abrdn New Dawn

Investment companies | Annual overview | 13 February 2023

A quality captain for a troubled Pacific

abrdn New Dawn (ABD) ended 2022 with the peculiar, if compelling, combination of the second-best 12-month performance within its peer group, and the widest discount, at 11.5%. Manager James Thom has highlighted the ongoing complexity of navigating the Asia Pacific region, given the lack of homogeneity in the varying countries’ outlooks. Whilst ABD has underperformed its benchmark over the last 12 months, as select low-quality stocks have rallied, it remains ahead of its peers, with James’s process generating sector-leading consistency in its outperformance over the longer-term.

Though headwinds undoubtedly remain for the Asia-Pacific investor, there have been clear advantages to James’s approach. This in combination with ABD’s comparatively wide discount, may make it an attractive time to buy, particularly given a backdrop of rising interest rates that could allow the trust’s quality-factor to return to form.

Capital Growth from Asia Pacific ex Japan

ABD aims to provide shareholders with a high level of capital growth through equity investment in the Asia Pacific countries, excluding Japan. The trust holds a diversified portfolio of securities in quoted companies spread across a range of industries and economies. ABD is benchmarked against the MSCI All Countries Asia Pacific ex Japan Index (in sterling terms).

Market Overview

Since publishing our last ABD note in June 2022, one might have reasonably expected that a series of new and different market shocks would have hit Asian equity markets. However, for much of the last six months, markets have continued to grapple with the same headwinds. Specifically, Asian markets remain in the grip of higher input and energy costs, the spectre of COVID-19 (particularly in China) and rising global interest rates. Over 2022, the MSCI AC Asia Pacific ex Japan index fell by -7.4%, though still ahead of the -8.0% provided by the MSCI AC World Index.

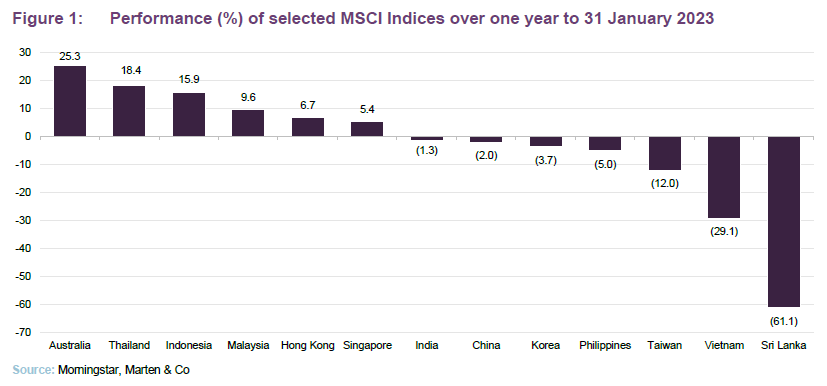

China’s reopening may be the most important development over the last six months.

Arguably the most significant factor affecting the Asia Pacific region has been China’s handling of COVID-19, although the recent relaxation of its strict zero-COVID policy is a move towards the full re-opening of the country. While the prospect of the world’s second-largest economy finally benefitting from a post-COVID rally is clearly a huge tailwind for the region (with the MSCI China having rallied some 13.8% over December and January alone), it has not yet been sufficient to fully reverse the pain that China’s draconian COVID policy and flawed vaccination programme has inflicted on its equity markets or its economy. China is now having to deal with the inevitable spike in COVID-19 cases, leaving professional investors holding their breath in anticipation of the impact on China’s healthcare infrastructure.

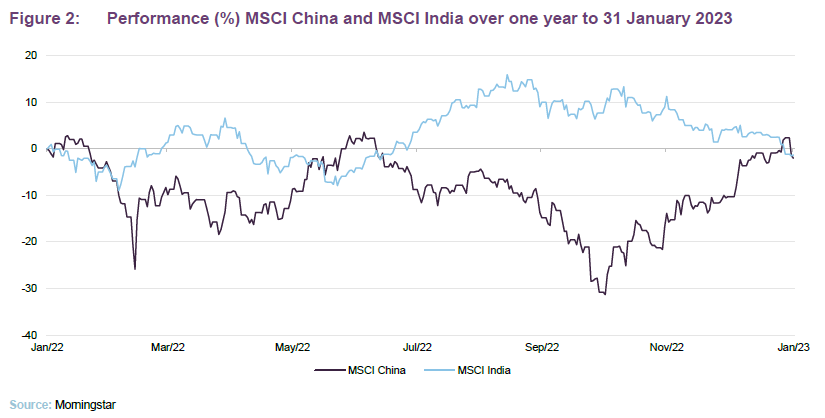

Thankfully, the Asia Pacific region is made up of a variety of hugely idiosyncratic regions, offering a plethora of opportunities for professional investment managers to add alpha. Even within the same geographic regions, investors can find major divergences between geographically close countries, with the disparity between Thailand and Vietnam, and Hong Kong and Taiwan being perfect examples. Though no emerging markets regions are more important than China and India, which combined represent more than 40% of MSCI AC Asia Pacific ex Japan index, as well as being the top two regional exposures for ABD. Despite having comparable 12 month returns, India and China have been on divergent paths with their performance offsetting each other, as seen by Figure 2, though for often un-associated reasons. Whereby China’s fortunes have been predominantly driven by the impact of its economic reopening, as well as its wider responses to the pandemic. While India’s fortunes have been driven by a combination of a robust economy, and a number of major stock-specific factors impacting its market performance, especially the recent decline in the share prices of the Adani Group of companies (which we describe on page 10). Despite the negative correlation, the factors influencing these countries have been largely unrelated, bar the possible impact on resource costs (though this is felt across the globe), reflecting the vast array of opportunities and the varied economic landscape offered by the Asia Pacific region.

US dollar and US interest rates have increased the cost of US denominated debt

Another major factor influencing the Asia Pacific region has been the strength of the US dollar and the rise in global interest rates, which are closely interlinked factors. Rising global interest rates have hit almost all equity markets, especially in markets with highly valued equities, vis-à-vis higher discount rates. Not only do higher rates directly impact equity valuations, they also slow down economic activity via higher financing costs. Declining global economic activity can be particularly painful for emerging markets, as their growth often hinges on higher demand for their exports.

Higher US interest rates have also led to the US dollar rallying over 2022 (though it has weakened over recent weeks thanks to the possibility of a forthcoming US recession). Given that a large amount of Asia Pacific debt, both sovereign and corporate, is denominated in dollars, a strong US dollar increases the cost of servicing such debt in the local currency. Though the US dollar today remains at levels higher than pre-2022, it has begun to weaken in recent months, to the relief of many emerging market debt issuers.

Manager’s view

In our recent conversations with James, he paints an equally mixed picture, with the environment creating both winners and losers at both a stock and regional level. However, he believes that the current environment will throw up tailwinds for ABD’s quality-bias, with the property sector a particular highlight, given its prominent role in facilitating Chinese economic growth. We note that James continues to remain bullish on India’s fundamentals, retaining a similar overweight to the region as per our last note.

Chinese finger-trap

China remains an underweight for ABD, but some tailwinds are starting to appear.

James highlights the wider issues that China continues to face, despite the potential re-opening boom. The Chinese economy has clearly slowed down – the strict zero COVID policies have taken their toll, the property sector is ailing, and cracks are beginning to appear in their banking system. The decline in the property sector is particularly painful, with Standard and Poor’s predicting an 8% drop over 2023, as it has been one of the major drivers of China’s past economic growth. James also highlights the increased political risk in China thanks to Xi Jinping’s consolidation of power. Having secured an unprecedented third term as Premier, he has pushed aside various counterbalances to his power, increasing the governance risks in China. Even prior to the recent congress, Xi had already begun to exercise greater influence on Chinese business practices, with the downfall of Alibaba’s Jack Ma and the withdrawal of the ANT IPO being clear warnings to investors.

Whilst growth and governance risks do weigh on James’ and the team’s mind, he believes there are some clear silver linings for investors in China. One of the starkest advantages China offers investors is the lack of inflation, being one of, if not the only, major economy not having to deal with material price rises. We note that because of the selloff in Chinese equities earlier in the year (a reflection of the painful COVID19 restrictions) Chinese equities also trade at more modest valuations, inherently reducing their interest rate sensitivity. The other tailwind James raised was the Chinese government’s support for the property sector. It has provided a support package which will allow builders more time to complete their projects, vis-à-vis funding extensions, as well as relaxing mortgage terms.

Trust in quality

In periods of heightened uncertainty, with or without the pain of a bear market, James believes that quality is amongst the few characteristics that investors can focus on to help mitigate higher risk. Although quality, which is by far the most dominant factor in the team’s investment process, has not held up as well as James hoped relative to the wider market over the last 12 months, it has shown a number of performance characteristics which does support the notion of its ‘reliability’, as we point out later in the note. A ‘high-quality’ business is determined by the assessment of management, business focus, the health of the balance sheet and corporate governance. We covered the team’s approach to quality (and their overall investment process) in greater detail in our previous note.

High-quality companies may offer a form of safety during periods of wider uncertainty.

The idea that a ‘quality’ company may be a superior investment during more challenging market environments is based on the notion that such companies are either better positioned to absorb any economic difficulty thanks to their healthy balance sheets (e.g., little to no debt outstanding which requires financing); or that their management teams have experience of similar environments and are therefore able to steward the company effectively. Quality companies can span multiple ‘styles’ of investing, with the team holding both cyclical and sectoral growth opportunities for example.

The team believes that high-quality companies have an effective floor to their operational downside, as they should be amongst the last of their peers to see material disruption to their business models from today’s economic headwinds. As a practical example, James believes that the quality factor should be an excellent defence against rising inflation, as management teams will either able to pass cost increases onto their customers or adjust their supply chains to limit the impact of rising costs.

James also notes that down-markets can produce several relative tailwinds for high-quality companies, such as the increased scrutiny on poor governance for their peers. Poorly governed companies will either fail to react to rapidly shifting market environments, or investors will simply give such companies less interest as they begin to become more risk averse.

Asset allocation

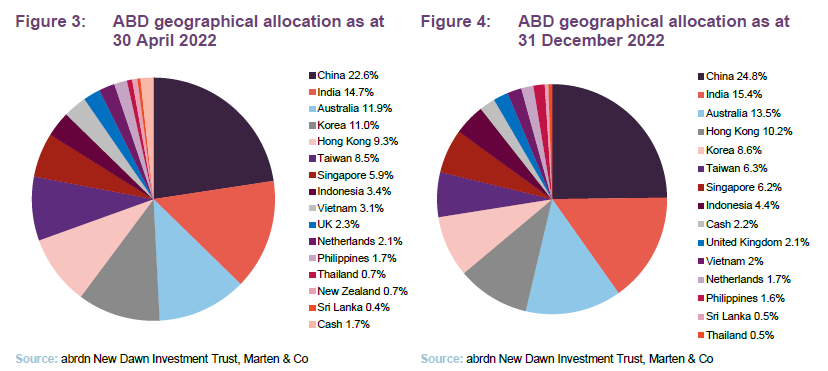

Comparing Figures 3 and 4 shows that ABD’s geographical allocation has changed slightly between 31 December 2022 (the most recently available data) and 30 April 2022 (this being the most recently available data when we last published).

At 23.5%, ABD’s exposure to China has increased – a reflection of both the recent uplift in the region’s performance, as well as some selective trading around the region to capitalise on possible rebound winners. ABD’s India exposure also continues to increase, reflecting the strong share price growth in the region since our last note. ABD’s exposure to Korea has been cut back further, and now accounts for less than 10% of the trust’s portfolio. The trust’s exposure to Taiwan has also been reduced, falling by 1.5% to 6.9% currently.

India remains a large overweight for ABD.

James comments that any changes to ABD’s allocation, beyond those implied by the relative strength of regions, have come via stock-specific decisions made by the team. These reflect an individual company’s prospects and not macro-level factors. We remind readers that ABD’s India exposure is achieved via the use of an abrdn-managed India equity fund, so granular changes in the trust’s India allocation are not immediately apparent.

The team has also rejigged ABD’s Vietnamese exposure since our last note, taking profits in a dairy company (Vinamilk) and recycling it into information technology firms, though the net effect is a 1.2% fall in the trust’s Vietnamese exposure.

James has also taken the opportunity to reduce ABD’s net gearing, with the trust currently operating on a 7% gearing. This fall in leverage reflects James’ overall caution around the market.

Top 10 holdings

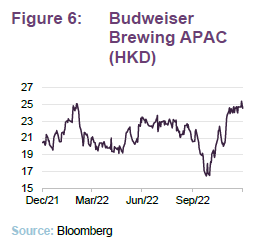

The constituents of ABD’s top 10 have remained largely constant since our last note, bar the change of a single position, with Oversea-Chinese Banking having fallen out in favour of Budweiser Brewing. The ranks of the other top 10 holdings have also remained largely consistent, with no major shifts apparent.

Budweiser Brewing

Budweiser Brewing APAC is the Hong Kong-listed Asian arm of the global brewing giant (budweiserapac.com). Budweiser is the largest beer producer in the Asia Pacific region by sales volume. There are clear tailwinds behind alcohol consumption within the Asia Pacific region, one being the long-term upward trend in alcohol consumption thanks to rising incomes, and the other being the bounce in consumer spending post lockdown, particularly in China. The latter has already had a substantial impact on Budweiser’s share price, with the company rallying some 50% over November, pushing it up into ABD’s top 10. The quality of Budweiser is made evident by both its market leadership but and strong brands, which in combination give it exceptionally strong pricing power as well as wide economic moats.

AIA Group

AIA Group (dbs.com), while not a new position for ABD has been added to over the course of 2022. AIA is the Hong Kong-listed financial group, primarily known for its insurance business, and is the largest listed insurance group in the Asia Pacific region. AIA is not simply a mainstay of the Asia Pacific market but also of ABD’s portfolio. AIA was a top 10 holding for the trust as far back as our initiation note in October 2018, though it was first included in ABD’s portfolio in 2010 when the company had its IPO. AIA is not only a market leader in the space, thanks to its successful use of agencies to distribute its products, but it also has a strong balance sheet which often makes it more attractive than banks of the equivalent size. Beyond its quality characteristics, AIA has a number of powerful tailwinds supporting its industry. The first is the rise in global interest rates (which increases the yields received form fixed income investments), and the second is rising demand for insurance products thanks to rising wealth (traditionally low adoption of insurance schemes throughout the developing Asia Pacific region means that this has a long way to run).

New additions to the portfolio

Since our last note, James has initiated a number of new positions in the trust, including a select few names in China despite his cautious approach to the country. These are all longer-term structural growth stories that James thinks are more immune from the current broader slow growth environment.

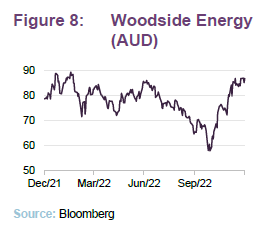

There have been several new positions added to ABD since our last update, all of which were added for stock-specific reasons, rather than to capture any shift in the current market tailwinds. As a result, these purchases have been made across a variety of regions, including the addition of the first energy company to ABD’s portfolio.

Woodside Energy

Though not a top 10 holding, the team has built a new position in Woodside Energy in recent months. Woodside is the Australia-based oil and energy producer, and the only such company within ABD’s portfolio. The team opted to initiate its position following the merger of BHP’s oil and gas assets with Woodside in June 2022, and only increased its position in the months following. Like AIA and Budweiser, Woodside has become an Asia Pacific market leader, solidifying its position with the BHP merger, although its assets are located across the world. Although Woodside cannot be a price setter in the energy market, its focus on liquidised natural gas means that it can capitalise on higher global energy prices without being exposed to the increased scrutiny the oil industry faces on environmental grounds.

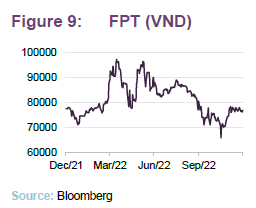

FPT

FPT is Vietnam’s largest information technology company and is another recent addition to ABD’s portfolio. FPT offers a diverse range of telecommunication and technology services, as well as an expansion into the education market. Despite its wide range of subsidiaries, FPT remains one of Vietnam’s largest internet service providers. It has also become Vietnam’s first domestic semiconductor manufacturer.

Telkom Indonesia

Another new purchase for ABD is Telkom Indonesia, Indonesia’s largest telecommunications provider with roughly a 50% market share. James highlights the improving market outlook for Telkom, with Indonesia’s telecommunications market having finally normalised after a period of consolidation, ending the price wars which that suppressed profits.

At a company level, James highlights Telkom’s attractive enterprise contracts, which are a sticky source of reoccurring revenue and should also benefit from the post-COVID-19 recovery as industries increasingly adopt the benefits of digitisation. Irrespective of any near-to-medium term tailwinds, the telecommunications industry is a highly resilient one, and offers a source of reliable revenues during a period of wider global economic uncertainty.

Sales

While there have been some outright sales since our last note, there have been no outright disposals within the top 10 holdings. The ABD team tends to take a long-term view to its holdings, with turnover being around 15% over the last 12 months. Examples of outright disposals include Vinamilk, the Vietnamese dairy producer. The relatively low turnover reflects both the team’s long-term approach, but also the uncertainty it perceives around the current macro environment, with the team already overweight in the regions that it considers are likely to have the strongest macro-economic outlooks.

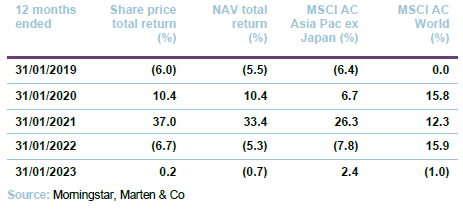

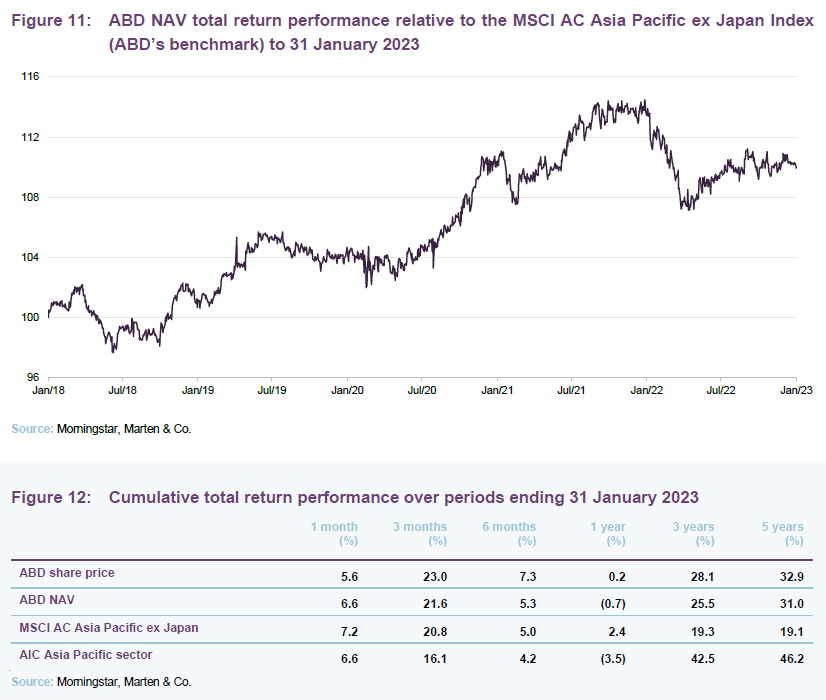

Performance

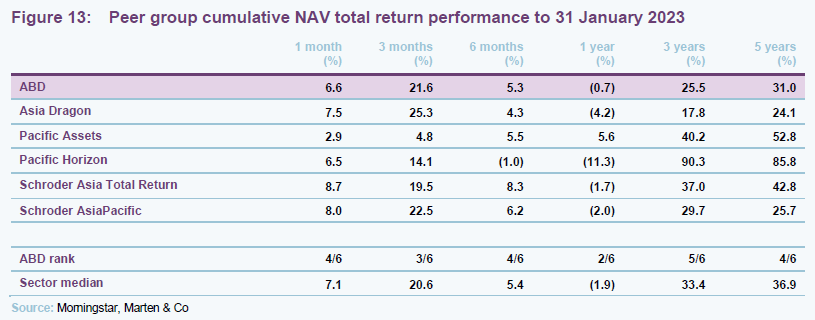

While ABD has generated a strong outperformance relative to its benchmark, the MSCI AC Asia Pacific ex Japan Index, over the long term (as measured over the three- and five-year time periods), it has lagged over the last year. Over the

12-month period to 31 January 2023, ABD generated a NAV total return of -0.7%, a 3.1 percentage point underperformance relative to its benchmark.

The rally in select low-quality companies has hit ABD’s relative performance.

One of the largest contributors to the trust’s underperformance over 2022 was the performance of the Aberdeen Indian Equity fund, which is managed with a similar philosophy to that of ABD. Whilst the team retained an overweight to India over the last 12 months – which was a net positive for the trust, given the region’s outperformance – the India fund’s focus on quality meant that it missed out on the rally in the Adani Group of companies over that period. These companies, which range from a port operation to an oil and gas business, were able to post strong revenue performance. The ABD team notes that the group falls far below its hurdle for a ‘high-quality’ group of companies, given their poor governance track records and high leverage, for example. We note that while not entirely captured by our sampled month-end time period, the team’s concerns around the Adani Group appear to have been vindicated. The Adani Group of companies have come under substantial selling pressure since 24 January, thanks to a report issued by a professional short-seller firm.

With its quality focus, ABD is likely to lag during low-quality rallies as such style rotations are not in the trust’s favour. While low-quality rallies are not as easy to categorise as growth versus value, they do have certain common characteristics. For example, they tend to occur during periods of investor over-enthusiasm, such as during strong bull-market rallies, with investors eschewing the reliability of high-quality companies for the growth potential of certain lower-quality businesses.

Whilst the ABD team believes that quality can be a source of safety during down markets, we do note that in the current market investors have begun to flock to certain types of lower-quality businesses, such as oil companies and banks, which could see powerful tailwinds from the current macro environment. Because of the various low-quality rallies we have seen in parts of the Asia Pacific region, ABD’s relative performance has not held up as well as the team might have expected it to, especially given the historic defensiveness of the trust.

Statistical metrics point to the reliability of ABD’s long-term outperformance.

There are a few statistics which do support the notion that ABD’s process does promote more resilient returns, reflecting the greater reliability of the revenues of high-quality companies. In particular we point to two mathematical performance metrics relative to ABD’s peers over the last five years (based on monthly returns): downside deviation and batting average, both of which rank best amongst its peers.

Downside deviation measures ABD’s underperformance during periods in which it returns less than MSCI AC Asia Pacific ex Japan, with a lower figure indicating that ABD’s underperformance adds the least amount of additional downside risk of any of its peers. ABD also has the second-lowest overall volatility of any its peers, though with a smaller gap between its peers when compared to its downside deviation.

ABD’s batting average measures the consistency of its outperformance relative to the MSCI AC Asia Pacific ex Japan, i.e., the percentage of months over the five-year period in which ABD outperforms the index. Whilst ABD has not been the best performer over the last five years, the superior consistency of its outperformance does support the idea that quality companies are far more reliable, and less likely to move in and out of favour.

Peer-group comparison – Asia Pacific sector

Please click here for an up-to-date peer group comparison of ABD versus its Asia Pacific peers.

ABD is a constituent of the AIC’s Asia Pacific sector. The Asia Pacific sector is comprised of six members, which are detailed in Figures 13 and 14.

Members of Asia Pacific sector will typically have:

- over 80% invested in quoted Asia Pacific shares;

- less than 80% in any single geographic area;

- an investment objective/policy to invest in Asia Pacific shares;

- a majority of investments in medium to giant cap companies; and

- an Asia Pacific benchmark

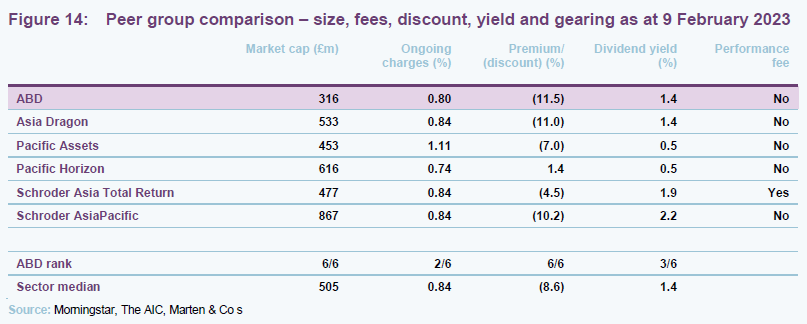

Each trust within the peer group has generated a negative NAV total return performance over the last 12 months, with only one trust (Pacific Assets) able to beat the MSCI Asia Pacific ex Japan Index’s return of 2.4%. ABD’s 12-month NAV performance is 1.2 percentage points ahead of the median NAV return for its peer group, although it is below the peer group median over the longer three- and five-year periods.

The relative performance of the trusts can be explained by a combination of their style biases, as well as their regional biases. Pacific Assets has a 45% allocation to India, which explains much of its outperformance over the 12-month period, while at the other end, Pacific Horizon, with its strong growth-stock bias and resulting heightened interest rate sensitivity, has outperformed over the longer term, but underperformed during the current rising-interest rate environment, leading to its bottom-of-the-pack 12-month performance.

ABD has both the second best 12-month performance and the widest discount.

Whilst ABD should be compared against all its peers, we remind readers of the manager’s belief that ABD is a ‘core’ Asia Pacific strategy with its quality bias allowing it to encompass the wider Asia pacific region, be it through developed markets like Australia and Korea, or emerging markets like India and Indonesia. ABD could be viewed as offering investors a look-through to the major regions of the Asia Pacific area, through a quality filter, which clearly sets it apart from some of its peers. ABD’s quality bias, and its more consistent outperformance (based on its historic ability to be the most likely to be outperform the wider index in a given month, indicated by its peer-group leading five-year batting average), go a long way to explaining its above average 12-month performance, as its lack of strong style biases (e.g. growth vs value) or regional biases means it had less exposure to 2022’s painful headwinds than its peers.

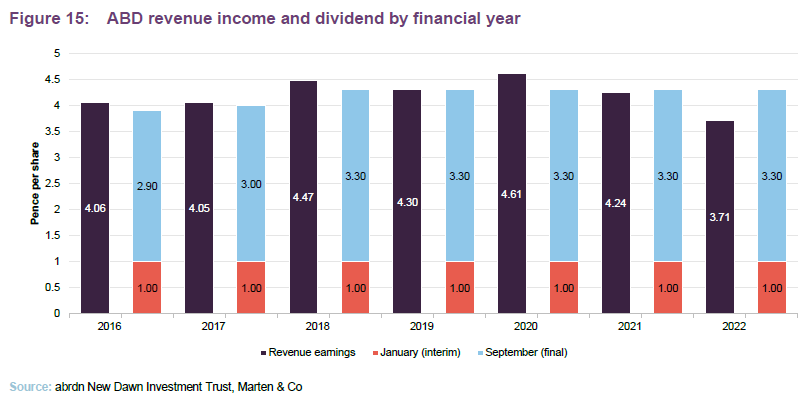

Despite its comparatively strong recent performance, ABD remains the smallest trust in the sector though with a market cap over £300m its size should not be a concern to investors. Despite its smaller relative size, ABD’s ongoing charges ratio is among the lowest in the sector and, like most of its peers, it does not incur a performance fee. The only exception in this regard is Schroder Asia Total Return, which charges a performance fee of 10% of the excess annual NAV total return of the fund above a 7% hurdle, subject to a high-water mark.

While ABD’s discount has narrowed slightly since our last note it remains the widest in the sector. In fact, the peer group average discount has also narrowed since our last note. This trend likely reflects the comparative strength of select Asia Pacific regions over recent months, as well as investors tentatively coming back to equity investing, having grasped the nature of the headwinds they faced at the start of the year. Given its capital focus, and sole use of its revenue account, ABD’s yield is best described as modest, and unlikely to be sufficient for income investors.

Biannual dividends

ABD’s focus is on generating capital growth rather than income. It pays two dividends a year, an interim in January and a final in September, from surplus income (unlike some of its peers, which pay a large part of their dividend from capital). ABD has sustained the same 4.3p per share dividend since 2018, though its revenues have been on a downward trend since the outbreak of the pandemic.

For the year ended 30 April 2022 (the most recently available data), revenue income was 3.71p per share, below the 2020 figure of 4.24p per share.

ABD has built up significant revenue reserves on which it could draw if there was a shortfall in revenue.

ABD’s revenue reserves stood at £12.7m as at 30 April 2022 (2021: £13.3m). The fall in revenue between 2021 and 2022 reflects the impact of the pandemic on the dividend payments of Asian companies, which, considering the longer length of lockdowns in the Asia Pacific region, may have had a more prolonged impact on dividends compared to the west. However, the level of the trust’s revenue reserves means that the board has the capacity available to maintain or even increase the dividend, without the need to pay these out of capital. We estimate that ABD has a revenue coverage ratio of 2.8 times the recent full year dividend.

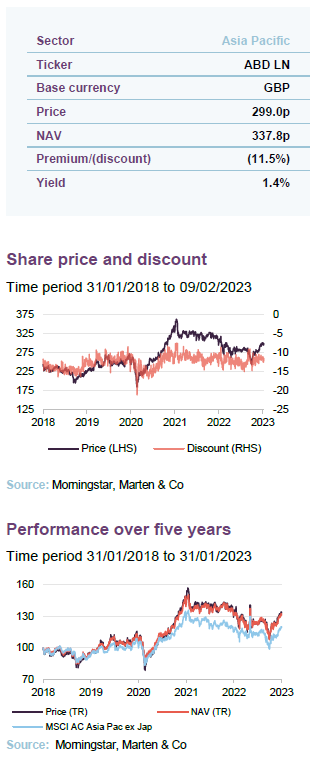

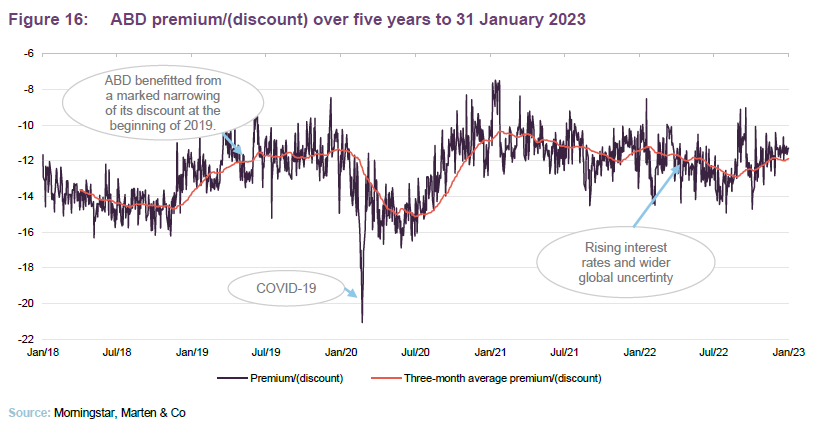

Premium/(discount)

ABD’s discount did see a narrowing in 2019, as we discussed in past notes, one which has largely been sustained since then, bar the brief impact of COVID-19. However, 2022 saw the three-month average drift downward slightly, with ABD unable to avoid the raft of headwinds facing wider global markets, as investors retreated from risk assets of all forms. However, thanks to the recent easing of Chinese lockdown restrictions, ABD’s discount is narrower than it was a couple of months ago.

ABD’s discount hit a five-year high of 21.1% on 23 March 2020, around the peak of the COVID-19 selloff, before hitting a five-year low discount of 7.5% in February 2022, reflecting the post COVID rebound in quality markets. We note that even with the 2022 market selloff, ABD’s year-end discount of 10.4% was still more than one standard deviation below its five-year average, reflecting the persistent re-rating.

During the last 12 months, ABD traded within a discount range of between 8.5% and 14.9%, with a one-year average discount of 12.1%. As at 09 February 2023, ABD was trading at a discount of 11.5%. This is wider than that of its Asia Pacific sector peers, which are trading on a median discount of 8.6%.

While ABD’s discount has drifted wider over 2022, it still remains narrower than its long-term average.

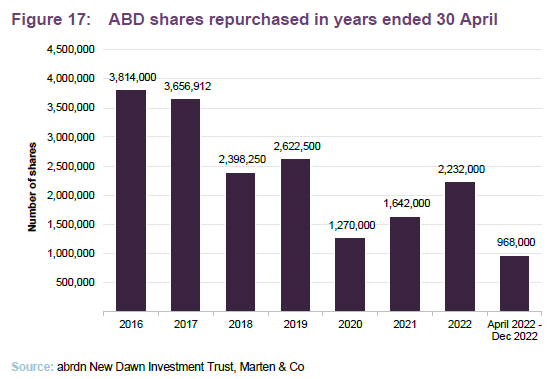

ABD is authorised to repurchase up to 14.99% and allot up to 10% of its issued share capital, which gives the board a mechanism with which it can influence the premium/discount. In normal market conditions, ABD repurchases shares when the discount is wider than the board would like. However, the board has no specific discount target in mind. Instead, its aim is to provide a degree of liquidity for shareholders. The authority to repurchase shares is renewed at each AGM (and more frequently, if necessary).

Like many trusts, ABD’s discount is closely related to its outperformance of its benchmark. None-the-less, ABD trades at one of the widest discounts of its peer group, despite having one of the best NAV returns over 2022. One could argue that if ABD’s quality bias returns to favour relative to its benchmark (as is the case over the longer term, given the outperformance of ABD over five years), and ABD can sustain its outperformance versus its average peer, then its current discount may offer a potential entry point for investors looking to capture any momentum behind the Asia Pacific region.

As illustrated in Figure 19, 2.23m shares were repurchased for the year to 30 April 2022. This is much higher than the past two years (1.64m in 2021, 1.27m in 2020), which is positive given the high level of uncertainty present during that time. Over the subsequent eight months, however, the rate of purchase has slowed, however.

Fund profile

You can access the trust’s website at: newdawn-trust.co.uk.

abrdn New Dawn (ABD) aims to provide shareholders with a high level of capital growth through equity investment in the Asia Pacific countries, excluding Japan. ABD holds a diversified portfolio of securities in quoted companies spread across a range of industries and economies.

Investments may also be made through collective investment schemes and in companies traded on stock markets outside the Asia Pacific region, provided that over 75% of their consolidated revenue is earned from trading in the Asia Pacific region, or they hold more than 75% of their consolidated net assets in the Asia Pacific region.

High levels of capital growth through equity investment in Asia Pacific ex Japan countries.

ABD is benchmarked against the MSCI All Countries Asia Pacific ex Japan Index (in sterling terms). We have also included comparisons against the MSCI AC World Index and its peer group within this report.

The manager is abrdn, which has delegated the investment management of the company to abrdn Asia Limited. On 1 June 2022, the trust changed its name from Aberdeen New Dawn Investment Trust Plc to abrdn New Dawn Investment Trust Plc to reflect the rebranding of the management company.

abrdn’s investment style is to manage money using a team approach. We spoke to James Thom, a senior investment manager in the team, for the purposes of preparing this note.

Previous publications

Readers interested in further information about ABD may wish to read our previous notes listed below. You can read them by clicking on the links in Figure 18 or by visiting our website.

Figure 18: QuotedData’s previously published notes on ABD

Source: Marten & Co |

Legal

This marketing communication has been prepared for abrdn New Dawn Investment Trust Plc by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and, if you are not a professional investor, or in any other way are prohibited or restricted from receiving this information, you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it, but in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this not.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.