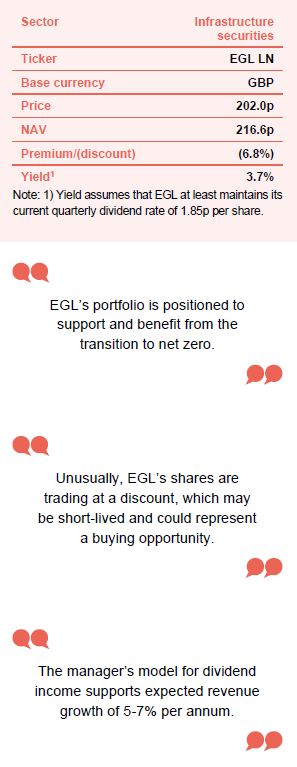

Ecofin Global Utilities and Infrastructure Trust

Investment companies | Update | 22 November 2022

A portfolio for all seasons

Even considering the particularly challenging markets we have seen during the last couple of months, Ecofin Global Utilities and Infrastructure Trust (EGL) has posted a very respectable performance (see page 18) and has been issuing shares. This most likely reflects the long-term strong structural growth drivers, inflation linkages and the defensive (less economically sensitive) nature of its investments, in an environment where the global economy is slowing down and tipping into recession.

There is little doubt that current uncertainty has been unhelpful, but as COP27 illustrates, the challenges of moving to net zero carbon emissions have not gone away and EGL’s portfolio is positioned to support and benefit from this energy transition. Its portfolio has shown resilience, which we explore in this note, and unusually, its shares are trading at a discount to net asset value (NAV). We think that this may be short-lived and could represent a buying opportunity.

Developed markets utilities and other economic infrastructure exposure

EGL seeks to provide a high, secure dividend yield and to realise long‐term growth, while taking care to preserve shareholders’ capital. It invests principally in the equity of utility and infrastructure companies which are listed on recognised stock exchanges in Europe, North America and other developed OECD countries. It targets a dividend yield of 4% per annum on its net assets, paid quarterly, and can use gearing and distributable reserves to achieve this.

Market outlook and valuations update

EGL’s NAV total return from since inception to 31 October 2022 was 11.2% per annum.

As we explore in greater detail in the performance section on page 18, EGL has generated substantial outperformance of both the MSCI World Utilities Index and the S&P Global Infrastructure Index over the last six years. As we discuss in the manager’s view section, 2022 year-to-date (YTD) has been a very challenging year in financial markets globally and, reflecting their defensive characteristics and considerable inflation protection, these two listed infrastructure indices have markedly outperformed global equities as a whole (as represented by the MSCI World Index) and UK equities (as represented by the MSCI UK Index). In this environment, investors will welcome EGL’s positive NAV return (6.9% for the 12 months to 31 October 2022), albeit that it has lagged the two US dollar-heavy comparator indices over this period. From inception to 31 October, EGL has provided an annualised NAV total return of 11.2% per annum, which is the same as that provided by the broader MSCI World Index (all figures in sterling terms).

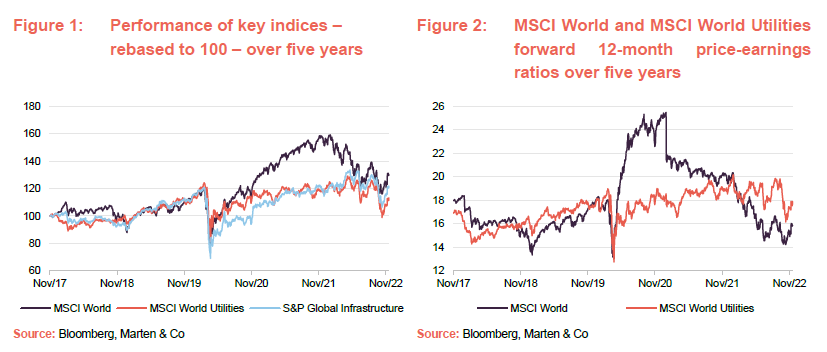

Figures 1 and 2 offer a useful illustration as to why investors may wish to consider having an allocation to EGL’s sectors: utilities (power, water and environmental services) and other economic infrastructure (transportation services), particularly with the current market backdrop of rising interest rates, inflation and risk of recession.

As illustrated in Figure 2, as financial markets collapsed in 2020, global utilities’ earnings were resilient, and their valuation multiples remained stable relative to history. The same could not be said for global equities more broadly, which rebounded very strongly in response to the considerable stimulus injected by governments and central banks (the forward 12-month price-earnings (P/E) ratio for the MSCI World rocketed). Whilst a recovery in earnings saw these companies partly grow back into their valuations, global equities continued to look expensive relative to their pre-pandemic levels, until rising inflation and the prospect of rising interest rates took the steam out of global equity markets (particularly growth stocks, which have suffered as investors rotated back into value).

The invasion of Ukraine drove up the prices of various commodities and energy, which had already been rising as the global economy recovered from the effects of COVID. This exacerbated the previous trends of rising inflation and interest rates, but with a much-increased risk of recession, which continues to weigh on global equity valuations that now look cheap versus utilities as a whole. The MSCI Utilities Index is also cheaper than it was, but its valuation has been more stable reflecting the more-defensive nature of its earnings.

Manger’s view

We live in interesting times!

Aided by good stock selection, EGL’s portfolio has been resilient.

EGL’s investment sectors had a challenging start to 2022, particularly in Europe, but EGL’s portfolio – aided by good stock selection, with a number of positions that benefitted from strong tailwinds – proved to be more resilient than the average. Markets have been very volatile and many sector and stock price moves have been top-down driven. Whilst the manager usually looks to take advantage of the opportunities that volatility throws up, Jean-Hugues has focused on the longer term and tried to keep portfolio turnover low in this year’s difficult markets.

Macro driven markets

Markets have been very driven by the macroeconomic situation recently, particularly during the last 12 months with the war in Ukraine and as inflation has increased significantly. Inflationary pressures, initially in response to the massive fiscal and monetary stimulus injected by governments and monetary authorities to prop up economies during the pandemic, have ballooned since Russia’s invasion of Ukraine, with the resultant impact on commodity and particularly energy prices from the ensuing supply curtailments and sanctions.

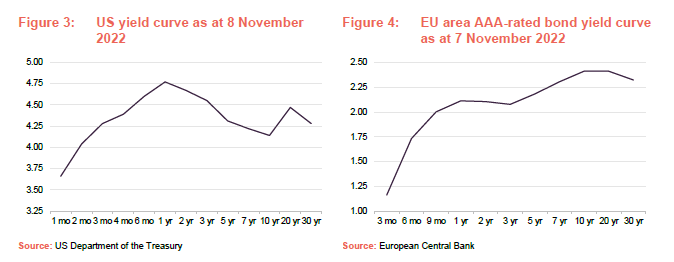

The US is ahead of the curve

The US has moved quickest this year to get to grips with the strikingly high inflation levels – the Federal Reserve (the US central bank) has raised short-term rates aggressively, the US dollar has been very strong, and the yield curve has flattened. (Note: a yield curve is a line that plots yields – interest rates – of bonds having equal credit quality but differing maturity dates. An inverted yield curve (short rates higher than long rates) is often a sign of an impending recession. The gap between short-term and long-term interest rates has narrowed – as is shown in Figure 3). A portion of the curve has even inverted. Historically, this flattening of yield curves has been supportive of US regulated utilities and this time has been no exception (with an increasing chance of recession, investors shift towards more defensive sectors).

In Europe, the situations has been more complicated

A steepening yield curve has been a headwind for equities in general. Utilities have also been weighed down by the uncertainty around energy policies with outstandingly high prices facing consumers.

While inflation and interest rates have also been marching upwards in Europe, the picture has been more complicated (Europe energy markets have felt the impact of the invasion of Ukraine more severely) and so European utilities have underperformed their global peers. Jean-Hugues comments that European utilities have been the clear under-performers amongst global peers this year, especially when measured in sterling terms. Inflation and interest rates have marched higher in Europe too, the war in Ukraine has presented great economic and geopolitical uncertainty, and there was a steepening of yield curves in the first half of the year, arguably reflecting concern that European inflation would be higher for longer. Yield curves have begun to flatten again, reducing this headwind for utilities.

European utilities are not a pack

Europe has been quicker to embrace the move to renewables than the US.

Whilst there have been some big macro factors weighing on the sector this year, Jean-Hugues observes that European utilities are not a pack. He comments that there are big differences in their business models and that stock picking is key to avoiding the big mistakes. Europe has, on average, been quicker to embrace the move to renewables than the US (this is not to say that progress has not been made in the US, despite the policies of its former president Trump) and Jean-Hugues says the proportion of utilities’ shares which are correlated with interest rates and yield curves (that is, which behave as bond proxies) has diminished due to significant changes in their business mixes over the last several years.

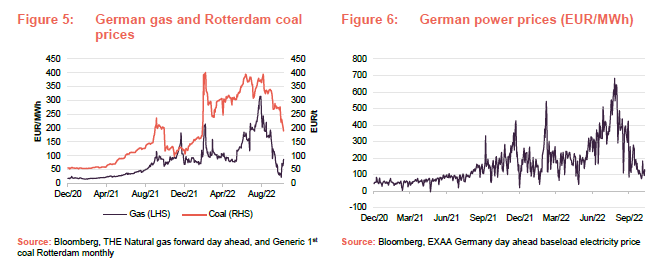

In Europe, in particular, dramatic commodity price increases have filtered through to power prices. Gas peaking plants tend to set the marginal price of electricity (although there has been much talk of decoupling the two), while coal prices have ballooned too, so traditional thermal generators (those that rely on fossil fuels) have found themselves at the sharp end of rising costs. However, this dynamic really benefits the renewables generators as the power price received rises, yet they have incurred little or no additional cost of production (the initial outlay for modules, turbines and inverters may have increased but the price of wind and sunshine is still zero).

Power prices have eased recently but remain at a significantly elevated level.

To give some sense of scale, at the beginning of 2021 the electricity price in Europe was €30-€60 per MWh; today it is closer to €130 per MWh, but has been as high as €683/MWh. Power prices have been falling recently as gas prices have edged down on good weather and full storage facilities, but nonetheless remain at a significantly elevated level, which can be a big positive or negative dependant on each company’s business model, and the extent to which power generated has been sold forward and pricing terms for procurements fixed. Reflecting this, there has been considerable discrepancy in performance between the European majors.

Large retail power suppliers are severely squeezed

Many retail-facing power companies are generally price takers in the wholesale electricity market.

As noted above, current high energy prices are a big positive for power generators that have fixed fuel costs (such as the renewable generators). These have experienced significantly higher earnings during the last three quarters (although some power is sold forward on power purchase agreements (PPAs) so they do not necessarily experience the full benefit of the higher pricing straightaway). However, higher prices are a big negative for many retail-facing power companies that are generally price takers (a supplier that does not have sufficient scale within a market to influence its price) in the wholesale electricity market. These operators are being heavily squeezed as they often do not control the production – they buy in the power – and it is impossible to pass on the increase to the final consumer to the extent that would be required to generate a profit.

Jean-Hugues considers that RWE and Drax (both EGL holdings) have been amongst the strongest beneficiaries of the current situation (because both have refocused their businesses on clean energy sources). At the other end of the spectrum, the share prices of E.ON and Enel, which are amongst the biggest retail power providers in Europe, have both suffered heavily (EGL also holds both but they are relatively small positions).

Larger operators are more likely to have the necessary balance sheets to weather the current storm.

The most obvious casualties have been Uniper and its parent Fortum, both of which have direct exposure to Russia. The German government has provided a €15bn bail-out package to Uniper in exchange for a 30% equity stake in the company, while Fortum took a €2.35bn loan from the Finnish government in September, which was primarily to cover its collateral needs in the Nordic power derivatives market.

Many smaller retail power companies need to buy power in the forward market (in the forward market a good or commodity, in this case electricity, is purchased at a price agreed today for delivery at some point in the future) and Jean-Hugues thinks that margin calls on contracts could lead to the collapse of some small players if they have insufficient balance sheet support (EGL does not hold these). In contrast, the larger operators are more likely to have the necessary balance sheets to be able to work their way through the problem.

Political interference

Political interference has been the number-one risk for utilities in 2022. Jean-Hugues says that there isn’t a country in Europe that hasn’t given some consideration to implementing measures to bring down power prices for the end consumer, which have ballooned since the invasion of Ukraine.

The UK government is now introducing a windfall tax (electricity generator levy).

The situation is sufficiently bad that even the UK government, which has traditionally been pre-disposed to allow market forces to take their course, has implemented measures to protect consumers with its Energy Bills Support Scheme. As announced in the government’s autumn statement on 17 November 2022, it plans to recoup some of the cost of its consumer support package with the introduction of its Electricity Generator Levy. This is a temporary 45% tax “on extraordinary returns from low-carbon UK electricity generation”, which will apply from 1 January 2023 to 31 March 2028.

For the purposes of the tax, the government is defining extraordinary returns as the aggregate revenue that generators make in a period at an average output price above a pre-crisis price baseline of £75 per MWh. The levy applies to generators using renewable, nuclear and biomass, although it specifically excludes generation that falls under the contracts for difference (CfD) regime.

The government is designing its legislation with a specific aim to exclude small generators from falling foul of the levy. To achieve this, the levy will only apply to generators whose output exceeds 100GWh across a period and will only then apply to extraordinary returns exceeding £10m. Regrettably, this may create an incentive for operators close to the threshold to curtail the expansion of their generation portfolio and equally for those that are just above it to perhaps sell off some assets, arguably at the expense of economies of scale in the process. We would also like to have seen an incentive for generators to reinvest the windfall in sorely need generation capacity, but this is absent.

Jean-Hugues comments that the baseline price of £75 per MWh, above which generators are subject to the levy, is set at quite a comfortable level. He thinks that while there could have been better incentives for reinvestment, the levy isn’t unduly damaging for generators. In the EU, the emergency intervention to address high energy bills is a straightforward cap on revenues for electricity producers using technologies with lower costs (such as renewables, nuclear, etc) of €180/MWh, which provides a large buffer, but each member country retains the flexibility to specify a lower price cap.

Nationalism – recent transactions do not a set a trend

At a cost of just €10bn, previously debt-laden nuclear power group EDF has been nationalised by the French government. We referred to the Uniper bailout above, this diluted majority shareholder Fortum’s stake to around 56%, from around 80%. With power companies under increasing pressure, this raises the question of whether we could see more nationalisations in Europe. Jean-Hugues thinks that this is unlikely, due to the large sums involved. It would be expensive to buy out the large utilities, and governments – having significantly expanded their deficits to prop up their economies during COVID – do not have the budgets to support these kinds of nationalisation programs.

Nationalisation – a natural conclusion to the EDF saga.

Jean-Hugues thinks that EDF in France was the exception. Reflecting its debt burden, the share price had fallen to around €7 per share and the government’s bid of €12 per share, whilst a marked discount to its intrinsic value, was a hefty premium to the prevailing share price prior to the bid. He says that all parties were broadly happy with the deal and that it was a natural conclusion to the saga.

The EU emergency energy plan is effectively a denial of market mechanisms.

Jean-Hugues comments that the EU emergency energy plan is effectively a denial of market mechanisms. There is talk of decoupling the cost of power generated by renewable sources from natural gas prices in favour of long-term PPAs on a regulated asset base (RAB)-type model that would enable them to earn a reasonable return on their investment with visibility on the prices they receive.

Shifting to a CfD model would provide predictable, long-term, inflation-linked income.

Another approach that has been mooted in the UK is to shift to something akin to the CfD model used in recent renewable power subsidy auctions. This would provide predictable, long-term, inflation-linked income, which could be attractive to the sector.

Large renewable generators have surprised on the upside

Positive surprises on large renewable generators’ earnings. The trend has been one of improving earnings guidance quarter on quarter.

Jean-Hugues says that the Ecofin team has been very positively surprised with the earnings performance of the large renewable generators this year. The market had reservations about these companies’ long-term PPAs in a higher-inflation environment. These concerns led to considerable underperformance of many of the big renewable generators earlier this year. However, these companies’ contracts have proved to be more flexible than many envisaged (while cost bases are mostly fixed) so existing portfolios of PPAs are more profitable than last year plus there is growth as new PPAs are being written. The trend has been one of improving earnings guidance quarter on quarter, and while governments may find ways to increase their tax take at the margin, the states really need these companies and so cannot penalise them excessively, particularly as they need to encourage further development.

Nuclear

In an environment of heightened concerns over energy security, nuclear generation is becoming central to the discussion of energy provision. In France, nuclear accounts for 80% of generation, and in the UK there is now a big focus on rebuilding our nuclear capacity so that it can sit alongside our growing renewables provision.

Nuclear offers a carbon-free source of baseload power.

Jean-Hugues says that even in countries where nuclear was out of the picture altogether, or where there was no investment in new generation, the debate is returning in light of what nuclear offers to the generation mix. Specifically, it is a carbon-free source of power; it is solid baseload capacity (renewables are inherently intermittent and therefore not suited to baseload); pricing is very predictable (there is a high fixed cost to developing plants, but once these are in place the uranium is a relatively small part of the overall cost); and it offers countries a route to greater geopolitical independence (Charles de Gaulle’s nuclear build out was driven by a desire to achieve independence in energy supply and, in contrast, Germany’s focus on intermittent renewables, coupled with cheap Russian gas, now looks ill-thought-out).

Jean-Hugues comments that whilst there was a big anti-nuclear movement in Germany, public opinion is turning around. The German government has effectively re-opened the debate by extending the lives of Germany’s two remaining nuclear power plants at least until April 2023, thereby pausing the final stage of the nuclear phase-out for domestic energy production that had begun under Angela Merkel’s rule.

Biden’s inflation reduction act provides significant support to nuclear power companies.

In the US, the Biden administration has put in place a number of measures to help nuclear power companies that, in the face of rising costs, have been struggling to compete against renewable generators and plants that have been fired by cheap gas. The most recent is the Inflation Reduction Act (IRA), which was signed into law in August with US$369bn earmarked for energy security and climate change. This allocates tens of billions of US dollars for the US nuclear fleet, including investment and tax incentives for both large, existing nuclear plants and newer, advanced reactors, as well as Haleu (high-dosage low-enriched uranium) projects.

Jean-Hugues highlights that many companies with nuclear assets have these valued at close to zero in some-of-the-parts (SOTP) valuations, but these are of increasing and strategic value. Reflecting this, Public Service Enterprise Group is considering keeping, rather than selling, its nuclear assets and Constellation Energy, a pure-play nuclear specialist spun out from Exelon, has been one of the portfolio’s best performers this year.

Mergers and Acquisitions

Regular readers of our research on EGL may remember that Ecofin published a white paper in 2020 that highlighted the marked disparity between the values at which infrastructure assets have been changing hands in private markets, versus the values being ascribed to them in listed markets. The broad conclusion of the paper was that the situation was unsustainable and would likely lead to mergers and acquisitions (M&A) in the infrastructure space, with listed infrastructure assets being taken private.

This appears to be coming to pass, with a number of major Australian infrastructure names being taken out by private equity in the last year. These include Spark Infrastructure, the Australian power grid operator, which was taken out by a consortium led by KKR and the Ontario Teachers’ pension fund; and Sydney Airport, which was led by IFM Investors and Global Infrastructure Partners. Atlas Arteria has seen private equity take a 15% stake and European infrastructure giant Atlantia (held in the portfolio) has also been taken out. Infrastructure is dominated by private assets and private equity investors. Jean Hugues thinks that the M&A trend will continue and be supportive of listed infrastructure names.

Asset allocation

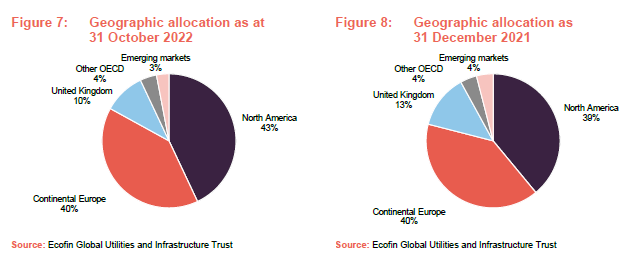

Comparing EGL’s exposures at the end of October 2022 and the end of December 2021, exposure to the US has increased by four percentage points, while the exposures to continental Europe and the UK have both fallen by two percentage points.

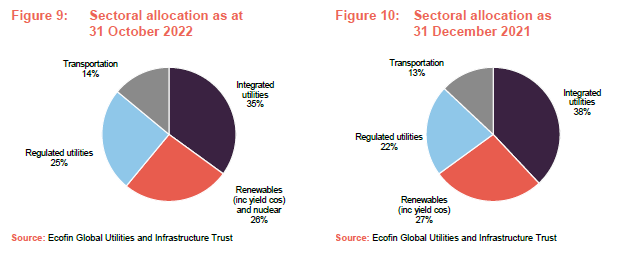

The allocation to regulated utilities has increased year-to-date, largely at the expense of integrated utilities, while the allocations to clean energy has held firm.

The number of holdings as at the end of October 2022 was 43, which is the same as at the beginning of the year.

Portfolio activity – YTD

So far this year, EGL’s manager has:

- continued to favour clean power generation;

- minimise exposure to power retailers; and

- been nimble in selling out of companies exposed to Russia following the invasion of Ukraine.

EGL’s holdings in Uniper, Pennon and PPL have all been disposed of in their entirety. Due to its Russian exposure, the entire Uniper holding was sold within 24 hours of Russian’s invasion of Ukraine. EGL did not have exposure to Fortum, or any of the Central European names so, overall, its portfolio had very limited exposure to Russia. Otherwise, the managers have used market volatility to trade around a few names, selling down holdings considered to be more fully valued to rotate the proceeds into better value opportunities. Pennon and PPL are discussed in further detail below.

EGL’s exposure to North American utilities has been broadened.

EGL’s manager has reinvested the sale proceeds, as well as the receipts from new share issuance, into a number of traditional US regulated utilities: Ameren, Xcel and Alliant Energy; all of which have performed well so far this year. Canadian yield co Brookfield Renewable Partners has been added too, all together effectively broadening the exposure to US utilities. In Europe, the manager has added Vinci and REN.

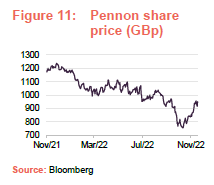

Pennon – sold on regulatory compliance concerns

Pennon (pennon-group.co.uk), which the manager describes as a best-in-class regulated water utility, was a constituent of EGL’s portfolio for some time. We last discussed it in our June 2020 annual overview note, observing that the main attraction for Jean-Hugues was Pennon’s Viridor recycling and waste management business, which was then sold to funds advised by KKR, for £4.2bn. Following the completion of that transaction, Pennon became a pure water supply business.

Historically, the strength of Pennon’s reputation and the quality of its earnings have meant that Pennon has tended to trade at a premium to its peers. However, in August 2022 Ofwat announced that it would be including South West Water in its investigation into how water and wastewater companies manage their wastewater treatment works. Pennon’s shares fell 8.9% on the day of the announcement and, while they experienced some recovery, they have fallen since as inflationary concerns have mounted (as at 18 November, Pennon was trading at 951p per share, a fall of 2.8% since Ofwat’s announcement in June). Fortunately, Jean-Hugues sold the position in April, ahead of an announcement by the water regulator.

PPL – sold following a not-so-ground-breaking transaction

As discussed in our October 2021 note (see page 10 of that note), PPL Corporation (pplweb.com) is a large, regulated utility operating in Pennsylvania and Kentucky (it is a FORTUNE 500 company and one of the largest utility companies in the US). The company was added to EGL’s portfolio in March 2021 on the manager’s expectation that the sale of its UK electricity distribution business, Western Power Distribution, to National Grid would achieve a price tag in excess of market consensus expectations. EGL’s manager felt that this should then lead to a revaluation for PPL’s shares.

Jean-Hugues says that following the completion of the transaction, he held on to the stock as it was expected that PPL would use its hefty cash pile from the sale of Western Power Distribution to make a ground-breaking purchase that would see it pivot into renewables. However, PPL instead deployed its cash pile to purchase Rhode Island Energy (previously Narragansett Electric Company), which Jean-Hugues considers to be a more traditional utility, in a transaction that completed in May 2022. Whilst Jean-Hugues believes PPL has secured a prime asset in Rhode Island that should be a positive for the company over time, he felt that the choice of asset was quite dull and he could not see any scope for a rerating in the near term, and the position was sold. Jean-Hugues says that the PPL holding was never a big position for EGL, and it was ultimately neutral to the profit and loss of the portfolio; but it was nice to own due to its optionality.

Ameren – accelerating retirement of coal-fired assets

Ameren (amereninvestors.com) describes itself as a fully rate-regulated electric and natural gas utility. The company, which serves customers in Illinois and Missouri, has electricity transmission, distribution and generation assets as well as natural gas distribution assets. The main attraction for Jean-Hugues is that Ameren is accelerating the retirement of its coal-fired energy assets and adding to its renewable generation capacity. The company has an infrastructure investment pipeline of over US$48bn+ between 2022 and 2031 and expects to see a compound annual growth rate (CAGR) in earnings per share (EPS) growth between 6% and 8% for 2022-2026. It also expects its future dividend growth to be in line with its long-term EPS growth expectations, with a pay-out ratio between 55% and 70% of annual EPS.

Xcel Energy – major focus on renewables

Xcel Energy (investors.xcelenergy.com) is an American utility holding company that has a strong focus on renewables and providing carbon-free power. Xcel provides power and natural gas to customers in the states of Colorado, Michigan, Minnesota, New Mexico, North Dakota, South Dakota, Texas and Wisconsin. In December 2018, it announced that it would deliver 100% clean, carbon-free electricity by 2050. It also said that it would achieve an 80% reduction in carbon from 2005 levels by 2035, which made Xcel the first major US utility to set itself such a strict carbon reduction goal.

In 2021, 49% of the power Xcel provided came from carbon-neutral sources: biomass, hydroelectric and nuclear plants, solar panels and wind turbines. The rest was generated by coal (25%) and natural gas (26%). Jean-Hugues says that of all of EGL’s recent US purchases, Xcel has the highest renewables exposure and, whilst it trades on a higher multiple, he believes it has the best growth prospects and is particularly well-placed to benefit from the transition to net-zero.

Alliant Energy – focused on the energy transition

Alliant Energy (alliantenergy.com) is an integrated utility providing regulated electric and natural gas services to approximately 985,000 electric and approximately 425,000 natural gas customers in the US Midwest, primarily Wisconsin and Iowa. It has a very strong focus on migrating its generation to renewable and clean sources and is planning to retire, or switch from coal to natural gas, various of its electricity generation units over the next few years.

Its renewable energy development and acquisition strategy includes 1,100 MW of solar generation with in-service dates in 2022-2023 for Interstate Power and Light (IPL), 400MW of solar generation with in-service dates in 2023-2024 for Wisconsin Power & Light (WPL) and 75MW of battery storage at IPL in 2024. December 2021 saw the completion of the fuel switch of its 212 MW Burlington Generation Station from coal to natural gas and it expects to retire four of its coal fired units by the end of 2024. Alliant is aiming to have removed all coal-fired electricity generation units from its fleet by 2040 and achieve net zero by 2050.

Jean-Hugues says that the regulatory environment is supportive of regulated growth in this part of the US (we have previously discussed how Alliant Energy has been well rewarded for burying cables, which is a relatively small change) and has a history of upgrading its targets for growing its renewables portfolio.

Vinci – high quality infrastructure name

Vinci (vinci.com) is a France-based developer and operator of transport infrastructure concessions (for example, motorways and 52 airports globally, including Gatwick) and energy infrastructure concessions (renewable energy projects) around the world (it is active in nearly 120 countries) that was added to EGL’s portfolio in April 2022 (the position was acquired at what Jean-Hugues describes as attractive levels prior to the French presidential election).

Jean-Hugues describes it as a very high-quality infrastructure operator. He says that it should be fast-growing and able to deliver good earnings growth with a bit of dividend yield (3.5%). With markets focussed on the risk of recession, performance has been muted thus far, but Jean-Hugues is expecting to see more. He says that it has a strong management team with a great acquisition track record. Traditionally, the business has not been too cyclical (it tends to buy small airports and improve their efficiency) coupled with toll roads, which Jean-Hugues believes will make it a strong diversifier within EGL’s portfolio, which should help in a recession.

REN – reinitiated a position

We last discussed REN (Redes Energeticas Nacionais – ren.pt) in our October 2021 note, where we commented that the manager exited REN (which owns the Portuguese electricity and gas grids) and reinvested the proceeds in Terna (which operates Italy’s transmission grid) as he wanted to increase exposure to regulated names that have inflation pass-throughs in their formulas (this turned out to be a very profitable trade for EGL).

Since then, the manager has reinitiated a position in REN at attractive valuations. Jean-Hugues describes it as a very steady regulated utility, with a strong focus on renewables, that has the potential to be a strong performer.

Gearing – diluted by share issuance

As at 31 October 2022, EGL had net gearing (borrowings less cash) of 10.2%. As discussed in our annual overview note, the gearing is not structural in nature and borrowings can be repaid at any time, which gives the manager considerable flexibility to deploy the gearing tactically. EGL has recently been operating with gearing around the 11–15% range, but the manager comments that this is effectively overstated by several percentage points given there have been a few names in the portfolio subject to takeovers (EDF, Atlantia), and EGL holds a SPAC (cash shell) which is yet to complete a transaction. These three positions account for 6-7% of the portfolio. In addition, cash inflows from shares issuances have also been helpful in managing gearing during recent market turbulence.

Top 10 holdings

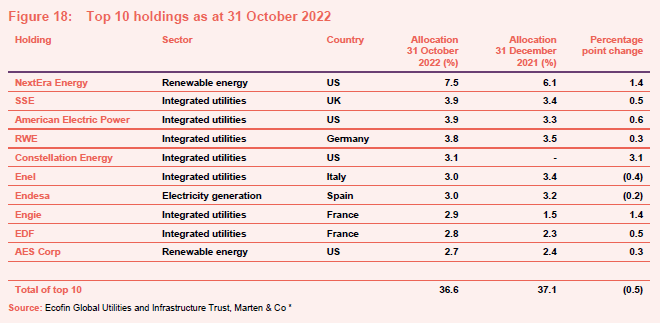

Figure 18 shows EGL’s top 10 holdings as at 31 October 2022 and how these have changed year-to-date. Names that have moved up into the top 10 are Constellation Energy, Engie, EDF and AES Corp (EDF has been propelled up the ranks due to its takeover – see page 8 of this note). Names that have moved out of the top 10 are Iberdrola, Exelon, Drax and Greencoat UK Wind.

We discuss some of the more interesting developments in the following pages. Readers interested in other names in the top 10 should see our previous notes.

American Electric Power (3.9%) – a utility in transition

We first mentioned American Electric Power (aep.com) in our October 2021 note where we commented that it was one of a number of holdings that Jean-Hugues had been reallocating into that have meaningful low-carbon ambitions (along with Alliant Energy – see above, and DTE Energy). American Electric Power, or AEP, is one of the largest power generators and distributors in the US, serving Ohio, Michigan, Indiana and other midwestern states. EGL describes it as a utility in transition – its generation fleet is transforming from majority coal- and natural gas-fired (89% in 2005) to majority renewables-sourced (hydro, wind, solar and pumped) by 2030. As at October 2022, 7,100 MW or around 23% of 31,000 MW of generating capacity, was renewables. AEP also owns a 40,000-mile network of high-voltage transmission lines spanning 38 eastern and central US states and eastern Canada – this is more transmission network miles than all of the other US transmission systems combined.

EGL’s manager considers that AEP is well positioned as a fully regulated business, as the regulatory environment is supportive of regulated growth in this part of the US. He expects dividends to grow in line with earnings growth of about 5-7% per annum, which is supported over the longer term by an investment programme that address the challenges of moving to net zero – upgrading regulated transmission infrastructure, improving grid resilience and expanding renewables.

Constellation Energy (3.1%) – benefitting from rising power prices and a renewed interest in nuclear

Constellation Energy (constellation.com) was spun out of Exelon in January 2022 as a vehicle for Exelon’s generation assets. Constellation Energy describes itself as the US’s largest producer of carbon-free energy and the leading competitive retail supplier of power and energy products and services for homes and businesses across the United States. In addition to its renewables portfolio, which should benefit from a climate of rising power prices, the company has the US’s largest nuclear fleet, which should benefit heavily from the IRA (discussed on page 10). Jean-Hugues describes the package as game-changing for nuclear in the US.

Endesa (3.0%) – targeting carbon neutrality by 2040

Endesa (endesa.com) is Spain’s largest power generator and the second-largest operator in the Portuguese electricity market after REN. The company, which is a subsidiary of Italy’s Enel, has a diversified portfolio of energy sources (nuclear, thermal, hydroelectric and renewables). Endesa is focused on growing its installed capacity in clean power sources (hydro, solar and wind), while progressively phasing out its coal-fired capacity. Jean-Hugues says that Endesa has been increasing its investments in new renewable capacity to both accelerate decarbonisation and to promote the digitalisation of the grid to improve service quality. Whilst it was previously aiming for net-zero by 2050, Endesa has pulled this forward to 2040 and intends to discontinue coal generation by 2027 and exit gas-fired electricity production by 2040.

Engie (2.9%) – benefitting from higher energy prices

Engie (engie.com), formerly GDF Suez, is a French multinational utility company that has three core businesses: power (electricity generation and distribution), gas, and energy services. Its electricity business has both thermal and renewable power-generation plants. These include solar, hydropower, offshore wind power, biomass, onshore geothermal, traditional thermal, and nuclear, and benefit from low carbon dioxide emissions. Its gas business is the largest in Europe and, following a surge in its first half profits on the back of higher energy prices, it said that the company was well prepared for a reduction in deliveries of Russian gas. We have previously discussed how Engie fits nicely with EGL’s focus on clean energy and decarbonisation. The company has invested over €800m in recent years in developing its green gas business (it aims to have at least 10% of its gas derived from green sources by 2030) and remains well-positioned to take advantage of the move to a low carbon economy.

AES Corp (2.7%) – American power generator with a high level of protected revenues

AES Corp (aes.com) is an American utility and power generation company that describes itself as a global energy company that creates greener, smarter and innovative energy solutions. It was added to EGL’s portfolio last year with its manager being attracted by its strong emphasis on renewables, a high level of revenues being protected by indexation or hedging (over 80%) and a strong development pipeline. AES has recently benefitted from the initial public offering (IPO) of Fluence (fluenceenergy.com), its joint venture with Siemens, which is focused on energy storage solutions. The stock achieved a valuation in excess of US$1bn, making it a unicorn.

Performance

Strong long-term performance record

Up-to-date information on EGL is available on the QuotedData website.

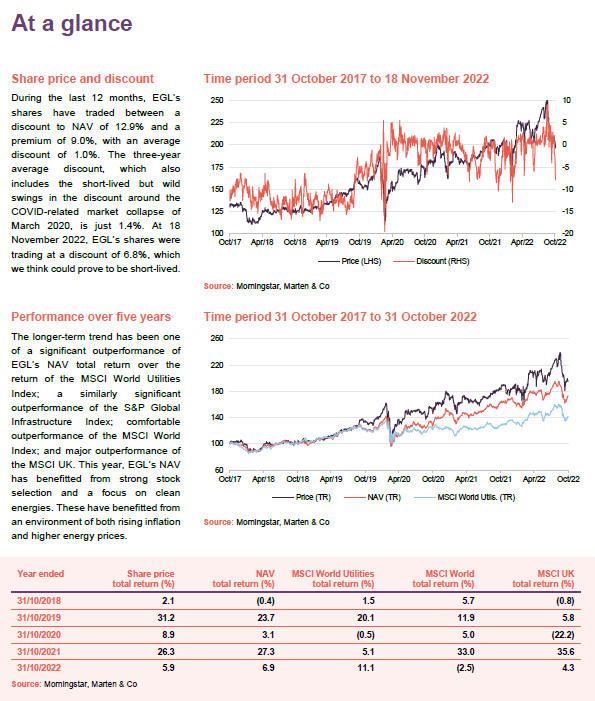

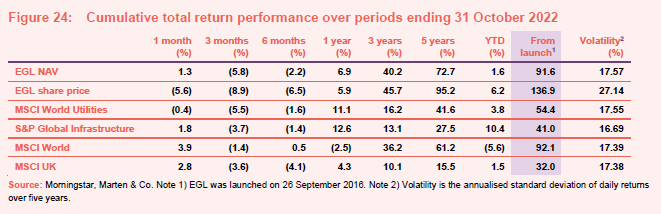

As illustrated in Figure 24, the longer-term trend has been one of a significant outperformance of EGL’s NAV total return over the return of the MSCI World Utilities Index (around two-and-a-half times the return on the over the last three -years); a similarly significant outperformance of the S&P Global Infrastructure Index (around three times the return on the index over the last three years); comfortable outperformance of the MSCI World Index (40.2% versus 36.2% over the last three years); and major outperformance of the MSCI UK (around four times the return on the index).

Reflecting the marked narrowing of the discount during the last few years (see premium/(discount section on page 22), EGL’s share price total returns are, for the longer-term periods, superior to its NAV, even surpassing the return on the broader MSCI World index by a healthy margin.

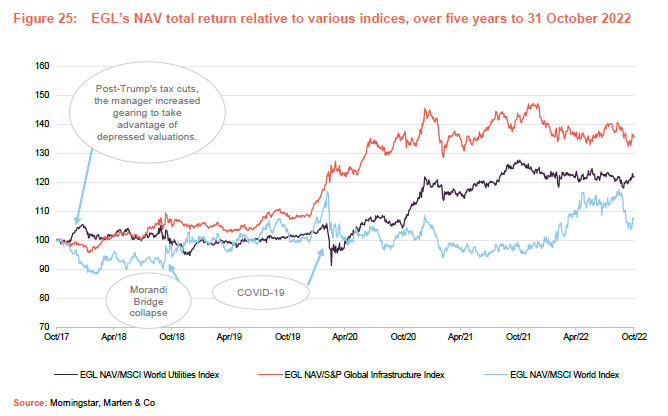

Our previous notes have discussed some of the headwinds that utilities and infrastructure have faced since EGL’s launch, which are illustrated in Figure 25. However, EGL’s NAV has benefitted from strong stock selection and a focus on clean energies, which have in turn benefitted from an environment of both rising inflation and higher energy prices. The portfolio has also benefited from M&A activity in the environmental services and infrastructure segments. While there are some near-term risks, we continue to believe that EGL’s portfolio, which is positioned to take advantage of the pivot to clean energies and the upgrade & modernisation of infrastructure generally, has a long growth runway ahead of it. With current high energy prices a key contributor to the cost of living crisis, the risk of political interference is elevated as discussed on page 8.

Year-to-date performance to 30 September 2022

EGL’s manager has kindly supplied us with some information on EGL’s main contributors to and detractors from performance year-to-date. The key positive contributors are:

- Constellation Energy (see page 17).

- American Electric Power (see page 16).

- EDF (see page 8).

- Williams Companies is a long-time EGL holding (last discussed in our October 2018 annual overview note – see page 12 of that note) that owns US gas transportation infrastructure. EGL’s manager says that the company is well positioned and considers Williams to be one of the best allocators of capital in the US gas industry.

- Acciona Energia (discussed above) has been benefitting from its significant exposure to renewables, which are benefitting from high energy prices.

- Atlantia, which has exposure to both airports and toll roads, was subject to a bid from the Benetton family and Blackstone.

The key detractors are:

- Enel, the Italian multinational producer and distributor of electricity and gas. This has been held by EGL for some time to benefit from an improving regulatory environment in Italy, reflecting the chronic need for investment. It is an example of a large retail power company that has suffered heavily this year due to its higher exposure to retail markets.

- ON, like Enel discussed above, is also a large power retailer that has been heavily squeezed by rapidly rising input costs that are difficult to pass on.

- Veolia, the French utility focused on water and waste management, has suffered this year for two main reasons. First, it is sensitive to long-term interest rates, and these have been rising (it has long-lived assets as well as contracts that range anywhere from 10 to 30 years). Second, it has a sizeable exposure to industrial customers, and increasing recessionary concerns have weighed on its share price. It was also the best performer last year (Jean-Hugues re-initiated a position late in 2020 as he considered that Veolia’s share price had decoupled from fundamentals and EGL was rewarded as it recovered).

- China Suntien Green Energy, the Chinese wind operator, was a strong performer in 2021 and has experienced some mean reversion this year as well as some negative sentiment regarding lockdowns in China.

- Uniper (discussed on page 8).

- China Longyuan Power has faced similar challenges to China Suntien.

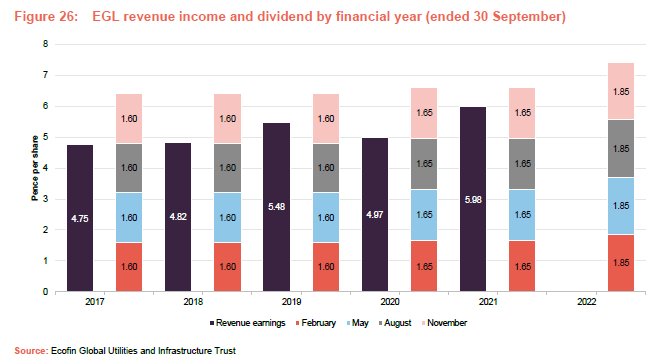

Quarterly dividend payments targeting 4% of NAV per annum

EGL can use its distributable reserves to augment its portfolio yield.

EGL targets a dividend yield of 4% on its net assets and can use gearing and, if necessary, distributable reserves to augment its portfolio yield. For a given financial year, the first interim dividend is paid in February, and the second, third and fourth interim dividends are paid in May, August and November, respectively. Dividends are paid on the last business day of the respective month.

The board advises that it seeks to pursue a progressive dividend policy and so, barring exceptional circumstances, we expect that the board will only want to make upwards revisions to the quarterly dividend rate and will seek to ensure that any increases are sustainable.

Annual dividend rate raised to 7.4p per share

Having maintained its total dividend at 6.60p per share for the financial years ending 30 September 2020 and 2021, EGL’s board announced, in December 2021, an increase in the quarterly dividend rate to 1.85p per share (from 1.65p), an increase of 12.1%, equating to a total dividend of 7.4p per share for the financial year. All four dividends have now been paid or declared. 7.40p is equivalent to a yield of 3.7% on the share price of 202.0p as at 18 November 2022.

Earnings and income receipts continue to be resilient

Trends is towards greater divided coverage.

Clearly, much has happened in global markets and the global economy since the board decided to increase the quarterly dividend rate in December 2021. However, while the dividend has been uncovered by revenue income in recent years (see Figure 26 above), the gap has been closing (we discussed EGL’s improving dividend cover in our October 2021 note). Jean-Hugues has previously commented that following the COVID-related market collapse of March 2022, earnings and dividends from EGL’s underlying holdings have proven to be resilient and it would appear that this trend has continued. The Russian invasion of Ukraine has caused a surge in gas and power prices which, whilst painful for consumers, is a boon to renewable generators with their fixed-cost bases.

In its interim accounts for the half-year ended 31 March 2022, EGL posted a revenue return per share of 2.24p per share, which is a 23.1% increase versus the 1.82p per share generated during the same period for the financial year. EGL’s manager models the revenue growth that it expects to see from its portfolio a number of years out, and this model supports expected revenue growth of 5-7% per annum.

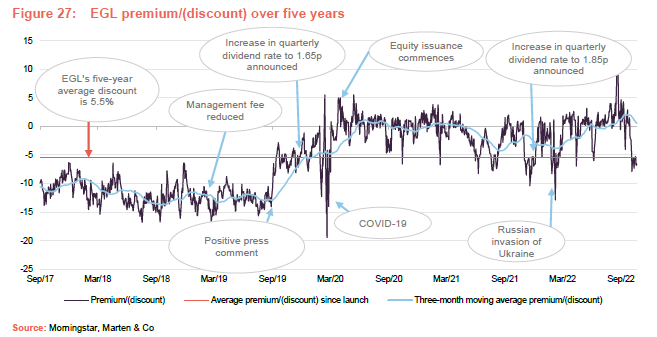

Premium/(discount)

A discount has emerged, but this might be short-lived

As is illustrated in Figure 27, despite the recent market turmoil, EGL continued to trade at a modest premium to NAV until very recently, with limited exceptions. This allowed the trust to continue to issue stock and grow, to the benefit of all shareholders, while helping to stop the premium from otherwise expanding to unhelpful levels. So far this calendar year, EGL has issued 11.45m shares, or 11.3% of its issued share capital at the start of the year.

During the last 12 months, EGL’s shares have traded between a discount of 12.9% and a premium of 9.0%, with an average discount of 1.0%. The three-year average discount, which also includes the short-lived but wild swings in the discount, is just 1.4%. At 18 November 2022, EGL’s shares were trading at a discount of 6.8%, which could prove to be short-lived.

The step change in EGL’s discount that occurs from September 2019 is a subject that we first discussed in our October 2019 note (see previous publications on

page 24). Since that re-rating, EGL’s share price performance has been more in step with the trust’s attractive NAV performance. EGL’s manager and board have made significant efforts to raise the profile of the trust and EGL has also benefitted from other shareholder-friendly initiatives such as the reduction in management fee illustrated in Figure 27. EGL has, through a combination of share issuance and strong performance, grown which serves to further boost liquidity in the trust’s shares.

Fund profile

Developed markets utilities and infrastructure exposure with an income and capital preservation focus

Further information regarding EGL can be found on the manager’s website ecofininvest.com/egl

EGL has a strong focus on capital preservation.

Reflecting its capital preservation objective, EGL does not invest in start-ups, small businesses or illiquid securities, as these may involve significant technological or business risk. Instead, it invests primarily in businesses in developed markets, which have ‘defensive growth’ characteristics: a beta less than the market average; dividend yield greater than the market average; forward-looking earnings per share (EPS) growth; and strong cash-flow generation.

It also operates with a strict definition of utilities and infrastructure as follows:

- electric and gas utilities and renewable operators and developers – companies engaged in the generation, transmission and distribution of electricity, gas, liquid fuels and renewable energy;

- transportation – companies that own and/or operate roads, railways, ports and airports; and

- water and environment – companies operating in the water supply, wastewater, water treatment and environmental services industries.

EGL does not invest in telecommunications companies or companies that own or operate social infrastructure assets funded by the public sector (for example, schools, hospitals or prisons).

No formal benchmark

EGL does not have a formal benchmark and is not constructed with reference to any index.

EGL does not have a formal benchmark and its portfolio is not constructed with reference to an index. However, for the purposes of comparison, EGL compares itself to the MSCI World Utilities Index, the S&P Global Infrastructure Index, the MSCI World Index and the All-Share Index in its own literature. We are using a similar approach here, but are using the MSCI UK Index to represent the UK market. Of the three indices, we consider the MSCI World Utilities to be the most relevant – although it should be noted that this index has a strong bias towards US companies.

Manager

Ecofin Advisors Limited is EGL’s investment manager and AIFM. Ecofin Advisors is a subsidiary of TortoiseEcofin Investments, LLC, a privately-owned US-based firm which owns a family of investment management companies. At the end of September 2021, TortoiseEcofin had approximately US$8.3bn of client funds under management.

EGL’s senior portfolio manager is Jean-Hugues de Lamaze. He has worked for Ecofin since 2008 and has managed both EGL and its predecessor, Ecofin Water & Power Opportunities (EWPO), since March 2016. Prior to joining Ecofin, Jean-Hugues co-founded UV Capital LLP and served as its chief investment officer. Previously, he oversaw the Goldman Sachs European Utilities research team and prior to that he was a senior European analyst and head of French Research & Strategy at Credit Suisse First Boston.

Jean-Hugues’s professional career began at Enskilda Securities. He is a CFAF-certified analyst and a member of the French Financial Analysts Society SFAF. Jean-Hugues completed the INSEAD International Executive Programme, graduated from Paris-based business school Institut Supérieur de Gestion and earned a LLB in Business Law from Paris II-Assas University. He was voted Top 10 Buy-Side Individual – All Sectors and Top 3 in the Utilities category in the 2018 Extel survey.

Well-resourced team.

Jean-Hugues leads a team of nine investment professionals – eight of whom are based in London and one who is based in Kansas City. He is also able to draw on extensive resources in Kansas City.

Previous publications

Readers interested in further information about EGL, such as investment process, fees, capital structure, trust life and the board, may wish to read our annual overview note Happy birthday to ya!, published on 28 October 2021, as well as our previous update notes and our initiation note (details are provided in Figure 28 below). You can read the notes by clicking on them in Figure 28 or by visiting our website.

Figure 28: QuotedData’s previously published notes on EGL

Source: Marten & Co

Legal

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Ecofin Global Utilities and Infrastructure Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.