It is 10 years since the worst of the financial crisis, and almost six years since Polar Capital Global Financials Trust (PCFT) was launched to take advantage of low valuations in the financial sector and to offer investors a lower risk way of accessing the sector.

It is 10 years since the worst of the financial crisis, and almost six years since Polar Capital Global Financials Trust (PCFT) was launched to take advantage of low valuations in the financial sector and to offer investors a lower risk way of accessing the sector.

Yet financial stocks (banks in particular) have lagged broader markets since then. This is despite banks rebuilding their balance sheets, a recovery in their profit margins, bad debts at multi-year lows and, crucially for PCFT, which is designed to offer an attractive and growing yield, restrictions on dividend pay-outs being eased.

PCFT’s managers acknowledge the signs that the global economy is slowing, but think investors’ fears of a return to 2008 (the global financial crisis) for the banking sector are misplaced. Regulatory actions and management’s burnt fingers have restricted bank lending over the past decade. Individuals and businesses have still been borrowing enormous sums, but the money has been coming from non-bank lenders. It is they who will have to deal with any surge in defaults and, if this reduces competitive pressures in the lending sector going forward, that will be good news for banks.

Growing income from financials stocks

Growing income from financials stocks

PCFT aims to generate a growing dividend income, together with capital appreciation. It invests primarily in a global portfolio, consisting of listed or quoted securities issued by companies in the financial sector. This includes banks, life and non-life insurance companies, asset managers, stock exchanges, speciality lenders and fintech companies, as well as property and other related sub-sectors.

Contents

- Fund profile

- Market outlook

- Investment process

- Asset allocation

- Performance

- Dividend

- Discount

- Fees and costs

- Capital structure and life

- Gearing

- Management

- Board

Fund profile

Polar Capital Global Financials Trust (PCFT) launched on 1 July 2013 and has a fixed life that expires in May 2020. Its twin objectives focus on growing investors’ income and their capital. It invests globally, making it a useful alternative for UK-based investors looking to diversify their financials exposure.

Predominantly, the portfolio is invested in listed/quoted securities. The trust may have some exposure to unlisted/unquoted securities, but this is not expected to exceed 10% of total assets at the time of investment.

The trust was benchmarked against the MSCI World Financials Index from launch until 31 August 2016. Then, when MSCI spun the Real Estate sector out of the Financials index, the benchmark became the MSCI World Financials plus Real Estate Net Total Return Index (in Sterling) – effectively a continuation of the pre-September 2016 benchmark. QuotedData thanks the managers for providing us with data on the reconstituted benchmark.

PCFT’s Alternative Investment Funds Manager (AIFM) is Polar Capital LLP and the lead managers are Nick Brind and John Yakas. More information on the management team is given on page 16.

Market outlook

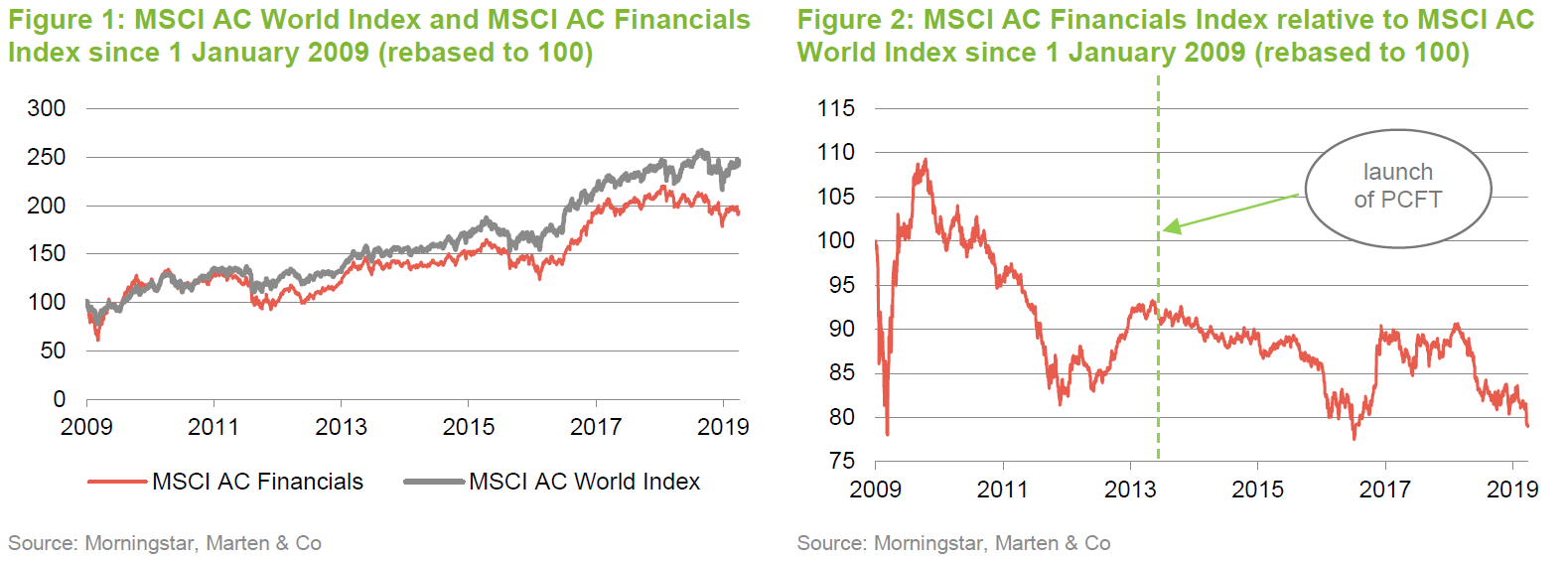

Financials are the largest of the industries that make up global stock markets (16.6% of the MSCI AC World Index at the end of March 2019) but, as Figure 2 shows, they have acted as a significant drag on the global index’s performance since the bottom of the global financial crisis in 2009. There are several factors at work here, including a slowing global economy, political uncertainty in Europe (Brexit/Italian politics) and the shift from quantitative easing or QE to tightening, but PCFT’s managers believe that the sector is now undervalued. They say that the discount of the financials sector relative to the wider market is as wide as it has been in 2012 and 2016. Notably, the sector has also underperformed since PCFT’s launch.

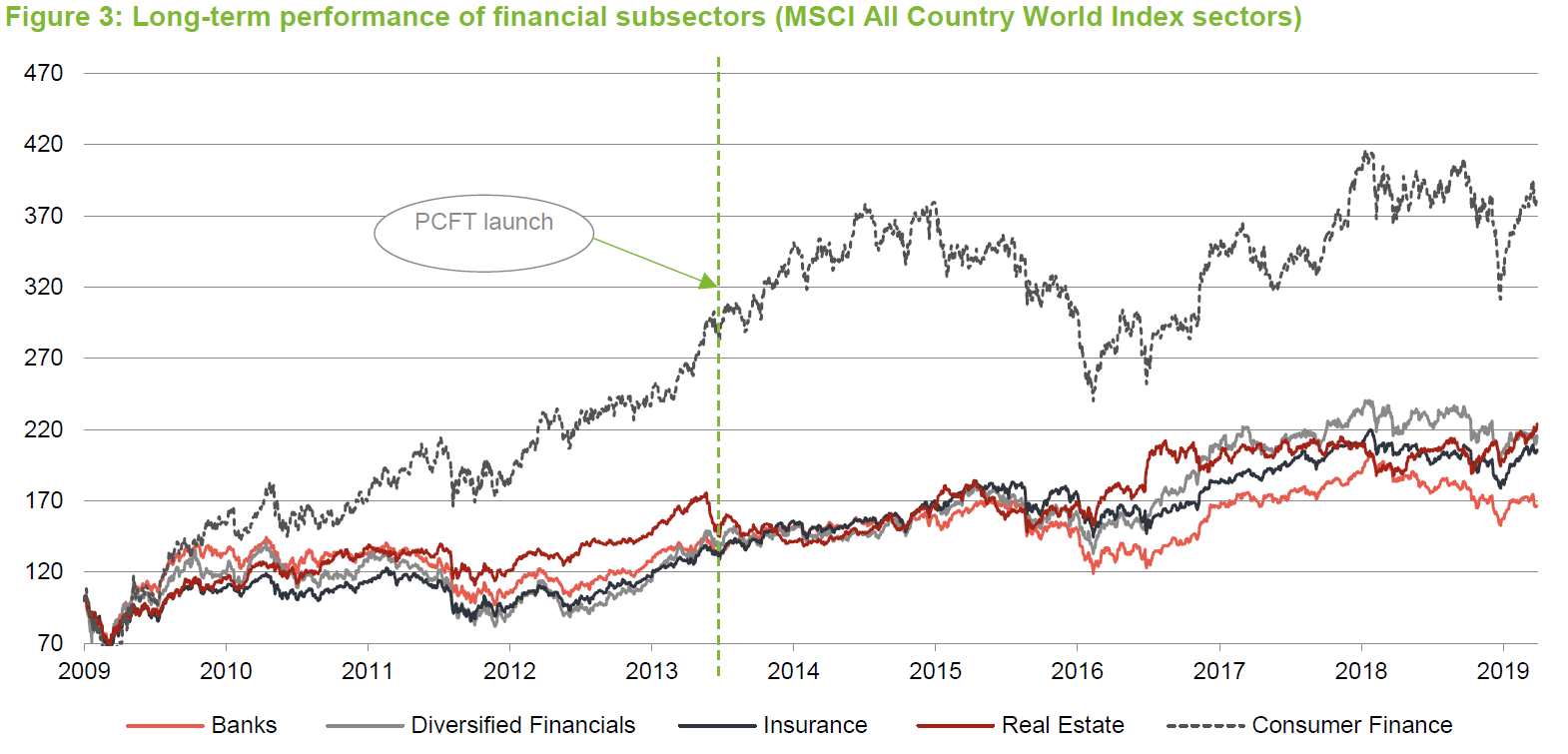

Within the financials index, the largest subsector is banks (diversified banks were 48.5% of the MSCI AC World Financials Index at the end of March and regional banks accounted for a further 4.5%). As Figure 3 shows, banks have lagged other parts of the financials sector since 2009, and have also underperformed since PCFT launched in July 2013, (note consumer finance is a subset of diversified financials).

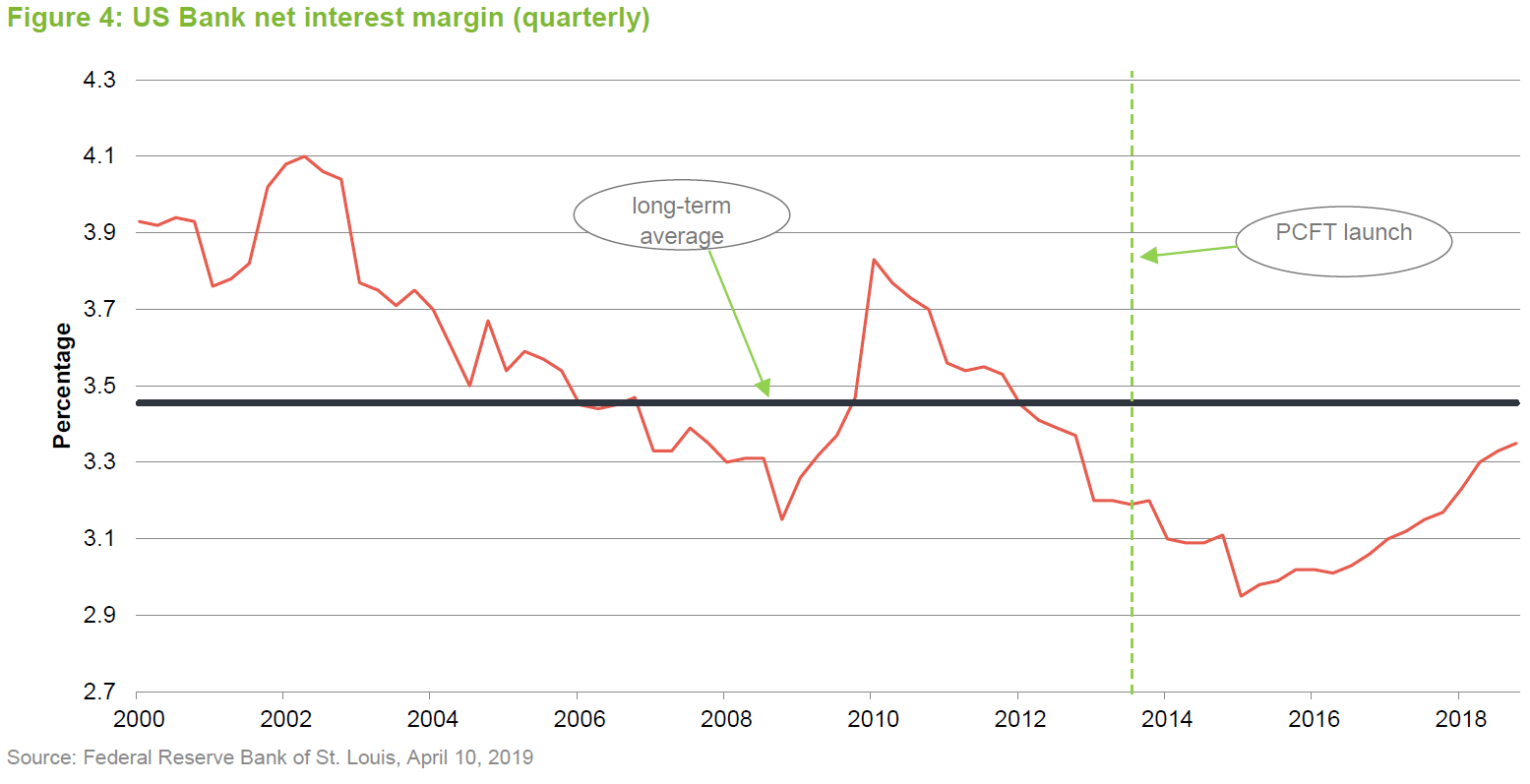

One reason why banks may have lagged is that for all of the period since PCFT’s launch, banks’ net interest margins (the gap between the interest they pay on deposits and other forms of funding, and the interest they receive from borrowers) have been below their long-term averages. As Figure 4 demonstrates, they have at least been on an improving trend. The managers point out that margins are a reflection of balance sheet risk/mix and so, as the banking system writes lower risk lending going forward, its margins are unlikely to ever recover to levels seen pre-2008. Nevertheless, risk adjusted returns should be better, as most of the riskiest lending is now being carried out by the non-bank lenders.

The US central bank, the Federal Reserve (Fed), recently reversed its policy and said that there would be no interest rate rises in the US in 2019. The managers acknowledge that this may affect sentiment towards the sector (interest rate rises present opportunities for banks to expand their margins) but say the sector was not riding high on the prospect of rate rises in any case, and the market reaction to the news has not been too bad.

Absence of loan growth?

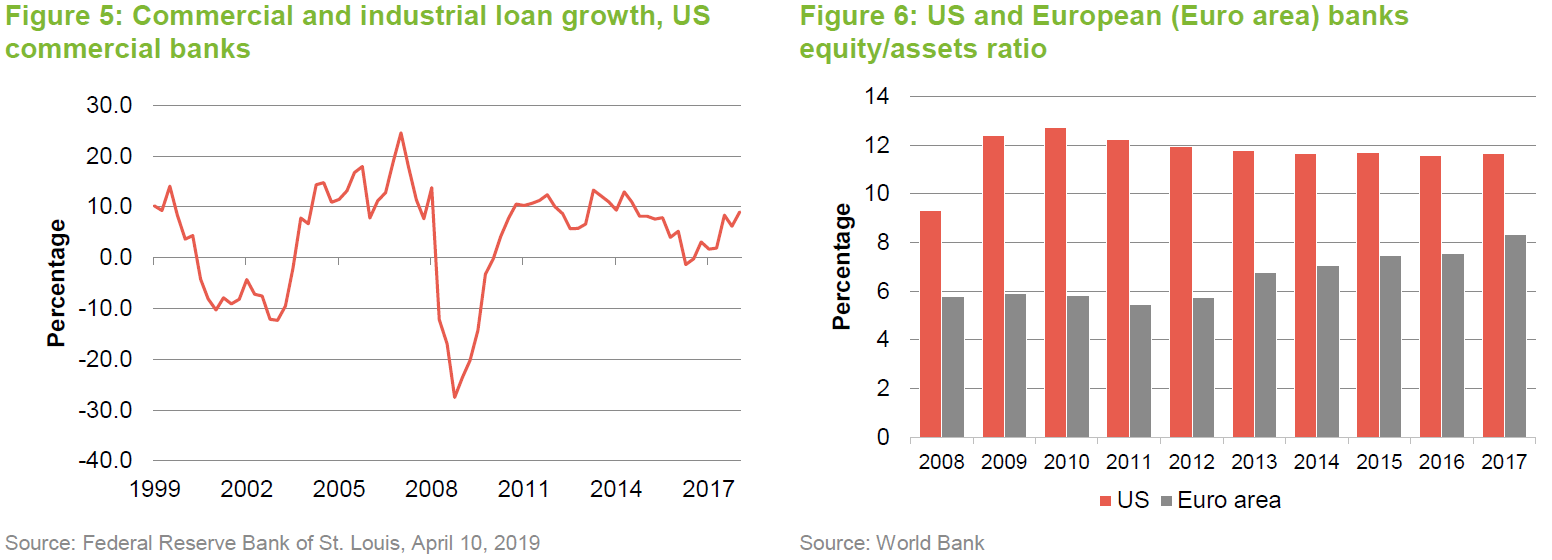

Bank loan growth has recovered since the financial crisis, but remains well below the highs of 2005/2008 (as the credit bubble inflated) and has been lagging GDP growth. Part of the reason for this may have been the regulator’s insistence on banks rebuilding their balance sheets, but the banks will also have been mindful of their experience in 2008.

The good news is that US banks are reasonably well capitalised, more so than European ones (although the equity/assets ratio for European banks has been improving). Where banks have stood aside, non-bank lenders have stepped into the breach. Private loan markets have boomed, aided by a resurgence in demand for loans to put into securitised structures in the form of collateralised loan obligations (CLOs). The influx of non-bank lenders may have helped to depress banks’ margins.

Balance sheet lending from alternative lending firms such as Lending Club is, in the managers’ opinion, just a form of regulatory arbitrage (these lenders are not subject to the restrictions that were imposed on banks as a way of addressing the problems caused by the global financial crisis). China is clamping down heavily on the subsector and the managers expect that this will happen elsewhere. Furthermore, there is a suspicion that many of the customers attracted by these lenders are of lower quality. That view might be reinforced by the recent news that Funding Circle SME Income Fund was throwing in the towel after predicting higher-than-forecast losses on business written in 2016/17. The managers note a similarity between some of the alternative finance companies and those of small banks trying to grow by pricing aggressively (offering loans at interest rates that might not reflect the risk being taken on) and funding wholesale rather than with deposits. Wholesale funding from a variety of sources, including other financial institutions, can dry up quickly or become much more expensive when investors become more risk averse).

The managers conclude that banks have not been taking excessive risk and that this should stand them in good stead if the cycle turns.

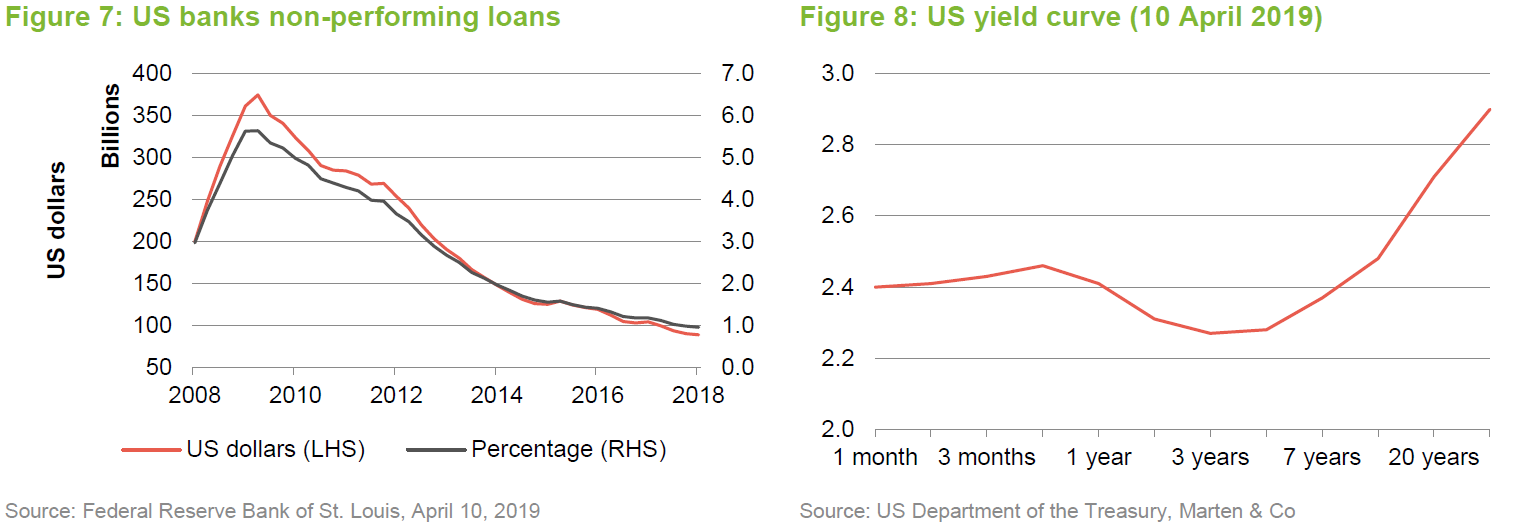

Non-performing loans (where the borrower has missed interest payments or failed to repay all or part of the loan when it was due) are not a problem currently, as Figure 7 shows. However, the US yield curve, which shows how the interest payable on US government borrowing varies according to how long the money has been borrowed for, is fairly flat and inverted (the long-term rate is lower than the short-term rate) out to seven years. This is one of a number of indicators that suggest, based on past experience, that we are approaching the end of the current economic cycle. Investors may now be worrying about an uptick in defaults. The consequence is that in the developed world, the banking sector underperformed quite markedly in 2018.

The managers agree that the economy is slowing, but they do not think that banks are going to be hit hard when the cycle turns down. They say that the warning signs that signalled past problems for the sector are not there today and, therefore, whilst margins may not rise from current levels, peak provisioning for bad debts may not be as high as in previous cycles. Their reasoning is that the bulk of loan growth that has occurred in recent times has been the responsibility of non-bank lenders rather than the banks themselves. If the non-bank lenders are hit disproportionately, as the managers suspect, their capacity to lend will be constrained and that could translate into improved margins for the banking sector as it faces lower competitive pressures.

Managers believe the sector’s income is sustainable

Crucially, given the income side of PCFT’s objective, the managers think that the banks can sustain and even increase distributions to shareholders. The banks have strong balance sheets, and payout ratios (the relationship between dividends and earnings) in the US are fairly low but the profitability of US banks is quite high. Returns on assets (ROAs) have recovered from their post-crisis lows. The managers say that ROAs between 1% and 2% are good for banks operating in mature markets. It is true that returns on equity (ROEs) are not as high as they were before the crisis, but this reflects the increased strength of banks’ balance sheets (more equity = a stronger balance sheet).

Technological innovation

One factor that has unnerved some investors in the sector is the rise of fintech (technological innovation in the financial sector), which accounts for about 7% of PCFT’s portfolio (including its holding in Mastercard). There is a common belief that disruptive new entrants are going to drive down margins and capture significant market shares in a range of financial services. The managers say that it is too early to provide an assessment of who the ultimate winners will be. We are in the early stages of financial services disruption and it is important to remember that banks are reacting to the threat. Nevertheless, the managers will look to exploit opportunities where they can.

For PCFT’s managers, accessing fintech creates a structural challenge; most of it is held by private equity (PCFT does have one unquoted holding, Atom Bank – see page 11). The managers note that in assessing fintech companies, there is a balancing act between their high valuations and correspondingly low dividend yields versus PCFT’s income requirement to be taken into consideration.

Companies that process payments, for example, sit on very high valuations. The managers do not think that this is necessarily justified – they cite a comparison between Mastercard and Square, for instance. In Q4 2018, the former processed $1.5trn of payments and made substantial profits, while the latter processed $23bn of payments and made a loss. Mastercard’s business is 65x larger than Square’s, but its market cap is less than 8x larger. The managers point out that the payments industry is always likely to be a heavily commoditised/regulated industry. Given this, they would prefer to hold a, hard-to-dislodge, incumbent.

In general, many of the ‘revolutionary’ advances in financial services that fintech offers can be and are being adopted by incumbent businesses. It is true that legacy software systems need to be replaced/upgraded. Some companies responded by creating new standalone businesses – HSBC’s First Direct is a good example of this. However, most are investing in existing operations and many have research and development budgets that far exceed those of the leading fintech companies (the managers point to data from Autonomous Research, which suggests Bank of America and JPMorgan are both investing more than twice as much as Chinese fintech company, Ant Financial and three times as much as PayPal, for example).

Where the new businesses struggle most is in customer acquisition. Financial services customers are notoriously ‘sticky’ and will often only move to access services that are given away for free – not a recipe for making money. The managers do see the potential for some dynamic, customer-focused businesses to expand into financial services. Amazon might be a good example of this.

Many millions of words have been written about blockchain. The managers can see some advantages for some firms from the use of the technology (notably, the prospect of lower transaction costs), but they point out that many so-called blockchain companies have very tenuous links to the technology.

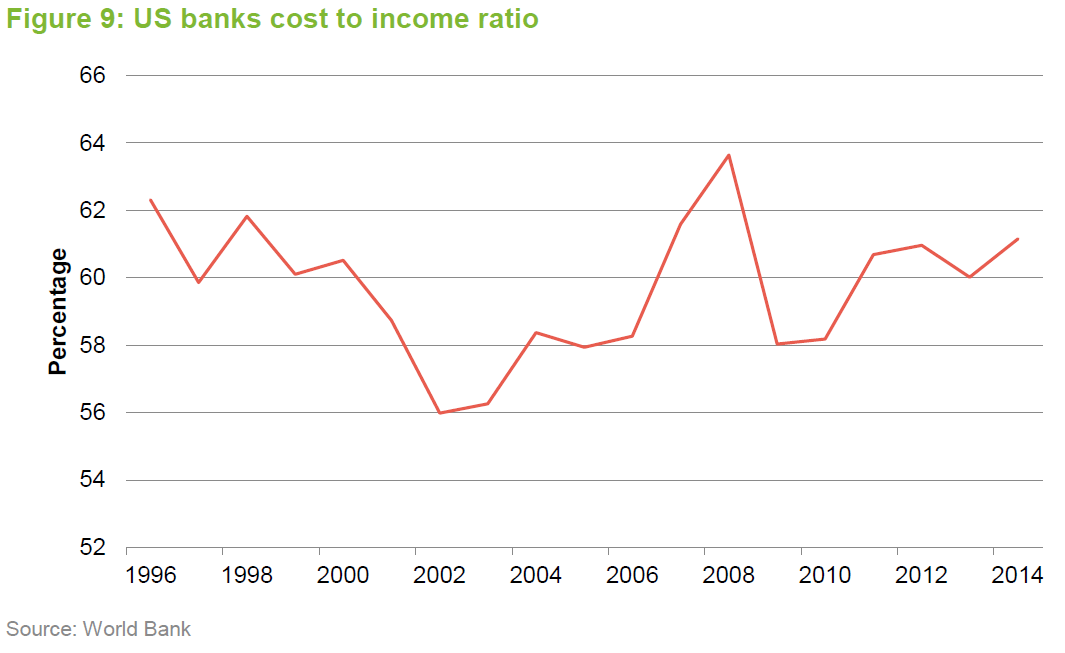

Figure 9 shows the cost to income ratio of US banks from 1996 to 2014, a period of considerable innovation. What is remarkable is how stable the ratio is. The managers say that cost-cutting is just given away in lower pricing. It seems likely that whatever advantages that blockchain brings will go the same way.

Regulation being eased

There is a strong argument that bigger is better in the banking world. Big banks have strong franchise values and find it easier to attract and retain customers. In May 2018, US lawmakers amended the 2010 Dodd-Frank Wall Street Reform Act to raise the $50bn threshold at which a bank is considered systemically important to $250bn. Effectively, this opens the door to a new wave of consolidation within the US banking industry. Only the three biggest banks remain blocked from making acquisitions. There has been an uptick in deals since the reforms – the recent tie-up between BB&T and SunTrust, for example – but the managers think there could be more to go for.

At the other end of the scale, in a further sign that the post-crisis regulatory environment is being relaxed, sub-$10bn banks are no longer covered by the Volcker rules. This means that they can use their own capital for proprietary trading. This relaxation may not affect these small banks much, but it could presage rule changes that make investment banking more profitable.

End of curbs on dividend pay-out ratios

One change that is particularly good news for PCFT is that the Federal Reserve has lifted a soft cap on dividend pay-out ratios (as bank balance sheets are stronger than they were). This could lead to a boost in PCFT’s revenue account.

Structural attractions in emerging markets

There was a significant bias towards emerging markets within the portfolio at launch (about 22% of the portfolio), predicated on superior economic growth, a growing middle class and a relatively low penetration of financial services products. However, a combination of factors, including a strengthening US dollar, encouraged more of an emphasis on US stocks and today emerging markets represent about 7% of the portfolio. With US rate rises on hold, the outlook for emerging markets could be brighter.

PCFT’s Asian exposure is to stocks that the managers perceive as being high-quality. These are not cheap, but the managers think their ratings are justified by their growth potential. The portfolio has no exposure to the State-controlled banks in China and India, but does hold HDFC Bank. The managers see potential for significant growth in Indian lending products, including the mortgage market, where penetration rates are less than half of those in Thailand and China, let alone developed markets.

The theme of increasing penetration of financial services in Asia is exploited through positions in stocks such as AIA, Tisco Financial and Bank Central Asia.

Investment process

PCFT’s managers are actively involved in the research process and, given their stock-picking approach, this is core to what they do. Their experience is that external research, produced by brokers and investment banks, tends to be quite short-term in focus. This may be because it is aimed at the hedge fund community. For that reason, aided by good access to companies’ management, much more emphasis is placed on in-house research. The extent to which the team uses external research varies by degrees.

Analysis of financial stocks differs from other sectors in that there is a focus on balance sheets. Strong growth in the top-line (revenue before expenses) is not necessarily good news, because this may come at the expense of quality. Risk-adjusted analysis is therefore more useful.

Most financials stocks are very highly geared (their balance sheets have a lot of debt relative to shareholders’ equity), and as a result there is a real need to focus on limiting the downside. Using the same lens as a growth investor, when choosing financials, could catch an investor out badly when the growth cycle turns down. The managers note that, in their experience, it is rare for the best short-term performers to do well over the long-term.

The remit is global and includes emerging markets. The universe is about 500 stocks (the smallest stock that the managers would consider for PCFT’s portfolio would have a market cap of around $500m). The managers say that this is a manageable number of stocks for the team to cover. The likes of Goldman Sachs and JPMorgan are complex beasts, but most banks have relatively simple business models. In many areas, pricing is commoditised and so the sector is quite generic, but research is essential to sort the good from the bad.

The managers use a scoring system to look at a range of variables around risk, growth and value. These include balance sheet strength; how the company is funded; the composition of the loan book; historical quality of the loan book; and trends in margins. This model is a framework for analysis rather than an engine to produce a buy list.

The team meets about 400 companies each year but a lot of this is double-checking their research findings. They talk to customers and competitors, for example.

For banks and similar companies, any assessment of value uses returns on equity and price to book (the relationship between the value that investors place on a business and the money invested in it). The managers find that, for the reasons outlined above, price to earnings ratios and measures of growth do not work as well.

The sector is not just about balance sheet businesses, however, and it is evolving. The managers use a more earnings-driven, traditional approach to valuing other companies.

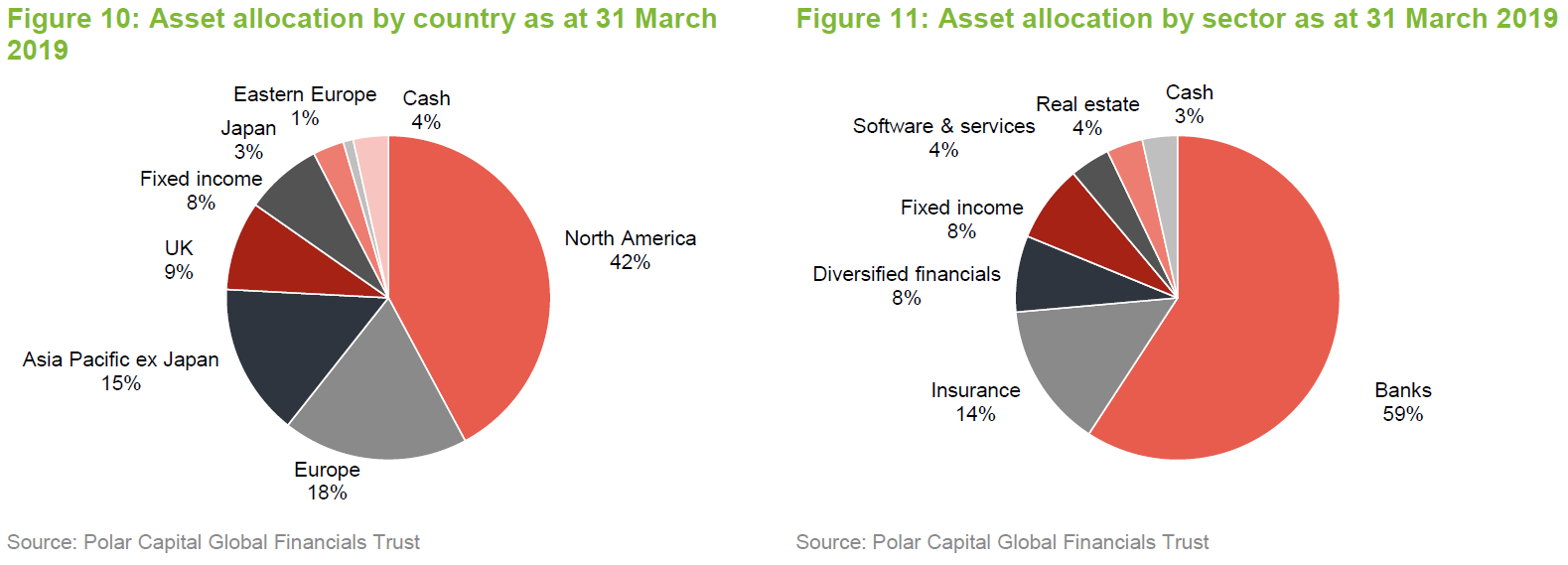

Asset allocation

The US dominates the benchmark. PCFT’s focus on growth of income influences stock selection decisions and, relative to the benchmark, results in a small structural underweight exposure to the US. The fragmentation of the US banking market (there are over 5,000 US banks) allows the managers to make allocations to particular regions within the US.

The UK tends to be about 10% of the portfolio or lower. The managers say that UK banks are just not as attractive as others in the portfolio. Smaller UK banks tend to be biased towards the buy-to-let sector.

At the end of March 2019, there were 71 positions in PCFT’s portfolio. Around 80% of the trust was invested in stocks with a market capitalisation in excess of $5bn, and 3.5% invested in small cap stocks with a market capitalisation less than $500m.

The portfolio includes an element of fixed income, as a way of boosting the yield. Here the emphasis is on an assessment of credit quality (there is a credit analyst within the team). Changes to the regulatory environment, such as Basel III (regulations devised by the Bank for International Settlements) and the EU’s bank recovery and resolution directive (BRRD), have created new opportunities as banks restructure their balance sheets.

Real estate investments offer income but are exposed to interest rate risk. John Yakas, through insight gained in managing Polar’s Asian Opportunities Fund, tends to favour Asian REITs. Currently, these are cheaper than European and US stocks and are operating in an environment of higher economic growth. Relative to the benchmark, PCFT’s portfolio has a significant underweight exposure to real estate (4% versus 16.6% at the end of March 2019).

The trust has some asset management exposure (through Blackstone, the private equity company; and City of London Investment Group, a largely emerging markets and closed-end fund-focused investor). However, for the most part the managers are not attracted to the industry at the moment, given the competition from passive investments such as index-trackers (which is putting pressure on fees) and ever-increasing regulation. There is no exposure to stock exchanges, which the managers consider to be unsuited to their investment approach, because their value tends to reflect the momentum of share prices rather than being based on fundamentals. Within the insurance market, the managers are encouraged by signs of firmer pricing in the property and casualty markets.

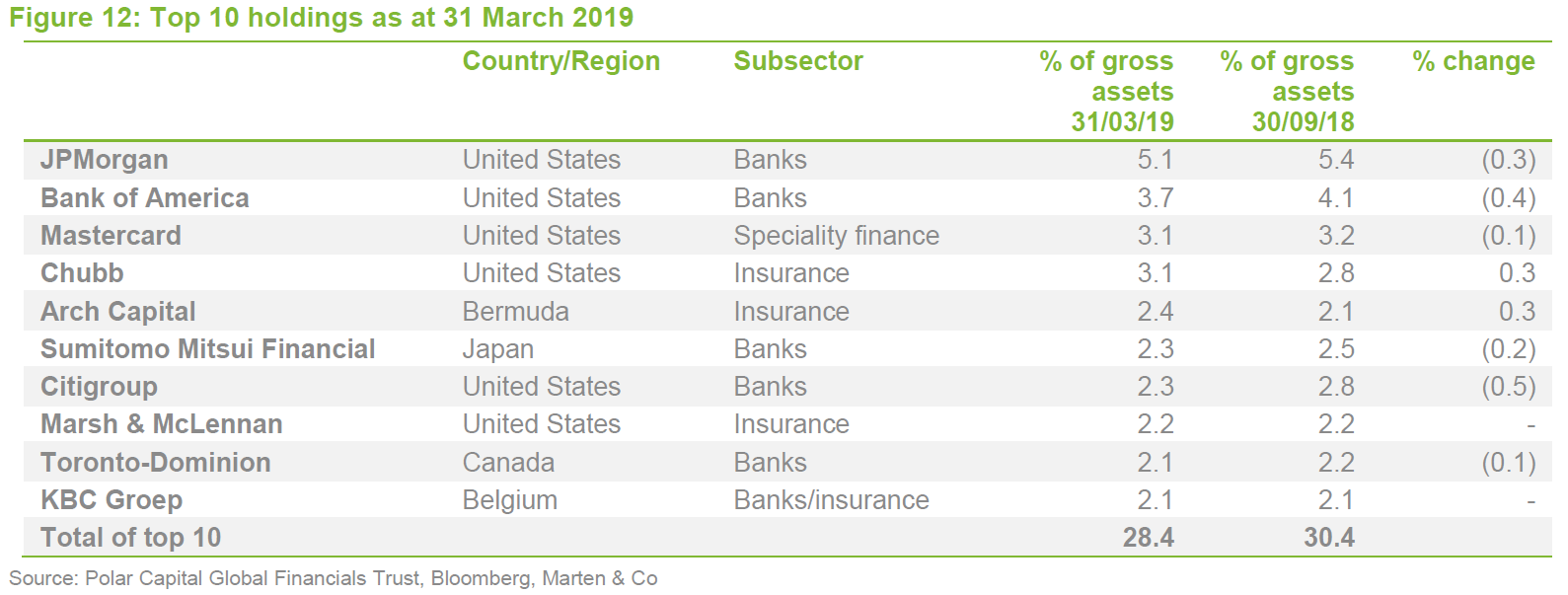

Top 10 holdings

It is noticeable that the composition of the top 10 holdings has not changed much over the past six months, reflecting the managers’ conviction in the portfolio. While four of PCFT’s top 10 also feature prominently in the benchmark, the portfolio is clearly differentiated with notable underweight exposures to Berkshire Hathaway, HSBC and Royal Bank of Canada.

Atom Bank

Atom Bank is PCFT’s only unquoted investment. The holding was valued at £3.2m at the end of September 2018. Atom Bank describes itself as the UK’s first app-only bank. It offers fixed-term savings accounts, mortgages and business loans. It has raised £400m from investors, led by the Spanish bank, BBVA (which now owns almost 40%). At the end of March 2018, it had £1.4bn in retail deposits and had loaned £1.2bn. For the year to the end of March 2018, it lost £53m “in-line with its plans at the start of the year”.

Performance

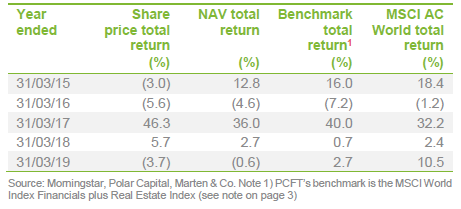

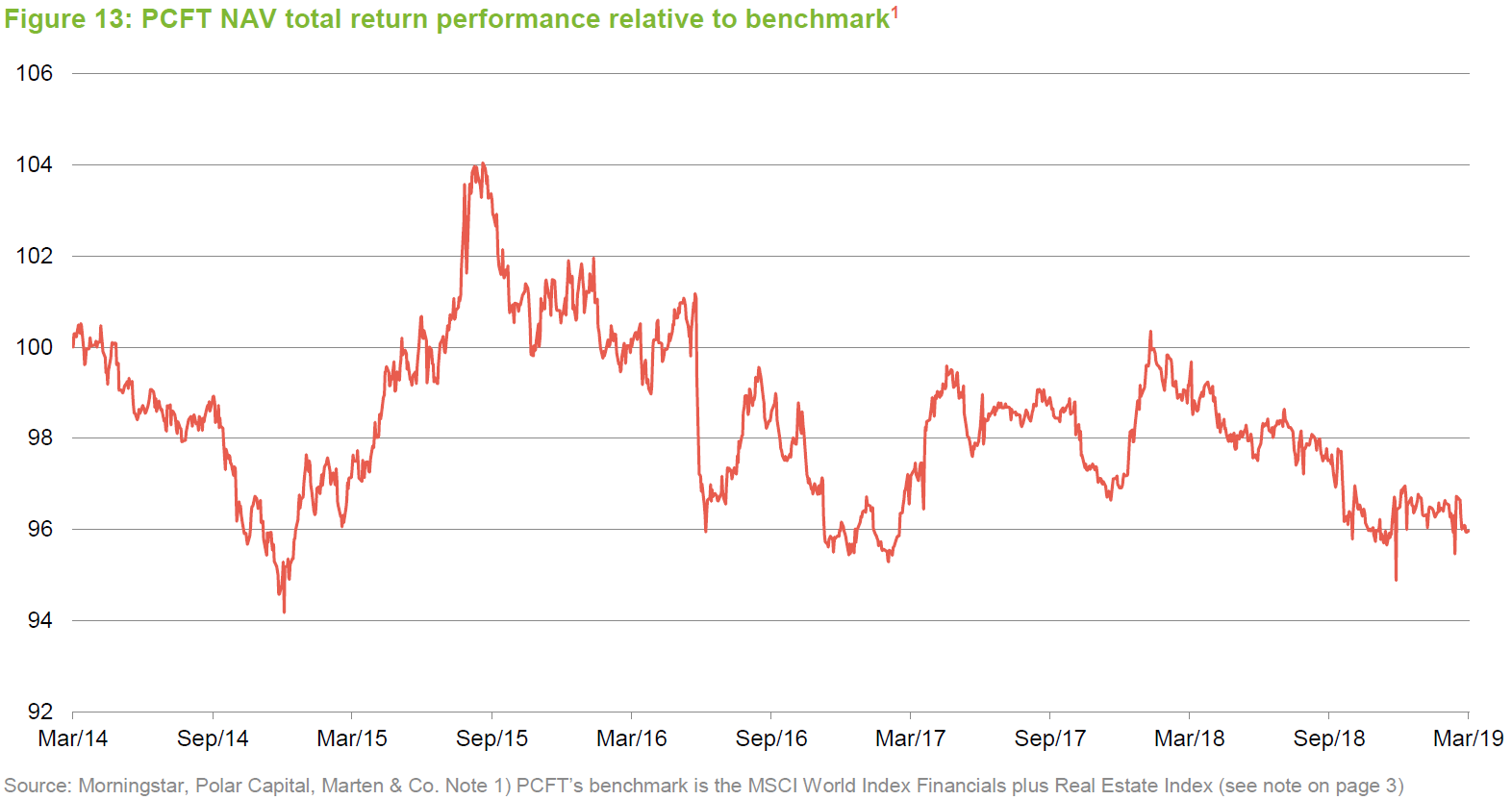

From launch until 31 March 2019, PCFT delivered an NAV total return of 65.1% or around 9.0% a year. In addition, the dividend has grown by an average of 7.0% a year.

The scale on the graph in Figure 13 makes PCFT’s relative performance look more volatile than it is. In fact, PCFT’s performance has matched the benchmark fairly closely since launch. Recent underperformance may reflect the portfolio’s underweight exposure to real estate investment trusts (REITs) and exposure to US banks (both on the back of a halt to US interest rate increases – REITs tend to do better when rates fall, banks often benefit from rates rising); the exposure to India, which was affected by fears of a liquidity squeeze (hitting the non-bank financial subsector) and nervousness ahead of elections (although that has eased somewhat in recent weeks); and accusations levelled at Swedbank that it had facilitated money laundering (the managers topped up the holding subsequently).

Figure 14 illustrates the extent of the financial sector’s underperformance of the MSCI AC World Index. If the managers’ theory that banks are oversold proves correct, PCFT’s relative performance should improve.

Note: no peer group information is included within this report. PCFT’s listed peer group is eclectic and provides a poor comparison. PCFT’s reports tend to compare the trust with the average of the Lipper Financial sector. For the year ended 30 November 2018, PCFT’s NAV total return was 2.4% ahead, in absolute terms, of the average of the 56 open-ended funds in the Lipper sector, and 20.1% ahead since PCFT was launched.

Dividend

PCFT pays dividends semi-annually on its ordinary shares in February and August. All dividends are paid as interim dividends. The payments are not necessarily of equal amounts. The company does not pay a final dividend.

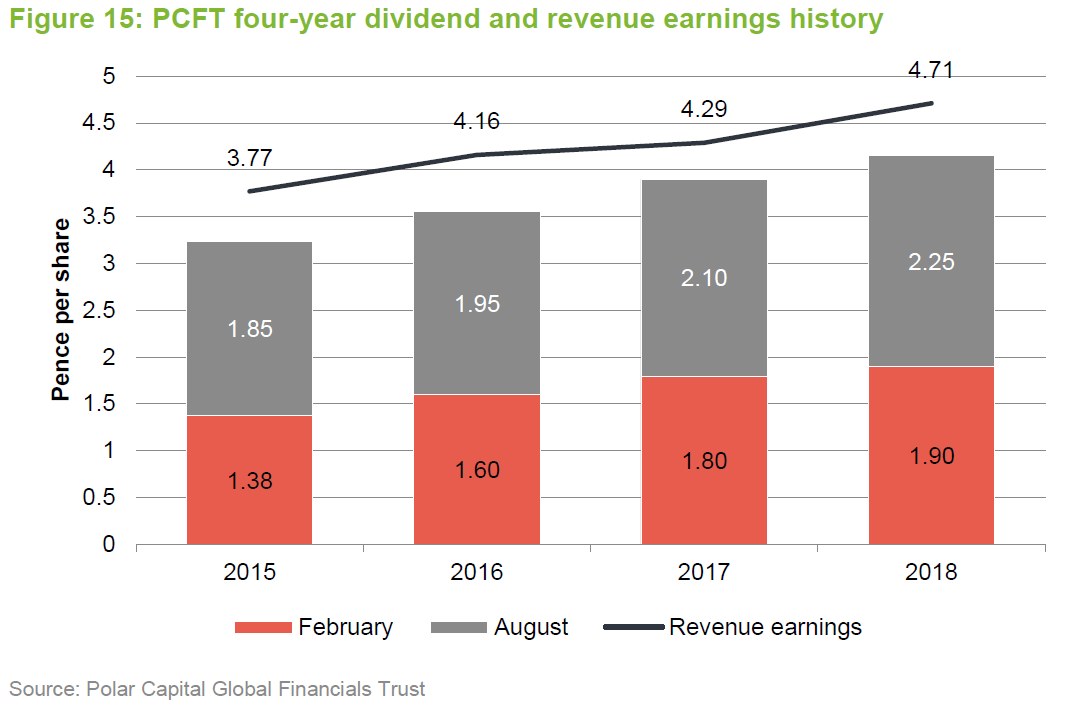

PCFT paid an interim dividend of 2.25p in August 2018. A second payment of 1.90p was declared for the 2018 financial year, to be paid in February 2019, giving a total of 4.15p for the year, representing a 6.4% year-on-year increase. PCFT has grown its annual dividend by an average of 7.6% over the four full financial years since its incorporation in 2013, handsomely achieving its core objective.

2018 revenue generation up nearly 20 percent

Being underweight in its exposure to US financials (particularly REITs) and overweight in European banks (relative to its benchmark in 2018) meant PCFT missed out on some extra revenue generation (European banks tend to be on higher yields than US ones). That said, its managers believe that the investment case for European banks is now more compelling as they have moved back to financial crisis level valuations.

PCFT delivered a solid year of income generation with its revenue return increasing by 19.6% to 4.7p per share, as the underlying trend of banks continuing to return capital through dividends and share buybacks remained intact.

As at November 30, 2018, PCFT had revenue reserves of 2.1p per share (after deducting the 1.90p interim dividend to be paid in February 2019). This is equivalent to half the total dividend for the 2018 year, suggesting that PCFT has some capacity to make up any revenue shortfall going forward (2017 equivalent figure was 38.5%).

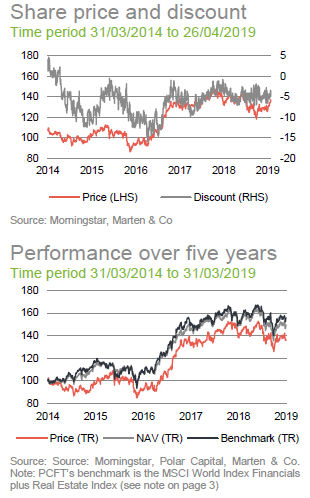

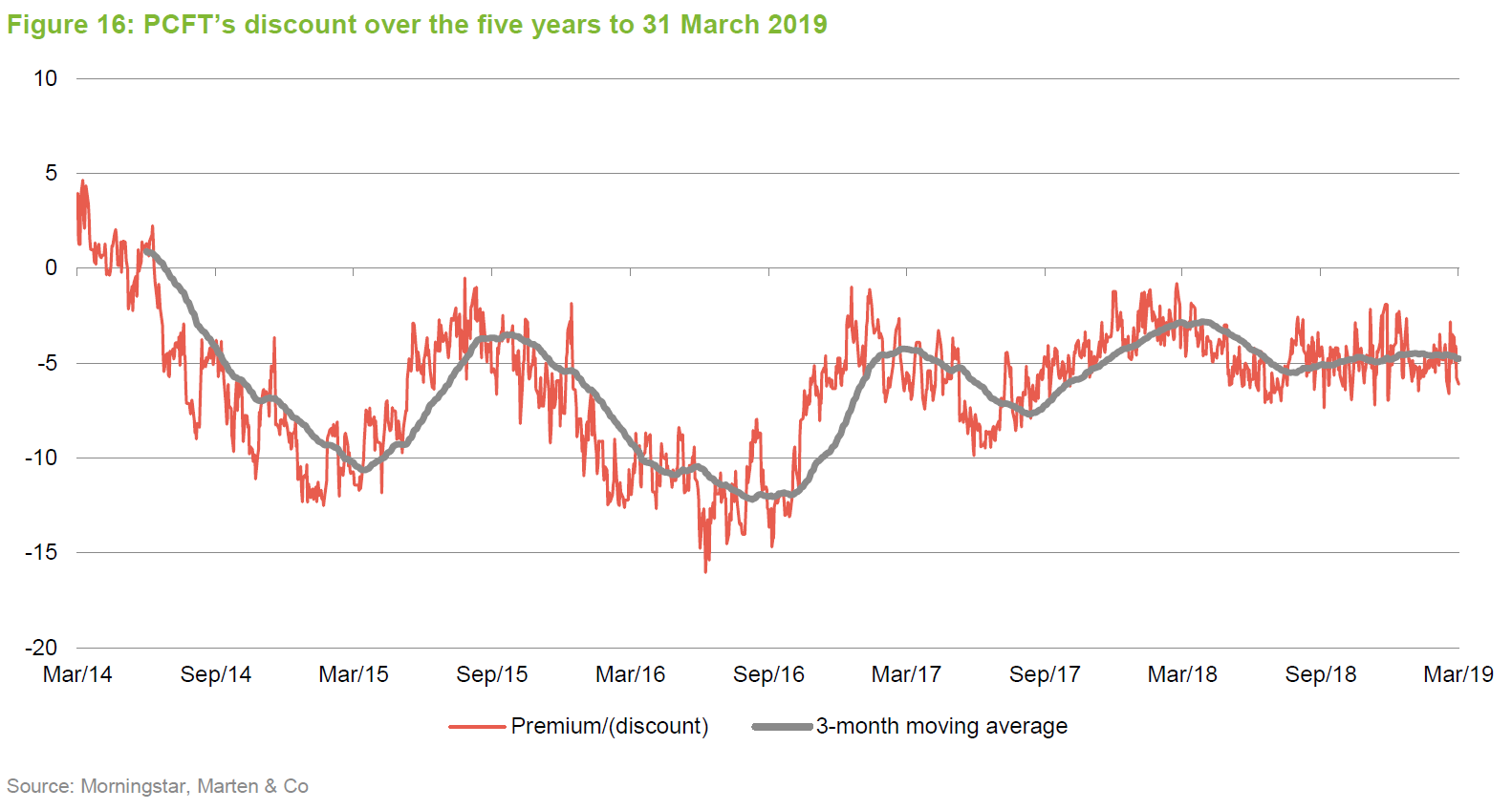

Discount

Over the year to the end of March 2019, PCFT’s discount has moved within a range of 7.4% to 1.8% and has traded at an average of 4.7%. At 26 April 2019, the discount was 4.9%.

At times in its life, PCFT has bought back shares (4.25m in total) as a way of limiting the size and volatility of its discount. The managers observe that the discount has often reflected general sentiment towards the financial sector.

Fees and costs

PCFT pays a base management fee of 0.85% a year on the lower of its market capitalisation and net asset value. Structuring the fee this way incentivises Polar Capital LLP to keep the discount narrow or eliminate it entirely. The base management fee is charged 80% to revenue and 20% to income.

Performance fee payable on PCFT’s liquidation

Polar Capital LLP may also be entitled to a performance fee paid in cash. The fee is calculated and accrues daily but is only payable on the liquidation of PCFT. To date no performance fee has been accrued.

Any performance fee paid will be an amount equal to 10% of the excess return per share (on an NAV basis) over a performance fee hurdle.

The performance fee hurdle is 100p, increased or decreased by reference to the return on the benchmark index plus 1.25p a year (reduced proportionately for periods of less than one full year) over the period from the day following admission to the date on which it is decided to liquidate PCFT.

For the purposes of calculating the performance fee, with regard to the NAV:

• dividends will be reinvested on their pay date (i.e. the NAV total return will be used);

• the dilutive effect of the subscription share issue will be reversed out;

• any enhancement to the NAV from issuing shares at a premium will be reversed out; and

• any enhancement to the NAV from buying back shares at a discount will be reversed out.

The net effect should be that the adjusted NAV return reflects the actual performance generated by the managers after base management fees have been deducted.

Finally, any performance fee payable will be adjusted so that the payment of the performance fee does not leave shareholders with less than 100p per share.

Capital structure and life

PCFT has a simple capital structure with a single class of ordinary shares in issue (subscription shares that were issued at launch were all exercised on 31 July 2017) and trades on the Main Market of the London Stock Exchange. At 26 April 2019, there were 202,775,000 ordinary shares in issue.

Gearing

PCFT’s mandate allows it to employ borrowing from time to time to enhance returns, subject to a maximum of 15% of net assets at the time of drawdown. PCFT has a £30m unsecured facility with ING Bank NV (a £15m one-year revolving facility and a £15m one-year term loan). The term loan has been drawn down in full and is due for repayment on 12 July 2019. The interest rate on this £15m loan is 1.775%.

Liquidation resolution to be voted on in 2020

PCFT refers to itself as a fixed life company. Its articles of association require that, at the seventh AGM in 2020, the directors must put forward a resolution to place the company into liquidation. The voting on that resolution will be enhanced such that, provided any single vote is cast in favour, the resolution will be passed. The seventh AGM is expected to be held in April 2020, but in any event, no later than 31 May 2020.

This does not preclude the possibility that shareholders may decide to extend the life of the trust or take some other action that supersedes the liquidation resolution, which would likely include a follow-on vehicle as well as a cash offer at NAV less expenses.

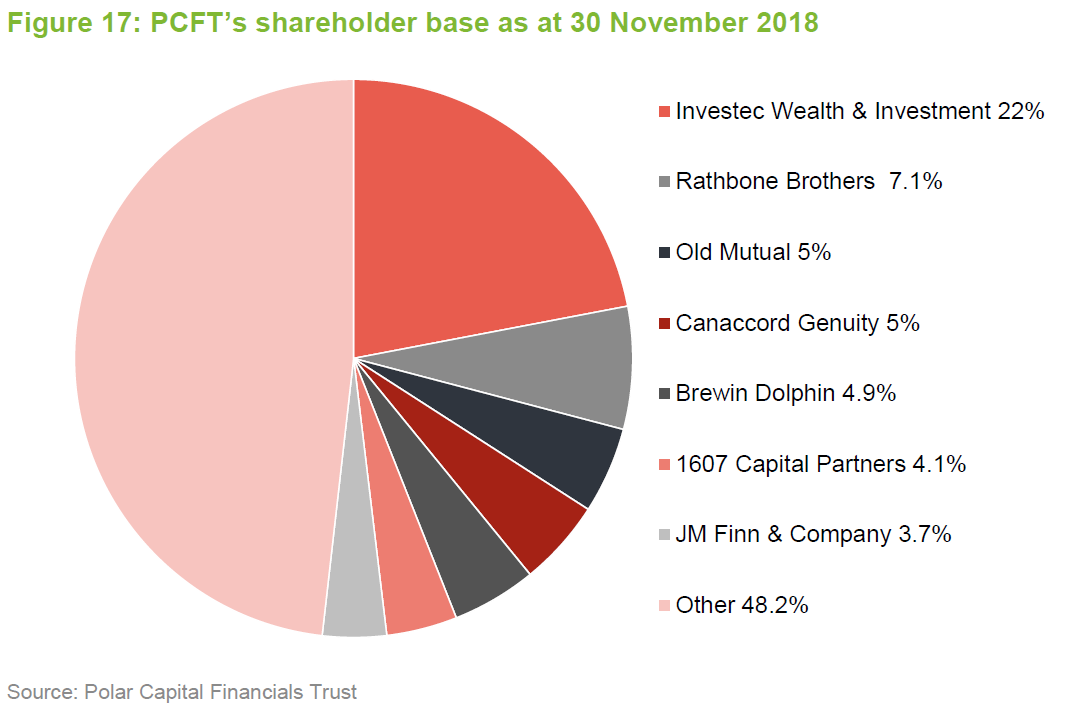

Major shareholders

Management

The seven-strong financials team at Polar Capital LLC (four fund managers and three analysts) was managing approximately $2.3bn at the end of 2018. PCFT is one of five funds for which the team has direct responsibility. At 31 December 2018, each of those funds had outperformed its respective benchmark index since launch. The managers say that the trust sits at the conservative end of what the team does.

Two of the team focus on insurance companies. Nick Brind looks after the fixed-income element of portfolios. John Yakas specialises in emerging markets and Asian stocks. George Barrow covers Europe. There is considerable experience within the team, but they have quite diverse backgrounds.

Nick Brind

Nick joined Polar Capital following the acquisition of HIM Capital in September 2010, and is manager of the Polar Capital Income Opportunities Fund and co-manager of PCFT. He has 25 years’ investment experience across a wide range of asset classes including UK equities, closed-end funds, fixed-income securities, global financials, private equity and derivatives. Prior to joining HIM Capital, Nick worked at New Star Asset Management. While there, he managed the New Star Financial Opportunities Fund, a high-income financials fund investing in the equity and fixed-income securities of European financials companies, which outperformed its benchmark index in all six years that Nick managed it. Previous to that, he worked at Exeter Asset Management and Capel-Cure Myers. At Exeter Asset Management, Nick managed the Exeter Capital Growth Fund from 1997 to 2003, which over this period was in the top decile of the IMA UK All Companies Sector. Nick has a Masters in Finance from London Business School.

John Yakas

John Yakas joined Polar Capital in September 2010 and is the manager of the Polar Capital Asian Opportunities Fund, Polar Capital Financial Opportunities Fund and co-manager of PCFT. John has 30 years’ experience in the financial services industry. Previously, he worked for HSBC as a banker, based in Hong Kong, and was the head of Asian research at Fox-Pitt, Kelton. In 2003 he joined Hiscox Investment Management, which later became HIM Capital. John has won Lipper awards in the Equity Sector Banks and Other Financials Sector in 2010, 2011, 2012 and 2013 for the performance of the Asian Opportunities Fund. He has an MBA from London Business School and studied at the London School of Economics (BSc Econ).

George Barrow

George Barrow joined Polar Capital in September 2010 and works closely with John Yakas on the Polar Capital Financial Opportunities Fund and the Polar Capital Asian Opportunities Fund. With over 11 years’ experience as an analyst, George has built up an in-depth knowledge of the banking sector, expanding his initial European focus to also cover Asia and emerging markets. Prior to joining Polar Capital, from 2008 he was an analyst at HIM Capital, where he completed his IMC. George has a Masters degree in International Studies from SOAS, where he graduated with merit.

Nabeel Siddiqui

Nabeel Siddiqui joined the Polar Capital Financials team as an analyst in August 2013 and works closely with John Yakas and Nick Brind, focusing on the global banking sector. Prior to this, he worked as an operations executive at Polar Capital. Nabeel began his career in August 2008 with Habib Bank, where he worked within a variety of functions. He has a Masters Degree in Money and Banking and has passed all three levels of the CFA.

Jack Deegan

Jack Deegan joined Polar Capital in October 2017 and works closely with Nick Brind on the Income Opportunities Fund. Prior to this, he worked at DBRS Ratings, covering the Swiss market as a lead analyst, as well as UK, Dutch, Japanese and Australian banks. Before DBRS, Jack worked in the Risk Management Division of the Bank of England for four years, assessing financial institutions with a view to determining access to the Bank’s Sterling Monetary Framework (SMF) facilities, and internal counterparty trading limits.

Nick Martin

Nick joined Hiscox plc in 2001. He participated in the management buyout of Hiscox Investment Management in 2007 when the business was renamed HIM Capital Ltd, and moved to Polar following its acquisition. He has developed a broad knowledge of the insurance sector during this time and from working for chartered accountants, Mazars Neville Russell, where he specialised in audit and consultancy work for insurance companies and brokers. He is a qualified chartered accountant and obtained a first-class honours degree in Econometrics and Mathematical Economics at the London School of Economics.

Dominic Evans

Dominic Evans joined Polar Capital in October 2012 and is an investment analyst working with Alec Foster and Nick Martin on the Polar Capital Global Insurance Fund. He has 10 years insurance experience, having previously worked as part of KPMG’s insurance segment, which he joined as a graduate trainee. At KPMG Dominic obtained broad experience working on a range of global insurance companies through roles within transaction services, audit and markets. Prior to KPMG he worked for a year in corporate finance, focusing on natural resource companies. Dominic is a chartered accountant and member of the ICAEW. He graduated with distinction in History with a first-class honours degree from the University of Newcastle upon Tyne.

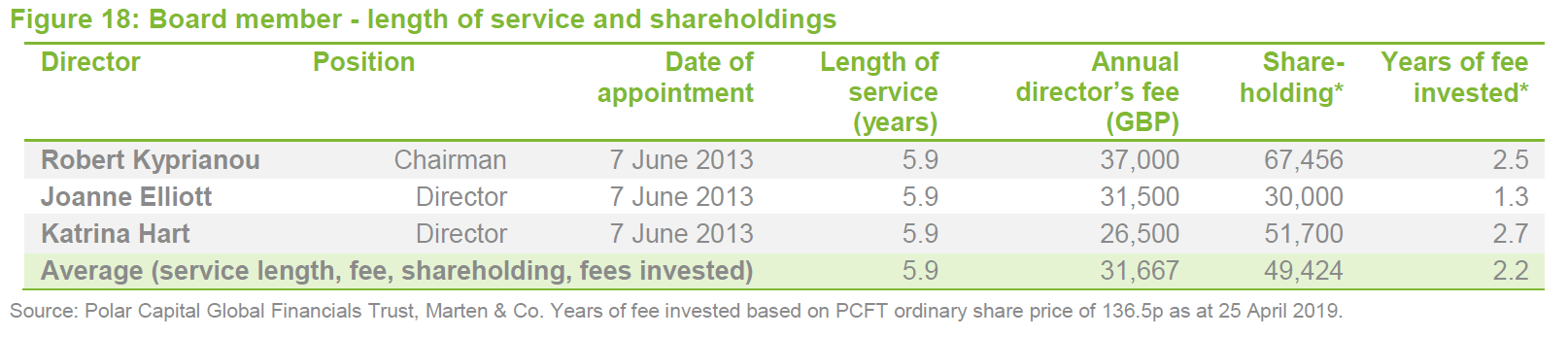

Board

Robert Kyprianou, Joanne Elliott and Katrina Hart were all appointed to PCFT’s board in June 2013, following its incorporation. There have been no changes to the board’s composition since then.

All directors stand for re-election at three-yearly intervals. All three of PCFT’s directors were re-elected by shareholders at the AGM in 2017. The directors meet at least four times a year, and the Audit committee meets at least twice a year.

Robert Kyprianou (non-executive chairman)

Robert was appointed to the board in June 2013 (as were Joanne and Katrina), bringing with him over 30 years of experience in asset management. He was previously CEO of Framlington until his retirement in September 2009. Robert has also served as global head of fixed income, and later deputy CEO and global head of securities at AXA Investment Managers SA; business head and global head of fixed income at ABN AMRO Asset Management Ltd and head of portfolio management at Salomon Brothers Asset Management Ltd. Robert also serves as the chairman of Eurobank Cyprus Ltd and is an independent director at Pimco Europe. He also chairs PCFT’s nomination and remuneration committees.

Joanne Elliott ACA (non-executive director)

Joanne has a wealth of experience working with property-related businesses in particular. She is currently the CFO of the property team at Thames River Capital and is the long-standing finance manager of the TR Property Investment Trust (since 1995). She has also served as the director of property, finance and operations for the Europe region at Henderson Global Investors. Joanne, through her association with Thames River Capital, holds directorships at several private companies and is the chair of PCFT’s audit committee.

Katrina Hart (non-executive director)

Katrina spent most of her career in investment banking, initially in corporate finance roles with ING Barings and Hawkpoint Partners. She then made the move to equity research at HSBC, where she covered financials. More recently, Katrina managed the financials research teams at Bridgewell Group and Canaccord Genuity, where she focused on fund and asset managers. Katrina chairs PCFT’s management engagement committee and holds three additional non-executive directorships at Miton Group, Keystone Investment Trust and AEW UK REIT.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Polar Capital Global Financials Trust.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.