CQS Natural Resources Growth and Income’s (CYN’s) managers believe the mining sector is only in the early stages of a recovery; real demand for commodities is on an upwards trend; and a reduction in capex has seen capacity removed from the market. If they are correct, all of these should be supportive of higher commodity prices in the future and support a sustained recovery in resource and mining stocks.

CQS Natural Resources Growth and Income’s (CYN’s) managers believe the mining sector is only in the early stages of a recovery; real demand for commodities is on an upwards trend; and a reduction in capex has seen capacity removed from the market. If they are correct, all of these should be supportive of higher commodity prices in the future and support a sustained recovery in resource and mining stocks.

Commodities and mining companies are attractively valued relative to both the broader global equity market and to history. CYN’s smaller size allows it to target mid-cap stocks and, when compared to competing funds (which tend to be large cap focused), ETFs and the major resources indices, it offers a very differentiated exposure. CYN’s managers see the strongest opportunities in mid-cap stocks, which are less well-researched; and have suffered as specialist funds have exited and ETF’s have increased their minimum market caps.

Capital growth and income from mining & resources

Capital growth and income from mining & resources

CYN aims to provide investors with capital growth and income by investing in a portfolio that predominantly comprises mining and resource equities, as well as mining, resource and industrial fixed interest securities. The fixed income securities include, but are not limited to, preference shares, loan stocks, corporate bonds (convertible and/or redeemable) and government bonds.

Fund profile

Diversified natural resources exposure

CYN’s aim is to provide investors with capital growth and income by investing in a portfolio that predominantly comprises mining and resource equities, as well as mining, resource and industrial fixed interest securities.

Investments are typically made in securities that the manager has identified as undervalued by the market (both equities and fixed income) and that it believes will generate above average income returns relative to their risk, thereby also generating the scope for capital appreciation of the security.

CYN’s portfolio is biased towards mid-cap stocks; meaning that it offers a more idiosyncratic exposure when compared against its large-cap focused peers. It also offers a markedly different exposure to ETFs and the major natural resource focused indices.

Name changed to emphasise CQS brand

At the company’s AGM on 4 December 2018, shareholders approved a resolution to change the company’s name to CQS Natural Resources Growth and Income Plc (previously City Natural Resources High Yield Trust Plc). The name change reflects a desire by the investment manager to consolidate and emphasise the CQS brand going forward. There has been increased advertising spend and CYN’s board were keen to align the trust to this. However, in all other respects the trust remains unchanged (this includes its ticker, which remains CYN). The trust retains its management team, who continue to follow the same strategy and investment process. CYN’s yield and growth objectives are also unaffected.

CQS Group and New City Investment Managers

New City Investment Managers (NCIM) has been CYN’s investment manager since June 2003, when the trust underwent a major reorganisation that saw a complete change of focus to natural resources (previously it had been focused on Latin American investments). On 1 October 2007, NCIM joined the CQS Group, a global diversified asset manager running multiple strategies with AUM of US$17.7bn as at 30 April 2019. Ian Francis, Keith Watson and Rob Crayfourd are responsible for the day-to-day management of CYN’s portfolio. Keith and Rob focus on CYN’s equity holdings, while Ian primarily focuses on its fixed income holdings (see pages 23 and 24 for more details of the management team).

Composite benchmark index

CYN has a composite benchmark index that is weighted two-thirds the Euromoney Global Mining Index (formerly the HSBC Global Mining Index) and one-third the Credit-Suisse High Yield Index. The composite is calculated using a base date of 1 August 2003 in sterling-adjusted total return terms. However, despite having this composite benchmark, CYN’s portfolio is not constructed with reference to it, or to any other index.

Market outlook and valuations

Commodities and natural resources are inherently economically sensitive sectors. Resource extraction tends to be high fixed cost (sinking shafts and drilling wells is expensive) and it therefore takes time to bring on new supply. Higher growth environments tend to demand higher levels of commodities, e.g. for energy and infrastructure development, and, with supply unable to respond quickly, prices will tend to rise sharply. Similarly, when economic growth cools, demand tends to react more quickly than supply, with prices falling and impacting profitability as a result.

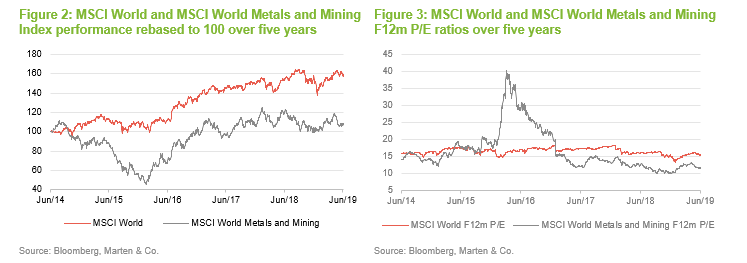

Commodities and natural resources recovered strongly in the post-financial crisis era. This was driven primarily by global emerging markets, and in particular China, which underwent an economic boom during this period. As illustrated in Figure 1, as markets became concerned about the outlook for global economic growth, and China in particular, commodities and natural resources suffered heavily between 2014 and early 2016. This was compounded as China, with high debt levels and an economy focused on exports, sought to rebalance its economy towards domestic consumption.

The result, as illustrated in both Figures 1 and 2, is that commodities and natural resources (as represented by the MSCI World Metals and Mining Index) have underperformed the broader global economy (as represented by the MSCI World Index) during the last five years. The overwhelming majority of this underperformance occurred during 2014 and 2015. 2016 saw a strong recovery and the last two years have seen the sector perform broadly in line with the broader global economy, albeit with periods of under- and outperformance as the outlook for the global economy has waxed and waned.

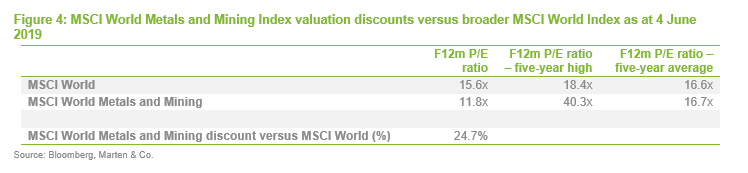

Natural resources are cheap relative to global equities

As is illustrated in Figures 3 and 4, commodities and natural resources look cheap in terms of price/earnings ratios relative to their five-year averages and are trading at a marked discount (24.7% – see Figure 4) to the broader global equity market.

Managers’ view

Mining sector is in the early stages of a recovery

CYN’s managers believe that the mining sector is only in the early stages of a recovery and think markets have overreacted to fears of an imminent economic downturn. They acknowledge that Chinese growth has slowed of late, and that this has been a headwind for the sector. The tariff war between the US and China has had some impact on Chinese growth. The managers note that supply chains appear to be adapting, to the benefit of countries such as South Korea, Thailand and Vietnam. They say that this cushions the effect on global growth.

Ideally, China and the US will strike a new trade deal. The managers think that, as the post-election stimulus from the last presidential race (and the end-2017 tax cuts) fades, this may encourage a greater willingness by Trump to compromise on trade negotiations with China in order to bolster his chances in the 2020 US presidential election.

Weaker Chinese data may also be the result of a corruption crackdown, deliberate measures to cool the property market, as well as environmental and clean air policies. The managers say that whilst they are disruptive in the short term, these measures are supportive of long-term economic and political stability and therefore of economic growth. A recurring theme has been high corporate indebtedness within China, but CYN’s managers believe that this is something that the Chinese state can manage. For example, 60% of corporate debt is held by state-owned banks.

China has injected some measured stimulus into its economy by easing monetary conditions and making direct infrastructure investments.

China is not the only driver of global growth. The managers highlight the high GDP growth rates being achieved by India (even after allowing for question marks over the veracity of that data). They also see little evidence of excess US spending or deteriorating labour market trends that might suggest an imminent US recession. Neither are they concerned about flattening yield curves (that show how the cost of borrowing changes over time – when it is cheaper to borrow for the long-term than the short-term, that is often a sign of an impending recession) or OECD leading indicators of economic strength.

The US Federal Reserve’s more ‘dovish’ stance (it has said that, given slower US growth it does not expect to raise US interest rates for the rest of 2019 and it will pause on the reversal of its quantitative easing programme) encourages the managers that forecasts of 3.3% global GDP growth in 2020 are achievable and they think the worst is over for commodities markets.

Period of active mandate changes coming to an end

CYN’s managers say that, in recent years, the resources sector has come under pressure from:

- Portfolio liquidations from the closure of a number of a number of specialist resource funds, and

- an increase in the minimum market caps that a number of ETFs will invest in.

These general trends have left miners, but particularly precious metals miners and those at the smaller end of the market capitalisation spectrum, trading at low valuations. In their view this is not sustainable over the long-term but, crucially, they believe that the period of active mandate changes is coming to an end. They believe that this could be the catalyst for a marked improvement in the sectors fortunes.

Real demand for commodities is still trending up

A previous market concern has been the extent to which a bubble exists in China’s housing market and the impact this may have on the property market, the broader economy, and, particularly, consumption, should it burst. The Chinese authorities have clearly been concerned and measures introduced to curb prices have had an impact. However, CYN’s managers remain comfortable with the longer-term outlook and feel that concerns have been overdone. They say that flat year-on-year pricing growth in the large, ‘Tier 1’ cities alleviates this risk and that measures to support social housing development both supports raw material use and puts the market on a more sustainable footing for the longer term. Moreover, newer buildings are being built to higher specifications and are using higher-quality steel, which is supportive of consumption of nickel, metallurgical coal and zinc. The managers conclude that the urbanisation trend continues, base metal demand is growing and, against a rising global population, real demand for commodities is still increasing.

Capital discipline has led to a reduction in capital expenditure, which is supportive of higher commodity prices in the future

Increased capacity during the commodities boom, set against falling demand, has lowered profitability and inevitably led to a reduction in capital expenditure by natural resources companies. Investors have pressured management teams to focus on capital discipline, which has forced mining companies to improve their focus on shareholder returns. Dividends and share buybacks have tended to be prioritised at the expense of capital expenditure, which erodes production capacity over the longer term. Furthermore, the low-price environment and environmental scrutiny has seen the closure of loss-making mines, which also removes capacity and helps to rebalance the market. However, as demand returns, supply cannot expand at the same rate and the managers expect that this will lead to a supply deficit and a superior pricing environment, particularly for base metals, in the future.

Gold – time to take a contrarian view?

Low inflation rates globally, rising interest rates, the expectation of further interest rate rises, and a strengthening US dollar have all been a headwind for the gold price in recent years. As noted above, this has been compounded by the closure of a number of specialist funds, and ETF’s increasing the minimum market caps of companies in which they will invest. The managers say that the sector is particularly unloved, with a number of precious metals producers and developers trading at less than half their NAV.

The managers believe that if investors are prepared to take a contrarian view, precious metals miners offer very attractive valuations at current spot gold prices, and the prospect of very attractive returns. Specifically, they highlight that improved capital discipline has seen very little new supply under construction, poor environmental practices have the seen the closure of some gold mines in China (as well as zinc and lead mines) and a recent improvement in the gold price could be a catalyst for mergers and acquisitions in the sector, spurred on by the mega-mergers of Barrick Gold and Randgold; and Newmont/Goldcorp.

Furthermore, gold is still a relevant form of portfolio insurance in the managers’ view; it offers a degree of inflation protection and tends to perform well in times of market dislocation. CYN’s managers believe that precious metals equities offer a superior way of gaining exposure to the gold price and the portfolio protection that it offers, given their attractive valuations. This is particularly acute in the mid-cap space, where CYN’s managers focus their efforts, as the majors need to replenish their reserves and typically look upon the mid-caps as a fertile hunting ground. The managers point out that industry reserves have been declining, global head grades (measures of how much gold is present in the ore) have been on a downward trajectory and that gold industry capital expenditure has also been on a steeply declining trend.

Oil sector is difficult – shale caps oil price at US$50-60 per barrel in the long term

CYN has some exposure to oil stocks and has benefitted as the oil price has recovered this year. However, the managers are generally cautious on the long-term outlook for oil and prefer to use shipping as an alternate way to get exposure that is less price-sensitive (for example, BW LPG, which is held in the portfolio, is a major owner of LPG (liquified petroleum gas) vessels and is a way of getting exposure to the rapid growth in US shale products).

CYN’s managers say that there is excess capacity for oil production globally, and whilst OPEC has cut production in the face of falling prices, US and Russian production is close to all-time highs. OPEC is handing market share to US shale producers, who are now the marginal producer (production in the Permian Basin (in the southwestern part of the United States) is driving US production growth). CYN’s managers acknowledge that disruption to Venezuelan supply could increase OPEC’s bite in the short term, but they do not think that OPECs cuts are sustainable over the longer term. They say that the oil price is broadly anchored in the US$50-60 per barrel range, as this is the level at which shale production starts to fall away. However, costs continue to fall as the efficiency of shale rigs improve and new pipelines come on stream.

CYN has been underweight in energy stocks, as the managers do not think they have been good value (for example, they think that operators in the North Sea need an oil price of US$55 per barrel to justify current valuations, which they find excessive). However, oil equities have been drifting down and are therefore becoming more interesting.

Investment process

CYN’s portfolio is managed using a mixture of top-down and bottom-up investment strategies. The portfolio is able to access the full spectrum of natural resource and commodity investments and, for CYN’s equity holdings, the investment process begins with an assessment of the factors driving global demand and supply for specific commodities (the ‘macro-overlay’).

This considers supply-side factors such as exploration success, capacity developments, potential for supply disruptions and technological developments. It also considers demand side factors such as new applications, the potential for substitution, and technological developments. The managers look at demand from developed markets, but particular emphasis is placed on developments in the large industrialising emerging markets, as these tend to utilise a lot of commodities as they develop. The analysis also takes into consideration inventory levels and how these might develop. This analysis identifies sectors and geographical areas for the managers to focus their attention on when conducting their bottom-up analysis of potential investments.

It should be noted that the portfolio is not managed with reference to the trust’s benchmark and, while the macro overlay acts as a guide by directing the managers research efforts, it does not provide specific targets for the geographic and sectoral allocations. Instead, these are a result of the managers’ stock selection decisions, which reflect the managers’ assessment of the relative strength of individual investment ideas.

When constructing the portfolio, the managers seek to build a core that is focused on high quality assets, that are cash flow generative, with strong balance sheets and management teams that have proven track records. In selecting companies, the managers focus on those:

- with commodities where they see little new supply additions;

- with commodities where they see a strengthening demand outlook;

- that have improving cost structures in terms of production;

- that have low cost operations and can self-sustain through the cycle; and

- that are multi-project (one-project operations are inherently risky)

The bulk of the managers’ efforts are focused on fundamental analysis of potential and existing investments. The CQS New City team meets an average of 20 resources companies a week and employs a range of valuation metrics to try and identify undervalued assets. These vary depending on the type of investment.

When selecting candidates for the portfolio, the managers seek to identify securities that they consider to be undervalued by the market. They expect these to generate superior income returns relative to their risk, with the scope for capital appreciation as the market rerates them. While income generation and the sustainability of income are key, capital preservation is also a major focus and the managers are not prepared to sacrifice capital in the pursuit of income. When selecting fixed income holdings, often the managers will seek to exploit opportunities presented by the fluctuating yield base of the market and from redemptions, conversions, reconstructions and take-overs to generate capital growth. The managers’ analysis, which is conducted in-house, includes:

- an assessment of the free cash flow available to the various security holders within a corporate’s capital structure (for example, equity holders, debt holders, preferred stock holders and convertible security holders);

- the prospect of changes to cash flows (for example, from changes in interest rates or the competitive landscape); and

- an assessment of the company’s track record in managing its obligations and the quality of the company’s management.

In assessing and selecting fixed income securities, the managers are able to draw on the expertise of a 16-strong team of credit analysts at CQS.

Once investments are included in the portfolio, the team continues to assess stocks to ascertain whether the level remains appropriate.

Investment restrictions

There are no restrictions for CYN’s holdings in terms of country, sector or size. When investing in higher yielding securities, CYN may invest beyond its traditional mining and resource companies.

CYN is permitted to acquire securities that are unquoted but which are about to be, or are immediately convertible at CYN’s option into securities that are listed or traded on a stock exchange. It may also continue to hold securities that cease to be quoted or listed if the manager considers this to be appropriate. In addition to this, CYN may invest up to 10% of its gross assets in unquoted securities. It may invest up to 10% of its total assets in other investment companies. CYN may borrow up to 25% of its net assets and will normally be fully invested.

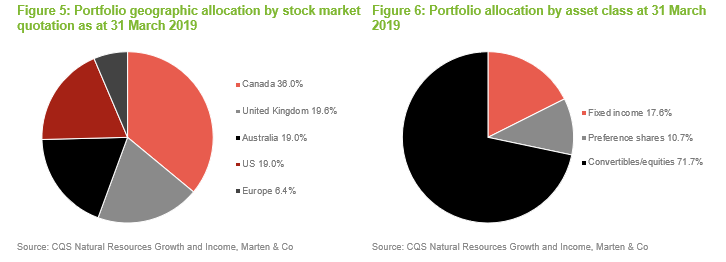

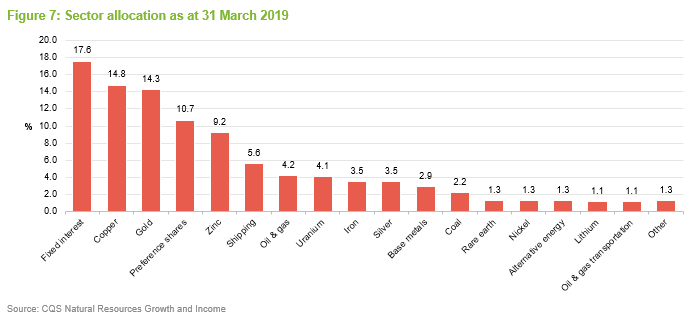

Asset allocation

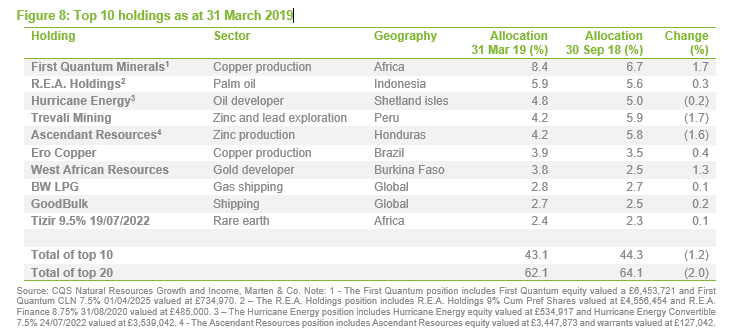

As illustrated in Figures 5, 6 and 7, CYN offers investors a broad natural resources exposure with a significant fixed income element. The names of the stocks that make up CYN’s top 10 holdings (see Figure 8) will likely be familiar to regular followers of CYN, which is arguably a reflection of the managers’ long-term low turnover approach. The managers typically expect portfolio turnover (sales and purchases as a percentage of portfolio value) to be around 50% a year but much of this will be trimming stocks whose prices have got ahead of themselves and adding to holdings where the managers see more value.

Portfolio concentration has increased as the managers have de-emphasised higher yielding securities

Last year, as the board decided to use CYN’s permission to pay dividends out of capital, the managers reduced the allocation to higher yielding securities – generally CYN’s fixed income holdings – in favour of those that the managers believed provide a superior total return (generally equities, as this is where the managers currently see more value). The managers were able to do this naturally as some instruments matured or were called. Reflecting this trend, the number of issues to which CYN is exposed has fallen markedly from 141 as at the end of June 2018 to 129 as at 31 December 2018 and 118 at the end of March 2019.

The portfolio has a bias towards mid-cap stocks. The managers believe that this is generally where the best opportunities are to be found (this is a differentiator versus some of its larger competitors). They say that the sector has seen significant flows into passive exchange traded funds (ETFs) but that these are generally focused on the large cap stocks that have the necessary liquidity. This, as well as less research coverage generally, means that the managers are more likely to find an undervalued security further down the market cap scale.

The portfolio has very little exposure to exploration and is biased towards producers, which make up its core. The managers prefer companies that are cash flow generative and can sustain themselves through the cycle. This can exclude some smaller cap operations.

Top 10 holdings

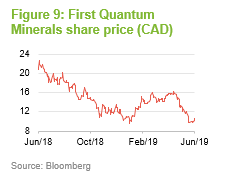

First Quantum Minerals (8.4%)

First Quantum Minerals (www.first-quantum.com) is a global top-10 copper producer, headquartered in Canada, with six mining operations. These are located in Africa (Kansanshi, Sentinel, Guelb Moghrein), Turkey (Çayeli), Spain (Las Cruces), Finland (Pyhäsalmi) and Western Australia (Ravensthorpe). It also has a number of development projects, the largest of which is Cobre Panamá, a large open-pit development located 120km west of Panama City and 20km from the Caribbean Sea coast. The concession consists of four zones totalling 13,600 hectares.

First Quantum’s Kansanshi mine is the largest copper mine in Africa. Mining is carried out in two open pits using conventional methods. Since it began operating in 2005, the mine has undergone several expansions that have seen its production capacity increase from 110k tonnes to 340k tonnes of copper and 120k ounces of gold per year.

CYN has held positions in First Quantum’s equity and convertible loan notes for many years. Having previously reduced CYN’s holdings as they felt valuations were looking stretched and were concerned that the company had been expanding aggressively, a distressed balance sheet in 2016 then provided the opportunity to increase CYN’s holdings. CYN’s managers felt that First Quantum had very high-quality core assets, located in good jurisdictions, and that the market reaction had been overdone. The sale of non-core assets along with cost-cutting led to a strong recovery in the share price. Shareholders have benefitted from a strong production growth profile since then.

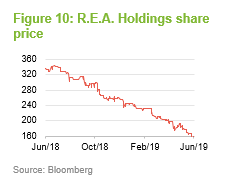

R.E.A. Holdings (5.9%)

R.E.A. Holdings (www.rea.co.uk) is engaged in sustainable cultivation of oil palms in the Indonesian province of East Kalimantan and in the production and sale of sustainable crude palm oil, and associated palm products, from the fruit harvested from its oil palms.

Like First Quantum Minerals, CYN has long held R.E.A.’s equity and cumulative preference shares within its portfolio. CYN does not generally hold exposure to soft commodities; palm oil is the exception, but the managers will only hold sustainable palm oil. R.E.A. obtained Roundtable on Sustainable Palm Oil (RSPO) supply chain certification in 2012. This allows it to sell the crude palm oil and crude palm kernel oil produced by its RSPO-certified estates to buyers that look to purchase RSPO-certified sustainable palm oil. The managers say that in addition to the environmental and reputational benefits of taking a sustainable approach, sustainable palm oil achieves a higher price because of its superior environmental credentials. Furthermore, environmental considerations limit the development of new supply and sustainable producers, such as R.E.A., are best positioned to benefit from this. More information is available here.

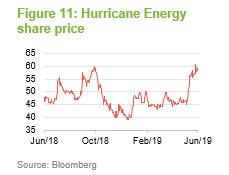

Hurricane Energy (4.8%)

Hurricane Energy (www.hurricaneenergy.com) is an oil exploration and development company that is focused in the west of Shetland region of the UK Continental Shelf. It is somewhat unusual in that it focuses on fractured basement reservoirs (found in metamorphic and igneous rock where faulting has led to the creation of a fracture network, underlying a sedimentary basin), where it has had some success. Hurricane has five major discoveries in the region. The most advanced of these is its Lancaster Field, which is targeting first oil in H1 2019. The Aoka Mizu, a floating oil platform, has arrived at the field. It initially encountered some difficulties getting anchored but was successfully hooked up to the turret mooring buoy on 19 March and is now in the process of being commissioned. Hurricane’s results announcement, published 28 March 2019, said that first oil, from Lancaster early production system, is imminent. Hurricane is also expecting first oil from its Great Warwick Area in Q4 2019.

As an exploration company, Hurricane features in the portfolio as CYN’s managers believe it has the quality of asset, expertise and finance that are necessary to get to production. The managers like Hurricane’s equity, but also participated in its convertible 7.5% 24/07/2022 when this came to market. They felt this finance would take Hurricane through to production and significantly de-risked Hurricane, making the bond very attractive. In this regard, it is worth noting that while the managers are generally cautious on oil as they think the price is broadly anchored in the US$50-60 per barrel range (see page 8), Hurricane is an exception to this due to relatively low cost of production. The managers say that using conservative assumptions and data from Hurricane, suggests it has operating costs in the region of US$13-14 per barrel. Adjusting for sustaining capital expenditure increases this to US$ 22-23 per barrel, which is materially lower than most other North Sea producers. The managers say that this means that Hurricane should be very profitable within its expected oil price range.

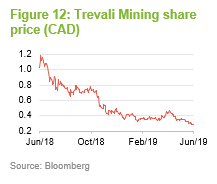

Trevali Mining (4.2%)

Trevali Mining (www.trevali.com) is a zinc producer with four operating mines in Canada (Caribou), Namibian (Rosh Pinah), Burkina Faso (Perkoa) and Peru (Santander). The company acquired two of its mines (Rosh Pinah and Perkoa) from Glencore in July 2017. This transaction moved Trevali up the rankings, making it a top 10 global zinc producer, and the world’s largest pure-play zinc producer. Glencore remains a cornerstone shareholder, with a 25.8% strategic stake, and provides technical and logistical support to the company.

Zinc production has declined globally, and the market is now in deficit. CYN’s managers say that inventories have now fallen to a level where the zinc price normally responds sharply, and they see strong recovery potential from here.

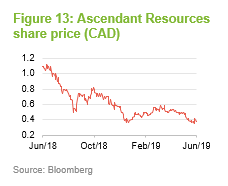

Ascendant Resources (4.2%)

Ascendant Resources (www.ascendantresources.com) is a pure-play zinc mining company with two primary assets: its El Mochito zinc, lead and silver mine in west-central Honduras, and its high-grade polymetallic Lagoa Salgada VMS Project, located in the prolific Iberian Pyrite Belt in Portugal. Since acquiring El Mochito in 2016, Ascendant has optimised the mine to deliver record levels of production and restore profitability. Ascendant is a low-cost producer, with further opportunities to drive down costs. This has allowed it to benefit from higher zinc prices. The managers see opportunities for it to expand its existing resource base and drive further free cash flow and profitability improvements.

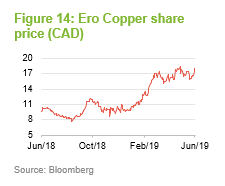

Ero Copper (3.9%)

Ero Copper (www.erocopper.com) is a base metals mining company, headquartered in Canada, which is focused on the production and sale of copper in Brazil. Its primary asset is its 99.6% interest in Mineração Caraíba S.A. (MCSA). MCSA is a long-established Brazilian copper mining company with over 37 years of operating history in the Curaçá Valley. MCSA’s primary asset is the MCSA Mining Complex, located in Bahia State, in north-eastern Brazil. The MCSA Mining Complex is a fully integrated mining and processing operation.

MCSA owns 100% of Boa Esperanҫa development project, an IOCG-type (Iron oxide copper gold) copper deposit located in southern Pará State, Brazil. The company says that this development offers it incremental low-cost production growth. Ero is targeting first production from Boa Esperanҫa in 2022.

Ero Copper also owns the NX Gold Mining Complex, a fully integrated operation that comprises an underground mine and above ground processing facility. The NX Gold Mining Complex is located in Mato Grosso State, south-eastern Brazil, approximately 670 km east of the capital, Cuiabá. Doré bars containing gold and silver, as well as lesser amounts of lead, are shipped from the mine weekly by air, via a gravel airstrip located on the property. (Note: A doré bar is a semi-pure alloy of gold and silver, which is usually created at the site of a mine. These will usually be transported elsewhere to be refined.)

CYN’s managers like the long-term outlook for copper and gold. They consider that Ero Copper, with its production revenues and operational experience, is well positioned to improve its existing operational assets and to bring the Boa Esperanҫa development project to production. Brazil is a good mining jurisdiction in their view, which is benefitting from a more business-friendly political backdrop.

Performance

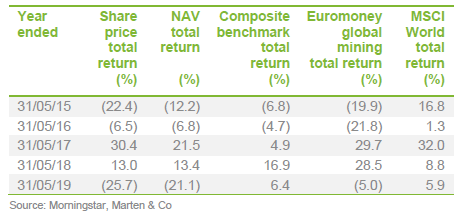

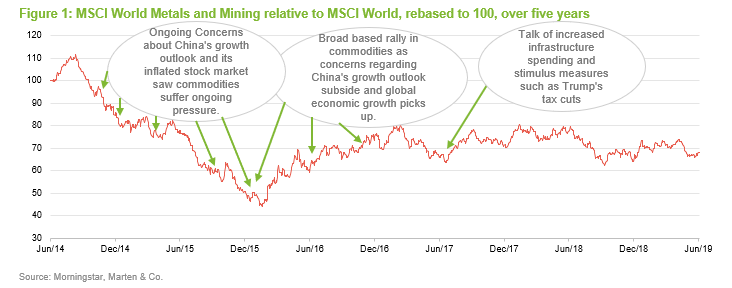

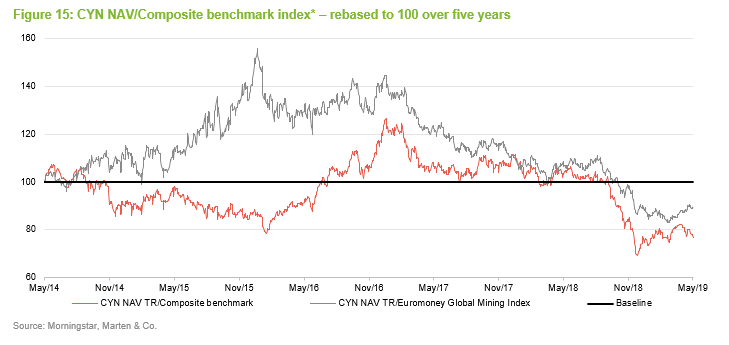

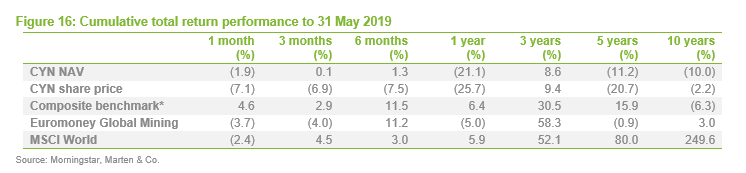

As illustrated in Figures 15 and 16, CYN’s NAV markedly underperformed its composite benchmark and the Euromoney Global Mining Index, during the second half of 2018. This has eroded the longer-term record, which was otherwise one of moderate performance during the last five years, albeit with marked periods of under- and outperformance within this. Whilst there were stock-specific wins and losses, CYN’s managers say that the primary cause was the unusually high levels of cash help in the portfolio in advance of repaying the company’s convertible unsecured loan stock, which matured at the end of September 2018 (see page 21 – in essence the returns on cash are typically modest and will be less than those of a strongly rising equity market). In 2019, to date, CYN has made up some of this underperformance against its benchmark.

The drag from the elevated cash eroded performance as markets peaked in the summer. The convertible unsecured loan stock (CULS) were repaid using a mixture of both cash and CYN’s revolving credit facility. This also meant that, as markets became unsettled in the last quarter of 2018 and sought cover in defensives (companies in sectors that are less cyclical in nature and therefore are less vulnerable to economic downturns), CYN’s portfolio was more geared (had higher borrowings relative to its net assets) than might have otherwise been the case, thereby compounding the problem. CYN’s bias towards the mid-caps was an additional factor, as these tend to be more sensitive in a setback than their larger-cap brethren. However, the managers say that they’re very comfortable with the shape of the portfolio and are confident regarding its long-term outlook. CYN no longer employs structural gearing (long term debt instruments) in its capital structure, and so the managers will have greater flexibility in how they deploy gearing going forward.

Peer group

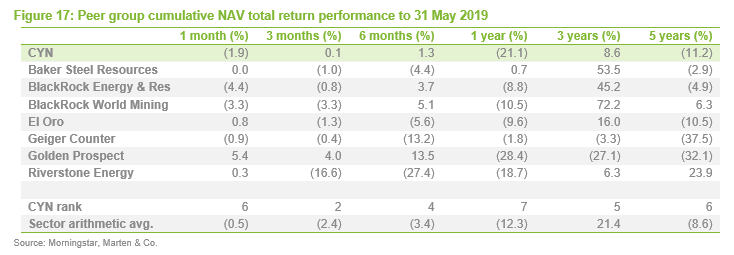

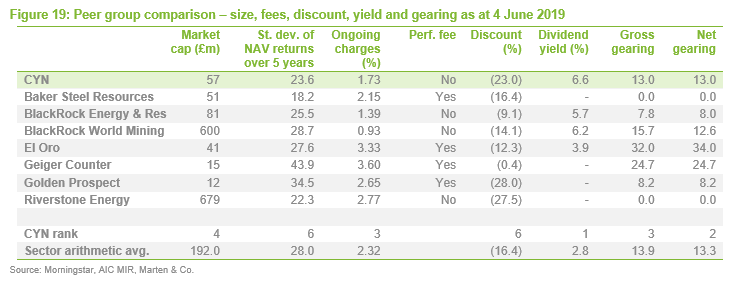

CYN is a member of the Association of Investment Companies sector commodities and natural resources sector, which comprises 10 members. Eight of these are illustrated in Figures 17 through 19. However, for the purposes of this peer group analysis, Global Resources Investment Trust (GRIT) and Tiger Resource Finance (TIR) have been excluded on size grounds. As at 4 June 2019, GRIT and TIR had market caps of £1.1m and £0.5m respectively. This makes them both markedly smaller than most of the other funds in the sector and do not have the necessary scale or liquidity to make them particularly useful comparators for CYN (in comparison, CYN had a market cap of £56.7m as at 4 June 2019).

Despite all being members of the commodities and natural resources sector, the funds included in this peer group comparison are quite diverse and are imperfect comparators for CYN. For example, some of the funds have a narrow focus: Geiger Counter (click here to see QuotedData’s recent note) is focused on Uranium; Golden Prospect Precious Metals is focused on Gold; Riverstone Energy has a concentrated portfolio of energy companies that are primarily engaged in oil exploration and production; El Oro has an eclectic mix of holdings some of which are not at all resource-focused; and the BlackRock funds are both primarily invested in larger cap stocks (see further discussion on this in the next paragraph). Of all of its peers, Baker Steel Resources (BSRT) is arguably the closest in terms of size and approach.

Due to its size, BlackRock World Mining (BRWM) is generally viewed as a core holding in the sector. However, it is worth highlighting that CYN’s portfolio and approach are radically different to those of BRWM. By way of illustration, the four largest stocks in the Euromoney Global Mining Index are BHP Billiton, Vale, Rio Tinto and Glencore (these will be the major components of almost any large cap global resources index) and collectively account for around 45% of the Euromoney Global Mining Index. Similarly, these stocks will also represent a large proportion of most ETFs that invest in the sector and, as at 28 February 2019, these four stocks were the top four holdings in BRWM’s portfolio (collectively they represented some 35.7% of the trust’s total assets). By comparison, CYN has no exposure to these four stocks.

BRWM’s stablemate, BlackRock Commodities Income (BRCI), has a portfolio and investment objective that is more akin to CYN’s than BRWM’s. However, as at 28 February 2019, three of the indexes top four stocks featured in BRCI’s top ten holdings, collectively accounting for 15.5% of BRCI’s total assets.

Because of these structural differences, CYN’s managers say that a holding CYN and BRWM could be seen as complementary as they offer markedly different exposures to the natural resources space.

As illustrated in Figure 17, CYN has tended to underperform BSRT, which may in part be due to the structural gearing into falling markets provided by CYN’s 3.5% convertible unsecured loan stock (CULS) during the last seven years. This should be less of an issue going forward. The CULS were issued in September 2011 and matured at the end of September 2018. This is a period that, overall, did not favour resources and commodities stocks and the gearing would have been a drag for CYN (in comparison, BSRT has followed an ungeared strategy). CYN’s CULS were repaid using a mixture of cash and a revolving credit facility, rather than putting new structural gearing in place. This should give CYN more flexibility in its use of gearing.

Relative to the more large-cap focused peers, CYN’s performance has been affected by a trend of large institutional holders selling down small cap names and focusing on large cap names instead. This has been through a combination of some of the specialist funds exiting the space and some ETFs increasing their minimum market caps for investment. In relative terms, this has benefitted the funds with a large cap bias and punished those with a small cap value bias. The managers believe that we are at the end of this trend of active mandate change and expect small cap value names to outperform as the valuation anomaly reverts, to CYN’s benefit.

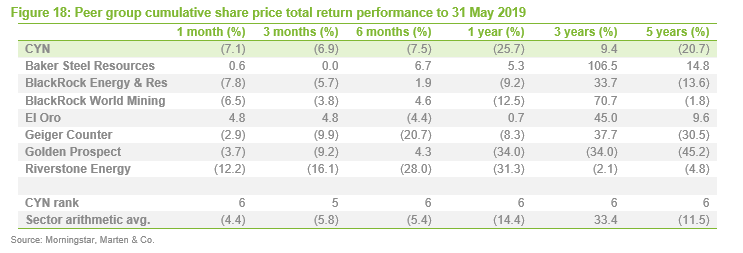

Figure 18 illustrates a similar story for share price total return as with NAV total return. It is notable that the majority of funds post very strong returns over the three-year period. This coincides with a marked recovery in the sector’s fortunes. BSRT’s performance over the three-year period stands out as meteoric but, in many respects, this appears to reflect the scale of its previous heavy decline.

CYN is the fourth-largest fund in the sector but, reflecting the significant scale of both BlackRock World Mining and Riverstone Energy, CYN’s market cap is markedly below the peer group average. CYN’s objectives include a focus on income and CYN offers the highest yield in the peer group; half of the funds do not offer a yield and this includes the largest fund, Riverstone Energy. In some respects, this is not surprising. As discussed on page 19, commodities and resources have not traditionally been high-yielding areas and, whilst this has been improving, it is the large cap stocks (generally the big producers) that are the best dividend payers. In this regard, it should be easier for the BlackRock Trusts, with their large cap focus, to provide a dividend.

The volatility of CYN’s NAV returns is below the peer group average (CYN has the third lowest behind Baker Steel Resources and Riverstone Energy), perhaps reflecting the fact that it has a more diversified portfolio than some of the funds in the peer group that have a very specific focus. It is notable that both of the BlackRock Funds, despite their large cap focus, have higher volatilities than CYN.

CYN’s ranks third in terms of its ongoing charges ratio, which is markedly below the peer group average and also below that of its closest peer, BSRT. CYN does not pay a performance fee. BSRT has not paid a performance fee recently but its management arrangements include the provision of one that could potentially become payable in future years. A number of the funds within the sector are quite small and have higher ongoing charges ratios as a result (i.e. they have a smaller asset base over which to spread their fixed costs), which serves to elevate the sector average. In this regard, CYN benefits from its additional scale. However, if CYN realises its ambition to grow, this should serve, all things being equal, to lower CYN’s ongoing charges ratio.

Perhaps reflecting its attractive yield and below average ongoing charges ratio, CYN’s discount is below the peer group average, if you exclude Geiger Counter, which is somewhat of an exception in benefitting from a marked improvement in the outlook for the uranium market. CYN’s ongoing charges ratio is also markedly below that of BSRT. Gearing is another consideration, and maybe more of a concern for investors when markets are at more elevated levels and the end of the cycle is approaching. CYN’s gearing levels are below the sector average although, in reality, the sector comprises a number of moderately geared funds and a number of funds that are ungeared.

Quarterly dividend payments

Subject to market conditions, the company’s performance, its financial position and financial outlook, the board intends to pay an attractive level of dividend income to shareholders on a quarterly basis. The company intends to pay all dividends as interim dividends. As discussed below, CYN will pay dividends out of capital when required.

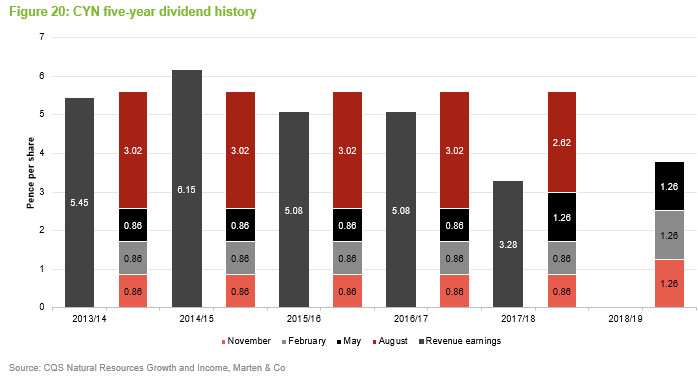

For a given financial year, the first interim dividend is paid in November (2018: 1.26p) with the second, third and fourth interims paid in February, May and August. As illustrated in Figure 20 overleaf, the total dividend paid for each of the last five financial years has been 5.6p per share. The target announced for the year ending 30 June 2019 has also been set at 5.6p per share. This is a yield of 6.6% on CYN’s share price of 85.3p as at 7 June 2019. As illustrated in Figure 19, CYN has historically paid three smaller interims with a significantly larger fourth interim. However, it is seeking to rebalance the dividend payments so that they are more equal in nature. To this end, the first three interims have been declared at 1.26p per share and CYN has said that it intends to pay the fourth interim for the current financial year at 1.82p per share (5.6p per share in total).

Permitted to pay dividends out of capital

As Figure 20 shows, CYN’s revenue income has also been less than its revenue earnings in four out of the last five years, meaning that the trust has dipped into its revenue reserves to maintain the dividend at the 5.6p per share level. Perhaps this should be expected. CYN’s investment objective includes both income and capital growth elements. Commodities and resources have not traditionally been high-yielding areas and, whilst this has been improving, the yield on CYN’s portfolio is likely to change as the manager adjusts its composition to best take advantage of the available opportunities. It seems reasonable that, in some years, investors should expect a shortfall, while in other years there may be an excess.

Following shareholder approval at CYN’s AGM in 2012, the trust is permitted to pay dividends out of capital and in March 2018 the board announced its intention to use CYN’s capital reserves, when required, to maintain or potentially increase the dividend level. This change has allowed the manager to focus on the total return from investments rather than needing to have an allocation to higher yielding investments, with a view to providing the necessary income to meet the dividend.

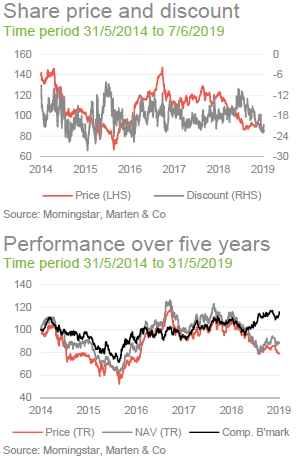

Premium/(discount)

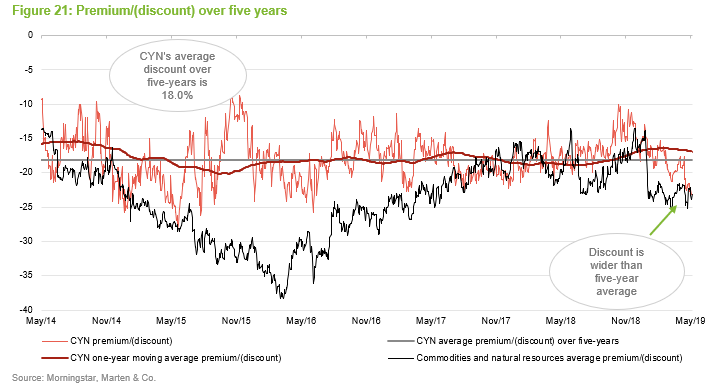

As illustrated in Figure 21, CYN’s discount has traded in a range of 8.1% to 28.3% during the last five years. However, the trend has been one of reduced discount volatility during the last three years and, as also illustrated in Figure 21, CYN did not suffer from the significant widening that occurred across the sector during the latter stages of the last commodities bear market. During the last 12 months, CYN has traded at discounts between 10.0% and 23.1%, and an average of 16.9%. As at 7 June 2019, the discount was 21.1%, which is above its longer-term five-year average and in the upper half of its one-year trading range. The sector’s five-year average discount is 23.8% so, with a five-year average discount of 18.0%, CYN tends to trade at a premium to the broader sector. This perhaps reflects the comfort offered by CYN’s peer group topping yield, which is significantly above the sector average.

Arguably reflecting the more cyclical nature of resource companies, CYN’s discount has exhibited a degree of cyclicality whereby it has tended to narrow when markets rally, and investors are seeking more cyclical exposures, and widen when markets soften, and investors’ appetite for more defensive exposures has increased. CYN’s mid-cap bias may amplify these movements. For example, when markets become more risk-on, large caps tend to rally first, with small and mid-caps experiencing a stronger rally later. Similarly, when markets become nervous, the small and mid-caps tend to suffer first as these are generally perceived to be higher risk, particularly if they are not operating and have cash flows to support their development programmes.

CYN is authorised to repurchase up to 14.99% and allot up to 9.99% of its issued share capital, which gives the board a mechanism with which it can influence CYN’s discount. Any repurchases or allotments must be NAV-accretive for remaining shareholders as well as being in the interests of shareholders as a whole. However, the board says that it has no current intention of using this authority and, to date, CYN has not repurchased any of its shares. The board considers that share repurchases would likely have a limiting ability to provide any sustained change in the discount and, reflecting this, there is no formal discount control mechanism or discount target.

Given CYN’s current size, share repurchases might have a limited impact on the discount as they would also serve to reduce liquidity and put upward pressure on CYN’s ongoing charges ratio (its fixed costs being spread over a smaller asset base). Instead, CYN might be better served by increasing its size. The board and manager hold this view and are focused on increasing awareness of the trust among investors.

Fees and costs

Tiered base management fee; no performance fee

Under the terms of the investment management agreement, CQS is entitled to receive a basic management fee of 1.2% per annum of total net assets up to £150m, 1.1% of total net assets above £150m and up to £200m, 1.0% of total net assets above £200m and up to £250m and 0.9% of total net assets above £250m. This arrangement was introduced from 3 April 2018. Prior to this, CYN paid a flat fee of 1.2% of total net assets.

The management fee is calculated and paid monthly in arrears and there is no performance fee element. The management agreement can be terminated on 12 months’ notice by either side.

Secretarial and administrative services

Company secretarial and administrative services are provided by Maitland Administration Services (Scotland) Limited (formerly R&H Fund Services Limited). Maitland’s total fees for the year ended 30 June 2018 were £93,000 (2017: £91,000).

Allocation of fees and costs

In CYN’s accounts, the investment management fees are allocated 25% to capital and 75% to revenue. All other expenses are charged wholly to revenue with the exception of costs incurred in relation to the disposal of investments, which are charged wholly to capital. The ongoing charges ratio for the year ended 30 June 2018 was 1.8% (2017: 1.8%).

Capital structure and life

CYN has a simple capital structure with one class of ordinary share in issue. Its ordinary shares have a premium main market listing on the London Stock Exchange and, as at 7 June 2019, there were 66,888,509 in issue with none held in treasury.

3.5% convertible unsecured loan stock repaid 30 September 2018

CYN is permitted to borrow and on 26 September 2011 the trust issued £40m of 3.5% convertible unsecured loan stock (CULS), which had a final conversion date of 28 September 2018. Following the final conversion opportunity, £34.5m nominal (face value) of the CULS remained outstanding and these were repaid using a combination of cash, asset sales and a new £20m unsecured revolving credit facility (a bank overdraft facility), with Scotia Bank (see below). As such, CYN no longer has any structural borrowings and its board says that it currently has no immediate plans to reintroduce structural gearing.

New unsecured revolving credit facility

From 20 September 2018, CYN has had a £20m unsecured revolving credit facility (RCF) with Scotia Bank. The RCF has a two-year term and pays interest at a rate of 1.05% per annum above the base rate. CYN’s board has set a borrowing limit of 25% of net assets for ordinary market conditions. As at 31 March 2019, CYN had gross gearing of 14.6% and net gearing of 13.6%.

Unlimited life with an annual continuation vote

CYN does not have a fixed winding-up date but at each annual general meeting (AGM), shareholders are given the opportunity to vote on the continuation of the company as an investment trust. This is a special resolution. If this resolution was not passed, the board would put forward proposals to liquidate or otherwise reconstruct or reorganise the company.

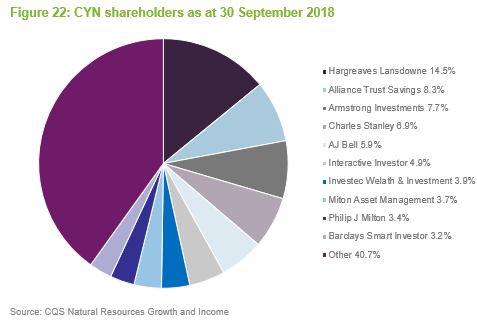

Major shareholders

Financial calendar

The trust’s year-end is 30 June. The annual results are usually released in September/October (interims in March) and its AGMs are usually held in November/December of each year. As discussed on page 18, CYN pays quarterly dividends in November, February, May and August.

Corporate history

CYN was originally established in November 1994 as a Latin American-focused investment trust, but in June 2003, shareholders approved a change of mandate with a completely new focus on natural resources. CYN’s shares have a premium main market listing on the London Stock Exchange. As noted on page 3, on 4 December 2018 shareholders approved a resolution to change the company’s name to CQS Natural Resources Growth and Income Plc (previously City Natural Resources High Yield Trust Plc).

Management team

CYN is co-managed by Ian Francis, Keith Watson and Rob Crayfourd. Keith and Rob focus on the equity side of the portfolio, while Ian primarily focuses on the fixed income securities. Keith and Rob also manage Geiger Counter Limited (also a client of Marten & Co – click here to read QuotedData’s initiation note) and Golden Prospect Precious Metals Limited.

Ian “Franco” Francis

Ian Francis is a partner at CQS and Head of New City. He also managers the CQS New City High Yield Fund, which, like CYN, is a client of Marten & Co (click here to read QuotedData’s most recent research note). Ian joined NCIM in 2007 and has over 35 years’ investment experience, primarily in the fixed interest and convertible spheres, having worked for Collins Stewart, WestLB Panmure, James Capel and Hoare Govett. Ian is able to draw on the expertise of a 16-strong credit analysis team at CQS.

Keith Watson

Keith Watson joined the NCIM team in 2013, initially as a dedicated natural resources analyst focused on supporting CYN’s managers.

Prior to NCIM, Keith worked for Mirabaud Securities, where he was a senior natural resource analyst; Evolution Securities, where he was director of mining research; Dresdner Kleinwort Wasserstein, where he was a top-ranked business services analyst; Commerzbank; and Credit Suisse/BZW. Keith began his career in 1992 as a portfolio manager and research analyst at Scottish Amicable Investment Managers. He has a BSc (Hons) in Applied Physics from Durham University.

Robert (Rob) Crayfourd

Rob Crayfourd joined the NCIM team in 2011. He has over 13 years’ financial experience, having previously worked for the Universities Super Annuation Scheme and HSBC Global Asset Management, where he focused on the resources sector. Rob holds a BSc in Geological Sciences from the University of Leeds and is a CFA holder.

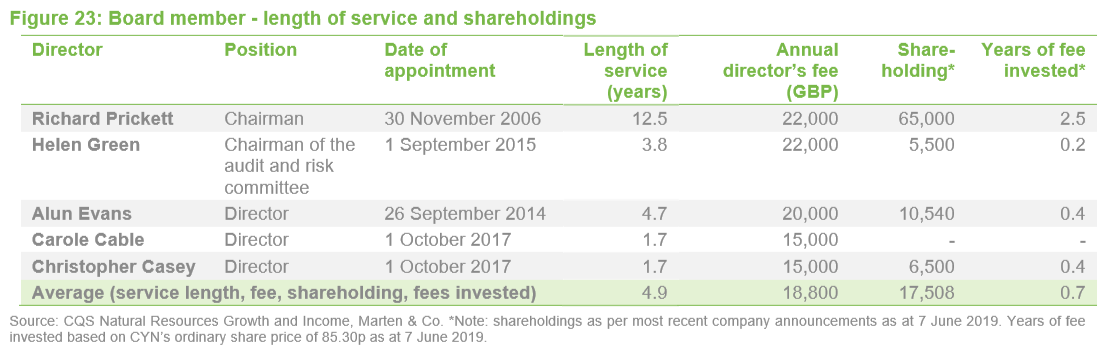

Board

CYN’s board is comprised of five directors, all of whom are non-executive and considered to be independent of the investment manager. The company’s articles of association limit the aggregate fees payable to the directors to a total of £125,000 per annum.

CYN’s articles of association require that board members offer themselves for re-election at least once every three years. Board members that have served for nine or more years must offer themselves for re-election annually. However, board policy is that all members offer themselves for re-election annually. All existing board members were re-elected at the AGM on 4 December 2018.

Of CYN’s board members, the only director to have served more than nine years is the chairman, Richard Prickett, who has been a board member since November 2006. In addition to CYN’s board, Richard Prickett and Helen Green also sit on the board of Landore Resources Limited. However, other than this, CYN’s directors do not have any other shared directorships.

Richard Prickett (chairman)

Richard Prickett is a chartered accountant with considerable experience in the mineral sector and in corporate finance. He is a director of Landore Resources Limited (an AIM listed mineral exploration company of which he was previously CEO and finance director). He was formerly chairman of both Brancote Holdings (until its merger with Meridian Gold in 2002) and Asian Growth Properties Limited. Richard is a non-executive director of The City Pub Group Plc and of privately-owned Lamaune Iron Inc (a mining exploration and development company focused on the Lamaune iron ore and gold property, located in northern Ontario, Canada). Although Richard has been a director for 12 years, his tenure as chairman is considerably shorter (14 months), having been appointed to succeed Geoffrey Burns, who stepped down in March 2018.

Helen Green (chairman of the audit and risk committee)

Helen Green is a chartered accountant with considerable experience of investment funds and, in particular, of fund administration and governance. She is a director of Saffery Champness (one of the UK’s Top 20 accountancy practices), in Guernsey. She joined Saffery Champness in London in 1984, relocating to Guernsey in 2000. Helen is a director of Acorn Income Fund Limited and Landore Resources Limited. She was formerly a director of Advance Frontier Markets Fund Ltd, Henderson Diversified Income Fund Ltd and John Laing Infrastructure Fund Ltd.

Alun Evans (director)

Alun has over 40 years’ experience working in the investment management industry. He began his career at Capel-Cure Myers, moving to Carr Sheppards Crosthwaite in 1990, where he became an executive director in 1998. He joined Cheviot in 2009 as Business Development Director, from which he retired in August 2017.

Carole Cable (director)

Carole has had a 25-year career connected to the mining and commodities sector, initially on the sell side at JP Morgan and Credit Suisse, and latterly as a non-executive director both of Nyrstar NV (a global mining and multi metals business) and Women in Mining UK. Carole is currently a partner and co-head of the Energy and Resources division at Brunswick Group LLP, where she advises clients in the mining sector.

Christopher Casey (director)

Christopher is a chartered accountant and was formerly a partner at KPMG until 2010. Since leaving KPMG, he has carried out a number of non-executive board roles, including chairman of China Polymetallic Mining Ltd. He is currently a director of Eddie Stobart Logistics Plc, TR European Growth Trust Plc, Black Rock North American Income Trust Plc and Mobius Investment Trust Plc.

The legal bit

This marketing communication has been prepared for CQS Natural Resources Growth and Income Plc by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and, if you are not a professional investor, or in any other way are prohibited or restricted from receiving this information, you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.