Herald Investment Trust

Investment companies | Update | 13 November 2023

Patience and power

Herald Investment Trust (HRI) demonstrates why patience can be key when it comes to investing. The managers highlight the drought of funding available to small cap technology stocks. The team has ensured that HRI has sufficient liquidity to take advantage of opportunities as these arise. HRI is operating in a buyers’ market, and this often gives it the power to dictate terms. HRI’s performance also reflects the divergence with the global technology sector, whereby US stocks, especially those with larger market caps, have driven both HRI’s, and the wider market’s, near-term return.

Small-cap technology, telecommunications and multi-media

HRI’s objective is to achieve capital appreciation through investments in smaller quoted companies in the areas of telecommunications, multimedia and technology. Investments may be made across the world, although the portfolio has a strong position in UK stocks. The business activities of investee companies include information technology, broadcasting, printing and publishing and the supply of equipment and services to these companies

At a glance

Market update

Developed market inflation growth rates have finally started to stagnate

In the face of rising interest rates, lacklustre global GDP growth (outside of the US), and a myriad of other factors like US-China trade spats, the global technology sector has seemed to shrug off the wider headwinds and has proven remarkably resilient over 2023 since our last note (which was published at the start of the year).

Be it the result of higher interest rates, lower energy prices, or simply an adaptation to the supply chain issues that resulted from COVID-19 and the Ukrainian conflict, inflation figures are coming down to much more manageable levels. Recently this fall in inflation has been seen in both core and non-core inflation (the latter excluding the more volatile energy and food costs, the former including these) decline, which will take much of the pressure off central banks. Expectations of higher interest rates have eased since our last note; in the UK forecasted peak interest rates are now around 0.5% lower, with the average pundit now expecting another 0.25% rise to 5.50%.

For HRI, and the wider technology sector, the single most important factor has been the rate-setting policy in the US, as determined by the Federal Reserve (Fed), which unlike the UK’s central bank has a dual mandate for both inflation control and economic growth. The Fed is further ahead than the UK in terms of getting inflation under control and has signalled a possible pause to interest rate rises in the near term, though it is open to increasing interest rates by another 0.25bps before the end of the year (to 5.50%). Some pundits even speculate that the Fed could cut interest rates by the end of the year, at the earliest, but bond markets have been jittery. Given the sensitivity of highly valued tech companies to interest rate policy, a cut in rates would be a clear boon for the industry’s valuations.

AI in charge

The proliferation of AI has been a powerful secular tailwind for the technology sector

We believe that the tech sector may have the ability to prove defensive if economic growth continues to be sluggish, given its seemingly inherent ability to grow irrespective of the current economic environment. Be it the disruptive nature of their products, like digital payment providers, the critical services they provide, like cloud computing or security, or the simple need for ever more powerful semiconductors, the key computational component in computers, there is a path to growth that is often unique to the tech sector, which allows it to progress regardless.

In recent months the secular growth story on everyone’s minds has been artificial intelligence (AI), instigated by the launch of Open AI, the generative AI tool (generative AI is capable of generating text, images and/or other media using generative models. These learn the patterns and structure of their input training data and then generate new data that has similar characteristics). This revitalised interest in the tech sector, reversing its post-interest-rate rise selloff and sending companies with strong exposure to the AI industry to all-time highs. While the flurry of interest around AI has come off recently, along with the equity valuations of the wider technology sector, technology still remains the winner of 2023, and has easily eclipsed the returns of other sectors.

The HRI team highlights that the AI story represents a material shift in the dynamics of the technology sector. There will be major ramifications in the demand for certain components, such as AI-oriented semiconductors (which was the primary reason

Developed market inflation growth rates have finally started to stagnate

The proliferation of AI has been a powerful secular tailwind for the technology sector

for NVIDIA’s skyrocketing share price), as well as the need for faster physical components like cables and switches to keep up with the rapid increase in computational capacity. The proliferation of AI will also lead to a much more efficient software development cycle, with companies also being able to deploy AI software into non-tech industries such as healthcare and law. The question the HRI team asks is not whether or not AI will be a driver of share price growth, but who will be the winners and losers from AI, and what are the new markets that it will open up? While investors initially flocked to large cap names exposed to the AI theme, in time some of the big winners will probably emerge from amongst the smaller companies.

Beyond AI, the HRI team has noticed growing tailwinds behind companies associated with the defence sector, given the increased defence spending by western governments in light of the war in the Ukraine, though there are fewer tech companies directly associated with this industry than AI. Conversely, the team is increasingly cautious around consumer sensitive tech sectors, as a possible weakness in the end consumer, i.e. the individual consuming the end product, (be it through weaker GDP or a decline in real purchasing power) will directly affect this sector. This is more of an issue in China which HRI has limited direct exposure to. The UK, on the other hand, where HRI’s traditional focus is, has little to no consumer tech.

The defence sector may offer another avenue of growth, while consumer-exposed stocks may stall out

HRI team view

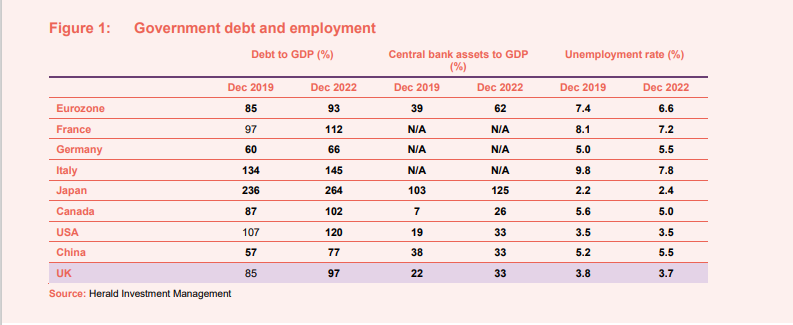

In our recent conversation with the HRI team, they raised their concerns around the fundamental shifts in global market dynamics. Specifically, how greater government indebtedness, which is leading to rises in taxation – the tax burden in Europe, for example, is at its highest level for at least 25 years – coupled with tight labour markets, which are pushing up costs, is putting a significant brake on GDP growth. As can be seen from Figure 1, debt to GDP across the major economies has increased, and for certain countries this has been fuelled in a large part by the central banks expanding their balance sheets, such purchasing debt via quantitative easing, especially in the case of the Eurozone. Very tight labour markets, which increases upwards pressure on wages and inflation, are leaving governments with less room to stimulate their domestic economies.

M&A activity has died out over 2023, while liquidity has also started drying up

This has more nuanced implications for equity investors than simply stalling economic growth. The rise in the volumes of debt present in the economy has warped market liquidity, as excess debt in the market has reduced the relative volumes of cash available to fund equity market transactions (with the cash being tied up in bond investments). Even more recently, the increasing attractiveness of bond yields (considering the sudden sharp rises in interest rates) combined with the huge volumes of debt in circulation has only drawn more investors out of equity markets, as they can gain sufficient returns by holding bonds, or even cash deposits.

Within tech, the manager notices that liquidity is often withheld for earnings announcements, as investors are delaying trades until companies give greater clarity around earnings, a cause and symptom of the declining lack of liquidity. We do note that while declining liquidity is an issue for the wider equity market, it can be a boon for HRI, as their closed ended structure allows them greater patience when investing, and they can take advantage of forced sellers or buyers to generate above market returns for HRI, especially when compared to the equivalent open-ended strategy.

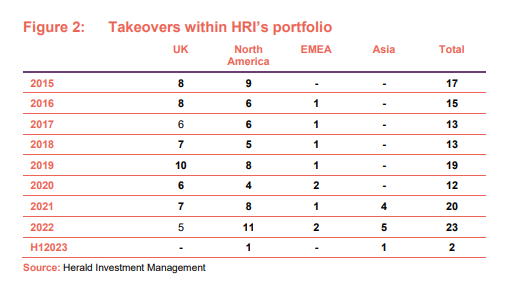

Overall, there has been a marked reduction in private market activity, and participation in the funding rounds in general. Where M&A activity had once been rife in the tech sector, thanks to cheap capital and the relative cheapness of UK equities, it has almost completely dried up. This can be seen clearly in Figure 2 which shows the number of takeovers of HRI’s invested companies.

In the US, venture capital fundraising (amongst the earliest stages of company funding) has fallen by more than 50% year on year (based on the first quarter of 2023).

Asset allocation

HRI is sitting on considerable ‘dry powder’ to capitalise on the lack of market liquidity

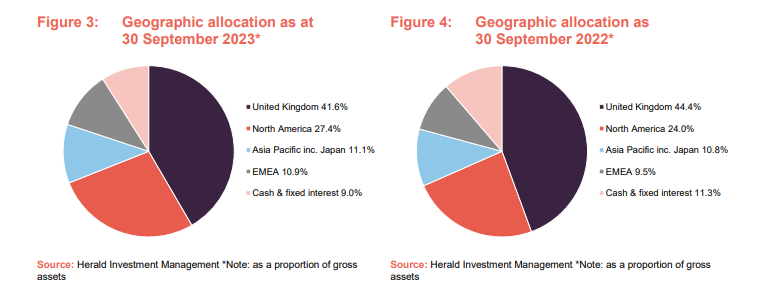

For the reasons that we have discussed above, HRI has about 9% of its portfolio in cash and fixed interest, a little less than it did in September 2022, but still a significant weighting. Investors may be encouraged that this is earning far higher returns in this higher interest environment.

On a geographical level there has been a shift towards the US within HRI, at the expense of its UK exposure. There are two reasons for this shift, the first being that the US is becoming the easier market to navigate, with it having superior liquidity versus other markets, making it easier for individuals to complete equity market transactions, as well as more companies within the ‘sweet spot’ of a $3bn market cap, a threshold which draws increased investor attention and thus liquidity. The second reason is simply that US technology stocks have blazed ahead of those in other regions, meaning there has been a natural increase in the size of HRI’s US equity position due to the increase in comparative value.

Top 10 Holdings

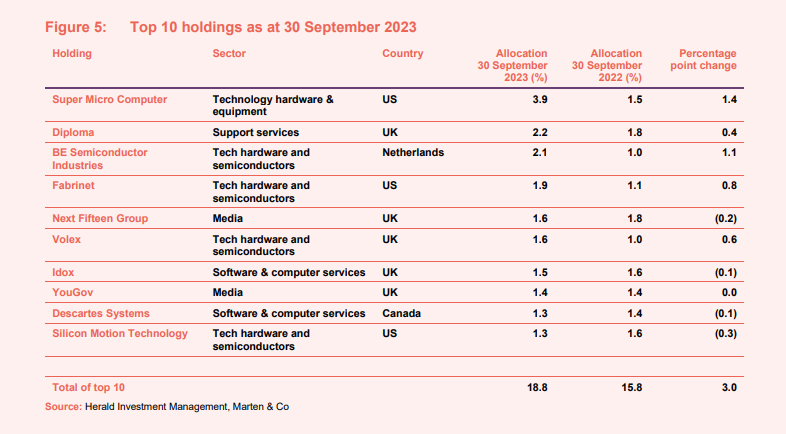

Figure 5 shows HRI’s top 10 holdings as at 30 September 2023 and how these have changed over the previous 12 months.

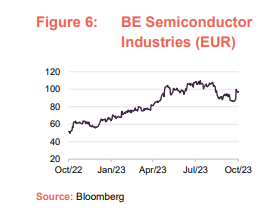

BE Semiconductior Industries

BE Semiconductor Industries (Besi) is a holding company that is engaged in the development, manufacturing, sales, and service of semiconductor assembly equipment. Besi does not produce semiconductor chips, but rather the niche equipment used by other companies in their own semiconductor production. Besi operates in three segments: Die Attach, Packing, and Plating.

Besi is an example of a company that is a critical cog in the global semiconductor industry despite its small size. Besi’s shares have shot up meteorically since COVID-19, as the proliferation of technology adoption has directly increased the demand for semiconductors. Besi’s highly advanced systems are also becoming increasingly integrated into semiconductor manufacturing, which is helping to solidify its position as a market leader. For example, Besi’s hybrid bonding technology is expected to go mainstream with smartphone processor makers around 2027.

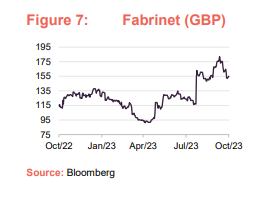

Fabrinet

Fabrinet is a Cayman Islands-based company, which provides advanced precision optical/electronic/mechanical manufacturing services. The company provides advanced optical packaging and precision optical, electromechanical and electronic manufacturing services to original equipment manufacturers of complex products, such as industrial lasers, medical devices and sensors, to name a few. Fabrinet offers a range of advanced optical and electromechanical capabilities across the whole manufacturing process, from the process design and engineering, to manufacturing, then final assembly and testing. Its primary focus though is on the production of low volume, high-mix products.

Thanks to the recent surge in AI-driven demand, Fabrinet has been able to post robust earnings for its fourth quarter 2023 (for its financial year). The surge in demand from AI-linked firms, with NVIDIA accounting for 13% of revenues, was more than enough to offset a falling demand from telecoms, which has traditionally been Fabrinet’s largest business – something which demonstrates the importance of sectoral growth opportunities (the advancement of AI in this case) in offsetting cyclical slowdowns.

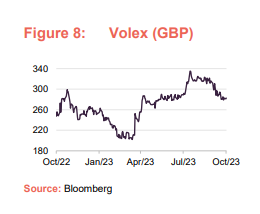

Volex

Volex is a UK based firm that is engaged in integrated manufacturing of performance-critical applications and power products. Volex’s range of products, capabilities, and solutions includes power cords, connectors, integrated manufacturing services, electric vehicle charging solutions, consumer cable harnesses and power products, higher speed internet and data transfer cables, and data centre power cables.

There has been a spate of recent wins for Volex, with it recently becoming a licensed charging system partner of Tesla, a testament to the quality of its products. It also acquired Murat Ticaret, a maker of wire harnesses, which it believes will provide it with immediate entry into a new growth market. These developments come after Volex reported a FY 2023 performance ahead of market consensus, growing its profits by 17% on the prior year, which sent its share surging in April. These results can be attributed to Volex’s ability to control costs and improve its margins, as well as its strategy of targeting structural growth industries like electric vehicles, complex industrial technologies, and the medical sector.

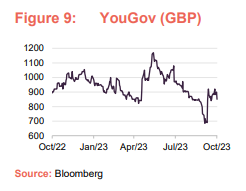

YouGov

YouGov is a UK based international research and data analytics company, providing its clients with data to help them explore, plan, activate and track the impact of their marketing and communications activities. UK readers will likely recognise the company for the polling data, which is frequently referred to by the UK’s press, especially during election periods. YouGov operates in three divisions: Data Products, Data Services, and Custom Research. YouGov’s data products division comprises its syndicated data products, such as its ‘BrandIndex’ and ‘Profiles’ products suites, which are offered to clients on a subscription basis. Its data services division provides clients with fast-turnaround and cost-effective survey solutions for national and specialist sample sizes. Its custom research division offers a range of quantitative and qualitative research tailored to fit each client’s specific requests.

YouGov’s recent activity includes the acquisition of the GfK’s Consumer Panel Business, a leader in European household purchase data, for €315m. The purchase was partially funded by a £51m equity issuance by YouGov, which in part explains the weakened share price over the year, given the diluting effect. YouGov’s shares were also impacted by the company’s announcement in July that while its 2023 operating profit would be in line with expectations, its revenues were on track to come in at the lower end of its estimates, which led to a fall in its share price. We note that YouGov has begun to look at the idea of listing in the US, which would dramatically increase the liquidity around the stock, and may be a future tailwind for its share price, enabling it to take advantage of the more conducive market dynamics in the US.

Performance

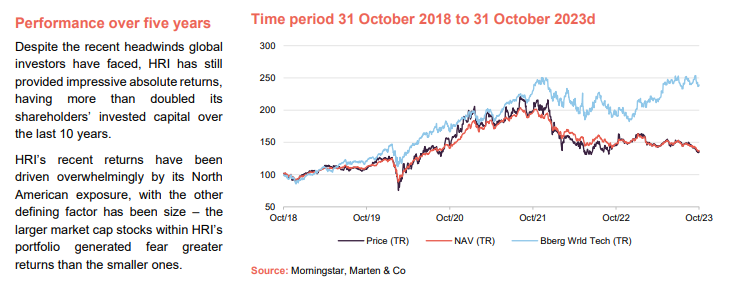

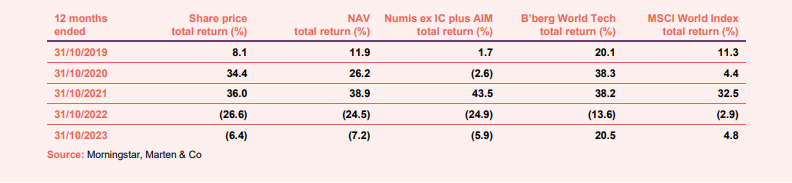

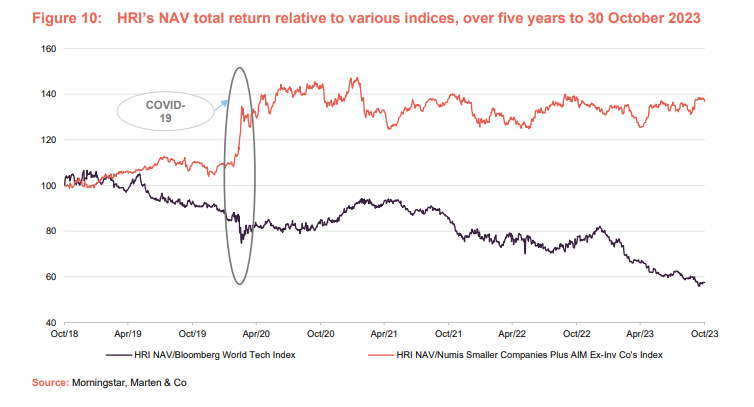

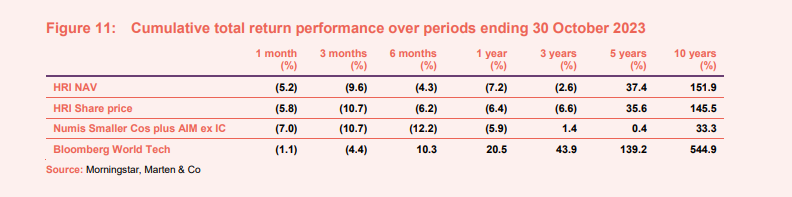

Despite the recent headwinds global investors have faced, HRI has still provided impressive absolute returns, having more than doubled its shareholders’ invested capital over the last 10 years, as well as generating a nearly 40% total return over five. This compares very favourably to the domestic UK small cap market, as the Numis small cap index has failed to add virtually any value over the last five years, having returned a paltry 0.4%.

HRI has however lagged global markets over the long term, falling behind the Bloomberg World Technology Index over nearly all sampled periods (as seen in figure 11). This is mainly due to its relative underexposure to the US and its zero allocation to large cap companies.

North American equities, in particular their technology stocks, have often represented the lion’s share of the growth in global equities, thanks to the US’s supportive equity markets, strong earnings results from US technology companies, and the abundance of cheap capital (due to prolonged rock bottom interest rates reducing the opportunity cost of equity investing and the cost of debt financing). While this has certainly been a boon to the US small and mid-cap sector, its greatest impact has been in the US mega cap sector.

Generally speaking however, the US’s equity market returns, and by extension global equity market returns, have been driven by the ‘magnificent seven’, seven of Americas largest technology companies (Apple, Amazon, Alphabet, Microsoft, Nvidia, Tesla, and Meta), which saw outsized rallies during the end of 2022 and 2023. This was in part due to their earnings but also due to the frenzy around AI, with investors sheltering in well-known companies to capitalise on the expected growth of a very complex sector. The Bloomberg Technology Index has also outperformed HRI for similar reasons – while it does not hold the consumer-focused technology companies like Amazon or Facebook, Apple, Microsoft, and NVIDIA account for 47% of the index alone, and these have arguably been an even greater beneficiary of the recent tech tailwinds than any other index or fund presented here. In the case of the Bloomberg World Technology Index Apple, accounts for 20%, while Microsoft accounts for 18%.

These very high concentrations in the largest stocks is a significant challenge for any strategies that are benchmarked against them. Many strategies do not allow managers to have allocations close these levels and, even if permitted, many would avoid this as it would not generally be considered to be good portfolio management (in order to achieve a sufficient level of diversification). As a consequence, in periods where mega cap technology outperforms, actively managed technology funds look set to underperform. This high concentration in the big names of the major technology indices increasingly raises questions about their practical use as benchmarks.

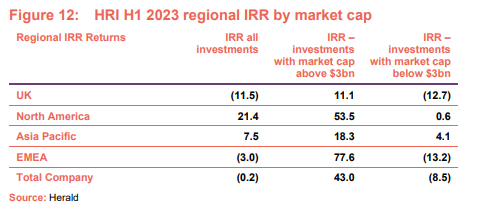

H1 2023 – A tale of two halves

The first half of 2023 has been a story of two distinct groups, as can be seen by Figure 12. Specifically, HRI’s returns have been driven overwhelmingly by its North American exposure. Asia Pacific was also a positive contributor but, at only c.10% of HRI’s allocation, its effect is muted versus that of North America’s. The other defining factor has been size – the larger market cap stocks within HRI’s portfolio generated fear greater returns than the smaller.

US equity gains have offset HRI losses in the UK market

Market returns during H1 2023 have been largely driven by higher-level macroeconomic or more industry specific, sector wide events. One of, if not the most, transformative developments within the technology space has been the excitement around AI, which has placed the spotlight on the US tech market once again as most of the major AI names, like Chat GP, have come out of the region.

While there have been several bright spots within tech over 2023, one cannot avoid the conducive macroeconomic situation the sector found itself in. Through the first half of 2023, we finally began to see a sustained reduction in US inflation, and a softening in the language used by the Fed, as well as a reduction in interest rate expectations by the wider market, which are now forecasting a possible interest rate cut early next year. The US is also benefiting from a comparatively robust economy. GDP growth is better than most other developed market and both businesses and consumers remain strong. The combination of economic strength and tempering interest rate expectations brought about renewed investor confidence in US markets, as shown in Figure 12. The strength of performance from the Asia Pacific region can also be attributed to similar factors, as the region has far lower inflation expectations that developed markets, although it has likely been weighed down by the economic woes of China (whose GDP growth has fallen to the lowest levels in recent memory).

The size effect present within HRI’s portfolio, whereby its larger market cap holdings outperformed the smaller market caps, can be attributed to the liquidity advantage larger companies have. As we outlined on page 5, there has been a decline in market liquidity since 2022, as investors retreated from the small cap equity market in favour of larger and more defensive positions (those with less market sensitivity) which are seen as safer. Given the dramatic shifts we have seen in both macro and sector trends in 2023, it is unsurprising that investors have favoured liquid stocks, given their advantages in navigating a volatile market environment.

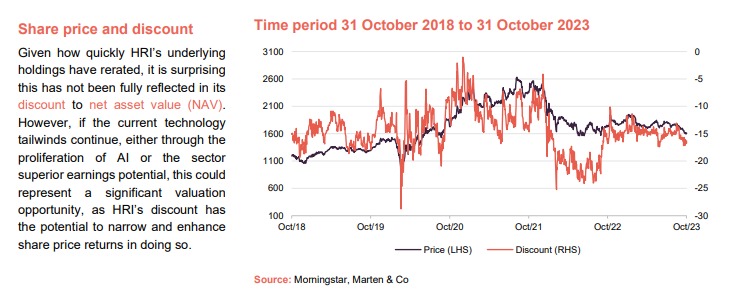

Discount

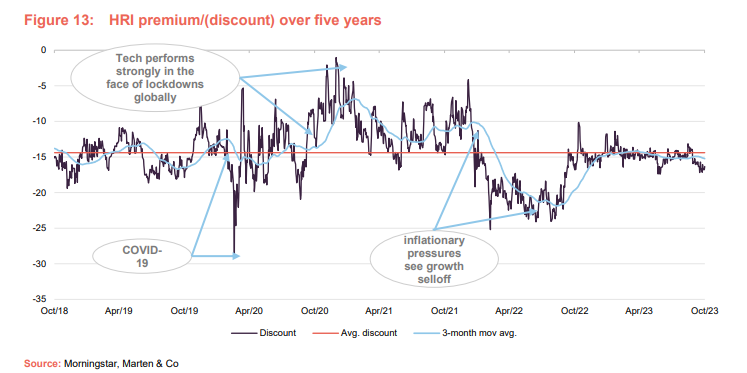

While HRI has traded at a continual discount across all of the last five years, the size of its discount has historically been a reflection of the outperformance of technology stocks, narrowing during periods of strong relative performance. This can be seen clearly during the post-pandemic-crash period (which started in mid-2020), which saw a substantial outperformance of technology stocks, with HRI trading at its narrowest discount of the last five years at the end of 2020.

HRI’s discount trades in line with its long-term average.

Given how quickly underlying holdings have rerated, though, it is surprising this has not been fully reflected in the discounts of tech focused trusts. However, if the current technology tailwinds continue, either through the proliferation of AI or the sector superior earnings potential, this could represent a significant valuation opportunity, as HRI’s discount has the potential to narrow and enhance share price returns in doing so.

HRI currently trades on a 15.2% discount and over the past year, HRI has traded on a discount ranging between 11% and 17%, with an average discount of 14.4%.

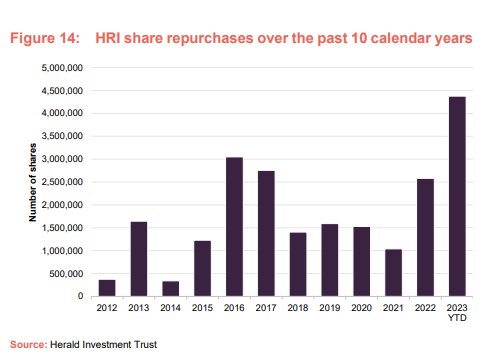

The board has increased its share repurchases over 2023, as can be seen by Figure 14. Whilst HRI’s policy is not to attempt to control the discount, because it is not considered appropriate given the limited liquidity available within the underlying portfolio companies, the trust will repurchase shares opportunistically. Where repurchases are undertaken, the aim is to enhance the NAV per share for remaining shareholders. Given the magnitude of the recent repurchases, it is a testament to the opportunity the board perceive in HRI’s recent discount.

Dividend

HRI is focused primarily on generating capital growth, and dividend income makes up only a small part of returns. The consequence of this is that HRI only declares a dividend where this is necessary to retain investment trust status, and in practice, no dividend has been declared since 2012.

Fund Profile

More information can be found at the trust’s website: www.heralduk.com.

Established in 1994, HRI invests globally in small technology, communications and multimedia companies with the aim of achieving capital growth. It is the only listed fund of its type. The trust invests globally, but has a strong bias towards the UK, which further distinguishes it from other global technology funds, which tend to be biased towards the US.

New investments in the fund will typically have a market capitalisation of $3bn or less but are generally much smaller when the first investment is made. If successful, these can grow to be a multiple of their original valuation. This type of investing is longer-term in nature and so the trust tends to have low turnover. Reflecting the risks inherent in this type of investing, and the liquidity constraints of having a small cap investment remit, the trust maintains a highly diverse portfolio of investments (typically in excess of 250) to help mitigate this risk.

Experience is important in markets such as these

One of the most consistent benefits the trust has offered has been the considerable experience offered by its lead fund manager Katie Potts, who has managed HRI since its launch. She was a highly-regarded technology analyst at SG Warburg (later UBS) prior to launching the fund. Katie owns a substantial stake in the company and a significant minority stake in the management company, and therefore is clearly motivated to ensure the success of the fund.

HRI’s closed-ended structure allows effective use of gearing during market selloffs

Under Katie’s stewardship, HRI has navigated several downturns and has benefited from the team’s ability to select companies capable of weathering difficult conditions. HRI’s closed-ended structure has also been used to great effect. Whilst open-ended funds are often forced sellers, HRI can capitalise on its ability to gear to pick up lines of stock at attractive prices (we discuss this further on page 9), though in practice it has seldom made use of this facility in recent years.

HRI’s size, focus on smaller companies and the depth of expertise within the management team mean that it plays an important role as a provider of much-needed ca44pital to listed technology companies looking for expansion capital. This is particularly valuable in a downturn and has offered HRI further opportunities to generate alpha when others may not have been able to.

HRI offers a liquid subcontract for any investor looking to gain access to this part of the market, and we believe that an investment in HRI complements an investment in one of the large-cap technology funds.

Previous Publications

Readers interested in further information about HRI may wish to read our previous notes (details are provided in Figure 15 below). You can read the notes by clicking on them in Figure 15 or by visiting our website.

Legal

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Herald Investment Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it, but in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.