Needs more time

Needs more time

India Capital Growth’s (IGC’s) board is asking investors to back a continuation vote scheduled for 12 June 2020 and it is important that shareholders make their vote count. COVID-19 has depressed valuations to levels not seen since the financial crisis. The managers see substantial upside when market confidence returns and are asking for more time to deliver that. The board believes shareholders should support the continuation of the company. This reflects their confidence in the measures taken to turn performance around, which we discuss in this note. When small and mid-cap valuations return to trading at long-term average valuations, IGC’s share price could improve meaningfully.

India’s response to the COVID-19 outbreak has been robust and this will have serious economic consequences. This has triggered a further leg down in the Indian market. A stimulus package of up to $266bn announced on 12 May should help stimulate a long-awaited recovery.

In a response to the reversal of fortune that IGC has experienced over the last couple of years, the adviser has strengthened its team and refined its investment approach. Shareholders that give IGC the benefit of the doubt will have the comfort of a full exit opportunity in December 2021.

Mid- and small-cap listed investments in India

IGC’s investment objective is to provide long-term capital appreciation by investing (directly or indirectly) in companies based in India. The investment policy permits the company to make investments in a range of Indian equity securities and Indian equity-linked securities. The company’s investments are predominantly in listed mid- and small-cap companies.

IGC puts forward proposals ahead of 12 June continuation vote

IGC announced on 26 May 2020 that it will hold an extraordinary general meeting on 12 June 2020, in Guernsey, where shareholders will be asked whether they want the fund to continue.

The board undertakes a performance assessment every three years and a vote on the trust’s continued existence is put to shareholders only in the event that either of the following criteria are met:

- the company’s monthly average market capitalisation million over the past year is below £30m; or

- the company’s published diluted NAV per ordinary share has underperformed the benchmark by more than a cumulative 5% over the previous three years.

While the first of these criteria has been satisfied, IGC’s performance is very unlikely to improve sufficiently to meet the second threshold by 6 August 2020 (the date for the next three yearly assessment). Diluted NAV per share fell 45.8% from 7 August 2017 to 15 May 2020, representing a cumulative underperformance against the benchmark (BSE Mid Cap Total Return Index) of 14.1%.

The board has therefore decided to bring forward the date for proposing the continuation resolution and its proposals.

In order for IGC to have a future, the board recognises that the following parameters must be satisfied:

- performance will need to improve significantly;

- the level of the discount must be brought in significantly;

- a pathway to liquidity must be provided to investors; and

- costs must be competitive.

The board believes there is potential for IGC’s performance to improve significantly and is proposing the company continues. To this end, the board has put forward the following, to redress the underperformance, subject to the passing of continuation resolution:

- the introduction of a redemption facility, giving shareholders the right to request the redemption of part or all of their shareholding on 31 December 2021, and every second year thereafter, at an exit discount equal to a maximum of a 6% discount to NAV per redemption share;

- a change to the investment manager’s fee from 1.25% of total assets per annum, to the lower of 1.25% of average market capitalisation (calculated on a daily basis) per annum or 1.25% of total assets per annum with effect from 1 July 2020 (which gives the manager an incentive to narrow the discount) with a further review to the investment manager’s fee in 2022; and

- IGC may seek to satisfy redemption requests by matching such requests with demand for new ordinary shares from incoming investors.

If the resolution is not passed, proposals to wind-up, reorganise or reconstruct the company, will be put to shareholders. Given the extremely volatile market environment and the as yet unknown impact of COVID-19 on India, the board considers that the realisation of the company’s portfolio of investments at the present time is likely to result in sub-optimal returns for shareholders.

Proposals follow refinements made to the investment process

Ocean Dial, IGC’s manager, has made a number of refinements to the investment process, over the past year. These are described on pages 8 to 10.

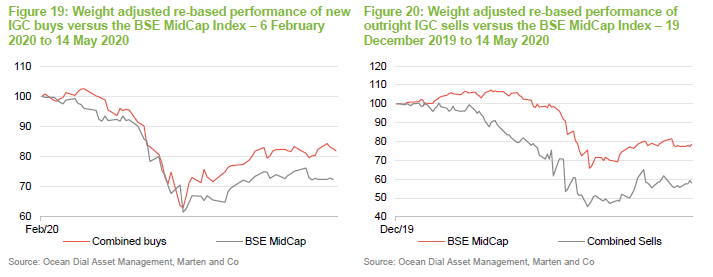

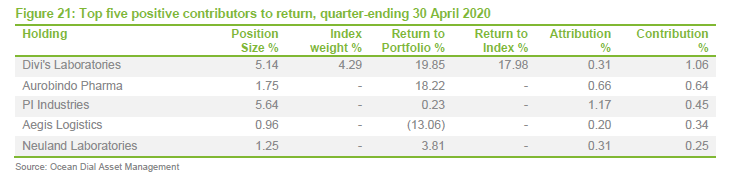

Stock selection has been the main culprit behind the poor relative returns since 2017, which the manager is redressing through process change and team development. There have been some encouraging signs of progress, with a weighted basket of new entries to the portfolio outperforming the benchmark, over the year-to-date by 9.5% and stocks sold underperforming by 20.5%. This is discussed in the performance section from page 13 onwards.

IGC believes voting in favour of the company’s continuation will provide the following benefits to shareholders:

- Being able to redeem some or all of their shareholding, without being reliant on the market liquidity of the shares;

- Progressively reducing the discount at which the shares trade compared to NAV per share;

- Addressing, through the redemption facility and the issue of shares from treasury, market imbalances in the supply of, and demand for, the shares;

- An uplift in NAV per share for the company and continuing shareholders as a result of the exit discount applied to the shares that are redeemed;

- A greater likelihood that the value of the shares will reflect the prospects of the company’s investment strategy;

- A more effective alignment between the manager and shareholders by switching the management fee calculation from total assets to market capitalisation; and

- A reduction in the manager’s fee and so to the operating costs of the company.

They also feel that this is a very attractive cyclical low point for valuations in the Indian market – particularly the segment focussed on by IGC. They particularly note that there is the potential for a considerable uplift in returns if India’s economy recovers and growth matches historic levels, small and medium-sized stocks return to trading at long-term average valuation multiples and if IGC’s discount tightens.

Webinars

David Cornell, manager of IGC, will be discussing the proposals at two webinars. The first of these is on 29 May 2020 at 12:00 and the second on 3 June 2020 at 12:00.

Registration for these webinars is possible by clicking the links in the dates above or by visiting the Events section on the QuotedData website.

Focus of India’s COVID-19 response shifts to stimulus

On May 12, Prime Minister Narendra Modi announced a stimulus package worth up to $266bn, corresponding to around 10% of GDP. Early critics of the stimulus say that the actual measures to boost demand amount to a much more modest 1-2% of GDP. A large part of the package is focused on monetary measures announced by the Reserve Bank of India, guarantees by the government as well as other forms of funding.

IGC’s adviser, Gaurav Narain (Gaurav) considers that the lack of measures to boost demand is disappointing, given the anticipation that had built-up following the initial announcement. He notes that a greater focus is being placed on using the crisis as a springboard to enact structural reforms, across several industries. He highlights the agriculture, mining, defence, and power sectors.

In this sense, the opportunity to enact reforms has seen the current period compared to 1991, when market reforms enacted by the then finance minister, Manmohan Singh (following a currency crisis) laid foundations that transformed India’s growth profile. True reform could be just as impactful.

Gaurav believes the agriculture industry could be a major beneficiary. Considerable reforms will take place as the outdated industry is liberalised. Ocean Dial note India has wild food price swings despite being a self-sufficient domestic producer of food, as several centuries of agriculture policy has kept the 50% of the population trapped in unproductive farming.

While India has been able to reduce the growth rate in active new cases of the virus, the number of new cases has continued to rise in a number of cities. Consequently, any easing of the lockdown will have to be very carefully managed, which poses idiosyncratic challenges in India, given its size and population density.

The state of Maharashtra has been the worst affected, with around one third of the caseload, though on balance, India has succeeded in keeping fatalities at much lower levels than many countries, helped by a young population.

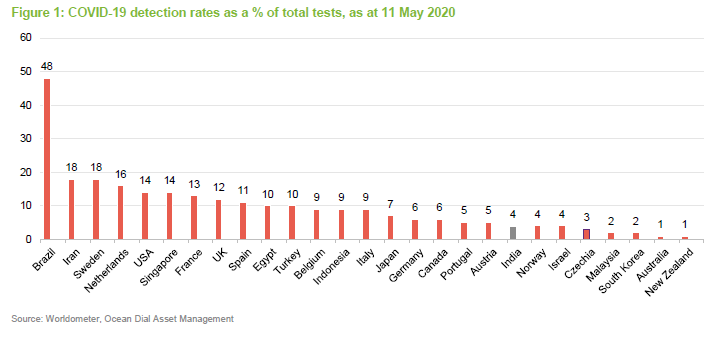

India has not lacked testing capacity in the way many countries have. This has mainly taken the form of targeted testing so far. India has also been able to use the lockdown period to ramp up its stock of ventilators.

The debate within India has been shifting increasingly to one of lives versus livelihoods. Initial government stimulus, amounting to just 1% of GDP, was inadequate against a backdrop of 80 million migrant workers being displaced, as business activity came to a standstill. The banking sector is still recovering from the 2018 default of IL&FS, which we discussed in our most recent annual overview note. Attempts to incentivise the banks to provide liquidity to small and medium-sized enterprises proved futile.

Many of the companies Gaurav has spoken to have said that operating beyond 50% of their manufacturing capacity will be very difficult – the focus has been on clearing inventory. Salary cuts of around 15%, across workforces, have been the norm. Once the economy begins to open-up, companies are anticipating a period of 6–9 months for operations to normalise. Corporates are anticipating challenges in re-integrating many of India’s labourers, who are still attempting to reach their home villages.

Economy better positioned than in 2008

COVID-19 will leave a dreadful imprint on corporate performance and India still needs to carefully manage the re-opening of the economy over the coming months.

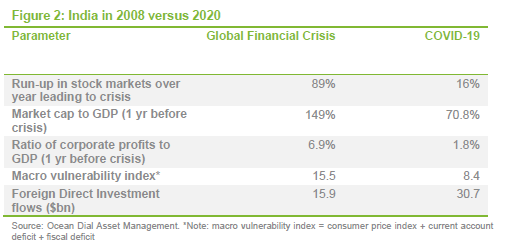

Gaurav says India entered the current crisis in better shape than for the most recent shock, the global financial crisis of 2008. While corporate earnings and the Indian equity market have faltered over the past two years or so, the stock market is much smaller in size than it was in 2008, as a percentage of India’s GDP. Figure 2 makes a comparison between the two periods.

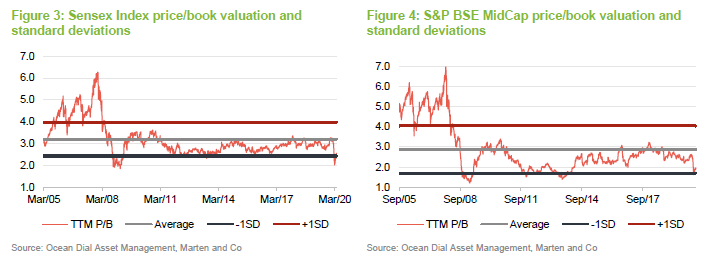

The Indian stock market has been heavily penalised so far this year. As at 30 April, the equity market had contracted by around 30%. Valuations are now below one standard deviation of their 15-year average.

Ocean Dial says that based on valuations that are one standard deviation below long term averages the portfolio has 15.4% upside, as at 15 May 2020. This is based on price/earnings, price/book value and EV/EBITDA multiples on historical (FY20) earnings (NB India runs on financial years ending 31 March. FY20 means the twelve months ended 31 March 2020 and FY21 means the twelve months ended 31 March 2021).

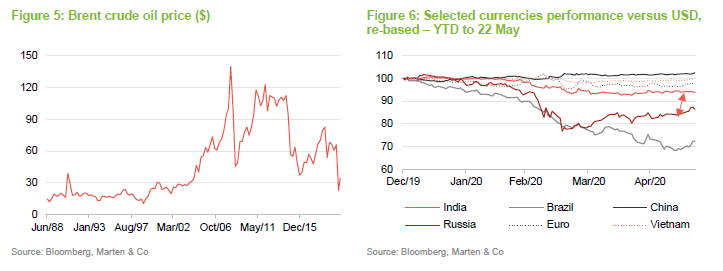

As a net energy importer, India benefits from low oil prices. It is also building out its natural gas capacity, which IGC has added exposure to, in the form of Gujarat Gas (discussed in the asset allocation section). As illustrated by Figures 5 and 6, crude oil prices are at levels not seen since 2003. So far this year, the rupee is down by less than 7%, against the dollar. Many other emerging market currencies have fared far worse.

India expected to benefit from supply-chain diversification

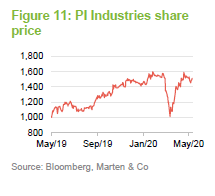

Along with perhaps Vietnam, India is amongst the best-positioned countries to provide an alternative to China in supply-chain manufacturing. Gaurav mentions chemicals and healthcare as two industries that are best positioned. China’s chemicals industry is presently around 10 times the size of India’s, so this has the potential to materially move the needle for Indian chemical companies. The agrochemical company, PI Industries, is well positioned to benefit, as one of the market leaders. The company is IGC’s second largest holding; it is discussed in greater detail in the asset allocation section.

Whilst India’s generic drug manufacturing industry is very well established, most of the world’s active pharmaceutical ingredients (APIs) are manufactured in China. As well as growing in-house API capabilities, India will see a major opportunity to take global share away from China. IGC has significant exposure to this through its second-largest holding, Divi’s Laboratories. The company is a core component in the supply chains of many of the world’s largest pharmaceutical companies. As at 13 May, Divi’s shares had increased by 30.9% over the year-to-date.

We also note that In March, the government announced a $1.3bn incentives package for local manufacturing of drugs as well as plans to establish industry manufacturing hubs. India will also look to expand its footprint in other areas of healthcare, such as medical devices.

As well as proving supply chain outposts for international companies, India will look to grow its export trade, across several industries, including consumer durables and textiles. India will be looking to deepen its technology industry as well.

In the past, India has often underwhelmed when opportunities to grow its manufacturing base have emerged. For example, when wage growth made garments increasingly uneconomical to produce in China, it was Bangladesh and Vietnam who benefited most. The stakes are higher this time, in higher value industries.

Broad-based sell-off brings more value to mid-caps

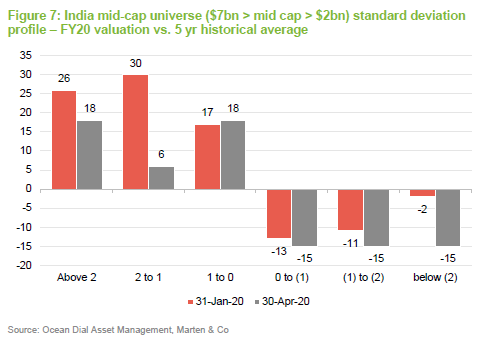

Gaurav notes that, at the end of April 2020, 30% of mid-cap stocks in India were trading at below one standard deviation, compared to their five-year averages – the equivalent figure was 13% as at 31 January 2020. We discuss what this has meant for the makeup of the portfolio in the asset allocation section below.

Smaller and medium-sized companies are most vulnerable to lockdown and many have found it difficult to access credit to fund their working capital requirements. In assessing value, Gaurav says he is paying more attention to historical earnings (forward earnings estimates hold little value at the moment), looking to cross-reference dislocations based on standard deviation movements and seeing how this interacts with business models in this environment, as well as leverage. Inevitably, there are companies that perform well in a crisis, which are caught up in a market route.

Refined investment process

IGC have refined their investment process since we last published. With the addition of a new co-head of equities and some new analysts, the investment team now has seven members – an eighth member is expected to join shortly.

Other recent changes of note include the introduction of artificial intelligence (AI) tools to the screening and monitoring process. AI has been introduced to the screening and monitoring process through a tool that pulls information on an investee company from multiple sources of unstructured data onto a single dashboard that is readily accessible by the investment team.

Team structure

Among the additions is Tridib Pathak. He joined Ocean Dial in October 2019, as co-head of equities, sitting alongside Gaurav Narain. The analyst team was strengthened by the addition of Saurabh Rathore and Ashutosh Garud, earlier this year.

Biographies of the investment team are provided in the appendix on page 20.

“House of Ocean Dial”

Gaurav and the rest of the India-based team at Ocean Dial are bottom-up investors (focused on picking stocks), operating in a market with historically strong and consistent earnings growth, where periods of elevated volatility have provided regular mispriced entry points.

Ocean Dial seeks out companies whose management practices are culturally aligned with theirs and whose business models are capable of creating long-term shareholder value in a sustainable manner. A focused universe of companies from which potential investments are scrutinised is referred to as the House of Ocean Dial. More specifically, companies with the following attributes are eliminated:

- Market capitalisation of below US$100m

- Environmental, Social, and Corporate Governance concerns

- Business models which are

- Incomprehensible

- Not scalable

- Driven by global commodity prices

- Conglomerated

- Unable to create sustainable economic value

- Business-to-Consumer companies where the consumers are predominantly based outside of India

- Insufficient knowledge to have an informed view on any of the above

This has resulted in a current universe of approximately 140 companies from which the managers can invest in. Each analyst covers roughly 35 names and coverage entails forensic accounting, detailed financial modelling, and one-to-one corporate interaction twice annually.

Portfolio Construction – aiming for 30 holdings

The House of Ocean Dial is a universe of companies on which the team can build focus. The manager will allocate to approximately 30 holdings which are independent both of the IGC’s benchmark and the market capitalisation of the business.

The starting point is to examine the highest ranked companies in the universe in terms of expected return and from this the manager has discretion to dive deeper. In addition to meeting regularly with senior management, the team meets with suppliers, customers, and business competitors where relevant. The portfolio looks to invest with a minimum position size of 2%. This could range to up to 8% depending on the liquidity of the traded volume and the strength of conviction.

Investment Committee

The House of Ocean Dial is a continuously evolving universe of investible opportunities. An investment committee exists to ensure that existing names continue to pass filters set, and to provide a forum for members of the investment team to propose new names for inclusion into the universe.

The investment committee meets quarterly and acts as a gatekeeper for stocks under consideration, with any changes needing to be approved by the committee. The agenda also includes the following issues.

Mitigating Behavioural risk

The team is cognisant of the challenge of distinguishing, without the benefit of hindsight, between temporary downward fluctuations caused by volatility from a genuine loss of capital. To diminish the probability of the latter, the research process is structured to ensure that each investment thesis is constructed on a sound basis whilst allowing the decision-making framework to react effectively should a change in the thesis occur over the course of the holding period. All investments are documented on initiation to enable the manager to assess the effectiveness of decisions made without being clouded by viewing them through the lens of hindsight.

Direct management interaction is limited where appropriate to twice a year, with healthy scepticism accorded to guidance to ensure the team remains detached in its assessment of a given company. Moreover, the investment committee provides an open forum for discussion on price movements or changes in fundamentals to ensure a continuous and systematic re-assessment of each investment thesis. The universe ranking tool provides a quantitative basis for guiding where the highest expected return opportunities exist, whilst triggering a re-assessment of holdings that are falling down the ranking.

Valuation risk

A broad range of relative and absolute measures are used in comparison to the company’s own history, its relevant peer group, and the broader market to create an expected return which is then ranked relative to the rest of the universe. A core part of mitigating valuation risk is to utilise a reverse discounted cash flow analysis, which uses the share price as the starting point to guide as to how much cash the company would have to generate to justify the current market valuation.

Asset allocation

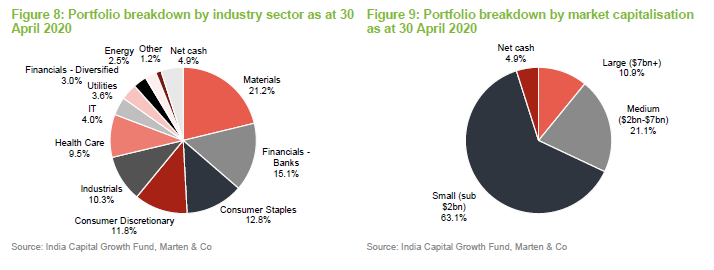

At the end of April 2020, IGC’s portfolio comprised 35 holdings. Since our last note was published in October 2019, exposure to the materials, industrials and healthcare sectors has increased. This has come largely at the expense of financials and IT. A number of banking exposures have been reduced – these are listed on page 11.

Over the year to date, turnover in the portfolio has inevitably been higher than the norm. Gaurav has pursued an incremental approach to buying and selling. Initially, when the outbreak seemed to be largely confined to China, Gaurav reduced the portfolio’s exposure to what seemed a likely collapse in Chinese aggregate demand, in areas such as auto ancillary parts. The period was also used as an opportunity to take profit in some stocks, both in anticipation of a global slowdown and to build up cash reserves. The latter provided resources to buy good-quality companies at discounted prices.

A current net cash weighting (IGC has no debt of its own) of 4.9% is slightly above average, though Gaurav notes that this is a by-product of the increased turnover in the portfolio, rather than a ‘view’ on cash.

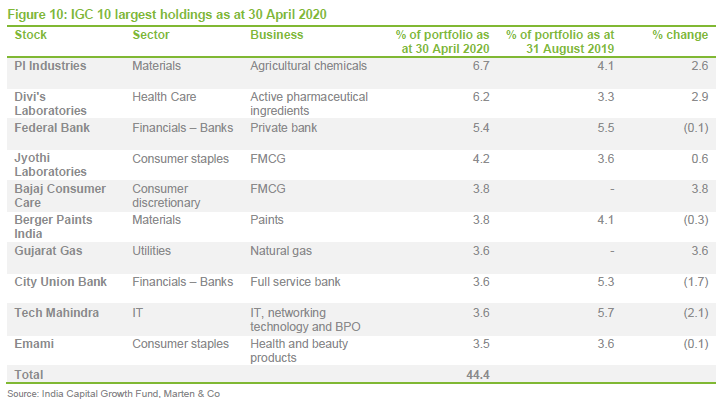

Top 10 holdings

Many of the stocks in the list of the top 10 holdings have been discussed in earlier notes (see page 19 for a list of these), having been longstanding positions within IGC.

At 30 April 2020, the 10 largest holdings in IGC’s portfolio accounted for 44.4% of the fund. Since we last published, Gaurav’s selling activity has followed three main themes:

- Reducing stakes in companies sensitive to export weakness.

- Motherson Sumi, a leading auto ancillary company was exited completely, while the exposure to Tech Mahindra was reduced. Its business lines include IT process outsourcing, which could suffer in the wake of the global recession. As at 22 May 2020, the company’s shares were down by over 30% over the year-to-date.

- Taking profit on holdings that were looking richly valued.

- Gaurav has reduced weights to Berger Paints and PI Industries. Berger Paints is one of the four major paint producers in India – it is the portfolio’s most richly valued holding, trading at a trailing price/earnings ratio of 69x, as at 13 May.

- PI Industries remains a high conviction holding – Gaurav says it has strong relationships with Japanese and European agrochemical companies; the company is also building out a pharmaceutical business line. We note that the shares have rebounded considerably over recent weeks. PI Industries fits the profile of a company that Gaurav believes can benefit from global supply-chain diversification.

- Reducing exposure to the financials sector.

- Exposure to City Union Bank was reduced, having been the third largest holding as at end-August 2019. Positions in DCB Bank, Indian Bank, Yes Bank and Jammu & Kashmir Bank have been sold in their entirety.

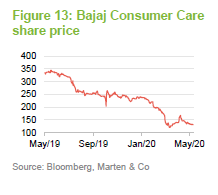

Elsewhere within the top 10, Gaurav said that companies that predominantly take payment in cash – predominantly fast-moving consumer goods (FMCG) companies – had an advantage, as they have more of a cash-flow cushion. The lack of receivables and the paying of creditors in 60 days or so allows them to stretch out their cash conversion cycle. Bajaj Consumer Care was discussed as an example. It is a major player in India’s hair oil industry, a category which has grown 11% in value over the last decade. Gaurav says the company has gross margins of 67%, a return on capital employed of 40% and cash in its books equivalent to 25% of its market capitalisation. Gaurav expects the shares to re-rate.

Gaurav also raised the fund’s holding in Jyothy Laboratories, which sits in fourth position in the top 10. The company sells a wide range of staple consumer goods, including insecticides and soap/detergent products. Gaurav says 90–95% of its range can be classified as essential products. It is currently trading at around 19x trailing earnings – about half its typical range. The manager does not expect the company’s margins to come under too much strain. Gross margins of 47% provide a buffer, while it can also trim advertising expense if necessary. The informal nature of most of India’s retail market means companies tend to not have to negotiate with powerful retailers as much.

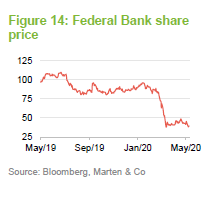

Banks have weighed on performance for some time. Federal Bank remains among the largest holdings, with Gaurav noting that its wholesale asset loan book contains largely triple-A-rated debt exposures, while its retail loan book is moving to higher yielding assets. He believes the bank is fundamentally sound on both asset and liability sides.

He expects high loss provisions to kick in, as they have been doing in banking across the world, but ultimately for Federal Bank’s shares to move back up. They are currently trading at about 0.6x book value, which the manager says is less than half the typical range for this stock.

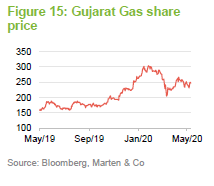

Gujarat Gas leads new additions to the portfolio

New additions to the portfolio include: Multi Commodity Exchange (Mumbai-based commodity exchange); Gujarat Gas (profiled below); Aegis Logistics (logistics provider to the oil, gas, and chemicals sectors); ICICI Lombard (general insurance) and CCL Products (instant coffee manufacturer).

Gaurav discussed CCL Products as an example of a good-quality company that became attractively valued. It is one of the largest private label manufacturers of instant coffee, operating in a sector that has been performing well through the global lockdown. Coffee consumption has simply shifted from the workplace and the retail market to the home.

Gujarat Gas (www.gujaratgas.com) is the largest of the recent portfolio additions. India is investing to shift more of its energy need from oil to gas, with new gas pipelines being installed across the country. Based in Gujarat, which Gaurav notes is India’s most industrialised state, Gujarat Gas operates across the gas sector. Gaurav notes that there has been more focus on pollution within India and it has observed China’s success in reducing pollution with gas.

Performance

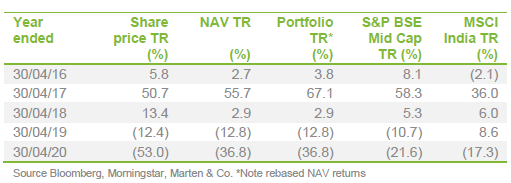

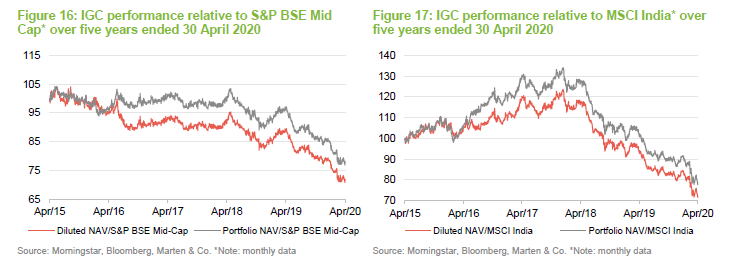

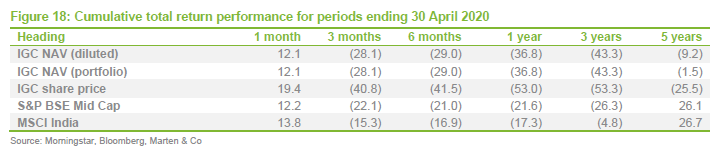

The data in Figures 16, 17 and 18 show returns for both IGC’s published NAV and for an adjusted, ‘portfolio’ NAV. The portfolio NAV removes the dilutive effects of IGC’s subscription shares (which were exercised in full in August 2016) and represents the performance generated by the manager and adviser.

Small- and mid-sized companies have been underperforming in India since 2018 and this trend has been exacerbated by COVID-19. This has weighed on IGC’s relative performance against the MSCI India and S&P BSE Mid Cap indices.

New holdings performing well

There have been some encouraging early signs of progress in redressing stock selection performance. The universe ranking tool, discussed in the investment process section, is seen as adding more factual, numbers-driven rigour to the investment process, as part of processes installed to mitigate behavioural risk.

Over recent months, a weight-adjusted basket (portfolio weights compared to the benchmark) of the new holdings mentioned above, has outperformed the benchmark. Similarly, the manager’s selling activity has been adding value. A concerted effort has been to reduce the portfolio’s exposure to India’s underperforming banking sector. Stocks that have been sold include: Indian Bank, Yes Bank, Motherson Sumi Systems and Jammu & Kashmir Bank.

Performance attribution

Ocean Dial kindly supplied us with performance attribution data for IGC’s portfolio relative to its benchmark. This covers both the five-year period and the three-month period ending 30 April 2020.

Looking first at the long-term picture, at a sector level, the portfolio’s longstanding underweight exposure to the energy sector accounted for 4.2% of the fund’s underperformance of its benchmark. An underweight exposure to health care cost 2.1%. The underweight to energy reflects the adviser’s longstanding aversion to business models driven by global commodity prices.

These adverse sector stances were offset by an overweight exposure to materials, which added 3.5% to relative performance, (chiefly cement companies, which have often been good investments for IGC) and the absence of any utilities exposure in the portfolio, which added 3.0%. The latter position reflects the adviser’s reluctance to have exposure to State-owned enterprises or business that are heavily reliant on them.

Overall, sector allocation was a net positive to relative returns over the five years ended 30 April 2020. The same cannot be said for stock selection.

Manpasand Beverages share price collapsed in 2018 when its auditor resigned (see our June 2018 note). Welspun was hit by accusations that it mislabelled some of its products as Egyptian cotton (see our October 2016 note). Emami’s share price fell when the founding family was forced to sell stock which it had pledged as collateral for a loan (see our October 2019 note). Ramkrishna Forgings and Motherson Sumi are victims of slowing economic growth and weak export markets.

The effects of COVID-19 on performance

In absolute terms over the three months ended 30 April 2020, the best-performing sector was healthcare, while financials, real estate and IT were hit hardest. The poor performance of IT shares in India is somewhat inconsistent with the general performance of technology equities globally. This probably reflects the large business outsource sub-sector within Indian IT. Overall, sector selection added 1.7% to returns.

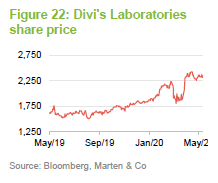

Looking at absolute contributions to performance in stock selection terms, some stocks were able to deliver gains over the period. Chief of these for IGC were the holdings in Divi’s Laboratories, Aurobindo Pharma and PI Industries, the first two of which are health care stocks (India’s pharmaceutical sector is one of its strengths and, the adviser believes, a great hope for the future of the country) and the latter stock is an agrochemicals company.

We highlighted Divi’s Labs and Aurobindo Pharma in our November 2018 report on IGC.

Divi’s has been a real success story, but also illustrates how dramatically the fortunes of these companies can change in a relatively short space of time. Back in 2017, the stock was hit by an FDA investigation into drug manufacturing facilities across India, including Divi’s facilities. Gaurav advised that IGC increase its position in the company and IGC has benefitted as the share price has recovered since. Divi’s is a core supplier to many of the world’s leading pharmaceutical companies.

Also within healthcare, generics drugs company Aurobindo Pharma has performed very well so far this year – its shares are up over 40%. The adviser suggests that the recent technical breakout in the shares (see Figure 23), reflects current sentiment. Aurobindo supplies active pharmaceutical ingredients to pharma companies globally and its own product portfolio includes antibiotics, anti-retrovirals, cardiovascular and central nervous system drugs.

IGC has additional exposure to this area through a holding in Neuland Laboratories (1.6% of the portfolio). It thinks that the pharmaceutical industry will be looking to de-risk global drug supplies by increasing diversification of sources away from China, to India’s benefit.

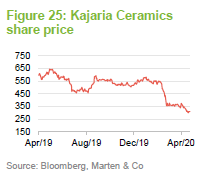

Companies that are particularly cyclically exposed to the downturn have led declines. Kajaria Ceramics and JK Lakshmi Cement have been amongst these, following the curtailment in construction activity. Bajaj Consumer Care’s presence is probably more surprising.

Peer group comparison

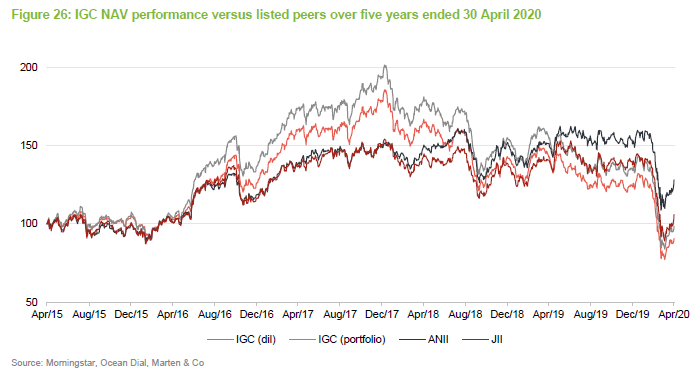

Compared to its listed peer group of three funds (Aberdeen New India, JPMorgan Indian and Ashoka India Equity), IGC follows a smaller-cap strategy. Ashoka is probably most similar in style to IGC. However, as is this case with all of the peer group IGC’s peer group, there continues to be very little overlap in the stocks held. Ashoka launched relatively recently, in July 2018, so is therefore excluded from Figure 26.

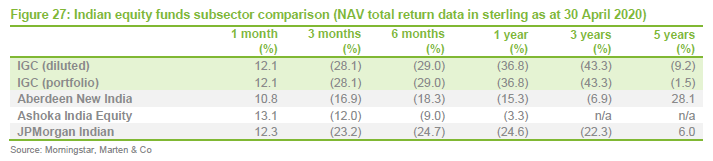

As Figure 27 shows, IGC outperformed Aberdeen New India and JPMorgan Indian up until; early 2018. In the period since, small- and mid-cap stocks have lagged larger ones, weighing down on IGC.

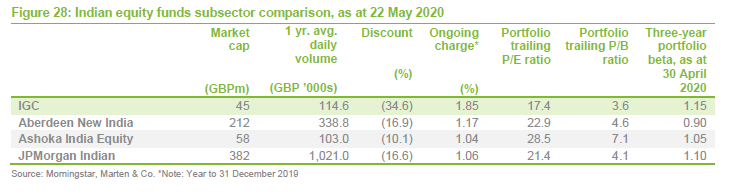

IGC is the smallest of the four UK-listed India-focused funds. Though performance over the past year has suffered, this has been true for all four funds – only Ashoka India has come close to a positive total return over the past year. Given that the none of the listed funds pay much in the form of income and the fact that IGC’s portfolio trades at a deep discount, based on data from Morningstar, its discount does seem overly wide.

IGC’s small-cap bias and the deeper discount of its portfolio suggests it has the most to gain from India successfully managing the re-opening of its economy and the implementation of the $266bn stimulus. This is without considering the discount to its peer-group.

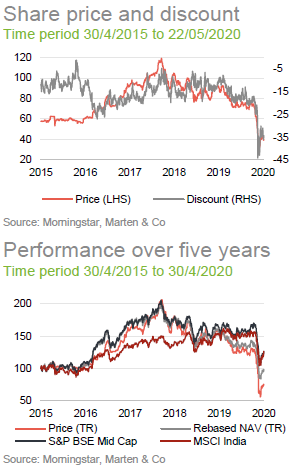

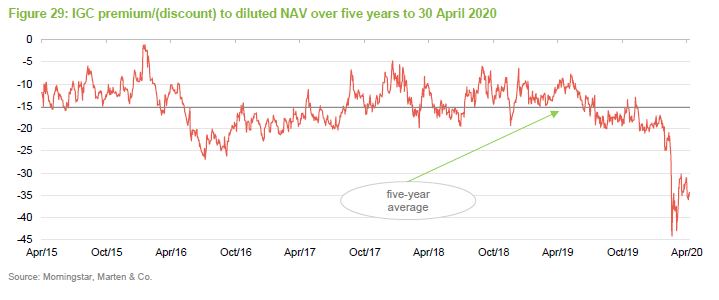

Discount

IGC’s discount has widened sharply since March 2020.Over the year to the end of April 2020, it traded within a range of (44.1%) to (7.8%) and. At 22 May 2020, the discount was (34.6%).

A catalyst for a narrowing of IGC’s discount would be an improvement in sentiment towards small-cap Indian stocks, which could be on the horizon as more details of the stimulus package emerge.

Should the portfolio companies start to perform better, this is likely to provide momentum for the discount to narrow, as more focus turns towards attractive valuations and India’s long-term opportunity to widen its manufacturing base.

As discussed on page 7, 30% of mid-cap stocks in India were trading at below -1 standard deviation, compared to their five-year averages at the end of April 2020.

Fund profile

IGC is an investment company listed on the Main Market of the London Stock Exchange. It invests in India, predominantly in listed mid- and small-cap Indian companies. The trust is aiming to generate capital growth for shareholders. IGC has not paid dividends in the past and the manager says it is unlikely to do so in the near future.

Management arrangements

IGC has been managed since 2010 by David Cornell of Ocean Dial, a company owned by Avendus Capital Private Limited, which in turn is backed by KKR. He has been assisted in this, since November 2011, by Gaurav Narain (Gaurav or the adviser) of Ocean Dial Asset Management India Private Limited, which is based in Mumbai. Gaurav has over 25 years of experience in Indian capital markets, having started his career as vice president of research for SG Asia. The seven-strong investment team is split between London and Mumbai. Each of the analysts is assigned responsibility for a number of industry sectors. The manager is responsible for monitoring portfolio risk and all dealing is done from London.

Ocean Dial manages two funds investing in India, IGC and an open-ended fund, Gateway to India fund. Ocean Dial had AUM of US$122.2m as at the time of publication. Employees of Ocean Dial collectively hold 403,822 shares in IGC, while members of IGC’s board collectively own 92,500 shares between them. Combined Ocean Dial employees and the three directors hold 0.4% of IGC’s issued share capital.

IGC invests through a Mauritian subsidiary (ICG Q Limited) in a portfolio of Indian securities. Changes to the Indian tax regime in 2018 mean that ICG Q Limited is now liable to pay capital gains tax at 15% on short-term gains and 10% on its long-term (over 12 months) gains. IGC will accrue any potential CGT liability in its NAV. Given the manager and adviser’s focus on holding companies for the long-term, it might be reasonable to expect that the bias will be to the realisation of long-term gains. No CGT was accrued as at 31 December 2019.

Index comparators

IGC’s main focus is on Indian mid- and small-cap companies, but the fund can and does hold large-cap stocks as well. The board and the manager use the S&P BSE Mid Cap Index (total return) for performance evaluation purposes, although the portfolio is not constructed with reference to this index.

Previous research publications

Readers interested in further information about IGC may wish to read our earlier notes listed in Figure 30. All of these are available on our website, www.quoteddata.com.

We have written notes that explain how the fund works:

- “Discounted value” published in October 2019 looks at the value within the trust’s portfolio following a period of disappointing economic growth in India

- “Shakeout uncovers value”, published in November 2018, looks at how ICG still sees value in their portfolio despite a slide in the Indian market mainly due to the price of oil

- “A return to earnings growth“, published in June 2018, notes how ICG’s portfolio is increasing with a focus on mid-and-small-cap companies delivering superior performance

- “Moving to the main board“, published in January 2018, describes ICG’s move to the premium listing segment of the London Stock Exchange main market

- “Full steam ahead“, published in March 2017, with strong performance and soild conditions in India IGC’s main focus now is driving down the discount on its shares

- “India at a significant discount“, published in October 2016, looks at a boost in net assets from converted shares while at the same time IGC’s discount has widened compared to peers

- “Indian powerhouse“, published in July 2016, talks about IGC’s discount gap and how India’s economy is in a good place for earnings and growth

- “Compounding machine“, published in March 2016, introduction to IGC and how they are they only London listed fund with a portfolio of small and mid-cap Indian companies

Appendix 1 – investment advisory team leadership

Gaurav Narain – co-head of equities

Gaurav Narain joined Ocean Dial in November 2011 and has been involved with the Indian markets for the past 25 years. He has held senior positions as both a Fund Manager and an equities analyst for New Horizon Investments, ING Investment Management India and SG (Asia) Securities India. He holds a Master’s in Finance and Control and a Bachelor of Economics from Delhi University and is based in Mumbai.

Tridib Pathak – co-head of equities

Tridib Pathak has a career in the Indian financial markets that spans over thirty years with stints in project finance, credit analysis and latterly pan-Asia equity research for UBS Securities. His buy-side career began in 1999 since when he has been investing in Indian equities for both domestic and international investors at firms including Lotus Asset Management and DBS Cholamandalam where he served as CIO. Tridib joined Ocean Dial in 2019 from the Enam Group where he was Senior Portfolio Manager for four years. He is a Chartered Accountant from the Institute of Chartered Accountants of India.

Shahil Shah – assistant fund manager

Shahil Shah was part of the original investment team which was set up in 2005 and specialises in Telecommunications, Consumer, Healthcare, and Media sectors. He holds a Master’s in Commerce and Finance from Mumbai University and is based in London. Shahil supports the Co-Heads of Equities in the day to day maintenance of the funds.

Saurabh Chugh – analyst

Saurabh Chugh was the part of the original investment team and joined in 2006. He specialises in Information Technology, Energy, Transport, Infrastructure and Soft Commodities. He holds an MBA in Finance from Nirma Institute of Management, Ahmedabad and is based in Mumbai.

Ankush Kedia – analyst

Ankush Kedia joined Ocean Dial team in April 2018 and is based in Mumbai. He has 12 years of investment experience in public markets and private equity. He previously worked for Avezo Advisors (a division of Avendus Capital) as Principal and Co-fund Manager focusing on private equity style investments in small and mid-cap listed companies in India. Prior to Avezo, Ankush worked with Mayfield Fund and Axis Bank. Ankush holds an MBA in Finance and Economics from XLRI, Jamshedpur and BTech in Mechanical Engineering from IIT Roorkee.

Ashutosh Garud – analyst

Ashutosh Garud joined Ocean Dial in 2020 after working as Associate Portfolio Manager in the Avendus Wealth Management Team. Prior to joining Avendus, Ashutosh worked with Reliance Wealth Management. Ashutosh holds an MBA in Finance from Chetana Institute of Management Studies, a Bachelor of Commerce & Economics from Mumbai University and is a CFA charterholder.

Saurabh Rathore – analyst

Saurabh Rathore joined Ocean Dial team in January 2020 and is based out of Mumbai. He has 3 years of experience in financial services across global markets, investment analysis and due diligence, business strategy and risk management. Prior to Ocean Dial, Saurabh has been associated with Avendus, Credit Suisse and J.P. Morgan. Saurabh holds a B.E(Hons) in Electrical and Electronics Engineering from BITS-Pilani and an FRM Charter and has cleared CFA Level-III examination.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on India Capital Growth Fund Limited.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.