Sunny outlook

Ecofin US Renewables Infrastructure Trust (RNEW) is just a few months old, but has already deployed well over half of its IPO proceeds and declared its maiden dividend two months ahead of target, putting it well on the way to achieving its 7.0-7.5% total return and 5.25%-5.75% dividend yield target (based on the $1 IPO price).

As we explain on page 6, RNEW’s US focus comes with much longer-term contracts for sales of the power it generates (power purchase agreements) than are typically available in the UK. This much reduces RNEW’s sensitivity to short-term power prices relative to its UK- and European-focused peers. RNEW’s broad remit, which focuses on solar and wind but allows investment in a range of other renewable energy generation, battery storage and other sustainable infrastructure assets, provides further differentiation.

The political and regulatory environment in the US is supportive of substantial and reasonably rapid growth in RNEW’s target markets. We believe that RNEW could and should be a much bigger fund, while maintaining its focus on the US middle market (see page 10).

Long-term, progressive income from diversified portfolio of US renewables

RNEW aims to provide its shareholders with an attractive level of current distributions by investing in a diversified portfolio of mixed renewable energy and sustainable infrastructure assets predominantly located in the United States with prospects for modest capital appreciation over the long term.

Fund profile

RNEW is an investment company that has been established to invest in a diversified portfolio of renewable assets. Predominantly, these will be in the United States, but it may also invest up to 15% of gross assets in other OECD countries. The company is being managed to qualify as an investment trust. Since 20 December 2020, RNEW has had a premium listing on the main market of the London Stock Exchange.

RNEW’s principal focus is on solar photo-voltaic (PV) – including ground-mount utility scale and commercial rooftop solar but excluding residential – and onshore wind. Within these target sectors, RNEW’s focus is on the middle market segment (see page 9). Solar and wind assets will account for at least 90% of RNEW’s portfolio. However, RNEW is also permitted to invest up to 10% of its portfolio in battery storage, biomass, hydroelectric and microgrids, water and waste-water and related renewable assets.

RNEW aims to generate attractive risk adjusted returns. It is targeting net total returns of 7.0%-7.5% per annum and a sustainable dividend yield of between 5.25% and 5.75% on the initial $1 issue price for an ordinary share.

The company’s functional currency is US dollars but, if they choose, investors may hold shares quoted and paying dividends in sterling (ticker RNEP), which have the same legal status as the dollar shares.

Ecofin Advisors LLC – the manager

RNEW’s investment manager and AIFM is Ecofin Advisors LLC (Ecofin), which is headquartered in Leawood, Kansas. That and Ecofin Advisors Limited, manager of Ecofin Global Utilities and Infrastructure, are indirect wholly-owned subsidiaries of TortoiseEcofin Investments LLC, a business with assets under management of $8.2bn with offices across the US and in London. The two subsidiaries had $1.4bn of assets under management between them at the end of March 2021.

Ecofin’s mission is to generate strong risk-adjusted returns while optimising investors’ impact on society. They describe themselves as socially-minded, environmental, social and governance (ESG) attentive investors.

The management team has a wealth of experience and expertise in investing in sustainable infrastructure, energy transition, clean water & environment and social impact sectors. Ecofin’s strategies seek to achieve positive impacts that align with UN Sustainable Development Goals by addressing pressing global issues surrounding climate action, clean energy, water, education, healthcare and sustainable communities. More information about the way that RNEW addresses issues of sustainability is available on page 14.

The senior members of the team managing RNEW have a combined 50 years of private investment experience and have worked together for seven years. More information on the team is available on page 22.

Why RNEW?

RNEW is a recent entrant to an increasingly crowded field (the AIC’s renewable energy infrastructure sector now has 17 constituents – see page 18). However, RNEW is clearly differentiated from its peer group. Only two other funds – US Solar Fund and SDCL Energy Efficiency Income Trust – offer exposure to US solar projects, and RNEW is likely to be the only fund offering pure play exposure to the wider renewable energy generation industry in the US. It is intended that predominantly all of the power generated by RNEW’s investments will be sold under long-term fixed price power purchase agreements (PPAs) to purchasers that would qualify as investment-grade in a credit assessment. This should give RNEW predictable cashflows that are uncorrelated to broader securities markets.

As we describe in the next section, there are many reasons why the US renewables sector is an attractive place to invest.

In its prospectus, RNEW identified an immediate pipeline of projects totalling $61m. These acquisitions have since been executed, the manager has committed to a further ground-mount solar project, and the company has now invested around 55% of its IPO proceeds. At 31 March 2021, the manager had a long term pipeline of opportunities worth $4.9bn.

The US renewable energy industry

We think the fundamental difference between the US renewable energy industry and that of the UK (which is the one that many readers may perhaps be most familiar with) is the revenue structure.

COVID-19-related falls in power prices (as demand for power has been lower than normal) have been an overhang on the wider renewable energy sector over the past year. However, RNEW is much less exposed to short-term fluctuations in power prices than most of its UK- and European-focused peers. The vast majority of power that RNEW’s projects generate is sold through long-term PPAs at fixed prices with an average contract length of at least 15 years. Therefore, the major source of risk is not power prices, which are wholly outside of the generator’s control, but credit risk of off-taker counterparties, which good underwriting standards and credit analysis, and RNEW’s focus on investment-grade quality purchasers can substantially mitigate. In addition, some PPAs incorporate annual price escalators which provide some inflation protection.

The opportunity set for RNEW is vast. The US power market is 12.9x the size of the UK’s and 1.3x that of the EU’s according to BloombergNEF. However, relative to the UK and EU, the US renewables sector is relatively underdeveloped.

Ecofin believes that the US renewables market is at an inflection point, with a substantial tailwind behind it. The Biden presidency’s commitment to addressing climate change is a significant factor in this, but Ecofin notes that the industry already seemed to be making reasonable progress under Trump.

The main reason for this comes down to economics. Falling costs and efficiency gains make renewable energy projects cheaper than fossil fuel equivalents, even without subsidy. Couple that with tax credits designed to stimulate investment in the sector and renewable energy makes a compelling proposition.

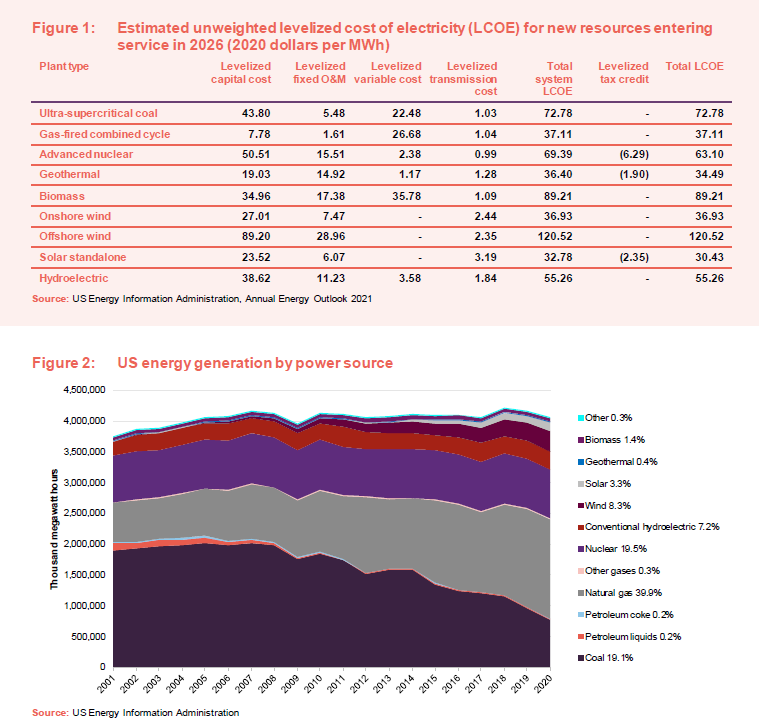

Figure 1 compares the cost of generating electricity from different fuel sources in the USA.

BloombergNEF reckons that investment in renewable energy in the US has exceeded $330bn over the past five years. Solar alone represented 43% of all new generating capacity in the US in 2020 (according to the Solar Energy Industries Association). However, compared to a market such as the UK, renewable energy’s share of generation in the US is far less developed. Take, for example, coal-fired powered generation, which accounted for over 19% of US energy generation in 2020, yet the equivalent figure in the UK was 1.6% and this is targeted to hit zero by 2025. By contrast, total generation from renewables in the US in 2020 accounted for 21% of energy generation against 40% for the UK.

The US installed 19.2GWdc of solar PV capacity in 2020 to reach 97.2GWdc of total installed capacity, enough to power 17.7 million American homes (based on data from the Solar Energy Industries Association). The US is already the second-largest solar power producer globally (after China). However, its potential is very unfulfilled.

The prospectus that RNEW produced in connection with its IPO says that, based on figures supplied by BloombergNEF, that thanks to its more southerly location, the 48 contiguous states of the US (i.e. excluding Hawaii and Alaska) receive more than 2.5x as much solar irradiation as the UK. The Solar Energy Industries Association reckons 324GWdc of new solar capacity will be installed in the US over the next decade, more than quadrupling the size of the sector.

RNEW will not invest in residential rooftop solar, but does have some exposure to commercial rooftop solar. These assets tend to offer higher returns than ground-mounted solar because of the added complexity of underwriting numerous smaller assets to achieve scale, which larger fund investors are not set up to do. Essentially, this “middle market” segment of wind and solar that RNEW targets has less crowded capital markets and so the manager can achieve better risk-adjusted returns in commercial solar versus large-scale utility solar ($100m+ assets that have utilities and large infrastructure funds bidding up in price).

In wind, again the US ranks second to China. According to the American Clean Power Association, at the end of 2020, there was 122.5GW of operating wind power capacity in the US, with over 60,000 turbines. They say that 2020 was also a bumper year for new installations, and the year finished with 17.3GW of capacity under construction and a further 17.5GW in advanced development.

Subsidies support the industry – solar and wind

Federal tax credits help support the development of new capacity. Congress passed a one-year extension to the wind production tax credit and a two-year extension to the solar investment tax credit in December 2020.

The solar investment tax credit was 30% for projects under construction in 2019. For 2020 it was 26%, is now maintained at that rate for 2021 and 2022 and falls to 22% for projects that begin construction in 2023 and 10% for projects commencing construction in 2024. Qualifying projects that had begun construction before 2020 are still entitled to the full 30% tax credit, provided that the projects become operational before 2024.

However, the Biden administration’s $2trn infrastructure plan envisions a 10-year extension to the solar investment tax credit. It is also supporting research efforts to drive down the cost of solar installations through the use of perovskite solar panels (a crystalline structure that is more efficient and cheaper to produce than traditional silicon PV).

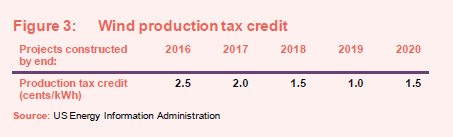

The wind production tax credit is inflation-adjusted and applies for the plant’s first 10 years of service. The rate has varied over the years. It was 2.5 cents per kWh for projects that began construction before the end of 2016. The figure has varied since then as Figure 3 shows. At the end of December 2020, Congress extended the production tax credit at the same rate as in 2020.

The infrastructure plan envisages a 10-year extension to this, but without this the production tax credit ceases from 2022 onwards. The same production tax credits also apply to geothermal and closed-loop biomass plants with the same time-dependent reductions.

There are also some State-level incentives. For example, Massachusetts has recently implemented legislation to target net zero emissions in the State by 2050 and has a longstanding policy to require that retail electricity suppliers provide customers with a minimum percentage of electricity from renewable energy. This ‘renewable portfolio standard’ has been applied in 30 of the 50 US States. The percentage varies by State. In Virginia, legislation requires that all power generation is renewable by 2045.

Other technologies

In respect of other technologies, RNEW’s prospectus stressed that similar to the company’s strategy for solar and wind, it will only seek investment in sectors that utilise proven technology and have long-term offtake contracts with investment-grade-quality customers to mitigate risk.

The US offshore wind market is considerably behind that of the UK and the costs of developing projects seem fairly high. Contrast the $120.5/MWh LCOE for wind projects in the US (2020 prices) from Figure 1 with £57/MWh for offshore wind projects in the UK (based on Department for Business, Energy and Industrial Strategy figure in 2018 prices).

Nevertheless, Ecofin recognises that offshore wind projects are big-ticket items and too big for the fund currently.

The International Hydropower Association says the installed base of hydroelectric generation was 80GW at the end of 2019. There was also 23GW of pumped storage hydropower. Using data from the Environmental Protection Agency’s US Hydropower Market Report for 2018, RNEW’s prospectus said that $7bn was invested across 160 projects over the decade from 2009-2018, with $493m invested in 36 new projects in 2018.

The American Biogas Council says that the US has over 2,200 sites producing biogas from 250 anaerobic digesters on farms, 1,269 water resource recovery facilities using an anaerobic digester, 66 stand-alone systems that digest food waste, and 652 landfill gas projects. They contrast this with the situation in Europe, which has over 10,000 operating digesters.

Energy storage is an important component of the transition to renewable energy generation. It can help to stabilise power grids trying to adapt to the short-term fluctuations in generation associated with many renewable energy technologies. Steep falls in the cost of batteries have increased the attractions of the energy storage market.

Ecofin also sees opportunities in micro-grids – localised electric grids – and smart grid technology. Another potential area of investment is in water and wastewater infrastructure, where it is generally acknowledged that the US has suffered from decades of under investment.

Conservative investment approach

Return rises for smaller projects

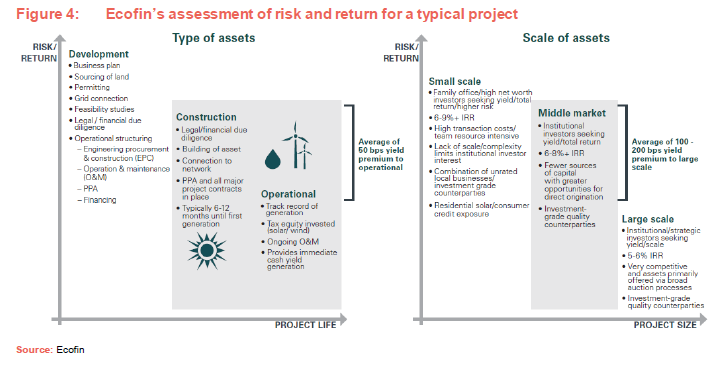

Whilst a very limited exposure to projects in the development phase is permitted (see page 13), RNEW will focus on construction-ready and operational assets in the middle market, where Ecofin feels that the balance of risk and reward is optimised. Figure 4 shows Ecofin’s assessment of the risk/returns based on project maturity and size.

RNEW’s focus is on mid-market deals, which are priced less keenly than larger transactions. Ecofin says that for vendors of assets smaller than $50m, it is hard to justify the extra cost of hiring an external advisor to conduct an auction process. It is simpler and cheaper to negotiate a bilateral deal. This focus on smaller assets also creates an opportunity for RNEW’s shareholders as, collectively, RNEW’s portfolio could be worth more than the sum of its parts.

Predictability of income

RNEW is aiming to sell the power that it produces under long-term (an average of at least 15 years) PPAs. The creditworthiness of the counterparties to these PPAs is a key consideration for the manager. Ecofin has in-house expertise in the analysis of credit risk. RNEW’s existing portfolio includes PPAs with diverse investment grade purchasers including a utility in California and numerous schools, universities and municipalities in Massachusetts.

Project structures

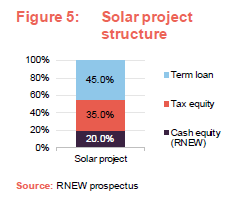

A typical US solar project may be funded with cash equity, tax equity (see below) and non-recourse project debt.

RNEW’s investment will typically be via cash equity, although it is permitted to gain its exposure through debt-type structures.

The tax equity is provided by the likes of US banks, insurers and corporates, who effectively buy the right to use the tax credits associated within a project to offset against their own tax liabilities.

Lenders are comfortable with the risks associated with financing solar assets and are prepared to lend on the basis of a 1.4x debt service coverage ratio (income:debt service cost), which typically translates into 40%–50% of the capital structure.

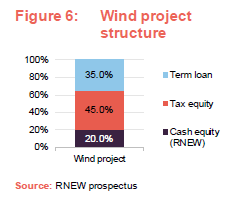

Investment structures for wind projects look similar. However, the proportion supplied by tax equity investors is higher. Tax equity investors get the benefit of production tax credits (which may be as high as 2.5 cents per kilowatt) over a 10-year period. They may also benefit from tax depreciation and a modest level of cash distributions.

Again, lenders are prepared to lend on the basis of a 1.4x debt service coverage ratio.

In both cases, the tax equity element of project financing is not available in the construction phase. Some projects in the construction phase may also seek bridge financing in addition to cash equity and loan finance.

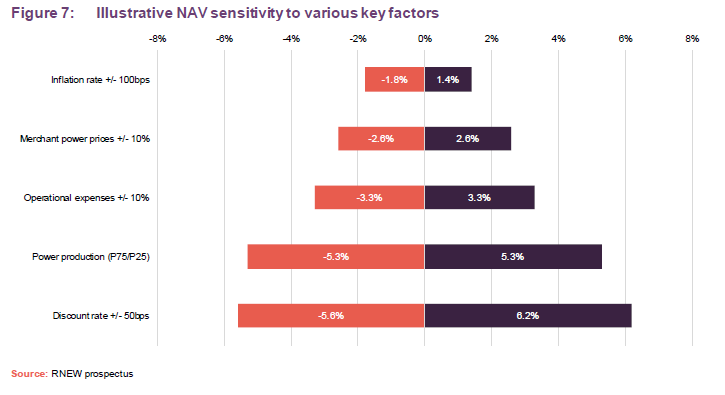

Sensitivities

RNEW’s prospectus included a chart showing the likely sensitivity of RNEW’s cash flows to various factors. We have reproduced this below. Please note, however, that the prospectus chart reflected an illustrative 7.5% per annum total shareholder return on an initial $250m US renewable energy portfolio over a 35-year term. The actual experience may deviate from this.

Investment process

RNEW’s prospectus, published in December 2020, contains a comprehensive description of RNEW’s investment approach and process. We have summarised the main elements of this here, but anyone interested to read more should refer to pages 92 to 101 of the prospectus.

Sourcing deals

Ecofin sees a strong advantage from having a team on the ground in the US. The Ecofin team has considerable expertise in acquisition origination, underwriting, structuring, construction, financing and asset management, having evaluated more than 750 opportunities worth approximately $35bn since 2016 and far more across their long careers (see page 22 for more information). Not only has the team built up relationships with hundreds of experienced solar and wind developers, operators and sponsors through the many investments that its members have made over the years, but they also lend out their expertise in consultation to smaller players in the industry on structuring projects, for example. Many of the people working at these businesses are ex-colleagues.

This gives Ecofin access to a significant pipeline of opportunities (around $6bn at end March 2021), many of which can be negotiated on a bilateral basis, securing assets at more attractive prices and avoiding the cost and frustrations associated with buying assets at auction.

Buying projects in the construction phase

When RNEW is buying assets that are in the construction phase, an important part of the manager’s job is to assess the suitability of the engineering, procurement and construction (EPC) contractor. Having the experience to negotiate attractive and watertight terms, warranties and protections in the event of default (the risks associated with construction such as cost overruns and delays will remain with the contractor) is essential. Payments to contractors will be made in relation to mutually-agreed milestones, typically with a material retention price which is only payable following completion.

Investment structures

Investments will be made either directly or through one or more project SPVs, which may in turn be held by a wholly-owned US subsidiary of the company. Such investments will typically be structured as equity investments or partnership interests, but the company may also invest through debt instruments or other structures.

The company will usually aim to take a 100% or a controlling interest in a project. Where it is a minority investor, Ecofin will seek customary rights in any shareholder or partnership agreement to protect the company’s investment.

The investment approval process

Having identified a potential acquisition, preliminary research and modelling is conducted on the business plan, economics and the project management team.

A private sustainable infrastructure management committee reviews the overall investment process, procedures and practices necessary to ensure the portfolio is in compliance with the company’s investment strategy, policy and investment restrictions (see page 14).

Proposed investments that pass these initial reviews will then be subject to detailed due diligence, often in conjunction with outside contractors, before being put before Ecofin’s private sustainable infrastructure investment committee. This committee is also responsible for reviewing and monitoring all of the company’s investments in renewable assets. It gets first sight of proposed investments.

An ESG risk assessment and an independent credit review and underwriting of an offtaker’s credit are fundamental parts of the due diligence process. Ecofin, along with its legal and technical advisors, reviews offtake agreements to ensure that they are enforceable and the project is capable of meeting its obligations under the contract to mitigate revenue risk.

This committee is responsible for approving investment decisions, monitoring investments and providing strategic oversight (including asset allocating between different classes of renewable assets).

Restrictions

RNEW will invest subject to the following investment limitations which, other than as specified below, shall be measured at the time of the investment and once the net initial proceeds are substantially fully invested (at least 75% of IPO proceeds). Percentages relate to gross assets as follows:

- a minimum of 20% will be invested in solar;

- a minimum of 20% will be invested in wind;

- a maximum of 10% of will be invested in renewable assets that are not wind or solar;

- exposure to any single renewable asset will not exceed 25%;

- exposure to any single offtaker will not exceed 25%;

- investment in renewable assets that are in their construction phase will not exceed 50%,

- exposure to renewable assets that are in the development (namely pre-construction) phase will not exceed 5%;

- exposure to any single developer in the development phase will not exceed 2.5%

- the company will not typically provide forward funding for development projects. Such forward funding will, in any event, not exceed 5% in aggregate and 2.5% per development project and would only be undertaken when supported by customary security;

- future commitments and developer liquidity payments, when aggregated with forward funding (if any), will not exceed 25%;

- renewable assets in the United States will represent at least 85%; and

- any renewable assets that are located outside of the United States will only be located in other OECD countries.

The company expects that construction will be primarily focussed on solar in the shorter term until the portfolio is more substantially invested and may thereafter include wind assets in the construction phase.

Sustainability

RNEW is clearly well-suited to an investor concerned with sustainable investing. Its ambition is to contribute towards the reduction of carbon and other greenhouse gas emissions, and reducing pollution, while not compromising investors’ desire for stable cash yields and attractive total returns.

Ecofin is a PRI signatory and conducts its business in alignment with the UN-supported Principles for Responsible Investment (PRI). The investment manager is committed to integrating ESG criteria into its investment process to enhance overall governance. All of RNEW’s investments are analysed through Ecofin’s proprietary ESG due diligence risk assessment framework for suitability prior to commitment.

ESG criteria and impact of the company’s investment activities will be measured, analysed and reported to investors on an ongoing basis, culminating with an annual ESG impact report.

Each asset’s contribution to decarbonisation will be assessed and the manager will actively manage RNEW’s assets to realise those objectives. In the due diligence phase of the investment process, Ecofin will engage third-party environmental consultants to produce reports that assess environmental impacts of each asset. It will also engage legal counsel and independent engineering firms to confirm project compliance with all permitting and regulatory requirements.

Ecofin will also analyse the impact investments have on the local community, including the extent to which they contribute a positive economic impact through tax related payments and recurring lease revenue to landowners.

Ecofin will engage with the community and hire experienced operations and maintenance (O&M), project asset management, and construction firms which will be held responsible for reporting on health and safety incidents related to the assets.

RNEW has been awarded the London Stock Exchange’s Green Economy Mark, which recognises companies that derive 50% or more of their total annual revenues from products and services that contribute to the global green economy.

Ongoing management

The framework of O&M contracts is agreed during the due diligence phase. The private sustainable infrastructure management committee is responsible for portfolio oversight and risk management. Renewable energy production figures are reviewed on a monthly basis. Existing investments are reviewed at quarterly management/partner meetings. The team may conduct site visits as well as engaging in regular dialogue with project stakeholders.

RNEW also benefits from a skilled operations team, based in Kansas City. It engages regularly with the operators to proactively address and mitigate technical and commercial issues. Keeping assets working optimally can help boost returns. It also helps that equipment comes with long-term warranties.

Hedging

The group may use derivatives for the purposes of hedging, partially or fully, as follows:

- electricity price risk relating to any electricity or other benefit, including renewable energy credits or incentives, generated from renewable assets not sold under a PPA, as further described below;

- currency risk in relation to any sterling (or other non-US dollar) denominated operational expenses of the company; and

- other project risks that can be cost-effectively managed through derivatives (including, without limitation, weather risk); and interest rate risk associated with the company’s debt facilities.

In order to hedge electricity price risk, the company may enter into specialised derivatives, such as contracts for difference or other hedging arrangements, which may be part of a tripartite or other PPA arrangement in certain wholesale markets where such arrangements are required to provide an effective fixed price under the PPA.

Members of the group will only enter into hedging or other derivative contracts when they reasonably expect to have an exposure to a price or rate risk that is the subject of the hedge.

Asset allocation and pipeline

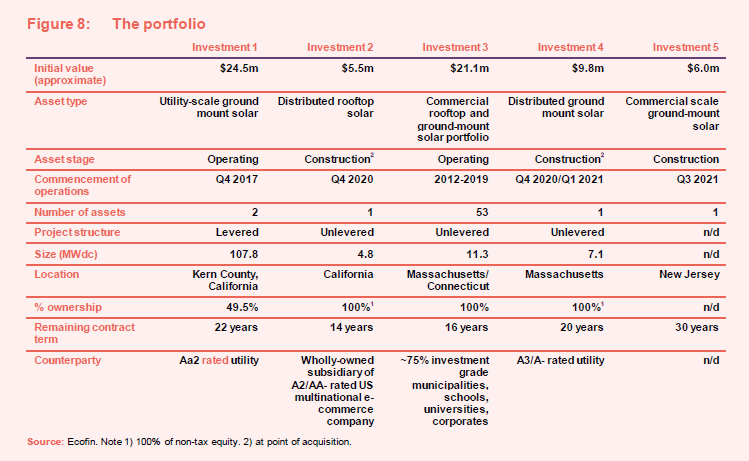

RNEW’s prospectus described a seed portfolio valued at about $61m and consisting of four solar investments. By 4 February 2021, the company had completed the purchase of all four seed investments and could claim to have invested approximately 50% of its net IPO proceeds. A fifth investment, a $6m commercial-scale ground-mount solar project in New Jersey, was announced on 4 May 2021.

All of the power output from these assets is contracted under long-term PPAs, 30 years in the case of the most recent acquisition.

Even post-acquisition, there may be opportunities to enhance the value of assets, through initiatives such as equipment upgrades, life extensions and refinancings.

For example, Ecofin says that ‘investment 1’ may benefit from a solar tracker software optimisation project to improve output.

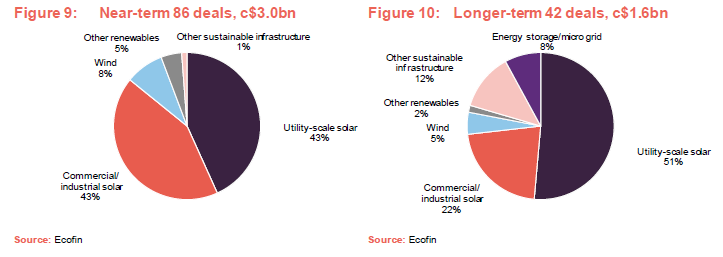

More detail on the $4.6bn pipeline that the Ecofin team had identified at launch is provided in Figures 9 and 10. The pipeline was broken down into nearer-term (six months from launch) and longer-term (six-to-12 months from launch). The pipeline has since grown, standing at $4.9bn at end March 2021.

Valuation

Ecofin will value the assets on a quarterly basis and, twice a year, these valuations will be reviewed by an independent valuation firm.

The fair value of renewable assets will be derived from a discounted cash flow (DCF) methodology. Assets which have not yet been placed into service will be valued at cost.

The choice of discount rate will reflect inputs such as:

- available discount rates used by competitors;

- discount rates applicable to comparable infrastructure asset classes;

- available discount rates for comparable market transactions;

- discount rates recently provided by the third-party valuation provider; and

- capital asset price model outputs and implied risk premium over relevant risk-free rates.

A broad range of assumptions is used in valuation models. Where possible, these assumptions are based on observable market and technical data and independent third-party data. Ecofin also engages technical experts such as long-term electricity price consultants to provide long-term data for use in its valuations.

Assets are not ascribed any terminal value. Termination dates tend to be associated with factors such as the expiry of grid connection permits and land leases.

Geographic diversification of the portfolio provides some mitigation against local adverse weather conditions, which can affect production.

Performance

It is very early days in RNEW’s life and hence we have not provided charts and tables related to RNEW’s performance since launch, or any analysis of its performance.

At the end of March 2021, RNEW’s NAV was $123.8m or 99.06 cents per share. This figure was stated inclusive of the 0.4 cent per share dividend declared on 4 May 2021 in respect of the period from IPO to 31 March 2021.

Peer group

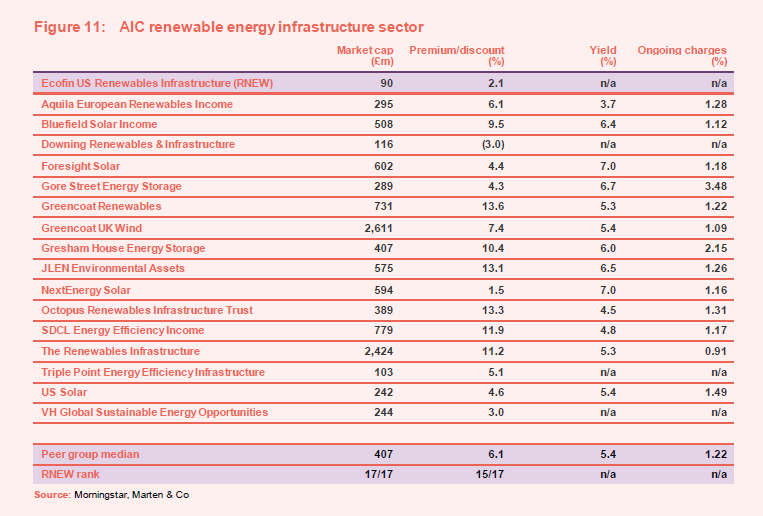

RNEW is one of the more recent entrants to the AIC’s renewable energy infrastructure sector, which now has 17 constituents. The peer group is reasonably diverse, however, and RNEW is differentiated from its peers.

Of the peer group, US Solar Fund and SDCL Energy Efficiency Income Trust do offer exposure to US solar projects. VH Global Sustainable Energy Opportunities is permitted to do so but, as yet has made only one investment. In any case, it intends to focus on projects in the development phase, which, as we have discussed, adds extra risk and complexity.

RNEW is likely to be the only fund offering pure play exposure to the wider renewable energy generation industry in the US.

RNEW is the smallest of these funds, and we would like to see it deploy its IPO proceeds and look to expand relatively quickly (although we acknowledge that Ecofin will be just as keen not to rush things). Many of the other funds also started off small but expanded over time.

Morningstar is not yet including a prospective dividend for RNEW within its statistics. Once the portfolio is established and RNEW’s dividends are up to speed (target FY 2022), its yield will be about middle of the pack for this peer group.

We do not yet have any indication of annual running costs for the fund – the figure in the prospectus was based on a much larger fund. Size is an important factor in this, as fixed costs are spread over a smaller base. This is easily rectified by growing the trust.

Dividends

RNEW will declare and pay dividends quarterly. The prospectus said that it aimed to pay an initial annual dividend yield of 2 to 3% (based on the $1 initial issue price per ordinary share) for the period from launch to 31 December 2021. One caveat was whether the renewable assets acquired using the IPO proceeds were substantially fully operational by 31 December 2021 or expected to be so within 12 months from the date of commitment). The dividend would be paid from operational cashflows plus a transfer from capital, if necessary.

In the event, a first dividend of 0.4 cents per share, covering the period from IPO to 31 March 2021, was declared on 4 May 2021. This first dividend came two months ahead of schedule and is payable from operating cashflows. The swift deployment of over half the IPO proceeds was a contributing factor in this. The board says that it is pleased with progress to date and this sets strong foundations to accomplish the initial dividend target.

For 2022 onwards, the target is an annual dividend yield of 5.25% to 5.75% on the initial issue price) and an average annual dividend growth rate of at least 1% over the medium term.

On 23 April 2021, the company announced that the court had approved the cancellation of the share premium account and the credit of an equivalent amount to a special distributable reserve. This increases RNEW’s distributable reserves by $121.25m.

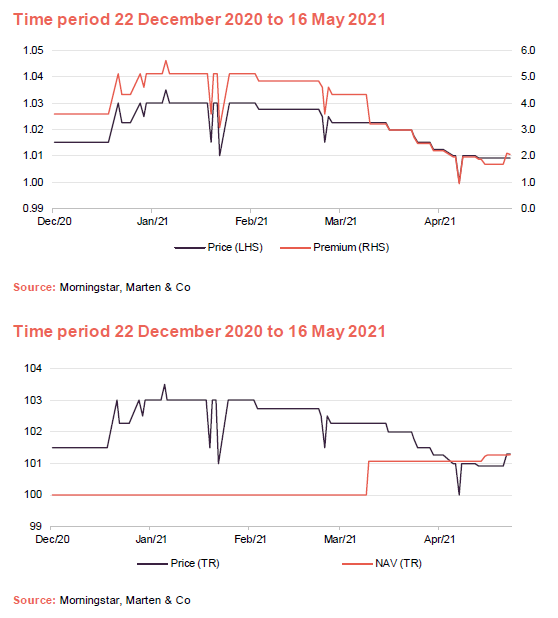

Premium/(discount)

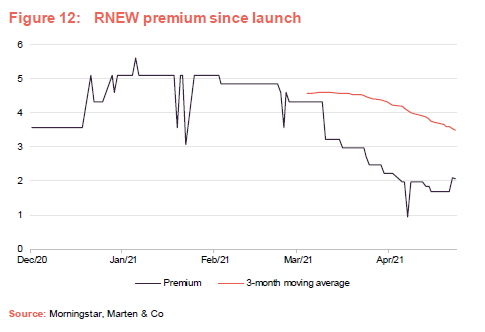

RNEW has traded consistently at a premium to NAV since launch and within a relatively narrow band.

With a view to moderating the level of the premium and expanding the company, the directors have authority to issue, in aggregate, up to 500m ordinary shares and/or C shares on a non-pre-emptive basis.

Issuance will only be undertaken at a price which is a premium to net asset value that at least covers any associated issue costs.

Where it might take some time to get the net proceeds invested, the intention is to issue C shares rather than new ordinary shares. This helps protect existing shareholders from the effects of cash drag.

In the event that the shares trade at a discount, the directors have discretion to authorise share repurchases with a view to managing any imbalance between the supply of and demand for shares. The board has powers to buy back up to 14.99% of RNEW’s initial share capital following admission. This authority expires at the conclusion of the first Annual General Meeting (AGM), but the board will ask shareholders for permission to renew the authority at each AGM.

The prospectus says that share buybacks are likely to be considered where the rolling 12-month average discount is 5% or more (commencing on the 18-month anniversary of admission, provided that the available cash is not required for working capital purposes or the payment of dividends).

Any shares bought back may be held in treasury and later re-sold at a premium.

Fees and costs

Ecofin is entitled to a management fee, which will only be charged on committed capital until commitments exceed 90% of the equity raised. The fee is calculated as 1.0% per annum of the first $500m of net assets, 0.9% per annum on the next $500m of net assets and 0.8% on any net assets in excess of $1bn.

On a quarterly basis, Ecofin will reinvest 15% of its fee in RNEW shares, which will then be subject to a rolling 12-month lock-up.

The administrator is entitled to an annual administration and company secretarial fee of £120,000 in respect of NAV up to and including $310m, plus an additional fee based on 0.025% of any NAV in excess of $310m.

The company’s auditor is BDO LLP. Its fee will be about £48,000 per annum.

Capital structure

At IPO, the issued share capital of the company consisted of 125,000,001 ordinary shares. Shares can be bought and sold in either dollars or sterling, but both lines of stock have equal rights and relate to the same pool of capital. The sterling quote is needed for RNEW to qualify for index inclusion.

RNEW does not have a fixed life. The directors may convene a continuation vote if the company has not invested, or committed to invest, at least 75% of its IPO proceeds within 18 months of admission. This seems unlikely to us, given that around 55% of the IPO proceeds have already been invested/committed.

In addition, shareholders will have an opportunity to vote on the continuation of the company at five-yearly intervals.

The company will hold an annual general meeting each year, commencing in 2022. Amongst other things, that AGM will include a vote on the company’s first full set of accounts covering the period from incorporation on 12 August 2020, through listing on 20 December 2020 and ending on 31 December 2021. Thereafter, accounting periods will end on 31 December in each year.

Gearing

Long-term debt shall not exceed 50% of gross assets and the short-term debt shall not exceed 25% of gross assets, provided that the total consolidated debt shall not exceed 65% of gross assets. Long-term debt would be used to provide structural leverage for investment in renewable assets.

The team is considering actively putting in place a revolving credit facility, which would be used to assist with the acquisition of investments in the periods between follow-on equity offerings. The manager says that this would benefit RNEW in enabling Ecofin to maintain a continuous presence in its markets and not have to pause while waiting for capital infusions through follow on equity offerings after the IPO proceeds are fully committed. It foresees benefits of raising long-term debt, as RNEW achieves greater scale, to provide optimal pricing and minimise transaction costs.

The gearing may be at the level of the relevant special purpose vehicle (SPV) holding a project or group of projects, at the level of any intermediate subsidiary of the company, or at the company level. Debt is likely to be denominated primarily in US dollars.

Financing provided by tax equity investors and any investments by the company in its project SPVs or intermediate holding companies which are structured as debt are not considered gearing for this purpose and are not subject to these restrictions.

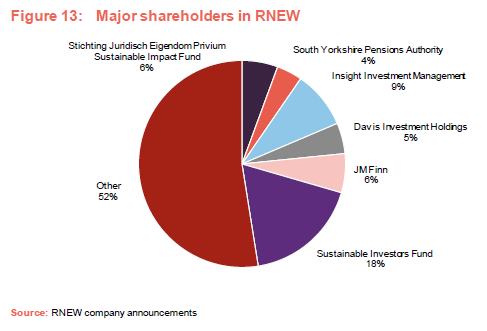

Major shareholders

Capricorn Investment Group, manager of Sustainable Investors Fund LP, is a longstanding strategic partner and seed investor in a number of Ecofin strategies.

Management team

Jerry Polacek, Matthew Ordway and Prashanth Prakash worked together at Energy & Infrastructure Capital LLC (EIC) for a number of years, before reuniting at Ecofin in 2016. Over their careers, the team has invested and managed investments in 58 solar projects worth $868m across nine US states, 50 wind projects worth about $4.9bn across 19 states and 11 other sustainable infrastructure projects (including hydroelectric, biomass, battery storage, geothermal and water), worth $495m.

Jerry Polacek, CFA, managing director and group lead

Jerry serves as the managing director and group lead. At EIC, he was chief executive officer and chief investment officer from 2014 to 2016.

Jerry has 23 years of experience, including 19 years of principal investing experience. His experience prior to EIC includes a period as a managing director at GE Capital, Energy Financial Services, where he held various leadership roles focused on private equity and credit investment in the global energy infrastructure sector.

At GE, Jerry co-founded the renewable energy group in 2006 as head of portfolio management and also managed its energy technology venture capital portfolio. He has also been a controller at Morgan Stanley in its venture capital investment division, and a senior auditor with Ernst & Young, where he passed the certified public accountant (CPA) exam.

Jerry graduated magna cum laude from Adelphi University with a Bachelor of Business Administration in accounting and earned a Master of Business Administration in finance and entrepreneurship with honours from Columbia Business School. He is a CFA charterholder.

Matthew Ordway, managing director

Matthew Ordway is a managing director within the business. At EIC he served as chief financial officer and chief operations officer from 2014 to 2016. He was responsible for the overall financial and operational management of the partnership, portfolio management, and originating, structuring and executing deals.

Matthew has 23 years of experience, including 18 years of principal investing experience, and more than seven years of process and operational experience. He has served as chief financial officer at Ridgeline Energy, a renewable energy developer, and has also worked for First Wind, Babcock & Brown’s North American infrastructure group, GE (where he served as a senior vice president at GE Capital, Energy Financial Services), Andersen Business Consulting and as an engineer at International Paper Company.

Matthew holds a Bachelor of Science in mathematics from Fairfield University, and a Bachelor of Science in mechanical engineering and Master of Business Administration from Columbia University.

Prashanth Prakash, CFA

Prashanth is a managing director within the business. He has more than eight years of experience in the energy and infrastructure sectors focused on private equity and credit investments. At EIC, Prashanth served as vice president of investments. Prior to EIC, he was an assistant vice president at Deutsche Asset & Wealth Management. He also spent three years as an associate at JPMorgan’s Infrastructure Investment Fund, where he was responsible for sourcing, structuring and executing private equity energy and infrastructure transactions in the OECD countries. Prior to JPMorgan, Prashanth was an associate in Deloitte’s financial advisory group in New York.

Prashanth holds a bachelor’s degree in electrical and electronics engineering from National Institute of Technology, India, and a Master of Business Administration from the University of Rochester. He is a CFA charterholder.

Jakob Tobler

Jakob joined TortoiseEcofin in 2015 and served four years as a research analyst covering a universe of more than 60 publicly traded companies. He also participated in and performed due diligence on private investments in public equity (PIPEs) totalling more than $100m. Prior to joining TortoiseEcofin, he was an analyst with New England Pension Consultants in Las Vegas, Nevada.

Jakob earned a Bachelor of Science in Business Administration from the University of Nevada, Las Vegas and a Master of Science in finance from Vanderbilt University’s Owen Graduate School of Management.

Board

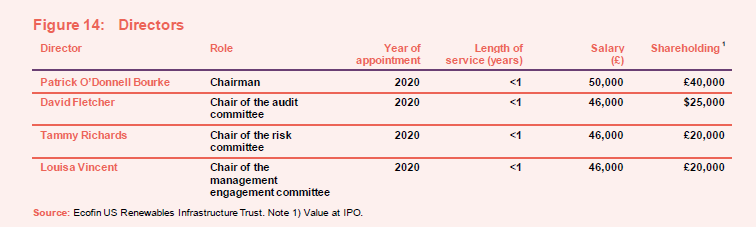

RNEW’s board consists of four non-executive directors, all of whom are independent from the manger and do not sit together on other boards. The company’s Articles of association cap the total fees payable to the directors at £400,000, but in practice the figure should be much lower than that as Figure 14 shows.

Patrick O’Donnell Bourke

Patrick O’Donnell Bourke is an experienced board member with 25 years of experience in energy and infrastructure, especially renewable energy. He also has significant international investment experience, particularly in Europe, US and Australia.

From 2013 to September 2020, Patrick served as chair of the audit committee at Affinity Water, the UK’s largest water-only company. Since February 2020, he has served as chairman of the audit and risk committee at Calisen Plc, an owner and operator of smart meters in the UK. From November 2020, he served as chairman of the audit committee of Harworth Group Plc, a leading regenerator of land and property for development and investment.

Patrick started his career at Peat Marwick, Chartered Accountants (now KPMG) and qualified as a chartered accountant. After that he held a variety of investment banking positions at Hill Samuel and Barclays de Zoete Wedd. In 1995, he joined Powergen Plc, where he was responsible for mergers and acquisitions before becoming group treasurer. In 2000, Patrick joined Viridian Group Plc as group finance director and later became chief executive. In 2011, he joined John Laing Group, a specialist international investor in, and manager of, greenfield infrastructure assets, as chief financial officer before retiring in 2019. While at John Laing, he was part of the team which launched JLEN Environmental Assets Group in 2014. Patrick is a graduate of Cambridge University.

David Fletcher

David Fletcher was group finance director of Stonehage Fleming Family & Partners, a leading independently-owned multi-family office, having joined in 2002. Prior to that, he spent 20 years in investment banking with JPMorgan Chase, Robert Fleming & Co. and Baring Brothers & Co Limited, latterly focused on financial services in the UK (asset management and life insurance).

He started his career with Price Waterhouse and is a chartered accountant. He is also an independent non-executive director of JP Morgan Claverhouse Investment Trust Plc, where he is the senior independent director and chairman of both the audit committee and the remuneration committee, and Aberdeen Smaller Companies Income Trust Plc, where he is the audit committee chairman. David is a graduate of Oxford University.

Tammy Richards

Tammy Richards is an experienced risk management professional with expertise in structured finance and a history of leadership in a global financial services business. She spent over 30 years at GE Capital in the risk management function, with more than 10 years in the energy sector.

While at GE Capital, Tammy held an array of risk leadership roles both in the US and in Europe serving as the European risk leader for the structured finance and capital markets units. She served as the deputy chief credit officer of the energy finance unit, a global US$15bn business focused on complex debt and equity investments in the energy sector. Most recently, she moved to the GE Capital headquarters unit as managing director, credit risk and portfolio analytics where she provided risk oversight of GE Capital’s aviation leasing and energy financial services units, developing risk appetite, credit delegations and governance and reporting frameworks. Tammy holds a B.S. degree in Economics from Cornell University and an M.B.A from the Amos Tuck School at Dartmouth College.

Louisa Vincent

Louisa Vincent has had a 30-year career in financial services, working globally in institutional, wholesale and retail financial services, most recently at Lazard Asset Management Limited where she was managing director, head of institutions, and in which she had overall responsibility for the firm’s institutional clients. Prior to that, she was with State Street Global Advisors (SSgA) in both its Sydney and London offices. She also chairs Fight For Sight, the UK’s leading eye research charity, taking up the role in March 2020, having been a board member since 2015. She is particularly committed to clear communication, bringing the customer’s voice to the boardroom and ensuring business sustainability through ESG.

Louisa began working in the investment field in 1988 in Sydney, Australia and has an MBA (Exec) from the Australian Graduate School of Management (AGSM).

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Ecofin US Renewables Infrastructure Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.