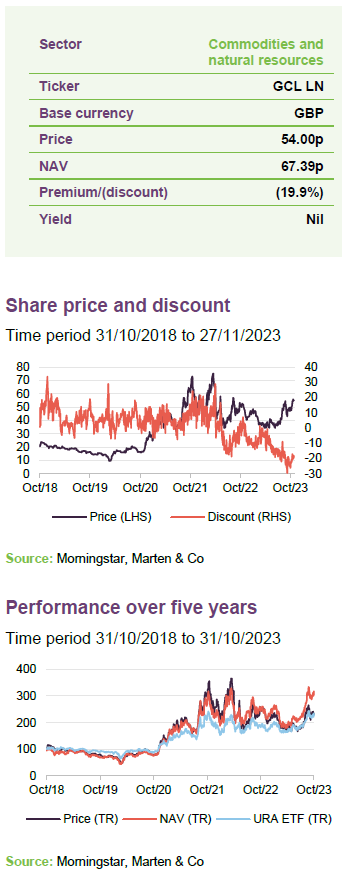

Geiger Counter Limited

Investment companies | Annual overview | 28 November 2023

Powered up for growth?

Geiger Counter (GCL), which invests in companies involved in the exploration, development and production of uranium, may benefit from nuclear power’s role in decarbonising the global electricity supply. Governments around the world appear to be making nuclear energy (a source of zero carbon baseload power) a cornerstone of their green agendas. Existing reactors’ lives are being extended, while Asia drives a global fleet expansion as demand for uranium surges. Meanwhile, a 10-year bear market has restricted investment in any new supply and created what GCL’s managers describe as a highly supportive backdrop for uranium, with the spot price jumping considerably in recent months. At less than 10% of the overall cost of power production, the managers believe that there is little to no demand destruction from higher pricing, which is why they consider that there is material further upside to come.

Capital growth from a diversified global portfolio of uranium stocks

GCL aims to provide investors with capital growth by investing in a portfolio of securities of companies involved in the exploration, development and production of energy, as well as related service companies. Its main focus is the uranium sector, but up to 30% of assets can be invested in other resource-related companies. These include, but are not limited to, shares, convertibles, fixed-income securities and warrants.

Fund profile

Diversified global uranium exposure

Further information can be found at: ncim.co.uk/geiger-counter-ltd.

GCL aims to provide investors with attractive returns, primarily in the form of capital growth, by investing in a portfolio of securities of companies involved in the exploration, development and production of energy and related service companies in the energy sector. Its main focus is uranium, but in order to allow for some diversification beyond this highly-concentrated sector, up to 30% of assets can be invested in other resource-related companies.

As discussed below, GCL does not have a formal benchmark and is not managed with the aim of providing outperformance relative to an index. Instead, the portfolio is managed with a more absolute return mindset, with the managers selecting the securities that they believe will provide the best risk-adjusted returns over the longer term. Although the managers consider uranium to benefit from long-term structural growth drivers, the portfolio is focused on securities that the manager has identified as being undervalued by the market. The expectation is that such securities will benefit from a re-rating over time, and therefore provide the scope for a capital appreciation beyond what the market expects.

GCL has a global remit, but its portfolio tends to be biased towards North American- and Australian-listed equities. The portfolio is predominantly invested in equities, but it is not restricted to these and can also invest in convertible securities, fixed-income securities and warrants.

CQS Group and New City Investment Managers

NCIM has managed GCL since its launch in July 2006.

New City Investment Managers (NCIM) has been GCL’s investment manager since its launch in July 2006. On 1 October 2007 NCIM joined the CQS Group, a global diversified asset manager running multiple strategies with AUM of US$13.5bn as at 31 October 2023. Keith Watson and Rob Crayfourd are responsible for the day-to-day management of GCL’s portfolio.

On 15 November 2023, CQS announced that it was being acquired by Manulife Investment Management, which has US$746bn in AUM. There are no planned changes to the investment management team. The deal is scheduled to close early next year, subject to regulatory approval.

No formal benchmark index

Reflecting both its specialist investment proposition and a relatively small universe, GCL does not have a formal benchmark. However, for the purpose of performance evaluation, the manager has traditionally made comparisons against the price of Cameco and the spot price of triuranium octoxide (U3O8 – the most stable uranium compound and consequently one of the more popular forms of the product).

This note includes comparisons against Cameco…

Cameco is the largest listed uranium producer in the world and the second-largest uranium producer globally. It also provides the processing services needed to produce fuel for nuclear power plants. Cameco has a Canadian listing and its share price and the associated total return series are readily available, so this has been included in this report.

Comparisons against the spot price of U3O8 have not been included in this note. Whilst a potentially useful comparator, visibility of the U3O8 spot price reduced dramatically from June 2017 onwards, making it much harder for market practitioners to observe and appears to have reduced its relevance. An additional concern regarding the validity of the U3O8 spot price, for the purposes of performance comparison, is that the majority of market practitioners cannot invest directly in this commodity.

… and the Global X Uranium ETF.

Finally, the Global X Uranium ETF (URA) has also been used as a comparator in this note. This is a reasonably large (net assets of around US$2.33bn) and liquid ETF that provides investors with access to a broad range of companies involved in uranium mining and the production of nuclear components (this includes companies involved in extraction, refining, exploration, or manufacturing of equipment for the uranium and nuclear industries). Its objective is to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the Solactive Global Uranium & Nuclear Components Total Return Index.

Market Outlook

Nuclear energy established in green strategies globally.

GCL’s managers state that a bull case for the uranium market has existed for at least a couple of years now, but multitudes of factors have aligned to make them more bullish on the prospects than for a long time. Having suffered from a decade-long bear market, following the Fukushima disaster in 2011, the uranium industry is now showing a marked shift in fortunes and sentiment, they add.

Nuclear energy appears to have been established in carbon emission reduction strategies across the world. Pro-nuclear governments – from the US, China, Japan and across Europe – have included nuclear power in green policy frameworks and have encouraged its growth through incentives. The resultant boost in global power production demand and for long-term supply contracts from utility companies has been combined with depleted stock levels and supply side issues in the uranium market.

The nuclear fuel supply chain begins with mining and milling uranium ore. This is then converted into uranium hexafluoride gas and then enriched and used in reactors to produce nuclear fuel.

Geopolitical events have curtailed supply.

Geopolitical events, such as the war in Ukraine and the military coup in Niger, have the potential to significantly curtail supply of uranium, while an anticipated long-term trend of increasing demand (see below) makes GCL’s managers very positive on the outlook for the sector.

Figure 1 shows that the uranium market has been in a supply deficit for an extended period of time – particularly so over the last three years where supply has met just 74%, 76% and 74% of global demand respectively. As a result of this supply and demand imbalance, the uranium spot price has spiked (as shown in Figure 4 on page 10 below), and GCL’s managers expect this to appreciate considerably further from here and lead to sustained higher pricing for uranium equities going forward.

We explore the influences on the supply and demand imbalance and the ramifications for the sector in more detail below, starting with demand.

Demand

Recognition by global governments of nuclear power’s role in reducing carbon emissions has been a major contributor to an increase in demand for uranium. As a result, an increasingly large number of long-term contracts have been signed to deliver U3O8 to reactors worldwide, the managers say.

Nuclear energy to provide 25% of global electricity by 2050 – from 10% today.

Nuclear power stations do not generate any carbon emissions in the production of electricity, unlike coal or gas power stations, and therefore are pivotal in global efforts to reach net zero, the managers believe. Intermittency of renewable energy sources, such as wind and solar which are dependent on the weather, as well as difficulties in finding a viable storage solution, mean that the importance of nuclear power in helping to provide clean, low-carbon electricity has grown, they add. Nuclear power plants generate energy 24 hours a day and are used extensively as baseload sources of electricity. Nuclear currently provides around 10% of electricity globally, with the aim of this growing to 25% by 2050.

Nuclear capacity forecast to expand nearly 80% and demand for uranium to double by 2040.

In an emissions sense, nuclear power is considered to be clean. It produces zero carbon emissions and doesn’t produce other greenhouse gases through its operation. The shift in political support for nuclear has been marked and the World Nuclear Association now forecasts nuclear capacity growing nearly 80% and demand for uranium roughly doubling by 2040.

In response to a change in policy, planned reactor decommissioning has also been deferred across the world (it appears that this is mainly in acknowledgment of the ability of reactors to operate safely for significantly longer than initially expected), typically adding around 20 years to the operating life.

61 reactors in construction, 112 planned and 318 proposed.

New reactors require significant fuel for an initial charge, and with 61 reactors currently under construction and a further 112 planned and 318 proposed (according to the World Nuclear Association), GCL’s managers expect that underlying uranium demand will rise by over 50m lbs (more than 3% per annum) by the end of the decade.

Figure 2 shows that total operable reactor net capacity in 2022 was 391.7GW, with 64.1GW currently under construction (across 61 projects) and 109.4GW planned (across 112). This leaves

![]()

The US

In the US – currently the largest nuclear power market – zero-emission credits and nuclear deployment incentives are now available to utilities under the Inflation Reduction Act, aimed at reducing US emissions by 40% within this decade. This builds on the Civil Nuclear Credit Program and legislation to fund a strategic fuel inventory.

US establishes strategic reserve for uranium to ween off dependence on Russia.

US legislation was passed in 2020 to establish a strategic reserve, with the purpose of moving away from dependence on Russia – around 20% of fuel used by the US nuclear reactor fleet is supplied through enrichment contracts with Russian suppliers. This is especially critical, the managers add, given that nuclear power will represent between 20% and 25% of the nation’s electricity.

The Biden administration has sought an extra $2.16bn from Congress to support a strategy to incentivise US-based companies to boost enrichment and conversion capacity. To work, this would also need long-term restrictions on Russian nuclear products and services to prevent Russia from dumping cheap enriched uranium products on world markets and undermining the US nuclear supply chain, the managers say.

A bill banning uranium imports from Russia is with the US Senate, having passed a sub-committee in the House of Representatives in May. The US is working closely with allies – Canada, France, Japan and the UK – to secure the supply chain and has begun funding some projects.

At the end of 2022, the US signed several long-term contracts with a number of US-based uranium companies to supply the newly formed US strategic reserves. It is supporting an expansion of capacity at an enrichment plant in New Mexico, owned by Urenco (a UK, German and Dutch consortium), which is scheduled for completion in 2027.

Between five to 10 contracts to build new reactors need to be signed within the next two to three years if the US were to meet its 2050 climate goals, according to Kathryn Huff, assistant secretary for nuclear energy.

China

China accelerated reactor build out programme and on course to be largest nuclear fuel consumer by 2030.

China has been accelerating the build-out of its nuclear power plant programme and is on course to replace the US as the largest nuclear fuel consumer by 2030 (according to the Oxford Institute for Energy Studies). It has indicated that it has the capacity to accelerate its reactor build-out from eight to 10 a year, while longer-term plans to build another 154 new domestic reactors by 2035 could see construction accelerate further.

![]()

Japan

Japan has revived its nuclear fleet.

Japan is looking to revive its nuclear restart programme and has received local state backing. GCL’s managers say that momentum is gathering pace in this regard after completion of more stringent reactor upgrades. The first two reactors to restart after the Fukushima disaster in 2011 did so in 2015. Since then, a further nine have restarted, and another 14 operable reactors are at various stages in the process of restart approval. Two under-construction reactors (Ohma and Shimane 3) have also applied for approval. The country has set an objective to raise the share of nuclear power to at least 20% by 2030 (it accounted for around 7.5% in 2019).

Europe

Nuclear power included in EU Taxonomy.

In Europe, nuclear power was included in the list of environmentally sustainable economic activities covered by the EU Taxonomy, which determines whether an economic activity is considered environmentally sustainable and helps guide private investment. The EU’s recognition of nuclear as an environmentally sustainable economic activity should garner further support from member governments and attract cheaper debt financing options for building new and extending the life of existing nuclear reactors, the managers contend. This is the case in France, where it has scheduled the return of 20% of its nuclear capacity, after a further round of safety system checks is completed later this year.

The UK

UK ambition for 25% of electricity to come from nuclear power by 2050.

The UK government has ambitions for up to a quarter of all UK electricity to come from nuclear power by 2050 and is backing the roll-out of small modular reactors (SMRs). In 2024 it will award contracts to companies to bring forward a fleet of SMRs to be operational by the mid-2030s. As well as backing SMRs, the government is also investing in the large-scale project at Sizewell C, a near-exact replica of Hinkley Point C nuclear power plant.

Supply

Uranium is reasonably abundant within the earth’s crust and, whilst it may require additional permitting and be subject to additional regulation when compared to other commodities, it is not technically difficult to mine. Uranium processing is heavily regulated, but mining permitting is not unduly onerous. However, uranium production is highly concentrated; the top five producers collectively control around 60% of production, while the top 10 account for around 85%. Furthermore, around 48% of production is located in regions of geopolitical risk (primarily Kazakhstan and Russia).

Concentrated market is vulnerable to supply-side shocks – including Russia/Kazakhstan.

The concentration of production in specific regions, companies and mines leaves the uranium market vulnerable to supply-side shocks, the managers say. The recent energy crisis, brought on by Russia’s invasion of Ukraine, highlighted an over-reliance on Russian and Kazakh-origin fuel by established markets. Kazakhstan controls over 40% of global uranium mining and supplies the West through a route through Russia. After the outbreak of war in 2022, an alternative route through the Caspian Sea and Azerbaijan was established but has proved difficult to get to work, and may result in Kazakhstan abandoning supply to the West and sending the material to China instead. This is a significant loss of supply to the West, the managers say, and one which may not return.

Russia itself controls almost 50% of the uranium enrichment market. As mentioned earlier, while there are no formal sanctions against using fuel sourced from Russia, governments and utilities appear increasingly focused on the need to diversify supply away from Russia and seek surer sources of supply, which the managers say will mainly come from North American companies. To overcome a potential lack of access to enrichment in the short term, the process of generating nuclear power can be altered to be more front-loaded with greater use of natural uranium, according to the managers.

The military coup in Niger earlier this year has added to the supply side complexities. Niger is the world’s seventh-largest producer of uranium, possesses Africa’s highest-grade uranium ores, and is the second-largest raw uranium exporter to the EU (accounting for up to a quarter of supplies, with France a major importer). Even though the junta has not banned uranium trade with the bloc, concerns have grown about access to Niger’s uranium.

Other supply-side issues include:

- Downstream bottlenecks in the fuel cycle, particularly conversion, in which uranium is converted from a solid “yellowcake” form into a gaseous “hexafluoride” state. This is slowly being eased with facilities in France and the US being ramped up to increase capacity of this conversion process. The managers say that further capacity expansion will be required beyond this.

- Cameco, one of the world’s largest uranium producers and publicly traded uranium companies, has all of its production contracted out for five years.

Uranium spot price expected to appreciate further

Uranium spot price up 56% in 2023 to a 12-year high.

Overcoming the supply side issues and building out new fleets of nuclear reactors is an extremely slow process, leading the managers to conclude that the supply and demand imbalance will persist for many years. The impact of this is a sustained, elevated uranium spot price, they add. Figure 4 shows that the spot price has climbed 56% so far this year, and 24% since August 2023, to a 12-year high.

Uranium prices have risen and fallen in tandem with shifts in global nuclear policy. During the 2000s, uranium climbed to $136 per pound in 2007. However, the Fukushima Daiichi meltdowns in 2011 left uranium hovering around $20 to $40 for more than a decade.

Although there is a mounting pressure to address the future deficit between supply and demand, a further step up in price from current levels will be needed to incentivise a significant uplift in supply, the managers contend.

Nuclear power plants are high-capital expenditure, long-term investments, with uranium supply typically tied to long-term contracts. Given this, and the fact that nuclear power stations are expensive to ramp up and down, demand for uranium tends to be price-inelastic, at least in the short to medium term.

The managers say that the uranium spot price makes up around 5% of the overall cost in the production of nuclear power. This means that material increases in the spot price are manageable for utilities. The managers say that a tripling of the price would not have an impact on demand from utilities and would still be competitive compared to other fuels.

As mentioned earlier, life extensions of existing reactors have increased globally while a roll-out of small modular reactors (SMRs) is a feasible route to increasing capacity, the managers say. This is the case in the UK, where SMRs are set to become a major part of the government’s ambition for up to a quarter of all UK electricity to come from nuclear power by 2050.

Unlike conventional nuclear reactors that are built on site, SMRs are smaller and can be made in factories – which may make construction faster and less expensive. The UK aims to have a fleet of SMRs operational by the mid-2030s. These are likely to be located on the sites of existing reactors that already have most, if not all, of the necessary infrastructure, which could make their roll-out easier to implement.

Investment process

Bulk of managers’ efforts focused on fundamental analysis.

The team at CQS New City manages its portfolios using a mixture of top-down and bottom-up investment strategies, although, reflecting the concentrated nature of its universe, the bulk of the managers’ efforts are focused on fundamental analysis of the risk and return prospects for potential and existing investments. The portfolio is primarily invested in equity securities, but the managers will consider other instruments where they feel these are appropriate.

Although GCL has a significant exposure to physically-backed uranium entities, its primary focus is on companies that the managers believe will offer strong returns at a U3O8 price in the range of US$45/lb to US$50/lb. The managers feel that prices above this will incentivise some mines to restart leading to a steep increase in supply. However, there is also a tail of higher-cost projects that will offer operational leverage as the uranium price increases.

CQS New City team meets an average of 20 resource related companies a week.

As a recognised investor in the natural resources space, the CQS New City team meets an average of 20 resource-related companies a week. The team employs a range of metrics to try and identify undervalued assets, which vary depending on the type of investment (for example, fixed income versus equities) but the team seeks to identify assets that offer superior returns relative to their risk. These will frequently have the potential for capital growth through a rerating of a security. The managers’ analysis, which is conducted in-house, includes assessments of the following:

- The quality of a company’s projects – are the projects in mining-friendly jurisdictions? Do the projects have high-quality deposits? Are there appropriate transport links as well as access to the necessary processing facilities?

- The quality of a company’s management – does the management team have a good track record in developing or managing similar projects? Do they have experience of operating in the relevant mining jurisdiction? Does management have a good track record in managing its obligations? Does management have a strong corporate governance record as well as a record of treating shareholders fairly?

- The free cashflow available from projects and how these flow to the various security holders within a corporate’s capital structure (for example, equity holders, debt holders, preferred stock holders and convertible security holders); and

- The prospect of changes to cashflows (for example, from changes in interest rates or the competitive landscape).

Macro analysis guides managers research efforts

The macro element of the investment process begins with an assessment of the factors driving global demand and supply for uranium. This considers supply-side factors such as exploration success, capacity developments, potential for supply disruptions and technological developments. It also considers demand-side factors such as new applications, the potential for substitution, and technological developments.

Emphasis placed on developments in large industrialising emerging markets, that have significant programmes to develop nuclear power stations.

The managers look at demand from developed markets, but particular emphasis is placed on developments in the large industrialising emerging markets, as these (China being an example) have significant programmes to develop nuclear power stations and are expected to be the major source of new demand for uranium in coming years (emerging and frontier markets energy demands tend to increase dramatically as they develop). The analysis also takes into consideration inventory levels and how these might develop. This allows the managers to identify areas (for example, sub-sectors and geographies) to focus their attention on when conducting their bottom-up analysis of potential investments.

Portfolio construction – unconstrained by benchmark

It should be noted that GCL’s portfolio is not managed with reference to any benchmark and, whilst the macro overlay acts as a guide by directing the managers’ research efforts, it does not provide specific targets for the geographic and sectoral allocations. Instead, these are a result of the managers’ stock selection decisions, which reflect their assessment of the relative strength of individual investment ideas.

Managers can draw on expertise of wider CQS New City team.

The managers, Keith Watson and Robert Crayfourd, make the final decision on what enters GCL’s portfolio, but they are able to draw on the expertise of the wider CQS New City team. Once included in the portfolio, the managers continue to assess stocks to ascertain whether the level remains appropriate.

Investment restrictions

- GCL’s main focus is on companies involved in the uranium industry, but up to 30% of gross assets may be invested in other resource-related companies.

- GCL does not have a specific gearing limit. Instead, the board sets borrowing limits, which it reviews regularly to ensure that gearing levels are appropriate to market conditions.

Asset allocation

GCL’s portfolio is highly concentrated.

As at 30 September 2023, GCL’s portfolio had exposure to 42 issues, in line with the 42 issues as at 31 March 2023 (six months prior). GCL’s portfolio is highly concentrated, with the top five holdings accounting for around 63.0% of the fund (see Figure 7).

GCL’s portfolio is inherently low turnover.

In part reflecting the managers’ investment style, but also the concentrated nature of the industry (10 producers control around 85% of supply between them), GCL’s portfolio is inherently low-turnover. Changes in the composition of the top five holdings (discussed in more detail below) are frequently driven by differences in near-term relative performance, rather than other considerations. The managers typically expect portfolio turnover to be around 10% per annum, but much of this will be trimming stocks whose prices have got ahead of themselves, and adding to holdings where the managers see more value.

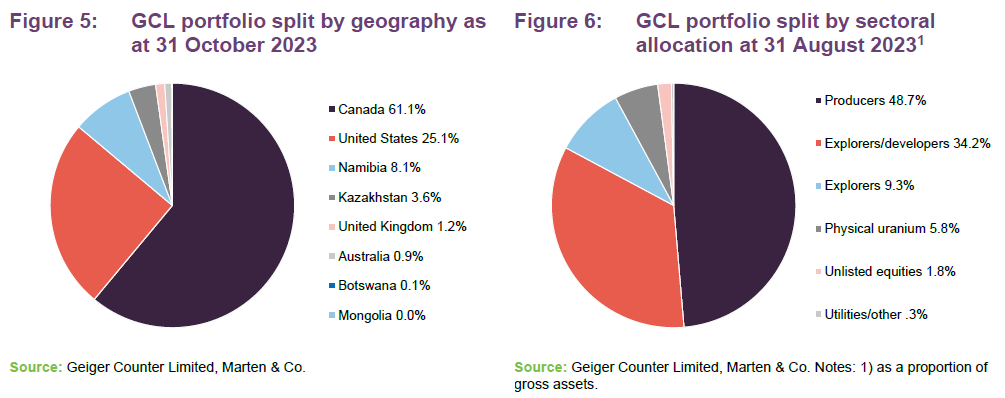

Figures 5 and 6 show the portfolio’s geographical allocation and sectoral allocations as at 31 October 2023 and 31 August 2023 respectively (this being the most recent publicly available data). These highlight a number of themes:

- Whilst GCL has a global mandate, it is focused on companies in North America with low contract coverage, which the managers say gives them maximum price participation in to a stronger pricing environment. North America is viewed by the managers as a politically safer region that has “extractable pounds”; that is, it has good geology and mining-friendly environments.

- Over half of GCL’s portfolio is invested in what the managers believe are safer assets; that is, producers or companies backed by physical uranium.

- Pure exploration plays are a limited component of the portfolio.

As at 31 March 2023, GCL had three unlisted investments, which were valued in total at £1.76m and accounted for 3.2% of its net assets. It also held two unlisted warrants, which were valued at just £73,000 in total.

GCL has a significant exposure to physically-backed uranium entities through its holdings in Sprott Uranium Trust (5.5% at 31 March 2023) and Yellow Cake Plc (1.4%). However, in comparison to alternatives such as the URA exchange traded fund (ETF), GCL is relatively underweight Cameco and Kazatomprom.

Top five holdings

Figure 7 shows GCL’s top five holdings as at 31 October 2023 and how these have changed since over six months.

Uranium Energy has moved up to the top five holdings.

In terms of movements in and out of the top five over the past six months, Uranium Energy has moved up into the top five, while Fission Uranium has moved out. Reflecting both the concentrated nature of the uranium sector and the manager’s long-term, low-turnover approach, the names in the top five portfolio holdings will be familiar to regular followers of GCL’s portfolio announcements and our notes on the company. Some commentary on the largest holdings are presented in the next few pages. Readers interested in other names in GCL’s portfolio should see our previous notes, where many of these have been discussed (see page 27 of this note for links).

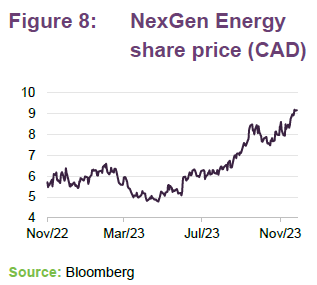

NexGen Energy (21.5%)

NexGen Energy (www.nexgenenergy.ca) has been GCL’s largest holding, by a significant margin, for some time. It is a uranium exploration and development company with a portfolio of projects that are centred on the Athabasca Basin in Canada, where it holds over 259k hectares of land. NexGen’s southwestern Athabasca Rook 1 property hosts the Arrow Deposit, the South Arrow discovery, the Harpoon discovery, the Bow discovery and the Cannon area. All of these are 100% owned by NexGen.

As illustrated in Figure 8, NexGen’s share price has performed very strongly since the end of May 2023 and is up 53.1% over the year to 27 November 2023. GCL’s managers remain very positive on the outlook for NexGen, which remains a core holding. GCL’s managers like NexGen’s assets, its management team and its financial strength.

Earlier this month, NexGen received approval to proceed with the development of its Rook I uranium project in Saskatchewan, Canada. It is the first company in more than 20 years to receive full Provincial Environmental Assessment approval for a uranium project in the province. The Arrow uranium deposit has measured and indicated mineral resources of 256.7m pounds U3O8 supporting an initial 10.7 year mine-life. Applications have been lodged for approvals of site earthworks, shaft sinking infrastructure, site water and mine waste management facilities.

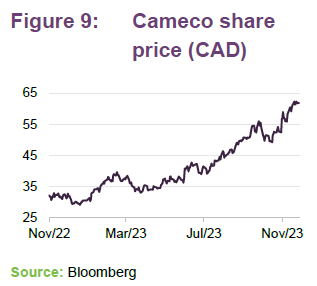

Cameco (13.1%)

Cameco (www.cameco.com), the world’s largest publicly traded uranium company, is GCL’s second-largest holding. It has been one of GCL’s largest underweight positions relative to the URA ETF, which had a 24.4% exposure to Cameco at

27 November 2023. Cameco’s land holdings, including exploration, span about 1.9 million acres, the majority of which are located in northern Saskatchewan, at the Athabasca Basin. It is home to two of the world’s largest high-grade uranium deposits, in Cigar Lake and McArthur River/Key Lake.

Cameco has the licensed capacity to produce more than 30 million pounds of uranium concentrates annually, backed by more than 469 million pounds of proven and probable mineral reserves.

As mentioned earlier, the company is contracted out for the next five years, meaning that it will see very little benefit from a surge in the uranium spot price. In its third quarter results, Cameco updated expectations for its full year realised price of CAD$63.50/lb, or around US$47/lb. This compares to the spot uranium price in excess of US$70/lb at the end of the quarter. This, the managers say, is indicative of the drag effect of prior forward sales contract terms on its uranium mining revenues.

Nevertheless, the company has performed very strongly in recent years, as shown in Figure 9, and has driven the recent NAV performance in GCL. The managers believe that Cameco’s market leading position in the sector justifies its position and weighting within the portfolio.

On 7 November 2023, Cameco acquired Westinghouse Electric Company, one of the world’s largest nuclear services businesses, in partnership with Brookfield Renewable Partners (Cameco 49%, Brookfield 51%) for a total enterprise value of $8.2bn. Westinghouse provides nuclear plant technologies, products and services, which should leave it well-positioned for the increasing need for secure, reliable and emissions-free baseload power. The managers point to Westinghouse’s position as a supplier for certified VVER (water-water energetic reactor) fuel assemblies (one of only a very small number of non-Russian alternatives) as a major growth opportunity for the business as countries seek to develop a reliable fuel supply chain independent of Russia.

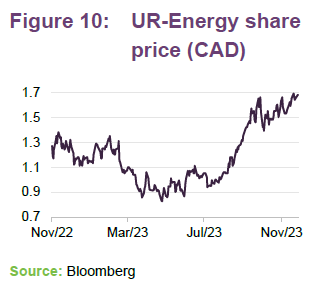

UR-Energy (12.9%)

Long-time GCL holding UR-Energy (www.ur-energy.com) is a junior uranium mining company that operates an in-situ uranium recovery facility at its Lost Creek property in south-central Wyoming. It also owns the Shirley Basin and Lucky Mc mine sites in the Shirley Basin and Gas Hills mining districts of Wyoming. The company’s tailings facility at the Shirley Basin site is also one of the few remaining facilities in the United States that is licensed by the US Nuclear Regulatory Commission (NRC) to receive and dispose of by-product waste material from other in-situ uranium mines.

UR-Energy’s share price has performed very strongly over the last two years, benefitting both from US government support for the nuclear sector, as detailed earlier, as well as its intention to create a strategic inventory of uranium and related services. GCL’s managers continue to like the company, which they say has decent quality assets and a proven operational record, with one of the cheapest costs of production of uranium per pound in the sector.

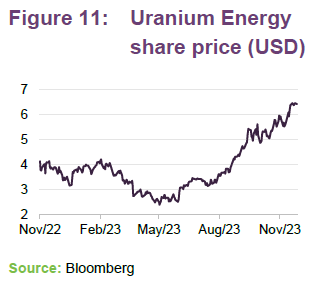

Uranium Energy (7.9%)

Uranium Energy (www.uraniumenergy.com) has an extensive portfolio of in-situ recovery (ISR) mining uranium projects in the US, as well as conventional projects in Canada. ISR technology uses fluid to recover uranium from the ground without digging and moving tonnes of earth. The company has two production-ready ISR hub and spoke platforms in South Texas and Wyoming, anchored by central processing plants. It has further fully permitted ISR uranium projects across the US.

The managers say that the company is set to benefit from an uplift in contracting by US and Western utilities, being one of a very few sources of contract supply in projects that can deliver in a two-to-three-year timeframe.

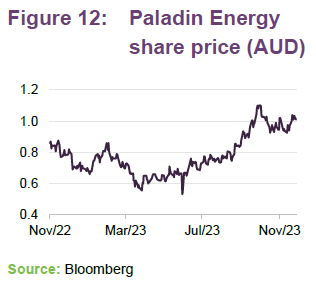

Paladin Energy (7.6%)

Paladin Energy (www.paladinenergy.com.au) is a Western Australian-based uranium production company that currently has one operating mine – the Langer Heinrich Mine in Namibia (which it owns 75%). At full production, the Langer Heinrich Mine’s annual uranium output is enough to supply more than 10 1,000-Mwe nuclear power plants for a year. The mine has already produced over 43 million pounds of U3O8 over 10 years.

The managers say that Namibia is one of the most stable countries politically in Africa and the most reliable to trade with. The mine is returning to strong production with first volumes targeted for the first quarter of 2024, with the company projecting production of over 77 million pounds of U3O8 in the future. The managers add that the company has meaningful capacity, being around 50% contracted, and can benefit from the uptick in the spot price of uranium. Its prior contracts have upside potential too, the managers say, with price linkage to the industrial production price index. Paladin also holds a portfolio of exploration and development facilities in Canada and Australia.

Performance

GCL and the broader uranium market have performed strongly since early 2021 as nuclear energy appears to have become a cornerstone of green agendas around the world. At the same time, supply side concerns have grown (as detailed earlier), putting pressure on the price of uranium and driving returns in the sector. The managers believe that further upside can be expected as governments step up their efforts to decarbonise, and forecast additional growth in the price of uranium will be needed to incentivise an uplift in supply.

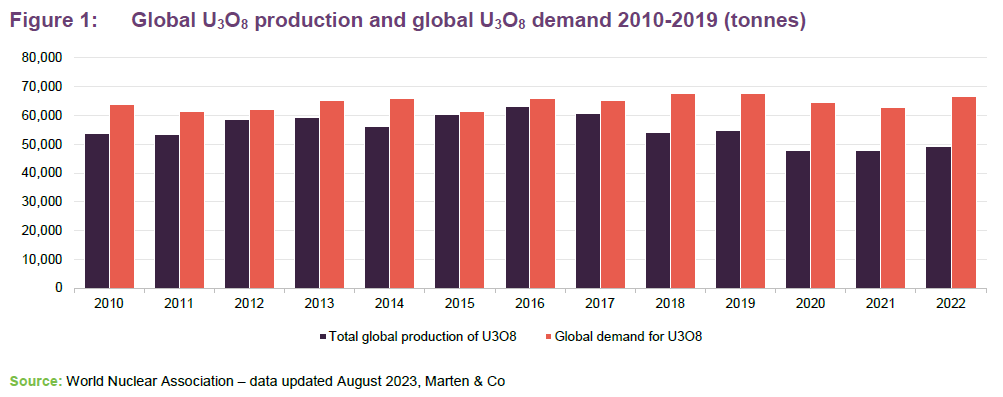

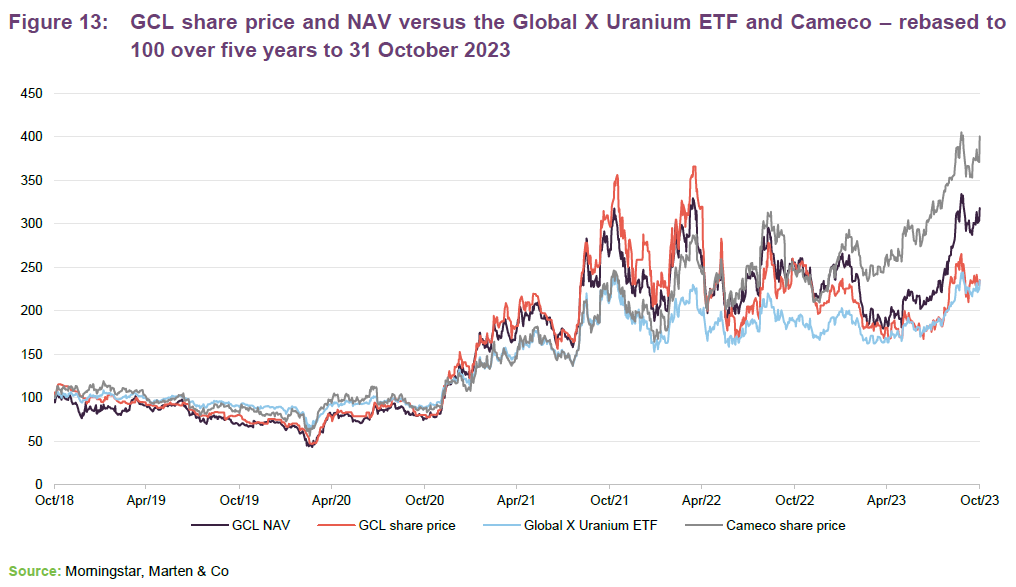

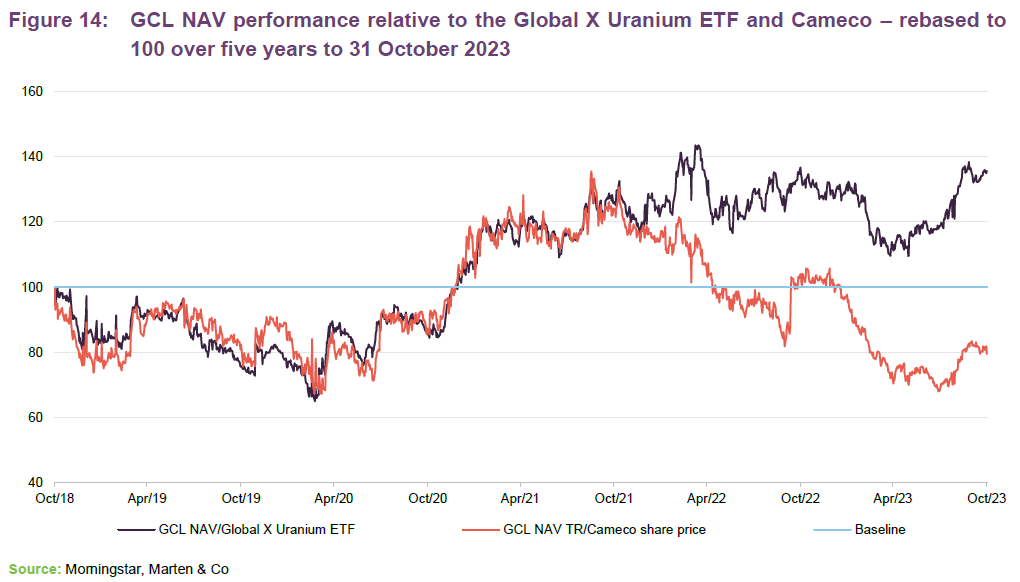

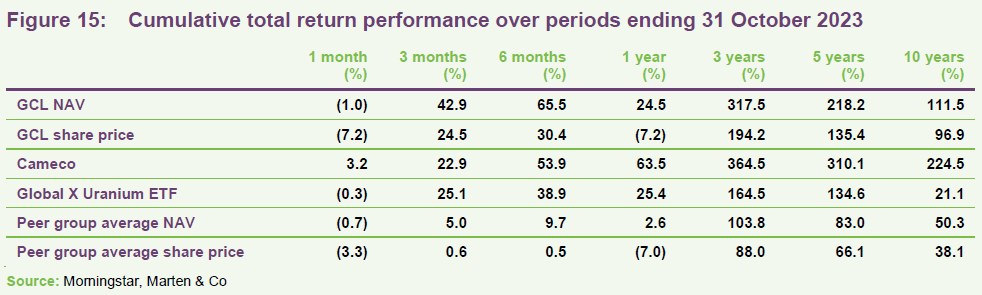

As illustrated in Figure 13, GCL has comfortably outperformed the URA ETF in NAV terms. This is despite the company being underweight relative to the ETF in Cameco, which has seen a substantial bounce in its share price over the last year. Figure 14 and 15 display the impact of the decade long bear market in uranium following the Fukushima in 2011, with its impact noticeable in the longer-term numbers.

GCL’s share price has consistently outperformed the Global X Uranium ETF over the longer-term period of three, five and 10 years. More recently, its share price has lagged the ETF, as shown in Figure 15. GCL’s recent NAV performance has been driven by Cameco, although NexGen Energy (GCL’s largest holding) has also been a strong positive contributor and the managers believe there is more to come from NexGen and UR Energy.

Figure 14 also illustrates GCL’s strong NAV performance relative to the URA ETF from early 2021. Its performance relative to Cameco diverged at the start of 2022 as Cameco’s share price took off. Cameco as the blue-chip Uranium name has been a go-to for generalist investors, the managers say, supporting the strong gains it has seen, but it now trades at a notable premium to the sector. This was even more apparent since Russia’s invasion of Ukraine in early 2022 as the supply shocks impacted Kazakhstan (as mentioned earlier) and Kazatomprom (another go-to uranium stock).

Peer group

GCL is a member of the AIC’s sector specialist commodities and natural resources sector, which is comprised of nine members. Eight of these are illustrated in Figures 18 through 20. However, for the purposes of this peer group analysis, we have excluded Global Resources Investment Trust (GRIT) and Tiger Royalties and Investments (TIR) on size grounds (both sub-£5m market cap).

Click here for a live comparison of the commodities and natural resources peer group.

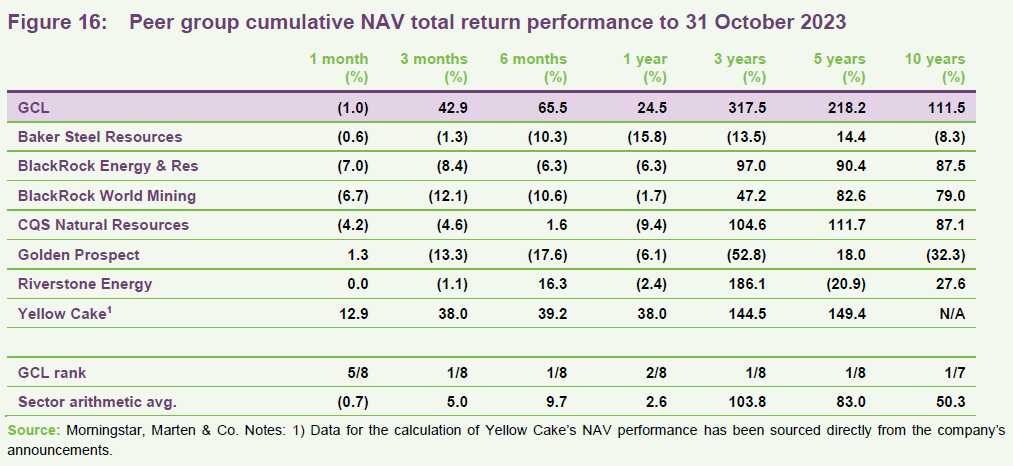

Whilst they are all members of the commodities and natural resources sector, the funds used in this peer group comparison are quite diverse, and GCL is unique as it is the only fund that invests in listed uranium equities. There is one other fund, Yellow Cake Plc (YCA), that is focused on uranium, but it invests in physical uranium (as discussed below). It should be noted that unlike GCL, which publishes daily NAVs, YCA tends to publish a NAV figure once a month. As such, there is greater uncertainty around its NAV performance versus that of the remainder of the peer group.

Within the wider peer group, GCL and YCA are not the only funds with a narrow focus. For example, Golden Prospect Precious Metals is focused on gold; Riverstone Energy has a concentrated portfolio of energy companies that are primarily engaged in oil exploration and production; and the BlackRock funds are both primarily invested in larger-cap stocks. As such, none of the funds used are perfect comparators for GCL.

Figure 16 shows that GCL’s NAV has consistently, and by some margin, outperformed its peer group over all long-term time periods. This is despite the longer-term numbers reflecting the 10-year bear market in uranium that was accelerated by the Fukushima disaster. Its recent strong performance (one year and below – excluding one-month) has only been matched by YCA.

YCA was established to purchase and hold triuranium octoxide (this is held in a storage account at Cameco’s Port Hope/Blind River facility in Ontario, Canada). It aims to provide investors with exposure to the uranium price and to exploit a range of opportunities offered by holding physical uranium.

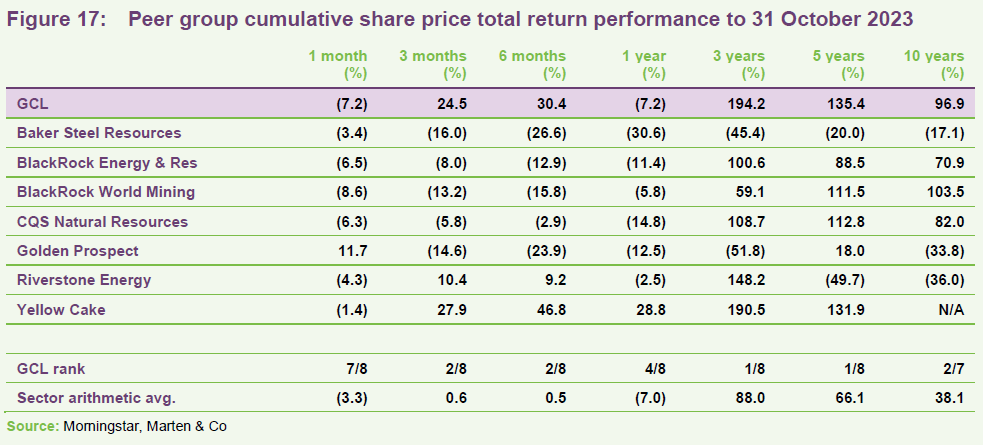

GCL has also been one of the best-performing funds in the peer group in terms of share price total return. A similar pattern to its NAV performance is witnessed in share price total return, albeit the returns are slightly different, reflecting the relative movements in the premium/(discount) over the individual periods.

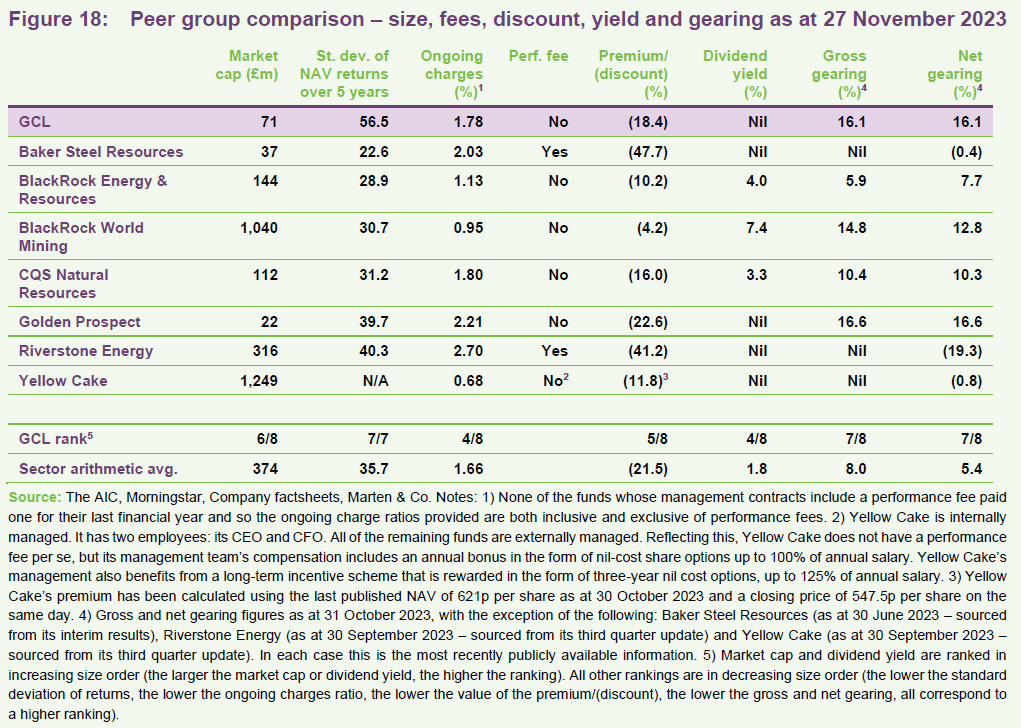

The volatility of GCL’s NAV returns is the highest within the peer group, perhaps reflecting the fact that it has a more concentrated portfolio than a number of the funds in the peer group, as well as having a narrow focus.

GCL has the highest ongoing charges ratio in its peer group. This does in part reflect its relatively small size. GCL does not pay a performance fee. GCL does not pay a dividend, while its net gearing is above the sector averages. This means that, all things being equal, it should benefit if uranium continues to perform well, but should suffer disproportionately if not.

Of the two uranium funds, GCL is the more expensive, but GCL has both a much longer track record and a much stronger performance record, although YCA is larger and has greater liquidity.

No dividend – capital growth focused

GCL’s investment objective is to achieve returns primarily through capital growth. Therefore, GCL does not have a formal dividend policy and has not paid a dividend since its launch. The investment objective and dividend policy are both a reflection of GCL’s underlying investments. Traditionally, commodities and natural resources have been among the lower-yielding sectors. These industries are capital-intensive, and companies have frequently retained a high proportion of earnings for reinvestment in the business, rather than returning cash to shareholders. In addition, where GCL holds physical commodities, these do not pay dividends. The combined effect is that GCL’s dividend income tends to be a relatively small component of its total return. GCL’s accumulated revenue reserve has been growing in recent years and at 31 March 2023 was just under £2.3m, equivalent to 1.7p per share.

Premium/(discount)

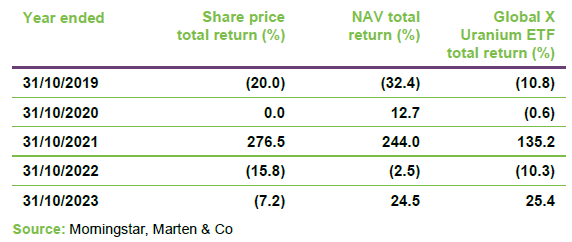

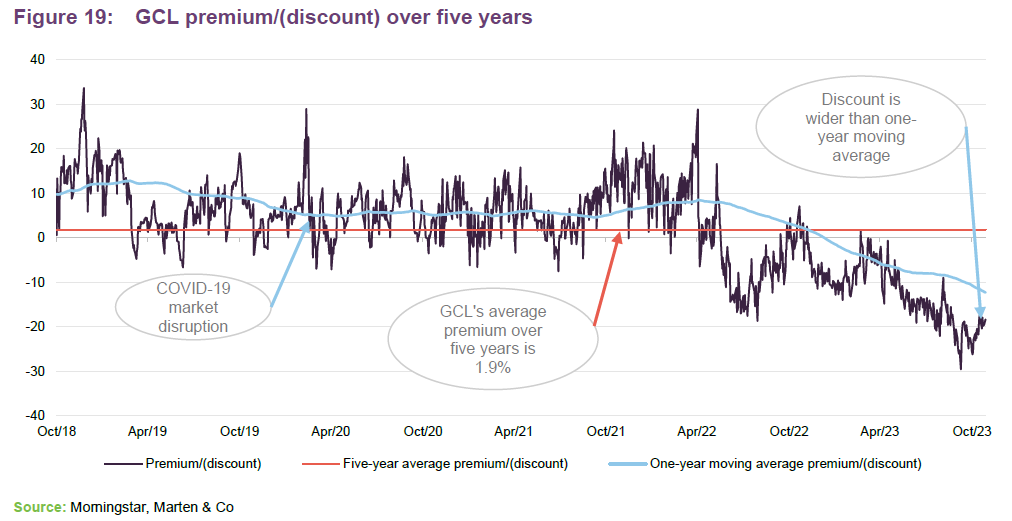

GCL has traded at an average discount of 12.2% over one year.

GCL has moved from trading at a premium (albeit with marked volatility) to a substantial discount as the company’s strong NAV performance has not been reflected in its share price. Over the last year, GCL has traded at an average discount of 12.2% and on 27 November 2023 its discount had widened to 19.9%. This is at the cheaper end of its trading range over five years (1.9% average premium, with a range of a 33.7% premium to a 29.6% discount) and three years (1.5% average discount).

GCL does not have an explicit discount management policy, but it is authorised to repurchase up to 14.99% and allot up to 10% of its issued share capital, which gives the board a mechanism with which it can influence the premium/discount. Any shares repurchased may be cancelled or held in treasury and later resold.

During October 2023, the company repurchased 2,893,000 shares to be held in treasury for a total of £1.37m, at an average price of 47.4p. This represents 2.15% of the issued share capital. The share purchases were made with a view to reducing discount volatility and are accretive for shareholders.

Fees and costs

Under the terms of the investment management agreement, CQS is entitled to receive a basic management fee of 1.375% per annum of net assets (after adding back any bank borrowings). The management fee is calculated and paid monthly in arrears and the company valued monthly, with assets valued using mid-market prices.

GCL’s management agreement can be terminated on 12 months’ notice by either side.

Fund administration services

GCL has an agreement with R&H Fund Services (Jersey) Limited for R&H to provide administrative, compliance oversight and company secretarial services to GCL.

From 1 January 2022, the fund administration fee increased to £140,000 per annum. Previously, the fund administration fee had been calculated as 0.1% of gross assets up to £50m and 0.075% of gross assets in excess of £50m, with an overall minimum fee of £75,000 per annum and an overall maximum fee of £115,000 per annum. R&H’s total fees for the year ended 30 September 2022 were £123,616 (2021: £74,948).

Allocation of fees and costs

The investment management fee, finance costs and costs incurred in relation to the disposal of investments are charged wholly to capital. All other expenses are charged wholly to revenue. The ongoing charges ratio for the year ended 30 September 2022 has been estimated at 1.78% (2021: 2.03%).

Capital structure and life

GCL has a simple capital structure consisting of ordinary shares only (of nil par value). As at 27 November 2023, there were 131,646,251 ordinary shares in issue. As at the same date, there were 2,897,902 ordinary shares held in treasury.

Subscription right mechanism

Shareholders approved an annual subscription right document at an EGM in 2021 that enables shareholders to subscribe for one new ordinary share for every five ordinary shares held on 30 April every year at a price equal to the undiluted NAV per share on 1 May one year prior. On 5 May 2022, the company raised £6.73m after shareholders subscribed for 17,796,176 new ordinary shares at a price of 37.84p per share.

The exercise date for the second subscription right was 2 May 2023. The price was 51.52p per share and applications for 70,655 new ordinary shares were received. However, the board determined that due to the company’s share price at the time (39.0p) it was not in the best interests of the company to issue the new shares. The third subscription rights price is 37.74p per share and the exercise date is 30 April 2024.

Shareholders will have the opportunity to review the subscription right mechanism at the company’s AGM in 2026, and at every fifth subsequent AGM thereafter, where an ordinary resolution will be proposed for the continuation of the subscription right mechanism.

Gearing

GCL is permitted to borrow and has a credit facility with BNP Paribas that incurs interest on any amounts borrowed at the SONIA overnight rate plus 83bps. The facility is flexible, allowing the managers to move money on and off the table when they consider it to be appropriate. The company is restricted by its prospectus to a maximum gearing level of 35%. GCL’s net gearing at 31 October 2023 was 16.1%.

Unlimited life with an annual continuation vote

GCL does not have a fixed winding-up date, but at each annual general meeting (AGM), shareholders are given the opportunity to vote on the continuation of the company. This is an ordinary resolution. If this resolution is not passed, the board is required to put forward proposals to shareholders within four months, to liquidate or otherwise reconstruct or reorganise the company.

Major shareholders

As at 31 March 2023, one shareholder held more than 10% of GCL’s ordinary shares – Hargreaves Lansdown Asset Management – which owned 20.57% of the company.

Financial calendar

The trust’s year-end is 30 September. The annual results are usually released in December (interims in June) and its AGMs are usually held in March of each year.

Corporate history

GCL is a Jersey-domiciled closed-ended investment company incorporated on 6 June 2006. It listed on the International Stock Exchange (formerly the Channel Islands Stock Exchange) on 7 July 2006 and trades on the London Stock Exchange SETS QX Electronic Trading Service (GCL was admitted to trading on the LSE on 10 July 2006).

Management team

GCL is co-managed by Keith Watson and Rob Crayfourd. Keith and Rob are able to draw on the expertise of the wider team at CQS. This includes Ian “Franco” Francis, who with over 35 years’ investment experience – primarily in the fixed interest and convertible spheres – can assist with the small number of fixed income investments that GCL may hold from time to time (Ian manages the CQS New City High Yield Fund). Ian, Keith and Rob also manage CQS Natural Resources Growth & Income Plc.

Keith Watson

Keith joined the NCIM team in 2013, initially as a dedicated natural resources analyst. Prior to NCIM, he worked for Mirabaud Securities, where he was a senior natural resource analyst; Evolution Securities, where he was director of mining research; Dresdner Kleinwort Wasserstein, where he was a top-ranked business services analyst; Commerzbank; and Credit Suisse/BZW. Keith began his career in 1992 as a portfolio manager and research analyst at Scottish Amicable Investment Managers. He has a BSc (Hons) in Applied Physics from Durham University.

Rob Crayfourd

Rob joined the NCIM team in 2011. He has 20 years’ experience of investing in resources, having previously worked for the Universities Superannuation Scheme and HSBC Global Asset Management, where he focused on the resources sector. Rob holds a BSc in Geological Sciences from the University of Leeds and is a CFA charterholder.

Board

GCL’s board comprises three directors, all of whom are non-executive and considered to be independent of the investment manager. Other than GCL’s board, its directors do not have any other shared directorships. Board policy is that all of GCL’s board members retire and offer themselves for re-election annually. GCL’s articles of association limit the maximum remuneration for directors to £30,000 per director per annum.

Ian Reeves CBE (chairman)

Ian has many years of boardroom experience and holds several director roles. He was formerly chairman of GCP Infrastructure Investments Limited until October 2022, and is currently senior independent director of Triple Point Social Housing REIT PLC and chairman of The Estates and Infrastructure Exchange (EIE). Ian is chief executive and co-founder of Synaps International Ltd, an international business advisory firm. Ian is visiting professor of infrastructure investment and construction at The Alliance Manchester Business School. He founded and chaired High-Point Rendel Group PLC, a management and engineering consultancy company, and has been president and chief executive of Cleveland Bridge, chairman of McGee Group, chairman of Constructing Excellence and chairman of the London regional council of the CBI. Ian was awarded a CBE in 2003 for services to business and charity.

Gary Clark (chairman of the audit and risk committee)

Gary is a chartered accountant with considerable experience in the investment fund industry. He is a non-executive director on a number of boards that cover investment funds, fund managers and investment management for a variety of financial services businesses. These include Emirates, Standard Life Aberdeen, Blackstone and ICG.

Gary served as chairman of the Jersey Fund Association from 2004 to 2007 and was managing director at AIB Fund Administrators Limited when it was acquired by Mourant in 2006. This business was sold to State Street in 2010, and until 1 March 2011, Gary was a managing director at State Street and their head of hedge fund services in the Channel Islands. Prior to his time at State Street, he was managing director of the futures broker GNI (Channel Islands) Limited in Jersey.

Gary was one of a number of practitioners involved in a number of significant changes to the regulatory regime for funds in Jersey. This included the move to function-based regulation and introduction of both Jersey’s expert funds and unregulated funds regimes. Gary is resident in Jersey. He graduated with a degree in mining engineering from Nottingham University in 1986.

James Leahy (director)

James has over 30 years’ experience in the mining sector as a senior mining analyst and as a specialist corporate broker with expertise in international institutional and hedge funds, foreign capital and private equity markets. He has previously worked at James Capel, Credit Lyonnais, Nedbank and Canaccord, and he was the founding partner of Mirabaud Securities. During his career, James has raised funds for a wide range of projects worldwide that include industrial minerals, precious metals, copper, diamonds, coal, iron ore, uranium and lithium (he was involved in more than 30 IPOs and a large number of primary and secondary placings).

Since 2010, James has been a director of a number of mining and exploration companies. His former roles include: non-executive director of Continental Coal Limited (between May 2011 and July 2013); a director of African Power Corporation (between May 2011 and May 2014); non-executive director of Bacanora Lithium Plc (between July 2011 and May 2017 – this also included a stint as interim chairman between July and November 2016); non-executive director of Forte Energy NL (between April 2012 and August 2015); non-executive director of BOS GLOBAL Holdings Limited (between April 2012 and August 2015); independent non-executive director of Mineral Commodities Limited (between December 2012 and May 2015); and independent non-executive director of Bellzone Mining Plc (Between November 2014 and May 2015).

James, a UK resident, has been a member of the advisory board at Aton Resources Inc since October 2015 and is a director of a private start-up, Energy Minerals Investments Ltd.

Previous publications

Readers interested in further information about GCL may wish to read our previous notes (details are provided in Figure 21 below). You can read the notes by clicking on the links or by visiting our website.

Figure 21: QuotedData’s previously published notes on GCL

| Title | Note type | |

| Nuclear exposure | Initiation | 20 March 2019 |

| Supply deficit unsustainable | Update | 21 November 2019 |

| Hot stuff | Annual overview | 6 August 2020 |

| Explosive performance | Update | 21 October 2021 |

Source: Marten & Co

Legal

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Geiger Counter Limited Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it, but in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.