Confidence building

Confidence building

After a brief period of extreme volatility in stock markets related to the coronavirus COVID-19 outbreak, confidence is returning in the technology sector. Shareholders seem to appreciate that the sector is well-placed to weather the disruption caused by measures that are being used to fight the pandemic. Polar Capital Technology Trust (PCT), buoyed by its strong track record, is attracting the attention it deserves. It has seen its discount eliminated and is issuing shares to meet investors’ demand.

The well-resourced management team, led by Ben Rogoff, has identified a number of themes that it believes will continue to drive market-beating returns from the trust. The take-up of some of these is being accelerated by the current situation. With meagre returns on offer from many other investment types, an actively managed and diversified portfolio of technology stocks offers one of the few paths to achieving genuine long-term growth.

Global growth from tech portfolio

PCT aims to maximise long-term capital growth through investing in a diversified portfolio of technology companies around the world, diversified across both regions and sectors within the overall investment objective to reduce investment risk.

Fund profile

PCT aims to maximise long-term capital growth through investing in a diversified portfolio of technology companies around the world, diversified across both regions and sectors. PCT launched in December 1996 as Henderson Technology Trust and, following a change of manager, became Polar Capital Technology Trust in April 2001.

Management arrangements

PCT’s AIFM is Polar Capital LLP and the lead manager assigned to the trust is Ben Rogoff, a partner in Polar Capital LLP. He is supported by a team of eight technology specialists, including another partner, Nick Evans. Polar believe that this is one of the best-resourced teams dedicated to this sector within Europe. In addition to PCT, the team also manages two open-ended funds, Polar Capital Global Technology Fund and the Automation & Artificial Intelligence Fund. More information on the team is available on page 18.

Ben joined the team from Aberdeen in 2003, having started his career in the years running up to the technology boom in 1999/2000. The events surrounding the collapse of the tech bubble have influenced the way that he manages money. One important lesson is that there is no permanence in the technology sector. It is forever engaged in a process of creative disruption. Change in the sector is a non-linear process. Once great companies can disappear and minnows can become giants. This dynamic is part of the appeal for Ben – the sector is never boring.

The trust went through a difficult period of performance in 2006 and this prompted a rethink. Ben became the sole manager of the trust at this point and the trust also adopted a new benchmark (which was finessed in May 2013 to adjust for relevant withholding taxes), the Dow Jones Global Technology Index total return, sterling adjusted. The underlying investment philosophy did not change at this point but, where PCT had been managed with a number of distinct regional portfolios, Ben adopted a truly global approach.

Nick Evans joined the team from Framlington in 2007. He complements Ben in that Nick has a more bottom-up approach to selecting stocks where Ben has a bias to a top-down stance.

Investing in technology

Whilst manufacturing and retail of technological devices has been affected by the pandemic, for the most part, the technology sector is unaffected. In some areas it has actually benefitted as businesses take advantage of technologies that support home-working. Companies such as Zoom have done very well in this environment as a once-niche product becomes mainstream.

In some ways, Zoom’s success helps illustrate the team’s approach to managing money in a sector that can offer fantastic rewards and can also be unforgiving when you get it wrong. Avoiding the riskiest stocks and the savage adverse swings in sentiment that accompany missed profit or revenue expectations can make a big difference to long-term returns.

Technologies go through cycles, like any other product. New entrants tend to displace yesterday’s winners. Sometimes these big companies can reinvent themselves, but usually not. PCT has no exposure to IBM, Cisco and Oracle for this reason.

A central premise of the investment approach is that the best returns can be made as a product or service moves from the early adoption phase to the mass adoption phase. The manager believes that stockbroking analysts find it hard to model the near-exponential growth that businesses can achieve as penetration of a product or service shifts from around 5% to around 30% and this presents an opportunity for active managers. PCT was an investor in Google, Facebook, Alibaba and Salesforce.com at IPO even though they looked expensive. The manager could not claim to know how big these companies would become, but believed that they were disruptive, next-generation platforms and that the growth potential of these firms justified the price that PCT was paying.

In the early stages, investors are attracted by the prospect of fantastic returns, but the initial excitement tends to dissipate as once-promising ideas fall by the wayside, losses mount and, at that stage, take-up of the product or service is minimal. PCT avoids this area, leaving it to the venture capital funds. Many of the companies exploring these early-stage technologies are not quoted on a stock market anyway. The manager also recognises that there are times when it is much harder for companies to attract funding. For that reason, it is important to invest in businesses that do not need capital.

The manager sees the sweet spot for PCT as technologies move from the “blue sky” to the “emerging phase”. The pace at which this is achieved can vary considerably between technologies. As the take up of the product or service gathers momentum, profits and sales can rise very quickly. There may be only one or two companies that end up dominating a technology. However, there is also money to be made from owning the second-line companies that get acquired.

Identifying technologies that are in their emerging phase and then selecting those companies best-placed to benefit from this is key to PCT’s long-term success. So too is getting out of the companies reliant on mature, mainstream technologies. By the time that technologies become mainstream, the buyer’s focus is shifting to the next exciting product and greater emphasis is being placed on the price of the product or service. Sales and profit growth stalls and market valuations of these companies begin to fall. Some of these can look like attractive value propositions, especially in the early stages of decline when they may be generating cash, but in the final phase, products and services can see a dramatic collapse in sales and profitability – the technology market is unforgiving.

As an example, the portfolio had no direct travel-related exposure ahead of the pandemic even though it had held reasonably large positions in Expedia and booking.com in the past. The manager had recognised that the penetration of ecommerce within travel is high and feels that Google has been becoming more competitive in this area. This is a sector approaching maturity and the best money has been made. The portfolio did have some secondary exposure to the sector through the likes of PROS Holdings (a SaaS business with some exposure to airline customers) and Dassault Systèmes (a 3D design software company with some aerospace exposure). However, both were sold in their entirety, alongside many other stocks that the manager perceived to be at risk, early during the sell-off.

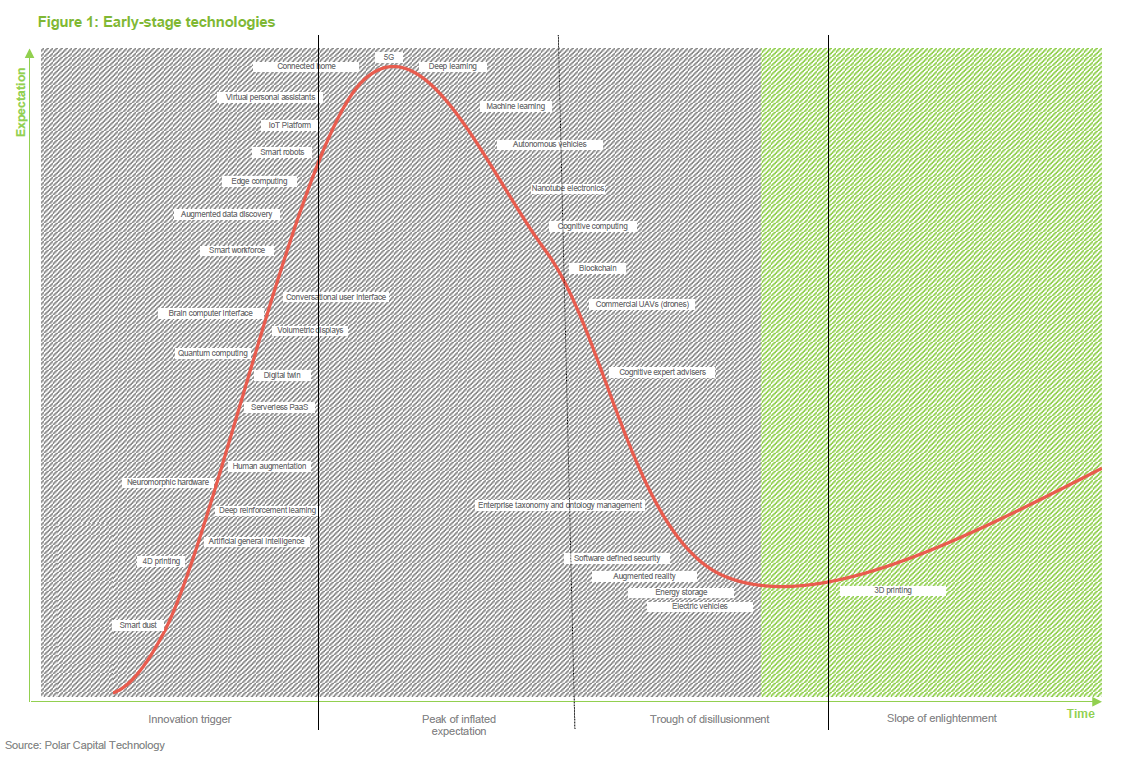

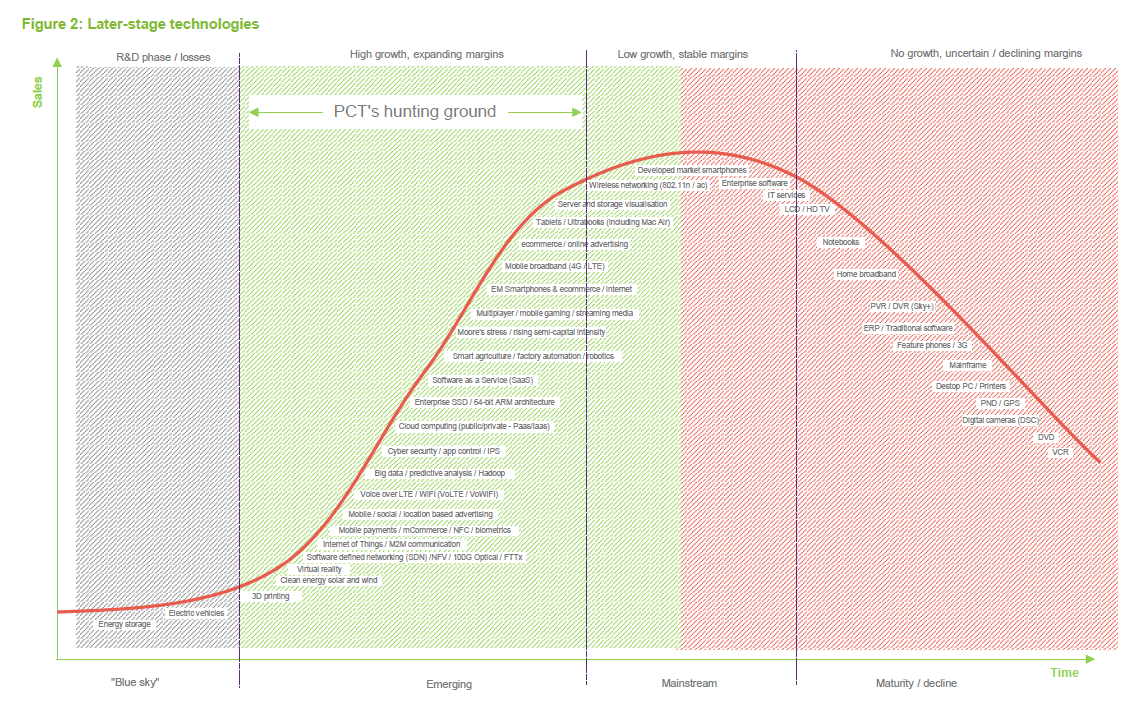

The following charts are reproduced from the presentation that the manager made at last year’s annual general meeting. The positions of the various technologies on the S curve – the line that describes the take up of a product or service – are a rough indication of the stage that the Polar team think these technologies had achieved last summer.

Themes

Once or twice a year, the management team will take stock of the market and determine the big themes that the portfolio should have exposure to.

The manager has identified eight big themes within the portfolio that he is seeking to exploit. These are:

- Ecommerce/digital payments

- Digital marketing/advertising

- Cyber/physical security

- Cloud infrastructure/artificial intelligence

- Software/SaaS – reshaping the world

- Digital content/games software

- Robotics/automation

- Rising semiconductor complexity

The sector today

COVID-19 has put an end to the bull market that had been in place since the financial crisis. The technology sector did well in this environment, drawing parallels with the tech bubble from some quarters. Ben points out, though that the bubble was built on ever-expanding valuations for untested companies. Today the listed technology sector is demonstrating strong growth in revenue and profits.

For more than a decade, central banks and governments have injected money into the financial system and held interest rates at historically low levels. The policy response to the virus has been more of the same.

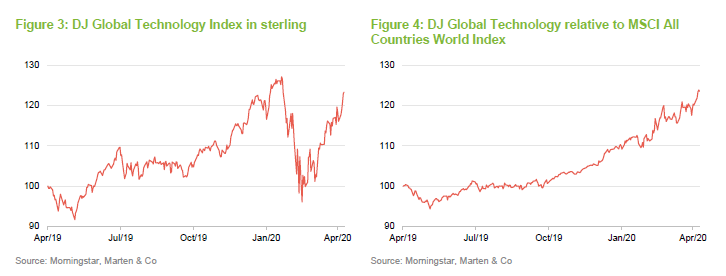

Investors looked warily at what was happening in China and then panic set in towards the end of February. The technology sector was not immune to the rising volatility, but gradually investors recognised that the sector was relatively well placed. Long-term underlying growth drivers remain intact and some companies are actually benefitting from the situation. Confidence returned and the sector recovered, although large caps were favoured over small caps and the sector is still some way short of the highs it was hitting in February 2020.

There is evidence of an uptick in demand for PCs, as many people switch to working from home. Related to this, communications-as-a-service companies seem to be doing well and the manager also expects to see increased demand for cybersecurity products, as home networks are incorporated into corporate networks.

Gaming and subscription TV and media companies are doing well. COVID-19 may accelerate the take-up of cloud storage (accelerating the move away from physical servers). It is also driving additional growth in online shopping and associated deliveries. All of this activity requires additional bandwidth and resilient data networks. This may encourage the adoption of 5G, although there is a risk that device launches are delayed as a result of the disruption. It may be, too, that consumer finances are stretched.

Ben acted quickly to cut exposure to companies that he thought would be hit by the pandemic, including some software companies focused on sectors that have been hit badly and payments companies reliant on retail transactions. He expects that advertising revenues will be hit and reduced PCT’s exposure to Facebook and Google as a result. Some companies have seen a disruption in manufacturing, but these should ease now that China is reopening its factories.

Many technology companies have strong balance sheets and have been using excess cash to buy back shares. Ben thought buybacks might be put on hold as markets fell, and this has proved to be the case.

Investment process

The management team behind PCT is described on page 18. The team carries out many hundreds of meetings a year. Not just with portfolio companies but also their competitors and suppliers. The team uses surveys and speaks to domain experts to cross-reference what customers think of products, where appropriate.

The manager selects from a universe of more than 4,000 stocks and looks to construct a diversified portfolio with about 100 stocks in aggregate. These should represent the best opportunities within the investment themes that the manager has identified, and should come at the right price. The team looks at the value chain and identifies areas where it is possible to generate super normal profits (where companies have an unfair advantage) and recurring revenue.

On average, the stocks that are selected for the portfolio should be capable of generating 30%-50% higher growth than the average stock in the benchmark index and the manager is prepared to pay up for this growth – roughly 20%-30% more than the benchmark, on average.

There is little merit in first screening the investment universe for value, in the manager’s opinion. It is better to think about which companies PCT should have exposure to, and only then about what is the price he is prepared to pay for them. The team is much more likely to screen for improving business fundamentals or stocks it may have missed at the periphery of PCT’s investment universe that may not be perceived as tech stocks today but might be in the future. An important part of this process is to think about the potential downside in a stock – how much will be lost if the investment case is wrong. For many of these stocks, missing an earnings forecast can be devastating to their rating.

PCT may miss out on the odd stock as a result – Zoom, for example – but the manager believes that this is an acceptable price to pay for avoiding the worst of the downside.

Sell discipline

Ben thinks that it is important to run your winners (do not sell just because an investment has done well), but do sell when you realise that you have made a mistake. Fair value is a moveable target and the potential upside and downside from any position needs to be reassessed regularly. The team has a bull, bear and base case for each stock, with a weighted probability to each of these scenarios.

Holdings will be trimmed as they approach the team’s target price. Sometimes Ben will hold onto a small position in a stock that he feels it is important to stay in touch with. PCT’s portfolio has a tail of 20 small positions – some of these are binary opportunities (either they will multiply in value or be almost worthless). In total, these account for about 3% of the portfolio. The ability to have exposure to this type of opportunity is a benefit of PCT’s closed-end structure (an open-ended fund would have to worry about being able to sell such positions in a hurry if investors wanted their money back).

Portfolio construction

PCT is managed very much with an eye to risk. It is designed to deliver 3%+ annual outperformance versus its benchmark after fees on a consistent basis, with typical active share of 40-50%. It rarely makes outsized stock-level bets, preferring to add value by avoiding losers (often mature, or blue-sky companies) and correctly identifying the most important secular themes (and allocating between them where value is perceived to be most compelling). This means that PCT ends up holding 100+ stocks. While this means that other, less risk-aware funds may perform better over shorter periods, this risk-adjusted/diversified approach has allowed PCT to deliver first quartile/first decile performance over almost every medium/longer timeframe.

From time to time, a handful of stocks can dominate the benchmark index. The board allows the manager to take a neutral position in any stock that accounts for more than 10% of the index (up to a maximum of 20% of the portfolio) but PCT cannot have an overweight exposure to these companies.

PCT is emphatically not a closet-tracking fund. If the manager does not like a company, PCT will have no exposure to it, regardless of its weight within the benchmark. This is currently true of IBM, Cisco and Oracle, for example.

Typically, the maximum exposure to a stock will be a 3.0%-3.5% active weighting (i.e. in over and above the benchmark weighting). The portfolio’s active share has ranged from about 30% to just over 50% max.

Investment in emerging markets is permitted but this is capped at 25% of gross assets. The board has also given the following indicative ranges for PCT’s asset allocation:

- North America up to 85%;

- Europe up to 40%;

- Japan and Asia up to 55%;

- Rest of the world up to 10%;

and has set specific upper exposure limits for certain countries where it believes there may be an elevated risk.

The remit allows investment in unquoted companies (subject to prior board approval and capped at 10% of gross assets) but in practice, this has not been used.

Asset allocation

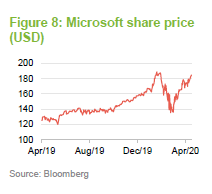

At the end of March 2020, PCT had net cash of 3.7% and no gearing (borrowing). The distribution of the fund both geographically and by sector did not change much over the six months ended 31 March 2020. The allocation to Asia rose while that to the UK fell. The cash weighting fell from 6.3% to 3.7% and the exposure to internet and direct marketing retail rose from 5.3% to 8.8%.

Top 10 holdings

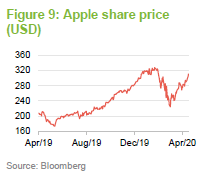

Microsoft (10.2%) – strong growth in Azure cloud computing platform and software subscriptions

Microsoft Corporation (www.microsoft.com), needs little introduction. It is one of the largest software makers in the world and almost all readers will have used one of its software products, be it Microsoft’s Windows operating systems, its Office suite, or its Internet Explorer and Edge web browsers. Many readers will also be aware of its main hardware products; these being its Xbox video game consoles and its Surface range of touchscreen personal computers.

As is illustrated in Figure 8, Microsoft’s share price performed strongly during 2019 as investors have become excited both by strong growth exhibited by its Azure cloud computing business and the company’s success in selling software subscriptions, particularly Office 365 related products. Like other tech giants, the company has boosted its credentials in the face of COVID-19. It has teamed up with UNICEF to launch a global learning platform to help address the growing education crisis as 1.6bn children have been forced from their classrooms as schools close.

Apple (6.9%) – benefitting from iPhone dominance and exposure to the new 5G cycle

Once again, most readers will have used or will certainly be aware of Apple Inc.’s (www.apple.com) hardware products. These include the iPhone, the iPad tablet, the Mac personal computer, the iPod portable media player, the Apple Watch smartwatch, Apple TV, AirPods wireless earbuds and the HomePod smart speaker. It also provides a range of well-known software (for example macOS, Safari and iTunes) and online services (for example the iOS App Store, Mac App Store, Apple Music, Apple TV+, iMessage, and iCloud).

As illustrated in Figure 9, it had an incredible run of performance during 2019, driven both by the take-up of the latest generation iPhone and by customers’ embrace of its AirPods (which exceeded most analysts’ expectations). The advent of 5G offers new opportunities.

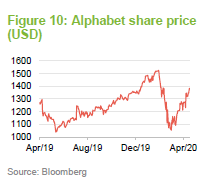

Alphabet (6.8%) – proactive in the face of COVID-19

Alphabet Inc is the parent company of the western world’s favourite search engine, Google (www.google.com). Alphabet was created in October 2015 as the holding company for Google’s diverse business lines. These include Calico (a research and development-driven biotech company), DeepMind (artificial intelligence), GV (life science venture capital), CapitalG (private equity), X (research and development), Google Fiber (fibreoptic connectivity in the US), Makani (energy from kites), Sidewalk Labs (urban innovation), Verily (life sciences research), Waymo (self-driving cars), Wing (drone-based deliveries) and Loon (internet connectivity via balloons).

Google (the largest subsidiary) offers an array of internet-based products that most readers will be familiar with. Particularly pertinent in the current environment are Google Hangouts, Google Docs, Google Sheets, Google Slides (designed to aid work and productivity), Gmail (its email service), Google Calendar and Google Drive (cloud storage), to name just a few. It also offers instant messaging video chat, translation mapping and navigation video sharing note taking and photo services. Google also leads the development of the Android mobile operating system, the Google Chrome web browser, and Chrome OS (an operating system based on the Chrome browser).

Like many technology companies, Google is seeing growth in demand for its services as people adjust their lifestyles and working habits in the face of COVID-19. It has also been proactive in its response to the virus, quickly following the lead of Facebook and Twitter in prominently featuring links to high-quality information from sources such as the Centers for Disease Control and World Health Organization in its search results.

Alibaba (4.3%) – experiencing major growth in cloud computing

Alibaba Group (www.alibaba.com) is a Chinese multinational technology company that provides a range of e-commerce, retail, internet, and technology related services primarily in China. It is an ecommerce giant that is famed for its online marketplaces, which are reportedly the largest in the world. These are Alibaba.com (business to business), Taobao (consumer to consumer), and Tmall (business to consumer). It also provides electronic payment services, shopping search engines and cloud computing services. However, it also owns a wide array of businesses, in numerous sectors, globally.

While still behind the market leaders, Alibaba’s cloud services have been a huge growth area for the company (revenue was up 62% during the fourth quarter of 2019 to US$1.5bn). On 23 April 2020, Alibaba Cloud launched a Global SME Enablement Program to provide cloud technology relief to SME customers around the world. The programme is reportedly worth some US$30m and is designed to provide both new and existing customers with solutions to maintain business continuity in the face of the COVID-19 pandemic. This would seem to mirror successful moves by the likes of Amazon and Google historically in offering free services that allow small and medium-sized enterprises to grow and thrive, while effectively tying them into the cloud provider for the long term.

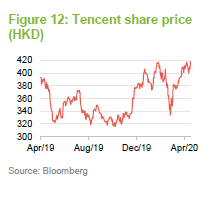

Tencent (3.4%) – Difficulties with Chinese authorities may be behind it

Tencent Holdings (www.tencent.com) specialises in internet-related products and services, entertainment and artificial intelligence (AI). Its services include social networking, music services, ecommerce, mobile games, internet services, online payment systems, smartphones, various web portals and multiplayer online games. Like Alibaba, it also has interests in a wide array of businesses, in numerous sectors, globally.

Tencent has fallen foul of the Chinese authorities in the last couple of years. China is the world’s largest gaming market, and the Chinese authorities put a freeze on approvals for new games, which impacted Tencent during 2018 and into early 2019. The tech giant’s shares also came under pressure during October 2019 after it decided to live-stream NBA games, thereby putting it at odds with China’s state broadcaster (Tencent paid US$1.5bn in 2018 for five years of exclusive streaming rights of NBA games). Tencent also angered the pro-democracy movement in Hong Kong when Blizzard, partly owned by the company, banned a gamer for endorsing the movement.

However, since then the company has benefitted from a strong set of results and increased demand for some of its services in the face of COVID-19. It has also burnished its public image by setting up two fund to help fight the pandemic: a US$211m fund to support healthcare workers in China, and US$100m global fund to provide protective equipment and other products for hospitals and healthcare services.

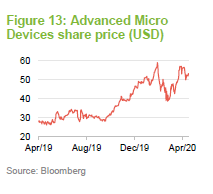

Advanced Micro Devices (2.4%) – economically sensitive but exposed to structural growth in chips for smart devices

Advanced Micro Devices (www.amd.com) is a California-based multinational semiconductor company that develops computer processors and related technologies for both consumer and business applications. It has operations in 23 countries and employs some 10,000 people globally. Its main products include microprocessors, motherboard chipsets, embedded processors and graphics processors for servers, workstations, personal computers and embedded system applications.

As illustrated in Figure 13, the stock had an incredible run of performance following the publication of its third-quarter results in October 2019, aided by a strong rally in semiconductor stocks more generally (AMD’s share price moved from around US$28 per share to around US$ 57 per share during this time).

Buyers built up huge inventories during 2018 in anticipation of the US imposing tariffs on China and potential memory price rises. However, with trade tensions easing and inventories running down, demand was expected to increase again as the economic outlook brightened (the semiconductor space is quite economically sensitive) and investors focused on the long-term structural demand for chips (most consumer products – large and small – are becoming increasingly smart with more and more chips inside). Whilst demand for PCs has been falling and smartphones are potentially lower growth over the longer term, there is strong growth potential for cloud computing, AI and Autos, for example. 5G will also give a boost over the next couple of years.

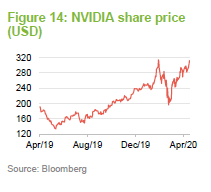

NVIDIA (2.3%) – benefitted from semiconductor rally

Nvidia Corporation (www.nvidia.com) is a California-based technology company that designs graphics processing units (GPU) for the gaming and professional markets, as well as system on a chip units (SoCs) for the mobile computing and automotive sectors. NVIDIA’s business is focused around four key segments: gaming, professional visualisation, data centres, and auto. It also has interests in AI and provides parallel processing capabilities that used in supercomputing sites globally. In the GPU space, NVIDIA’s main product is its GeForce range. This competes directly with Advanced Micro Devices Radeon range of GPUs. As illustrated in Figure 14, like AMD, NVIDIA had a very strong run of performance during the second half of 2019 as semiconductor stocks rallied strongly.

Performance

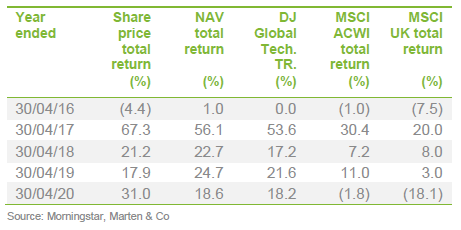

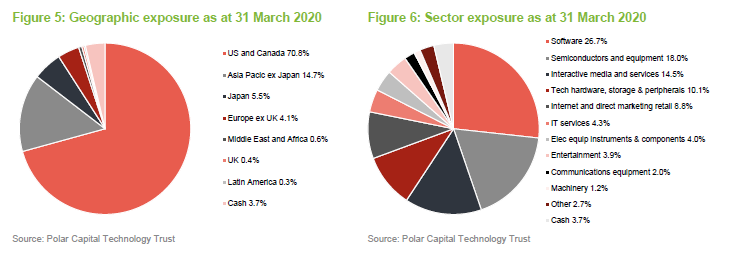

In an era of low inflation, low interest rates and low economic growth that has dominated the global economy since the 2008 financial crisis, the technology sector stands out. Figure 16 shows the superior returns that the benchmark index has delivered over the past five years relative to the MSCI All Countries World Index. UK investors that stuck to their home market barely made a profit over the five years ended 31 March 2020. By contrast, an investor in PCT saw returns of 170%, well ahead of its benchmark index.

Over 2020, year to date, PCT and the benchmark index have held up well (PCT is one of only a handful of investment companies that made a positive return over Q1 2020.

Peer group

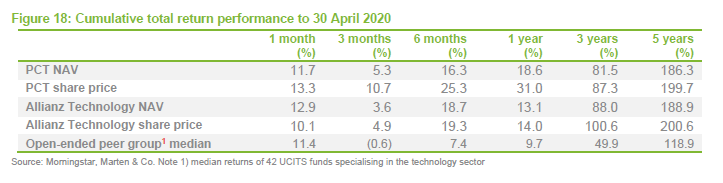

PCT’s competition in the AIC’s Technology and media sector is really restricted to Allianz Technology Trust. Augmentum Fintech and Sure Ventures are focused on early-stage companies and are much smaller companies. PCT is the larger trust and, at present, trades on a slightly lower rating than Allianz Technology. Neither trust pays a dividend. PCT has a slightly higher historic ongoing charges ratio, but changes to the investment management agreement made with effect from 1 May 2019 (see page 16) should have brought this down.

In Figure 18 we have also compared the two listed funds with a peer group of 42 UCITS funds specialising in the technology sector. Over the five years ended 30 April 2020, an investment in PCT’s shares would have beaten all but one of these.

Dividend

PCT is not designed to produce a dividend. Over the years, its running expenses have exceeded its revenue. The board would declare a dividend if this was needed to maintain the company’s status as an investment trust. However, PCT would first need to eliminate its brought forward revenue reserve deficit (£95.9m at 31 October 2019).

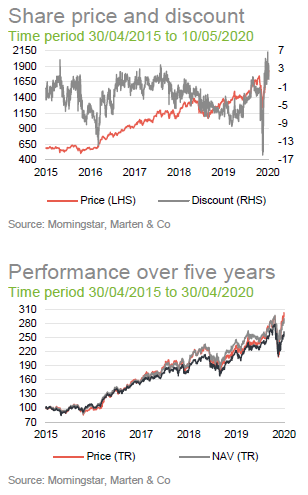

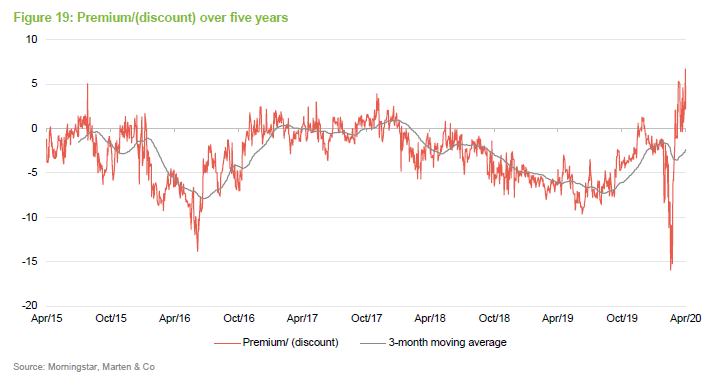

Premium/(discount)

Over the year ended 30 April 2020, PCT ranged between trading at a discount of 15.9% to a premium of 6.7%. The average discount over this 12-month period was 4.3%.

The discount that opened up in 2018/19 was perverse, given the trust’s outperformance of broad stock market indices. Investors recognised this at the end of 2019. A spike out on the discount as the COVID-19 panic set in was swiftly eliminated. We see no obvious reason why the trust should move back to trading at a discount.

PCT’s board takes powers at each annual general meeting to issue and buyback stock (issuance of up to 10% of issued share capital and repurchases up to 14.99% of issued share capital both at the date of the meeting). The board recognises that investors dislike discount volatility, but from a pragmatic point of view it believes that it is unrealistic to expect that a specialist trust such as PCT will always be in favour with investors. The board has not set a discount target but will use the company’s buyback powers when it thinks it is appropriate. Shares repurchased may be held in treasury but currently there are no shares in treasury.

Similarly, the board seeks to moderate any premium with the issuance of shares. Shares are only issued at a premium to asset value. 1,151,000 shares have been issued in recent weeks following the strengthening of PCT’s share price.

Fees and costs

The fee payable to the manager is tiered. PCT pays 1.0% on the first £800m of net assets, 0.85% on the next £800m, 0.80% on the next £400m and 0.7% on amounts above £2bn. (Prior to 1 May 2019, the fee was 1.0% on the first £800m of net assets, 0.85% on the next £900m, 0.80% on amounts above £2bn.)

A performance fee of 10% of the fund’s outperformance of the benchmark is payable. The performance fee is subject to a high watermark and a cap of 1% of net assets. No fee is payable if the NAV fails to exceed the high watermark, but outperformance in such years is carried forward to subsequent years. (Prior to 1 May 2019, the performance fee was 15% of the fund’s outperformance of the benchmark.)

The ongoing charges ratio for the year ended 30 April 2019 was 0.95%, down from 0.99% for the previous year. Ongoing charges ratios exclude performance fees. Were these included, the equivalent figures would have been 1.33% and 1.76%.

In addition to the old scale of management fees, the ongoing charges ratio for the year ended 30 April 2019 included £238,000 of research costs which, with effect from 1 January 2019 are all borne by the manager. It also included £43,000 of PR, website and marketing expenses. The first £100,000 of marketing expenses is now borne by the manager. Details of directors’ fees are given on page 20. £137,000 was payable in depositary fees and £159,000 in custody and other bank charges: these services are provided by HSBC Bank Plc.

Capital structure

PCT has 134,976,000 ordinary shares in issue and no other classes of share capital.

PCT’s financial year end is 30 April and AGMs are usually held in September. PCT has an unlimited life, but at this year’s AGM shareholders will be asked whether they want the fund to continue. Assuming that this is passed (and we see no reason why it would not be) the same question will be put to shareholders in 2025 and every five years thereafter.

The use of gearing and derivative instruments is permitted and overseen by the board.

Derivative instruments such as financial futures, options, contracts-for-difference and currency hedges would be used for the purpose of efficient portfolio management. Any leverage resulting from the use of such derivatives will be subject to the restrictions on borrowings.

PCT has no long-term borrowings and, at present, no short-term borrowings either.

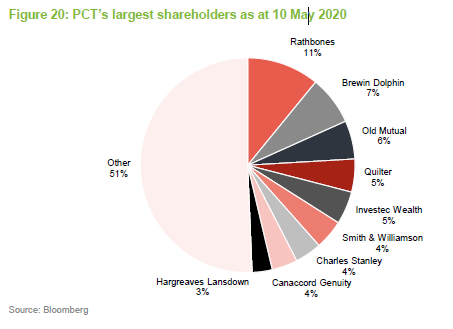

Major shareholders

Management team

Ben Rogoff

Ben is the lead manager of Polar Capital Technology Trust and is a fund manager of the Polar Capital Global Technology Fund and Polar Capital Automation and Artificial Intelligence Fund.

Ben has been a technology specialist for 23 years. Prior to joining Polar Capital, he began his career in fund management at CMI, as a global technology analyst. He moved to Aberdeen Fund Managers in 1998, where he spent four years as a senior technology manager. Ben graduated from St Catherine’s College, Oxford in 1995.

Nick Evans

Nick Evans joined Polar Capital in 2007. He has 21 years’ experience as a technology specialist and has been lead manager of the Polar Capital Global Technology Fund since January 2008. He is also a fund manager on the Polar Capital Technology Trust and Polar Capital Automation and Artificial Intelligence Fund.

Prior to joining Polar, Nick was head of technology at AXA Framlington and lead manager of the AXA Framlington Global Technology Fund and the AXA World Fund (AWF) – Global Technology from 2001 to 2007 (both rated five stars by S&P). He also spent three years as a Pan-European investment manager and technology analyst at Hill Samuel Asset Management. Nick has a degree in Economics and Business Economics from Hull University, has completed all levels of the ASIP, and is a member of the CFA Institute.

Fatima Iu

Fatima joined Polar Capital in 2006. She has 14 years’ experience and is a fund manager on the Polar Capital Technology Fund, Polar Capital Technology Trust and Polar Capital Automation and Artificial Intelligence Fund. Fatima is responsible for the coverage of European Technology, Global Security, Networking, Clean Energy and Medical Technology.

Prior to joining Polar, Fatima spent 18 months working at Citigroup Asset Management with a focus on consumer products and pharmaceuticals. She holds an MSc in Chemistry with Medicinal Chemistry from Imperial College of Science & Technology in London. Fatima is also a CFA Charterholder.

Xuesong Zhao

Xuesong joined Polar Capital in 2012. He has 12 years’ investment experience and is a lead manager of the Polar Capital Automation and Artificial Intelligence Fund. He is a fund manager on the Polar Capital Technology Trust and Polar Capital Global Technology Fund.

Prior to joining Polar Capital, Xuesong spent four years working as an investment analyst within the emerging markets & Asia team at Aviva Investors, where he was responsible for the technology, media and telecom sectors. Prior to that, he worked as a quantitative analyst and risk manager for the emerging market debt team at Pictet Asset Management. Xuesong holds an MSc in Finance from Imperial College of Science & Technology, a BA in Economics from Peking University and is also a CFA Charterholder.

Alastair Unwin

Alastair joined Polar Capital in June 2019 as a fund manager and senior analyst. Prior to joining Polar Capital, Alastair co-managed the Arbrook American Equities Fund. Between 2014 and 2018 he launched and then managed the Neptune Global Technology Fund, and managed the Neptune US Opportunities Fund. Prior to Neptune, Alastair was a technology analyst at Herald Investment Management. He has a BA (1st Class Hons) in history from Trinity College, Cambridge and is a CFA Charterholder.

Chris Wittstock

Chris joined Polar Capital in 2017.as a senior technology analyst based in the US. Prior to this, he led the international research sales effort at Pacific Crest, a technology investment bank that was ultimately acquired by KeyBanc Capital in 2014.

Prior to joining Pacific Crest in 2004, Chris led the international sales effort at Schwab SoundView, the successor company to Soundview Technology Group, where he was from 1996.

Chris spent significant time in Europe as a derivative products specialist in the late ‘80s and ‘90s, lastly with Morgan Stanley International. He is a graduate of the University of Toronto, Faculty of Engineering (Industrial).

Paul Johnson

Paul joined Polar Capital in 2012. Prior to this, he helped manage a private investment fund between 2010 and 2012.

Paul holds a BA in History and Politics and a Masters in History from Keele University. He has successfully passed all three levels of the CFA programme.

Bradley Reynolds

Brad joined Polar Capital in 2011 as an analyst and trader working within the European Market Neutral team with a focus on media and internet. In 2014, he joined the Technology team as an investment analyst.

Prior to joining Polar, Brad worked at Ratio Asset Management as an analyst and trader, and from 2007 to 2011 he worked at F&C as a hedge fund analyst. Brad started his career in 2001 at Gartmore Investment Management working within the hedge fund team. He graduated from the University of Hertfordshire with a degree in Business Studies and has passed the Level I examination of the CFA programme.

Nick Williams

Nick joined Polar Capital in June 2019 as an analyst on the Polar Capital Technology team. Prior to joining Polar Capital, Nick worked at Neptune Investment Management as the assistant fund manager on its US Opportunities growth fund. Prior to that he worked in academia at the University of Oxford.

Board

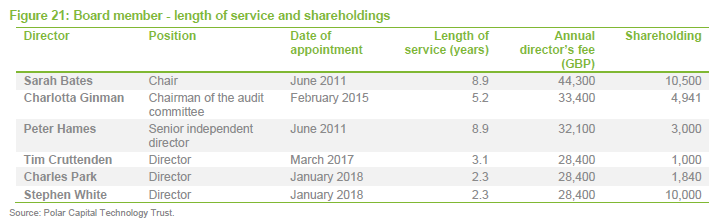

PCT’s board is comprised of six non-executive directors, all of whom are independent of the manager and who do not sit together on other boards. As part of its regular programme of refreshing the board, PCT has announced that Sarah Bates will retire as chair following the AGM in 2022 and Peter Hames will retire at the AGM in 2020. Each of the directors stands for re-election at each AGM.

The directors’ fees were increased by between 2.9% and 3% for the accounting year that commenced on 1 May 2019. At the last AGM, shareholders approved an increase in the maximum aggregate levels of fees in any year to £250,000.

Sarah Bates

Sarah Bates is a past chair of the Association of Investment Companies and has been involved in the UK savings and investment industry in different roles for over 30 years.

Sarah is chair of Merian Global Investors Limited (formerly Old Mutual Global Investors) and is a non-executive director of Worldwide Healthcare Trust Plc. She is also chair of the Diversity Project Charity, a member of the investment committees of the BBC Pension Scheme and of the University Superannuation Scheme. Previously, Sarah was chair of St James’ Place Plc, JPMorgan American Investment Trust Plc, Witan Pacific Investment Trust Plc and was also chair of the audit committees of New India Investment Trust Plc and of U and I Group Plc. Sarah is a Fellow of CFA UK.

Charlotta Ginman

Charlotta Ginman qualified as a Chartered Accountant at Ernst & Young before spending a career in investment banking and commercial organisations, principally in technology-related businesses. She held senior roles with UBS, Deutsche Bank, JP Morgan and the Nokia Corporation.

Charlotta is a non-executive director and chairs the audit committees of Pacific Assets Trust Plc, Motif Bio Plc and Keywords Studios Plc. She is also a non-executive director of Consort Medical Plc and Unicorn AIM VCT Plc.

Peter Hames

Peter Hames spent 18 years of his investment career in Singapore, where in 1992 he co-founded Aberdeen Asset Management’s Asian operation and as director of Asian Equities he oversaw regional fund management teams responsible for running a number of top-rated and award-winning funds.

Peter is a director of MMIP Investment Management Limited. He is also an independent member of the Operating Committee of Genesis Asset Managers LLP and is a director of the Genesis Emerging Markets Investment Company.

Tim Cruttenden

Tim is currently chief executive officer of VenCap International Plc, having been with that company in various positions since 1994. VenCap invests in venture capital funds in the US, Asia and Europe, with a primary focus on early-stage technology companies.

Tim is a non-executive director of Merian Investment Company Limited.

Charles Park

Charles Park has over 25 years of specialist investment experience and is a co-founder of Findlay Park Partners, an investment firm specialising in quoted American equity investments. Prior to this, he was a US fund manager at Hill Samuel Asset Management.

Charles is a non-executive director of North American Income Trust Plc and is a member of Salters’ Management Company Ltd.

Stephen White

Stephen White qualified as a Chartered Accountant at PwC before starting a career in investment management. He has more than 35 years’ investment experience, most notably as head of European Equities at Foreign & Colonial Investment Management and currently as head of European and US Equities at British Steel Pension Fund.

Stephen is a non-executive director and chairman of the audit committees of Blackrock Frontiers Investment Trust Plc and Aberdeen New India Investment Trust Plc and a non-executive director of JPMorgan European Smaller Companies Trust Plc.

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Polar Capital Technology Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.