to have paid out a minimum of 3.92p per share to maintain ABD’s investment trust status, so it was comfortably able to achieve this by maintaining the dividend at 4.3p per share (which was once again fully covered).

Reflecting the fact that ABD has paid fully covered dividends during the last five years, ABD has grown its revenue reserve per share. ABD’s revenue reserves stood at £13.4m as at 30 April 2020 (2019: £13.1m) or 12.1p per share (2019: 11.7p per share). ABD’s reserves equate to some 2.8x the total dividend paid for the 2019/20 year. Indications so far would suggest that ABD’s revenue income does not appear to have been significantly affected by the pandemic. However, the level of the trust’s revenue reserves means that the board has significant capacity available to it to maintain or even increase the dividend, without the need to pay these out of capital, if necessary.

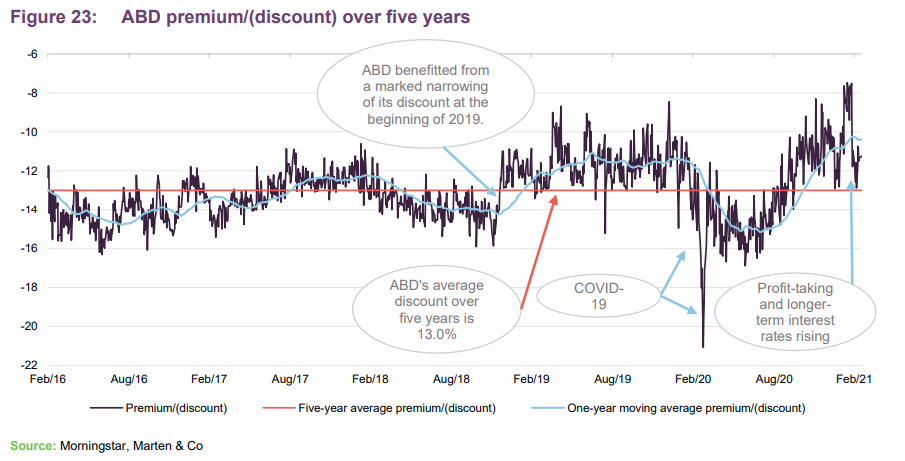

Premium/(discount)

As we have discussed in previous notes, ABD’s discount underwent a marked narrowing at the beginning of 2019, which was sustained throughout the rest of the year and through most of the first quarter of 2020. However, with market wobbles in relation to the coronavirus outbreak, ABD’s discount, along with that of its entire peer group, widened, with ABD hitting its five-year discount high of 21.1% on 23 March 2020. The discount narrowed again quickly, so that ABD was trading at discounts of around 14% by the end of March 2020, but as is illustrated in Figure 23, ABD’s discount was still markedly wider than its pre-pandemic discount range.

As is also illustrated in Figure 23, ABD’s discount continued to narrow over the course of 2020 and into 2021 but has widened again since the middle of February. This is a period that has seen markets correct through a combination of investors taking profits in the face of rising long-term interest rates (a potential signal of rising inflation expectations, which can lead to higher near-term rates, all of which can be negative for equities) that have taken the steam out of markets globally.

During the last 12 months, ABD has traded within a discount range of between 7.5% and 21.1%, with a one-year average of 13.0%. As at 16 March 2021, ABD was trading at a discount of 11.3%. This is above that of the Asia Pacific sector, which was trading at an average discount of 4.0%.

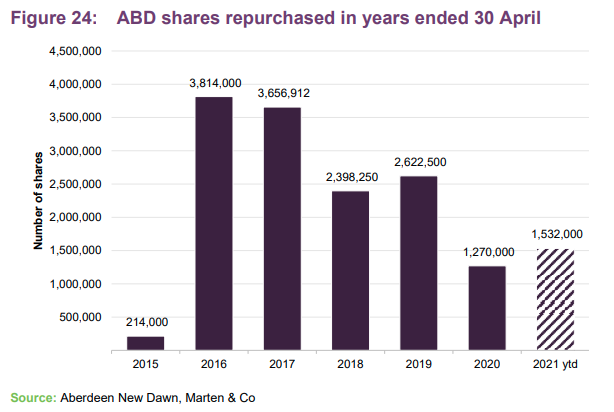

ABD is authorised to repurchase up to 14.99% and allot up to 10% of its issued share capital, which gives the board a mechanism with which it can influence the premium/discount. In normal market conditions, ABD repurchases shares when the discount is wider than the board would like. However, the board has no specific discount target in mind. Instead, its aim is to provide a degree of liquidity for shareholders. The authority to repurchase shares is renewed at each AGM (and more frequently, if necessary).

As we have previously discussed, ABD’s discount has tended to trade at tighter discounts when it has been displaying strong outperformance of its benchmark. The trust has suffered more heavily in the recent market setback than the average of the peer group, which may have contributed to the recent discount widening. However, if ABD is able to provide decent performance as the Asia Pacific ex Japan region continues to recover, and investors’ confidence around Asian markets improves, the discount could tighten further from here, but the reverse may also be true.

As illustrated in Figure 24, 1.53m shares – or 1.39% of ABD’s issued share capital at 30 April 2020 – have been repurchased so far during the current financial year. This repurchase activity is broadly in line, albeit slightly above that of the prior year (1.27 shares or 1.14% of the opening number of shares in issue), which seems reasonable given the high level of uncertainty present during much of 2020.

Fees and costs

The management fee is payable monthly in arrears based on an annual rate of 0.85% of NAV. There is no performance fee. The fee is adjusted so that there is no additional fee charged on other funds managed by the manager. The management agreement is terminable by either side on not less than 12 months’ notice.

All expenses are charged fully to revenue with the exception of management fees and finance costs, which are charged 50% to revenue and 50% to capital. This allocation reflects the board’s long-term return expectations in terms of income and capital respectively.

In addition to the management fee, the company pays an amount each year to the manager for its promotional activities in relation to the trust. This was £146k for the year ended 30 April 2020, down from £152k for the previous year.

For the year ended 30 April 2020, ABD’s ongoing charges ratio, including look-through costs for collective investment schemes, was 1.10% (a modest decrease over the ratio for the year ended 30 April 2019 of 1.13%). Excluding look-through costs, ABD’s ongoing charges ratio was 0.83% (2019: 0.87%).

Capital structure and life

ABD has a simple capital structure with one class of ordinary share in issue. Its ordinary shares have a premium main market listing on the London Stock Exchange, and as at 16 March 2021, there were 120,229,449 in issue with 11,190,101 of these held in treasury and 109,039,348 otherwise in general circulation.

The board determines the gearing strategy for the company subject to a current maximum limit of 25% of net assets. Borrowings are short- to medium-term and particular care is taken to ensure that any bank covenants permit maximum flexibility of investment policy. ABD has a £40m multi-currency loan facility provided by The Royal Bank of Scotland International Limited for this purpose.

This comprises a five-year fixed rate loan of £20m, with an interest rate of 2.626%, which matures on 14 December 2023, and a £20m three-year multi-currency revolving loan facility, which matures on 14 December 2021. As at 28 February 2021, ABD had gross gearing of 8.3% and net gearing of 7.1% of net assets respectively.

ABD’s financial year end is 30 April. Its annual results are usually published in June (interims in December) and its AGMs are usually held in September of each year. ABD pays biannual dividends in in January and September.

Discount triggered continuation vote

ABD does not have a fixed life. However, under its articles of association, if in the 90 days preceding ABD’s 30 April year end its average discount exceeds 15%, notice will be given of an ordinary resolution to be proposed at the following AGM to approve the continuation of the company.

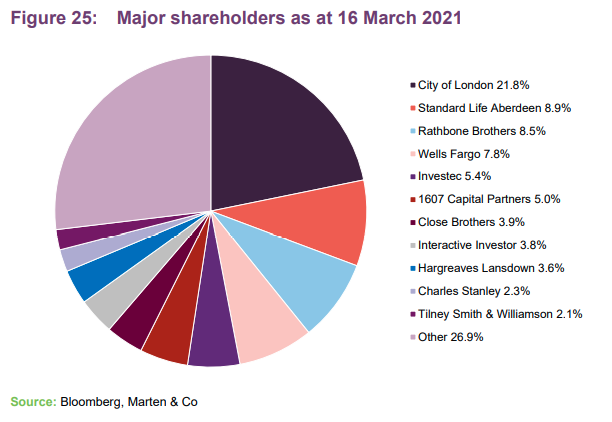

Major shareholders

Management team

ASI investment directors James Thom and Gabriel Sacks are the lead managers on ABD’s portfolio.

ASI is a global asset management company with offices in over 40 locations and more than 20 investment centres. Within the Asia Pacific region, it has 11 offices.

Flavia Cheong heads up a team of over fifty investment managers in Asia. The Singapore office is the manager’s largest. This is where James Thom, Gabriel Sacks and ABD director Hugh Young (see below) are based.

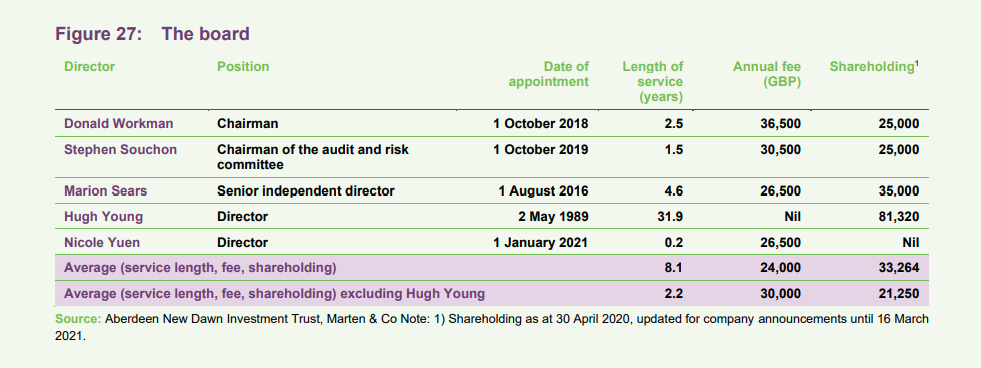

Board

ABD’s board currently has five directors, all of whom are non-executive and who do not sit together on other boards. The majority are independent of the manager, with the exception of veteran fund manager Hugh Young (see below), who is a director of various entities connected with or within the Standard Life Aberdeen Group, which owns the manager. Hugh is the longest-serving director, with a tenure of

31.9 years. Neither Hugh nor ASI earns a director’s fee from his service as a director of ABD.

John Lorimer retired at the AGM in September 2020 and he was succeeded as chairman of the audit and risk committee by Stephen Souchon.

Susie Rippinghall, who had been a director since 2014, stepped down from the board on 31 December 2020 to avoid a potential conflict of interest with another board position. Nicole Yuen was recruited in her place and she will stand for re-election at the AGM scheduled for September 2021.

Directors’ fees are capped at £200,000, but as the table shows, total fees are well within that limit.

Donald Workman (chairman)

Donald had an executive career until 2016 at The Royal Bank of Scotland PLC, where over a period of 23 years he held a number of senior positions. Latterly, this included acting as executive chairman of the group’s Asia Pacific business. Donald was a member of the RBS Group Executive Committee from 2014. He was also an independent non-executive director of Standard Life Private Equity Trust Plc between 2006 and 2013. Donald is currently non-executive chairman of JCB Finance Limited.

Marion Sears (senior independent director)

Marion had an executive career in stockbroking and investment banking and was latterly a managing director of investment banking at JPMorgan. She is also a non-executive director of Dunelm Group Plc and Fidelity European Values Plc.

Stephen Souchon (chairman of the audit committee)

Stephen is a chartered accountant. He had an executive career until 2015 at Morgan Stanley, where he was latterly head of the EMEA Corporate Financial Control Group. Stephen was a non-executive director and chair of the audit committee of Morgan Stanley’s Swiss Bank, during which time he oversaw the development of the Swiss wealth management business within Asia. Stephen is currently a non-executive director and chair of the audit committee of SMBC Nikko Capital Markets Limited.

Hugh Young (director)

Hugh Young is chairman of Aberdeen Standard Investments business in Asia and was previously the head of Asia Pacific for Aberdeen Standard Investments, a main board director, and head of investments for Aberdeen Asset Management (before its merger with Standard Life Plc).

Hugh joined the company in 1985 to manage Asian equities from London, having started his investment career in 1980. He founded Singapore-based ASI Asia in 1992 as the regional headquarters. Hugh is a director of a number of group subsidiary companies and group-managed investment trusts and funds. He graduated with a BA (Hons) in Politics from Exeter University.

Nicole Yuen (director)

Nicole is a Hong Kong national and a graduate of the University of Hong Kong and Harvard Law School. She had an executive career initially in law and subsequently in equities with UBS and latterly Credit Suisse (Hong Kong) where she was chief operating officer for the Greater China region and subsequently managing director, head of equities, North Asia until 2018. Nicole is currently a non-executive director of Interactive Brokers Group, Inc.

Previous publications

Readers interested in further information about ABD may wish to read our previous notes by clicking the links.

Market setback creates opportunities, initiation note, published October 2018

Moving up the league table, update note, published July 2019

Illuminating value, annual overview, published February 2020

COVID positive, update note, published August 2020

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Aberdeen New Dawn Investment Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.