Building on a great 2019

Building on a great 2019

The second half of 2019 proved profitable for investors in Shires Income (SHRS) as the trust extended its outperformance of both the UK market and the average of its peer group. Investors also benefitted from the elimination of the discount. The trust continues to expand, and this should both help widen its audience, improve liquidity, and reduce its average running costs.

The manager remains focused on identifying good quality and attractively valued stocks rather than gaming macroeconomic shifts but the prospect of a more stable political environment in the UK seems to be helping sentiment.

High level of income with potential for growth

SHRS aims to provide its shareholders with a high level of income, together with the potential for growth of both income and capital from a portfolio substantially invested in large cap UK equities. The portfolio may be further diversified with exposure to smaller UK companies and overseas equities. SHRS augments its income with a portfolio of irredeemable preference shares and convertibles (and, when the manager believes appropriate, fixed income securities), financed, in part by lower cost gearing.

Fund profile

SHRS aims to provide its shareholders with a high level of income, together with the potential for growth of both income and capital from a diversified portfolio substantially invested in UK equities but also in preference shares, convertibles and other fixed income securities. The company is benchmarked against the FTSE All-Share Index. We have substituted this with the MSCI UK Index for the purposes of this report.

SHRS generates income primarily from its investments in ordinary shares, convertibles and a geared portfolio of preference shares. It may supplement this by writing call and put options on shares owned by the trust or shares the manager would like to buy.

SHRS’s preference share portfolio is funded, in part, by lower cost debt (effectively, the equity portfolio is ungeared). The income that this arrangement contributes to SHRS’s returns allows the manager to hold some lower-yielding equities that offer better prospects for both dividend and capital growth. The pool of income available for distribution is augmented further by writing calls and options. In the past, when interest rates were higher, fixed interest investments and interest on cash deposits would also have made a meaningful contribution to SHRS’s revenue account. This may be the case again if interest rates rise.

SHRS’s manager is Aberdeen Standard Fund Managers Limited which has delegated the day-to-day management of the company to Aberdeen Asset Managers Limited (“Aberdeen” or “the manager”). Both companies are wholly owned subsidiaries of Standard Life Aberdeen Plc. The manager emphasises a team approach to managing money. The lead manager for SHRS is Iain Pyle, who is also lead portfolio manager for the Standard Life Investments UK Equity High Income Fund and the Bothwell UK Equity Income Fund.

Iain is an investment director on the UK equities team, having joined Standard Life Investments in 2015. Previously, he was an analyst on the top-ranked oil and gas research team at Sanford Bernstein. Iain graduated with a MEng degree in Chemical Engineering from Imperial College and an MSc (Hons) in Operational Research from Warwick Business School. He is a chartered accountant and a CFA charterholder.

The company gains exposure to smaller companies through an investment in Aberdeen Smaller Companies Income Trust Plc (ASCIT). The two companies have no directors in common and the manager does not charge a fee on this portion of the portfolio.

Election outcome small positive

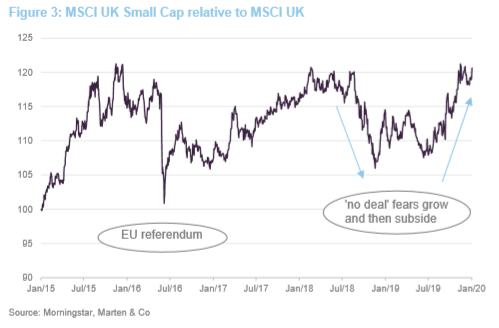

The UK market has made headway over the past five years, but relative to global equity markets, it has lagged by a significant margin. The biggest influence has, of course, been Brexit and fears of ‘no deal’, in particular. The election result gave a small boost to UK equities and particularly small cap stocks, which are more domestically exposed, but these had been rallying beforehand – on hopes of the UK securing an exit deal – and post-election moves have been relatively modest. The arbitrary imposition of a 31 December 2020 deadline on a UK/EU trade deal has introduced a new ‘cliff edge’ and may cause further jitters as 2020 progresses.

UK economic growth has been muted and talk is growing of another UK interest rate cut. On a wider context, the trade dispute between the US and China continues to weigh on global demand.

Iain did not try to bias SHRS’s portfolio in favour of a particular election outcome and remained focused on the fundamentals of the companies in the portfolio rather than attempting to game macroeconomic shifts – in accordance with the investment process and philosophy outlined below.

Investment process

Iain is a member of Aberdeen Standard Investments’s (ASI – the brand that Standard Life Aberdeen Plc uses for its asset management activities) 16-strong UK equity team, 11 of whom are based in Edinburgh and five in London. It is complemented by the small cap team, headed up by Harry Nimmo, and can draw on the considerable resources of the wider global research team.

Each member of the team has been assigned research responsibilities on a sector-bysector basis. Investment ideas are put forward by analysts and peer-reviewed, with the aim of building consensus. A list of 20 high-conviction ideas is generated. The UK team meets daily and analysts’ recommendations are presented at UK team sector reviews. Individual portfolio managers are responsible for deciding what goes into their portfolios. They may hold stocks that the analyst has recommended for sale, but have to write and circulate a ‘dissent note’, putting the case for why the stock should remain in the portfolio.

With the aim of building a portfolio that can deliver a high level of income and the prospect of capital growth, the manager incorporates high-yielding preference shares, high-yielding equities and growth equities into the mix. Diversified exposure to smaller companies is achieved through a holding in ASCIT, which is managed by Harry Nimmo’s team, centred on the Edinburgh office.

The manager believes that SHRS’s objective could be achieved solely through investment in high-yielding equities. However, investing only in the highest-yielding equities would compromise the emphasis on quality that is a key criterion in the selection of potential investments.

SHRS’s preference share portfolio is funded, in part, by lower-cost debt. The income that this arrangement contributes to SHRS’s returns allows the manager to hold some lower-yielding equities that offer better prospects for both dividend and capital growth. The pool of income available for distribution is augmented further by writing calls and options. In the past, when interest rates were higher, fixed interest investments and interest on cash deposits would also have made a meaningful contribution to SHRS’s revenue account.

The upshot is that SHRS’s sources of income are much more diverse than would be the case for many equity income funds, especially given that a handful of stocks account for a significant proportion of the income available in the UK equity market.

Equity investment

When selecting equities for inclusion within the portfolio, the manager adopts a buy and hold strategy. It looks for good quality companies that are trading cheaply, defined in terms of the fundamentals that in their opinion drive share prices over the long term. Particular emphasis is placed on meeting the management of these companies, at least twice a year. The long-term approach helps limit portfolio turnover, although the manager does take advantage of gyrations in markets to top-slice and add to existing positions, where appropriate.

Portfolio construction is driven by stock selection and benchmark weights are not taken into account when determining position sizes. Care is taken to ensure that the portfolio is adequately diversified with respect to a range of metrics. At the end of December 2019, excluding ASCIT, the largest position in the equity portfolio was 4.0%.

Investment restrictions

The board has set some absolute limits on maximum holdings and exposures (these apply at the time of the acquisition of the investment):

• a maximum 10% of total assets invested in the equity securities of overseas companies; • a maximum 7.5% of total assets invested in the securities of one company (excluding ASCIT);

• a maximum 5% of quoted investee company’s ordinary shares (excluding ASCIT);

• a maximum of 10% of total assets invested directly in AIM holdings;

• a maximum of 7.5% of total assets may be invested in the preference shares of any one company; and

• the company cannot hold more than 10% of any investee company’s preference shares.

In addition, with respect to the trust’s investments in options:

• call options written must be covered by stock;

• put options written to be covered by net current assets/borrowing facilities;

• call options not to be written on more than 100% of a holding of stock;

• call options not to be written on more than 30% of the equity portfolio; and

• put options not to be written on more than 30% of the equity portfolio.

The preference share portfolio

SHRS invests in a number of irredeemable preference shares and, at present, one convertible stock. These carry fairly high, fixed coupons and trade at a premium to par.

The preference shares were issued in the early 1990s and it appears that for some time investors thought these were truly irredeemable.

However, in March 2018, Aviva announced that it planned to redeem its preference shares at par. This triggered sharp falls in the prices of preference shares and impacted on SHRS’s NAV. Investors cried foul and Aviva withdrew its plans, saying that it would revisit the decision in 2026 (when ESMA rule changes about the makeup of insurers’ regulatory capital come into effect). Aviva said it would then take into account the fair market value of the preference shares in setting the redemption price, rather than the par value. The manager believes that the market reaction to Aviva’s actions makes any future attempt to redeem preference shares at par less likely.

Option writing

The decision whether to write call or put options is entirely at the discretion of the manager. The manager may write calls on stocks that it wants to sell and puts on stocks that it wants to buy, but only where stock volatility makes that an attractive prospect in terms of the premium available. The manager does not write uncovered calls. Typically, options are short-dated (one-to-three months) and 5–10% out of the money.

Asset allocation

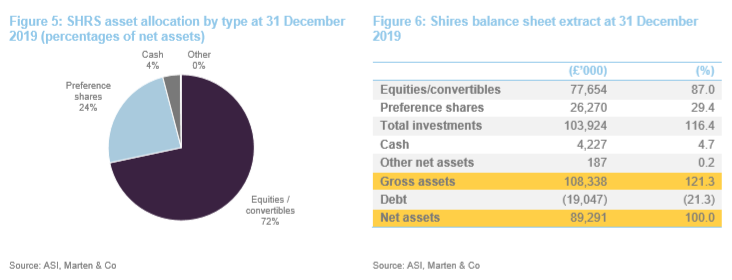

SHRS’s preference share portfolio is financed by a combination of debt and equity. The income this generates allows the manager to invest in a number of low to non-incomepaying growth stocks, without compromising the trust’s attractive yield. The trust’s asset allocation split is shown in Figures 5 and 6 below. The value of the preference share portfolio exceeds that of the debt by some margin and therefore the equity portfolio is ungeared.

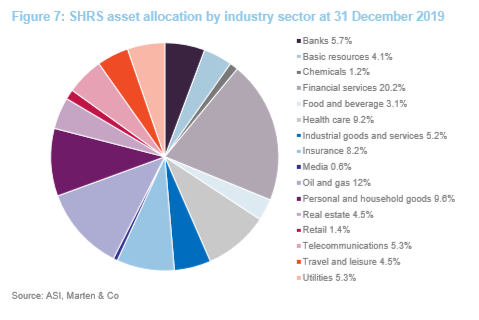

SHRS had 55 investments at the end of December 2019.

Top 10 holdings

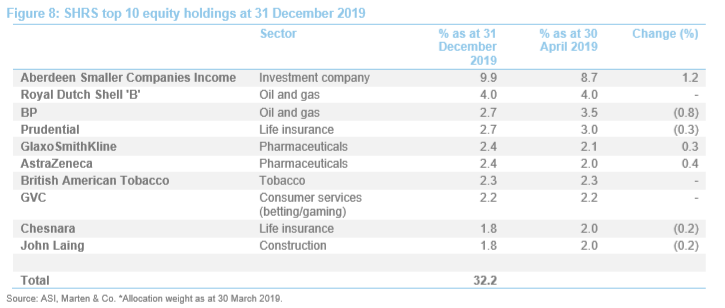

The company’s 10 largest equity holdings are shown in Figure 8.

Reflecting the manager’s long-term buy and hold strategy, there has been very little change to the composition of SHRS’s list of top 10 holdings since 30 April 2019 (the data we used in our last publication). Both GVC and GlaxoSmithKline were portfolio constituents at that date, although outside the top 10. St James’s Place and HSBC have dropped out of this list, but are still held within the portfolio.

Relatively strong performance from the equity portfolio has slightly reduced the percentage of the portfolio exposed to preference shares, but the composition of this part of the portfolio remains unchanged from when we last published.

With the exception of the Balfour Beatty convertible, none of the securities listed in Figure 10 has a fixed redemption date.

Portfolio activity

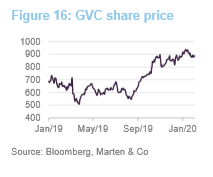

A few new holdings have made it into the portfolio over the past year. These include Cineworld, SSE, Axa, Telenor and Fortum (these are discussed in more detail below). The manager says that the companies yield in the 5%–7% range and were acquired on P/E ratios of 10x-12x. The manager also added to the position in GVC.

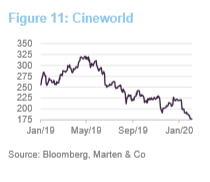

Cineworld

Cineworld (www.cineworldplc.com) is the world’s second largest cinema business by number of screens, with operations in the UK, Ireland, eastern Europe, Israel, US and now potentially Canada. Iain says that this is a more highly-leveraged stock than he would normally consider for the portfolio. The investment case is also sensitive to the success of Cineworld’s US expansion plans. However, Iain is attracted by its strong cashflow, high yield and the prospect of a capital uplift if its North American expansion goes to plan. In the short term, like-for-like revenue contracted over the year to the end of November 2019, which the company is attributing to the timing of major film releases. The acquisitions of Regal in the US and the planned acquisition of Cineplex in Canada are expected to be earnings-enhancing.

SSE

Iain was attracted to SSE (www.sse.com/investors/) as he felt that it, in common with other UK utilities, was trading at a discount to its intrinsic value. This could be attributed partly to the risk that Labour would win the election and implement its policy of nationalisation. The timing of the purchase meant that the SHRS revenue account benefitted from an additional dividend. The greater attraction for Iain, though, was the way in which SSE has been reshaping its business – away from sales of power to consumers and towards renewable power generation. The retail operations were lowmargin and attracted a low valuation multiple. They were sold to Ovo Energy in September 2019 for £500m. This freed up additional capital which SSE is redeploying towards offshore wind, in particular. The visibility of earnings from this business allows SSE to add more leverage and should attract a higher valuation multiple.

Axa

Axa (www.axa.com/en/investor) is an insurance business headquartered in France but with operations globally. It acquired a US P&C insurer, XL Group for $15bn in 2018 and the market did not react favourably to the move. This allowed SHRS to pick up its stake at an attractive valuation (around 8.5x earnings). Iain says that the US business is improving and the insurance cycle is turning in their favour (pricing is firming). In March 2019, the company freed up $1.5bn by reducing its stake in its US life insurance subsidiary. While the shares have rallied since SHRS invested, Iain believes that the stock is still cheap. With sales improving and increased balance sheet strength, this is a self-help story. The high yield and the defensive nature of the business add to the attraction.

Telenor

Norwegian telecoms business Telenor (www.telenor.com) has a strong position in its home markets and offers exposure to growth from its Eastern European and Asian operations. This was a stock that was recommended to Iain by the manager’s European telecommunications analyst. Iain feels that it makes a good alternative to an investment in the UK telecoms companies. The prospect of long-term earnings and dividend growth, a strong balance sheet and good cash generation help underpin the story. In the short term, revenue and earnings growth have been held back by its Pakistani operations, which in turn have been impacted by the reintroduction of a telecoms tax.

Fortum

Fortum (www.fortum.com/about-us) is a Finnish utility company with plants in the Nordic region, Poland, Russia and India deriving power from hydroelectric, nuclear and a small amount of coal. The company has delivered decent dividend growth and was trading on a 6% yield at the time SHRS invested. Iain says that this is one of only a few utilities that offer leveraged exposure to carbon pricing. He expects that carbon prices will move higher next year as the EU enforces its permits regime. Fortum is a clear beneficiary of this.

GVC

We have discussed the multinational sports betting and gaming company, GVC (www.gvc-plc.com) in our previous notes. Iain likes the company’s cash flow and dividend yield. Many investors are sceptical of gaming companies in general and GVC’s ability to make a success of its expansion into the US, in particular. Iain is willing to back the management team, however. GVC has forged a partnership with MGM, which should help as it tries to penetrate the US online gaming market. This is a big untapped market, as many US states have only recently legalised online gaming and others are yet to do so. GVC is extracting cost savings, following its purchase of Ladbrokes, and these will help offset the shrinkage of its UK business.

Sales

The manager sold positions in Nordea, Weir, Inmarsat and Saga. Nordea is a Scandinavian bank which, like a few other direct competitors, was caught out by money laundering allegations. The shares dipped but Iain decided to exit the position when the price recovered a little.

Weir, the engineering company best-known for its pumps business, has been affected by slower sales in its mining-related operations (linked to the global trade dispute) and within its US pressure pumps business, as a weaker oil price impacts on demand from US oil and gas companies. After a strong run, the yield had fallen below market levels.

Inmarsat was sold to a bid, netting a decent profit for SHRS. Another disposal was of Saga. This investment did not match Iain’s expectations. The synergies between the two arms of the business were not as strong as anticipated, as price comparison sites undercut its insurance operations.

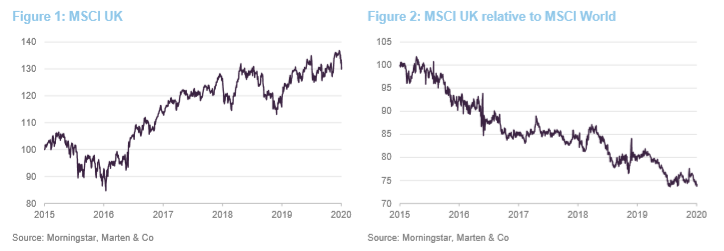

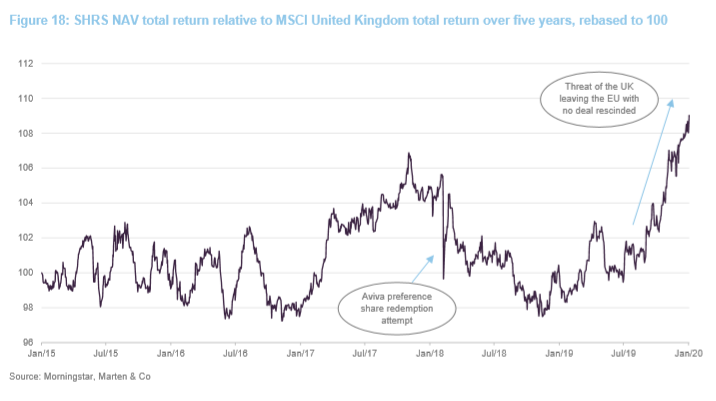

Performance

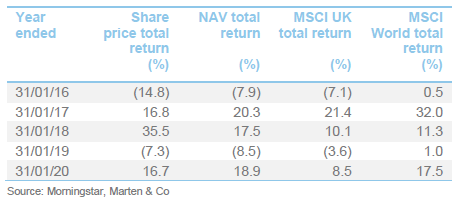

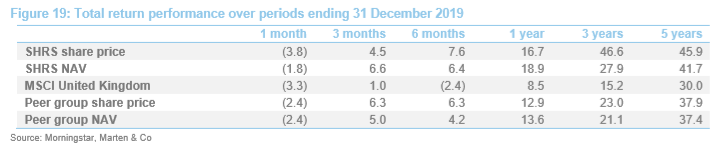

As Figures 18 and 19 show, an easing of Brexit-related nervousness and some profittaking on ‘growth’ stocks, especially over the second half of 2019, dispersed earlier headwinds and allowed SHRS to hit new highs relative to the UK market, as represented by the MSCI UK Index.

Figure 19 also highlights SHRS’s outperformance of peer group averages, as we explore in more detail below.

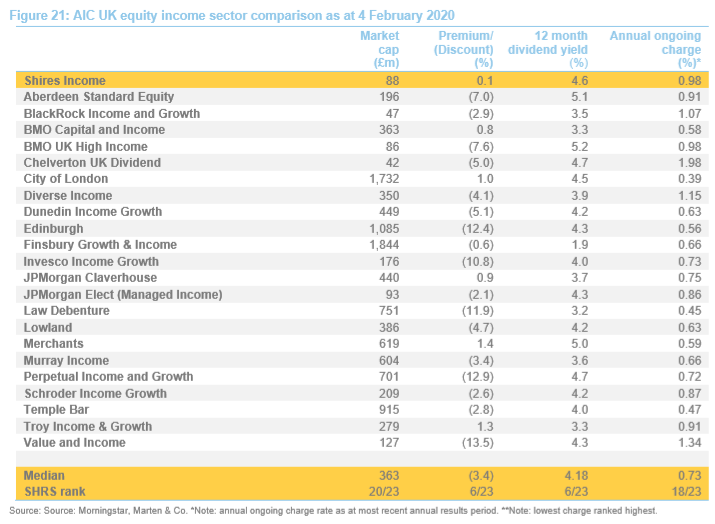

Peer group

SHRS is a constituent of the AIC’s UK equity income sector. For the purposes of this note, we have excluded investment companies with a market cap of less than £40m. A full list of the investment companies in our peer group is provided in Figure 21.

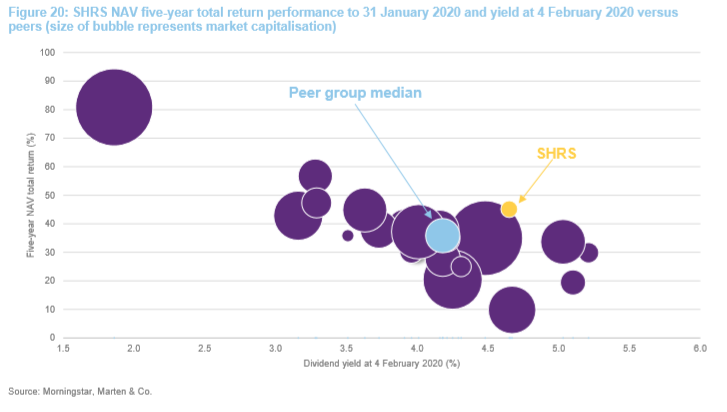

SHRS’s policy of augmenting its income through its preference share portfolio, funded in part by low-cost gearing, enables the manager to hold a higher proportion of higher growth companies than many of its peers. Figure 20 illustrates the effect of this. In an environment where investors have been favouring growth stocks, one competitor – Finsbury Growth & Income – has achieved high NAV growth, but at the cost of a much lower dividend income for its investors. SHRS ranks as one of the highest-yielding trusts in its sector but has still achieved respectable long-term NAV growth and, as Figures 19 and 20 show, both its yield and NAV growth have been well ahead of peer group averages.

One of the perhaps more surprising things evident in Figure 20 is that SHRS is relatively small within the peer group, especially given its track record.

SHRS’s relatively small size has a direct impact on its ongoing charges ratio. However, as we explain on page 15, the twin attractions of decent performance and an attractive yield have helped the trust trade close to asset value and issue stock. As it expands, the ongoing charges ratio should fall (as fixed costs are spread over a wider base).

Dividend

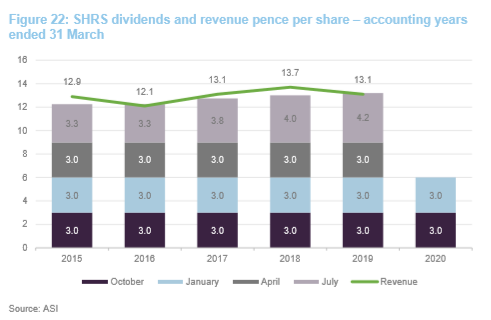

SHRS pays quarterly dividends in October, January, April and July. The board has indicated that it intends to continue to pay three quarterly interim dividends of 3p each and will decide on the level of the final dividend having reviewed the full-year results. Assuming that the final dividend is at least maintained, the current annual rate of dividends is 13.2p, representing a yield of 4.6%.

As Figure 22 demonstrates, this portfolio has produced a modestly growing revenue stream and has allowed SHRS to grow its dividend while growing its revenue reserves. SHRS’s revenue reserves at the end of March 2019 amounted to £6,819,000, equivalent to 22.2p per share or almost 1.7x last year’s dividend.

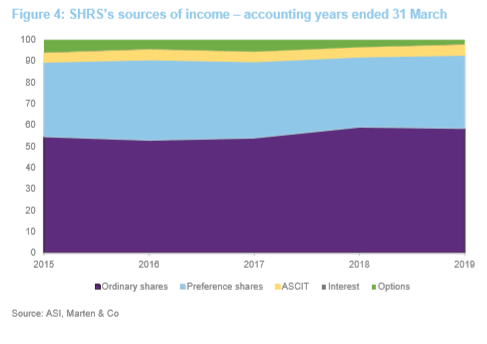

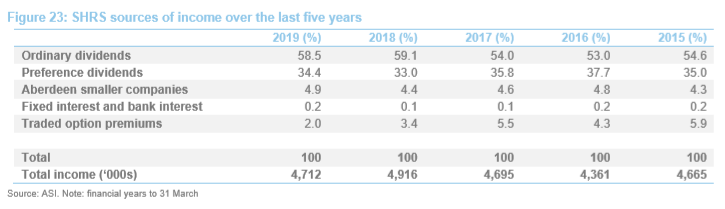

Figure 23 illustrates the diversity of SHRS’s revenue sources.

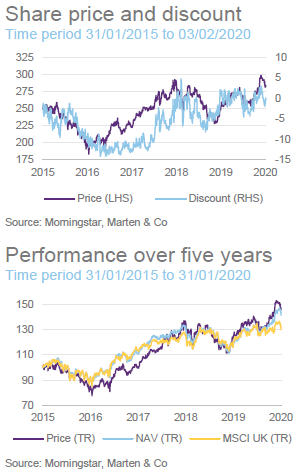

Premium/(discount)

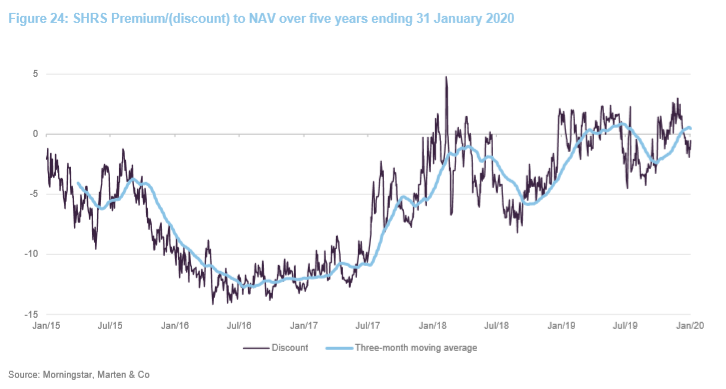

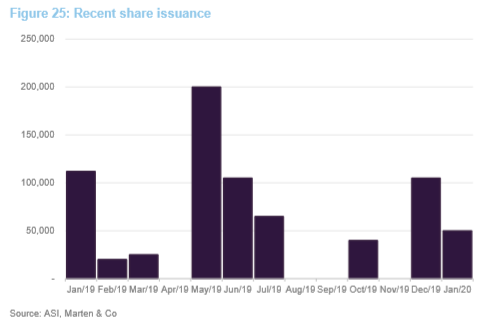

Over the 12 months ended 31 January 2020, SHRS traded within a range of a 4.5% discount to a 3.0% premium and an average discount of 0.2%. The discount narrowed over the course of 2018 and has traded close to asset value for over a year now. The board is moderating the premium by issuing shares to meet demand. As these shares are issued at a premium; these transactions benefit the NAV for existing shareholders.

At the last AGM, shareholders granted the board permission to issue up to 10,100,516 shares, equivalent to 33.33% of the then-issued share capital. No shares will be issued at a price less than NAV. This permission expires on 30 September 2020 or at the next AGM, whichever is earlier. Should the discount widen excessively, the board has authority to repurchase up to 14.99% of the trust’s issued share capital. We would expect that the board will seek to renew these authorities at the forthcoming AGM in July 2020.

Fees and costs

The management fee is 0.45% per annum on amounts up to £100m and 0.40% over £100m. It is calculated monthly and paid quarterly. The calculation of the fee is based on the company’s net assets, plus any borrowings up to a maximum of £30m, less any amount invested in ‘commonly managed funds’ (i.e. Aberdeen Smaller Companies Income Trust Plc). The total of the fees paid and payable to the manager covering the year to 31 March 2019 was £406,000.

The management contract covers the cost of company secretarial and administration services, and is terminable on six months’ notice by either side. The management fee is allocated 50% against the revenue of the company and 50% against its capital. The same treatment is applied to the interest on SHRS’s borrowings. All other expenses are charged against revenue.

Other expenses include an amount paid to the manager for the provision of promotional activities. This was £58,000 for the year ended 31 March 2019, down from £78,000 for the prior year (including VAT). SHRS’s ongoing charges ratio for the year ended 31 March 2019 was 0.98% (0.95% for the prior accounting year) and the running rate at the half-year mark for the current accounting year was 0.94%. The fall most likely reflects the expansion of the company as fixed costs are spread over a wider base.

Capital structure and life

As at 4 February 2020, SHRS had 30,719,580 ordinary shares and 50,000 3.5% cumulative preference shares in issue. Each of the ordinary shares and cumulative preference shares has a vote at general meetings of the company. In the event of a winding-up of the company, the cumulative preference shareholders are entitled to any cumulative preference share dividends accrued but not yet paid to them, plus a return of their capital (£1 per share). Ordinary shareholders are entitled to the balance.

SHRS’s accounting year end is 31 March. Its annual results are usually released in May and interims published in November. Its AGMs are held in July. It has an unlimited life and no scheduled continuation votes.

Gearing

The maximum level of gearing on the equity portfolio has been set at 35% of net assets (at the time the funds are drawn down).

On 23 September 2019, SHRS entered into a new £20m loan provision facility with Scotiabank Europe Plc, covering the three-year period to 20 September 2022. This extends an existing £20m facility with the same bank that was to mature on 30 October 2020. Under the terms of the new facility, the trust has drawn down £10m at a fixedrate of 1.706% that holds until the new facility matures. Proceeds from the new £10m loan have been used to repay SHRS’s previous £10m fixed-rate loan, which carried a higher interest rate of 1.956%. In addition, £9m has been drawn down on a revolving basis.

Total borrowings amounted to £19.047m at end-November 2019.

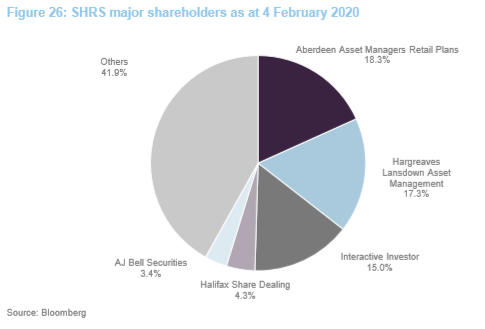

Major shareholders

Board

SHRS has five directors (soon to be four once again), all of whom are non-executive, do not sit together on other boards and are independent of the manager. In light of the publication of the UK Code of Corporate Governance in July 2018, board members now stand for re-election annually. Accordingly, Robert Talbut, Andrew Robson, Marian Glen and Robin Archibald retired at the AGM held in July 2019, before being subsequently re-elected.

Andrew Robson’s tenure is nearing its end. He is the longest-serving member of the board and is due to retire at the next AGM to be held in 2020. To smooth the transition, Robin Archibald was appointed chair of the audit committee following the most recentlyheld AGM on 4 July 2019 and the board has just recruited Jane Pearce. Jane will stand for re-election at the AGM planned for July 2020.

Robert Talbut (chairman)

Robert Talbut was formerly chief investment officer of Royal London Asset Management and has over 30 years of financial services experience. He has represented the asset management industry through the chairmanship of both the ABI Investment Committee and the Asset Management Committee of the Investment Association. He has also been a member of the Audit & Assurance Council of the FRC and the Financial Conduct Authority’s Listing Authority Advisory Panel. Robert is chairman of EFG Asset Management (UK) Limited and a non-executive director of Pacific Assets Trust Plc, Schroder UK Mid Cap Fund Plc and JPMorgan American Investment Trust Plc.

Andrew Robson (senior independent director)

Andrew Robson is a chartered accountant, with many years of experience in investment banking and as a finance director. He was a director of Robert Fleming & Co Limited and SG Hambros, and finance director of eFinancialGroup Limited and the National Gallery. He has over 15 years of experience as a director of a number of quoted investment trusts, and is currently a business adviser, working with smaller UK companies. He is a non-executive director of JPMorgan Smaller Companies Investment Trust Plc and Witan Pacific Investment Trust Plc. Andrew is due to retire from the board in 2020, following over 12 years of board service to SHRS.

Marian Glen (director and chair of the remuneration committee)

Marian Glen is a non-executive director of Martin Currie Global Portfolio Trust Plc and The Medical and Dental Defence Union of Scotland. She was a non-executive director of Murray Income Trust Plc, Friends Life Group Limited and other companies in the Friends Life group of companies. She was formerly the General Counsel of AEGON UK and, prior to that, was a corporate partner and head of funds and financial services at Shepherd and Wedderburn.

Robin Archibald (director and chair of the audit committee)

Robin Archibald has a wide range of experience in advising and managing transactions in the UK closed-ended funds sector over his 35-year career as a corporate financier, including with Samuel Montagu, SG Warburg and NatWest Markets. He retired from Winterflood Investment Trusts in May 2014, where he was formerly head of corporate finance and broking. He is currently a non-executive director of Albion Technology & General VCT Plc, Ediston Property Investment Company Plc, Capital Gearing Trust Plc and Henderson European Focus Trust Plc. Robin has experience of serving as audit chair on other investment companies.

Jane Pearce (director)

Jane Pearce is a co-opted external member of the Audit and Risk Committee of the University of St Andrews. She had an executive career as an equity analyst at leading investment banks and latterly was an equity strategist at Lehman Brothers and Nomura International. Jane is a Chartered Accountant and was a member of the Governing Council of the Institute of Chartered Accountants of Scotland from 1999-2000.

Previous publications

Readers interested in further information about SHRS may wish to read our previous notes by clicking on the links or by visiting our website.

Sustainable high yield, initiation note, 22 October 2018;

Growing again, update note, 30 May 2019.

The legal bit

This marketing communication has been prepared for Shires Income Plc by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and if you are not a professional investor, or in any other way are prohibited or restricted from receiving this information you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it but, in practice and in accordance with our internal code of good conduct, will refrain from doing so. Nevertheless, they may have an interest in any of the securities mentioned in this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.