Burnished copper

CQS Natural Resources Growth and Income (CYN) has provided exceptionally strong absolute and relative performance during the last 12 months, and has markedly outperformed its commodities and natural resources peer group. A key driver of this has been the managers’ preference for base metals, with significant exposure to copper being a major contributor.

With supply struggling to respond to resurgent demand for most major commodities, the managers believe that many of these markets are structurally short. An increased focus on meeting carbon reduction targets and replacing ageing infrastructure is commodity-intensive.

Despite recent strong performance, resources companies look attractively valued on a forward earnings basis and the managers believe the commodity cycle has much more to offer.

Capital growth and income from mining & resources

CYN aims to provide investors with capital growth and income by investing in a portfolio that predominantly comprises mining and resource equities, as well as mining, resource and industrial fixed-interest securities. The fixed income securities include, but are not limited to, preference shares, loan stocks, corporate bonds (convertible and/or redeemable) and government bonds.

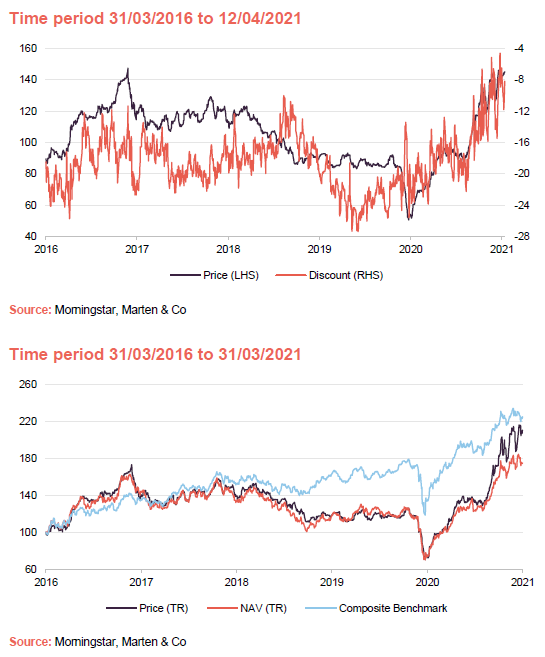

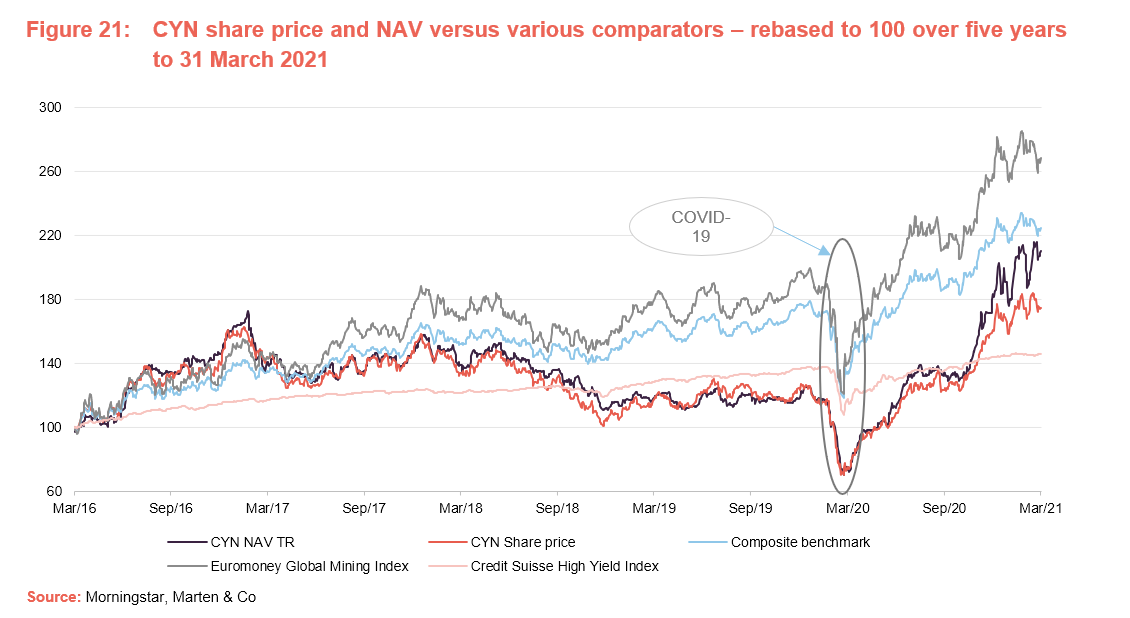

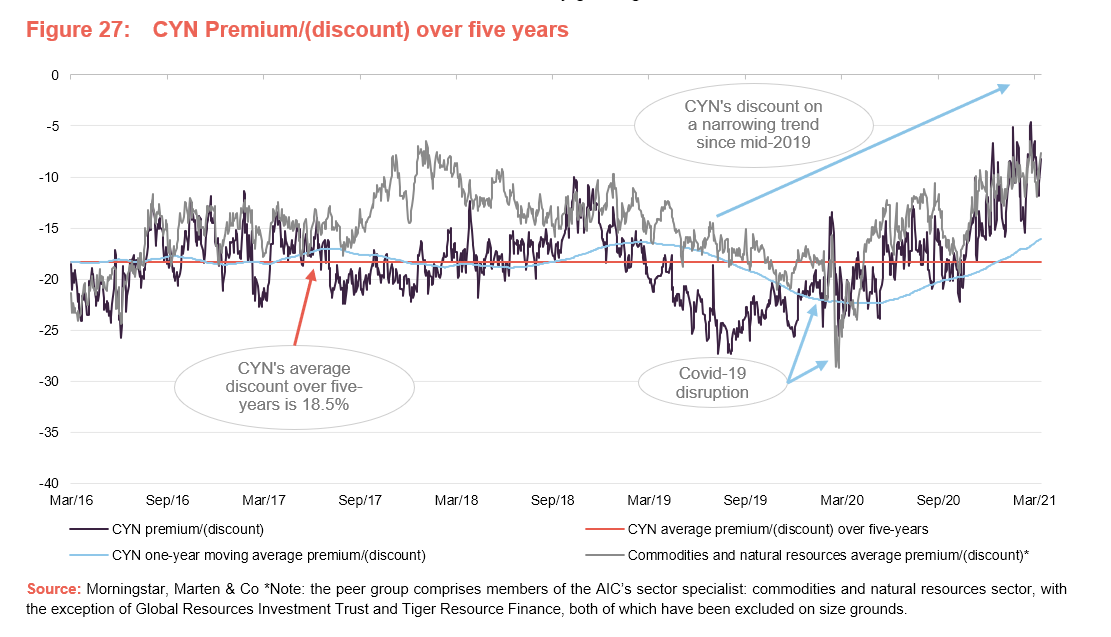

Bar the market disruption caused by COVID-19, CYN’s discount has broadly been on a narrowing trend, since mid-2019. During the last 12 months, CYN has traded at discounts between 4.6% and 23.9%, and an average of 16.0%. As at 12 April 2021, the discount was 8.2%, which is significantly below its longer-term five-year average and towards the narrower end of its one-year trading range.

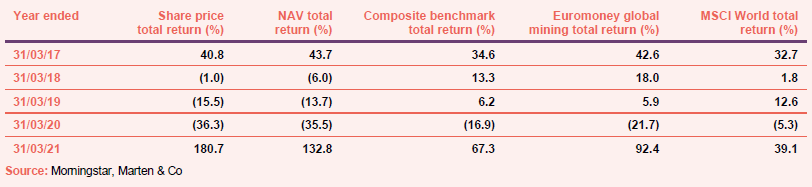

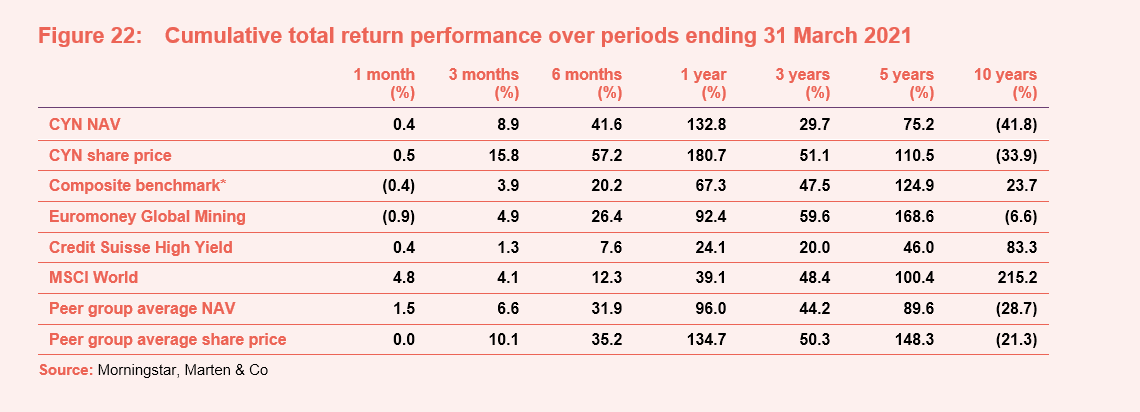

CYN has seen a marked improvement in both its absolute and relative performance during the last twelve months. It has also been able to outperform, by a margin, a strongly rising market. As illustrated in Figure 22 on page 20, CYN has also markedly outperformed its peer group averages, in terms of both NAV and share price total return, during the last 12 months.

Fund profile

Diversified natural resources exposure

CYN’s aim is to provide investors with capital growth and income by investing in a portfolio that predominantly comprises mining and resource equities, as well as mining, resource and industrial fixed interest securities.

Investments are typically made in securities that the manager has identified as undervalued by the market (both equities and fixed income) and that it believes will generate above average income returns relative to their risk, thereby also generating the scope for capital appreciation.

CYN’s portfolio is biased towards mid-cap stocks; meaning that it offers a more idiosyncratic exposure when compared against its large-cap focused peers. It also offers a markedly different exposure to exchange traded funds (ETFs) and the major natural resource focused indices.

CQS Group and New City Investment Managers

New City Investment Managers (NCIM) has been CYN’s investment manager since June 2003, when the trust underwent a major reorganisation that saw a complete change of focus to natural resources (previously it had been focused on Latin American investments). On 1 October 2007, NCIM joined the CQS Group, a global diversified asset manager running multiple strategies with asset under management (AUM) of US$21.8bn as at 26 February 2021. Ian Francis, Keith Watson and Rob Crayfourd are responsible for the day-to-day management of CYN’s portfolio. Keith and Rob focus on CYN’s equity holdings, while Ian primarily focuses on its fixed income holdings (see pages 28 and 29 for more details of the management team).

Composite benchmark index

CYN has a composite benchmark index that is weighted two-thirds the Euromoney Global Mining Index (formerly the HSBC Global mining Index) and one-third the Credit-Suisse High Yield Index. The composite is calculated using a base date of

1 August 2003 in sterling-adjusted total return terms. However, despite having this composite benchmark, CYN’s portfolio is not constructed with reference to it, or to any other index.

Market outlook and valuations

Natural resources remain cheap relative to global equities on a forward earnings basis

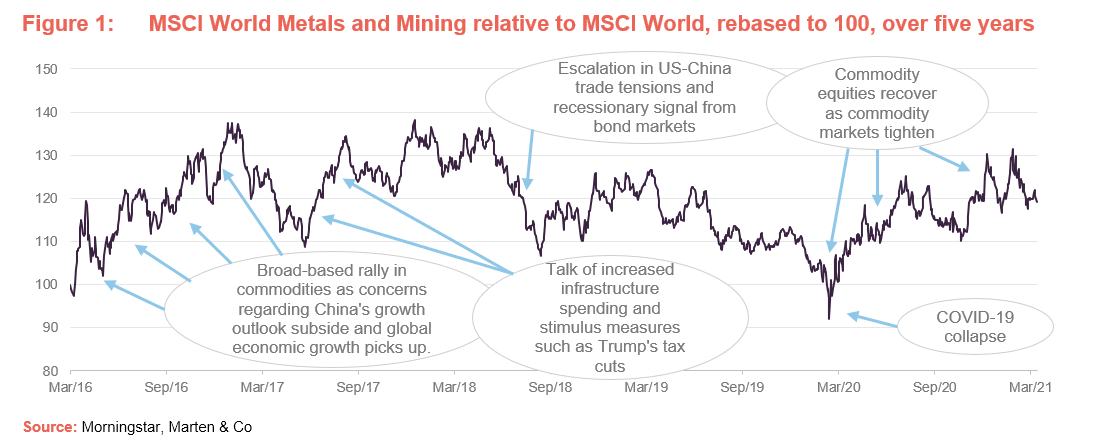

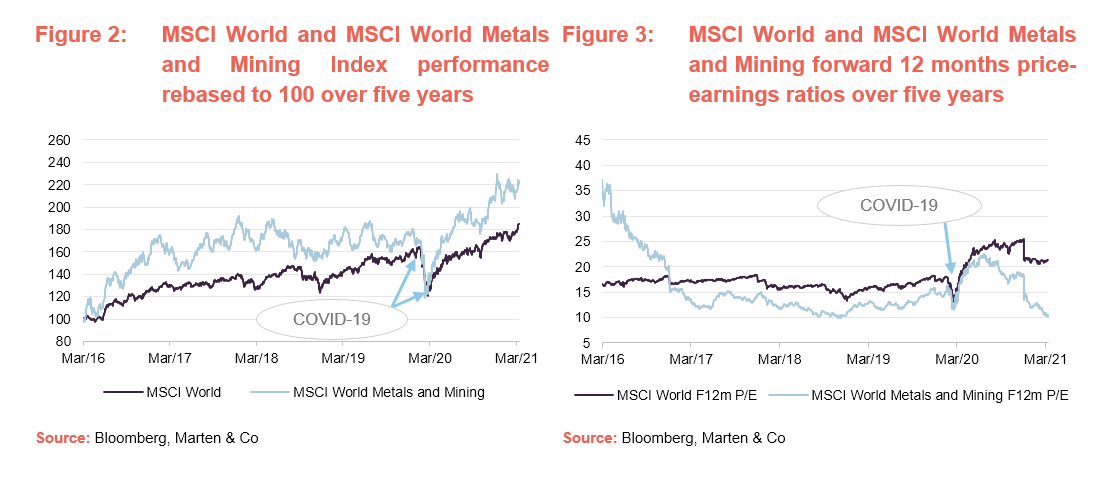

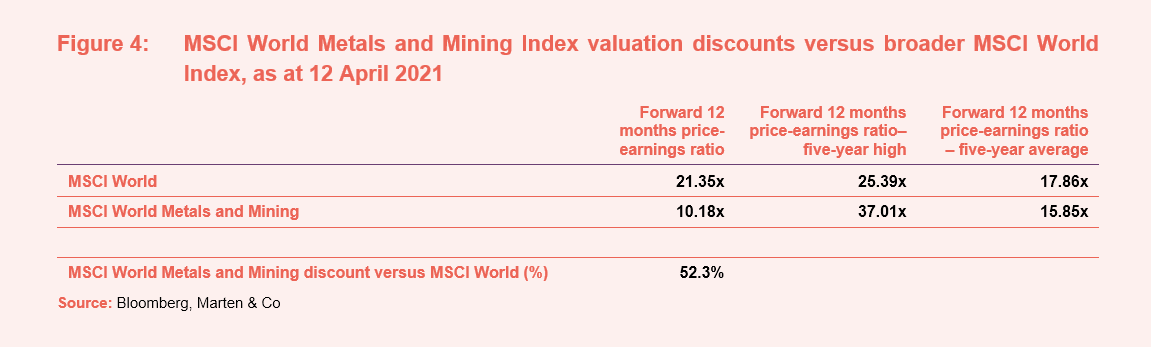

As illustrated in both Figures 1 and 2, commodities and natural resources stocks (as represented by the MSCI World Metals and Mining Index) have outperformed the broader global economy (as represented by the MSCI World Index) during the last five years. Almost all of the outperformance of the first four years was given back during the COVID-related market collapse of March last year (see pages 2 and 3 of our June 2020 note for more discussion). However, over the last 12 months the sector has rebounded, aided by significant supportive action by the authorities. Both the commodities and natural resources sector and broader global equities are trading at, or close to, five-year highs.

Nevertheless, despite the strong absolute and relative performance of commodities during the last year, the sector is trading at a marked discount to broader global equities on a forward price-earnings (P/E) basis (see Figures 3 and 4). This reflects a number of considerations, which are explored further below.

Commodities and natural resources are economically sensitive

As discussed in detail in our June 2019 initiation note, commodities and natural resources are inherently economically sensitive sectors. Resource extraction tends to be high fixed cost (sinking shafts and drilling wells is expensive) and it therefore takes time to bring on new supply. Higher growth environments tend to demand higher levels of commodities, e.g. for energy and infrastructure development, and with supply unable to respond quickly, prices will tend to rise sharply. Similarly, when economic growth cools, demand tends to react more quickly than supply, with prices falling and impacting profitability as a result.

Commodities and natural resources recovered strongly in the post-financial crisis era. This was driven primarily by global emerging markets, and in particular China, which underwent an economic boom during this period and ultimately led to what was deemed a ‘commodity-super cycle’. However, as markets became concerned about the outlook for global economic growth, and China in particular, commodities and natural resources suffered heavily between 2014 and early 2016. This was compounded as China, with high debt levels and an economy focused on exports, sought to rebalance its economy towards domestic consumption.

Things improved for the sector when concerns about China’s growth outlook subsided and global economic growth picked up. In the second half of 2017, talk of increased infrastructure spending and stimulus measures such as Trump’s tax cuts were working in the sector’s favour. However, the wind was taken out of its sails as Trump increased his anti-Chinese rhetoric. Commodities have suffered since, as high prices led to over-supply and ultimately a poor pricing environment. Inevitably, capacity then exited the market as, initially, higher marginal cost producers became unprofitable. This constrained supply helped lay the foundation for the current recovery in commodity prices.

Initially, as markets collapsed in the face of the pandemic, most commodities found themselves at the sharp end of the demand shock. Base metals and energy were hit particularly hard, as industry ground to a halt under the imposition of lockdown restrictions globally. Oil prices were crushed by a dispute between Organization of the Petroleum Exporting Countries (OPEC) and Russia (see page 10) and then fell further, as travel restrictions took effect and economic activity was curtailed. West Texas Intermediate (WTI) crude briefly saw negative pricing in April 2020. However, it quickly became apparent that supply for many commodities had been significantly affected by restrictions required to control the spread of the virus. Furthermore, as markets and economies rallied and industrial production recovered, supply has not been able to respond as quickly as demand. Many commodity markets saw inventory levels fall.

Infrastructure investment positive for commodities

The pandemic has exposed the frailties of infrastructure in many parts of the world. Governments are looking to infrastructure spending as a way of boosting the economy and supporting employment. Infrastructure investment is inherently commodity intensive and so this is expected to be supportive of the outlook for commodities.

In addition, if governments are to meet their climate change targets – such as net zero emissions by 2050 in the UK, Europe and the US and 2060 in China – considerable investment is required in renewable energy generation. There will also be new demand for power to support areas such as electric vehicle (EV) charging and domestic electric heating. Investment is also needed in national power grids and battery storage. This will require high levels of some commodities of which supply is structurally short.

A key feature of many governments’ recovery plans are initiatives similar to ‘build back greener,’ which is a cornerstone of UK government policy. There also appears to be an emerging consensus that, after a decade of ’informational wins‘, where companies have added value through the development of software, intellectual property (IP) and the like, and with investors focusing on asset light businesses, the next stage of progress will be much more reliant on physical components. Markets may be waking up to this, but CYN’s managers think that the scale of the problem is still vastly under-appreciated and that the value of these companies’ reserves could grow as the value of the end-product increases.

Managers’ view

Base metals and oil

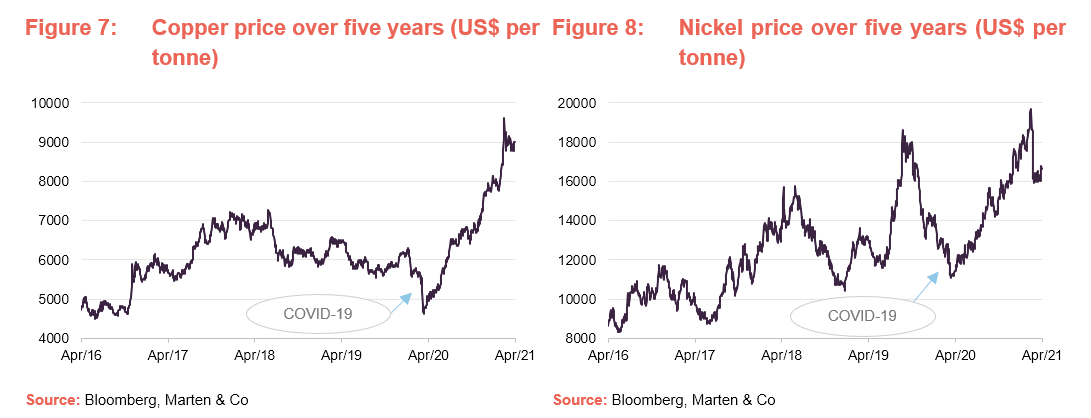

CYN’s portfolio has considerable exposure to base metals (a group of common and relatively inexpensive metals excluding precious metals such as copper, iron, nickel, lead and zinc), which have performed very strongly since the depths of the market crash. As is illustrated in Figure7, copper has done well, but the same can also be said for other base metals. For example, Figure 8 shows a much-improved nickel price over the last five-years. CYN’s managers say that markets are now looking towards a post-COVID world of demand returning, as well as the move to green energy. The managers also comment that the pandemic has highlighted how lacking infrastructure is in certain places and sectors.

With interest rates as low as they are and economies in need of stimulus, there is support for increased infrastructure spending. The managers think this is a long-term trend that will support demand for commodities. A backdrop of low supply growth should lead to increasingly tight markets.

For copper in particular, they see a tight market for the next four to five years, in part due to the project lead times that are required to put in new copper production capacity. The managers say that all copper-related stocks have been lifted recently, but they think this is justified on fundamentals over the medium term.

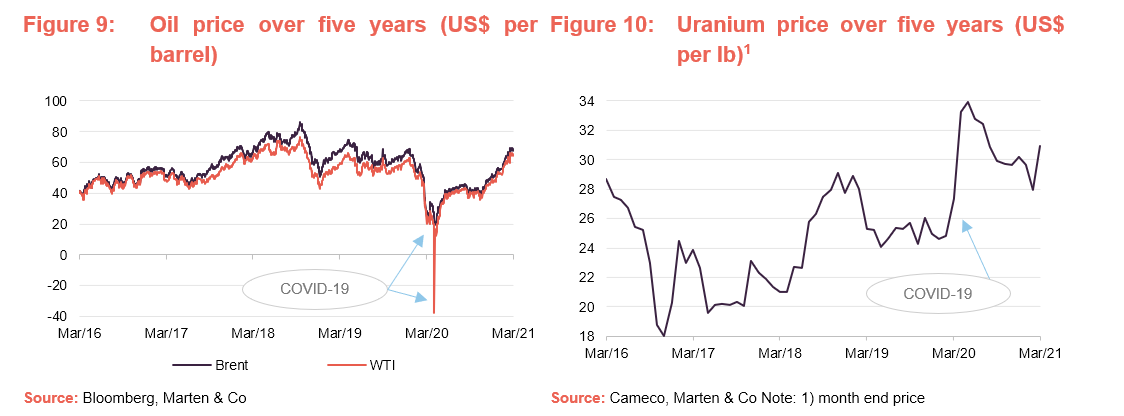

With regards to energy, they say that the argument is much more nuanced, but they believe that the energy backdrop is the best they have seen for five years, particularly in the oil space, which is reflected in the recent recovery in the oil price (see Figure 9).

Precious metals

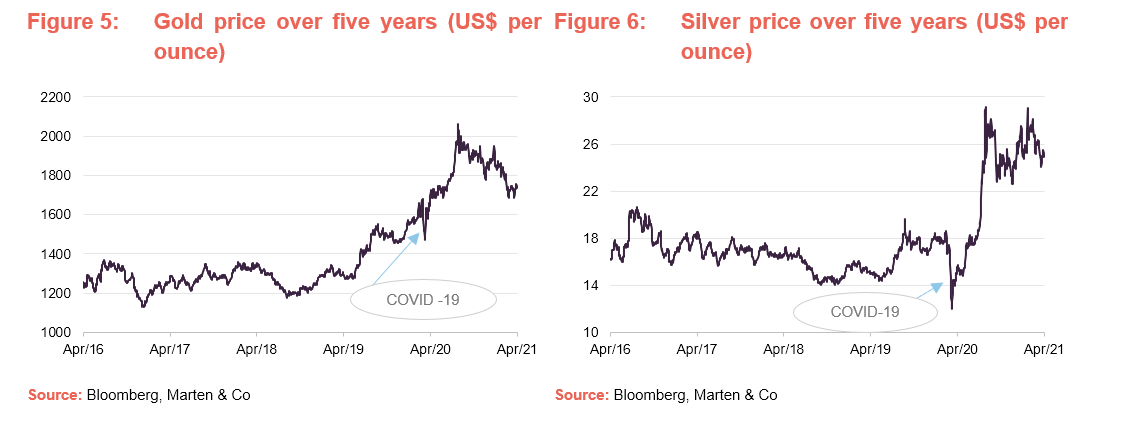

Precious metals, particularly gold and, to a lesser extent, silver, had a strong end to 2020 and a strong beginning to 2021. However, as is illustrated in Figures 5 and 6, there has been a pullback since. CYN’s managers say that while precious metal miners have increased in price, they still look very attractive in valuation terms. Furthermore, they consider that CYN’s holdings are attractive on a standalone basis and do not need an increase in the gold price to offer good returns.

Nevertheless, the managers think that recent increases in precious metal prices are yet to be fully reflected in the valuations of the underlying equities. They also believe that interest in gold could return. The managers observe that, during the pandemic, many people have increased their savings and they believe that as confidence returns, we could see an increase in demand for jewellery. The managers also see the potential for increased demand as industrial activities continue and expand and feel that, following the recent monetary expansion, central banks need to rebuild their reserves.

With regards to inflation, the managers think that there is mild deflationary pressure in the system (technology is leading to cost-cutting and margin compression) but, should inflation pick up due to high levels of government stimulus, gold will benefit. The managers observe that there are high levels of debt globally and think that this could be a key risk to the system. They also believe that, at least in the short term, the release of pent-up demand as people utilise some of the savings they have recently accrued, could also prove to be inflationary.

Uranium

Although it retrenched during the second half of 2020, the uranium price saw a substantial uplift in the second quarter of 2020 as markets tightened. CYN’s managers say that nuclear power is benefitting from a positive swing in sentiment in its direction. They say that both non-governmental-organisations (NGOs) and investors are increasingly aware of the need for nuclear power, both as a non-carbon emitting energy source and to provide baseload power in support of the green energy agenda (note: baseload is the minimum level of demand on a electrical grid over a given period of time. The grid needs to be able meet this demand and respond to demand increases as they occur).

Whilst renewables are an ever-increasing component of energy supply, production is intermittent in nature, making nuclear a useful part of the energy mix.

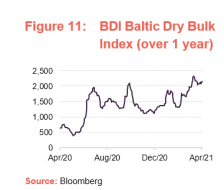

Shipping

CYN’s managers continue to observe that shipping is a very interesting space. New environmental regulations, in the form of IMO 2020 (IMO is a reference to the International Maritime Organisation), are designed to cut sulphur dioxide emissions and limit the amount of sulphur in the fuel oil used on board ships operating outside designated emission control areas to 0.50% m/m (mass by mass). This is a significant reduction from the previous limit of 3.5%.

CYN’s manager says that the new regulations, in combination with the effects of the pandemic, curtailed orders for new ships. Orders for cruise ships, dry bulk carriers, tankers and containerships are close to all-time lows. In addition, scrapping of some vessels was brought forward in the face of low day rates (for example, they say that crude shipping capacity has reduced from 100m barrels a day to 94m barrels a day). This is laying the foundations for a sustained supply and demand imbalance going forward.

While a resurgence in demand will lead to improved confidence and a revival in orders, these new ships will take time to build. Where there is a strengthening demand backdrop against a tight supply, shipping rates can increase dramatically leading to very high profitability for shipping companies.

The Baltic Dry Index, which is a measure of shipping costs, has risen from lows close to 400 in May 2020 to over 2,270 today, not far off decade highs. CYN’s managers believe that shipping will perform strongly in late 2021 into 2022, and beyond.

ESG considerations are increasing permitting times

As the row about the UK’s proposed new coal mine in Cumbria illustrates, environmental, social and governance (ESG) considerations are increasing focus of both governments and markets, which CYN’s managers believe is increasingly limiting the ability of commodity producers to add new supply. Mining is generally a dirty activity and can be an environmentally unfriendly one as well. CYN’s managers say that as societies look to improve their environmental footprint, it is becoming increasingly hard to get the necessary planning permission and permits to develop new mines. This means that this process takes longer and by extension it also means that supply demand imbalances, with the opportunity to earn supernormal profits, can last for longer before they are competed away.

Valuation

As noted in the valuations section above, while commodities and natural resources have performed strongly, on a forward price-earnings basis the sector looks cheap relative to broader global equities, arguably reflecting the strong earnings outlook for the sector. The managers also comment that, relative to current spot pricing, the sector looks cheap and they can consider that current EBITDA multiples are also easily justified. The manager continues to believe that despite recent share price increases, the market has not factored in the increase in the price of the underlying commodity properly.

Investment process – bottom-up coupled with a top-down macro-overlay

CYN’s portfolio is managed using a mixture of top-down and bottom-up investment strategies. The portfolio is able to access the full spectrum of natural resource and commodity investments and, for CYN’s equity holdings, the investment process begins with an assessment of the factors driving global demand and supply for specific commodities.

This considers supply-side factors such as exploration success, capacity developments, potential for supply disruptions and technological developments. It also considers demand side factors such as new applications, the potential for substitution, and technological developments. The managers look at demand from developed markets, but particular emphasis is placed on developments in the large industrialising emerging markets, as these tend to utilise a lot of commodities as they develop. The analysis also takes into consideration inventory levels and how these might develop. This analysis identifies sectors and geographical areas for the managers to focus their attention on when conducting their bottom-up analysis of potential investments.

It should be noted that the portfolio is not managed with reference to the trust’s benchmark, and while the macro overlay acts as a guide by directing the managers’ research efforts, it does not provide specific targets for the geographic and sectoral allocations. Instead, these are a result of the managers’ stock selection decisions, which reflect the managers’ assessment of the relative strength of individual investment ideas.

When constructing the portfolio, the managers seek to build a core that is focused on high-quality assets that are cash flow-generative, with strong balance sheets and management teams that have proven track records. In selecting companies, the managers focus on those:

- with commodities where they see little new supply additions;

- with commodities where they see a strengthening demand outlook;

- that have improving cost structures in terms of production;

- that have low cost operations and can self-sustain through the cycle; and

- that are multi-project (one-project operations are inherently risky).

The bulk of the managers’ efforts are focused on fundamental analysis of potential and existing investments. The CQS New City team meets an average of 20 resources companies a week and employs a range of valuation metrics to try and identify undervalued assets. These vary depending on the type of investment.

When selecting candidates for the portfolio, the managers seek to identify securities that they consider to be undervalued by the market. They expect these to generate superior income returns relative to their risk, with the scope for capital appreciation as the market rerates them. Whilst income generation and the sustainability of income are key, capital preservation is also a major focus and the managers are not prepared to sacrifice capital in the pursuit of income. When selecting fixed income holdings, often the managers will seek to exploit opportunities presented by the fluctuating yield base of the market and from redemptions, conversions, reconstructions and take-overs to generate capital growth. The managers’ analysis, which is conducted in-house, includes:

- an assessment of the free cash flow available to the various security holders within a corporate’s capital structure (for example, equity holders, debt holders, preferred stock holders and convertible security holders);

- the prospect of changes to cash flows (for example, from changes in interest rates or the competitive landscape); and

- an assessment of the company’s track record in managing its obligations and the quality of the company’s management.

- In assessing and selecting fixed income securities, the managers are able to draw on the expertise of a 16-strong team of credit analysts at CQS.

Once investments are included in the portfolio, the team continues to assess stocks to ascertain whether the level remains appropriate.

Investment restrictions

There are no restrictions for CYN’s holdings in terms of country, sector or size. When investing in higher yielding securities, CYN may invest beyond its traditional mining and resource companies.

CYN is permitted to acquire securities that are unquoted but which are about to be, or are immediately convertible at CYN’s option into securities that are listed or traded on a stock exchange. It may also continue to hold securities that cease to be quoted or listed if the manager considers this to be appropriate. In addition to this, CYN may invest up to 10% of its gross assets in unquoted securities. It may invest up to 10% of its total assets in other investment companies. CYN may borrow up to 25% of its net assets and will normally be fully invested.

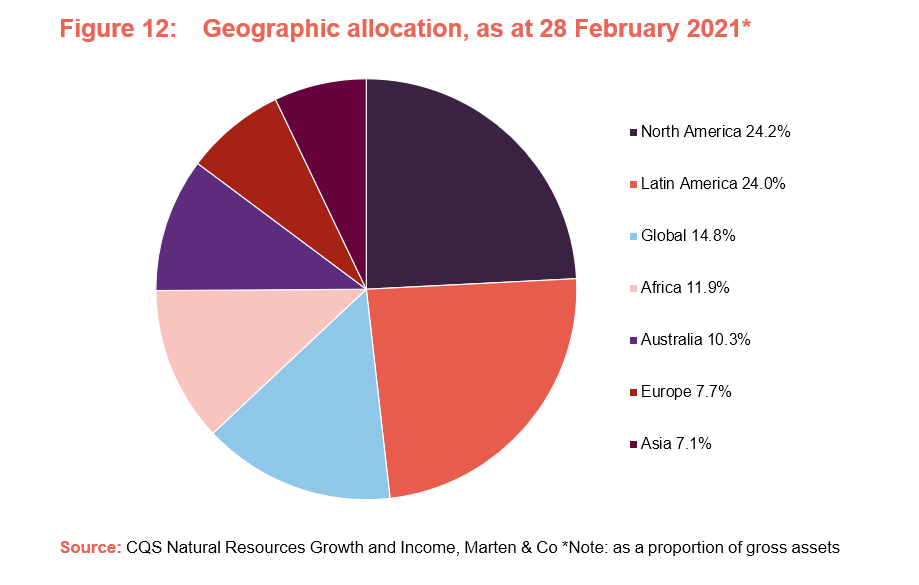

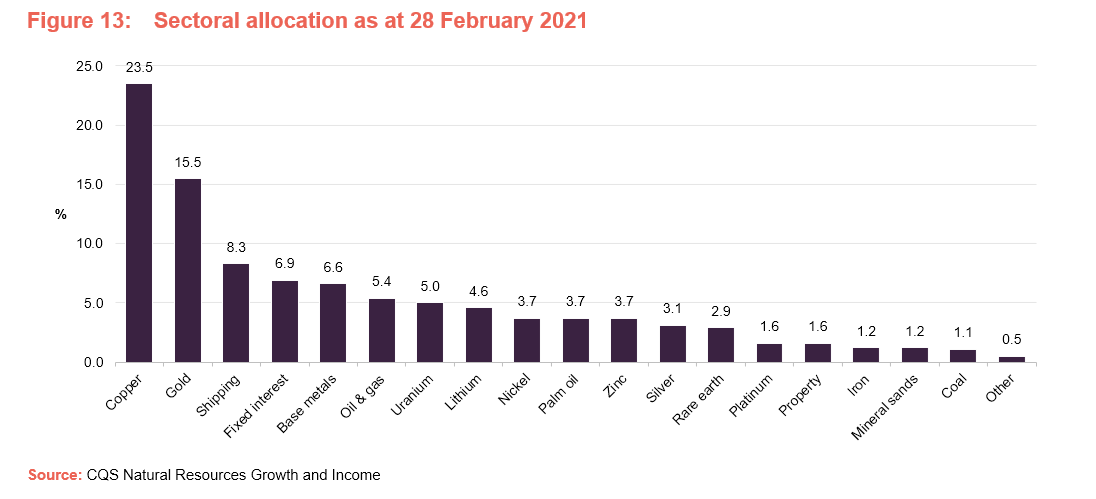

Asset allocation

Diversified portfolio that is biased to mid-caps and producers

As illustrated in Figures 12, 13 and 14, CYN offers investors a broad natural resources exposure with a modest fixed income element. The allocation to the fixed income has been reduced during the last 12 months as the managers have continued to de-emphasise higher yielding securities (see page 10 of our December 2019 initiation note for more discussion).

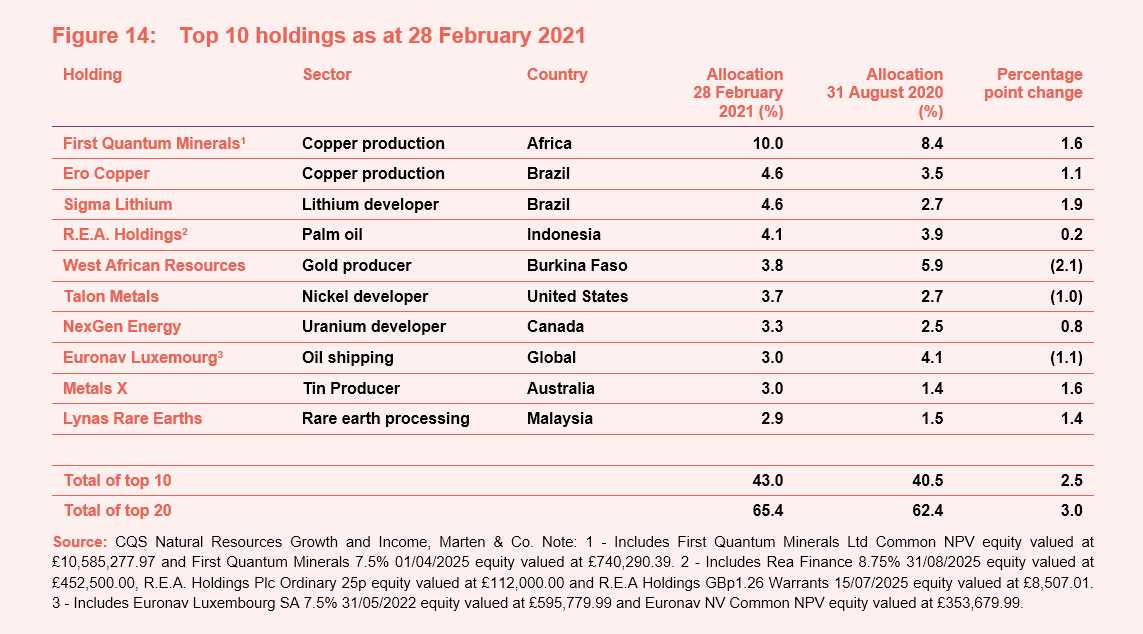

As discussed in our June 2020 note, the managers used the market turbulence created by COVID-19 to take advantage of inconsistencies that were thrown up by the market, although this was via existing names within the portfolio. There has been uplift in activity recently as the managers have used recent buoyant markets to make adjustments to the portfolio. As at 28 February 2021, CYN’s portfolio had exposure to 124 issues; an increase of six over 30 August 2020.

The names of the stocks that make up CYN’s top 10 holdings (see Figure 14) will likely be familiar to regular followers of CYN, which is arguably a reflection of the managers’ long-term low turnover approach. The managers typically expect portfolio turnover to be around 50% per annum but much of this will be trimming stocks whose prices have got ahead of themselves and adding to holdings where the managers see more value.

CYN’s portfolio has a bias towards mid-cap stocks, as the managers believe that this is generally where the best opportunities are to be found (this is a key differentiator versus some of its larger peers). It is also a differentiator versus the passive resource-focused ETFs, but these are generally focused on the large cap stocks and, in a post-MiFID II world, less research coverage generally means that they are more likely to find an undervalued security further down the market cap scale.

The portfolio has very little exposure to exploration and is biased towards producers, which make up its core holdings. The managers prefer companies that are cash-flow-generative and can sustain themselves through the cycle. This can exclude some smaller-cap operations.

Looking at Figure 13, and comparing this against the allocations as at 31 August 2020 (six months prior), the allocations to copper and gold have largely reversed their positions due to commodity price moves.

Gearing

It is worth noting that CYN now has much more flexible gearing (borrowing) – in the form of its revolving credit facility – than when its capital structure included convertible unsecured loan stock (CULS). It is much easier now for the managers to take money off of the table when they believe this is appropriate. The managers continue to say that the new mechanism is working well. At 26 February 2021, CYN’s net gearing was 11.6%.

Top 10 holdings

Figure 14 shows CYN’s top 10 holdings as at 28 February 2021 and how these have changed since over the six months from 31 August 2020.

New entrants to the top 10 are NexGen Energy, Metals X and Lynas Rare Earths. We discuss some of the more interesting developments in the next few pages and have also provided some commentary on Talon Metals and Sigma Lithium, which we have not written about previously. Readers interested in other names in the top 10 should see our previous notes, where many of these have been previously discussed (see page 31 of this note).

Sigma Lithium (4.6%) – lithium market could be tight through to 2026 and sigma lithium is trading at a discount to peers

Sigma Lithium (www.sigmalithiumresources.com) is a lithium developer and its assets are in Brazil. CYN’s manager says that the company has been able to position itself as a ‘green’ developer; the company has a small open-pit operation, which is generally less damaging to the environment then deeper excavations, and it is able to power the pit using green hydroelectric power.

![]()

CYN’s manager added to the position during the placing in February. Having moved into the production phase around 12 months ago, the company is now in discussion with the major battery manufacturers and CYN’s manager says that it expects it to secure agreements shortly. Against a backdrop of escalating demand due to green initiatives – for example, electric vehicles and increasing renewables elements with electricity grids – and inelastic supply due to poor investment in recent years, CYN’s managers are expecting to see a lithium shortage during the next 12 to 24 months. However, they think that the market is looking tight through to 2026 and possibly beyond and believe that Sigma Lithium is well-positioned to benefit, with the added comfort that it is trading at a discount to its peers.

Talon Metals (3.7%) – benefitting from successful drilling results, and a rising nickel price

Talon Metals (talonmetals.com) is a Toronto stock exchange-listed nickel explorer that was added to CYN’s portfolio around 18 months ago. Its primary deposit is the high-grade Tamarack Nickel project, which is a joint venture with Rio Tinto. The project, which is located in Minnesota, has been producing battery-grade lithium concentrate on a pilot scale since 2018. The company says that it has been shipping high-purity green and sustainable 6% Li2O battery-grade lithium concentrate samples to some of the leading global cathode and battery producers for electric vehicles.

CYN’s manager says that Talon has been successful in progressing this asset (its exploratory drilling program which has seen its hit high grades with a very high hit rate) and has also benefitted from a rising nickel price, all of which has helped lift the company’s share price. CYN’s managers say that in its last appraisal, which was for drilling results to the end of August 2020, it had a net asset value of US$570m. It has returned successful drilling operations since, so CYN’s managers expect to see a further uplift in both its reserves and NAV coming through. The manager has not added to the position; instead,

Talon Energy has moved up CYN’s rankings due to its strong performance. Subject to meeting certain obligations, Talon’s agreement with Rio Tinto entitles it to buy-out some of Rio Tinto’s position – first to give Talon Energy a 51% interest and then a 60% interest. Once it reaches a 60% holding, Rio Tinto is required to fund its 40% interest, or dilute its position. Furthermore, Rio Tinto has no back-in rights and Talon will control 100% of the off-take, irrespective of to whom the product is sold. Consequently, CYN’s managers see considerable further upside potential.

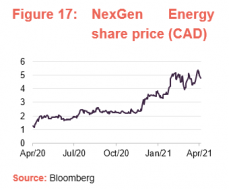

NexGen Energy (3.3%) – manager’s favourite uranium name

NexGen Energy (www.nexgenenergy.ca) is a uranium exploration and development company with a portfolio of projects that are centred on the Athabasca Basin in Canada, where it holds over 259k hectares of land. NexGen’s southwestern Athabasca Rook 1 property hosts the Arrow Deposit, the South Arrow discovery, the Harpoon discovery, the Bow discovery and the Cannon area. NexGen has long been a constituent of CYN’s portfolio and that of its sister Fund, Geiger Counter, where it has traditionally held a more prominent position (it is typically a top five Geiger Counter holding).

In May last year, NexGen completed a US$30m fundraise following which it said it had cash reserves of approximately CAD78m, which will be used to fund the permitting and development of the company’s Rook I Project (which hosts the 100%-owned Arrow Deposit) and for general corporate purposes. The NCIM team like NexGen’s assets, its management team and its financial strength. They consider that NexGen is well positioned to bring the Arrow Deposit into production and say that it remains their favourite of the uranium names. They comment that NexGen has the largest and best quality uranium assets in the world; its properties in the Athabasca basin are tier 1 assets that are under-appreciated by the markets in their view. Despite share price strength in the final quarter of 2020 – in part a reflection of a significant strengthening of the uranium price, the manager believes that the asset quality will drive a rating of the company. It also expects to see the assets go into production sooner than the market currently expects.

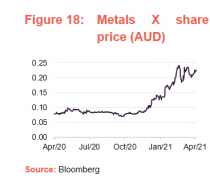

Metals X (3.0%) – sold copper assets to focus on tin operations

Metals X (www.metalsx.com.au) is an Australian base metals mining company which explores and develops metals and minerals in Australia. It has a 50% share in the Renison Tin Operation, which is Australia’s largest tin producer and one of the world’s largest and highest-grade tin mines globally. Until recently (see below), it was a top 10 Australian copper producer. It also has the country’s largest nickel-cobalt assets through its Wingellina, which hosts a resource continuing over 1.9Mt of nickel and 150Kt of cobalt.

As illustrated in Figure 18, after being largely during the second and third between the middle of May through to the end of October, the company’s share price saw a marked uplift since the end of November that has continued to climb into 2021, aided by the announcement in February that it has sold its portfolio of copper assets (including its Nifty copper operation, Maroochydore copper project and the Paterson exploration project) to focus on its tin operations. The copper assets were sold to Australian stock exchange-listed Cyprium Metals in a transaction that comprised a mix of cash, convertible notes and equity. Metals X said that the combination of cash and the release of its cash-backed bonds would both provide working capital and allow for a reduction in its debt. The convertible notes also provide upside if the copper operations are successful in the future. The company has been a constituent of CYN’s portfolio since 2016 and has risen up its ranks due to the recent strong share price appreciation.

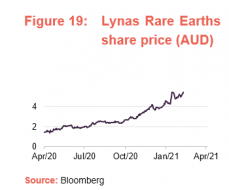

Lynas Rare Earths (2.9%) – largest rare earths producer outside China

Lynas Corporation (www.lynascorp.com) is an Australian company that, while small in mining company terms, is the largest rare earths producer and processor outside of China. The company, which is the second largest producer of rare earths globally, has been a constituent of CYN’s portfolio since 2016. Its rare earths deposit in Mount Weld, Western Australia, is one of the highest-grade rare earths mines in the world. The deposit, which is a collapsed volcano, is particularly attractive as it contains very low levels of thorium (a radioactive element frequently found within rare-earth elements), making the output from Mount Weald easier and less costly to process than other rare earth deposits. The company also operates the world’s largest single rare earths refining facility in Kuantan, Malaysia, which has been in operation since 2012.

Mount Weld has a flotation plant with which it processes the ore to turn it into a concentrate. This plant is designed to process 240,000 tonnes per annum of ore to produce up to 66,000 tonnes per annum of concentrate containing 26,500 tonnes of rare earth oxides. This concentrate is shipped to Malaysia for processing.

As we have discussed in previous notes, CYN’s managers have long considered that the outlook for rare earths is very favourable. As their name suggests, they are scarce and there is the added complication that the majority of global supply is concentrated in China. They are increasingly used in a broad range of high-tech applications for example in motors, hard drives, catalysts for the chemical industry, batteries; making their way into products such as cell phones, batteries for a rage of uses and wind turbines. They think that Lynas is one of the best positioned companies to benefit from the tight rare earths market. As illustrated in Figure 19, Lynas has performed very strongly during the last 12 months and this has pushed it up CYN’s rankings.

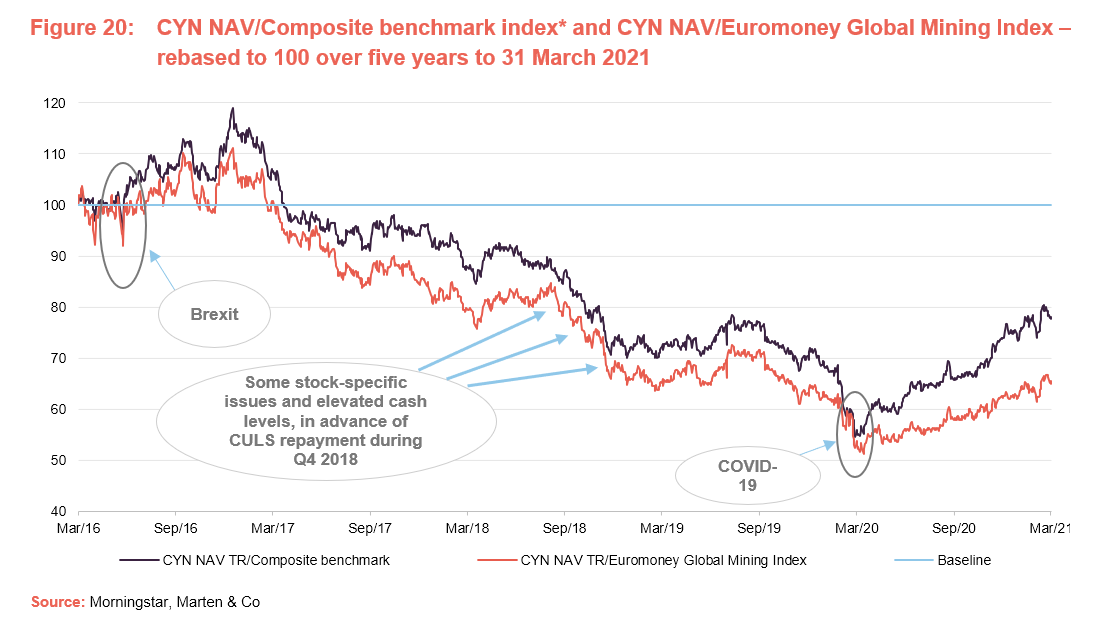

Performance

Figures 20, 21 and 22 illustrate that, after a four-year period of challenging performance relative to both its composite index and commodities and resources companies more generally, CYN has seen a marked improvement in both its absolute and relative performance during the last twelve months. While some caution must be exercised with regards to the absolute numbers, as a significant element of this includes the market recovery post the COVID-related collapse, CYN has nonetheless been able to outperform, by a margin, a strongly rising market. As illustrated in Figure 22, CYN has also markedly outperformed its peer group averages, in terms of both NAV and share price total return, during the last

12 months.

Looking in more detail at CYN’s sources of returns, CYN has a significant exposure to copper players and these have done well. Signal Lithium, discussed in the asset allocation section, has also done well, as has Lynas Rare Earths. The managers also say that companies exposed to the electric vehicle and green energy themes more broadly have also been among the stronger-performing holdings.

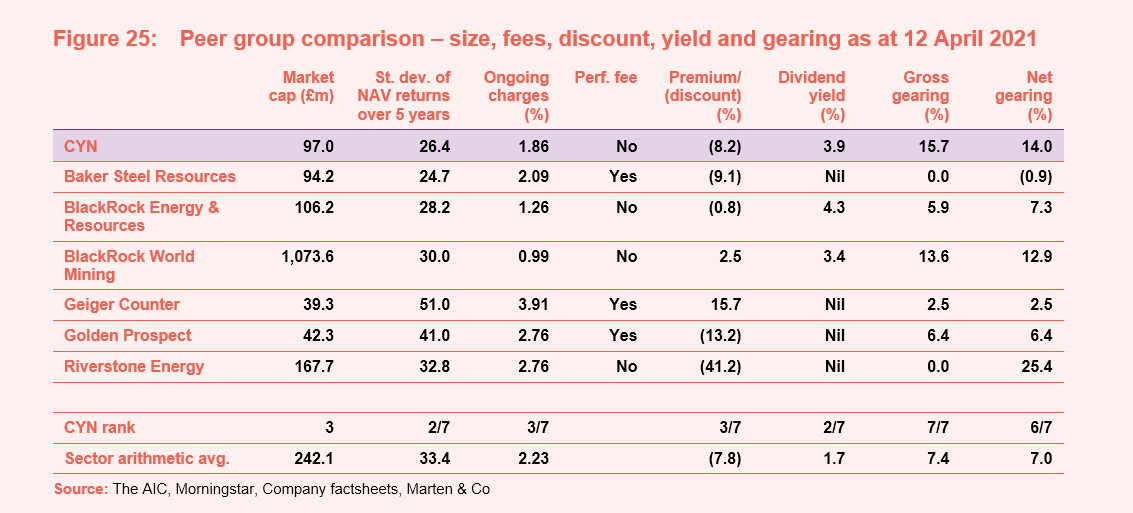

Peer group

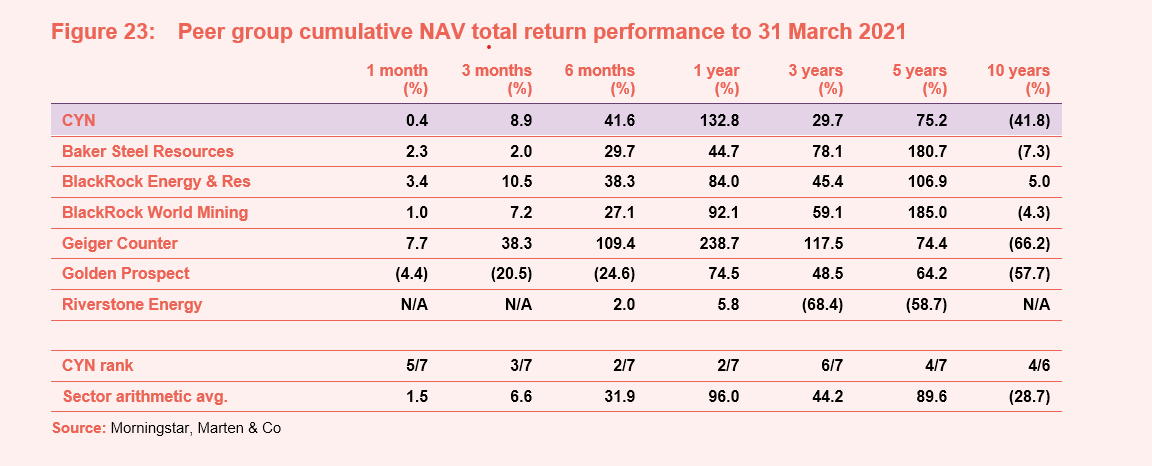

CYN is a member of the AIC’s sector specialist: commodities and natural resources sector, which is comprised of nine members. Seven of these are illustrated in Figures 23 through 25. However, for the purposes of this peer group analysis, we have excluded Global Resources Investment Trust (GRIT) and Tiger Resource Finance (TIR) on size grounds (both sub £5m market cap).

Despite all being members of the commodities and natural resources sector, the funds included in this peer group comparison are quite diverse and are imperfect comparators for CYN. For example, some of the funds have a narrow focus: Geiger Counter (click here to see our recent note) is focused on Uranium; Golden Prospect Precious Metals is focused on gold; Riverstone Energy has a concentrated portfolio of energy companies that are primarily engaged in oil exploration and production; and the BlackRock funds are both primarily invested in larger cap stocks (see further discussion on this in the next paragraph). Of all of its peers, Baker Steel Resources (BSRT) is arguably the closest in terms of size and approach.

Due to its size, BlackRock World Mining (BRWM) is generally viewed as a core holding in the sector. However, it is worth highlighting that CYN’s portfolio and approach are radically different to those of BRWM. By way of illustration, the four largest stocks in the Euromoney Global Mining Index are BHP Billiton, Vale, Rio Tinto and Newmont (these will be the major components of almost any large cap global resources index) and collectively account for around 36% of the Euromoney Global Mining Index. Similarly, these stocks will also represent a large proportion of most ETFs that invest in the sector. Rio Tinto, Vale and BHP are driven primarily by iron ore.

As at 31 January 2021, eight of the indices top 10 holding where also top 10 holdings in BRWM’s portfolio (collectively they represented some 51.3% of the index and 50.4% of the trust’s total assets). By comparison, CYN has no exposure to the top four index stocks, and there is no overlap between CYN’s top 10 holdings and the top 10 constituents of the index.

BRWM’s stablemate, BlackRock Energy and Resources Income Trust (BERI – formerly BlackRock Commodities Income), has a portfolio and investment objective that is more akin to CYN’s than BRWM’s. However, as at 31 January 2021, three of the indexes top four stocks featured in BERI’s top 10 holdings, collectively accounting for 19.6% of BERI’s total assets.

Because of these structural differences, CYN’s managers say, and we agree, that a holding CYN and BRWM could be seen as complementary as they offer markedly different exposures to the natural resources space.

As illustrated in Figure 23, having previously exhibited a tendency to underperform BSRT, which was possibly in part be due to being geared into falling markets due to its 3.5% CULS, CYN has strongly outperformed BSRT in NAV terms during the last 12 months. It is noteworthy that, in the absence of the structural gearing, CYN performance has seen a marked improvement. In fact, during the last year, CYN’s performance is only outstripped by its stablemate Geiger Counter, which has benefitted from particularly strong dynamics in the uranium market.

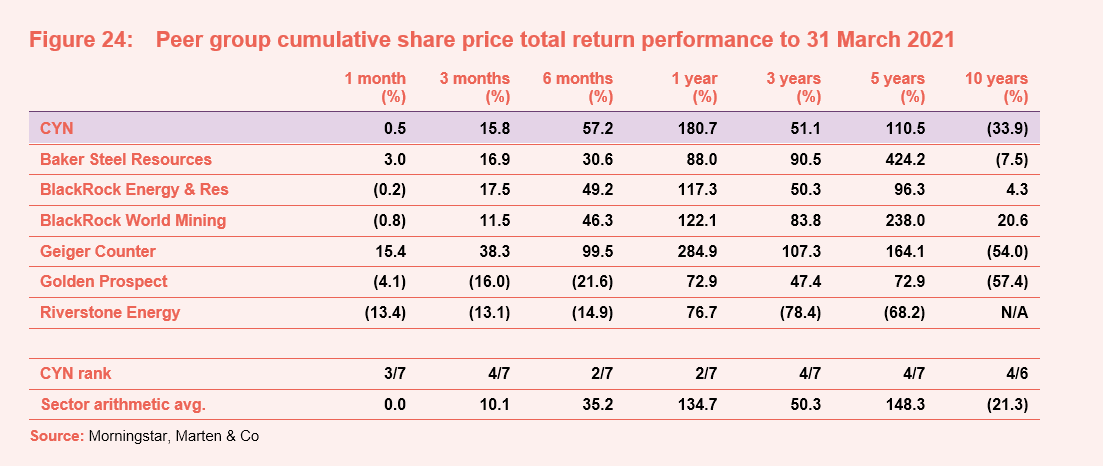

Figure 24 illustrates a similar story for share price total return as with NAV total return. It is notable that Geiger Counter is once again the top fund in the peer group and that CYN, with its small-cap focus, tends to outperform its large-cap-focused peers when markets are more buoyant.

CYN is the fourth-largest fund in the sector but, reflecting the significant scale of BlackRock World Mining, CYN’s market cap is markedly below the peer group average. CYN’s objectives include a focus on income and CYN offers the second highest yield in the peer group; over half of the funds do not pay a dividend. In some respects, this is not surprising. As discussed on page 25, commodities and resources have not traditionally been high-yielding areas and, whilst this has been improving, it is the large-cap stocks (generally the big producers) that are the best dividend payers. In this regard, it should be easier for the BlackRock Trusts, with their large-cap focus, to provide a dividend.

The volatility of CYN’s NAV returns (as illustrated by the standard deviation column in Figure 25) is lower than the peer group average, perhaps reflecting the fact that it has a more diversified portfolio than some of the funds in the peer group that have a very specific focus. It is notable that both of the BlackRock Funds, despite their large-cap focus, have higher volatilities than CYN.

CYN’s ranks third in terms of its ongoing charges ratio, which is markedly below the peer group average and also below that of its closest peer, BSRT. CYN does not pay a performance fee. BSRT has not paid a performance fee recently but its management arrangements include the provision of one that could potentially become payable in future years. A number of the funds within the sector are quite small and have higher ongoing charges ratios as a result (i.e. they have a smaller asset base over which to spread their fixed costs), which serves to elevate the sector average. In this regard, CYN benefits from its additional scale. However, if CYN realises its ambition to grow, this should serve, all things being equal, to lower CYN’s ongoing charges ratio.

Perhaps reflecting its strong performance, attractive yield and below-average ongoing charges ratio, CYN’s discount is below the peer group average. Gearing is another consideration, and maybe more of a concern for investors when markets are at more elevated levels and the end of the cycle is approaching. CYN’s gearing levels are above the sector averages although, in reality, the sector comprises a number of moderately geared funds and a number of funds that are ungeared.

Quarterly dividend payments

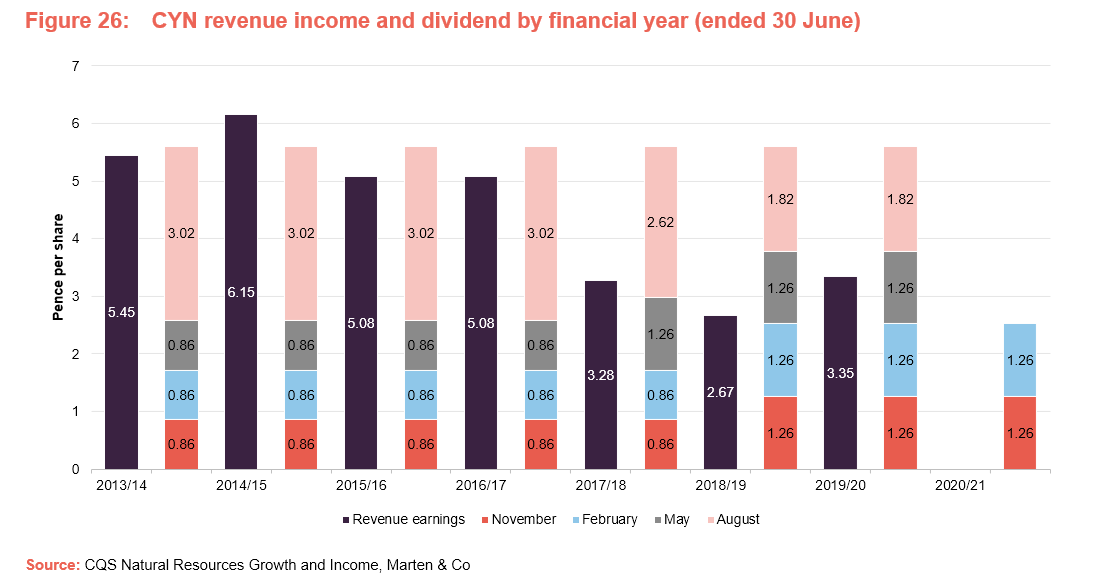

Subject to market conditions, the company’s performance, its financial position and financial outlook, the board intends to pay an attractive level of dividend income to shareholders on a quarterly basis. The company intends to pay all dividends as interim dividends. As discussed below, CYN will pay dividends out of capital when required.

For a given financial year, the first interim dividend is paid in November (2020: 1.26p) with the second, third and fourth interims paid in February, May and August. As illustrated in Figure 20 below, the total dividend paid for each of the last five financial years has been 5.6p per share. The target announced for the year ending 30 June 2021 has also been set at 5.6p per share. This is a dividend yield of 3.9% on CYN’s share price of 145.0p as at 12 April 2021. As illustrated in Figure 26, CYN traditionally paid three smaller interims with a significantly larger fourth interim. However, beginning with the year ended 30 June 2019, CYN rebalanced its dividend payments so that they are more equal in nature. To this end, the first two interims have been declared at 1.26p per share and it seems reasonable that CYN will pay the third interim at the 1.26p per share rate and the fourth interim at 1.82p per share as it has down for the last two financial years (5.6p per share in total).

Permitted to pay dividends out of capital

As Figure 26 shows, CYN’s revenue income has been less than its revenue earnings in six out of the last seven financial years, meaning that the trust has dipped into its revenue reserves to maintain the dividend at the 5.6p per share level for the last four financial years. As we have said previously, we think that to a certain extent, this should be expected. CYN’s investment objective includes both income and capital growth elements. Commodities and resources have not traditionally been high-yielding areas and, whilst this has been improving, the yield on CYN’s portfolio is likely to change as the manager adjusts its composition to best take advantage of the available opportunities. We think that in some years, investors should expect a shortfall, while in other years there may be an excess.

Following shareholder approval at CYN’s AGM in 2012, the trust is permitted to pay dividends out of capital and in March 2018 the board announced its intention to use CYN’s capital reserves, when required, to maintain or potentially increase the dividend level. This change has allowed the manager to focus on the total return from investments rather than needing to have an allocation to higher yielding investments, with a view to providing the necessary income to meet the dividend.

As at 30 June 2020, CYN had revenue reserves of £157k, or 0.23p per share (2019: £1,665k or 2.49p per share), which is equivalent to 4.1% of the 5.6p target for the year. In addition, as at 30 June 2020, CYN had a capital reserve of £13.9m or 20.72p per share (2019: £24.1m or 36.07p per share), which suggests that CYN has plenty of capacity to maintain the dividend at 5.6p per share, provided the board is still comfortable to pay this out of capital.

Premium/(discount)

As illustrated in Figure 27, bar the market disruption caused by COVID-19 in the first quarter of 2020, CYN’s discount has broadly been on a narrowing trend, since mid-2019. During the last 12 months, CYN has traded at discounts between 4.6% and 23.9%, and an average of 16.0%. As at 12 April 2021, the discount was 8.2%, which is significantly below its longer-term five-year average and towards the narrower end of its one-year trading range. However, CYN’s discount is modestly wider than the sector average of 7.8%. In comparison, the sector’s five-year average discount is 14.8% (with a range of 6.4% to 28.7%). CYN’s five-year average discount is 18.4% (with a range of 4.6% to 27.4%).

As we have discussed previously, arguably reflecting the more cyclical nature of resource companies, CYN’s discount has also exhibited a degree of cyclicality. This has been borne out by recent discount moves – CYN’s discount has continued on its general trend of narrowing, albeit with marked volatility, during a period that has seen the outlook for commodities improve.

CYN’s mid-cap bias may amplify market movements, although its relatively-high yield (the highest in the sector) offers investors a degree of comfort in that they are paid to wait.

While CYN has the authority to repurchase up to 14.99% and allot up to 9.99% of its issued share capital, the board says that it has no current intention of using this authority and, to date, CYN has not repurchased any of its shares. The board considers that share repurchases would likely have a limiting ability to provide any sustained change in the discount and, reflecting this, there is no formal discount control mechanism or discount target.

We have previously said that, given CYN’s current size, we believe share repurchases would likely have a limited impact on the discount as they would also serve to reduce liquidity and put upward pressure on CYN’s ongoing charges ratio (its fixed costs being spread over a smaller asset base). The board and manager are focused on increasing awareness of the trust, with the aim of eliminating the discount and ultimately growing the trust.

Fees and costs

Tiered base management fee; no performance fee

Under the terms of the investment management agreement, CQS is entitled to receive a basic management fee of 1.2% per annum of total net assets up to £150m, 1.1% of total net assets above £150m and up to £200m, 1.0% of total net assets above £200m and up to £250m and 0.9% of total net assets above £250m.

The management fee is calculated and paid monthly in arrears and there is no performance fee element. The management agreement can be terminated on

12 months’ notice by either side.

Secretarial and administrative services

Company secretarial and administrative services are provided by BNP Paribas Securities Services S.C.A., who replaced Maitland Administration Services (Scotland) Limited with effect from 15 September 2020. Maitland’s total fees for the year ended 30 June 2020 were £78,000 (2019: £106,000). BNP Paribas Securities Services also acts as CYN’s custodian, banker and depositary in place of HSBC Bank Plc. Custody and depositary fees were £36,000 and £15,000 respectively for the year ended 30 June 2020 (2019: £33,000 and £21,000).

Allocation of fees and costs

In CYN’s accounts, the investment management fees are allocated 25% to capital and 75% to revenue. All other expenses are charged wholly to revenue with the exception of costs incurred in relation to the disposal of investments, which are charged wholly to capital. The ongoing charges ratio for the year ended 30 June 2020 was 1.8% (2019: 1.9%).

Capital structure and life

CYN has a simple capital structure with one class of ordinary share in issue. Its ordinary shares have a premium main market listing on the London Stock Exchange and, as at 12 April 2021, there were 66,888,509 in issue with none held in treasury.

Short-term unsecured loan facility

CYN is permitted to borrow and has a short term £15m unsecured loan facility with Scotia Bank (Europe) Plc for this purpose. The loan facility is rolled every three months and can be cancelled at any time. The company also has the option to extend the facility to £20m if the board deems this to be appropriate. Under the terms of the facility, CYN is not permitted to allow the adjusted asset coverage ratio to be less than 3.5 to 1, and CYN’s total net assets are not permitted to be less than £30m.

CYN’s board has set a borrowing limit of 25% of net assets for ordinary market conditions. As at 31 March 2021, CYN had gross gearing of 15.7% and net gearing of 14.0%.

Unlimited life with an annual continuation vote

CYN does not have a fixed winding-up date, but at each annual general meeting (AGM) shareholders are given the opportunity to vote on the continuation of the company as an investment trust. This is a special resolution. If this resolution was not passed, the board would put forward proposals to liquidate or otherwise reconstruct or reorganise the company.

Financial calendar

The trust’s year-end is 30 June. The annual results are usually released in September/October (interims in March) and its AGMs are usually held in November/December of each year. As discussed on pages 24 and 25, CYN pays quarterly dividends in November, February, May and August.

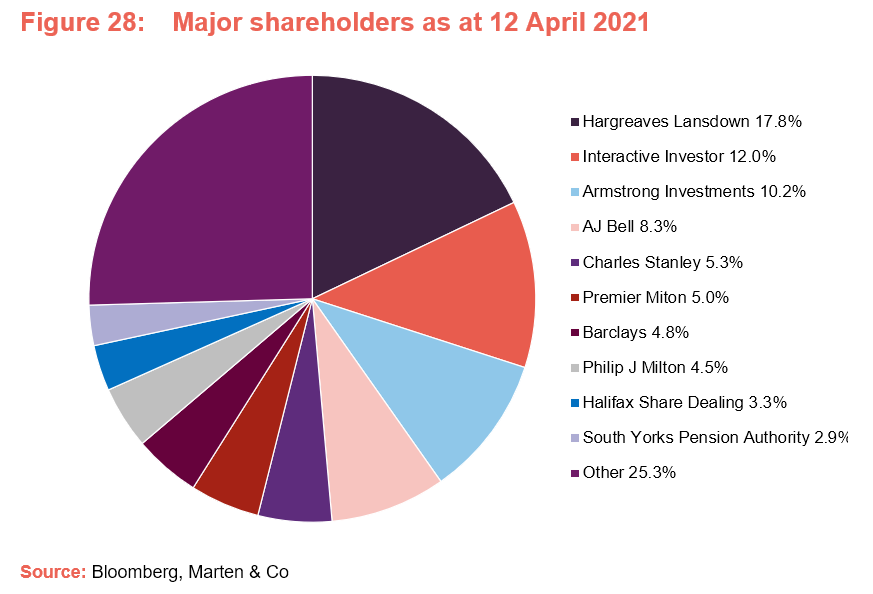

Major shareholders

Management team

CYN is co-managed by Ian Francis, Keith Watson and Rob Crayfourd. Keith and Rob focus on the equity side of the portfolio, while Ian primarily focuses on the fixed income securities. Keith and Rob also manage Geiger Counter Limited (also a client of Marten & Co – click here to read our most recent note) and Golden Prospect Precious Metals Limited.

Ian “Franco” Francis

Ian is a partner at CQS and Head of New City. He also manages the CQS New City High Yield Fund, which, like CYN, is a client of Marten & Co (click here to read our most recent research note). Ian joined NCIM in 2007 and has over 35 years’ investment experience, primarily in the fixed interest and convertible spheres, having worked for Collins Stewart, WestLB Panmure, James Capel and Hoare Govett. He is able to draw on the expertise of a 16-strong credit analysis team at CQS.

Keith Watson

Keith joined the NCIM team in 2013, initially as a dedicated natural resources analyst focused on supporting CYN’s managers.

Prior to NCIM, he worked for Mirabaud Securities, where he was a senior natural resource analyst; Evolution Securities, where he was director of mining research; Dresdner Kleinwort Wasserstein, where he was a top-ranked business services analyst; Commerzbank; and Credit Suisse/BZW. Keith began his career in 1992 as a portfolio manager and research analyst at Scottish Amicable Investment Managers. He has a BSc (Hons) in Applied Physics from Durham University.

Robert (Rob) Crayfourd

Rob joined the NCIM team in 2011. He has over 13 years’ financial experience, having previously worked for the Universities Super Annuation Scheme and HSBC Global Asset Management, where he focused on the resources sector. Rob holds a BSc in Geological Sciences from the University of Leeds and is a CFA charterholder.

Board

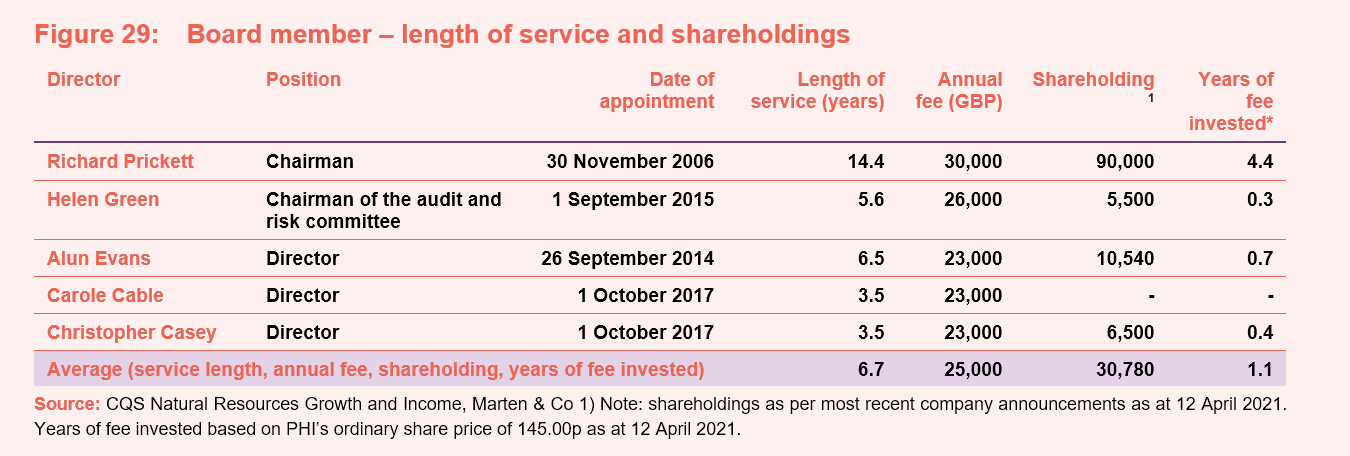

CYN’s board is comprised of five directors, all of whom are non-executive and considered to be independent of the investment manager. The company’s articles of association limit the aggregate fees payable to the directors to a total of £175,000 per annum.

CYN’s articles of association require that board members offer themselves for re-election at least once every three years. Board members that have served for nine or more years must offer themselves for re-election annually. However, board policy is that all members offer themselves for re-election annually. All existing board members were re-elected at the AGM on 9 December 2020.

Of CYN’s board members, the only director to have served more than nine years is the chairman, Richard Prickett, who has been a board member since November 2006. However, as is illustrated in Figure 29 below, Richard has a substantial personal investment in the trust (which was equivalent to over four years of his director’s fee as at 12 April 2021), which is positive in our view as it helps to ensure his interests are aligned with other shareholders.

In addition to CYN’s board, Richard Prickett and Helen Green previously sat on the board of Landore Resources Limited together, but following Richard’s retirement from that board in February 2020, CYN’s directors do not have any other shared directorships.

Richard Prickett (chairman)

Richard is a chartered accountant with considerable experience in the mineral sector and in corporate finance. He was a director of Landore Resources Limited (an AIM listed mineral exploration company of which he was previously CEO and finance director) until February 2020. Richard was formerly chairman of both Brancote Holdings (until its merger with Meridian Gold in 2002) and Asian Growth Properties Limited. He is a non-executive director of The City Pub Group Plc and of privately-owned Lamaune Iron Inc (a mining exploration and development company focused on the Lamaune iron ore and gold property, located in northern Ontario, Canada). Although Richard has been a director for just over 14 years, his tenure as chairman is considerably shorter (three years), having been appointed to succeed Geoffrey Burns, who stepped down in March 2018.

Helen Green (chairman of the audit and risk committee)

Helen is a chartered accountant with considerable experience of investment funds and, in particular, of fund administration and governance. She is a director of Saffery Champness (one of the UK’s Top 20 accountancy practices), in Guernsey. Helen joined Saffery Champness in London in 1984, relocating to Guernsey in 2000. She is a director of Acorn Income Fund Limited and Landore Resources Limited. She was formerly a director of Advance Frontier Markets Fund Ltd, Henderson Diversified Income Fund Ltd and John Laing Infrastructure Fund Ltd.

Alun Evans (directors)

Alun has over 40 years’ experience working in the investment management industry. He began his career at Capel-Cure Myers, moving to Carr Sheppards Crosthwaite in 1990, where he became an executive director in 1998. Alun joined Cheviot in 2009 as Business Development Director, from which he retired in August 2017.

Carole Cable (director)

Carole has had a 25-year career connected to the mining and commodities sector, initially on the sell side at JP Morgan and Credit Suisse, and latterly as a non-executive director both of Nyrstar NV (a global mining and multi metals business) and Women in Mining UK. She is currently a partner and co-head of the Energy and Resources division at Brunswick Group LLP, where she advises clients in the mining sector.

Christopher Casey (director)

Christopher is a chartered accountant and was formerly a partner at KPMG until 2010. Since leaving KPMG, he has carried out a number of non-executive board roles, including chairman of China Polymetallic Mining Ltd. Christopher is currently a director of Eddie Stobart Logistics Plc, TR European Growth Trust Plc, Black Rock North American Income Trust Plc and Mobius Investment Trust Plc.

Previous research

Readers interested in further information about CYN may wish to read our previous notes. You can read the notes by clicking on the links below.

Strong recovery potential? – Initiation – 11 June 2019

Recovery on-hold, hold on – Update – 23 June 2020

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on CQS Natural Resources Growth and Income Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.